TDSR and MSR are the two regulatory ratios the Monetary Authority of Singapore (MAS) uses to decide how much home loan any Singapore buyer can take. Get these wrong in your budgeting, and the pre-approval letter from the bank will come back smaller than the deposit you have already put down on a flat. This guide breaks down what each ratio means, how they stack, and exactly how to calculate your own limit for 2026.

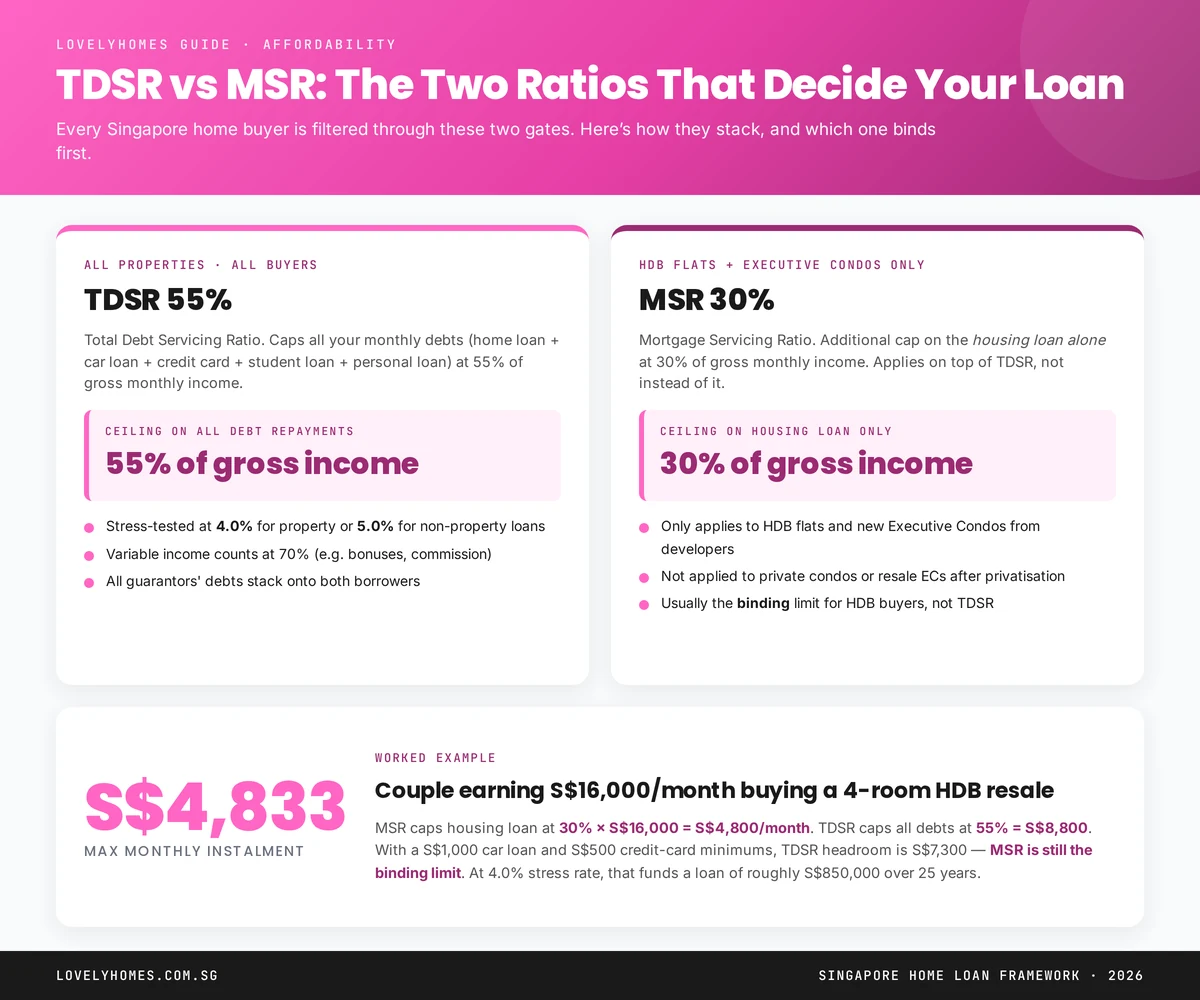

TDSR 55%: All your monthly debts (home loan, car loan, credit card minimums, student loans, personal loans) must stay at or below 55% of your gross monthly income.

MSR 30%: For HDB flats and new Executive Condos only — your monthly home loan alone must stay at or below 30% of gross monthly income. MSR sits on top of TDSR.

Stress rate: Both ratios are calculated using a 4.0% stress interest rate, not the actual package rate you are quoted.

Variable income: Bonuses, commission and rental income count at only 70% of their face value.

MSR is usually binding for HDB and EC buyers; TDSR is usually binding for private condo buyers.

What is TDSR and Why Does It Matter?

TDSR — Total Debt Servicing Ratio — was introduced in June 2013 as the backbone of Singapore’s sustainable-lending framework. It forces banks to look beyond your home loan and consider every monthly debt commitment you carry. If the sum of all those instalments exceeds 55% of your gross monthly income, the bank cannot extend you any further credit.

In practice, TDSR means that two borrowers on identical salaries can qualify for very different loan sizes if one of them also carries a car loan, a renovation loan, or a large outstanding credit-card balance. Because the ratio is regulatory rather than bank-specific, shopping around will not get you past it.

