Jurong East Neighbourhood Guide Singapore 2026: Property Prices, JLD Uplift, Schools and Investment Outlook

Quick Answer: Jurong East 2026 — What Buyers and Investors Need to Know

- Location: District 22 (D22), Outside Central Region (OCR). Well-connected on the East-West Line (EWL) and the incoming Jurong Region Line (JRL, ~2028).

- JLD catalyst: Jurong Lake District (JLD) — 360 hectares — is Singapore’s largest mixed-use development outside the CBD. The URA has designated it as a second Central Business District, with URA’s 2H2026 GLS programme including a landmark JLD white site for tender in July 2026.

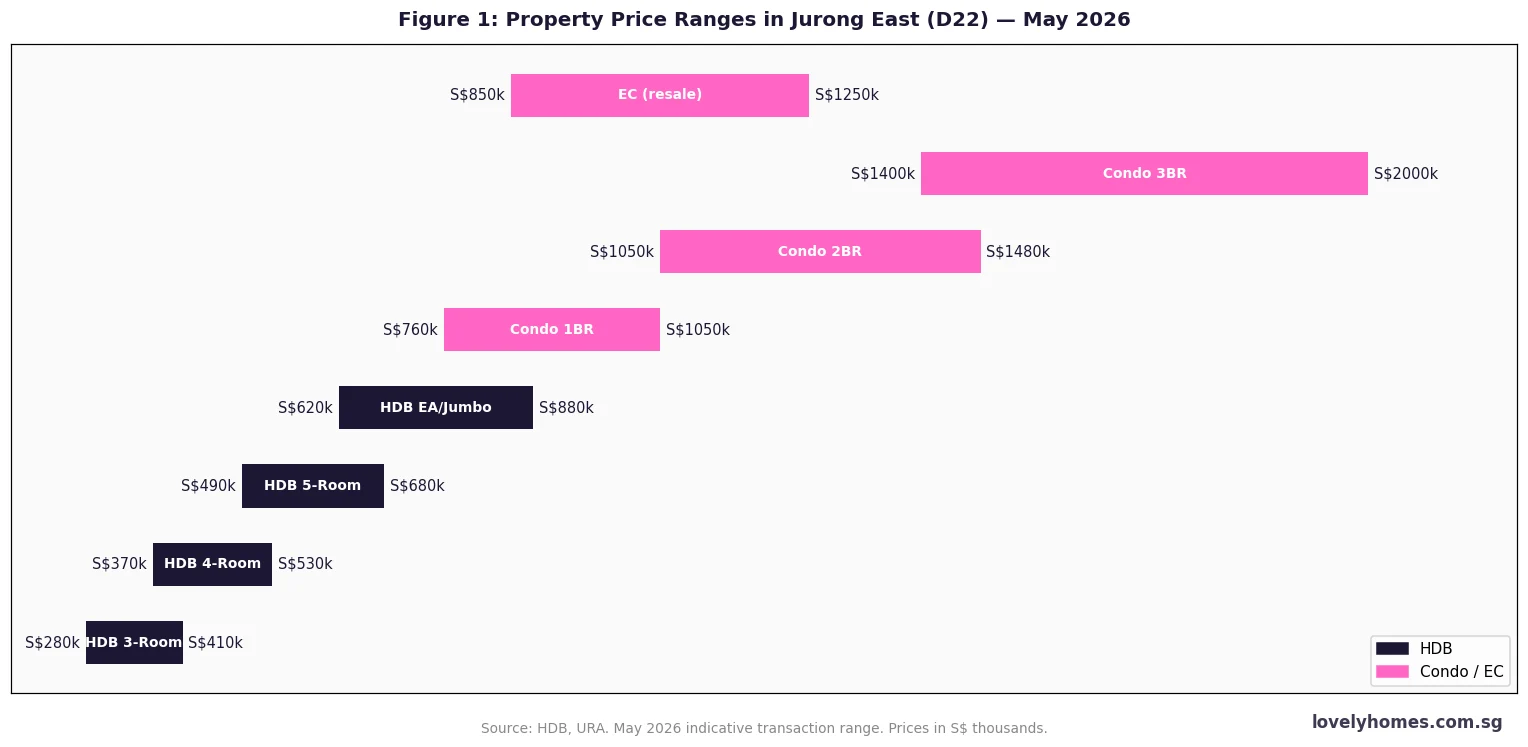

- Property prices: HDB 4-room resale flats trade at S$370,000–S$530,000; OCR condos at S$1,050,000–S$1,480,000 (2BR) as at May 2026.

