Renting a Condo in Singapore 2026: Complete Guide to Leases, Costs and Tenant Rights

Quick Answer — Renting a condo in Singapore at a glance

- Median condo rent in 2026: S$3,100–S$5,700/month depending on unit size and region

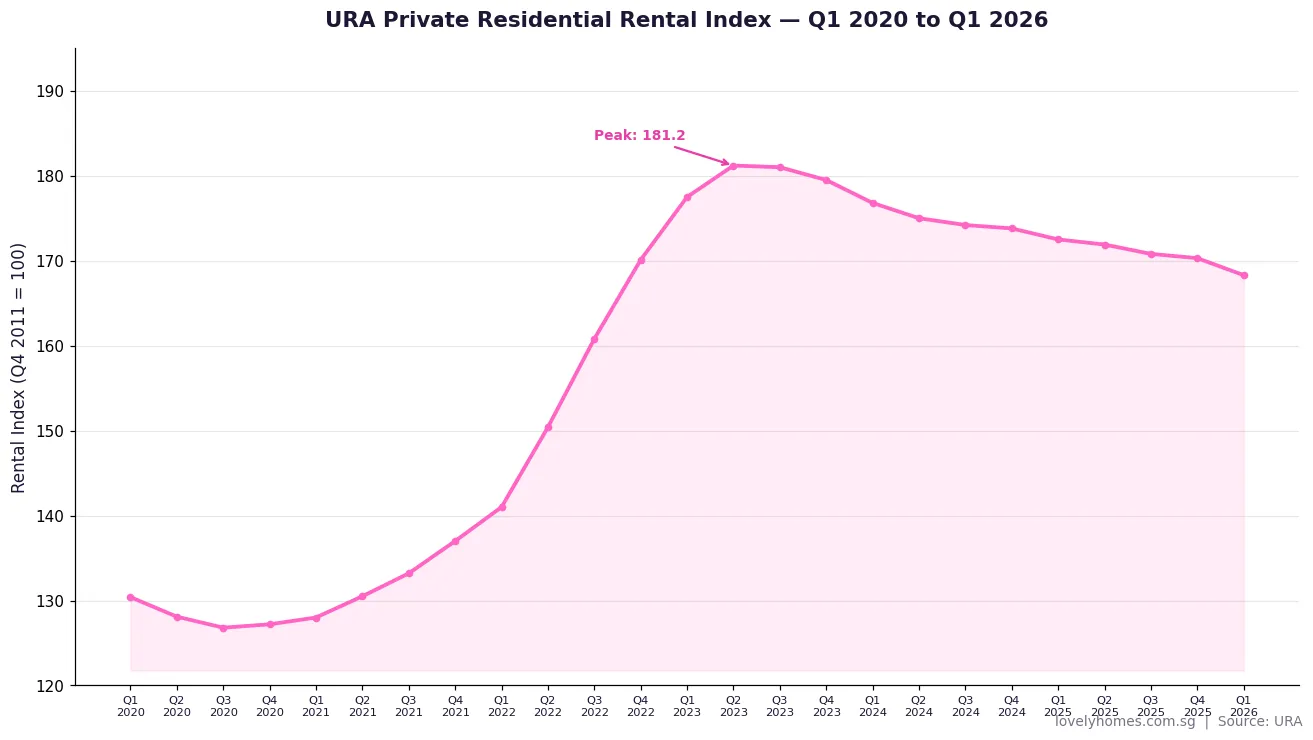

- URA private residential rental index fell 1.2% in Q1 2026 as new supply enters the market

- Minimum legal tenancy for private property: 3 months (short-term rentals under 3 months are prohibited)

- Upfront costs: typically 1+1 month security deposit + half-month agent commission

- Stamp duty on tenancy agreement: 0.4% × annual rent × number of years

- Landlord must supply a functional, habitable unit; tenant pays utilities and minor repairs

- Look for a diplomatic clause if your stay may be cut short — usually exercisable after month 12

- The non-citizen quota (NCQ) limits foreign tenants in HDB estates to 8% per neighbourhood and 11% per block — condo rentals have no NCQ restriction

Renting a condominium in Singapore is the entry point for most expatriates, professionals on employment passes, and Singaporeans who are in between home ownership. It is also increasingly attractive to local upgraders who sell their HDB flat but want flexibility before committing to a private purchase. In 2026, the rental market has shifted in tenants’ favour: vacancy rates have edged up to around 7%, the Urban Redevelopment Authority (URA) reported a 1.2% quarterly decline in the private residential rental index in Q1 2026, and landlords in many districts are now negotiating where they once insisted. This guide explains how renting a condo in Singapore actually works — from understanding what a unit costs across different regions, to signing a legally compliant tenancy agreement, to knowing your rights as a tenant when things go wrong.

