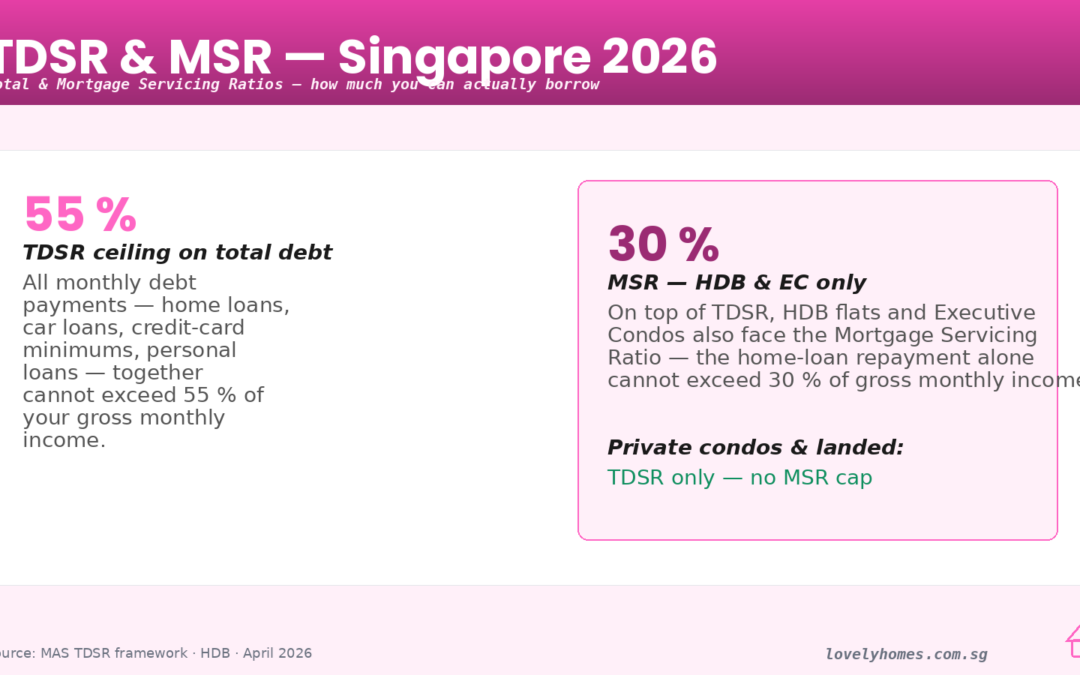

Figure 1: The two numbers that decide every Singapore home loan — TDSR at 55% of income and MSR at 30% for HDB and EC purchases.

If you have ever wondered why the bank’s pre-approval letter gave you a smaller loan than you budgeted for — or why a friend on the same salary can borrow noticeably more than you — the answer almost always comes down to two acronyms: TDSR and MSR. These are the two borrowing limits the Monetary Authority of Singapore (MAS) bakes into every residential mortgage, and in 2026 they are the single biggest determinants of how much home you can actually finance.

This guide is the 2026 edition. It covers exactly how TDSR and MSR are calculated, how they interact with the loan-to-value (LTV) cap, where the 4.0% stress-test rate comes from, what counts as income, what doesn’t, and — crucially — how to game the numbers in your favour without breaking any rules. We walk through a fully-worked Singapore example end-to-end and finish with the policy trajectory so you know what to watch for next.

Quick Answer: The 10 Things Every Singapore Borrower Should Know

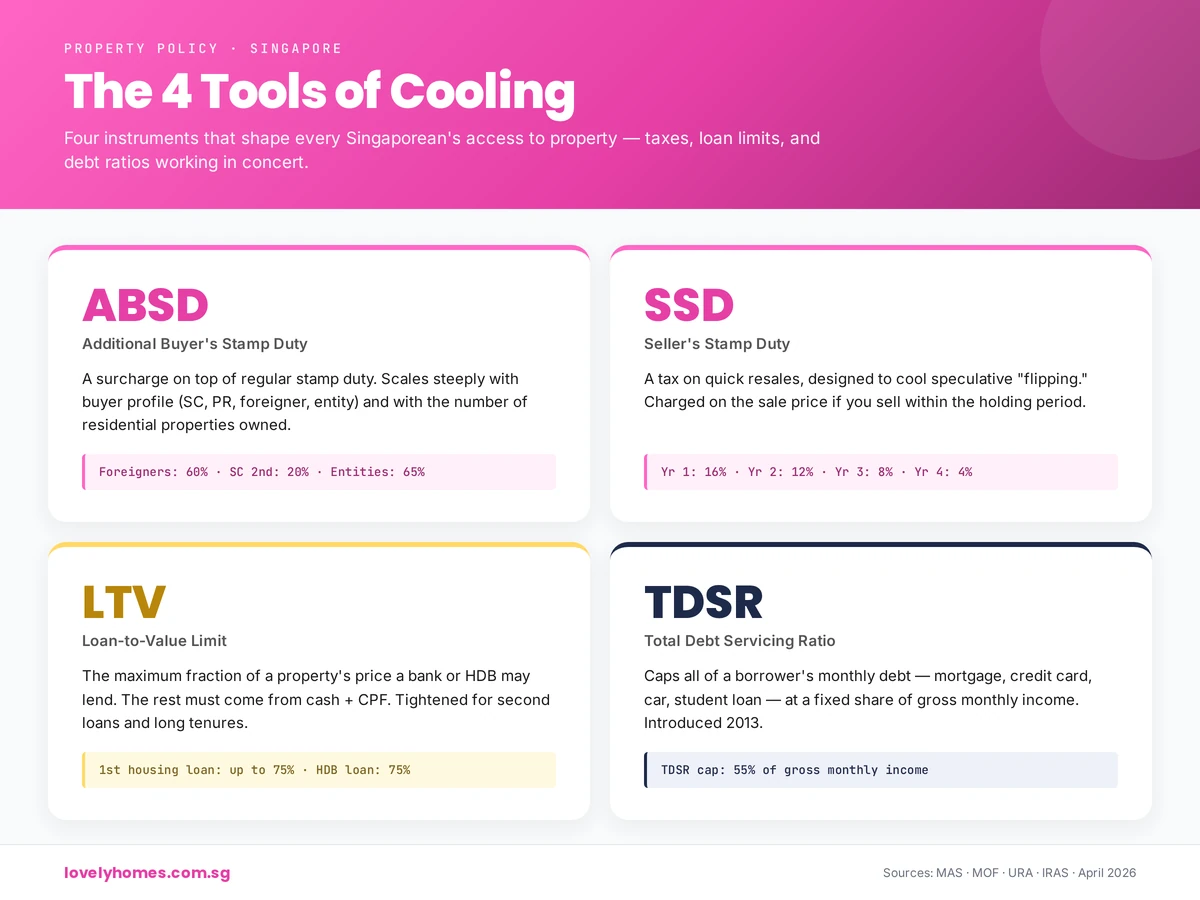

TDSR is 55%. Total monthly debt repayments — including the new mortgage — cannot exceed 55% of your gross monthly income. Applies to every residential property loan.

