Singapore HDB BTO Application Guide 2026: Eligibility, HFE Letter, Balloting and Key Collection Explained

📌 Quick Answer: HDB BTO Application 2026

- BTO (Build-To-Order) flats are HDB flats built after a sales application — you apply first, HDB builds to the number of units needed, so there is no speculative inventory.

- Eligibility essentials: at least one Singapore Citizen applicant, combined household income at or below the flat-type ceiling (S$7,000–S$14,000), and no private property ownership in the 30 months before application.

- The HDB Flat Eligibility (HFE) Letter is now mandatory before you can submit a BTO application — obtain it through the MyHDBPage portal with Singpass; it takes about 2–3 weeks.

- BTO exercises are held roughly 4–5 times per year; each exercise lists flats in multiple towns, with application windows typically 5–7 days.

- A successful ballot means you are invited to select a flat during a flat selection appointment; unsuccessful applicants join the queue for subsequent exercises.

- Completion times range from 3 to 4.5 years after booking, depending on the project and site conditions.

- Standard Minimum Occupation Period (MOP) is 5 years from the date of key collection. Plus and Prime model flats carry a 10-year MOP and resale restrictions.

- Grants available: Enhanced CPF Housing Grant (EHG) up to S$120,000 for families, S$60,000 for singles; Proximity Housing Grant (PHG) up to S$30,000 for buying near parents.

What Is an HDB BTO Flat and How Does It Work?

The Build-To-Order (BTO) scheme is the Housing & Development Board’s primary mechanism for supplying new public housing to eligible Singapore households. Unlike resale flats — which are purchased from existing owners on the open market — BTO flats are sold directly by HDB at subsidised prices before construction begins. HDB only proceeds with a project once sufficient applications have been received, hence the “build to order” terminology. This demand-led model keeps supply aligned with actual household formation needs and limits speculative overbuilding.

BTO flats come in a range of types from 2-Room Flexi (35–47 sqm) through to 5-Room (110–113 sqm) and the 3-Generation (3Gen) layout designed for multi-generational households. Prices are subsidised relative to private market equivalents; a 4-room BTO flat in a non-mature estate typically prices at S$350,000–S$520,000, compared to resale equivalents at S$490,000–S$720,000 in the same area. The subsidy is funded by HDB and supported through a system of CPF Housing Grants that further reduce the effective purchase price for eligible households.

