HDB Resale Flat Eligibility Singapore 2026: Who Can Buy, Citizenship Rules and How to Qualify

HDB Resale Flat Eligibility Singapore 2026: Who Can Buy, Citizenship Rules and How to Qualify

Quick Answer

- No income ceiling to purchase an HDB resale flat — income caps apply only to the HDB Concessionary Loan (≤ S$14,000/month for families; ≤ S$7,000 for singles) and to grants such as the EHG (≤ S$9,000/month).

- Singapore Citizens may buy under the Public Scheme, Singles Scheme (35+), Joint Singles, Fiancé/Fiancée, Non-Citizen Spouse or Orphans Scheme depending on their household composition.

- Singapore PRs must have held PR status for at least 3 continuous years and must form a valid family nucleus. PR singles cannot buy HDB resale.

- Foreigners and non-PRs are not eligible under any HDB resale purchase scheme.

- Private property owners are subject to a 30-month wait-out period (introduced 30 September 2022) after disposing of their private property before they may buy a resale HDB flat. Exception: Singapore Citizens aged 55 and above buying a 4-room or smaller flat.

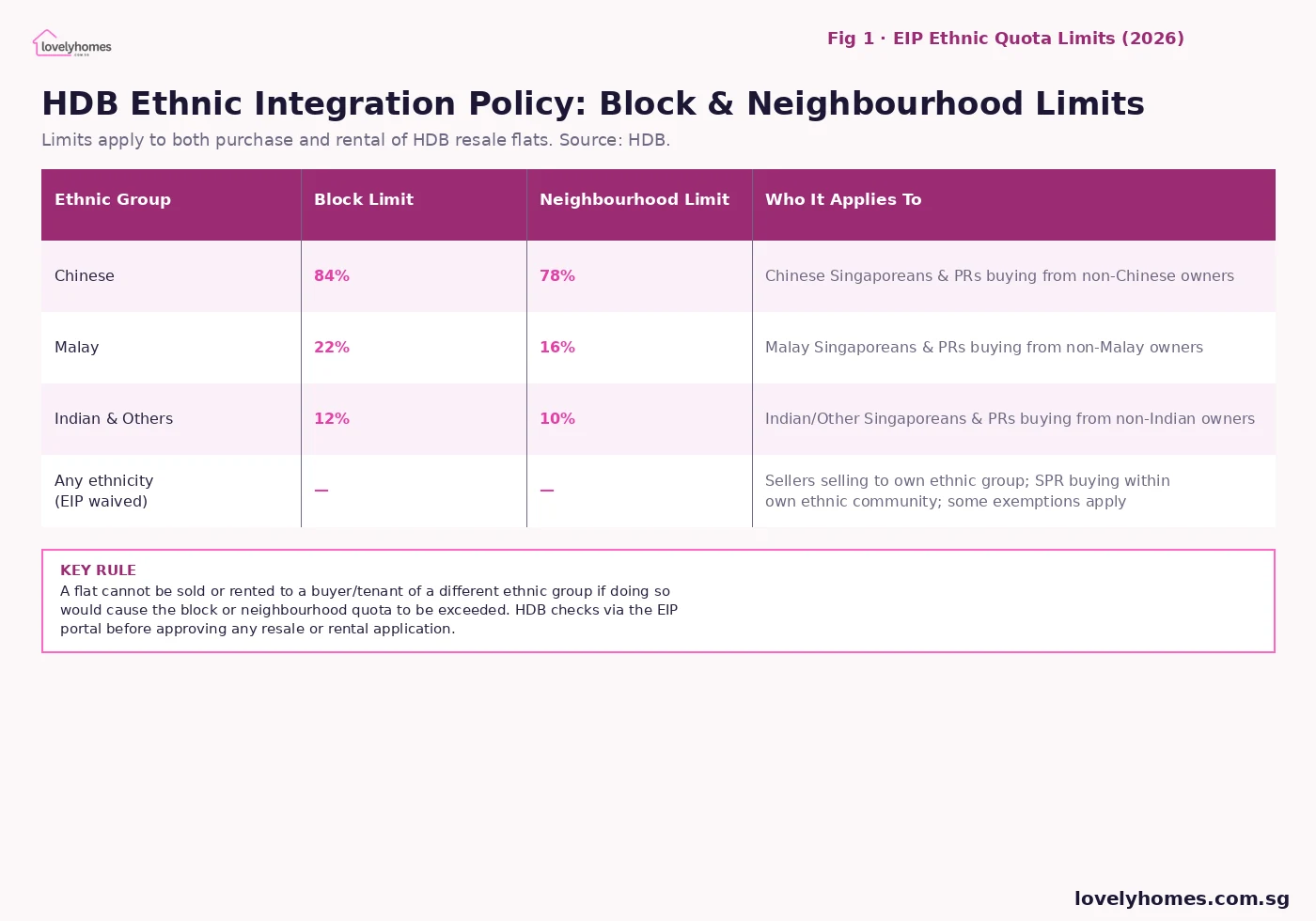

- EIP quotas apply to all resale purchases — available units depend on the ethnic composition of the block and neighbourhood (see our HDB Ethnic Integration Policy guide).

- Eligibility is determined at the date of HDB application, not the Option to Purchase date.

What Is HDB Resale Flat Eligibility?

HDB resale flat eligibility refers to the set of rules administered by the Housing and Development Board (HDB) that determine who may purchase a resale flat on the open market in Singapore. Unlike Build-To-Order (BTO) flats, which are sold directly by HDB at subsidised prices, resale flats are transacted between a seller and a buyer at market prices. The resale market is open to a broader range of buyers than the BTO programme — including Singapore PRs — but it still operates within a strict framework of nationality, household composition, age, and ownership rules.

Understanding eligibility is the essential first step before placing an Option to Purchase (OTP). Submitting an HDB application for a flat you are not eligible to buy will result in rejection and the forfeiture of the OTP exercise fee (typically 1% of the purchase price). Eligibility is confirmed at the point of HDB application, so it is important that you qualify on the date you submit — not just on the date you sign the OTP.

