Renting out your Singapore condo or HDB flat sounds simple — sign a tenancy agreement, collect a monthly transfer, repeat. Then April rolls around, and the IRAS e-filing portal asks you to declare your net rental income. Suddenly you are wrestling with deductible mortgage interest, the 15% deemed-expense option, what counts as “repairs” versus “improvements”, and whether your S$420 monthly MCST bill is a write-off (it is). Get it wrong by a thousand dollars in either direction, and the result is either a real cash tax overpayment, or an IRAS query letter you do not want to receive.

This guide walks you through how rental income is taxed in Singapore in 2026, what the IRAS rules actually say, the two paths you can choose between for expense deductions, and a fully-worked example using realistic 2026 numbers for a typical leveraged condo investor. By the end you should be able to fire up your IRAS Income Tax e-Filing screen, key in Total Annual Rent, Allowable Expenses and Net Rental Income, and be confident the numbers reconcile to your actual cashflow.

Quick Answer — how Singapore taxes your rental income in 2026

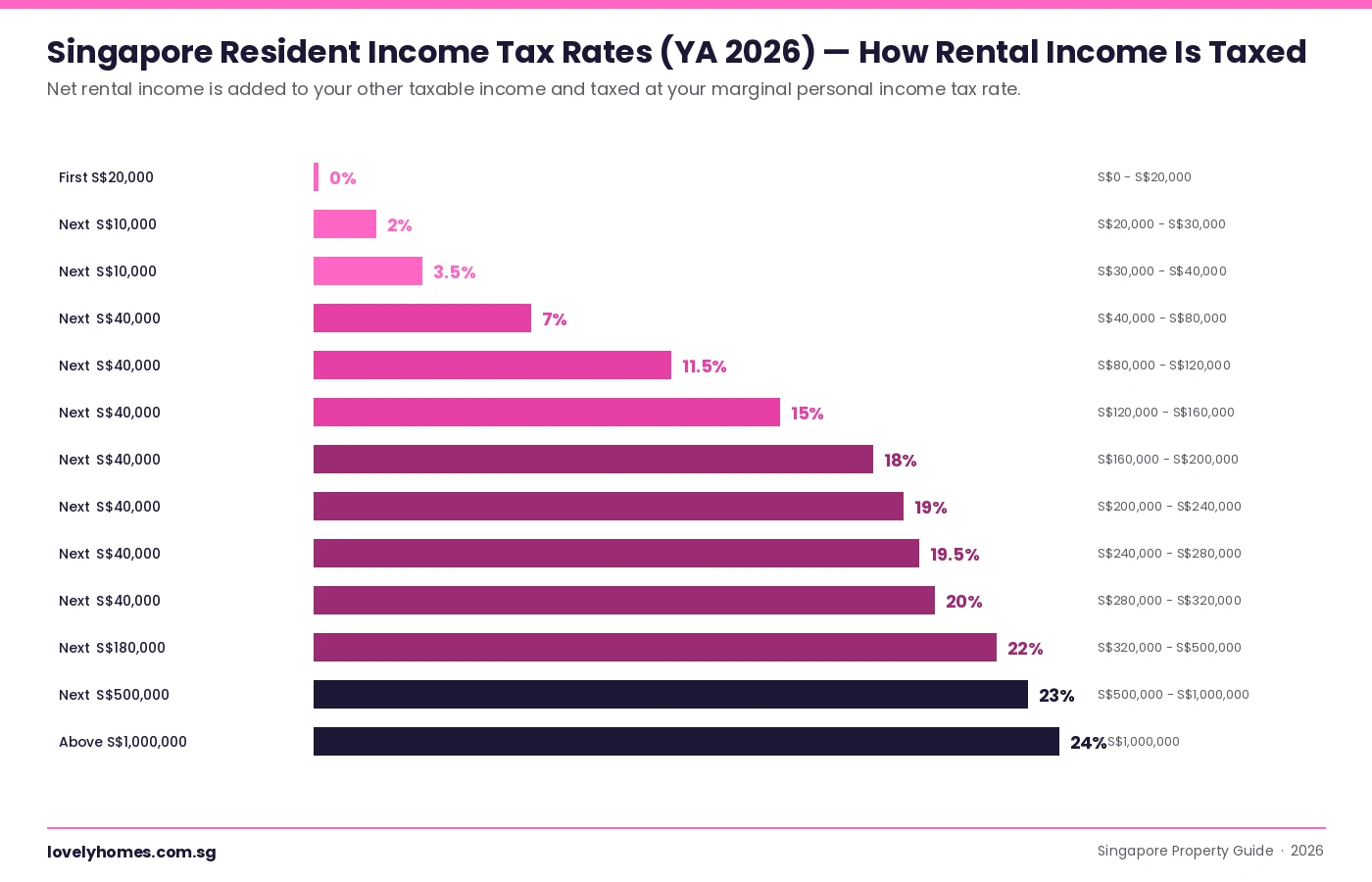

- Rental income is not a separate tax — net rental is added to your other income and taxed at your marginal personal income tax rate (0% to 24% for residents in YA 2026).

- You can claim actual qualifying expenses (with receipts) OR a flat 15% deemed-expense deduction. Pick whichever is higher.

- Mortgage loan interest is always deductible on top of the 15% deemed deduction — do not forget this; it is the single largest line for most leveraged landlords.

- Property tax for a tenanted unit is at the higher non-owner-occupier rate (12-36% of AV in YA 2026). It is fully deductible from rental income.

- Furniture, renovations and capital upgrades are not deductible — they are capital items.

- Foreign-property rents owned by a Singapore tax resident are taxable only if remitted to Singapore (with conditions).

- Filing deadline: 15 April (paper) or 18 April (e-Filing) for individuals, every year of assessment.

What “Rental Income” Means for IRAS Purposes