MSR is 30%. Mortgage repayments on an HDB flat or Executive Condominium (EC) bought from the developer cannot exceed 30% of gross monthly income. Private condos and landed property have no MSR.

Stress-test rate is 4.0%. TDSR and MSR are calculated at a medium-term interest rate of 4.0% for residential loans, regardless of the rate you actually pay today.

LTV caps layer on top. First housing loan: up to 75% of purchase price. Second housing loan: up to 45%. Third and beyond: up to 35%.

Age and tenure matter. If the loan tenure pushes past age 65, or exceeds 30 years (25 for HDB), the LTV cap drops by 20 percentage points.

Variable income is haircut by 30%. Commission, bonus, rental and freelance earnings are only counted at 70% of the proven figure.

Existing debts eat into headroom. Car loans, credit-card minimum payments, student loans, and other mortgages all hit your TDSR ceiling before the new home loan does.

Guarantors are counted too. If you guarantee a sibling’s loan, it may sit in your TDSR — not theirs.

Cash down-payment rules mirror LTV. The first 5% (25% at higher LTV tiers) must be paid in cash; the balance can be CPF Ordinary Account funds.

Refinancing carve-out. Borrowers refinancing an owner-occupied property with no cash-out may be exempted from TDSR — a narrow but useful escape hatch.

What Is TDSR — The Framework That Underpins Every Home Loan

The Total Debt Servicing Ratio was introduced in June 2013 as part of MAS’s cooling-measures programme (see our full cooling measures timeline for the wider context). Its purpose is simple: to stop households from levering up to a level where a modest rise in interest rates would push them into negative cash flow. The 2010s saw Singapore’s household debt-to-GDP ratio climb past 70%, and MAS wanted a circuit-breaker that worked the same way regardless of which bank a buyer walked into.

TDSR caps all monthly debt obligations at 55% of gross monthly income. “All debt” is deliberately broad: it includes the prospective home-loan instalment (calculated at the stress-test rate), existing mortgages, car loans, personal loans, renovation loans, student loans, credit-card minimum repayments and any loans you have personally guaranteed. Even a dormant credit card with a S$20,000 limit is counted if the bank uses the 3% minimum-payment convention.

The ratio was originally set at 60% in 2013 and tightened to 55% in December 2021, where it remains in 2026. That three-percentage-point shave looks small on paper but at a typical Singapore household income removes roughly S$150,000–S$200,000 of borrowing capacity.

What Is MSR — The Second Ratio You Cannot Ignore for HDB and EC Buyers

The Mortgage Servicing Ratio is narrower but stricter. Introduced for HDB loans in 2011 and extended to bank loans on HDB flats in 2013, MSR caps the mortgage portion alone at 30% of gross monthly income for purchases of HDB flats and Executive Condominiums bought directly from the developer.

MSR is a subset of TDSR, not a substitute. HDB and new-EC buyers must clear both ratios — the tighter of the two binds. In practice MSR is almost always the binding constraint for HDB buyers because existing debt rarely adds up to the 25-percentage-point gap between MSR (30%) and TDSR (55%). For EC buyers the numbers narrow as the project moves through its 10-year maturation period — after the five-year minimum occupation period and the ten-year privatisation, a resale EC is treated like a private condo for borrowing-limit purposes, so TDSR alone applies.

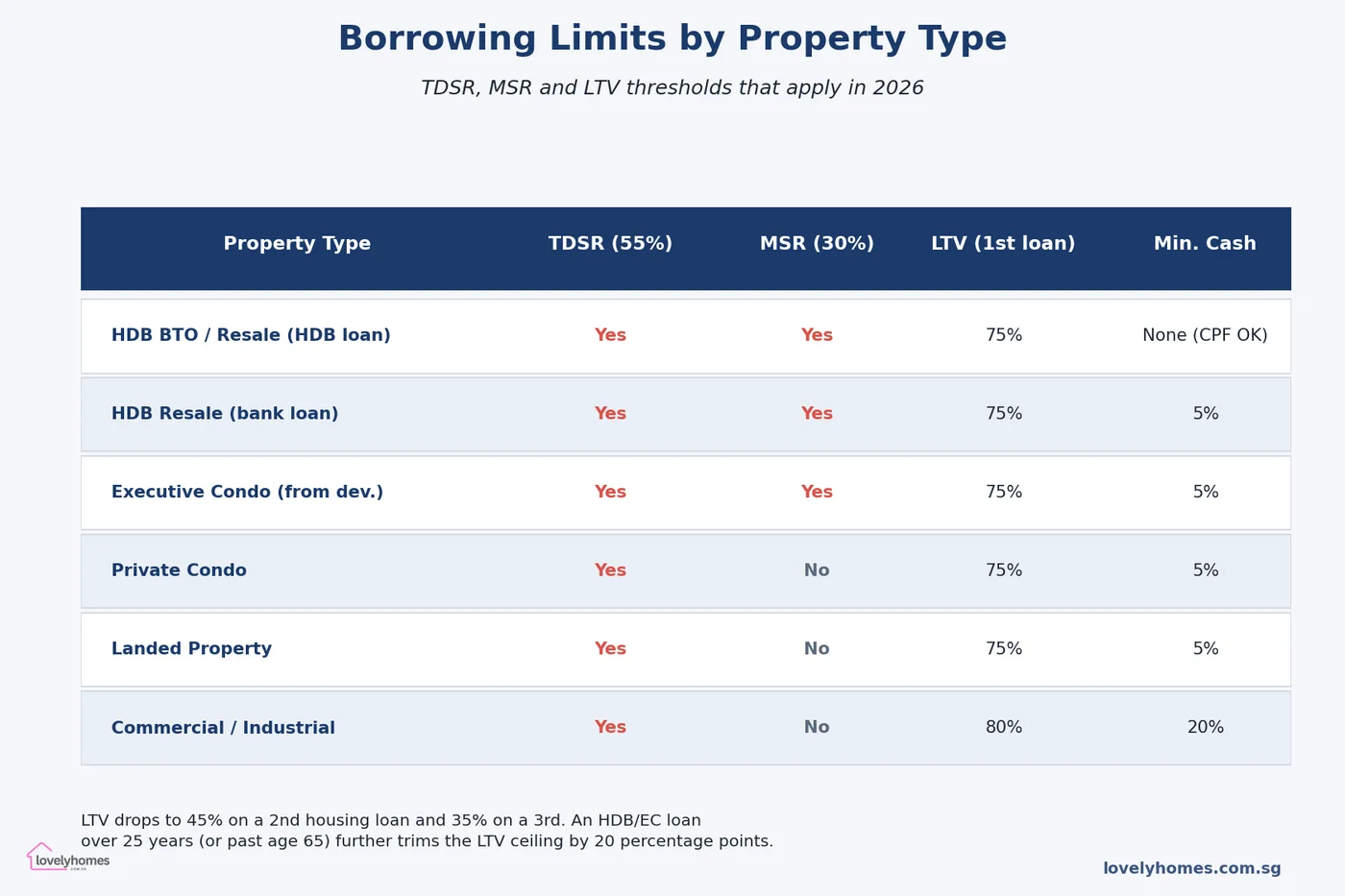

For a side-by-side look at which ratios hit which property type, the matrix below summarises 2026 rules.

