Singapore HDB Flat Eligibility Guide 2026: HFE Check, Income Ceilings and What Qualifies You

- The HDB Flat Eligibility (HFE) letter replaced the old HDB Loan Eligibility (HLE) letter in May 2023. It is a single document that confirms both your eligibility to buy an HDB flat and your eligibility for an HDB housing loan and CPF housing grants.

- The HFE letter is mandatory before you can apply for a BTO flat or place an Option to Purchase (OTP) on a resale HDB flat.

- It is valid for 9 months from the date of issue and can be renewed by reapplying.

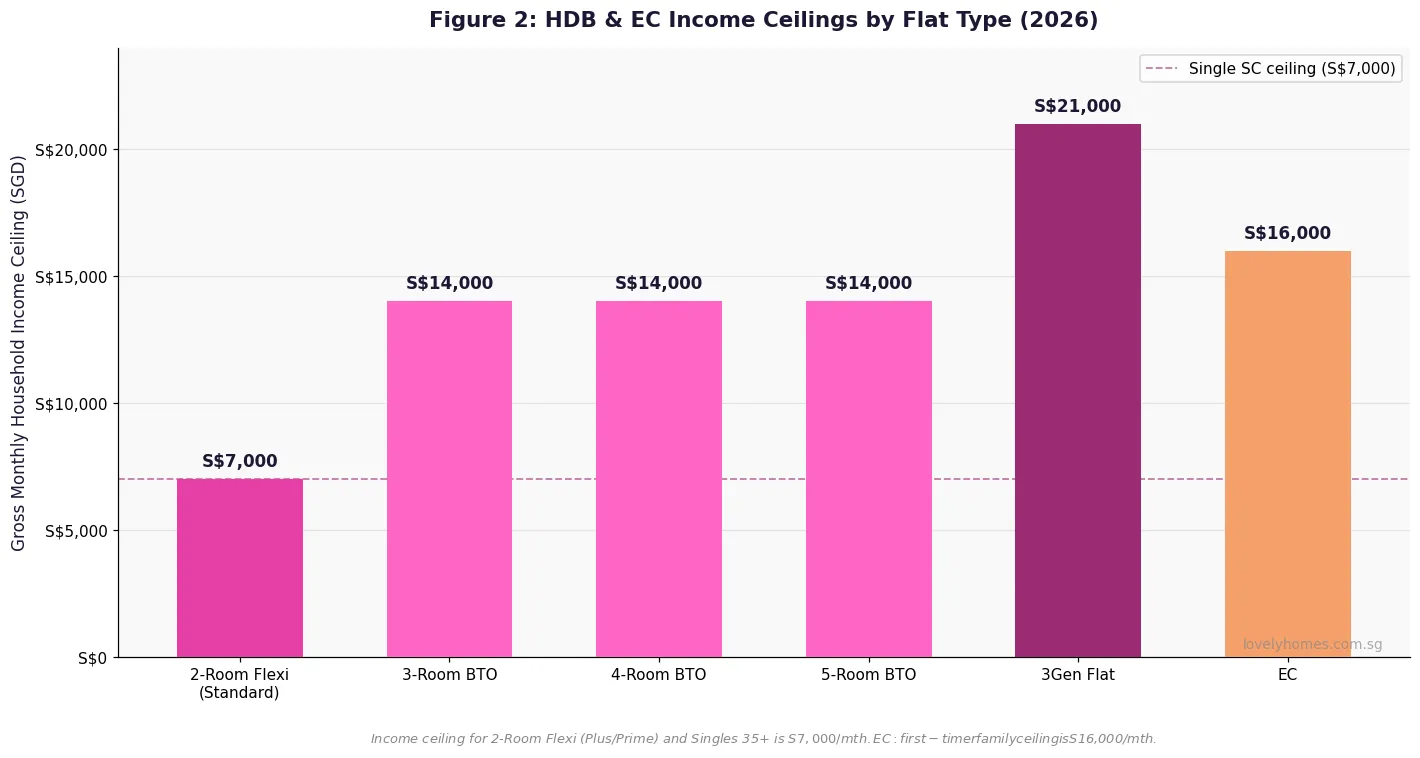

- The income ceiling for most BTO flat types (excluding Singles schemes) is S$14,000 per month gross household income.

- For Singles 35+ buying 2-Room Flexi under the Single Singapore Citizen Scheme, the income ceiling is S$7,000/mth.

- You cannot buy a subsidised HDB flat if you currently own private property or have sold private property within the last 30 months.