What counts in the 55% ceiling?

Housing loans (existing and the new one being applied for)

Car loans, motorcycle loans, and hire-purchase instalments

Renovation loans, education loans, personal loans

Minimum monthly payments on credit cards and overdraft facilities

Guarantor obligations on another party’s loan — even if you are not the primary borrower

What is MSR and When Does It Apply?

MSR — Mortgage Servicing Ratio — is a narrower, tougher cap that applies only when you are buying:

An HDB flat (BTO, Sale of Balance Flat, Open Booking, or resale), or

A new Executive Condominium (EC) directly from a developer, still within its minimum occupation period scheme.

MSR says that your monthly housing loan instalment alone must not exceed 30% of gross monthly income. Unlike TDSR, MSR does not let you compensate by showing you have no other debt — the housing instalment itself cannot breach the 30% line.

Private condos, landed property, and resale ECs after their 10-year privatisation milestone are not subject to MSR. Only TDSR applies. This is one of several reasons why private-property buyers on the same income can often borrow more than HDB buyers.

Figure 1: TDSR applies to every Singapore buyer; MSR adds a second, tighter cap for HDB flats and new ECs from developers.

How Banks Actually Calculate Your Limit

Here is the sequence every MAS-regulated bank follows when you submit a loan application:

Gross monthly income is totalled. Salary contributes 100%; variable income (bonus, commission, rent, freelance earnings) is haircut to 70%. For rental income, the bank also deducts a vacancy allowance.

Other monthly debts are added up. This includes a 3% notional minimum on your total credit-card outstandings if you do not pay in full.

Housing loan instalment is calculated at 4.0% stress rate, over your requested tenure (capped at 30 years for HDB, 35 for private). This is the rate used for ratio maths — not the 2.6% or 2.8% your package may quote.

Apply TDSR: (All debts + new housing loan at 4.0%) ÷ gross income must be ≤ 55%.

If HDB/new EC, apply MSR: New housing loan at 4.0% ÷ gross income must be ≤ 30%.

The loan is sized to the tighter of the two ceilings.

Worked example: couple earning S$16,000 a month

Consider a married couple with combined gross income of S$16,000, a car loan costing S$1,000 a month, and credit-card minimums of S$500 a month. They want to buy a 4-room resale HDB flat.

At 4.0% stress rate over 25 years, S$4,800/month supports a loan of approximately S$910,000. At the actual package rate of 2.6%, the real payment on that loan would be around S$4,127/month — giving the couple a S$673 monthly buffer once they move in.

Take away the car loan and the maths does not change — MSR still binds at S$4,800. Take away MSR (i.e. if they were buying a private condo instead), and the binding number becomes S$7,300 of TDSR headroom, translating to roughly a S$1,380,000 loan. Same couple, same income, different rule set, S$470k of extra purchasing power.

Stress Rate: The 4.0% That Quietly Decides Everything

MAS introduced the 4.0% medium-term interest rate floor (officially the “medium-term rate benchmark” or MTRB) in 2022, raising it from 3.5%. The stress rate is higher than virtually any home loan package in the market, which is the point — it builds in resilience against future rate rises.

Because the maths compounds, every 1% of stress-rate uplift cuts affordability by roughly 10%. That is why a package teaser rate of 2.5% does not actually buy you more house than a teaser of 3.0% — both are calculated at 4.0% for TDSR/MSR. What the lower package rate does buy you is cash-flow during the package term.

Variable Income: The 70% Haircut

If you earn a significant bonus, commission or rental income, the 30% haircut matters. Take a relationship manager earning S$10,000 base plus an average S$4,000 a month in commission. Gross looks like S$14,000. TDSR-countable gross is S$10,000 + (0.70 × S$4,000) = S$12,800.

To “grossed-up” income, banks typically require 24 months of commission history (12 for the more flexible ones). First-year hires with fat bonuses but short tenure often cannot count that income at all.

Three Levers to Increase Your Loan Ceiling

Extend the loan tenure (within the 30/35-year cap) — a longer tenure reduces the monthly instalment under the 4.0% stress calculation, freeing headroom under both ratios.

Retire consumer debt. Every S$1,000 of car-loan instalment taken off releases exactly S$1,000 of TDSR headroom. For HDB buyers, note this only helps if TDSR (not MSR) is the binding constraint.

Add a younger co-borrower. Tenure is capped at the weighted average age of all borrowers — bringing in a younger, income-earning co-borrower lifts the tenure ceiling and, by extension, your qualifying loan amount. Be deliberate about the legal and ownership implications before doing this.

Frequently Asked Questions

Does TDSR apply to refinancing?

For owner-occupied residential property, TDSR does not apply to refinancing of an existing loan (this is the “owner-occupier refinancing exemption”). For investment property, TDSR does apply on refinancing, with a debt-reduction plan over three years if you exceed the 55% cap.

Is rental income counted towards TDSR?

Yes. Rental income is haircut to 70% of face value, and banks further deduct a vacancy allowance. A 12-month tenancy agreement is usually required as evidence.

Does my existing home loan count if the property is rented out?

Yes, always. Every housing loan you are servicing — owner-occupied or rented — enters the TDSR calculation on the debt side, regardless of whether the rental income covers it.

Can I get a higher loan if I pay down my credit card before applying?