The Singapore Private Rental Market in 2026

Singapore’s private residential rental market is administered indirectly by the URA, which tracks rental transactions and publishes quarterly price and rental indices. Unlike HDB rentals, private condo rentals are not subject to nationality quotas — a landlord may rent to any nationality with a valid pass or PR status. The market is therefore more internationalised, with a significant proportion of tenants being expatriates on Employment Passes (EP) or S Passes, as well as Singaporeans awaiting new-launch completion.

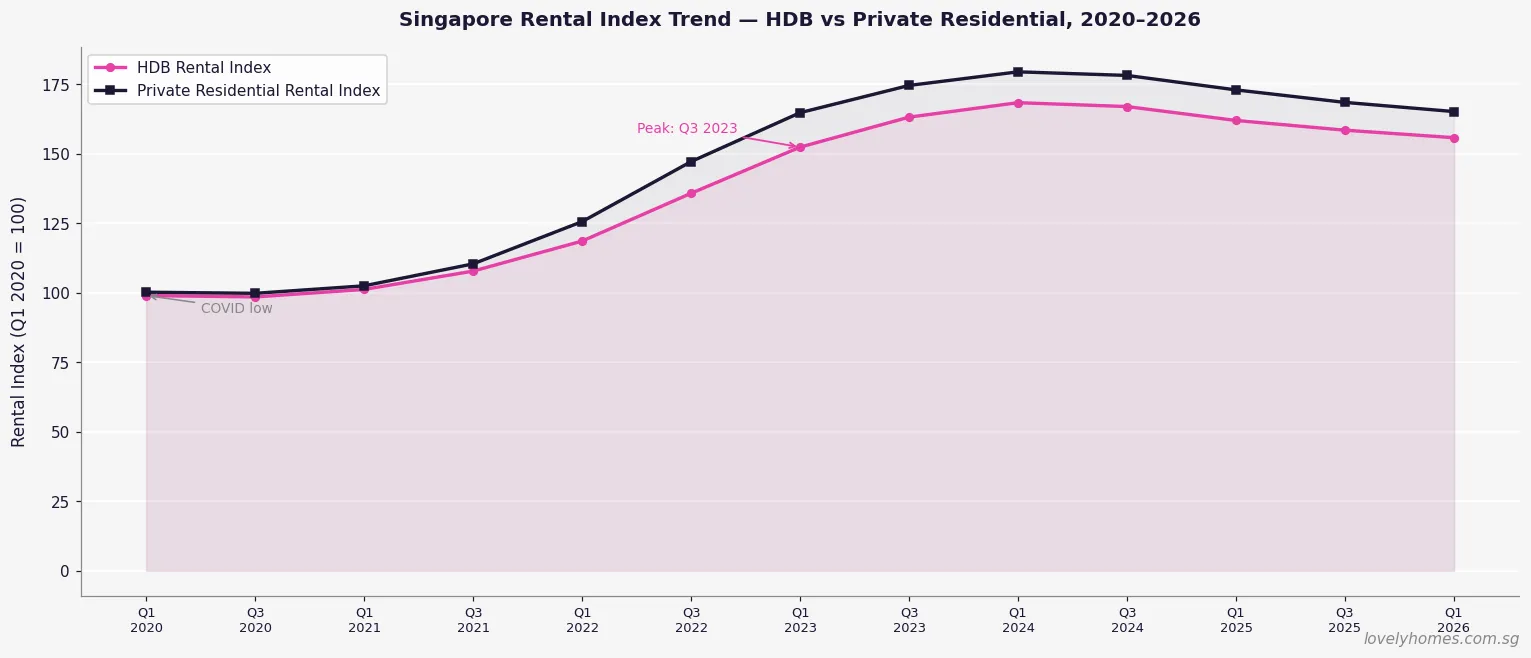

After an extraordinary run-up of over 40% in rental values between 2021 and 2023 — driven by post-pandemic return of expats, supply constraints, and HDB delays — the market began softening in late 2023 and has continued to normalise. As at Q1 2026, private residential rents remain elevated against 2019 levels but are declining gradually as the pipeline of 17,032 unsold units (URA Q1 2026) and completions from 2022–2024 launches add supply. Vacancy has widened to an estimated 7%, giving tenants meaningful negotiating leverage for the first time in years.