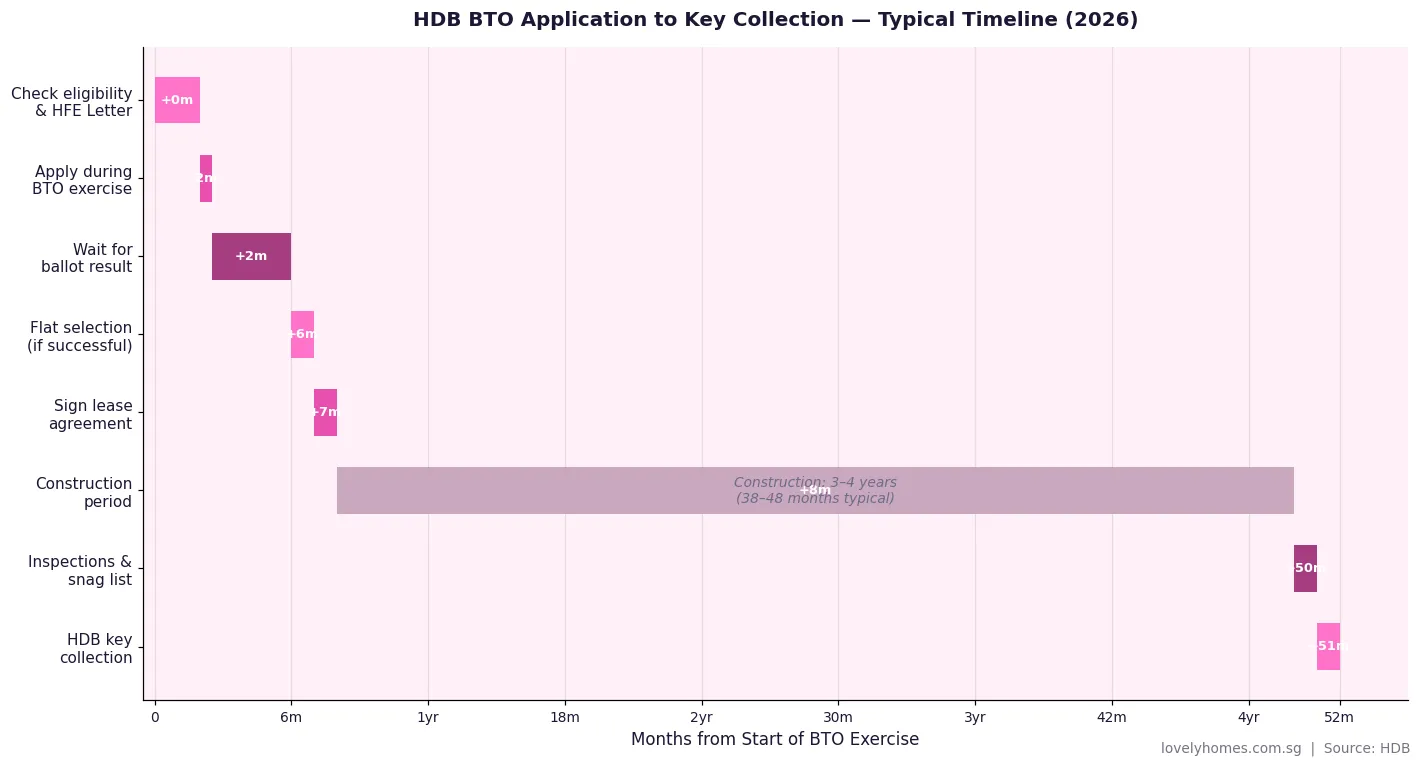

The BTO process involves several distinct stages — eligibility checking, HFE letter application, ballot application, flat selection, signing of the lease, a construction wait of three to four-and-a-half years, and finally key collection and move-in. This guide walks through each stage in detail with the 2026-current rules, timelines, and the specific grant amounts that apply this year.

BTO Eligibility: Who Can Apply?