Figure 2: 2026 borrowing limits by property type. HDB flats and ECs face both MSR and TDSR; private condos, landed property and commercial assets only face TDSR.

How the 4.0% Stress-Test Rate Works — And Why It Matters More Than Your Actual Rate

Here is the trap that catches most first-time buyers: banks must calculate your monthly instalment using an assumed rate of 4.0% for residential mortgages, even if your actual rate is 2.5% or 3.0%. This is the medium-term interest rate, set by MAS and reviewed from time to time. It was revised upward from 3.5% to 4.0% in September 2022 and has not moved since.

Why 4.0%? The rate is designed to approximate the long-run average that Singapore floating-rate loans have oscillated around over a 30-year horizon. It is deliberately punitive — regulators would rather have borrowers told “you qualify for less” at origination than have the same borrowers go into arrears when rates spike. Anyone who lived through the 2022–2023 rate cycle, when three-month SORA went from 0.2% to 3.8% in 18 months, will appreciate the logic.

The mechanic: the bank plugs a 4.0% rate into the standard amortisation formula using your chosen loan tenure, derives an assumed monthly instalment, and tests that figure against your TDSR (55%) and, if applicable, MSR (30%). Your actual repayment — calculated at whatever rate the bank is offering — will be lower in most cases, leaving you with a margin of safety that MAS consciously engineered.

What Counts as Income — And Why Variable Pay Is Penalised

Income for TDSR/MSR purposes is not what you see on your IRAS tax statement. MAS prescribes a structured treatment:

Fixed salary. Counted at 100%. Evidenced by payslips (usually three to six months) and the latest CPF contribution history.

Variable income. Commission, bonus, overtime, and freelance earnings are haircut by 30%, so only 70% of the verified average is recognised. The haircut applies to the entire variable component, even if you can show multiple years of steady track record.

Rental income. Counted at 70% of the gross rent receivable, net of void periods. A two-year tenancy agreement is strong evidence; month-to-month leases are viewed more sceptically.

Self-employed / business income. Two years of Notice of Assessment (NOA) are the default evidentiary bar, with the 30% haircut applied.

Allowances and AWS. Typically 100% if contractual and evidenced; otherwise haircut.

This is where the seemingly simple 55% number becomes surprisingly individual. A banker earning S$12,000 monthly but with 40% of that as variable gets assessed on S$7,200 fixed + S$3,360 post-haircut variable = S$10,560 — so the TDSR ceiling drops to S$5,808 per month rather than the nominal S$6,600.

What Counts as Debt — The Items Borrowers Miss

The other half of the equation is debt. The headline items — the new home loan instalment, existing mortgages, and car loans — are obvious. Less obvious items often catch borrowers out:

Credit-card minimum payments. Banks use a 3% minimum convention on the outstanding balance (or sometimes on the total credit limit). If you carry S$30,000 revolving credit across cards, that is a S$900 monthly hit on your TDSR — shaving S$192,000 off your loan ceiling at a 4.0% stress rate over 30 years.

Renovation and personal loans. Unsecured loan instalments count in full.

Student loans. Included in TDSR from the date repayments begin.

Guarantor obligations. If you have co-signed a relative’s loan and there is no formal debt-transfer, some banks will count the full instalment against you. Others use 50%. Ask the relationship manager explicitly.

Outstanding ABSD remission obligations. If you are on a remission schedule (e.g. from selling a prior property to claim remission on a new purchase), the existing loan remains in TDSR until the sale completes.