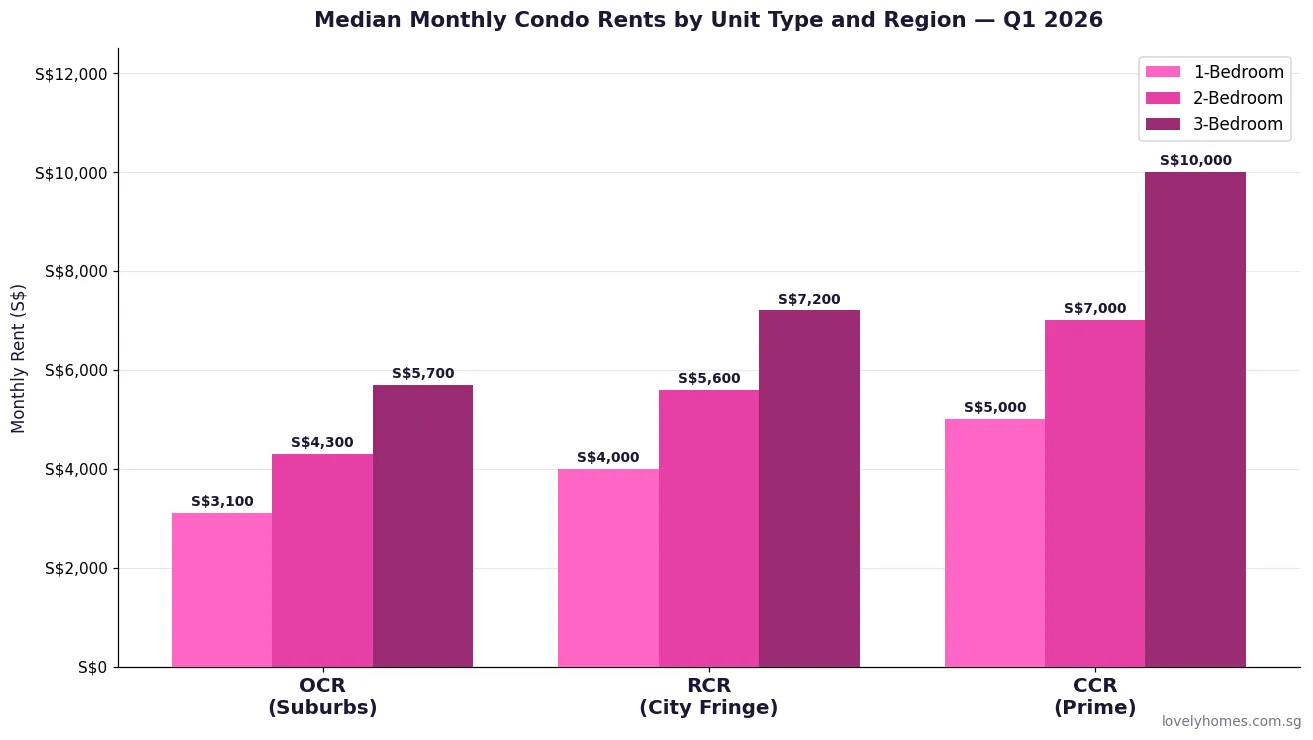

Condo Rental Rates by Region and Unit Type

Rental rates vary significantly by district, unit size, floor level, and age of development. The URA divides Singapore into three broad rental markets: the Core Central Region (CCR), covering Districts 9, 10, 11, and the Downtown Core; the Rest of Central Region (RCR), covering city-fringe areas such as Queenstown, Bishan, Toa Payoh, and Geylang; and the Outside Central Region (OCR), covering mass-market suburbs such as Punggol, Sengkang, Tampines, Woodlands, and Jurong.