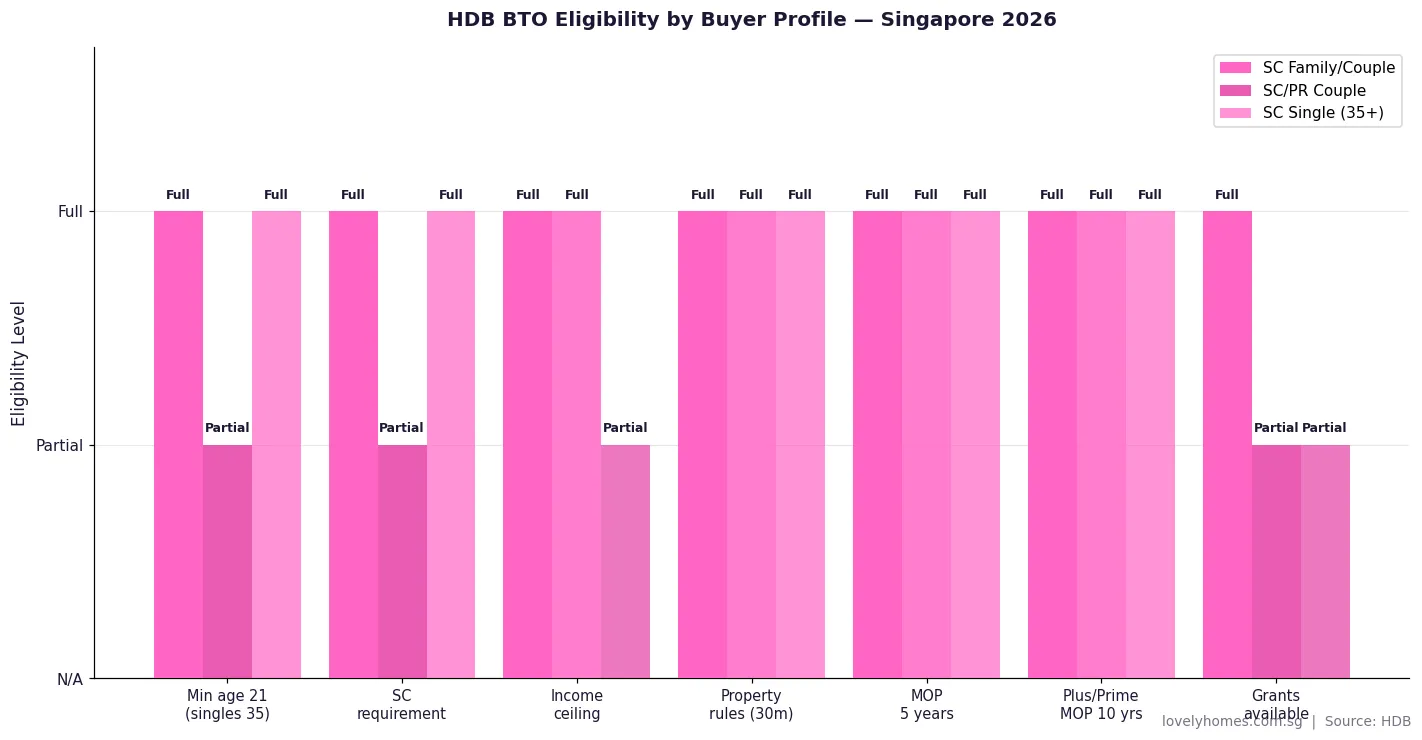

HDB BTO flats are available only to Singapore Citizens and, under certain schemes, Singapore Permanent Residents (PRs). The eligibility framework as at June 2026 is set out below.

| Eligibility Criterion | SC Family / Couple | SC/PR Couple | SC Single (35+) |

|---|---|---|---|

| Minimum age | 21 years (main applicant) | 21 years (SC applicant) | 35 years |

| SC requirement | At least 1 SC applicant | SC + PR (PR must be spouse) | Must be SC |

| Income ceiling (4-Room) | S$10,000/mth combined | S$10,000/mth combined | S$7,000/mth |

| Income ceiling (5-Room / 3Gen) | S$14,000/mth combined | S$14,000/mth combined | Not eligible for 5-Room |

| Private property rule | No private property 30 mths before & at application | Same | Same |

| Flat types eligible | All types | All types | 2-Room Flexi only |

| EHG grant available | Up to S$120,000 | Up to S$120,000 (if SC component) | Up to S$60,000 |

Foreigners who are neither SC nor PR cannot apply for BTO flats under any scheme. PRs who are single also cannot apply. Under the SC/PR scheme, the PR must be the applicant’s spouse and must obtain SC status within a specified period after key collection or face resale restrictions. Additionally, applicants must not own or have disposed of any flat in a manner that disqualifies them under HDB’s ownership rules — for example, those who have previously received a HDB housing subsidy are not eligible for a second subsidised flat unless they meet specific criteria such as the Married Child Priority Scheme (MCPS) rules.

The HDB Flat Eligibility (HFE) Letter: Step One

Since May 2023, prospective BTO buyers must obtain a HDB Flat Eligibility (HFE) Letter before applying for a BTO flat. The HFE Letter replaced the old Housing Loan Eligibility (HLE) letter and the flat eligibility check — it combines both into a single document that confirms: (a) which flat types you are eligible to purchase; (b) the maximum HDB concessionary loan amount; and (c) the CPF Housing Grants you qualify for.

To apply for an HFE Letter, log in at hdb.gov.sg using Singpass. You will need to provide income documents (CPF contribution history is auto-retrieved), particulars of all household members, and details of any existing properties. HDB typically issues the HFE Letter within 21 business days. The letter is valid for 6 months; apply for it approximately one month before the BTO exercise opens to ensure it is ready in time.

Applying for a BTO Flat: The Exercise and Ballot

HDB launches BTO exercises approximately 4–5 times per year, typically in February, May, August, and November (with occasional additional exercises). Each exercise lists projects in multiple towns. The application window is usually 5–7 days, during which eligible applicants may submit one application per exercise via the HDB website or at an HDB Branch.

Key rules during application: applicants may apply for only one flat type in one town per exercise. An application requires a non-refundable application fee of S$10. Successful applicants in the 2-Room Flexi Ballot who do not eventually select a flat will have the S$10 refunded. Households with more children receive priority queue positions under the Parenthood Priority Scheme (PPS), and first-timers receive ballot priority over second-timers.