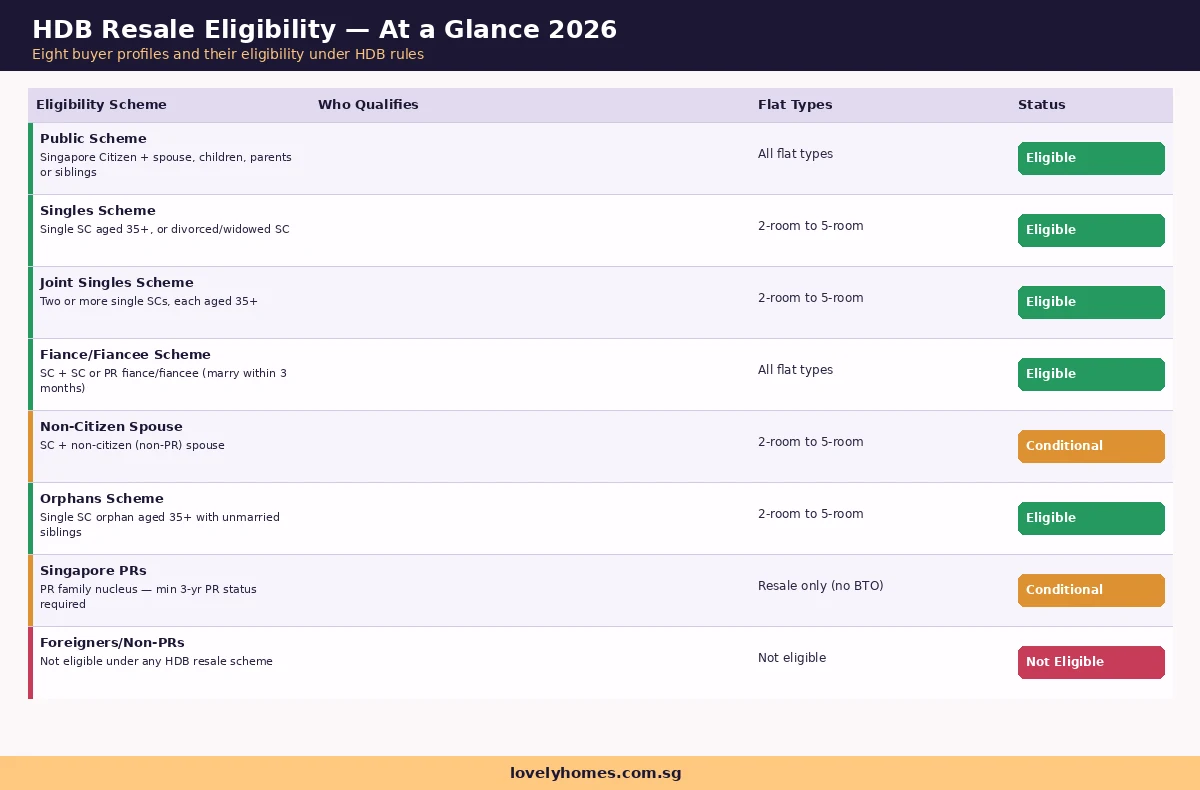

The Eight Eligibility Schemes at a Glance

HDB administers eight distinct eligibility schemes for resale flat purchases. Each scheme defines who may be listed as an essential occupier or co-applicant. The table below summarises all eight.

Singapore Citizens: Eligibility Schemes in Detail

Singapore Citizens (SCs) have the broadest access to the HDB resale market. Most SC buyers will purchase under the Public Scheme, which requires at least one SC applicant forming a family nucleus with a spouse (SC, PR or foreigner on a long-term pass), children, parents, or unmarried siblings. There is no age restriction under the Public Scheme beyond the minimum legal age of 21.

For singles, the Singles Scheme allows an unmarried, divorced, or widowed SC aged 35 and above to purchase a resale flat of any room type (2-room to 5-room) independently. Two or more single SCs who each meet the age criterion may combine under the Joint Singles Scheme to co-purchase a flat — this is particularly useful for siblings or friends who wish to buy together before meeting eligibility under the Public Scheme.

Other SC-specific schemes include the Fiancé/Fiancée Scheme (for couples who will marry within three months of the HDB application) and the Non-Citizen Spouse Scheme (for SCs whose spouses hold neither SC nor PR status but are on a long-term Singapore pass). Under the Non-Citizen Spouse Scheme, the flat is restricted to 2-room through 5-room types. The Orphans Scheme enables a single SC who has lost both parents and is at least 35 years old to purchase a resale flat, listing unmarried siblings as essential occupiers.