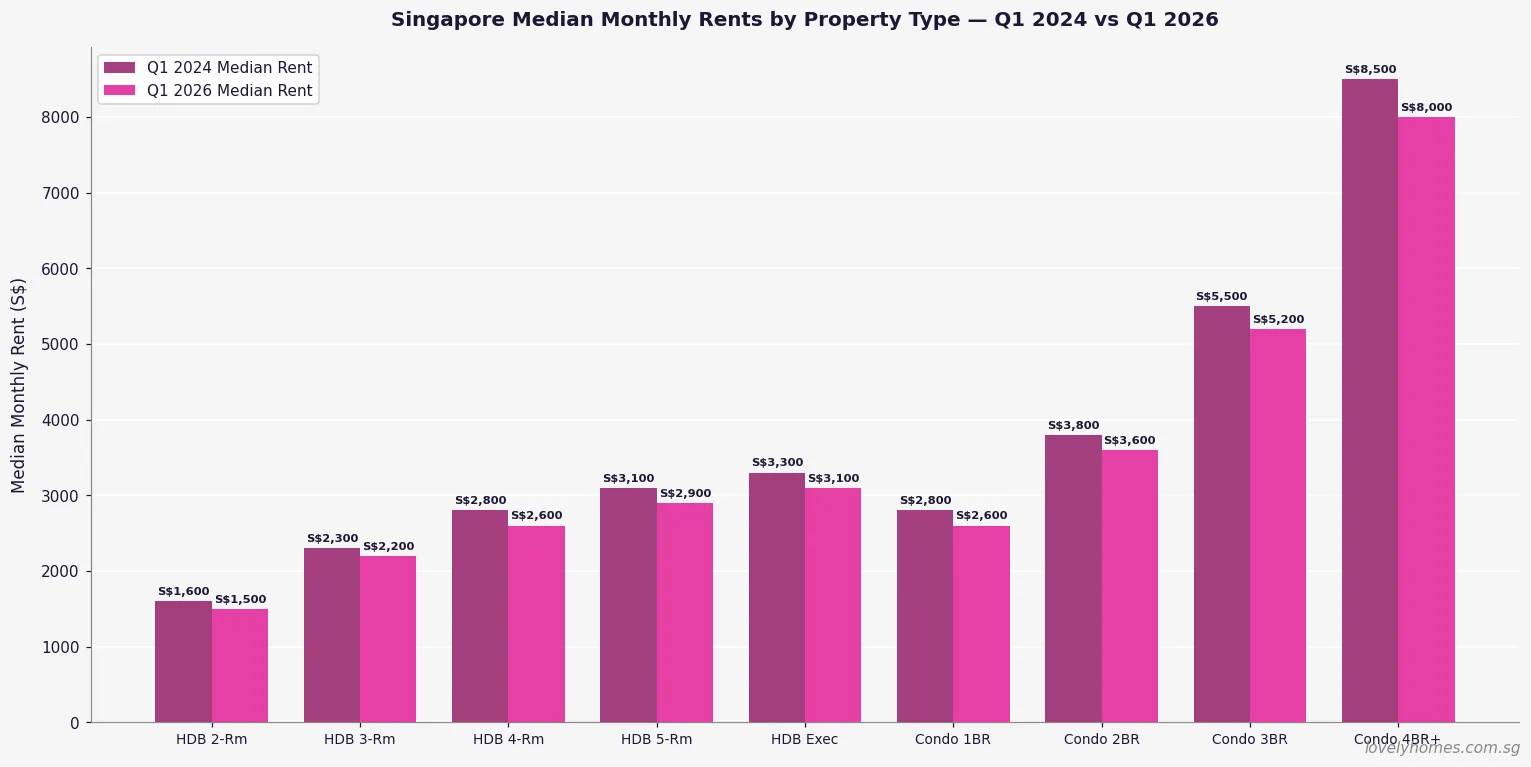

| Unit Type | OCR (Suburbs) | RCR (City Fringe) | CCR (Prime) |

|---|---|---|---|

| Studio / 1-Bedroom | S$2,800–S$3,500/mth | S$3,500–S$4,500/mth | S$4,000–S$6,000/mth |

| 2-Bedroom | S$3,800–S$5,000/mth | S$4,800–S$6,500/mth | S$5,500–S$9,000/mth |

| 3-Bedroom | S$5,000–S$6,500/mth | S$6,000–S$8,500/mth | S$7,500–S$14,000/mth |

| 4-Bedroom / Penthouse | S$6,500–S$9,000/mth | S$7,500–S$12,000/mth | S$10,000–S$25,000+/mth |

These are indicative ranges for units in good condition within well-maintained developments. Older freehold condos in established CCR districts (such as Nassim Road or Ardmore Park) can command premiums well above the ranges shown. Conversely, mass-market condos in OCR estates near an MRT station but without premium fittings typically sit at the lower end. Furnished units command a premium of roughly 10–20% over unfurnished equivalents, though most condo landlords provide at minimum white goods and air-conditioning units.

Types of Condo Available for Rent

Singapore’s private residential market offers several distinct product types under the broad “condo” umbrella. A standard condominium is a multi-unit strata development of six or more floors with full facilities — swimming pool, gym, function room, and 24-hour security. An apartment block (fewer than five floors, no mandatory facilities) is technically different from a condominium under the Planning Act but is marketed identically. Landed property — terraces, semi-detached, detached houses — is rented by Singaporeans and permanent residents with ease, but foreigners require approval from the Singapore Land Authority under the Residential Property Act to rent non-condominium landed property; condo units are fully open to foreigners.

Serviced apartments, though physically similar to condos, operate under a hotel licence and are typically rented on weekly or monthly terms. They sit outside the standard tenancy framework and carry no stamp duty obligation but command significant rent premiums for the flexibility and daily services included. They are a popular bridge while a new expatriate’s permanent housing is arranged.

Step-by-Step Rental Process

Renting a condo in Singapore follows a reasonably standardised process, though timelines can compress or extend depending on landlord circumstances and market conditions.

Step 1 — Search and shortlist. Most tenants search on PropertyGuru, 99.co, or STProperty. View three to five properties in person before making an offer. Pay attention to maintenance standards, lift lobby cleanliness, pool condition, and the responsiveness of the management corporation (MCST) — all signal how well-managed the development is.