Yes, provided the payment clears before your bank pulls the credit bureau report. Banks calculate TDSR based on bureau-reported outstandings — pay down early enough for the next monthly report cycle.

What happens if my income drops after I take the loan?

TDSR is tested only at origination and on refinancing of investment property. A mid-loan income drop does not trigger a call on your loan — you simply need to keep paying the contracted instalment.

What to Do Next

TDSR and MSR are the first conversation with any bank, but they are not the only one. Your Loan-to-Value ratio and cash-on-hand position matter just as much. Your logical next reads on LovelyHomes:

Disclaimer: This guide is for general information and does not constitute financial advice. TDSR and MSR rules are set and periodically revised by MAS. Always verify current rules at mas.gov.sg and consult a licensed mortgage broker or bank before committing to any property purchase.

For most Singaporeans, purchasing a home represents the single largest financial commitment they will ever make. A typical S$500,000 home loan over 25 years will cost between S$180,000 and S$280,000 in interest alone—making the difference between an HDB concessionary loan (fixed at 2.6%) and a bank loan (pegged to SORA, pegged to 3M compounded SORA plus a bank spread) the difference between financial security and prolonged vulnerability to rate shocks. This 2026 guide walks you through both options, the figures that matter, and how to choose the right one for your circumstances.

Quick Answer

HDB Loan: 2.6% fixed for the loan’s life; rate stable; 75% max LTV; no surprises—but higher than current bank rates and you must be eligible (SC or PR, income ≤ S$14,000/month for families).

Bank Loan: Currently cheaper (1.5%–3.0% depending on fixed or floating); rate risk if SORA rises; 75% max LTV; fewer eligibility restrictions—but your monthly repayment could jump 20%+ if rates climb.

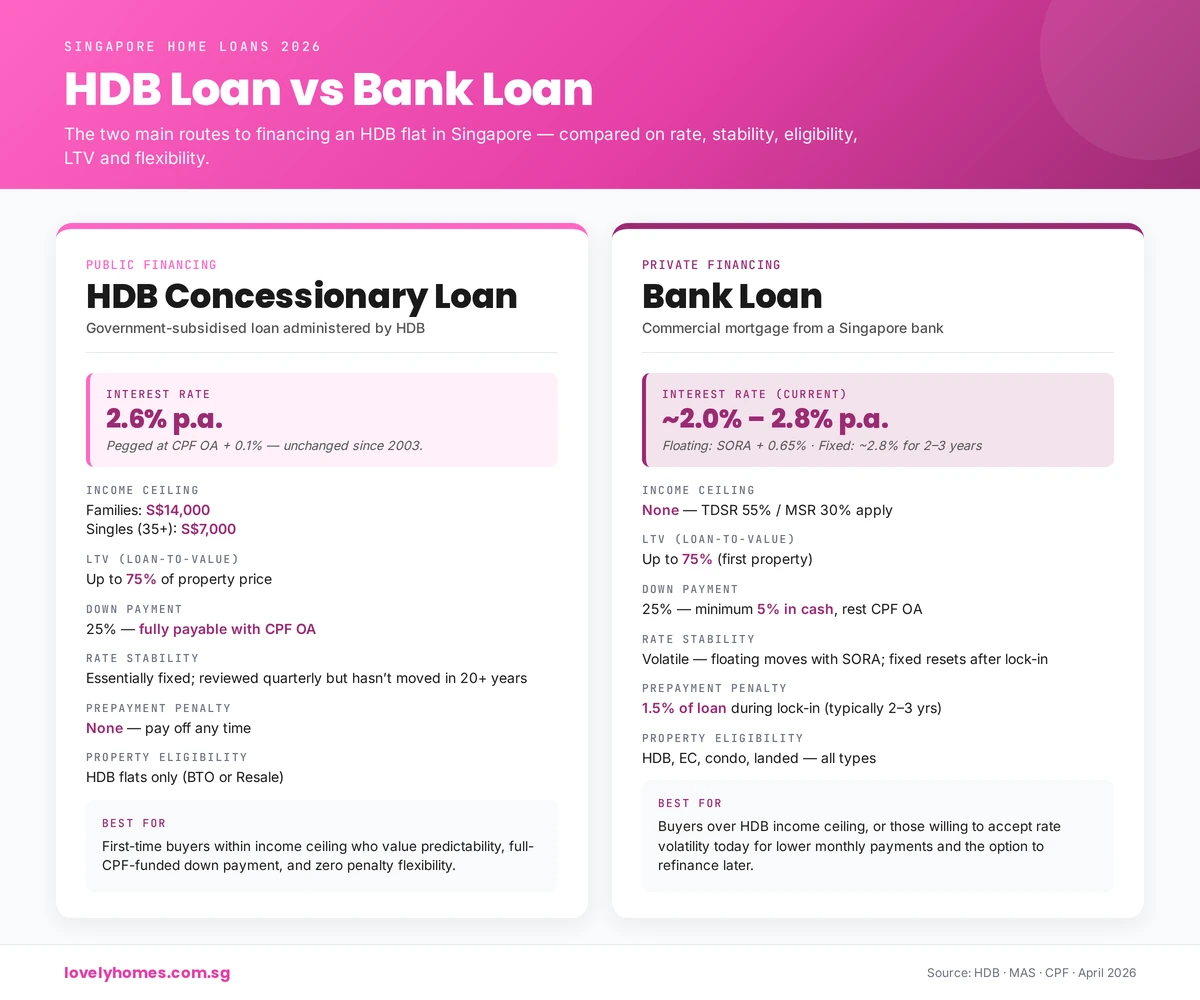

The HDB concessionary loan is Singapore’s most accessible home financing product. It is pegged to the CPF Ordinary Account (OA) interest rate plus 0.1%—a formula that has held since 1999. For 2026, the OA rate is 2.5%, making the HDB loan rate exactly 2.6% per annum, fixed for the life of the loan (or until you choose to refinance into a bank loan, at which point you cannot switch back).