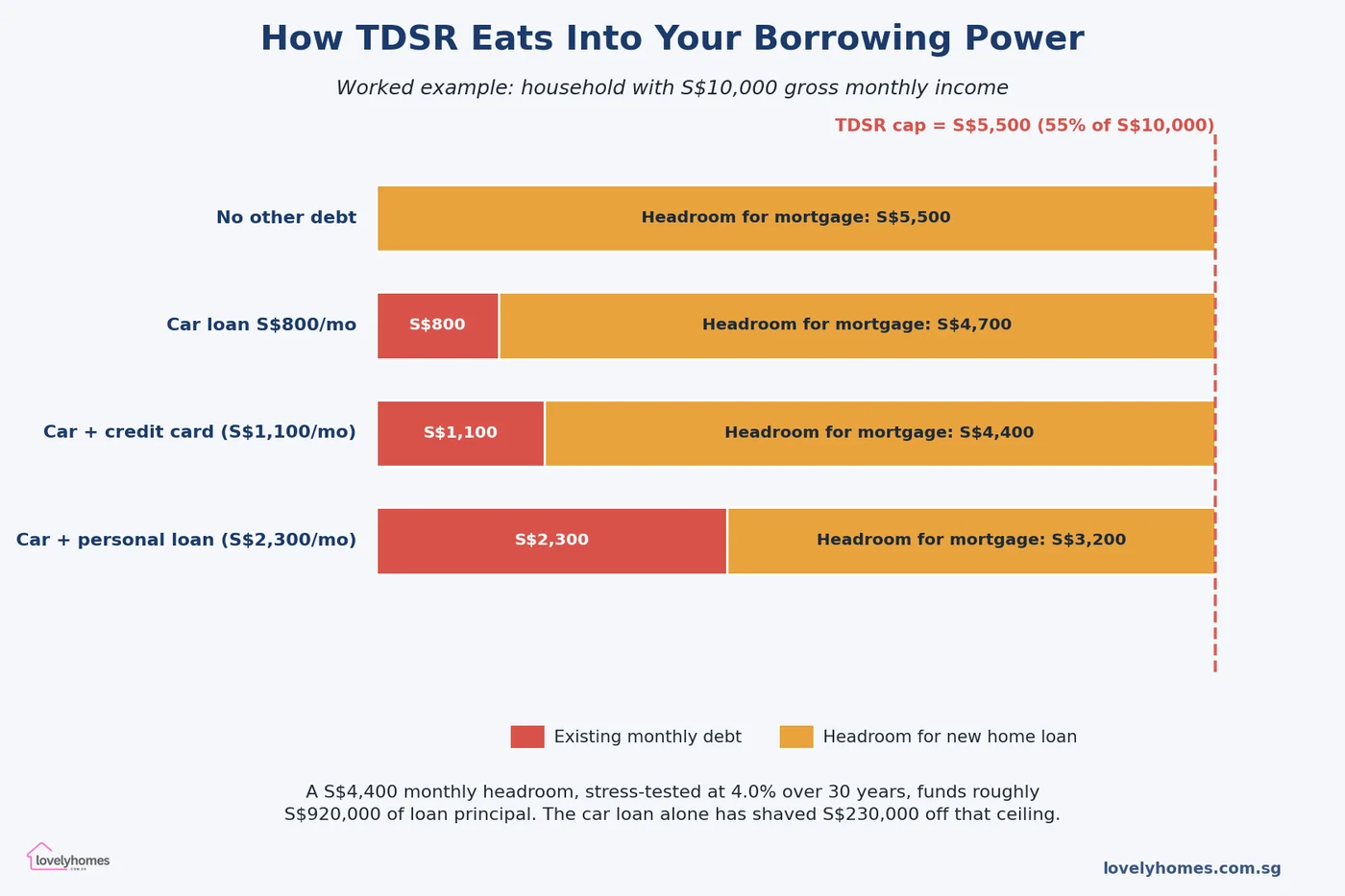

A Fully-Worked Example: A S$10,000-a-Month Household Buying a Private Condo

Figure 3: How different existing-debt profiles crater the monthly headroom available for a new mortgage, given a household earning S$10,000 gross.

Consider a dual-income couple: combined gross monthly salary S$10,000, both on fixed pay, no variable component. They are looking at a S$1.8 million resale private condo in District 15.

Step 1 — TDSR cap. 55% × S$10,000 = S$5,500. No MSR applies because this is a private condo.

Step 2 — Existing debts. One car loan at S$800/month and revolving credit balances generating a S$300/month minimum payment. Total existing obligations: S$1,100.

Step 3 — Headroom for the new mortgage. S$5,500 − S$1,100 = S$4,400 per month available for the new home loan instalment.

Step 4 — Maximum loan principal. At the 4.0% stress rate over a 30-year tenure, S$4,400 monthly funds approximately S$922,000 of loan principal (standard amortisation formula: P = M × [(1 − (1 + r)^(−n)) / r]).

Step 5 — LTV cap. At 75% LTV on an S$1.8m purchase, the bank could lend up to S$1,350,000 — but TDSR limits them to S$922,000 here, so TDSR binds, not LTV. The couple needs S$878,000 of combined cash and CPF equity.

Flip the same household to an HDB flat at S$700,000: now MSR binds first. 30% × S$10,000 = S$3,000 maximum mortgage instalment. That fundamentally funds roughly S$628,000 — well below the 75% LTV ceiling of S$525,000… wait. In this case the 75% LTV actually binds below MSR, because S$525,000 of loan needs only about S$2,500/month at 4.0% over 25 years, comfortably inside MSR. So the couple’s CPF-plus-cash needs to fill the remaining S$175,000.

These two scenarios show the recurring pattern: for HDB/EC buyers, MSR or LTV usually binds; for private/landed buyers, TDSR usually binds. The flow of the calculation matters, and every added dollar of existing debt has a disproportionate impact through the 30-year amortisation lever.

How to Legitimately Maximise Your Borrowing Ceiling

Nothing below involves gaming the system — each lever is recognised by banks and MAS. Together they can add S$200,000–S$400,000 to a buyer’s loan ceiling.

Close dormant credit facilities. A S$50,000 unused overdraft or a clutch of credit cards still hits TDSR via the 3% minimum rule. A week of admin before you apply for pre-approval can move the needle.

Pay down the car loan. High-instalment vehicle finance is the single most common TDSR killer. A S$1,000 monthly car note costs you roughly S$210,000 of home-loan capacity at 4.0%/30yr.

Lengthen the tenure (cautiously). A 30-year tenure beats a 25-year one on headline TDSR because the stress-rate instalment is lower — but watch the age-65 and 30-year triggers that knock the LTV down 20 points.

Co-apply with a higher earner. Joint applications aggregate income and debt. If spouses have different debt loads, consider which combination maximises the pooled headroom.

Formalise variable income. A commissioned sales professional with one year of written contracts may be haircut more heavily than one with two years of NOAs. Waiting one tax cycle can unlock meaningful capacity.

Use a Loan Assessment before committing. Banks in Singapore offer in-principle approval (IPA) at no cost. Three IPAs from different banks let you benchmark the figure.

How Singapore’s Framework Compares Globally

Singapore is not alone in prescribing debt-service ratios, but its combination is unusually strict. Hong Kong applies a 50% debt-service ratio with a 70% LTV cap for first-time owner-occupiers — broadly comparable but no separate MSR for public housing. The United Kingdom uses a 4.5× income loan-to-income ratio at most lenders (soft cap), with affordability stress-tested at 3 percentage points over the reversion rate. Australia’s prudential regulator APRA applies a serviceability buffer of 3 percentage points over the contracted rate — a rule-of-thumb approach rather than a hard ratio.

The common thread in all four jurisdictions is a stress-test mechanism designed to withstand a rate spike. Singapore’s 4.0% medium-term rate is higher (more conservative) than the contracted-rate buffers used in the UK and Australia, which is one reason Singaporean household debt has been more resilient through recent cycles than peers. MAS has been explicit that this is by design: household leverage is viewed as a systemic risk, not purely a consumer-protection issue.

What Might Come Next — The Forward View

The 4.0% stress rate has held since September 2022. Three scenarios could prompt a revision in the next 12–18 months:

Sustained higher long-term rates. If three-month SORA settles above 3.5% on a durable basis, MAS may nudge the medium-term rate to 4.25% or 4.5% to preserve the buffer it represents.

Renewed leverage in the private condo segment. If luxury-segment TDSR headroom is being used aggressively to bid up prime-district prices, expect tighter LTV on second/third loans rather than a TDSR change.

Public housing affordability stress. If HDB resale prices outrun wage growth materially, MSR could tighten from 30% to 25%. This would be the single most consequential move for first-time buyers.

None of the above is signalled by MAS at the time of writing (April 2026) — but the Financial Stability Review due in November 2026 is the data release to watch. Historically MAS has adjusted TDSR and MSR in the December statement that accompanies the cooling-measures package.