- Rental yields: Condos in D22 yield 3.4–3.7% gross; HDB flats deliver higher at 4.3–5.1%.

- 5-year HDB price growth: approximately +9.5% for 4-room flats — broadly in line with the national OCR trend.

- JRL uplift thesis: the opening of JRL Phase 1 from approximately 2028 (J1 Jurong East as the key interchange) historically correlates with 8–15% price appreciation in proximate properties based on past MRT openings.

- Retail and lifestyle: three major malls — JEM, Westgate, and IMM — plus Jurong Point, make Jurong East one of Singapore’s most self-contained suburban retail hubs.

- Education: Ngee Ann Polytechnic and proximity to NUS and NTU create solid rental demand from students and academic professionals.

Jurong East: Location, Planning Context and Why It Matters

Jurong East is a mature HDB town in Singapore’s west, administered under District 22 of the Outside Central Region (OCR). It sits at the intersection of two major MRT lines — the East-West Line (EWL) at Jurong East station (EW24) and the future Jurong Region Line (JRL) at J1 — making it the gateway interchange for the western catchment. It borders Jurong West to the north-west, Clementi to the east, and Bukit Batok to the north.

What sets Jurong East apart from other OCR towns is the Jurong Lake District (JLD). In its Master Plan, the Urban Redevelopment Authority (URA) has designated the 360-hectare JLD — stretching from Jurong East MRT station to the Chinese and Japanese Gardens — as Singapore’s second CBD. The vision encompasses 100,000 new jobs, 20,000 new homes, a new integrated tourism development, and a network of car-lite streets around Jurong Lake Gardens. The June 2026 Government Land Sales programme confirmed a major JLD white site for tender in July 2026, capable of accommodating up to 1,200 residential units, at least 40,000 sqm of office space, and 44,000 sqm of complementary uses — marking a tangible next step in JLD’s realisation.

For property investors, the JLD story represents a medium-to-long-term structural re-rating of Jurong East and its immediate environs. The comparison most frequently drawn is to the Marina Bay Financial Centre development: Marina Bay residential properties within walking distance of the financial district saw significant price appreciation over the 2008–2018 development period. If JLD develops as planned — and the government’s investment in the JRL, Jurong Lake Gardens, and GLS pipeline suggests strong commitment — Jurong East’s pricing relative to the OCR average could narrow meaningfully over the next decade.

Connectivity: MRT and Public Transport

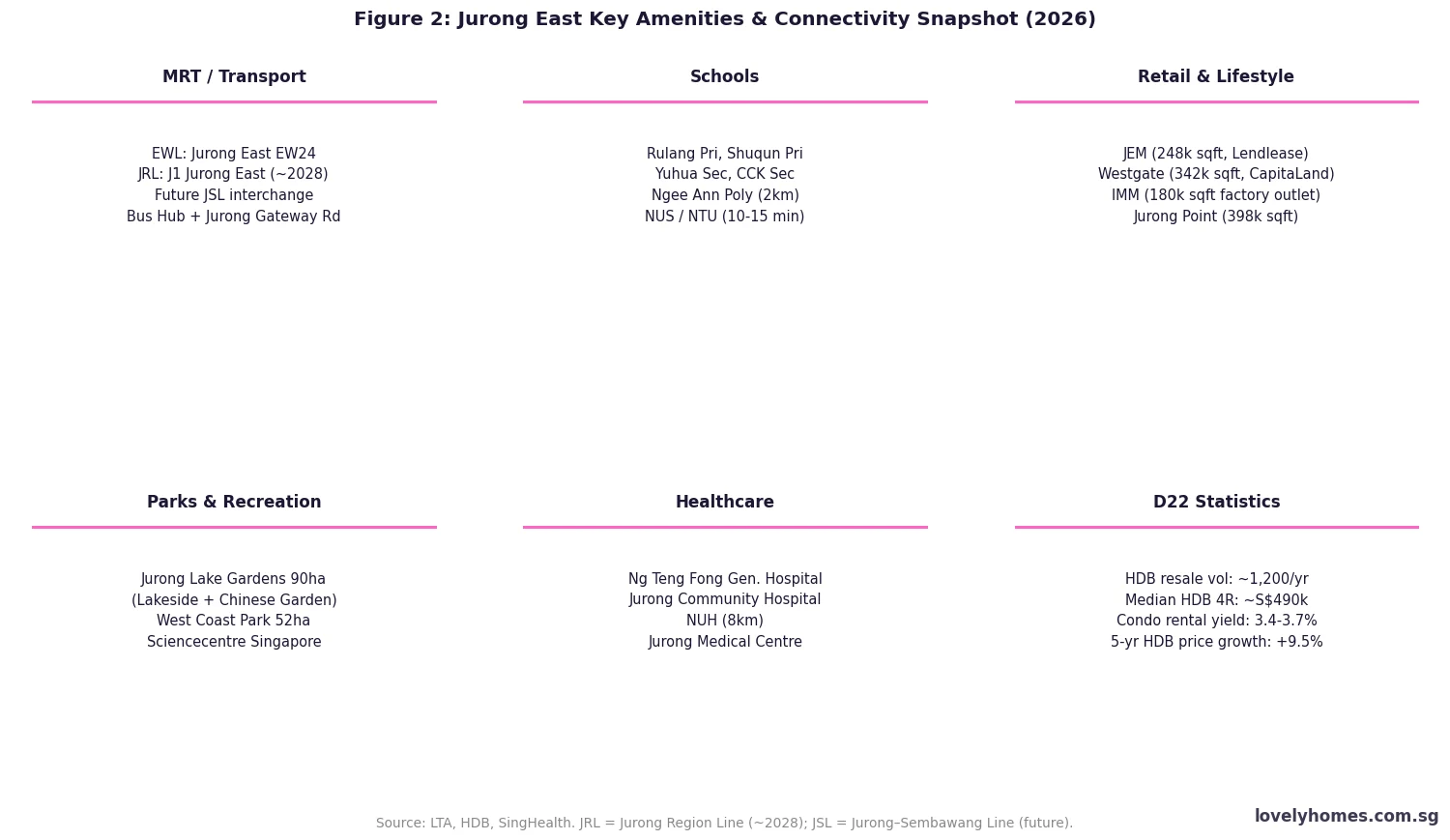

Jurong East’s transport infrastructure is already strong and improving. The East-West Line (EWL) connects Jurong East (EW24) to Raffles Place in approximately 32 minutes and to Changi Airport via transfer in around 50 minutes. The station is also served by a major integrated bus interchange handling cross-island routes. The Jurong Region Line (JRL), targeted to open in phases from approximately 2028, designates Jurong East as its J1 station — the key interchange with the EWL. The JRL’s three branches (Boon Lay Branch, Choa Chu Kang Branch, and Tengah Branch) will connect an estimated 150,000 residents in the Tengah, Choa Chu Kang, and Boon Lay corridors to Jurong East, substantially increasing footfall through the precinct. A future Jurong–Sembawang Line (JSL) — still in planning — has been identified in URA’s Long-Term Plan as eventually running through Jurong East, offering a cross-island link to the north.

Driving connectivity is similarly well-served. The Ayer Rajah Expressway (AYE), Pan Island Expressway (PIE), and Bukit Timah Expressway (BKE) intersect near Jurong East, providing fast access to the CBD (approximately 20–25 minutes off-peak), Changi (approximately 30–35 minutes), and the Second Link to Malaysia at Tuas. The proximity to the causeway is an important feature for Jurong East’s professional tenant pool, which includes engineers, logistics managers, and workers at Jurong Island’s petrochemical complex.