HDB Loan: Eligibility

Citizenship: At least one owner must be a Singapore Citizen (SC). Permanent Residents (PRs) and foreigners cannot apply.

Income ceiling (monthly household): S$14,000 for families; S$7,000 for singles under the Young Single Scheme; S$21,000 for extended family schemes. These are hard ceilings—exceed them and you are ineligible, regardless of other factors.

Age: At least 21 at the time of the application.

Repayment by age 65: Loan tenure is 25 years maximum, or until you reach age 65, whichever is earlier.

HDB Loan: Key Terms

Term

HDB Loan

Interest Rate

2.6% p.a. (fixed; CPF OA + 0.1%)

Maximum LTV

75% (lowered from 80% on 20 Aug 2024)

Minimum Down Payment

25% (mix of cash & CPF OA; no mandatory cash minimum)

Maximum Tenure

25 years or age 65, whichever is earlier

MSR Cap

30% of gross monthly income

TDSR Cap

55% of gross monthly income

Rate Lock

Rate never increases; locked at 2.6% for life of loan

Early Repayment

No penalty; can pay down anytime using CPF or cash

Refinancing to Bank

Can refinance to bank loan (one-way; cannot switch back)

Example MSR Calculation: Your gross monthly household income is S$10,000. HDB MSR allows up to 30%, so your maximum monthly loan instalment is S$3,000. On a 2.6% 25-year loan, this translates to a maximum loan amount of roughly S$1,090,000 (before other debt).

Bank Loan: How It Works

Bank loans offer more flexibility than HDB loans but introduce interest-rate risk. Banks offer two primary structures: floating rates (pegged to SORA + spread) and fixed-rate packages (locked for 1–3 years, then typically floating). Check the current 3-month compounded SORA on the MAS domestic interest rates page. Banks typically add a spread of around 0.5%–1.0% on top. Fixed-rate packages range from 1.4% to 1.8% for 1–2-year locks.

Bank Loan: Eligibility

Citizenship: SCs, PRs, and even some foreigners can qualify (though foreigner terms are stricter, requiring higher down payments and lower LTV).

Income: No hard ceiling, but TDSR and MSR caps apply (see below).

Credit & Employment: Banks assess credit history, employment stability, and income verification.

Age: At least 21 at the time of application; typically loan must be repaid by age 60–75 (varies by bank).

Bank Loan: Key Terms

Term

Bank Loan (HDB)

Bank Loan (Condo)

Interest Rate (Floating)

3M SORA + 0.5–1.0% (current ~2.0%)

3M SORA + 0.5–1.0% (current ~2.0%)

Interest Rate (Fixed)

1.4%–1.8% for 1–2 yr lock

1.4%–1.8% for 1–2 yr lock

Maximum LTV (1st property)

75% (with 25-year tenure)

75% (with 30-year tenure)

LTV (2nd property outstanding)

45% max

45% max

Minimum Down Payment

25% (5% cash minimum; rest CPF or cash)

25% (5% cash minimum; rest CPF or cash)

Maximum Tenure

25 years (or to age 65)

30 years (or to age 65)

MSR Cap (HDB only)

30% of gross monthly income

N/A

TDSR Cap

55% of gross monthly income

55% of gross monthly income

Interest Rate Floor (TDSR calc)

3% (for calculation only)

4% (for calculation only)

Early Repayment Penalty

1.5% of outstanding balance (typically during lock-in; 2–3 yr lock-in standard)

1.5% of outstanding balance (typically during lock-in)

Rate Risk

After lock-in expires, rate floats; monthly payment can increase significantly

After lock-in expires, rate floats; monthly payment can increase significantly

Important TDSR Note: Banks use a minimum interest-rate floor when calculating whether you are eligible, even if the actual rate is lower. For HDB loans, the floor is 3%; for private property, it is 4%. So even if a bank offers you 2.0% floating, they assume 3%–4% when working out your TDSR, making the true affordability ceiling lower than the headline rate suggests.

Figure 1: The two main home-loan routes in Singapore — compared on rate, eligibility, LTV and flexibility.