Step 2 — Letter of Intent (LOI). Once you identify a unit, you submit a Letter of Intent — a one-page document specifying the agreed rent, tenancy term, move-in date, and any special requests (additional parking, pet clause, specific appliances). The LOI is accompanied by a good-faith deposit equal to one month’s rent. The landlord has three to seven days to sign or counter-propose.

Step 3 — Tenancy Agreement (TA). Once the LOI is agreed, the landlord’s solicitor (or the landlord directly) prepares the Tenancy Agreement. This is the binding legal contract. Review it carefully — particularly the diplomatic clause, the inventory schedule, the repair obligations, and any early termination penalties. Once signed, both parties pay the stamp duty on the TA.

Step 4 — Stamp duty and move-in. The tenant (or landlord, depending on agreement) stamps the TA with the Inland Revenue Authority of Singapore (IRAS) at 0.4% of the annual rent multiplied by the number of years of the tenancy. On the move-in date, the balance of the security deposit is paid and a thorough condition check of the unit is conducted and documented.

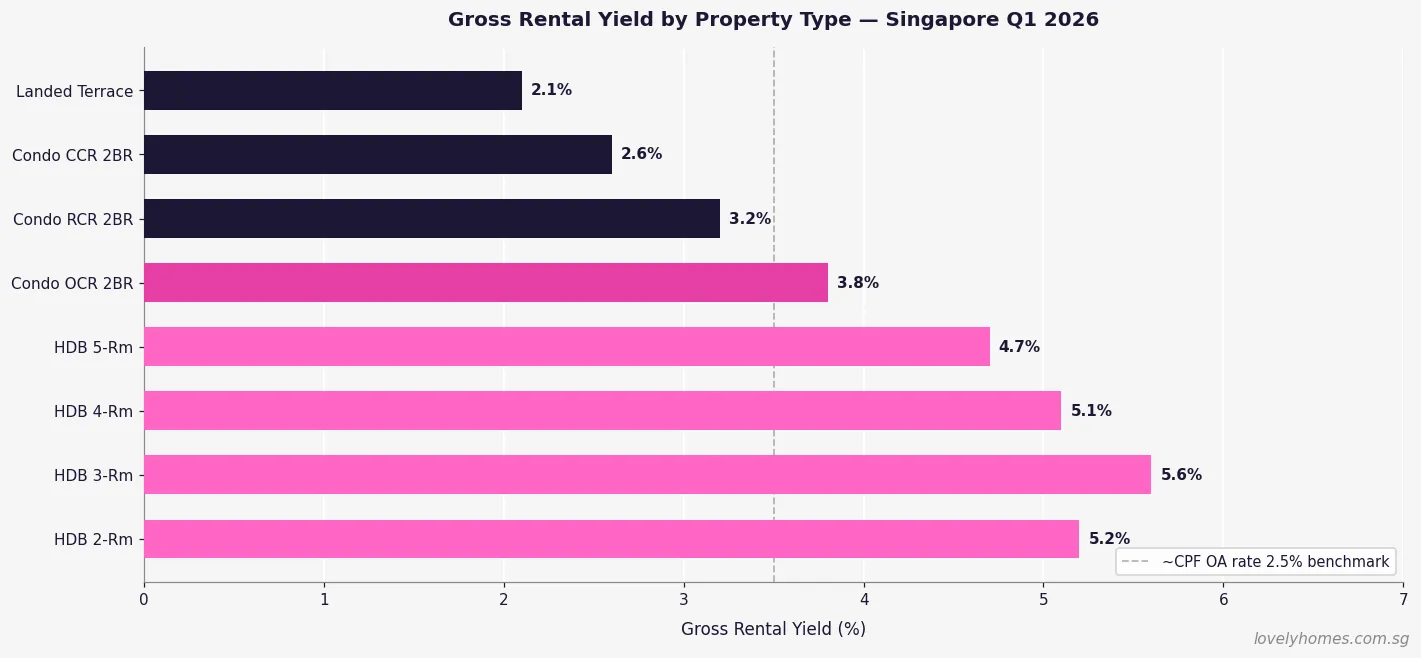

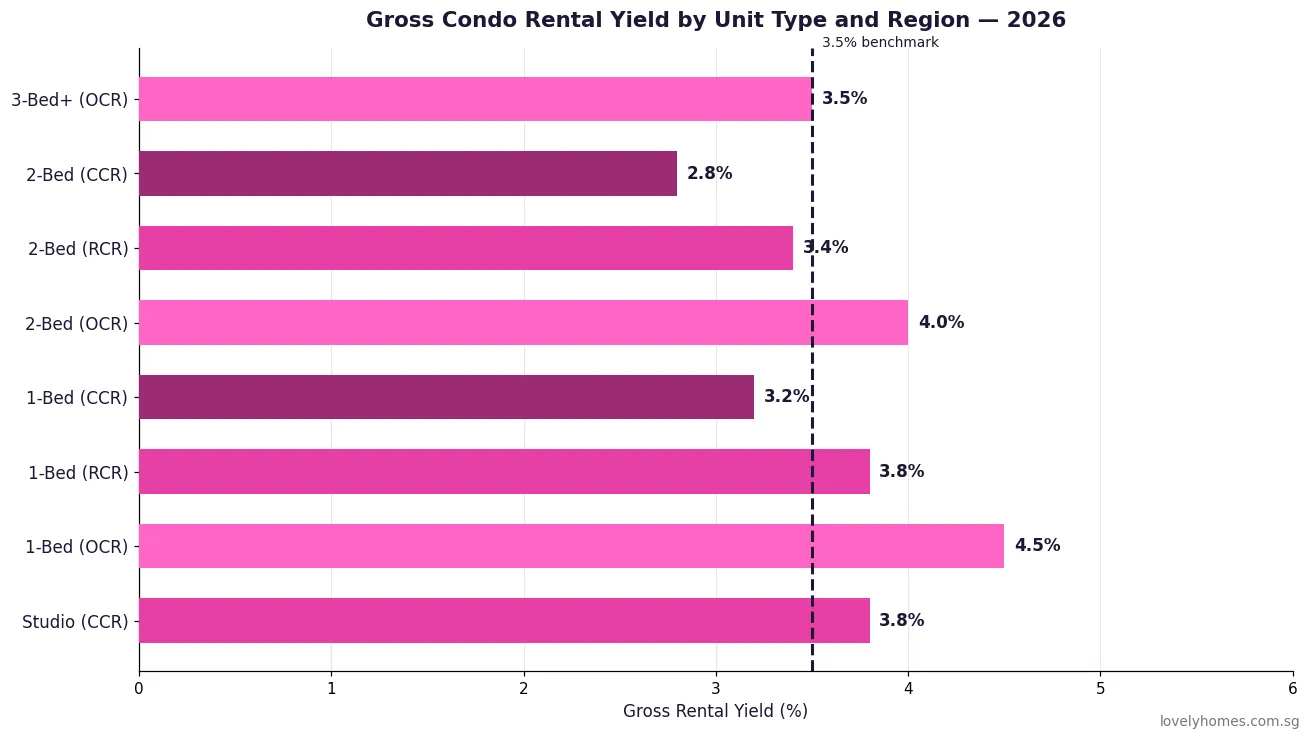

Rental Yields — Understanding the Landlord’s Perspective

Gross rental yield is the annual rent divided by the purchase price of the property. Understanding yields helps tenants appreciate why landlords price units the way they do, and can be a useful data point in negotiations — a landlord who bought at the peak of 2022–2023 faces significant yield compression and may be more flexible on rent than official asking prices suggest.

Costs to Budget For as a Tenant

The headline monthly rent is not the only cost a prospective condo tenant must account for. Before signing, budget for the following upfront payments.