After the application window closes, HDB computer-ballots all applicants. Results are released approximately 3 weeks later. Successful applicants receive a ballot queue number and a flat selection appointment within approximately 3–6 months. If the ballot number is not reached (all flats selected before your turn), the applicant is treated as unsuccessful and is given an additional ballot chance (2nd timer status not triggered — first-timer status preserved for a stated number of unsuccessful attempts).

First-Timer Priority and Queue Balloting

HDB’s priority allocation system is designed to give first-time buyers and families with young children a better chance of success. In a standard BTO exercise, approximately 85–90% of flat supply is set aside for first-timers (those who have never owned or received a housing subsidy before). The remaining 10–15% is allocated to second-timers. Within the first-timer pool, the Parenthood Priority Scheme (PPS) reserves a further 30% of supply for families with Singaporean children aged 18 or below.

After three or more unsuccessful ballots, first-timer applicants (with children) may apply under the Additional Ballots Scheme, which gives them a higher chance. HDB has progressively expanded priority rules — from 2024, those who have collected a BTO flat and are applying again (e.g., for a larger flat after having more children) are classified as second-timers and face a smaller allocation pool.

Flat Selection, Booking and Signing the Lease

Upon receiving a flat selection appointment, applicants visit an HDB Branch (or select online via the portal in more recent exercises) and choose their preferred unit from the remaining available options. At selection, a booking fee is payable: S$2,000 for 2-Room Flexi, S$4,000 for 3-Room, S$8,000 for 4-Room and 5-Room/3Gen (as at 2026; fees are reviewed periodically). The booking fee is non-refundable if you subsequently withdraw from the purchase.

After booking, HDB typically schedules the signing of the Agreement for Lease (Lease Agreement) within 4–6 months. At this appointment, applicants pay the down payment and stamp fees. For those taking an HDB concessionary loan, the down payment is 10% of the flat price (payable via CPF OA or cash); for those using a bank loan, the down payment is 25% (with 5% minimum in cash). Buyer’s Stamp Duty (BSD) is also payable at this stage. After signing, construction proceeds and buyers await key collection.

CPF Housing Grants for BTO Buyers (2026)

BTO buyers may be eligible for significant grant support that directly reduces the effective purchase price. As at June 2026, the key grants are:

- Enhanced CPF Housing Grant (EHG): Up to S$120,000 for families (income ≤ S$9,000/mth average over 12 months before application) and up to S$60,000 for singles. The EHG is income-tiered — a family earning S$2,000/mth receives the full S$120,000; at S$9,000/mth, the grant is S$5,000. Effective from 20 August 2024.

- CPF Housing Grant — Families (Family Grant): An additional S$10,000–S$30,000 for eligible first-timer families purchasing 4-Room or smaller BTO flats, depending on flat type and town classification.

- Step-Up CPF Housing Grant: S$15,000 for second-timer SC families moving from a 2-Room to a 3-Room BTO flat.

- Proximity Housing Grant (PHG): S$30,000 for buying within 4 km of parents’ or child’s home; S$20,000 for buying in the same town. Available for resale HDB purchases — not BTO directly, but may apply on the eventual resale.

Grants are disbursed as CPF credits into the recipient’s OA account, reducing the cash required at booking and lease signing. They do not reduce the outstanding loan; rather, they offset the cash/CPF down payment needed.

📌 Worked Example: Mr & Mrs Goh — First-Timer BTO Application, Tampines 4-Room

Mr Goh (SC, age 29) and Mrs Goh (SC, age 27) are first-timer applicants. Combined household income: S$7,200/mth (based on 12-month CPF contribution average). One child aged 2. They apply for a 4-room BTO flat in Tampines during the June 2026 BTO exercise, priced at S$478,000.

- HFE Letter: Applied 30 days before exercise opens; issued in 16 business days. Confirms eligibility for 4-Room, HDB loan S$382,400 (80% LTV), EHG S$50,000 (income S$7,200 tier).

- Ballot result: Successful; queue number 38 out of 220 applicants for 240 available units. Flat selection appointment in Month 4.

- Flat price: S$478,000. Grants: EHG S$50,000 → effective price S$428,000.

- Booking fee: S$8,000 (cash or NETS).

- BSD: (1% × S$180,000) + (2% × S$180,000) + (3% × S$118,000) = S$1,800 + S$3,600 + S$3,540 = S$8,940 on S$478,000.