Frequently Asked Questions

1. Does TDSR apply to refinancing my existing mortgage?

For owner-occupied properties, a clean refinance without any cash-out and without extending the principal is generally exempted from TDSR under a carve-out MAS introduced to avoid penalising existing borrowers. If you take a cash-out top-up or increase the principal, the full TDSR test applies. For investment-property refinancing, TDSR applies in full regardless of cash-out status, so build in a review of your current debt profile before signing any refinance Letter of Offer.

2. How is TDSR calculated if I am self-employed with irregular income?

Banks use two years of Notice of Assessment (NOA) as the primary evidentiary source, take the simple average, apply the 30% haircut, and treat the resulting figure as your recognised gross monthly income. A particularly strong year — say a bumper bonus — will be smoothed. If you have less than two years of NOAs the bank will often decline or require a significantly larger down-payment. Incorporating yourself through a Pte Ltd does not change this; director’s remuneration drawn as salary is still subject to the haircut.

3. Can I borrow more by stretching the loan tenure?

Up to a point, yes. A 30-year tenure reduces the stress-rate instalment versus a 25-year tenure, increasing how much loan principal S$4,400 (in our worked example) can support. But two triggers cap the benefit: if your loan extends past age 65 or exceeds 30 years (25 for HDB), the LTV cap drops by 20 percentage points — from 75% to 55% on a first loan. The net effect is usually worse, not better. Most brokers recommend landing the tenure such that the loan concludes at or just before age 65.

4. Are joint-borrower applications better than going solo?

Usually, because they aggregate income while both parties still share the TDSR ceiling. The nuance is “income-weighted average age” for tenure calculations — if a 55-year-old and a 35-year-old co-apply, the bank blends their ages by income share to determine the maximum allowable tenure. Adding a much older co-applicant to a younger borrower can shorten the tenure and reduce the headroom on paper. Structured correctly, joint applications reliably produce higher approvals than solo for dual-income households.

5. What happens to TDSR if interest rates fall sharply?

Nothing, in the short run. The 4.0% stress rate is a regulatory input, not a market rate. Falling SORA means your actual monthly instalment shrinks and your actual debt-service ratio improves, but the ceiling at which MAS sets the TDSR bar is unchanged. Over a multi-year horizon, if rates settle well below 4.0% on a sustained basis, MAS may consider lowering the stress rate — but the precedent is that adjustments are infrequent (the last move was September 2022).

6. Does CPF Ordinary Account balance count as income for TDSR?

No. CPF OA is treated as equity (part of the down-payment and subsequent instalments), not as income. The monthly CPF contribution inflow also does not count as additional income — your CPF contributions are already a reduction from your gross pay, and gross pay is what banks use. The only way CPF affects borrowing capacity indirectly is through the Home Protection Scheme (for HDB loans) and through the cash-CPF split in the down-payment.

7. I was denied because of TDSR — what are my options?

First, get the denial reasoning in writing and compare it with a second IPA at a different bank — underwriting interpretations vary on edge cases, particularly around variable income and guarantor obligations. Second, tackle the debt side: clear a car loan, consolidate or close credit cards, discharge a guarantor role. Third, stretch the timeline: a fresh NOA next April may unlock the variable-income shortfall. Fourth, reduce the target property price — a 10% lower purchase price typically requires a proportionally smaller loan and therefore a smaller headroom. Finally, consider a joint application with a fixed-income parent (though this binds their future TDSR too).

This article is an editorial guide for general information only and does not constitute financial, legal or mortgage advice. The figures quoted reflect rules in force on the date of publication (April 2026) and may change. Confirm the authoritative position with the Monetary Authority of Singapore (MAS), the Housing & Development Board (HDB), your bank’s credit officer and a licensed mortgage broker before committing to any loan or property purchase. Interest-rate scenarios and worked examples are illustrative; your actual borrowing ceiling depends on the full underwriting review at application.

Wait-Out Period: Private property owners must wait 15 months before buying HDB resale without grant.

What are Singapore’s Property Cooling Measures?

Singapore’s property cooling measures are a suite of policy tools designed to moderate demand, curb speculation, and ensure housing remains affordable. They exist because rapid property price growth can outpace wage growth, lock first-time buyers out of the market, and create unsustainable bubbles. Four key agencies administer these measures: the Monetary Authority of Singapore (MAS), the Urban Redevelopment Authority (URA), the Inland Revenue Authority of Singapore (IRAS), and the Housing and Development Board (HDB). Together, they apply tools such as stamp duties, loan limits, affordability tests, and holding periods to regulate the market and protect both buyers and the broader economy.