Under section 10(1)(f) of the Income Tax Act 1947, “rents” derived from any property in Singapore are chargeable to tax. The Comptroller of Income Tax interprets this broadly: it covers the basic monthly rent, anything else the tenant pays you under the tenancy agreement, and certain non-cash benefits.

What goes into your gross rent figure on your tax return:

- Monthly rent — the headline figure on the tenancy agreement.

- Furniture and fittings rent — if your tenant pays a separate fee for furnishings, it is rent.

- Maintenance fees billed to the tenant if they pass through you (uncommon but valid).

- Compensation for early termination of the lease (if not specifically structured as damages).

- Any non-refundable lease premium received.

What is not rental income: the tenant’s security deposit while you still hold it (you owe it back), and any reimbursement of utility bills paid by the tenant directly to SP Group, M1, etc. Forfeited security deposits, however, do count as rental income at the time of forfeiture.

How Rental Income Is Taxed: The Marginal-Rate Mechanic

Singapore does not have a separate “rental tax” or a flat rate on rental income. Instead, your net rental income — gross rent less allowable expenses — is added to all your other taxable income (employment income, trade or self-employment profits, interest, royalties) and taxed at the resident progressive rates.

| Existing income before rent | Marginal rate on next S$1 of rental income | Tax on +S$10,000 net rent |

|---|---|---|

| S$30,000 (e.g. retiree) | 3.5% / 7% | ~S$525 |

| S$80,000 (mid-career employee) | 11.5% | S$1,150 |

| S$120,000 | 11.5% / 15% | ~S$1,250 |

| S$200,000 (senior professional) | 18% / 19% | ~S$1,850 |

| S$500,000 (top tier) | 22% / 23% | ~S$2,250 |

The same rental property therefore generates very different tax outcomes for two landlords. A retired SC with no employment income may pay almost no tax on a S$60,000 gross rent year, while a senior professional earning S$250,000 from employment can lose 19-22% of every dollar of net rent to the marginal-rate stack. This is why high-income Singaporean landlords often plan property purchases under the lower-earning spouse’s name — a perfectly legitimate (though ABSD-sensitive) way to lower household tax.

