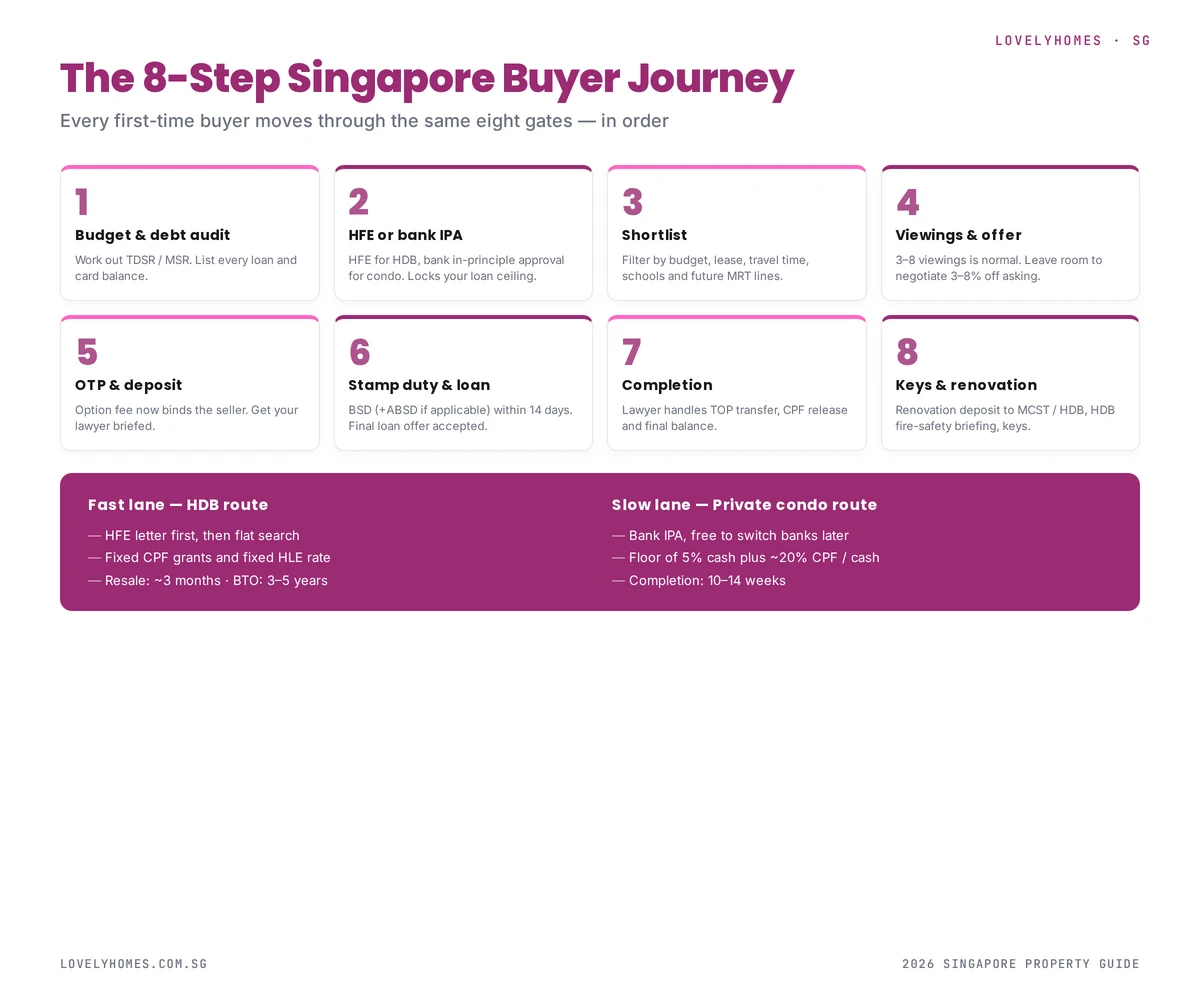

CPF Housing Grant Singapore 2026: Complete Guide to EHG, Family Grant & Proximity Grant

- First-timer families can receive up to S$80,000 in Enhanced CPF Housing Grant (EHG) for BTO or resale flats (household income ≤ S$9,000/month).

- Singles buying a 2-Room Flexi BTO qualify for up to S$40,000 EHG (individual income ≤ S$4,500/month).

- Resale buyers can stack the Family Grant (up to S$50,000) with the EHG and the Proximity Housing Grant (PHG, up to S$30,000) — potentially S$160,000 in total grants.

- The PHG has no income ceiling and rewards buyers who live near or with parents or children.

- All CPF grants go into your CPF Ordinary Account (OA) and are used against the purchase price — but they accrue interest that must be refunded upon sale.

- Grants do not eliminate your cash component of the downpayment — at least 5% cash is still required for bank loans.

- Applications are via the HDB flat portal and must be completed before exercising the Option to Purchase (OTP).

What Are CPF Housing Grants and Who Administers Them?

CPF Housing Grants are direct subsidies paid by the Singapore Government into the buyer’s CPF Ordinary Account (OA) to help Singaporeans afford their first — and in some cases, second — HDB flat. They are administered jointly by the Housing & Development Board (HDB) and the Central Provident Fund Board (CPF Board), with eligibility rules updated periodically to reflect prevailing market conditions and government housing policy.

Unlike an ABSD remission or a bank subsidy, a CPF Housing Grant is a genuine cash transfer from the public purse into your CPF OA. It immediately reduces the amount you need to borrow or fund from savings, which lowers your monthly mortgage instalment. However, grants are not free in the accounting sense: when you eventually sell the flat, the grant amount — plus accrued interest at the CPF OA rate of 2.5% per annum — must be refunded back into your CPF OA. The net effect is deferred rather than eliminated cost.

As of 26 April 2026, the key grant types in force are the Enhanced CPF Housing Grant (EHG), the Family Grant, the Proximity Housing Grant (PHG), and the Step-Up CPF Housing Grant for eligible second-timers under the Fresh Start Housing Scheme.

Enhanced CPF Housing Grant (EHG) — Rates and Eligibility

The Enhanced CPF Housing Grant, introduced in September 2019 to replace the Additional CPF Housing Grant (AHG) and Special CPF Housing Grant (SHG), is the flagship subsidy for first-timer buyers. It is progressive — the lower the household income, the higher the grant — and applies to both new BTO flats and resale HDB flats, making it more flexible than its predecessors.

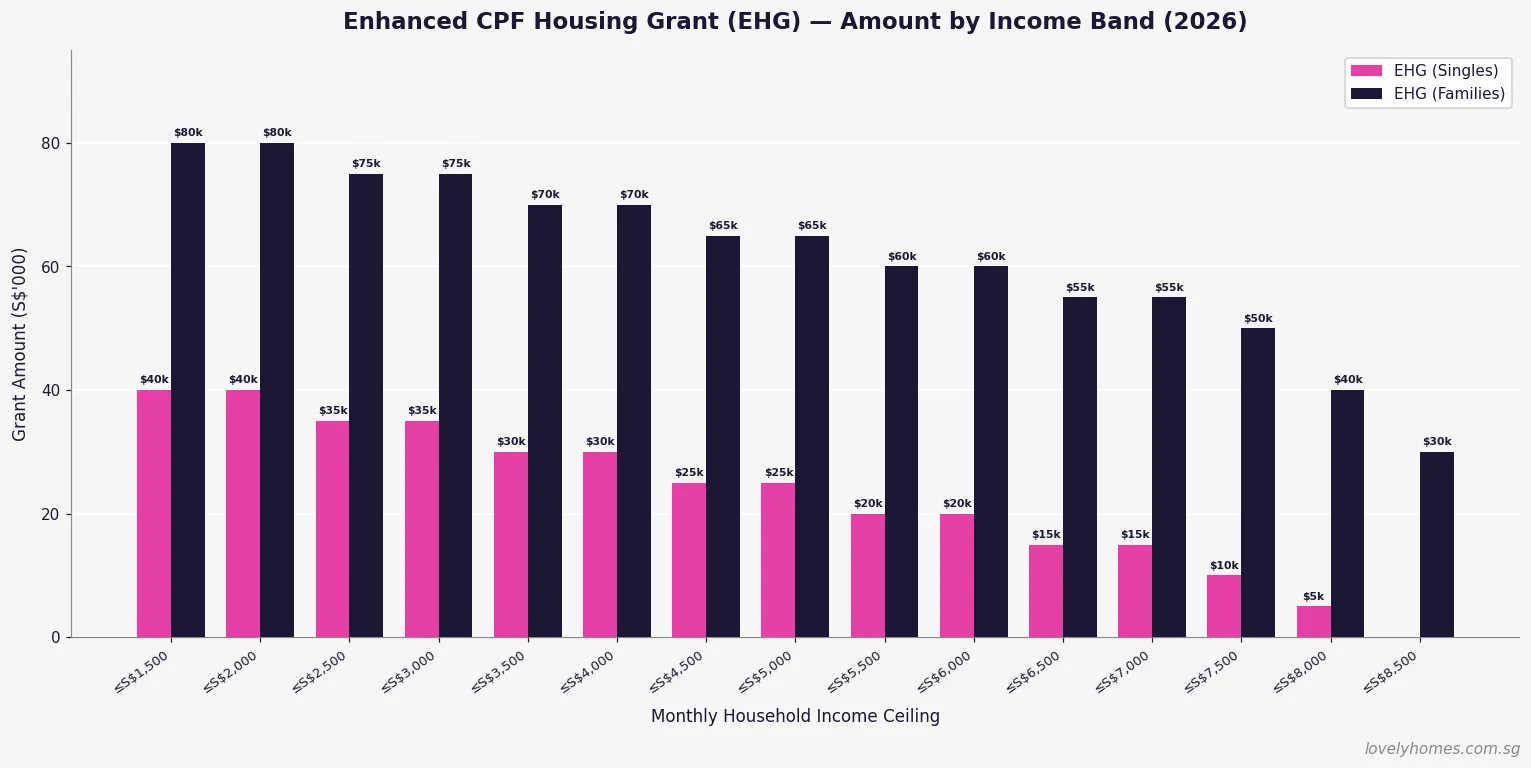

Figure 1: EHG amounts (S$’000) for singles vs families, by monthly household income band. Source: HDB (2026).

EHG for Families

For married or engaged couples — including those applying under the Fiancé/Fiancée Scheme — the EHG ranges from S$5,000 (household income ≤ S$8,000/month) to S$80,000 (household income ≤ S$1,500/month). The income assessed is the average gross monthly income of both applicants over the 12 months preceding the application. If the combined household income exceeds S$9,000/month, no EHG is payable.

EHG for Singles

First-timer singles aged 35 and above buying a 2-Room Flexi BTO flat in a non-mature estate qualify for EHG on a scaled basis, up to S$40,000 (individual income ≤ S$1,500/month). A single with income ≤ S$4,500/month qualifies for a minimum S$5,000 grant. Singles buying resale flats under the Single Singapore Citizen (SSC) scheme are also eligible, provided they purchase a 5-room flat or smaller.

| Monthly Gross Income (Household) | EHG — Families | EHG — Singles |

|---|---|---|

| ≤ S$1,500 | S$80,000 | S$40,000 |

| ≤ S$2,500 | S$75,000 | S$35,000 |

| ≤ S$3,500 | S$70,000 | S$30,000 |

| ≤ S$4,500 | S$65,000 | S$25,000 |

| ≤ S$5,500 | S$60,000 | S$20,000 |

| ≤ S$6,500 | S$55,000 | S$15,000 |

| ≤ S$7,500 | S$50,000 | S$10,000 |

| ≤ S$9,000 | S$30,000–S$40,000 | Not eligible |

Family Grant — For Resale HDB Buyers

The Family Grant is available exclusively to buyers of resale HDB flats and is stackable on top of the EHG. It acknowledges that resale flat prices in many estates carry a premium over BTO prices, and provides an additional buffer for buyers who prefer a specific location or immediate occupancy over the BTO ballot process.

The Family Grant is administered by HDB and paid into the CPF OA of eligible applicants. Key parameters as of 2026:

- SC + SC couple or family: S$50,000

- SC + SPR couple or family: S$40,000

- Singles (SSC scheme, resale 5-room or smaller): S$25,000

- Income ceiling: S$14,000/month combined household income

- Flat type restriction: any resale flat type; no restriction by town or estate

The S$14,000/month income ceiling makes the Family Grant accessible to many dual-income professional couples who earn too much for the EHG but still value the additional subsidy when purchasing resale.

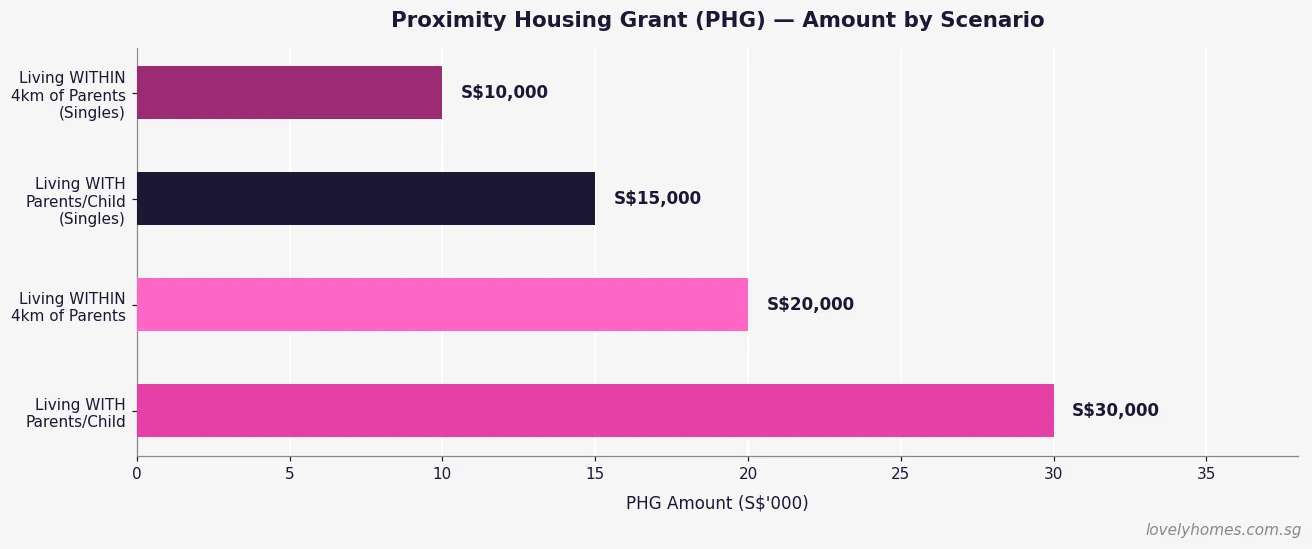

Proximity Housing Grant (PHG) — Rewarding Family Ties

Introduced in August 2015, the Proximity Housing Grant is one of the most distinctive features of Singapore’s housing policy. It uses a direct cash subsidy to incentivise multi-generational proximity — encouraging adult children to live near, or with, their elderly parents. It applies only to resale HDB flats and has no income ceiling, meaning higher-earning buyers can benefit too.

Figure 3: PHG amounts by proximity scenario, for families and singles. Source: HDB (2026).

The PHG has four tiers based on whether you are buying as a family or single, and whether you are moving with parents or children (same household) or within 4 km of them:

| Buyer Type | Living With Parents/Child | Living Within 4 km |

|---|---|---|

| Families (married/engaged couples) | S$30,000 | S$20,000 |

| Singles (SSC scheme) | S$15,000 | S$10,000 |

The “living with” criterion requires the parent or child to be registered on the same flat as an occupier. The “within 4 km” criterion uses the straight-line distance between postal codes, verified at the point of application. The PHG is a one-time benefit — once received, it cannot be claimed again on a subsequent flat purchase.

Step-Up CPF Housing Grant — Fresh Start Scheme

The Step-Up CPF Housing Grant is a targeted measure for a specific group: second-timer applicants who previously owned a subsidised flat and now qualify for a second chance at affordable owner-occupied housing under HDB’s Fresh Start Housing Scheme, which was introduced in October 2016 and expanded over subsequent years.

Eligibility is tightly defined: second-timer families with at least one child aged under 16; monthly household income ≤ S$7,000; must apply for a 2-Room Flexi BTO flat; must not currently own a flat or private residential property; and must fulfil a 5-year Fresh Start Housing Scheme Minimum Occupation Period on the new flat. The grant amount is up to S$50,000. It is not stackable with the EHG.

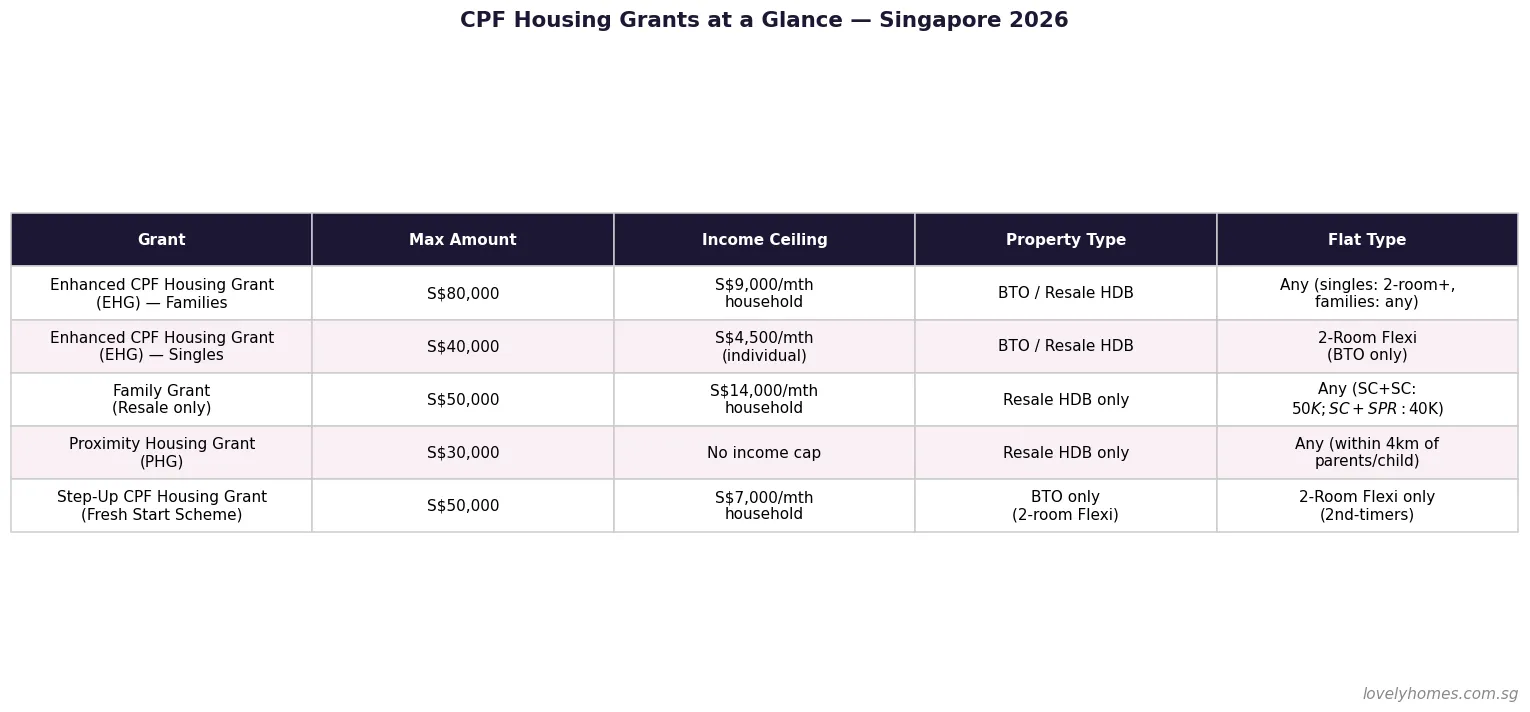

CPF Housing Grants at a Glance — Summary Table

Figure 2: Summary of all CPF Housing Grant types — amounts, income ceilings, and eligible property types. Source: HDB / CPF Board (2026).

Worked Example — Maximum Grant Stack for a Resale Buyer

Scenario: SC + SC First-Timer Couple, Resale Flat Near Parents

Buyer profile: Mr and Mrs Tan — married, both Singapore Citizens, first-timer applicants. Combined monthly gross income: S$6,800. Mrs Tan’s parents reside in the same block as the resale flat they are purchasing in Ang Mo Kio.

- EHG (family, income band S$6,500–S$7,500): S$50,000

- Family Grant (SC + SC, resale): S$50,000

- PHG (same block as parents = “living with”): S$30,000

- Total grants: S$130,000

Purchase price: S$600,000 (4-Room resale, Ang Mo Kio)

Effective net cost after grants: S$470,000 (before stamp duties and legal fees).

BSD on S$600,000: approximately S$12,600.

ABSD: Nil (first residential property, Singapore Citizen buyers).

Legal / conveyancing fees: approximately S$2,500–S$4,000.

Taking an HDB concessionary loan at 90% LTV: loan = S$540,000 less S$130,000 grants = S$410,000 loan needed, reducing the monthly instalment significantly versus purchasing without grants.

The CPF Accrued Interest Rule — The Hidden Cost of Grants

Every dollar drawn from your CPF OA — including grant monies — accrues interest at the CPF OA rate (currently 2.5% per annum). When you sell the flat, the CPF Board requires you to refund the principal amount used (including grants) plus the hypothetical interest that amount would have earned in the OA. This refund is returned to your CPF OA — not the government — and is available for future use in retirement or a subsequent property purchase.

Practical implication: a S$80,000 EHG held for 10 years accrues approximately S$22,000–S$25,000 in interest (compounded at 2.5% p.a.), bringing the total CPF refund for the grant alone to roughly S$102,000–S$105,000. Plan for this when modelling net sale proceeds on exit. If the sale price is insufficient to cover the full CPF refund, you keep the shortfall — you are not personally liable to top up the difference.

Why CPF Housing Grants Matter for Singapore’s Property Market

CPF Housing Grants fulfil a dual function in Singapore’s property ecosystem. At the individual level, they represent one of the most powerful demand-side subsidies in the world — transferring significant public funds directly to low- and middle-income buyers to help them achieve owner-occupation without over-relying on private financing. At the market level, they compress effective pricing for first-timers in the HDB resale segment, sustaining affordability across economic cycles.

The 2019 introduction of the EHG deliberately raised the income ceiling to S$9,000/month (from S$6,000/month under the legacy AHG/SHG regime), reflecting the Government’s recognition that median household incomes had risen and the historical ceilings were excluding a growing segment of first-timers who genuinely needed assistance.

Compared with equivalent policies in Hong Kong — where the Home Ownership Scheme provides a flat discount on market price rather than a direct grant — or Australia, where the First Home Owner Grant is a modest flat sum, Singapore’s progressive, stackable grant framework is both more generous and more targeted to income need.

What Might Come Next — Grant Policy Outlook for 2026–2028

The CPF Housing Grant framework is reviewed periodically in tandem with BTO flat pricing and HDB resale indices. Three plausible near-term developments:

- EHG income ceiling revision: With household income growth continuing, HDB may raise the S$9,000/month family ceiling to extend coverage to the lower-professional bracket — especially as Prime Location Public Housing (PLH) flat prices edge towards S$700,000–S$800,000 in central estates.

- PHG extension to BTO buyers: Currently restricted to resale buyers, extending the PHG to BTO buyers in family-friendly towns like Tengah and Bidadari has been discussed in policy circles, though not confirmed as of this date.

- Grant indexing to flat type or BTO pricing band: A flat S$80,000 EHG ceiling becomes proportionally less meaningful as PLH BTO prices climb. Grant amounts indexed to flat type could better reflect affordability gaps across different segments.

These are speculative. Always verify current grant levels at the HDB Grant Eligibility page before exercising any OTP.

Frequently Asked Questions

Can I use CPF Housing Grants towards the downpayment?

Grants are credited into your CPF OA and can be applied in the same way as your own CPF savings — towards the downpayment, the purchase price, and stamp duties (BSD). However, if you are taking a bank loan, the minimum 5% cash downpayment must be paid in cash; CPF (including grants) cannot cover this component. If you are taking an HDB concessionary loan, there is no mandatory cash component, so grants can fully offset the downpayment requirement alongside your other CPF OA balance.

Can both the EHG and Family Grant be claimed for the same resale flat purchase?

Yes. For resale flat purchases, a first-timer SC couple can claim both the EHG and the Family Grant simultaneously, provided they meet the eligibility criteria for each. If the couple also qualifies for the PHG — for example, buying near parents — that can be added on top. The theoretical maximum for an SC + SC couple buying resale is S$80,000 (EHG) + S$50,000 (Family) + S$30,000 (PHG living-with) = S$160,000, though achieving the maximum EHG requires a household income ≤ S$1,500/month, which is uncommon for buyers at today’s resale prices.

Does receiving a CPF Housing Grant affect my HDB Loan Eligibility (HLE)?

Grants and HLE are assessed separately. Your HDB Loan Eligibility letter determines the maximum HDB concessionary loan you can borrow, based on income, credit history, outstanding debts, and MSR/TDSR compliance. Grants reduce the net amount you need to borrow, but the HLE loan quantum is not directly inflated by the grant. You apply for both the HLE and the grant through the HDB flat portal before exercising the OTP.

I am a Singapore Permanent Resident married to a Singapore Citizen. What grants are we eligible for?

An SC + SPR couple counts as a mixed-citizenship household for CPF grant purposes. You are eligible for the EHG at the family rate (since one applicant is SC), the Family Grant at the reduced SC + SPR amount of S$40,000, and the PHG if applicable. You are not eligible for the full SC + SC Family Grant of S$50,000. The SPR spouse’s income is included in the combined household income calculation for EHG and Family Grant means-testing.

What happens to my grant if I divorce after purchasing the flat?

Divorce does not trigger a grant clawback. The grant remains in the CPF OA of the respective owner(s) and normal CPF refund-on-sale rules apply. However, if the divorce results in one party retaining the flat and the other being bought out, the outgoing party’s CPF contributions — including grant amounts attributed to them — must be refunded at that point, with accrued interest. This is handled through the matrimonial asset division process, usually with the assistance of a family law solicitor.

Can I appeal for a higher grant if my income is irregular or I am self-employed?

Yes. HDB uses average gross monthly income over the 12 months preceding the application for means-testing. If your income is irregular — for example, you are a freelancer, commission-based worker, or recently returned to employment — HDB has a declared income process for the self-employed and an appeal mechanism for unusual circumstances. Supporting documents such as Notice of Assessment from IRAS, payslips, or CPF contribution history are typically required. Speak to an HDB branch officer early in the process if your income situation is non-standard.

Do the grants expire if I do not use them within a certain period?

CPF Housing Grants are credited into your CPF OA at the point of flat purchase — they are not a time-limited voucher. However, your eligibility to receive grants can change: if your income rises above the ceiling before application, or if you purchase a private property before your HDB flat, you may lose eligibility. The grant application must be submitted before you exercise the Option to Purchase, and the grant is disbursed only upon completion of the purchase.