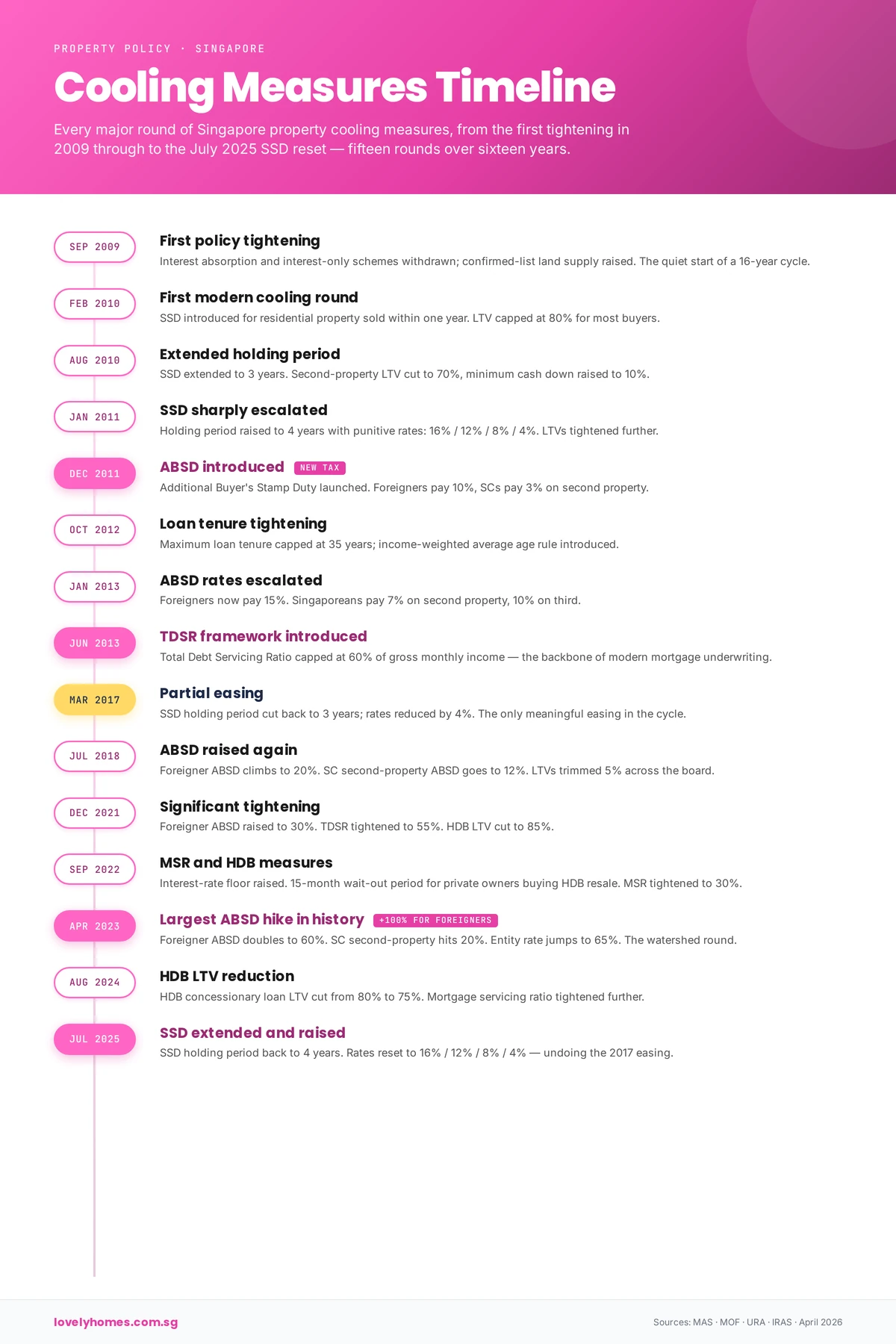

Figure 1: The 15 major rounds of Singapore property cooling measures, 2009–2026.

September 2009: The First Policy Tightening

Before the modern cooling era, the government moved to restrict lending practices. In September 2009, the Monetary Authority of Singapore (MAS) disallowed two risky loan products: the Interest Absorption Scheme (IAS) and Interest-Only Housing Loans (IOL). These products had allowed borrowers to defer principal repayment during the early years of a mortgage, increasing default risk during rate rises. By banning them, the government signalled a preference for prudent, full-amortising loans and set the stage for the more comprehensive cooling measures that would follow.

February 2010: The First Modern Cooling Round

On 20 February 2010, Singapore introduced its first comprehensive cooling package, reflecting rapid price growth and surging demand. The government introduced two major tools:

Seller’s Stamp Duty (SSD): Properties sold within one year were hit with a 3% SSD. The intent was to discourage “flipping”—rapid resale for short-term gain.

Loan-to-Value (LTV) limit: Reduced from 90% to 80%, requiring buyers to put down at least 20%. This reduced lender exposure and made buyers more cautious.

These measures reflected a key insight: when buyers can leverage heavily and exit quickly, prices can spiral. By raising the entry cost and the holding cost, the government aimed to attract only genuine buyers.

August 2010: Extended Holding Period

By mid-2010, demand remained strong. On 19 August 2010, the government extended the SSD holding period from 1 year to 3 years, raising the cost of short-term resale. For those with existing loans, the LTV limit tightened further to 70%, and cash downpayment requirements rose, particularly hurting leveraged investors.

January 2011: Sharp SSD Escalation

Recognising that the market was still overheating, the government on 8 January 2011 escalated the SSD significantly. The new structure was:

Year 1: 16%

Year 2: 12%

Year 3: 8%

Year 4: 4%

The rationale was unmistakable: hold for less than a year and lose a sixth of your sale price. LTV limits were also tightened to 60% for those with existing loans, making it much harder for property investors to string together multiple mortgages.

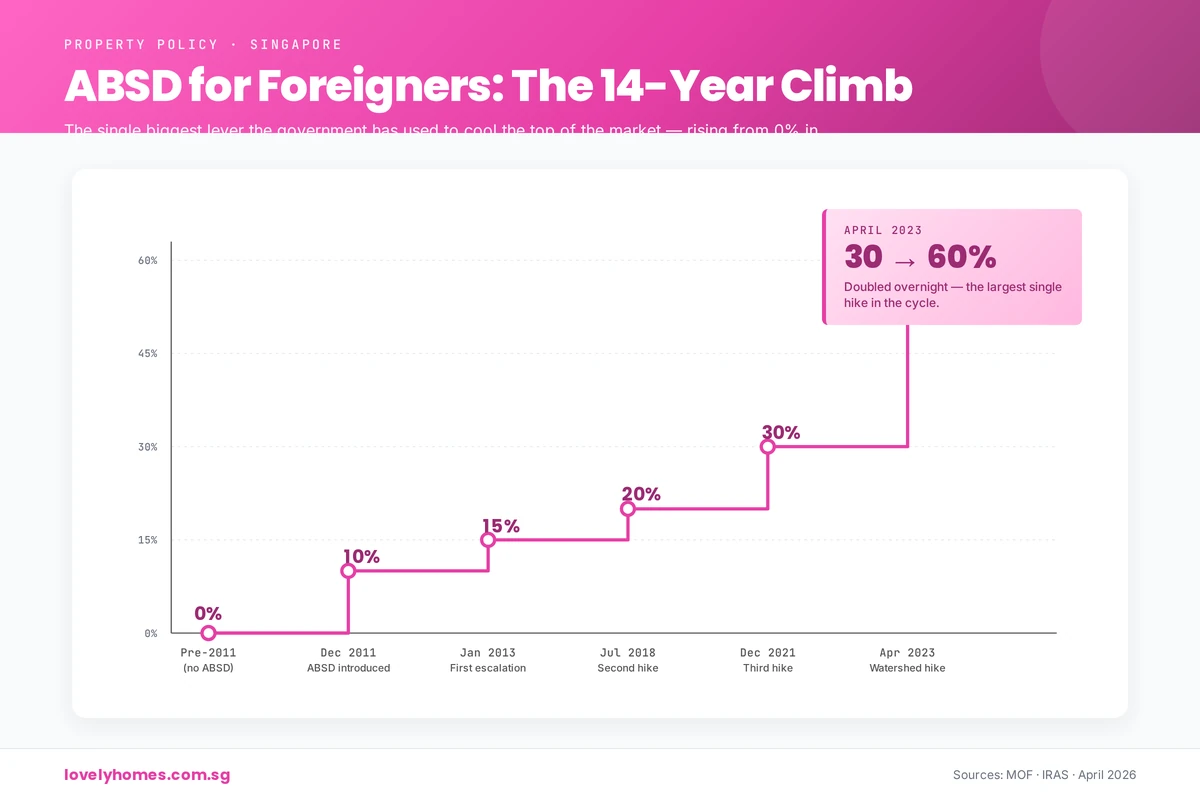

December 2011: ABSD Introduced

On 8 December 2011, Singapore introduced the Additional Buyer’s Stamp Duty (ABSD), its most powerful tool. ABSD was a second layer of stamp duty on top of the normal Buyer’s Stamp Duty (BSD), calibrated to buyer type:

Singapore Citizens buying a 2nd+ property: 3%

Singapore Citizens buying a 3rd+ property: 3%

Permanent Residents buying a 2nd+ property: 3%

Foreigners: 10%

Corporate entities: 10%

ABSD was revolutionary because it directly attacked investment demand, particularly from overseas. It signalled that Singapore prioritised homeownership for citizens over investment returns for outsiders.

October 2012: Loan Tenure Tightening

The Monetary Authority of Singapore further tightened lending on 19 October 2012. The maximum loan tenure was capped at 35 years, with a penalty: if LTV remained above 60% after 30 years, the LTV would be capped at 40% in year 31 onwards. This forced borrowers to repay principal faster, reducing their borrowing power and making loans less attractive.

January 2013: ABSD Escalation

On 11 January 2013, the government raised ABSD across the board:

Singapore Citizens (2nd property): 7%

Singapore Citizens (3rd+ property): 10%

Permanent Residents (2nd+ property): 10%

Foreigners: 15%

Entities: 15%

The hike reflected continued demand, particularly from foreign investors and corporate buyers. Cash downpayment requirements also rose, targeting multiple-property owners and entities.

June 2013: TDSR Framework Introduced

On 28 June 2013, the Monetary Authority of Singapore introduced the Total Debt Servicing Ratio (TDSR) framework. TDSR capped total monthly debt repayments (mortgage, car loan, credit cards, personal loans, etc.) at 60% of gross monthly income. The intention was to prevent over-leverage: even if house prices were rising, a banker couldn’t lend to someone whose entire income was going to debt service.

This was a game-changer because it wasn’t about house prices directly—it was about borrower health. It also forced banks to stress-test loans, assuming interest rates would rise, to ensure borrowers could survive a shock.

March 2017: Partial Easing

By 2016–2017, prices had stabilised and growth had slowed. On 5 March 2017, the government eased some measures:

SSD holding period reduced from 4 years to 3 years, though rates remained steep (12%/8%/4% for years 1–3).

TDSR and ABSD eased slightly for refinancing.

This signalled a shift: the government was confident the market was no longer overheating and could afford marginal relief.

July 2018: ABSD Raised Again

By mid-2018, there were signs of renewed speculative interest, particularly from foreign and corporate buyers. On 6 July 2018, the government raised ABSD sharply:

LTV limits also tightened by 5 percentage points across all categories, making down payments larger and borrowing power lower.

December 2021: Significant Tightening

After years of near-zero interest rates post-COVID, demand surged again. On 16 December 2021, the government announced a comprehensive tightening:

ABSD raised again: foreigners to 30%; entities to 35%; PR 2nd property to 20%.

TDSR tightened from 60% to 55% of gross monthly income.

Interest-rate floor for TDSR/MSR calculations raised to 3.5% for private bank loans (previously 3%).

HDB LTV limits reduced across the board.

This was a significant hardening, reflecting real concern about affordability following three years of price growth.

September 2022: MSR and HDB Measures

On 30 September 2022, the government introduced new measures targeting the HDB resale market, where first-time buyers (and upgraders) primarily shop:

Mortgage Servicing Ratio (MSR) introduced: For HDB and Executive Condominium (EC) loans, monthly mortgage payments cannot exceed 30% of gross income—stricter than TDSR’s 55%.

15-month wait-out period: Private property owners must wait 15 months after selling before buying an HDB resale flat, curbing investor demand for subsidised public housing.

Interest-rate floor for TDSR/MSR raised from 3% to 3.5% for private loans; 3% for HDB loans.

These moves directly sheltered first-time HDB buyers from investor competition.

Figure 3: Foreigner ABSD climbed from 0% in 2011 to 60% in April 2023 — the largest single hike in the cycle.

April 2023: Largest ABSD Hike in History

On 27 April 2023, faced with renewed price acceleration in Q1 2023 (especially among owner-occupiers), the government announced its largest ABSD increase:

This was the most aggressive escalation since ABSD’s introduction, reflecting the government’s determination to prioritise homeownership for citizens and slow speculation. A foreign buyer purchasing a S$2 million condo now faced S$1.2 million in ABSD—an enormous barrier.

August 2024: HDB LTV Reduction

On 20 August 2024, the government reduced the Loan-to-Value (LTV) limit for HDB-granted housing loans from 80% to 75%. This meant HDB buyers now needed a 25% down payment instead of 20%, directly reducing borrowing power for this segment. Concurrently, higher CPF Housing Grants were introduced for first-time buyers to offset the impact, retaining affordability.

July 2025: SSD Extended and Raised

On 3 July 2025, the government responded to a spike in “flipping”—buyers purchasing uncompleted units (off-plan) and reselling before completion or soon after. The SSD holding period was extended from 3 years to 4 years, and rates were raised across the board by 4 percentage points:

Year 1: 20% (from 16%)

Year 2: 16% (from 12%)

Year 3: 12% (from 8%)

Year 4: 8% (from 4%)

This further discouraged short-term speculation while allowing long-term owners to exit penalty-free after four years.

Current Cooling Measures Framework (April 2026)

The current cooling-measures framework, established by the 27 April 2023 ABSD hike and subsequently adjusted by the 20 August 2024 HDB LTV reduction and the 4 July 2025 SSD restructure, remains in force as at April 2026. MAS, MND, URA and HDB jointly review the framework regularly and have repeatedly indicated they will recalibrate the measures — either tightening or easing — in response to market conditions.

Figure 2: The four core cooling tools — taxes (ABSD, SSD), loan limits (LTV) and debt ratios (TDSR) working in concert.

Let’s illustrate the impact with a hypothetical Singapore Citizen (SC) buying a second property valued at S$2 million:

Year

ABSD Rate

ABSD Cost (S$)

BSD + ABSD Total

2010 (Feb)

0%

S$0

~S$20,000 (BSD only)

2013 (Jan)

7%

S$140,000

~S$160,000

2018 (July)

7%

S$140,000

~S$160,000

2023 (April)

20%

S$400,000

~S$420,000

2026 (April)

20%

S$400,000

~S$420,000

Notice the leap from 2013 to 2023: the cost of buying a second home more than doubled in stamp duty alone, while the property value remained constant. This is the direct impact of cooling measures: they make property ownership more expensive, not by changing the property itself, but by raising friction and entry costs.

Why Have Cooling Measures Worked?