Security deposit: The market convention is one month’s security deposit per year of tenancy. A standard two-year tenancy therefore requires a two-month security deposit — typically paid in two instalments: one at LOI stage and one at TA signing. The deposit is held by the landlord and returned within 14 days of vacating (subject to any deductions for damage beyond fair wear and tear).

Agent commission: For a two-year or longer lease, the tenant typically pays half a month’s commission to the tenant’s agent, and the landlord pays one month to the landlord’s agent. For shorter leases, commission structures vary. Always clarify this before engagement — some co-broking arrangements shift the full commission to the tenant.

Stamp duty on tenancy agreement: The rate is 0.4% of the total rent payable. For a two-year tenancy at S$4,500/month, this works out to S$4,500 × 12 × 2 × 0.4% = S$432. This is typically paid by the tenant within 14 days of signing the TA.

Utilities: Utilities (electricity, water, gas) are the tenant’s responsibility in virtually all private condo tenancies. In 2026, a typical 2BR condo unit incurs electricity costs of approximately S$120–S$220/month depending on air-conditioning usage. The Open Electricity Market (OEM) allows tenants to choose between retailers for potentially lower rates.

| Cost Item | Typical Amount | Who Pays | Timing |

|---|---|---|---|

| Security deposit (2yr lease) | 2 months’ rent | Tenant | At LOI + at TA signing |

| Agent commission | 0.5–1 month’s rent | Tenant (0.5) + Landlord (1) | At TA signing |

| Stamp duty on TA | 0.4% × annual rent × years | Usually tenant | Within 14 days of TA signing |

| First month’s rent | 1 month’s rent | Tenant | On move-in date |

| Utilities connection | S$100–S$200 deposit | Tenant | Before move-in |

| Minor maintenance | Varies | Tenant (fair wear & tear) | Throughout tenancy |

Tenancy Agreement — Key Clauses to Negotiate

The Tenancy Agreement is a standard-form document in Singapore, often based on the Law Society’s approved template, but landlords routinely customise it. As a tenant, pay particular attention to the following clauses before signing.