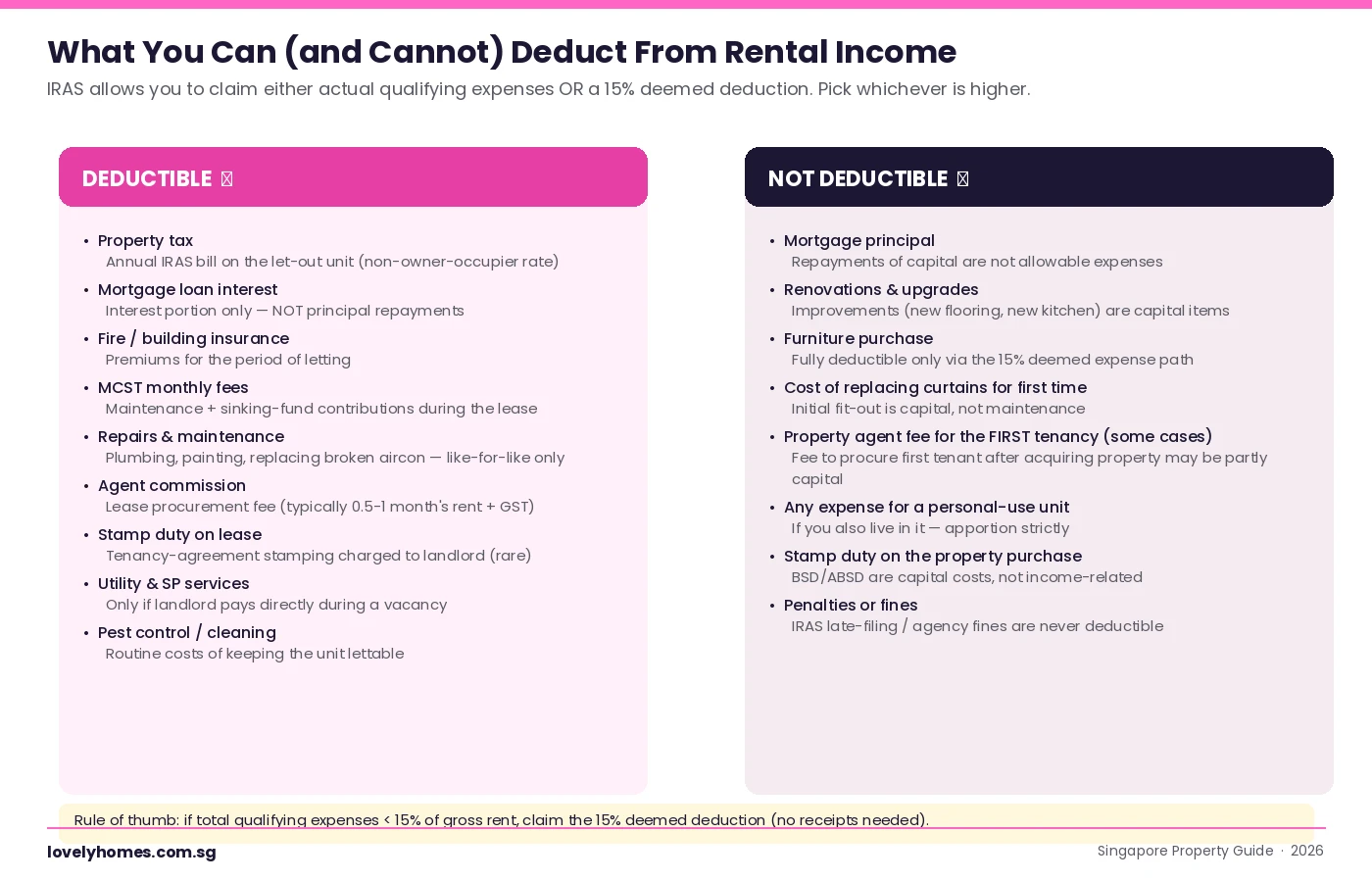

What You Can Deduct: The Two Paths

Once you have your gross rent, IRAS lets you choose between two paths to compute net rental income. The choice is made property by property on each year’s filing — there is no lock-in.

Path A: Actual qualifying expenses

You add up every expense incurred wholly and exclusively in earning the rent during the year and deduct it from gross rent. Required to keep receipts and supporting documentation for 5 years (IRAS Income Tax Records Keeping Requirement). The full list of typical deductible items:

- Property tax on the tenanted unit (non-owner-occupier rate, 12-36% of AV in 2026).

- Mortgage loan interest — the interest portion of every monthly instalment. The principal repayment portion is not deductible.

- Fire / building insurance premiums.

- MCST monthly fees (maintenance + sinking-fund contributions) for the period of letting.

- Repairs and maintenance — like-for-like fixes only. Replacing a broken aircon compressor is repair; replacing the entire aircon system with a higher-end model is partly improvement (not deductible).

- Agent commission on lease procurement (typically 0.5-1 month of rent + GST). The first-tenancy commission may be partly disallowable; subsequent commissions are fully deductible.

- Stamp duty on the tenancy agreement — if landlord has agreed to bear it (rare; usually tenant pays).

- Vacancy-period utilities and SP Services when paid directly by the landlord.