- HDB Loan: S$382,400 at 2.6% p.a. over 25 years → monthly instalment S$1,731. MSR: S$1,731 ÷ S$7,200 = 24.0% ✓ (below 30% MSR limit).

- Total upfront cash outlay at lease signing: Booking fee S$8,000 + down payment (10% S$47,800 less EHG S$50,000 already in CPF OA) → effectively S$5,800 cash + S$8,940 BSD (payable by CPF OA) = approximately S$14,740 in cash/CPF.

- Key collection: Estimated 3 years 8 months from booking, approximately Q2 2030. MOP: 5 years from key collection date (standard flat).

Plus and Prime BTO Flats: Stricter Rules for Better Locations

From 2024, HDB restructured the BTO flat classification. “Standard” flats (in non-mature, non-central estates) carry the familiar 5-year MOP and standard resale/rental rules. “Plus” flats — in choicer locations such as Kallang/Whampoa, Queenstown fringe, and new towns with strong transport links — carry a 10-year MOP and cannot be rented out for the first 10 years. “Prime” flats — in the most central, highest-demand locations near the CBD and in mature estates — carry a 10-year MOP, are subject to a subsidy clawback on first resale (buyers must return a portion of their capital gain to HDB), and have additional resale restrictions to ensure the flats remain affordable for future first-timers. If you are considering a Plus or Prime flat, factor the longer holding period and clawback into your financial planning.

Why the BTO Route Matters for Most Singapore Families

For first-timer Singapore Citizens, the BTO route remains the most financially sound path to home ownership. The built-in subsidy can be S$100,000 or more relative to resale market prices in the same estate, and when layered with the EHG and other grants, the effective discount for a median-income family can approach S$200,000 over the life of ownership. The trade-off is the waiting period — typically three to four-and-a-half years from booking to key collection — which requires careful planning if you are currently renting or living with parents.

The Plus and Prime restructuring reflects HDB’s continuing effort to balance locational desirability with long-term affordability. By imposing longer MOPs and clawbacks on high-demand locations, HDB aims to prevent BTO flats from functioning as pure financial instruments for short-term gain, keeping them as genuine homes for resident families. For buyers who prize flexibility and liquidity, the standard resale market or an Executive Condominium (EC) may be more appropriate despite the higher entry cost.

📊 Upcoming BTO Exercises and Policy Signals (2026–2027)

This section reflects publicly available information and should not be treated as investment advice.