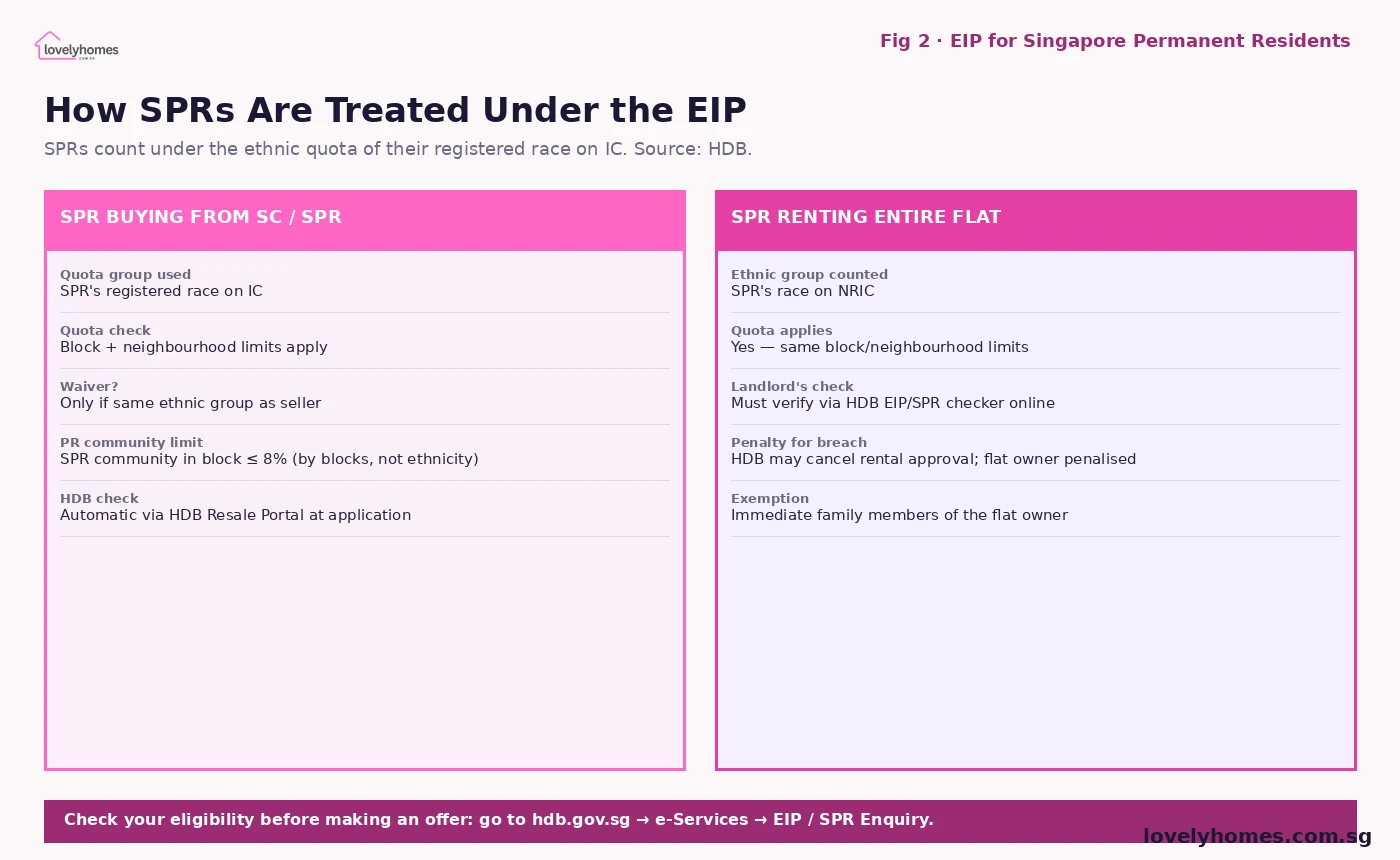

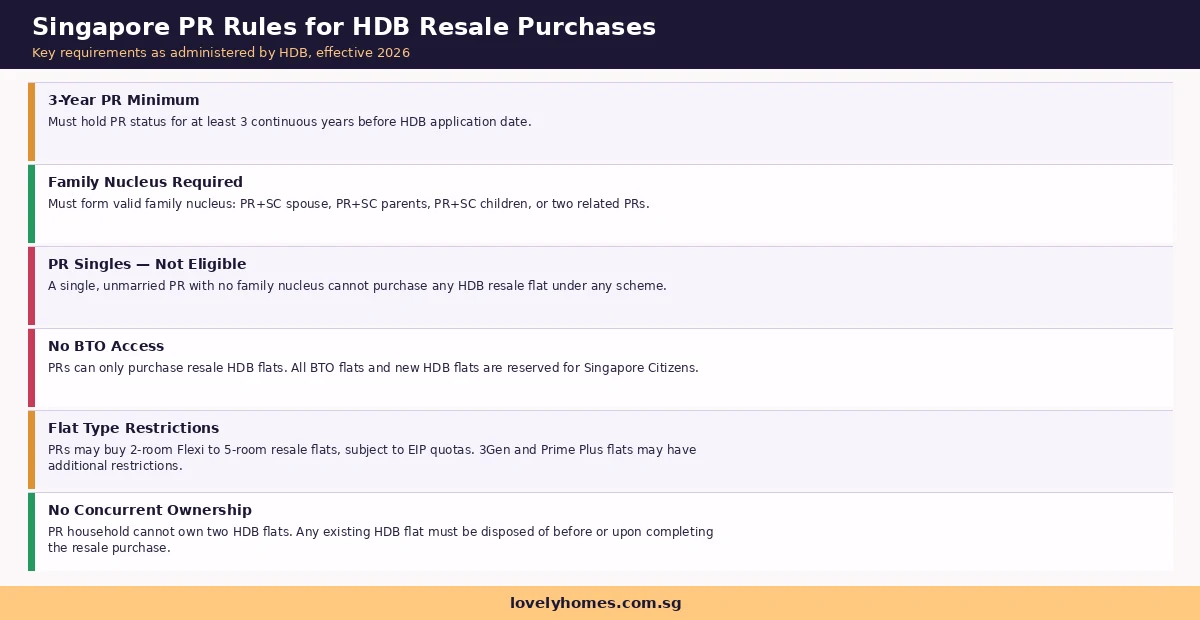

Singapore Permanent Residents: What You Need to Know

Singapore PRs can purchase HDB resale flats — but with important restrictions that do not apply to SCs. The key rules are summarised in the infographic below.

The most significant PR restriction is the 3-year minimum: every PR applicant (and co-applicant) must have held PR status for at least three continuous years before submitting the HDB application. This clock starts from the date on the PR In-Principle Approval (IPA) letter, not the date of collection of the NRIC. A couple where both spouses obtained PR status in January 2023 would not be eligible to buy a resale HDB flat until January 2026 at the earliest.

PRs must also form a valid family nucleus. A PR may co-purchase with an SC spouse, SC parents, SC children, or another PR who is a spouse or parent. Critically, PR singles cannot buy HDB resale — there is no singles or joint-singles scheme equivalent for PRs. A single, unmarried PR has no pathway to HDB ownership and must rent or purchase private property instead.

PRs are also limited to the resale market. BTO flats, new HDB flats sold under the Sale of Balance Flats (SBF) exercise, and EC projects during their initial launch window are reserved for SCs only (ECs become available to PRs only after they pass their 5-year Minimum Occupation Period). Additionally, PR households cannot own a private residential property simultaneously with an HDB resale flat — they must dispose of their private property within six months of completing the HDB resale purchase.

Foreigners and Non-Residents

Non-citizens who are not PRs are generally not eligible to purchase any HDB flat — resale or new. This includes foreigners on Employment Passes, Dependant Passes, Student Passes, and Long-Term Visit Passes. The only limited exception is the Non-Citizen Spouse Scheme, which allows an SC to co-purchase with a foreign spouse (not holding PR status) — but the SC must be the sole applicant and the flat is restricted to 2-room through 5-room resale types. The foreign spouse is listed as an essential occupier, not a co-owner, and cannot hold legal title to the flat.

Key Disqualifications and the 30-Month Private Property Wait-Out

Even if you meet the citizenship and household composition requirements, you may be disqualified from buying an HDB resale flat if certain ownership or financial conditions apply. The most significant disqualification to understand in 2026 is the 30-month private property wait-out period, which was introduced as part of the September 2022 cooling measures.