- Routine cleaning, pest control, gardening attributable to the unit during letting.

Path B: 15% deemed expense + mortgage interest

From YA 2017 onwards, IRAS allows residential-property landlords to claim a flat 15% deemed deduction on gross rent in lieu of itemising actual expenses, plus their actual mortgage interest. No receipts are needed for the 15% portion.

This is a real shortcut for low-cost landlords. If you own a HDB flat free-and-clear (no mortgage interest), with low MCST and minimal repairs, your actual qualifying expenses might be 8-12% of rent — the 15% path delivers a higher deduction, with no admin. For leveraged condo landlords, by contrast, mortgage interest alone often runs 50-70% of rent; the actual-expense path almost always wins.

Important: the 15% deemed-expense path is only available for residential property let to a tenant who occupies the unit. Commercial property landlords, AirBnB-style serviced-apartment hosts, and corporate-structured property trusts cannot use it.

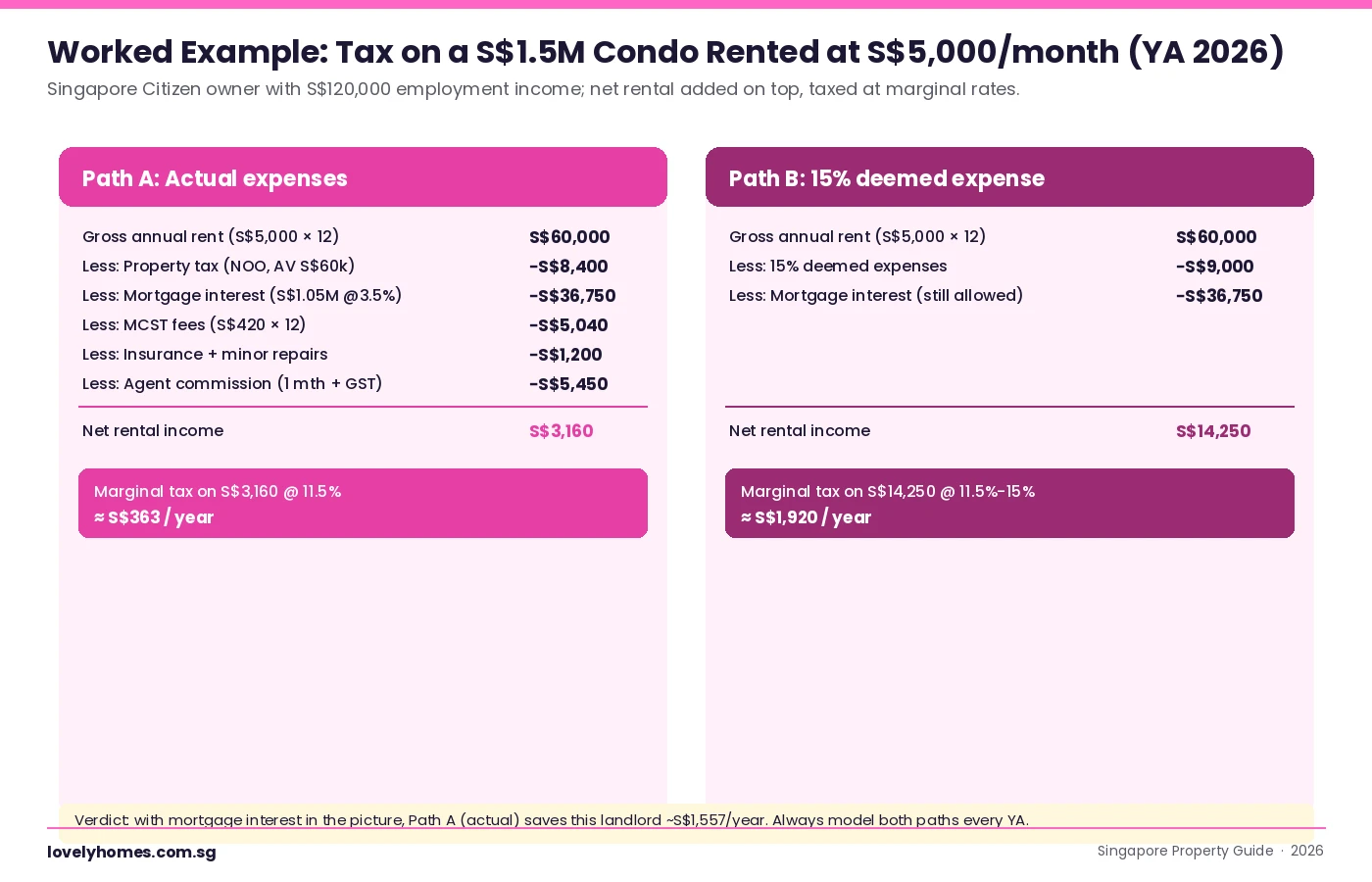

Worked Example: A S$1.5M Condo Let at S$5,000/Month

Numbers make this concrete. Consider a Singapore Citizen owner-occupier of a 1,000-sqft 3-bedroom OCR condo bought at S$1.5M with a S$1.05M loan (LTV 70%) at 3.5% all-in. The unit is rented at S$5,000/month from January to December. The owner has S$120,000 of employment income.

Three lessons from this example:

- For any landlord with a meaningful mortgage, Path A almost always wins. Mortgage interest is the single biggest deductible.

- If you remortgage and your interest expense changes mid-year, your tax position changes mid-year — track it monthly.

- The marginal rate matters as much as the deduction. A landlord at the 22% bracket saves ~S$340 more on the same S$1,557 deduction than the same landlord at the 15% bracket.

Property Tax for Tenanted Units

The instant your property is rented out, IRAS automatically reclassifies it from owner-occupied to non-owner-occupied (NOO). The tax rate ladder differs sharply:

- Owner-occupier rates: 0% on the first S$8,000 of AV, rising progressively to 32% on AV above S$100,000.

- Non-owner-occupier rates: 12% on the first S$30,000 of AV, rising to 36% above S$60,000 AV in 2026.

For a typical S$1.5M OCR condo with an AV of around S$60,000, the owner-occupier annual property tax would be about S$8,400; the same unit as a NOO investment is taxed at S$8,400 (owing to the band structure crossing 12%/24%/36%) — in this band, NOO is significantly higher. You must notify IRAS within 15 days of the unit becoming tenanted (or vacated) so the rate is correctly applied. This NOO property tax is then a fully deductible expense against your rental income on the income-tax side.