Singapore’s housing market has not crashed, despite aggressive cooling measures—a fact some cite as evidence of failure. But that misses the point. Cooling measures are designed to slow, not stop, price growth; to reduce speculation, not eliminate it; and to align prices with incomes, not freeze them.

Consider the evidence:

Slower growth: Private residential property annual price gains have typically stayed in the 2–5% range post-2013, compared to double-digit growth in the early 2010s. This moderation reflects a market rebalancing, where price appreciation has settled into a more sustainable trajectory aligned with economic fundamentals such as wage growth and rental yields.

Affordability preserved: First-time buyers, particularly HDB upgraders, have continued to buy; median house prices have not become so extreme relative to median incomes that the market has fractured. The price-to-income ratio in Singapore remains among the most manageable in developed Asia, allowing younger buyers to enter the market without undue hardship.

Comparison to global peers: Hong Kong, Vancouver, and Sydney have seen much steeper price-to-income ratios despite less stringent cooling measures. In Hong Kong, for example, a property may cost 20–30 times annual median household income; in Vancouver and Sydney, the ratio exceeds 12–15. Singapore’s pragmatic approach has kept the ratio at a more sustainable 8–10 times, making the market more accessible.

Investor activity moderated: The share of property transactions by investors (vs. owner-occupiers) has declined, indicating cooling measures are successfully crowding out speculative demand. This shift is crucial: when investors withdraw, price volatility typically decreases and stability improves.

Market resilience: The market has absorbed multiple rounds of tightening—seven major cooling packages since 2009—without experiencing a crash. This speaks to the underlying strength of Singapore’s economy and the government’s ability to calibrate policy precisely, neither so tight as to stifle the market nor so loose as to permit excess.

In short, cooling measures have succeeded in their core mission: managed, sustainable growth that preserves homeownership as an achievable goal for Singaporeans whilst safeguarding financial stability.

What Might Come Next?

Predicting future cooling measures is speculative, but several potential levers exist if the market overheats again. The government has shown it is willing to adjust policy swiftly when conditions warrant, and the following measures are within the realm of possibility:

Further LTV tightening: LTV could drop below 75% for HDB and 70% for private, forcing larger down payments. This would particularly affect HDB first-time buyers, though offsetting grants could mitigate the impact.

ABSD escalation on entities: Corporate and foreign entity purchases could face rates exceeding 70%, further discouraging institutional investors and offshore funds from treating Singapore residential property as an alternative asset class.

TDSR reduction: The 55% threshold could tighten to 50%, limiting borrowing power even further. This would reduce the quantum of debt banks could extend and force buyers to increase down payments or reduce property search prices.

Extended hold periods: SSD holding could extend beyond four years; MSR wait-out could lengthen beyond 15 months. A 5–7 year SSD period would effectively end short-to-medium-term flipping as an investment strategy.

Targeted HDB measures: Given HDB’s social mission, the government could ring-fence HDB buying further (e.g., longer wait-out periods for private owners, stricter owner-occupancy rules for upgrade purchases).

Differentiated ABSD by property type: Separate ABSD rates for landed (houses, land) vs. non-landed (condos, ECs) to focus cooling where prices are most extreme. Landed property prices have historically appreciated faster than condominiums, making them a natural target for stricter cooling.

Interest-rate floor adjustments: The MAS could raise the notional interest-rate floor used in TDSR/MSR calculations from the current 4% (private) to 4.5% or 5%, making loans seem more expensive during qualification, thereby reducing lending volumes.

These possibilities are illustrative, not predictions. The Government has consistently emphasised that cooling measures are reviewed against prevailing market conditions, and that any further recalibration — tightening or easing — will be driven by the data. Buyers and sellers should plan on the framework in force today and monitor MAS, URA, MND, IRAS and HDB announcements for updates.

Frequently Asked Questions

1. What’s the difference between ABSD and SSD?

ABSD (Additional Buyer’s Stamp Duty) is a tax paid by the buyer when purchasing a property (typically 2nd or 3rd+). It’s calibrated by buyer type (citizen, PR, foreigner, entity) and aims to dampen investment demand. SSD (Seller’s Stamp Duty) is a tax paid by the seller when selling within a holding period; it discourages flipping. Both reduce demand, but ABSD targets entry; SSD targets exit.

2. Are cooling measures permanent?

No. All cooling measures are policy tools, not constitutional laws. They can be eased or tightened depending on market conditions. For example, SSD was partially eased in March 2017, and TDSR has been adjusted twice (60% → 55%). The Government reviews the framework regularly against market conditions.

3. Can you appeal a cooling-measure penalty (e.g., SSD)?

No. Cooling measures are statutory levies applied uniformly. Once a property is sold within the SSD holding period, the duty is automatically calculated and due. There is no appeal mechanism, though you can seek professional tax advice if you believe your classification is incorrect. Early repayment of SSD (before expiry) is not available.

4. How do cooling measures affect HDB owners?

Cooling measures affect HDB owners primarily when upgrading (selling to buy private) or downgrading (selling private to buy HDB resale). HDB owners upgrading to private face ABSD. Private owners downgrading to HDB resale face a 15-month wait-out period and stricter MSR limits (30% vs. TDSR 55%). Cooling measures have also reduced HDB LTV to 75%, requiring larger down payments.

5. Do foreigners face the toughest measures?

Yes, unambiguously. Foreigners pay 60% ABSD (vs. 20% for SC 2nd property), and are excluded from some HDB categories altogether. The government’s policy framework explicitly prioritises owner-occupation for citizens and PRs over foreign investment. A foreigner buying a S$2M property pays S$1.2M in ABSD alone, making foreign residential investment significantly less attractive.

6. Will the government remove cooling measures if the market drops?

Possibly, but history suggests a “last in, first out” approach. When prices fell during COVID-19, cooling measures were retained (some were even tightened). The government views cooling measures as structural policy, not cyclical. However, if prices fell sharply and sustained (e.g., 15% decline year-on-year), measures like ABSD could be eased to stimulate demand. The government’s current stance (April 2026) is that stabilisation is preferable to rollback, unless emergency conditions warrant it.

This guide is for general information only and does not constitute legal, tax, or financial advice. Cooling measures are subject to change at any time by the relevant authorities (MAS, URA, IRAS, HDB). Interest rates, property values, and policy frameworks are subject to modification. Before entering into any property transaction, verify the current ABSD rates, SSD holding periods, LTV limits, TDSR/MSR thresholds, and any other applicable cooling measures with the Inland Revenue Authority of Singapore (IRAS), the Housing and Development Board (HDB), or the Monetary Authority of Singapore (MAS). Consult a licensed conveyancing lawyer and a qualified mortgage specialist or financial adviser to assess your personal circumstances and borrowing capacity. LovelyHomes.com.sg takes no responsibility for losses or liabilities arising from reliance on this article.