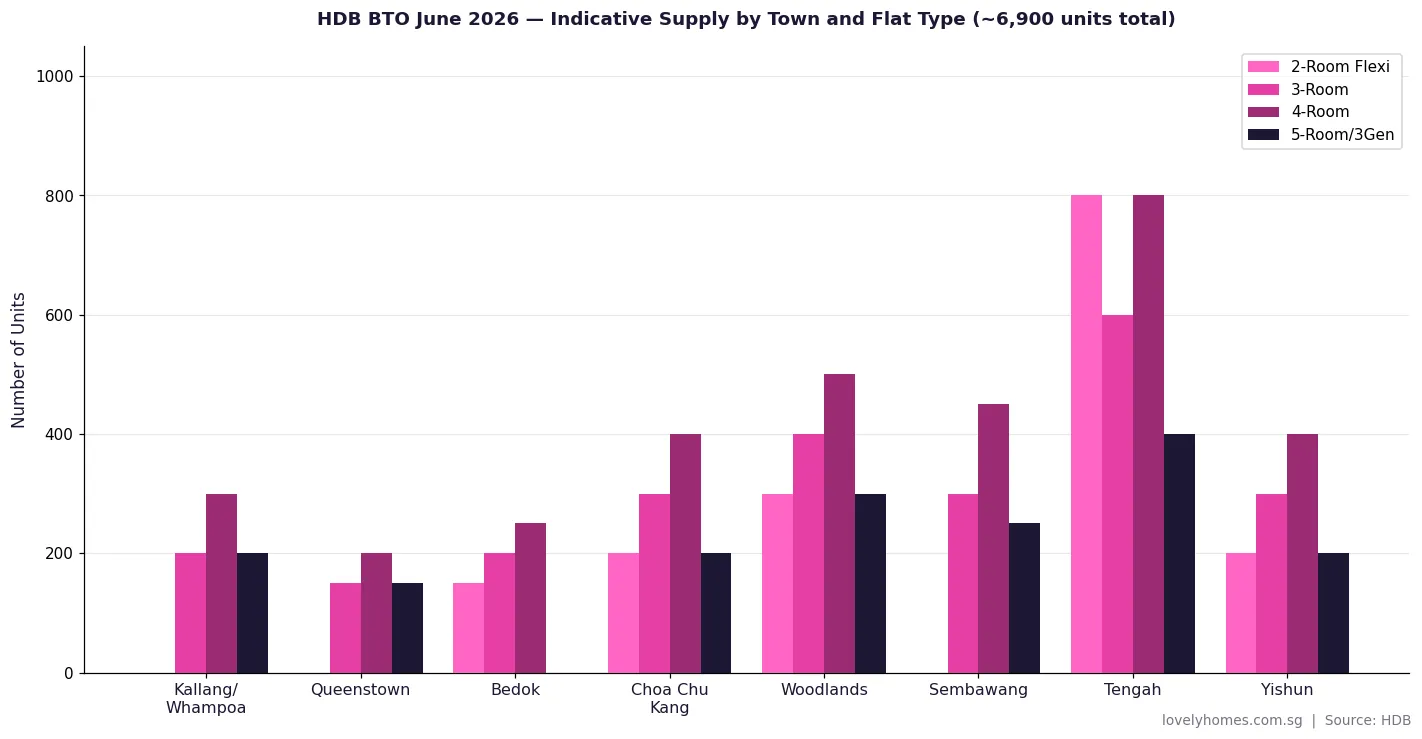

HDB has announced approximately 6,900 BTO units for the June 2026 exercise across Kallang/Whampoa, Queenstown, Bedok, Choa Chu Kang, Woodlands, Sembawang, Tengah, and Yishun. The next exercise is expected in August or September 2026, with further supply planned for Tengah (which is receiving the largest allocation as the new town builds up) and potentially a new site in the Jurong Lake District area. HDB’s annual BTO supply target for 2024–2025 was 19,000–20,000 units; this pipeline is expected to continue through 2027 to address the demand backlog from the COVID-era construction delays. Buyers who are unsuccessful in the June 2026 exercise should track MyNiceHome and the HDB press releases portal for the August–September launch announcement.

Frequently Asked Questions: HDB BTO Application 2026

How long does it take to get a BTO flat from application to key collection?

The total journey from submitting a BTO application to receiving your keys typically spans four to five years. Allow 2–3 weeks to obtain the HFE Letter, then 5–7 days for the application window. Ballot results are released in approximately 3 weeks; flat selection appointments are scheduled 3–6 months after that. Construction takes 38–48 months (roughly 3–4 years) from project launch. So the full door-to-door period is approximately 44–54 months, or about 4 years from application date. Some projects in non-mature estates have been delivered in under 40 months; complex urban-infill sites have taken longer. HDB publishes an estimated completion date for each project at the time of launch, which is the most reliable reference for your specific project.

Can Singapore Permanent Residents (PRs) apply for a BTO flat?

PRs can apply for a BTO flat only under the SC/PR scheme — that is, when they are applying jointly with a Singapore Citizen spouse. A PR cannot apply for a BTO flat on their own, nor can two PRs apply together. Under the SC/PR scheme, the PR must subsequently obtain Singapore Citizenship within a specified period after key collection (HDB’s latest requirement is that the PR spouse applies for citizenship if they have not done so within a reasonable time). PR singles and unmarried PR couples are not eligible for BTO. PRs who are single or not applying with an SC spouse should consider the HDB resale market under the HDB resale rules for PRs, which permit PR family/couple applications for resale flats.

What is the income ceiling for BTO flats in 2026?

The income ceiling depends on the flat type. For 2-Room Flexi and 3-Room BTO flats, the ceiling is S$7,000 per month gross household income. For 4-Room flats, the ceiling is S$10,000 per month. For 5-Room and 3-Generation (3Gen) flats, the ceiling is S$14,000 per month. Income is assessed based on the average gross monthly income over the 12 months preceding the application. Bonuses, commission, and variable pay are included in the calculation. For self-employed or commission-based applicants, IRAS Notice of Assessment income averaged over 12 months is used. If your income fluctuates, it is advisable to time your application to a 12-month window when your average income falls below the ceiling.

What happens if I am unsuccessful in the BTO ballot?