The 30-month wait-out period means that if you or any listed occupier have disposed of a private residential property (local or overseas), you must wait 30 months from the date of disposal before you can apply for a resale HDB flat. This rule was specifically designed to prevent buyers from “downgrading” to a subsidised HDB flat while pocketing private property gains. The exception is for Singapore Citizens aged 55 and above buying a 4-room or smaller resale flat — they are exempt from the 30-month wait-out entirely, recognising that downsizing in retirement is a legitimate and healthy housing progression.

Summary Table: HDB Resale Eligibility at a Glance

| Buyer Profile | Min Age | Family Nucleus | Flat Types | Key Restrictions |

|---|---|---|---|---|

| SC (Public Scheme) | 21 | Required | All types | EIP quotas apply |

| SC (Singles Scheme) | 35 | Not required | 2–5 room | Single, divorced or widowed |

| SC (Joint Singles) | 35 each | Co-purchasers | 2–5 room | All co-purchasers must be SC |

| SC (Non-Citizen Spouse) | 21 | SC applicant only | 2–5 room | Spouse is occupier, not co-owner |

| Singapore PR | 21 | Required | 2–5 room | 3-yr PR minimum; no BTO |

| PR Single | — | — | Not eligible | No HDB scheme available |

| Foreigner / Non-PR | — | — | Not eligible | No HDB scheme available |

Worked Example: Divorced SC Buying Under the Singles Scheme

Scenario. Ms Tan Wei Ling, 39, is a Singapore Citizen who divorced in 2023. She has one child, aged 9. She sold her former matrimonial HDB flat as part of the divorce settlement in early 2023. She has not owned any private property. She earns S$6,800 per month and is looking at a 4-room resale flat in Tampines priced at S$620,000.

Eligibility check. As a divorced SC aged 35 or above, Ms Tan qualifies under the Singles Scheme. Her child (a minor) can be listed as an essential occupier on the application — this does not change the scheme type. She has not owned private property, so the 30-month wait-out does not apply. Her previous HDB flat was sold in 2023, and she is not concurrently owning another HDB flat, so concurrent ownership is not an issue.

Loan and grant eligibility. Ms Tan’s gross monthly income of S$6,800 is just under the S$7,000 singles income ceiling for the HDB Concessionary Loan. She is eligible to apply for the HDB loan at 2.6% per annum. At 80% LTV, her loan would be S$496,000. Over a 25-year tenure, the monthly repayment is approximately S$2,230. Her Mortgage Servicing Ratio (MSR) is 2,230 ÷ 6,800 = 32.8%, which slightly exceeds the 30% MSR cap. To stay within MSR, she can: extend her tenure to 30 years (monthly ~S$1,975, MSR 29.0% ✓); or switch to a bank loan at ~1.5% (monthly ~S$1,706 on S$464,250 at 75% LTV, MSR 25.1% ✓, though requiring more cash upfront). For the Enhanced Housing Grant (EHG), her income of S$6,800 is under the S$9,000 ceiling — she may qualify for EHG of up to S$40,000 as a single first-timer.

What This Means for You

The HDB resale market offers a pragmatic pathway to home ownership for groups who cannot access BTO flats — including PRs, older singles, divorced buyers, and those who need to move quickly without a BTO wait of several years. The key trade-off is price: resale flats are priced at market rates, which in 2026 means a 4-room flat in a mature estate typically costs S$580,000–S$780,000, substantially more than BTO pricing for comparable units. However, the grants system (EHG, CPF Housing Grant, Proximity Housing Grant) can offset S$30,000–S$160,000 of the purchase price depending on your household profile.

Understanding which scheme you qualify under is more than a bureaucratic exercise — it determines your flat-type entitlements, whether you need a co-applicant, and the grants you can access. If you are unsure which scheme applies to your situation, HDB’s e-Service portal provides an eligibility self-assessment tool, and HDB sales teams at HDB Hub (Toa Payoh) can advise on individual circumstances.