Side-by-Side Comparison: HDB vs Bank Loan

Factor

HDB Loan

Bank Loan

Interest Rate Type

Fixed (pegged to CPF OA)

Fixed (1–3 years) or Floating (SORA+)

Current 2026 Rate

2.6%

1.5%–1.8% (floating); 1.4%–1.8% (2yr fixed)

Maximum LTV (1st property)

75%

75% (HDB); 75% (Condo)

Min Cash Down

0% (full 25% can be CPF)

5% cash; remainder CPF or cash

Max Tenure

25 yrs or age 65

25 yrs (HDB) / 30 yrs (Condo), or age 65

MSR / TDSR

MSR 30%; TDSR 55%

TDSR 55% (no MSR for condo)

Rate Stability

Locked forever; never increases

Floating rate risk after lock-in; monthly payment can jump 20%+

Early Repayment Penalty

None

1.5% during lock-in (typically 2–3 yrs)

Switching Flexibility

Can refinance to bank (one-way; no switch-back)

Can refinance to another bank; cannot switch to HDB

Eligibility Ceiling

Income ceiling: S$14,000/mth (families); SC required

No income ceiling; open to PRs & some foreigners

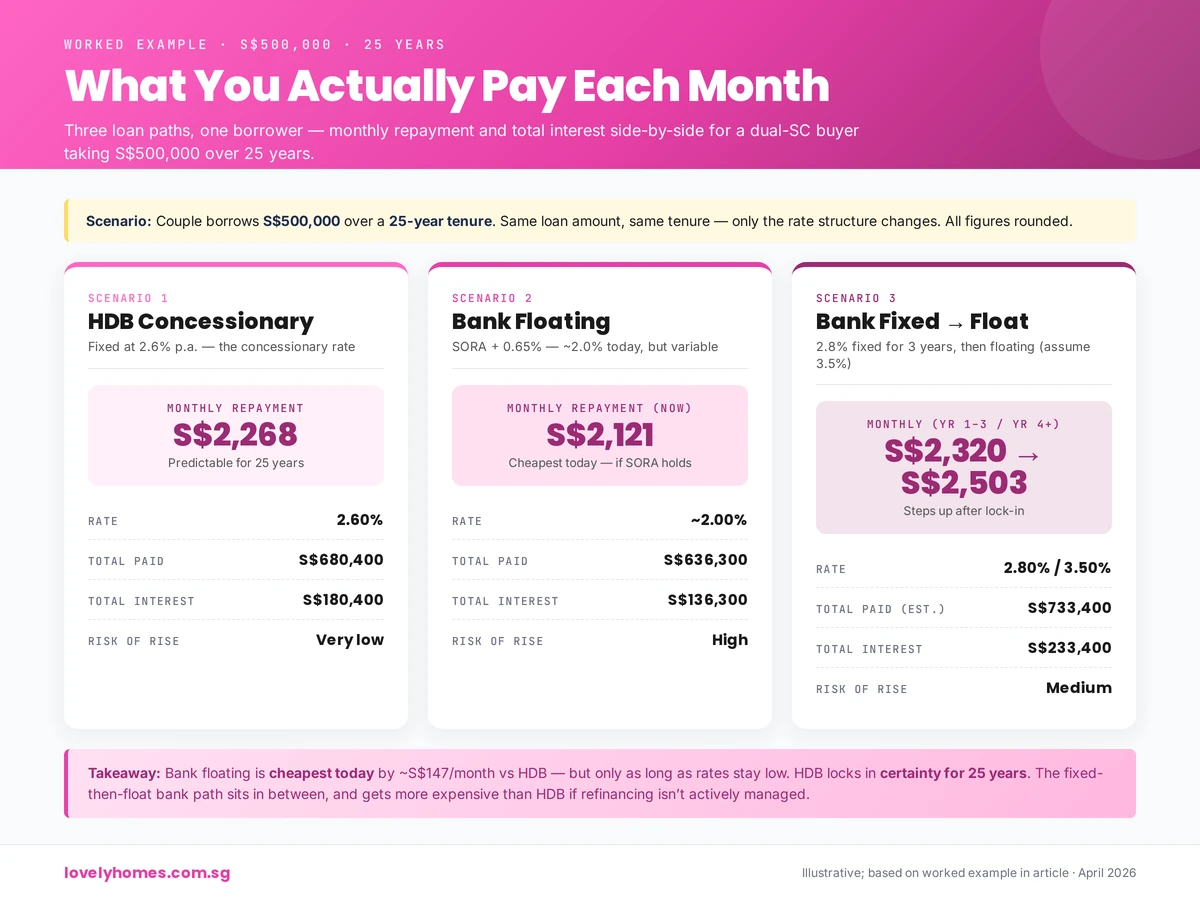

Figure 2: Three loan paths, same borrower — HDB S$2,268/mo; Bank floating S$2,121/mo; Bank fixed-to-floating S$2,320 → S$2,503/mo.

Worked Example: S$500,000 Loan, 25-Year Tenure

Let’s compare the true cost of an HDB loan versus two bank scenarios: a floating-rate loan and a fixed-then-floating loan.

Scenario 1: HDB Concessionary Loan at 2.6%

Loan Amount: S$500,000 Interest Rate: 2.6% p.a. (fixed for life) Tenure: 25 years (300 months) Monthly Instalment: S$2,269 Total Interest Paid: S$180,700 Total Amount Repaid: S$680,700

Scenario 2: Bank Floating Loan (SORA + 0.65%, Current ~2.0%)

Loan Amount: S$500,000 Interest Rate (Current): 2.0% p.a. (floating; SORA ~1.35% + 0.65% spread) Interest Rate (Assumption: Average over 25 yrs): 3.0% p.a. (to account for expected rate normalisation) Tenure: 25 years Monthly Instalment (at 2.0%): S$2,108 Monthly Instalment (at 3.0% average): S$2,372 Total Interest Paid (at 3.0% average): S$210,600 Total Amount Repaid: S$710,600 Life-of-Loan Difference vs HDB: +S$29,900 (approximately 3.5% higher total cost)

Note: The bank loan appears to save S$161/month initially, but that saving evaporates as rates normalise. Over the 25-year life, the HDB loan saves roughly S$30,000 despite starting at a higher rate.

Scenario 3: Bank Fixed (2.8%) for 3 Years, Then Floating (Assume 3.5%)

Years 1–3: 2.8% fixed

Monthly instalment: S$2,294

Years 4–25: 3.5% floating (after lock-in)

Recalculated instalment: S$2,506

Average Monthly Instalment: S$2,404 Total Interest Paid: S$221,200 Total Amount Repaid: S$721,200 Life-of-Loan Difference vs HDB: +S$40,500 Monthly Jump at Year 4: +S$212 (9% increase)

Key Insight: Even if you start with a bank loan at 2.0%–2.8%, the long-term cost edge of the HDB loan (at fixed 2.6%) becomes clear once you account for rate normalisation and the arithmetic of compound interest over 25 years. Moreover, the HDB loan offers psychological and budgetary peace of mind—your monthly repayment is guaranteed never to rise.

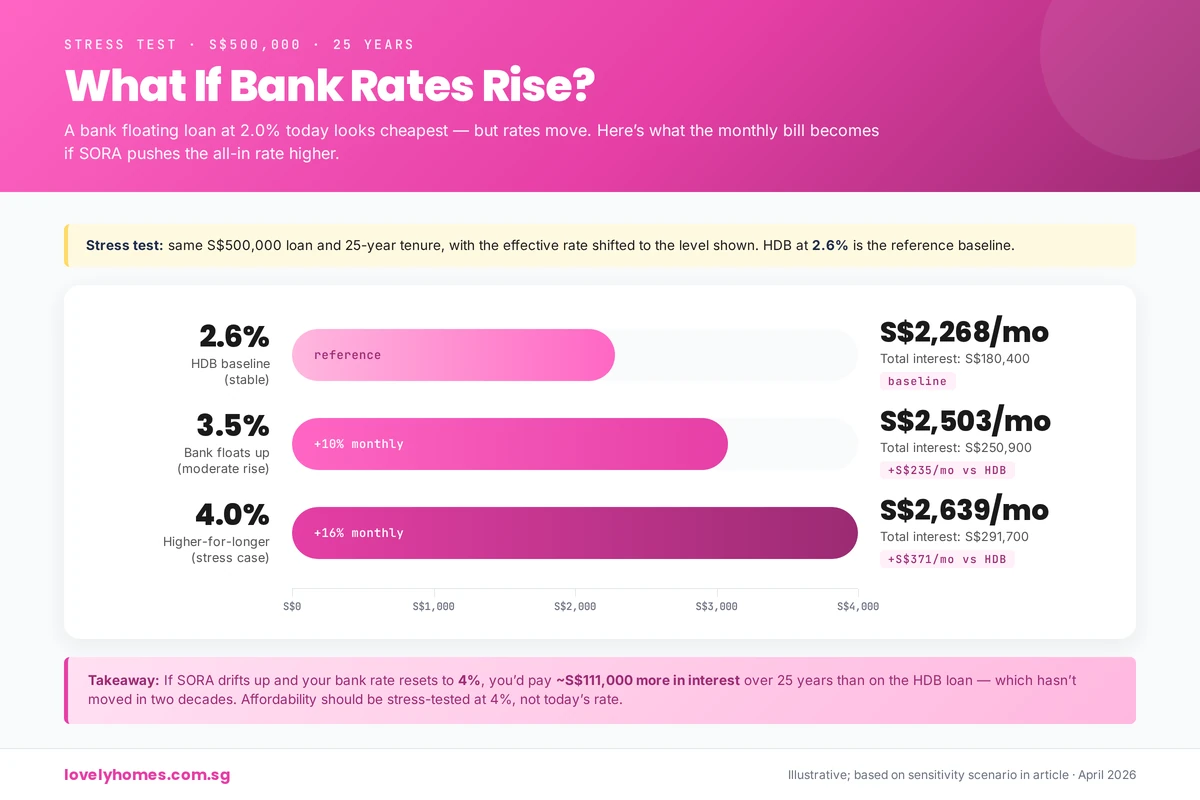

Sensitivity: What If Bank Rates Rise to 4.0%?

If 3M SORA drifts back toward 2.5% and bank spreads remain at 0.65%, a floating-rate loan would reset to approximately 3.15% base, but with TDSR floors at 4%, some borrowers would see repayments jump further. At a 4.0% effective rate:

S$500,000 loan, 25 years remaining (worst-case: rate shock in year 1): Monthly Instalment at 4.0%: S$2,639 vs HDB at 2.6%: S$2,269 Monthly Shock: +S$370 (+16.3%) Annual Impact: +S$4,440

For a household spending 30% of gross monthly income on the mortgage, a 16% rate shock could push TDSR above 55%, triggering a lender’s demand for early repayment or refinancing—a real risk during volatile rate environments.

Figure 3: Stress-tested at 2.6%, 3.5% and 4.0% — a rise to 4% adds ~S$111,000 in interest over 25 years vs the HDB baseline.

Which Should You Choose?

Choose HDB Loan If:

You are eligible (SC, income ≤ S$14,000/mth for families).

Rate stability is a priority. You plan to stay in the home for 15+ years and want zero uncertainty about future payments.

You are risk-averse or budget-conscious. Your household income is tight, and a 10%–16% payment jump would strain your finances.

You value the psychological benefit of a locked rate and a simpler loan structure.

You expect rates to rise. If SORA normalises to 2.5%+ (and spreads remain), HDB’s 2.6% becomes increasingly competitive.

Choose Bank Loan If:

You exceed HDB income ceilings (e.g. dual-income household exceeding S$14,000/mth) or are a PR/foreigner.

You are comfortable with rate risk and have sufficient financial buffers to absorb a 10%–20% payment increase.

You plan to sell or refinance within 5–10 years. Lower initial rates and longer maximum tenures (30 years for condos) offer flexibility.

You believe rates will stay low. If you expect SORA averages well below 2.6% over the life of your loan, a floating bank loan saves vs the HDB concessionary rate. If it averages above 2.6%, HDB is cheaper.

You want to refinance easily. Bank loans can be refinanced to another bank mid-term; HDB loans, once converted to a bank, cannot be converted back.

You own a condo or landed property. Bank loans offer longer tenures (30 years) and higher potential LTV; HDB loans only apply to HDB flats and ECs.

Refinancing: When and Why to Switch

The option to refinance exists at any point in your loan journey. Understanding when and why to refinance is crucial to optimising your loan cost.

HDB to Bank Refinance

If you currently hold an HDB loan at 2.6%, you can refinance to a bank loan. This is a one-way decision—once you switch to a bank, you cannot switch back. Refinancing makes sense if:

Bank rates fall significantly below 2.6% and are locked in for an extended term (5+ years).

You exceed HDB’s income ceiling due to a salary increase and want to increase your loan amount.

You are refinancing to raise cash (e.g. home equity release) against your property.

Give HDB three months’ written notice of your intention to refinance. HDB will calculate the outstanding balance and any adjustment due to CPF contributions.

Bank to Bank Refinance (or HDB → Bank)

If you hold a bank loan, you can refinance to another bank or (once) to HDB, depending on your eligibility. Refinancing makes sense if:

Your current fixed-rate lock-in is about to expire and rates have fallen; refinance before the jump.

Another bank offers 0.3%–0.5% lower rates or a longer fixed-rate tenure.

You want to consolidate multiple loans or restructure your debt.

Typical lock-in periods: 2–3 years. Early repayment within the lock-in incurs a 1.5% penalty on the outstanding balance. After lock-in, partial or full repayments are fee-free.

Lock-In Mechanics

Most bank home loans come with a lock-in clause that penalises early repayment during the initial fixed-rate period. The lock-in typically lasts 2–3 years. Here’s what you need to know:

Lock-in Period: Typically 2–3 years from the date of drawdown.

Early Repayment Penalty: 1.5% of the outstanding loan balance if you repay (or refinance) before lock-in expires.

After Lock-In: You can repay in full or in part without penalty. You can refinance to another bank.

Fixed-Rate Lock vs Lock-In: Do not confuse the fixed-rate period (e.g. 2.8% for 2 years) with the lock-in period. A 2-year fixed rate typically comes with a 2–3-year lock-in penalty clause.

Frequently Asked Questions

1. Can I switch from HDB to bank and back?

No. Refinancing from HDB to bank is one-way. Once you switch to a bank loan, you cannot return to HDB financing. Choose carefully before making the switch. If you are considering it, ensure bank rates are significantly lower and locked in for at least 5 years to justify the irreversibility.

2. What happens if I miss an HDB or bank loan payment?

Missing a payment triggers late fees and can damage your credit score, making future refinancing more expensive. For HDB loans, persistent defaults can lead to legal action and, in extreme cases, repossession of the flat. For bank loans, the consequences are similar. Both lenders are empowered to initiate enforcement proceedings if you default for more than three months. Contact your lender immediately if you foresee difficulties; many offer restructuring or deferment options for borrowers facing temporary hardship.

3. Can I use CPF to pay my mortgage?

Yes. You can use CPF Ordinary Account (OA) funds to pay both HDB and bank home loan monthly instalments, subject to:

Your CPF OA balance must be sufficient to cover the instalment.

CPF will automatically deduct the monthly instalment from your OA if you have set up standing instructions.

If your CPF OA is insufficient, you must pay the balance in cash.

You cannot use your CPF Medisave Account (MA) or Special Account (SA) for loan repayment.

After loan maturity, CPF regulations allow you to retain a minimum sum in your Retirement Account (RA) for healthcare and longevity protection; excess funds can be withdrawn.

4. What is SORA, and why does it matter?

SORA stands for Singapore Overnight Rate Average. It is the interest rate at which banks lend to each other overnight in the Singapore money market, published daily by the Monetary Authority of Singapore (MAS). Most bank home loans in Singapore are now pegged to 3-Month Compounded SORA (reviewed quarterly) rather than the older SIBOR benchmark.

Why it matters: Your bank loan interest rate is typically SORA + a bank spread (e.g. 0.65%). As SORA fluctuates, your loan rate (and monthly payment) fluctuates. Historically 3M SORA has moved widely — from well under 1% in 2020–2021, rising above 3% through 2023–2024, and moderating thereafter. Always check the latest rate on the MAS website before committing to a package. Understanding SORA trends helps you forecast your likely repayment path.

5. How does the interest-rate floor affect my loan amount?

When calculating whether you qualify for a loan (TDSR test), banks assume a minimum interest rate, even if the offered rate is lower. For HDB loans, the floor is 3%; for private property, it is 4%. This means:

If a bank offers you 2.0% floating but applies a 4% floor for TDSR calculation, you are approved based on 4% affordability, not 2%.

If your income is S$10,000/month and TDSR is 55%, your maximum total debt repayment is S$5,500/month.

At a 4% rate (the TDSR floor), a S$500,000 loan over 25 years costs ~S$2,639/month.

Even though the actual rate might be 2.0%, the lender approves you at 4% to protect against future rate rises.

This floor is a safeguard for lenders and borrowers alike, preventing over-leverage in a low-rate environment.

6. Can I take a joint loan with a family member?

Yes. Both HDB and bank loans can be taken jointly (e.g. spouse, parent, or adult child). Joint applicants must:

Both be on the property title (either as joint tenants or tenants-in-common).

Both pass the eligibility checks (citizenship, age, credit, income).

Both be liable for the loan; if one co-borrower defaults, the lender can pursue either or both.

Agree on the split of ownership (50:50 is common; other splits are possible but more complex for tax and CPF purposes).

Joint borrowing increases the combined household income for TDSR/MSR purposes, often allowing a larger loan. However, both parties remain responsible if the other defaults.

7. Is a fixed or floating rate better?

There is no universally correct answer; it depends on your risk appetite and rate outlook.

Fixed Rate (1–3 years): Choose if you want certainty and believe rates will rise. Lock-in at the lowest rate available (currently 1.4%–1.8% for 1–2 years). After lock-in expires, you will refinance or face a floating rate, so you are not truly “locked” for 25 years.

Floating (SORA+): Choose if you believe rates will stay low and you can afford a 20%–30% payment increase. Currently, floating rates are lower than fixed (around 1.5%–2.0% all-in vs 1.4%–1.8% fixed), so you pay a rate-stability premium if you lock in.

In 2026, most experts recommend a 2-year fixed rate as a compromise: you get near-current rates locked in for two years, and then you can reassess when the lock-in expires.

Summary: Making Your Decision

Choosing between an HDB loan and a bank loan is ultimately a question of values: stability vs savings, predictability vs flexibility. The HDB loan offers peace of mind and long-term cost protection but requires eligibility. The bank loan offers potential short-term savings and flexibility but introduces rate risk. Work through the decision tree below to clarify your path:

Start here: Are you a Singapore Citizen with household income ≤ S$14,000/month (families)?

Yes: You can access the HDB loan. Proceed to the next question.

No: You must use a bank loan. Skip to bank-loan considerations below.

Next: Is rate stability your top priority, or are you comfortable with rate risk?

Rate stability: Choose HDB. You cannot beat a fixed 2.6% rate that will not rise for 25 years.

Comfortable with risk: Compare HDB (2.6%) with current bank rates (floating 1.5%–2.0%; fixed 1.4%–1.8%). If bank rates are <2.2% and locked in for 5+ years, bank may be worthwhile. If rates are expected to rise to 3%+, HDB’s 2.6% becomes increasingly attractive.

For bank-loan applicants: What is your holding timeline?

Short term (5–10 years): Floating or short fixed-rate packages (1–2 years) are fine; refinance or sell before rate shock.

Long term (15+ years): Lock in a fixed rate (2.8%–3.0%) for as long as possible (5+ years if available). The certainty is worth 0.3%–0.5% in extra rate cost.

Key Takeaways

HDB loans are fixed at 2.6% (pegged to CPF OA + 0.1%). This rate will not increase for the life of the loan—a powerful advantage in a rising-rate environment.

Bank loans are currently cheaper (1.5%–2.0% floating; 1.4%–1.8% fixed for 1–2 years) but introduce rate risk. After lock-in expires (typically 2–3 years), your payment can jump 10%–30%.

Over a 25-year life, an HDB loan typically costs S$30,000–S$40,000 less than a bank loan that averages 3.0% over the tenor, even though it starts at a higher rate.

Eligibility is the first gatekeeper. If you are a SC with income ≤ S$14,000/month, HDB is an option; otherwise, you must use a bank.

Refinancing is possible but irreversible. HDB → bank is one-way; bank → bank is flexible. Plan before you switch.

Rate floors and TDSR caps mean that your true affordability is often lower than headline rates suggest. Always ask your lender what rate floor they use in their TDSR calculation.

In 2026, the optimal strategy for most Singaporeans is: (1) if HDB-eligible, take the HDB loan unless bank rates are locked below 2.2% for 5+ years; (2) if bank-eligible only, lock in a 2-year fixed rate at 1.4%–1.8% as a bridge, then reassess when lock-in expires.

This guide is for general information only and does not constitute legal, tax, or financial advice. Interest rates, LTV limits, MSR/TDSR caps, and eligibility rules change frequently. Always verify current figures with HDB (hdb.gov.sg), MAS (mas.gov.sg), and your bank before committing to a loan package. For complex situations—mixed-nationality couples, self-employed income, or refinancing decisions—consult a licensed mortgage advisor or conveyancing lawyer. CPF rules, tax treatment, and grant eligibility have edge cases; always verify your specific situation with the relevant authority.