If you apply but do not receive a ballot queue number, or if your queue number is not reached (all flats are selected before your turn), you are treated as an unsuccessful first-timer applicant. Your first-timer priority status is retained, and HDB gives you one additional ballot chance: in the next BTO exercise, you will be issued two ballot chances instead of one for the same flat type and town category (non-mature or mature). After two or more consecutive unsuccessful attempts, first-timer families with children may apply under the Married Child Priority Scheme (MCPS) or the Additional Ballots Scheme for enhanced priority. There is no penalty for multiple unsuccessful applications. You may also wish to consider the HDB Sales of Balance Flats (SBF) exercises, which release unsold BTO units from previous exercises at (typically) lower prices and with shorter remaining construction wait times.

Can I rent out my BTO flat before the MOP?

No. You cannot rent out the entire BTO flat before completing the Minimum Occupation Period (MOP), which is 5 years from the date of key collection for standard flats (10 years for Plus and Prime flats). During the MOP, you and at least one listed occupier must be physically residing in the flat. You may rent out individual rooms (but not the entire flat) to eligible tenants, subject to HDB approval and the Non-Citizen Quota (NCQ) rules. Full subletting of the entire flat is only permitted after the MOP is complete and upon receiving HDB’s written approval. Violation of the MOP subletting restriction is a serious offence under the Housing and Development Act and can result in the compulsory acquisition of the flat by HDB with no compensation to the owner.

How much CPF can I use to buy a BTO flat?

For HDB flats (including BTO), CPF Ordinary Account (OA) savings may be used to pay the down payment, monthly mortgage instalments, BSD, and legal/conveyancing fees, subject to the Valuation Limit (VL) and Withdrawal Limit (WL). The Valuation Limit is the lower of the purchase price and the HDB assessed value at purchase; you may withdraw up to 100% of the VL from CPF. The Withdrawal Limit is 120% of the VL — beyond this, no further CPF can be used for housing and all mortgage repayments must be in cash. Since BTO flats are new and HDB sets the price equal to the assessed value, the VL and purchase price are the same and the 120% WL is typically reached only after many years of repayment. Any CPF withdrawn for housing is subject to accrued interest at the OA rate of 2.5% per annum, which must be refunded to your CPF account upon the eventual sale of the flat.

What is the difference between BTO, SBF, and ROF flat types?

HDB offers three main channels for buying new or near-new subsidised flats: BTO (Build-To-Order) — new flats that have not yet been built; buyers commit before construction and wait 3–4.5 years for key collection. SBF (Sales of Balance Flats) — unsold units from previous BTO exercises, typically with shorter wait times (1–3 years) as construction is already underway or complete; these are released approximately twice per year. ROF (Re-Offer of Balance Flats) — flats returned or unselected from prior exercises, offered in smaller batches more frequently. BTO offers the widest choice and (for popular estates) the lowest price relative to eventual resale value, but requires the longest wait. SBF and ROF can be good options for buyers who need to move sooner or who prefer a known, near-complete building. Eligibility rules are broadly similar across all three channels.

Related Articles on HDB and Property Buying in Singapore

- Singapore HDB Resale Guide 2026: Complete Guide to Buying and Selling HDB Resale Flats

- Singapore Executive Condo (EC) Buying Guide 2026: Eligibility, Prices, MOP and the New 10-Year Rules

- Singapore HDB Upgrading Guide 2026: Costs, ABSD, CPF and Step-by-Step Process

- Singapore Home Loan Complete Guide 2026: HDB Loans, TDSR, MSR and Best Rates

- HDB Grants Singapore 2026: EHG, CPF Housing Grant, Proximity Grant and Step-Up Grant Explained

- Singapore Buyer’s Stamp Duty (BSD) 2026: Rates, Calculations and Worked Examples

Disclaimer

This article is for general informational purposes only and does not constitute financial, legal, or housing advice. HDB BTO eligibility criteria, grant amounts, income ceilings, and MOP rules are set by the Housing & Development Board (HDB) and may be updated at any time. Always verify current eligibility at hdb.gov.sg and consult a licensed HDB solicitor or financial adviser before making any application or commitment. CPF rules are governed by the CPF Board; verify current withdrawal limits at cpf.gov.sg. LovelyHomes is not an HDB-authorised agent and this article does not constitute an application, booking, or commitment to any HDB flat.