What Might Come Next

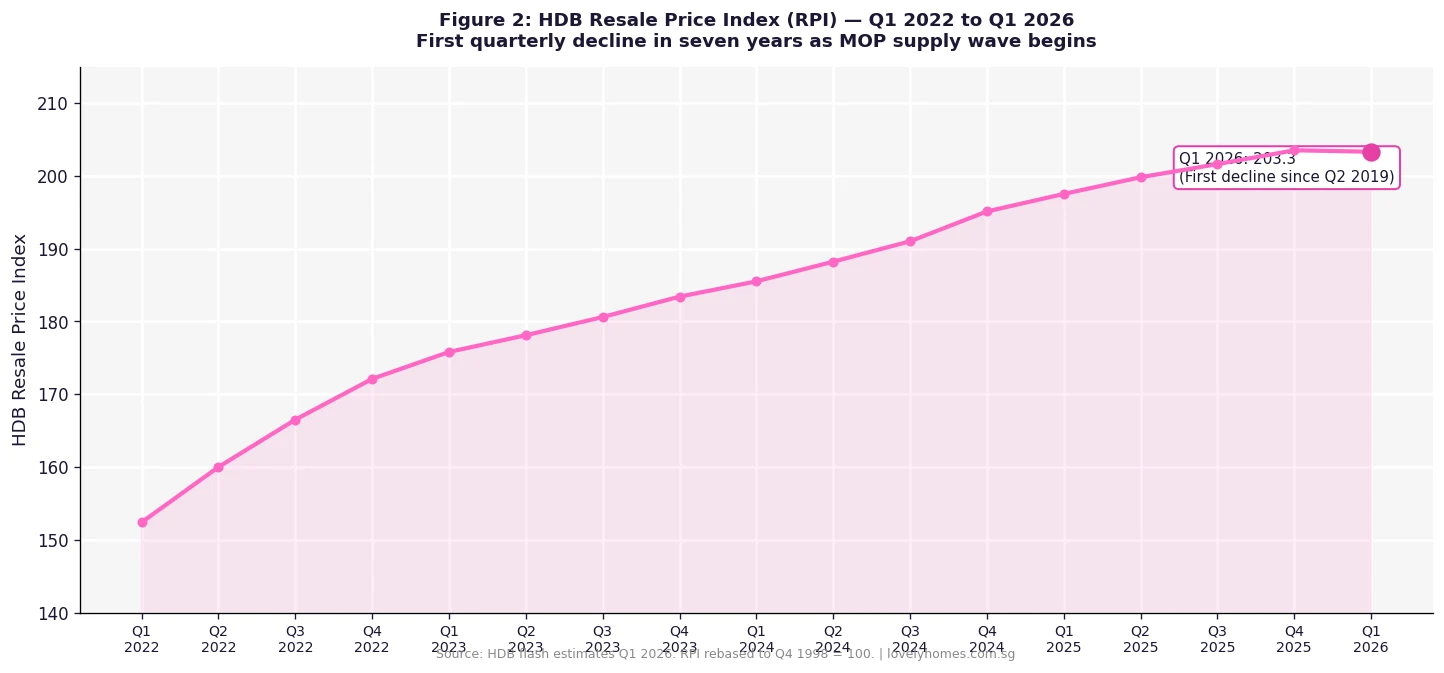

The HDB eligibility framework has remained broadly stable since the September 2022 cooling measures, but there are two areas to watch. First, the government has signalled continued attention to the resale market — if the Resale Price Index (RPI) resumes material increases after Q1 2026’s modest 0.1% dip, further demand-side measures targeting eligibility or wait-out periods cannot be ruled out. Second, the ongoing rollout of HDB’s new flat classification system (Standard, Plus and Prime) is reshaping what constitutes a “subsidised” flat — future eligibility amendments may further restrict resale proceeds from Plus and Prime flats, which already carry a 6%–9% subsidy clawback on sale.

Frequently Asked Questions

Can I buy an HDB resale flat if I own a private property overseas?