Diplomatic clause: This entitles the tenant to terminate the lease early if they receive a confirmed repatriation or job transfer. The standard form allows exercise after the first 12 months of a 24-month lease, with two months’ written notice. Not all landlords will agree to this, especially for shorter leases. If you are on an Employment Pass that could be cancelled, insist on this clause.

Repair obligations: The landlord is generally responsible for structural repairs and maintaining fixed installations such as built-in kitchen appliances, water heaters, and air-conditioning systems in working order. The tenant is responsible for day-to-day maintenance — changing light bulbs, maintaining cleanliness, and repairing damage caused by the tenant. The TA should specify a cost threshold (commonly S$150–S$300) below which the tenant handles repairs without recourse to the landlord.

Pet clause: Most condo tenancy agreements prohibit pets by default. If you have a pet, negotiate the pet clause in the LOI stage — do not assume goodwill after signing. Landlords who agree often require an additional deposit.

Subletting: Subletting without written landlord consent is a breach of the TA. If you may need to sublet a room, negotiate an express subletting clause at the outset. Note that subleasing to more than six unrelated persons in a condo unit breaches the Urban Redevelopment Authority’s occupancy cap regulations.

Worked Example: Mr Rajesh, Renting a 3-Bedroom OCR Condo

Mr Rajesh is a Malaysian national on an Employment Pass, earning S$12,000/month. He is relocating from a company-provided serviced apartment to a self-arranged private condo for a 24-month lease starting 1 August 2026. He identifies a 3-bedroom, 1,300 sq ft condo unit in Sengkang (OCR) at S$5,200/month (unfurnished).

Upfront costs:

- Good-faith deposit at LOI: S$5,200 (1 month)

- Balance security deposit at TA signing: S$5,200 (2nd month of 2-month deposit)

- First month’s rent: S$5,200

- Stamp duty: S$5,200 × 12 × 2 × 0.4% = S$499

- Tenant agent commission (0.5 month): S$2,600

- Utilities connection deposit: S$150

- Total upfront: approximately S$18,849

Ongoing monthly: Rent S$5,200 + estimated utilities S$200 = S$5,400/month. This represents 45% of Mr Rajesh’s gross income, within the comfort range for a single-income expat household. He negotiated a diplomatic clause exercisable after month 14 with two months’ written notice, which his employer agreed to support if repatriation is required.

Market check: The landlord originally listed at S$5,500/month. Because vacancy in the OCR rental market has widened and two similar units in the same development are vacant, Mr Rajesh’s agent negotiated S$5,200 — a S$300/month or S$7,200 saving over the two-year lease. This illustrates the current market dynamic: asking prices are often negotiable by 5–8% for quality tenants willing to commit to longer terms.

The Market Shift: What the Rental Index Tells Us

The URA private residential rental index peaked around Q1 2023 at approximately 181.5 (base Q4 2011 = 100). It has since declined to around 168.3 in Q1 2026 — a fall of about 7.3% from peak — but remains some 29% above Q1 2020 pre-pandemic levels. This context matters for tenants: rents are lower than the 2023 frenzy but are not at pre-2021 levels, and the rate of decline has slowed. A sustained oversupply scenario would push rents further down; conversely, if global business activity picks up and EP inflows accelerate, the market could tighten again by late 2026 or 2027.

What Might Come Next — Rental Market Outlook

The short-to-medium outlook for Singapore condo rentals in 2026 and 2027 leans modestly in tenants’ favour. Three supply-side factors support further gentle softening: the completion pipeline from 2022–2024 new launches continues to deliver units; the 2H 2026 Government Land Sales programme announced in June 2026 will add further medium-term supply; and the 17,032 unsold private units as at Q1 2026 represent a substantial buffer. On the demand side, the Singapore labour market remains tight with EP inflows expected to hold at current levels, which should provide a floor under rental demand.

That said, the era of 8–15% annual rental increases is clearly over for now. Tenants in 2026 should expect flat to modestly declining rents in OCR and RCR areas, while CCR prime districts — where international tenant budgets are less price-sensitive — may see more stable or even firmer rents if global financial activity sustains. Tenants renewing leases expiring in mid-2026 should push firmly for discounts of 5–10% versus their 2024 contracted rates.

Frequently Asked Questions

Can a foreigner rent a condo in Singapore?