Joint Owners and Couples

For jointly-held properties, IRAS apportions rental income and deductions equally by default among co-owners, regardless of who actually pays the mortgage or collects the rent. If you want a different split (e.g. 70/30 to reflect actual capital contributions or beneficial ownership), you must file a declaration of beneficial interest and IRAS may ask for evidence.

This is the heart of the Singapore tax-planning playbook for couples: where one spouse earns in the top marginal bracket and the other earns less, splitting the rental income via a 50/50 joint-tenancy or a deliberately-skewed tenancy-in-common can lower household tax materially. The trade-off — ABSD — is covered in our Joint Tenancy vs Tenancy in Common guide.

Vacancy, Mid-Year Letting, and Voids

When you let your property only for part of the year, only the rent received is taxable, and only the expenses attributable to the letting period are deductible (pro-rated). Common scenarios:

- Owner moves overseas mid-year and rents out from August. Pro-rate the property tax (NOO rate from 1 August), MCST fees, and insurance from August onwards. Mortgage interest is fully deductible against rent because the loan continues throughout, but only the August-December portion is matched against the August-December rent.

- Tenant moves out, unit vacant for 2 months, new tenant moves in. Vacancy-period expenses (utilities, MCST, mortgage interest) are still deductible if the property was actively marketed for re-letting during the void.

- Property partly let, partly self-occupied. Only the let portion’s expenses are deductible; the personal-occupation portion is not. Apportion strictly by floor area and time.

What Might Come Next: Rental Tax Watchpoints

The basic IRAS framework has been stable since the 15% deemed-expense option was introduced in YA 2017. Two areas to watch in 2026:

- Short-term let crackdown. URA’s 3-month minimum residential let rule is now policed more aggressively. AirBnB-style sub-3-month lets are not legal residential lettings and may also be reclassified as a trade by IRAS, attracting higher tax and disqualifying the 15% deemed path.

- NOO property-tax escalation. The NOO rate ladder has steepened in each Budget since 2022 (peak rate raised from 27% to 36% over three years). Investors should model continuing escalation when underwriting yield.

None of the above is a tax-rate change yet. We will update this guide when Budget 2027 announcements land in February 2027.

Frequently Asked Questions

I let out a single room in my owner-occupied flat. Is that rental income?

Yes. The rent received from a sub-let or room-let is taxable on the same basis as a whole-unit let. You can deduct a fair-share portion of expenses — typically based on the floor area of the let room versus total floor area, multiplied by the days let. The 15% deemed-expense path is also available. You do not have to convert the entire property’s tax status to NOO — that conversion only applies if the whole unit is let out and you no longer occupy it.

Can I deduct the cost of a new sofa I bought when I started renting out the unit?

Not under Path A — the initial fit-out of furnishings is a capital cost, not a maintenance cost. However, if you choose Path B (15% deemed deduction), the deemed-expense covers wear-and-tear and replacement furnishings implicitly. If you replace a broken sofa with a like-for-like sofa later, that is deductible as a repair under Path A.

I am a Singapore tax resident with an apartment in London that I rent out. Is the UK rent taxable in Singapore?

Foreign-source rental income earned by a Singapore tax-resident individual is taxable only when remitted to Singapore (and even then, certain remittances are tax-exempt under section 13(7A) of the Income Tax Act). If the UK rental income stays in a UK bank account and you do not bring it back, it is generally not taxable in Singapore. UK tax on the rent (HMRC Self Assessment) is a separate matter — you should keep that compliance current to avoid double-tax issues. Singapore has a Double Taxation Agreement with the UK that provides relief.

Can my parent (who has no employment income) be the named landlord to lower household tax?

The beneficial owner of the property is the person taxed on the rental income, not necessarily the legal title-holder. If your parent merely holds the title but you funded the deposit, paid the mortgage, and collect the rent, IRAS will still tax you. Genuine transfers to a parent (with proper SDL stamping, ABSD implications, and a real change in beneficial ownership) can shift the tax base, but the costs and ABSD trigger usually outweigh the income-tax savings unless the property has a long runway. Always model the all-in cost across BSD, ABSD, conveyancing, and 5+ years of expected tax savings before transferring.

What happens if I file the wrong figure?

If IRAS detects a discrepancy via its automated checks against your bank records, agent-reported tenancy stampings, and property-tax NOO classification, you will receive an enquiry letter (typically 1-2 years after filing) asking you to reconcile. Genuine errors made in good faith can be self-corrected via an Objection or Amendment within 4 years. Deliberate under-declaration can attract a penalty of up to 200% of the tax undercharged plus interest, plus criminal prosecution in serious cases. The honest path is materially cheaper than the alternative.

Is there any way to claim depreciation on the building structure?

No. Singapore tax law does not allow capital allowances (depreciation) on residential buildings or land. This is one of the structural differences from the US, UK and Australian regimes, where depreciation can shelter meaningful rental cashflow. The only “depreciation-equivalent” reliefs available to Singapore landlords are repairs (Path A) and the 15% deemed expense (Path B).

Do I need to register for GST as a residential landlord?

No. Residential lettings are exempt supplies under the Goods and Services Tax Act — you do not charge GST on rent, and you cannot register for GST on the basis of residential rental income alone. Commercial-property landlords are different: they charge 9% GST (in 2024 onwards) on rent, and must register if their taxable turnover exceeds S$1 million per year.

Related Articles

- Singapore Property Tax 2026 — the underlying NOO-vs-owner-occupier rate split that flows into your rental tax math.

- Landlord Guide HDB & Condo Singapore 2026 — lease structure, security deposits, end-of-lease rules.

- Rental Stamp Duty Singapore 2026 — the tenancy agreement stamping that goes alongside your tax filing.

- Singapore Rental Yield Guide 2026 — gross vs net yield, stress-test against tax outcomes.

- Singapore Strata Title and MCST Guide 2026 — the MCST monthly fee that lands on every condo P&L.

- Joint Tenancy vs Tenancy in Common — how to structure ownership across a couple for tax efficiency.

- Foreign Buyer Guide Singapore 2026 — non-residents are taxed at flat 24% on Singapore rental income.

Disclaimer

This guide is for general information only and does not constitute tax, legal, or financial advice. Singapore income tax law — including the rates, deductibility rules, and remission frameworks discussed above — is subject to change at the discretion of the Minister for Finance and the Comptroller of Income Tax. Always verify the current position on the Inland Revenue Authority of Singapore rental-income page, the relevant individual income tax rate schedules, and the latest annual Ministry of Finance Budget statement — and consult a licensed tax adviser before acting on any specific position. Worked examples are illustrative only; your actual tax outcome will depend on your full facts.

0 Comments