No. The disqualification applies to any private residential property, whether in Singapore or overseas. If you or any listed occupier own a foreign private property, you must dispose of it before applying for an HDB flat. The 30-month wait-out period runs from the date of disposal, unless you are an SC aged 55 and above buying a 4-room or smaller flat (who is exempt from the wait-out).

My spouse is a foreigner on an Employment Pass. Can we buy an HDB resale flat?

Yes, under the Non-Citizen Spouse Scheme, you (as the SC applicant) can purchase a 2-room to 5-room resale flat with your foreign spouse listed as an essential occupier. Your spouse will not be a co-owner — the flat is held in your name only. You must be the sole applicant, and the flat type is limited to 2-room through 5-room (not 3Gen or certain premium flat types). Standard EIP quotas and CPF/grant rules apply based on your citizenship and income.

I became a PR three years ago. Does that mean I can buy an HDB resale flat immediately?

Yes, provided you meet all other eligibility conditions — you must form a valid family nucleus (you cannot buy as a PR single), you cannot own another HDB flat concurrently, and you cannot own a private residential property. The 3-year PR minimum is measured from the date on your In-Principle Approval (IPA) letter, not your NRIC collection date. If your PR was granted in April 2023, you would be eligible from April 2026 onwards, assuming all other criteria are met.

I sold my condo in January 2025. Can I buy an HDB resale flat now in May 2026?

Yes — by May 2026, 16 months have passed since your January 2025 disposal. However, the 30-month wait-out period requires 30 months from disposal, which means you would not be eligible until July 2027 (30 months after January 2025). Unless you are an SC aged 55 and above buying a 4-room or smaller flat, you will need to wait until July 2027 before submitting an HDB resale application.

What is the difference between an applicant and an essential occupier?

The HDB applicant (and any co-applicant) is the legal owner of the flat. An essential occupier is someone who forms part of the family nucleus for the purpose of qualifying for the flat, but who does not hold any ownership interest. For example, under the Non-Citizen Spouse Scheme, the foreign spouse is an essential occupier — they live in the flat and are listed on the application, but are not on the title. Essential occupiers are bound by certain ownership restrictions and must remain listed for a minimum period as specified by HDB.

Can I apply for an HDB resale flat if I am an undischarged bankrupt?

Yes, with conditions. HDB does allow undischarged bankrupts to apply for a resale flat, but you cannot use an HDB Concessionary Loan if you are bankrupt — you must finance using a bank loan or cash. Additionally, your co-applicant (if any) may face restrictions on CPF usage. You should disclose your bankruptcy status in the HDB application; non-disclosure is an offence under the Housing and Development Act and can result in compulsory acquisition of the flat.

Does the Ethnic Integration Policy (EIP) affect my eligibility to buy a specific flat?

Yes. The EIP sets ethnic quotas at both the block level and neighbourhood level to maintain racial integration across HDB estates. If the block or neighbourhood quota for your ethnic group has been reached, you will not be able to purchase that specific flat, regardless of your broader eligibility. The EIP quota is checked at the time of the HDB application — it is possible to receive an OTP and then find the flat is unavailable under EIP when you apply. See our detailed guide on the HDB Ethnic Integration Policy for block-level and neighbourhood quota mechanics.

Related Articles

- HDB Ethnic Integration Policy Singapore 2026: Block Quotas, Neighbourhood Limits and SPR Rules Explained

- HDB Resale Market Q1 2026: Prices Fall 0.6% in First Decline Since 2019

- HDB Grants Singapore 2026: EHG, CPF Housing Grant, Proximity Grant and Step-Up Grant Explained

- Upgrading from HDB to Private Property Singapore 2026: Step-by-Step Guide, Costs and Timing

- Minimum Occupation Period (MOP) Singapore 2026: HDB, EC and Private Property Rules Explained

- 13,480 HDB Flats Reaching MOP in 2026: What the Supply Wave Means for Buyers and Sellers

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty