Rental Income Tax Singapore 2026: Complete IRAS Guide for Landlords

If you own a property in Singapore and rent it out — whether an HDB flat, a private condominium, or a landed house — the rental income you receive is taxable. The Inland Revenue Authority of Singapore (IRAS) treats rental income as part of your total chargeable income for that Year of Assessment (YA), taxed at the prevailing personal income tax rates. Knowing how the system works, which expenses you may deduct, and when to file are not merely compliance obligations — they directly affect your net return on any investment property you hold.

This guide covers every aspect of rental income tax in Singapore for YA 2026 (income earned in 2025): what counts as rental income, allowable deductions, the tax rate schedule, filing deadlines, worked examples, and the most common landlord mistakes that trigger IRAS scrutiny.

- Rental income from Singapore properties is taxable; you must declare it in your annual income tax return.

- Net rental income = gross rent minus allowable deductions (mortgage interest, property tax, maintenance, insurance, agent fees for renewals).

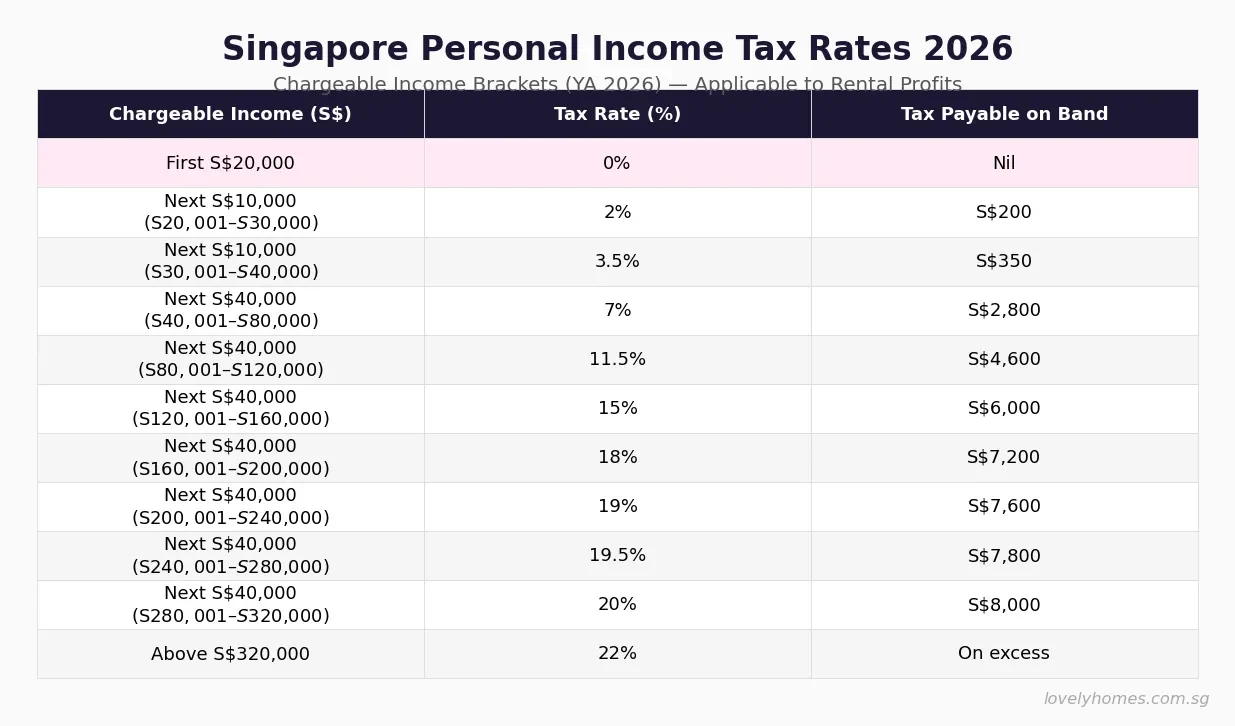

- Personal income tax rates for YA 2026 range from 0% (first S$20,000) to 22% (above S$320,000 chargeable income).

- Capital expenditure — renovations, improvements, furniture purchases — is not deductible; only revenue expenses qualify.

- IRAS filing deadline: 18 April 2026 (paper) / 18 April 2026 (e-filing via myTax Portal); penalties of up to 200% of unpaid tax may apply for non-declaration.

- Mortgage principal repayments are not deductible; only the interest component qualifies.

- Foreign rental income remitted to Singapore by tax residents is also taxable (with credit for foreign taxes paid).

- A property rented partially for personal use requires apportionment of expenses.

What Counts as Rental Income in Singapore

IRAS defines rental income broadly. It includes all amounts received or receivable from letting out a property in Singapore: monthly or annual rent, advance rent, premiums received for granting a lease, and service or facility charges included in the rental arrangement. If your tenant pays utilities as part of a gross rental arrangement and reimburses you, that reimbursement is also rental income.

What does not count: genuine security deposits that you hold in trust and will refund are not income. However, if a deposit is forfeited (e.g., the tenant breaks the lease), the forfeited amount becomes income in the year it is forfeited.

Rental income is assessed on a received basis for individuals — meaning you declare what you actually received (or were entitled to receive) during the calendar year 2025 for YA 2026, regardless of when the tenancy period technically falls.

The tax rates above are progressive and cumulative. A landlord whose only income is rental income of S$60,000 net does not pay 7% on the full S$60,000. Instead, the first S$20,000 attracts 0%, the next S$10,000 attracts 2% (S$200), the next S$10,000 attracts 3.5% (S$350), and the remaining S$20,000 attracts 7% (S$1,400) — a total tax of S$1,950, an effective rate of 3.25%.

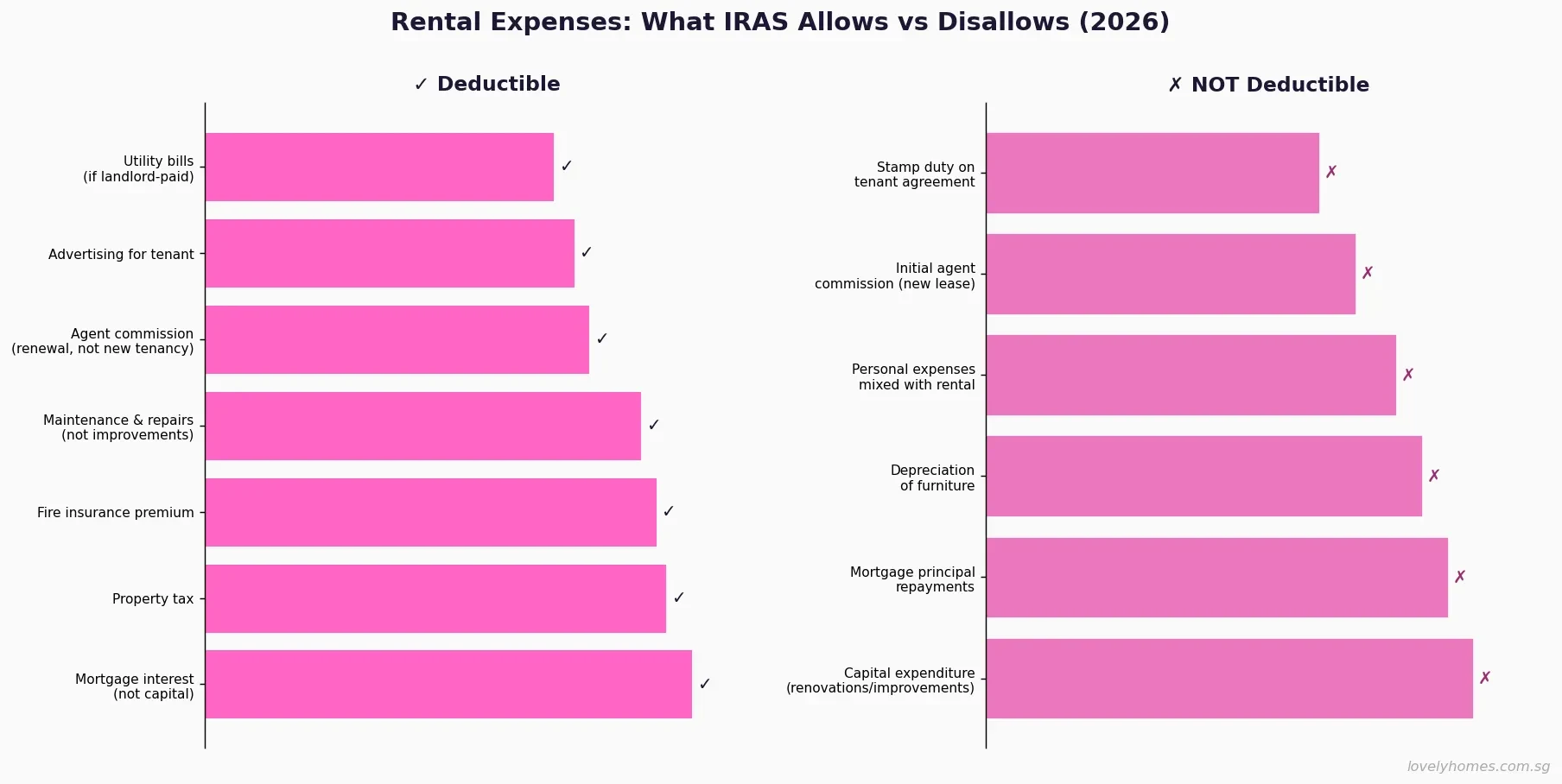

Allowable Deductions: What You Can Claim Against Rental Income

IRAS applies the revenue versus capital test to every expense. Revenue expenses — those incurred to earn rental income on an ongoing basis — are deductible. Capital expenses — those that create or improve a long-term asset — are not. The distinction sometimes requires careful analysis, especially for renovation and repair costs.

| Expense Category | Deductible? | Notes |

|---|---|---|

| Mortgage interest | ✓ Yes | Interest portion only; not principal repayment. Proportionate if property partly owner-occupied. |

| Property tax (annual) | ✓ Yes | The property tax bill from IRAS itself is deductible as a landlord expense. |

| Fire / home insurance premium | ✓ Yes | Premiums for insurance on the rented property are allowable. |

| Maintenance and repairs | ✓ Yes | Restoring to original condition (e.g., repainting, plumbing repairs) — revenue in nature. |

| Agent commission (renewal) | ✓ Yes | Renewal commissions are revenue expenses. First-time lease commissions may be disallowed. |

| Advertising costs | ✓ Yes | Costs of finding a tenant (online listings, print ads). |

| Furniture rental | ✓ Yes | Monthly rental of furniture provided to tenant is deductible; purchase of furniture is not. |

| Renovation and improvements | ✗ No | Capital in nature — creates new value. Not deductible regardless of amount. |

| Mortgage principal repayment | ✗ No | Capital repayment only reduces liability; does not generate income. |

| Furniture purchase | ✗ No | Capital expenditure; no depreciation allowance available to individuals. |

| Initial agent commission (new lease) | ✗ No | IRAS typically treats this as capital to secure the tenancy; not ongoing revenue. |

| Personal expenses | ✗ No | Any expenses not wholly and exclusively incurred to produce rental income. |

Repairs vs Improvements — The Critical Distinction

The boundary between a deductible repair and a disallowed improvement is one of the most contested areas in rental tax practice. IRAS looks at whether the work restores an asset to its original working condition (deductible) or improves it beyond its original state (capital, not deductible). Replacing a broken tile with an identical tile: deductible. Replacing worn carpet with hardwood flooring: capital. Repainting walls in the same colour: deductible. Knocking down a wall to open plan the kitchen: capital. When in doubt, document the original condition and the work scope, and retain quotes and invoices.

Mortgage Interest — Most Valuable Deduction for Leveraged Landlords

For landlords who financed their investment property with a bank loan, the interest component of each monthly mortgage instalment is deductible. You must obtain a mortgage statement from your bank showing the split between principal and interest for the year — this is typically included in your annual statement or available via the bank’s portal.

If you live in the property for part of the year and rent it out for the remainder, you must apportion the interest on a time basis. For example, if you rented the property for nine out of twelve months, only 9/12ths of the annual interest is deductible.

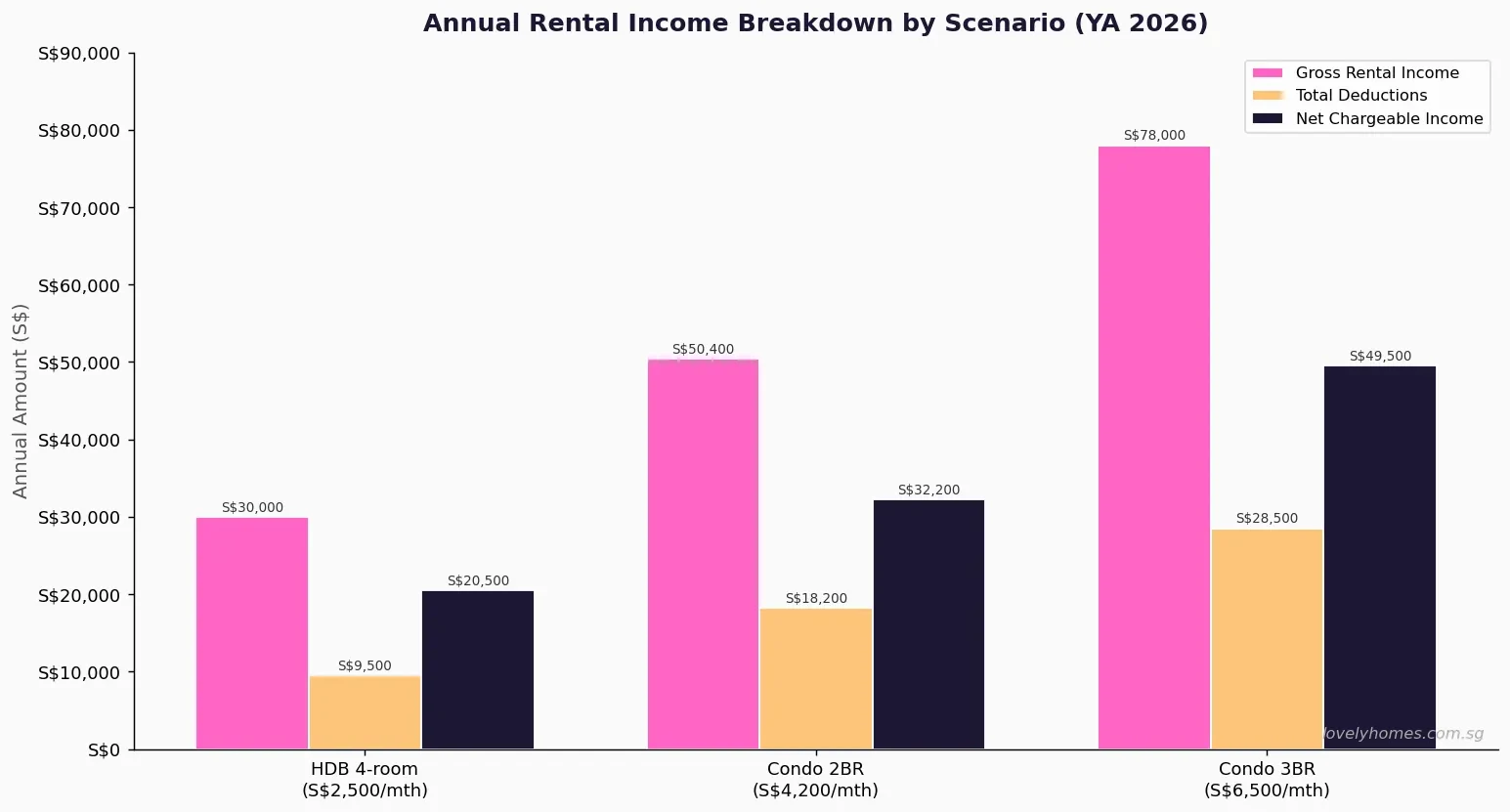

How Net Rental Income Is Calculated: Three Scenarios

The three scenarios above reflect a spectrum of Singapore rental situations. A modest HDB 4-room flat in a mature estate rented at S$2,500 per month (S$30,000 gross per year) might yield deductions of approximately S$9,500 (mortgage interest S$6,500, property tax S$1,800, fire insurance S$400, maintenance S$800), leaving net chargeable rental income of roughly S$20,500. A city-fringe condo 2-bedroom at S$4,200 per month carries higher deductions (larger mortgage, higher property tax) and nets approximately S$32,200. A 3-bedroom at S$6,500 per month nets roughly S$49,500 after all allowable deductions.

Worked Example: Mr Tan’s Investment Condo, YA 2026

Property: 2-bedroom condominium in Tampines, purchased March 2023 for S$1.2 million. Bank loan of S$840,000 at 3.0% p.a. fixed (2-year lock-in, now on floating SORA+0.9% ≈ 3.25% p.a.). Rented at S$3,800 per month for the full 12 months of 2025.

Step 1 — Gross Rental Income: S$3,800 × 12 = S$45,600

Step 2 — Allowable Deductions:

- Mortgage interest (from bank statement): S$26,000

- Annual property tax (owner-letting rate at AV S$26,400): approx. S$3,696

- Fire insurance premium: S$480

- Maintenance and service charge (tenant-occupied): S$0 (tenant pays MCST; landlord pays S$200/qtr sinking fund) = S$800

- Agent commission for renewal (year 2 renewal, half-month): S$1,900

- Total Deductions: S$32,876

Step 3 — Net Rental Income: S$45,600 − S$32,876 = S$12,724

Step 4 — Tax on Rental Income: Mr Tan also earns an employment income of S$120,000. His total chargeable income is S$120,000 + S$12,724 = S$132,724 (assuming standard personal reliefs of, say, S$20,000 apply, reducing to S$112,724 chargeable). Applying the YA 2026 brackets, his incremental tax on the S$12,724 rental profit (falling in the 11.5–15% marginal bands) is approximately S$1,850.

Key insight: Mortgage interest is the single largest deduction — without it, net rental income would have been S$38,724, and the incremental tax nearly four times higher. Landlords with high-interest-rate loans in 2025 (SORA-linked packages averaging 3.0–3.5%) benefit the most from the interest deduction.

Filing Obligations: How and When to Declare Rental Income

Rental income is declared in your annual income tax return via myTax Portal (IRAS). The filing deadline is 18 April each year for both paper and e-filing; for YA 2026 (income earned in calendar year 2025), you should have filed by 18 April 2026. If you missed the deadline, file immediately to minimise late penalties.

On your return, you will see a section titled Rental Income where you enter: the address of each rented property, gross rent received, and itemised deductions. IRAS may request supporting documents — keep mortgage statements, tenancy agreements, property tax bills, invoices for maintenance, and insurance schedules for at least five years.

| Obligation | Detail | Consequence of Non-Compliance |

|---|---|---|

| Declare rental income | Gross rent from all Singapore and foreign rental properties | Penalty up to 200% of unpaid tax; prosecution for wilful non-declaration |

| e-File via myTax Portal | Deadline: 18 April each YA | Late filing penalty; estimated assessment by IRAS if returns not filed |

| Retain records | 5 years from relevant YA | IRAS may disallow deductions if supporting documents unavailable |

| Notify IRAS of change in rental status | If property was previously owner-occupied | Incorrect owner-occupier property tax rates may trigger recovery |

Property Tax on Rented Properties — A Related but Separate Obligation

Property tax (administered by IRAS separately from income tax) applies to all Singapore properties. Owner-occupiers receive a concessionary progressive rate; landlords renting out their properties pay the higher non-owner-occupier rate on the Annual Value (AV) of the property. The non-owner-occupier residential property tax rates for 2026 range from 12% (first S$30,000 AV) to 36% (AV above S$90,000), reflecting the government’s ongoing property cooling stance.

Critically, the property tax bill itself is a deductible expense against your rental income for income tax purposes — effectively giving you a partial recovery of the property tax cost at your marginal income tax rate. For a landlord in the 15% income tax bracket, a S$5,000 property tax bill reduces rental income tax by S$750.

HDB Flat Rental — Additional Considerations

HDB flat owners who sublet their flat (or individual rooms) must first obtain HDB approval before renting. Once approval is granted, all rental income rules above apply equally — declare gross rent, claim allowable deductions, pay income tax on the net profit. The mortgage interest deduction is particularly significant for HDB owners who carry an outstanding HDB concessionary loan (2.60% p.a. as at May 2026), as the interest on that loan is deductible.

Note that HDB owner-occupier property tax rates apply to HDB flats irrespective of whether you sublet individual rooms (as opposed to the whole flat). If you rent out the entire flat, HDB requires you to rent a replacement home, and the non-owner property tax rate applies.

Foreign Rental Income for Singapore Tax Residents

If you are a Singapore tax resident and receive rental income from overseas properties (Malaysia, Thailand, Australia, the United Kingdom, and so on), that income is generally taxable in Singapore when it is remitted or deemed remitted to Singapore. Singapore does not tax foreign income that is kept offshore. However, once transferred to a Singapore bank account — even briefly — it is treated as remitted. You may claim a credit for foreign taxes paid on that income, subject to the double tax agreements Singapore maintains with over 80 countries.

What This Means for Singapore Landlords in 2026

Singapore’s rental income tax framework is moderate by global standards — the progressive rate structure, generous mortgage interest deduction, and property tax deductibility all reduce the effective tax burden for most landlords. However, three factors are squeezing margins in 2026: elevated mortgage rates (SORA-linked packages remain near 3.0–3.5%), higher non-owner-occupier property tax rates following the 2024–2025 AV revision cycle, and increased ABSD costs that raise the entry price for new investment purchases.

Net rental yields across Singapore private residential properties averaged 3.0–3.6% in Q1 2026 (industry data), down from the 4.0–4.5% range prevalent in 2022. For a leveraged landlord on a 75% LTV mortgage at 3.25% interest, the after-tax net yield may narrow to 1.5–2.5% depending on location and property type — compelling careful cash-flow modelling before any new acquisition.

What Might Come Next: Rental Tax Policy Outlook

This section is speculative and should not be relied upon for financial decisions. Singapore’s tax authorities have signalled no imminent changes to the personal income tax treatment of rental income. However, three developments are worth monitoring: (1) further property tax AV revisions for 2026–2027, which IRAS reviews annually and which directly affect the size of the deductible property tax bill; (2) any shifts in SORA-linked benchmark rates as the global monetary cycle evolves, affecting deductible mortgage interest; and (3) potential tightening of the regime for short-term rental platforms (Airbnb, Booking.com), which IRAS may subject to different rules if legislative changes follow proposed government reviews.

Frequently Asked Questions

Do I need to declare rental income if I only rent out one room?

Yes. IRAS requires you to declare all rental income, including income from subletting a single bedroom in your HDB flat or private property. The gross rent received for the room, less allowable deductions (apportioned based on the rented room’s floor area as a proportion of total floor area), must be reported in your annual income tax return. The apportionment approach applies to expenses like mortgage interest, property tax, and maintenance that cover the whole property.

Can I deduct renovation costs incurred before the tenant moved in?

Generally, no. IRAS treats renovation expenditure as capital expenditure, even if done to attract a tenant. The only exception is expenditure that constitutes genuine repair — restoring the property to its existing condition — rather than improvement. A fresh coat of paint before a new tenancy commences is typically allowable; a full kitchen overhaul or new bathroom suite is not. Retain full documentation of the pre- and post-renovation condition and all invoices.

My property was vacant for three months — can I still deduct mortgage interest for those months?

IRAS’s position is that you may deduct mortgage interest for vacant periods only if the vacancy arises because you are actively seeking a tenant (for example, the existing tenant has moved out and you are marketing the unit). If the property is vacant because you are occupying it for personal use or have no intention of renting during that period, the interest for those months is not deductible. Keep records of your rental marketing efforts (listing screenshots, agent correspondence) during any vacancy period.

How does IRAS know I have rental income if I do not declare it?

IRAS has multiple data-matching sources: HDB approval records for flat subletting, URA rental contract submissions (required for private properties since 2021), tenancy agreements registered with SLA, and property transaction data. IRAS also receives bank interest income information and can cross-reference rental deposits with landlord declarations. Undeclared rental income has led to IRAS audits resulting in penalties of up to 200% of underpaid tax. The risk of non-declaration significantly outweighs any short-term saving.

Can joint owners of an investment property both claim deductions?

Yes. Where a property is jointly owned, both owners must declare their respective share of the rental income and may each claim their proportionate share of the allowable deductions. If the property is held as tenants-in-common with unequal shares (for example, 60/40), each owner declares income and deductions in those proportions. Joint tenants (equal shares by default) split 50/50. Each owner files a separate income tax return.

Is rental income from Airbnb and short-term lets treated the same way?

For income tax purposes, yes — all rental income, whether from long-term tenancies or short-term platform bookings, is taxable. However, short-term rentals of private residential properties (less than three consecutive months per guest) are illegal in Singapore under URA regulations unless the property has a specific hotel or serviced apartment licence. HDB flats require a minimum rental period of six months per tenant. Accordingly, most Airbnb-style activity in Singapore private homes is legally prohibited. IRAS’s income tax rules would apply to any such income, but the underlying activity also exposes the owner to URA enforcement.

What if my rental income creates a loss (deductions exceed rent received)?

If your allowable deductions exceed your gross rental income for a year (producing a rental loss), IRAS generally does not allow that loss to be offset against other income sources such as employment income. Rental losses may in some circumstances be carried forward to offset future rental income from the same property. The rules on loss relief are complex and depend on whether the rental activity constitutes a trade — for most individual landlords, losses are quarantined within the rental income category. Consult a registered tax professional if you anticipate a rental loss position.

Related Articles

- ABSD Singapore 2026 — Complete Guide to Additional Buyer’s Stamp Duty

- Seller’s Stamp Duty (SSD) Singapore 2026 — Full Guide

- Rental Yield Singapore 2026 — Which Districts Perform Best?

- Property Tax Singapore 2026 — Owner-Occupier vs Non-Owner Rates

- Singapore Stamp Duty Guide 2026 — BSD, ABSD, SSD Calculator

- Using CPF to Buy Property in Singapore 2026

- HDB Flat Subletting Singapore 2026 — Rules, Approval and Process

Disclaimer

This article is intended for general informational purposes only and does not constitute tax, legal, or financial advice. Tax rules are subject to change; always verify current rates, thresholds, and filing requirements directly with the Inland Revenue Authority of Singapore (IRAS) at iras.gov.sg and the Monetary Authority of Singapore (MAS). Readers with specific tax questions regarding their rental properties should consult a qualified Singapore tax professional or a licensed financial adviser. Figures and examples used are illustrative and may not reflect your individual circumstances.

Click anywhere or press Esc to close