Yes. Foreigners with a valid pass (Employment Pass, S Pass, Dependent Pass, Long-Term Visit Pass, or Student Pass) may rent any private condo unit without restriction. There is no nationality quota on private condo rentals, unlike HDB estates which are subject to the non-citizen quota. Foreigners may not rent landed property (terrace, semi-detached, or detached house) without approval from the Singapore Land Authority under the Residential Property Act, but this restriction does not apply to condominium units.

What is the minimum tenancy period for a condo?

The minimum tenancy for a private residential property in Singapore is three consecutive months. Short-term rentals of less than three months — including Airbnb-style arrangements — are illegal for private residential units under the Planning Act. Penalties for illegal short-term rentals are severe: landlords face fines of up to S$200,000 for each infringement. Serviced apartments that are licensed as hotels operate under different rules and may rent on daily or weekly terms.

How much is stamp duty on a condo tenancy agreement?

Stamp duty on a Tenancy Agreement is payable to the Inland Revenue Authority of Singapore (IRAS) at a rate of 0.4% of the total rent payable over the lease term. The formula is: Annual Rent × Number of Years × 0.4%. For a 2-year lease at S$4,800/month, the calculation is S$4,800 × 12 × 2 × 0.4% = S$461. Stamp duty must be paid within 14 days of signing the TA. Either the landlord or the tenant may pay — it is negotiable but conventionally the tenant’s responsibility. The stamped TA is the enforceable document for any dispute resolution in the Singapore courts.

What is a diplomatic clause and do I need one?

A diplomatic clause (also called a “relocation clause”) entitles the tenant to terminate the lease early if they receive a confirmed job transfer, repatriation, or redundancy. In Singapore, the standard diplomatic clause allows the tenant to break a 2-year lease after 12 months by giving two months’ written notice and providing documentary evidence (e.g., a letter from the employer). The clause is named “diplomatic” because it was originally designed for embassy and diplomatic personnel but is now used widely by all corporate tenants on Employment Passes. If there is any chance you may be relocated during your lease, insist on a diplomatic clause before signing — it cannot easily be added after the TA is executed.

Who is responsible for air-conditioning servicing?

The landlord is responsible for ensuring the air-conditioning units are in working order at the commencement of the tenancy. During the tenancy, the maintenance obligation depends on the TA wording. Most standard TAs require the tenant to service the air-conditioning units every three months and maintain them in working order for normal wear and tear, while the landlord is responsible for major repairs (compressor failure, refrigerant recharging) that exceed the minor repair threshold (typically S$150–S$300). Always ensure the TA specifies who pays for which type of air-con repair to avoid disputes.

Can my landlord increase the rent mid-tenancy?

No. Once a Tenancy Agreement is signed and stamped, the agreed rent is contractually fixed for the duration of the lease. The landlord cannot unilaterally increase the rent during the tenancy term. Rent may only be renegotiated at renewal. This is one key reason to sign a longer lease in a falling rental market — it locks in your current rate and protects against any potential reversal. Conversely, in a rising rental market, signing a shorter lease preserves your ability to relocate to a lower-priced unit or negotiate more aggressively at expiry.

How do I get my security deposit back?

At the end of the tenancy, both landlord and tenant (or their agents) conduct a check-out inspection against the original check-in inventory report. The landlord has 14 days from the end of the tenancy to return the deposit (or the agreed balance). Deductions may only be made for damage beyond fair wear and tear — meaning damage caused by misuse, negligence, or accident, not ordinary ageing. If the landlord disputes deductions, the tenant can escalate to the Small Claims Tribunal (SCT) — the SCT hears rental disputes up to S$30,000 and does not require legal representation. Always photograph the unit thoroughly at both check-in and check-out and keep all written communications with the landlord.

Related Articles

- Singapore Rental Market Guide 2026: HDB and Condo Rents, Yields and Outlook Explained

- Renting Out Your HDB Flat 2026: Rules, Quotas, Rental Rates and Step-by-Step Landlord Guide

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Home Loan Complete Guide 2026: HDB Loans, Bank Loans, TDSR, MSR and Best Rates Explained

- Singapore Property Conveyancing Guide 2026: OTP, S&P Agreement, Legal Fees and Timelines Explained

- Singapore Property Investment Guide 2026: How to Buy, Rent and Build Wealth Through Property

Disclaimer: This article is intended as general information only and does not constitute legal or financial advice. Rental market figures are indicative estimates based on URA published data and industry surveys as at Q1–Q2 2026 and may differ from individual transactions. Tenancy law, stamp duty rates, and regulatory requirements may change — always verify current figures with the Inland Revenue Authority of Singapore (IRAS), the Urban Redevelopment Authority (URA), and a qualified property lawyer before entering into any tenancy. LovelyHomes does not act as a property agent and does not endorse any landlord, developer, or property service provider.