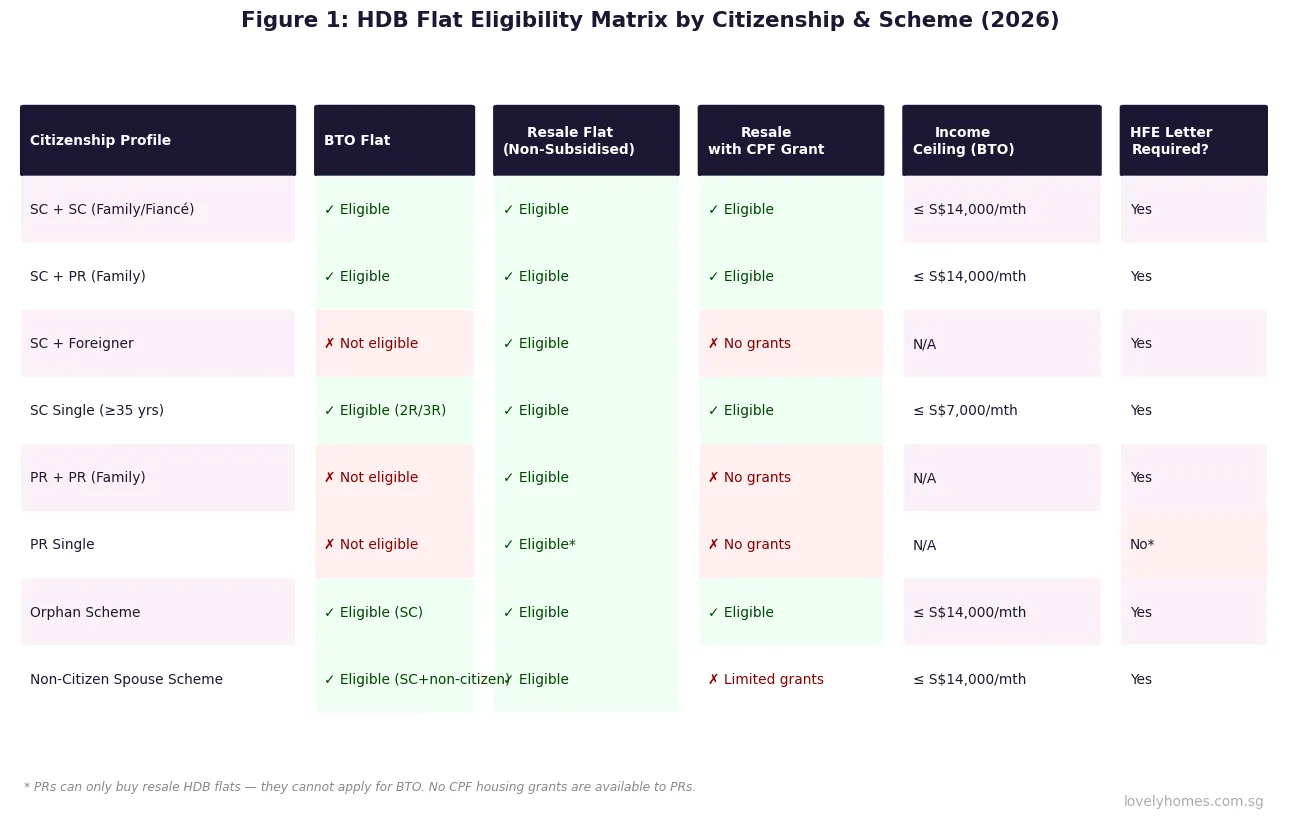

- Permanent Residents (PRs) can buy resale HDB flats but are not eligible for BTO flats or CPF housing grants.

- For Executive Condominiums (ECs), the income ceiling is S$16,000/mth for first-timer families.

What Is HDB Flat Eligibility — and Why the HFE Letter Matters

Buying an HDB flat in Singapore is not simply a matter of picking a unit and signing a contract. The Housing and Development Board (HDB) administers the most heavily subsidised public housing programme in the world: as of 2026, over 78% of Singapore’s resident population lives in HDB flats, many purchased at significant subsidies relative to market prices. To maintain the fairness and integrity of this system, the HDB enforces a detailed eligibility framework governing who can buy which type of flat, under what conditions, and with what assistance.

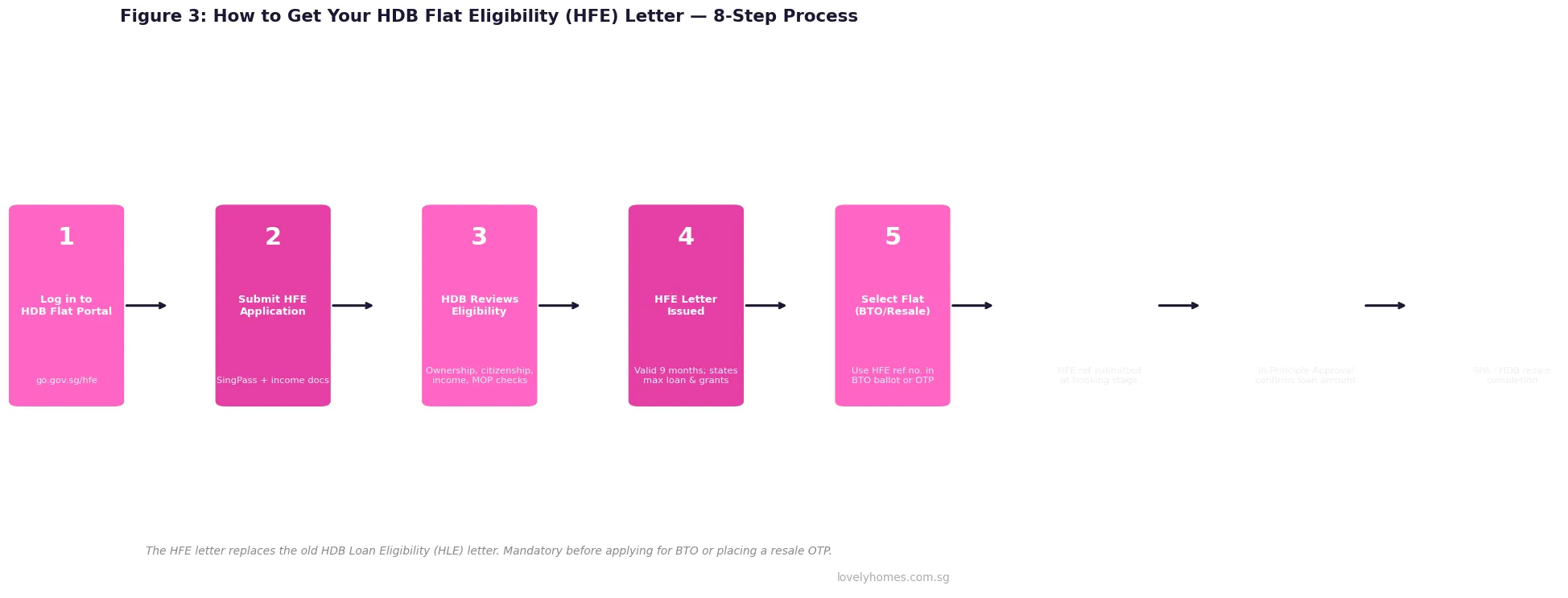

The centrepiece of this framework — for buyers — is the HDB Flat Eligibility (HFE) letter, introduced in May 2023. The HFE letter replaced both the old HDB Loan Eligibility (HLE) letter and the separate eligibility self-check that buyers previously performed themselves. Today, a single HFE application, submitted via the HDB Flat Portal, generates a letter that simultaneously confirms your:

- Eligibility to purchase an HDB flat (including flat type and scheme).

- Eligibility for an HDB concessionary housing loan and the maximum loan quantum.

- Eligibility for CPF housing grants and the grant amounts applicable to you.

No HFE letter means no BTO application and no resale OTP. Understanding how to obtain the HFE letter — and what it assesses — is therefore the logical starting point for any prospective HDB buyer in 2026.

The Seven HDB Eligibility Schemes: Which One Applies to You?

The HDB does not use a single eligibility rule. Instead, it operates seven distinct eligibility schemes, each designed to accommodate a specific family or household configuration. Every applicant must qualify under one of these schemes.

1. Public Scheme: The most common scheme. Requires at least one Singapore Citizen (SC) applicant. The other person(s) in the nucleus (spouse, children, parents, or siblings) can be SCs or Permanent Residents (PRs). This covers the vast majority of married couples and families applying for BTO or resale flats.

2. Fiancé/Fiancée Scheme: Allows SC couples who are not yet married to apply for a BTO flat or book a resale flat together. Both parties must be at least 21 years old and must register their marriage within three months of the resale flat keys being collected, or within three months of the BTO flat booking.

3. Orphan Scheme: For applicants who are single SCs (i.e., unmarried, widowed, or divorced) and whose parents are deceased. The applicant must have at least one sibling who is also unmarried or widowed and who was living with the parents prior to their passing. This scheme allows siblings to pool their eligibility to purchase a flat together.

4. Non-Citizen Spouse Scheme: Allows an SC to buy a flat with a foreign (non-PR, non-SC) spouse. The SC applicant must be the essential occupier; the foreign spouse is named as an occupier. Only a limited selection of HDB flat types is available under this scheme, and CPF grant eligibility is more restricted.

5. Single Singapore Citizen (SSC) Scheme: For SCs aged 35 and above who are single (unmarried, widowed, or divorced). Singles may only purchase 2-Room Flexi flats in non-mature estates under BTO, or any resale flat size. The income ceiling under this scheme is S$7,000 per month.

6. Joint Singles Scheme: Allows two to four single SCs, each aged 35 or above, to buy a flat jointly. The same rules as the SSC Scheme apply; participants must remain as joint owners during the Minimum Occupation Period (MOP).

7. Joint Singles with Widowed/Divorced Persons Scheme: A specific subset allowing a widowed or divorced SC of any age to purchase a resale flat jointly with other single SCs (aged 35+).

Income Ceilings: BTO, Resale and EC

Income ceilings for BTO flat purchases exist to ensure subsidised flats are channelled to households that genuinely cannot afford private market alternatives. The ceilings are based on gross monthly household income — the sum of all assessable income of all applicants and essential occupiers listed in the application.

| Flat Type / Scheme | Income Ceiling (Gross Monthly) | Notes |

|---|---|---|

| 2-Room Flexi BTO (Standard estates) | S$14,000 (family) / S$7,000 (singles) | Singles 35+ eligible for S$7,000 ceiling |

| 2-Room Flexi BTO (Plus / Prime) | S$7,000 (family) | Lower ceiling for higher-subsidy estates |

| 3-Room BTO | S$14,000 | Standard, Plus, and Prime classifications |

| 4-Room BTO | S$14,000 | Most common flat type |

| 5-Room and 3Gen BTO | S$14,000 / S$21,000 (3Gen) | 3Gen flats require multi-generational households |

| HDB Resale (no CPF grant) | No income ceiling | Any eligible buyer can purchase at market price |

| HDB Resale (with CPF grants) | S$14,000 (family) / S$7,000 (singles) | EHG eligibility requires household income check |

| Executive Condominium (EC) | S$16,000 (first-timer family) | EC is quasi-private; higher ceiling than HDB BTO |

Ownership History and Private Property: The 30-Month Rule

One of the most consequential eligibility rules concerns private property ownership. To prevent higher-income households from simultaneously benefiting from HDB subsidies and private market appreciation, the HDB imposes strict conditions:

- You and any listed occupier must not currently own private residential property in Singapore or overseas at the time of application.

- You and any listed occupier must not have disposed of any private residential property (in Singapore or overseas) within the 30 months immediately before the HFE application date (for subsidised BTO or resale with grants). This is the so-called “30-month wait-out period” for private property owners.

- Owning a commercial property does not affect HDB eligibility, but owning a residential property held through a company or trust may be assessed on a case-by-case basis.

For buyers purchasing a resale flat at market price without any CPF housing grant, the private property ownership rule does not apply — you can own a private property and buy a resale HDB flat simultaneously, subject to paying the applicable stamp duty. However, you would need to sell the private property if you wish to continue owning the HDB flat beyond the applicable occupation period under the terms of the purchase.

MOP Interaction: When Previous Flat Ownership Matters

If you have previously owned an HDB flat, your Minimum Occupation Period (MOP) history affects your eligibility for a subsequent subsidised purchase:

- You must have fully completed the MOP on your current or most recently sold HDB flat before applying for a new BTO flat.

- If you are currently within the MOP of an existing HDB flat, you cannot book a new BTO flat — you must wait until the MOP is cleared and the existing flat is sold.

- Second-timer applicants applying for BTO flats have reduced priority balloting and are subject to a resale levy payable to HDB if they had previously received a housing subsidy on a first subsidised flat.

- The resale levy ranges from S$15,000 to S$55,000 depending on the flat type of the first subsidised flat, and is payable upon the booking of the second flat.

How to Apply for the HFE Letter: Step-by-Step

Applying for the HFE letter is done entirely online via the HDB Flat Portal at homes.hdb.gov.sg (also accessible at go.gov.sg/hfe). The process requires all applicants to log in via Singpass and provide income documentation. Here is what you need:

- Singpass login for each applicant.

- Latest CPF contribution history (auto-retrieved with Singpass consent).

- Latest payslip(s) for each employed applicant.

- Income Tax Notice of Assessment (if self-employed or commission-based).

- Documents for variable income, including bonuses, allowances, and rental income (typically the average over the past 12 months).

- Details of all outstanding loans (used to assess HDB loan quantum and TDSR/MSR compliance).

Once submitted, HDB typically issues the HFE letter within 5 to 7 working days, though complex applications (e.g., overseas property interests, atypical income structures, or previous flat ownership history) may take longer. The HFE letter is valid for 9 months. If you do not book a flat or sign a resale OTP within this window, you must renew the HFE application.

Worked Example: The Lee Family’s HFE Application and BTO Journey

Mr Lee Jian Ming and Ms Tan Wei Ling are Singaporean citizens, both aged 29, engaged to be married in August 2026. They wish to apply for a 4-Room BTO flat in Bishan under the Fiancé/Fiancée Scheme. Their combined gross monthly income is S$9,200. Neither owns any private property; both are first-time flat buyers.

Step 1 — HFE Application: They apply jointly via the HDB Flat Portal, logging in via Singpass and uploading their payslips. Mr Lee earns S$5,800/mth; Ms Tan earns S$3,400/mth. Combined: S$9,200/mth.

Eligibility check: Income S$9,200 < ceiling S$14,000 ✓. Both are SCs ✓. Neither owns private property ✓. Both are first-timers ✓. Scheme: Fiancé/Fiancée (Public Scheme) ✓.

HFE Letter outcome: Eligible to purchase 4-Room BTO. Eligible for HDB concessionary loan at 2.6% p.a. (pegged to CPF OA rate + 0.1%). Maximum loan quantum: based on TDSR/MSR — HDB assesses their monthly repayment capacity. Eligible for Enhanced CPF Housing Grant (EHG) at S$9,200/mth household income = approximately S$20,000 (tapering scale, family; income ≥ S$9,001 and ≤ S$9,500 band).

At ballot: The Lees apply for a 4-Room flat in Bishan Lakeview (June 2026 BTO exercise, Prime classification). As first-timers under the Fiancé/Fiancée Scheme, they receive a First-Timer Priority ballot advantage. Wait time: approximately 4.5 years (Top in 2031).

Key numbers: BTO price approximately S$680,000 (indicative, Prime D20 4-Room). BSD: S$14,400. No ABSD (first HDB purchase). HDB loan 90% LTV = S$612,000 at 2.6% 25 years = S$2,780/mth. MSR 30%: maximum monthly mortgage S$2,760 — just at the boundary. The couple may consider topping up CPF or adjusting the loan tenure to keep monthly payments within MSR.

Why HFE Matters: Singapore’s Public Housing System and What It Delivers

The HFE framework reflects the extraordinary scope of Singapore’s public housing commitment. The government subsidises HDB flats at prices well below what a private developer would charge for comparable space in comparable locations — a deliberate policy to enable homeownership across virtually all income bands. This subsidy comes with conditions, and the HFE is how those conditions are enforced consistently and fairly.

For buyers, the HFE letter serves another practical function: it gives you certainty before committing. Knowing your exact grant quantum, maximum loan, and MSR headroom before entering the ballot prevents over-commitment and planning failures — a significant improvement over the old system where buyers sometimes discovered eligibility issues only at the booking stage.

By global comparison, few countries provide both a guaranteed right to affordable housing and a structured eligibility framework as rigorous as Singapore’s. The HFE system continues to be refined: the HDB has signalled that digital verification of income will become more automated through MyInfo and CPF integration, reducing the documentation burden on applicants whilst maintaining eligibility integrity.

What Might Change in HDB Eligibility Rules From 2026 Onwards

The HDB and the Ministry of National Development have signalled several potential directions for HDB eligibility policy in the medium term. Observers expect further calibration of the Plus and Prime flat classification framework — introduced in October 2024 — including the possibility of expanding the number of estates with Plus-level restrictions as the scheme matures. The resale levy quantum, last revised in 2006, is overdue for review given the rise in flat prices. The HDB has also mooted reforms to the singles policy, potentially lowering the age threshold below 35 in future BTO launches for certain flat types, in response to demographic changes and the rising number of young singles. Any policy changes would be announced by the Ministry of National Development and take effect for BTO sales exercises from the announcement date.

Frequently Asked Questions

How long is the HFE letter valid, and what happens if it expires?

The HFE letter is valid for 9 months from the date of issue. If you do not apply for a BTO flat or place a resale OTP within this period, you must reapply. The reapplication process is the same as the original application — you log in via the HDB Flat Portal, update your income and financial details, and HDB reassesses your eligibility. Your eligibility may change if your income, property ownership status, or household composition has changed since the last application. There is no limit on the number of times you can renew an HFE application.

Can a Permanent Resident buy a BTO flat in Singapore?

No. Permanent Residents (PRs) are not eligible to apply for BTO flats. PRs may only purchase resale HDB flats, and only if they form a family nucleus with at least one SC (or apply under the PRs-only joint purchase arrangement for resale flats). PRs are not entitled to CPF housing grants. Furthermore, PRs who buy an HDB resale flat must sell the flat before buying or owning any private residential property.

What is the resale levy, and when does it apply?

The resale levy is a payment to HDB made by second-timer applicants who are buying a second subsidised HDB flat (BTO or resale with CPF grants) after having previously received a housing subsidy on a first flat. The levy ranges from S$15,000 (for a previous 2-Room flat) to S$55,000 (for a previous 5-Room or larger flat), indexed to the flat type at time of first subsidy. The levy is intended to reduce the cumulative housing subsidy received by any one household. It is payable at the booking of the second flat and can be paid from CPF OA funds.

Can I apply for the HFE letter if I am currently renting an HDB flat?

Yes. Renting an HDB flat — whether through HDB directly or through a sub-tenancy arrangement from a flat owner — does not disqualify you from applying for the HFE letter or purchasing an HDB flat, provided you meet the other eligibility criteria (citizenship, income, ownership history, age). Your rental status is not assessed as part of the HFE eligibility check. However, note that if you are renting a room in an HDB flat owned by someone else, the owner’s eligibility is what governs the rental — not yours as a tenant.

What happens if my income exceeds the ceiling after I have already booked a BTO flat?

Once you have successfully booked a BTO flat and the booking is confirmed, the income ceiling is assessed at the point of application and booking — not retrospectively at key collection. A temporary increase in income after booking (for example, a salary increment or bonus) does not cause you to lose your booking. However, if you fraudulently misrepresented your income at the time of application, HDB can cancel your booking and take disciplinary action. The CPF grant quantum is fixed at the time the HFE letter is issued; subsequent income changes do not affect the grant amount already confirmed.

Can foreigners buy HDB flats in Singapore?

Foreigners (non-SC, non-PR) cannot buy HDB flats in Singapore under any scheme. They are also ineligible for CPF housing grants. Foreigners may purchase private residential property subject to paying Additional Buyer’s Stamp Duty (ABSD) at 60% of the purchase price (as at 2026). A small category of citizens from countries with bilateral Free Trade Agreements (Iceland, Liechtenstein, Norway, and Switzerland under the EUSFTA/FTA frameworks) may be treated similarly to SCs for ABSD purposes on first purchases, but are still ineligible to purchase HDB flats.

Does the 30-month wait-out period apply if I am giving up my private property through inheritance?

The 30-month wait-out period applies to the disposal of private residential property, not to its acquisition through inheritance. If you inherit private residential property, you are not immediately disqualified from HDB eligibility — however, you must dispose of the inherited private property before your HFE application or BTO booking (within the timeframe specified by HDB). If you are applying for a subsidised BTO flat or resale flat with CPF grants, you cannot hold private property simultaneously. The 30-month clock starts running from the date you legally dispose of the inherited private property, not from the date of inheritance.

Related Articles

- Singapore HDB CPF Housing Grant Guide 2026: EHG, Family Grant, PHG and More

- Singapore Property MOP Guide 2026: HDB Minimum Occupation Period Rules Explained

- Singapore HDB Ethnic Integration Policy Guide 2026: EIP Quotas and Resale Impact

- HDB BTO June 2026 Launch Review: 6,952 Units Across 7 Projects

- Singapore First-Time Buyer Guide 2026: HDB, Resale or New Launch?

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

Disclaimer

This article is intended for general information purposes only and does not constitute legal, financial, or professional advice. HDB eligibility rules, income ceilings, grant quantum, and related policies described in this article are accurate to the best of our knowledge as at June 2026 but are subject to change by the Housing and Development Board and the Ministry of National Development. Readers should verify all information directly with HDB before making any purchase decisions. Official HDB flat eligibility information is available at hdb.gov.sg. CPF housing grant information is available at cpf.gov.sg. Income tax and stamp duty information is available at iras.gov.sg.