Property Market: Prices, Types and Investment Profiles

Jurong East’s residential stock is predominantly HDB. The town has a well-established mix of 3-room, 4-room, 5-room, and executive apartment (EA) flats spread across estates like Yuhua, Toh Guan, Bukit Batok East (boundary), and the Jurong East town centre precincts. HDB 4-room resale flats in Jurong East currently trade at approximately S$370,000–S$530,000, with well-positioned units near Jurong East MRT or in high-floor blocks commanding the upper range. 5-room flats trade at S$490,000–S$680,000; executive apartments at S$620,000–S$880,000.

The private condominium supply in D22 is relatively thin compared to adjacent districts, which itself supports pricing. Key developments include J Gateway (99-year leasehold, 738 units, directly above Jurong East MRT), valued at approximately S$1,400–1,600 psf as at mid-2026; Vision (99-year, 294 units, Boon Lay Way/Jurong East Ave 1 corner), valued at approximately S$1,100–1,250 psf; and Lake Grandeur (99-year, 396 units, Jurong Lake area), valued at approximately S$1,050–1,200 psf. The scarcity of private supply in D22 — no new private residential GLS site in the immediate Jurong East precinct since J Gateway’s site was awarded in 2012 — means that the JLD GLS pipeline will be the first significant new supply in over a decade. New-build prices from the JLD white site (if awarded and launched) are expected to set new benchmarks for D22 pricing, potentially in the S$2,200–2,800 psf range based on comparable city-fringe mixed-use projects.

The EC resale market is represented primarily by Westwood Residences (EC, 480 units, Jurong West Ave 1, privatised 2024) trading at S$850,000–S$1,250,000, offering post-privatisation investors a mid-point between HDB and full private pricing.

Schools, Education and Family Amenities

Jurong East is well-served for families at all school levels. Within 2 km of the town centre, primary schools include Rulang Primary School (well-regarded, popular in the primary-one registration priority exercise), Shuqun Primary School, Yuhua Primary School, and Fuhua Primary School. Secondary schools include Yuhua Secondary and Chua Chu Kang Secondary. At the tertiary level, Ngee Ann Polytechnic is approximately 2 km east (Clementi Road), while NUS Kent Ridge is approximately 8 km and Nanyang Technological University (NTU) is approximately 10–15 minutes by bus or future JRL. The student rental demand from NTU in particular is a significant driver of D22 condo rental volume, particularly for 1-bedroom and small 2-bedroom units.

For retail, Jurong East is exceptional by suburban Singapore standards. The Jurong Gateway commercial precinct contains three integrated malls: JEM (248,000 sqft, Lendlease REIT), Westgate (342,000 sqft, CapitaLand), and the adjacent IKEA Tampines equivalent replaced by IMM (180,000 sqft factory outlet, Lendlease REIT). A further 4 km down the EWL, Jurong Point (398,000 sqft, Singapore’s largest suburban mall) serves the Boon Lay/Jurong West catchment. The combined retail density within 5 km of Jurong East MRT is among the highest of any OCR town in Singapore.

Healthcare is anchored by Ng Teng Fong General Hospital (NTFGH) — the 700-bed regional hospital replacing the former Alexandra Hospital Jurong for the western region, opened in 2015 — and the co-located Jurong Community Hospital (JCH) (228 beds for intermediate and long-term care). National University Hospital (NUH) is approximately 8 km via AYE, and the Jurong Medical Centre serves polyclinic-level primary healthcare for the precinct.

Rental Market and Investment Case

The Jurong East rental market is underpinned by three distinct tenant pools. First, NTU/NGP students and academic professionals — particularly relevant for 1BR and studio condos, commanding rents of approximately S$2,400–3,200/month for 1BR units. Second, Jurong Island and western industrial workers — engineers, petrochemical and logistics professionals who prefer to rent in the western corridor to minimise their commute. Third, expats from Malaysian corporates and cross-border professionals — Jurong East’s proximity to the Tuas Second Link (approximately 25 minutes by car) attracts a segment of Malaysian professionals and senior managers who commute daily or bi-weekly.

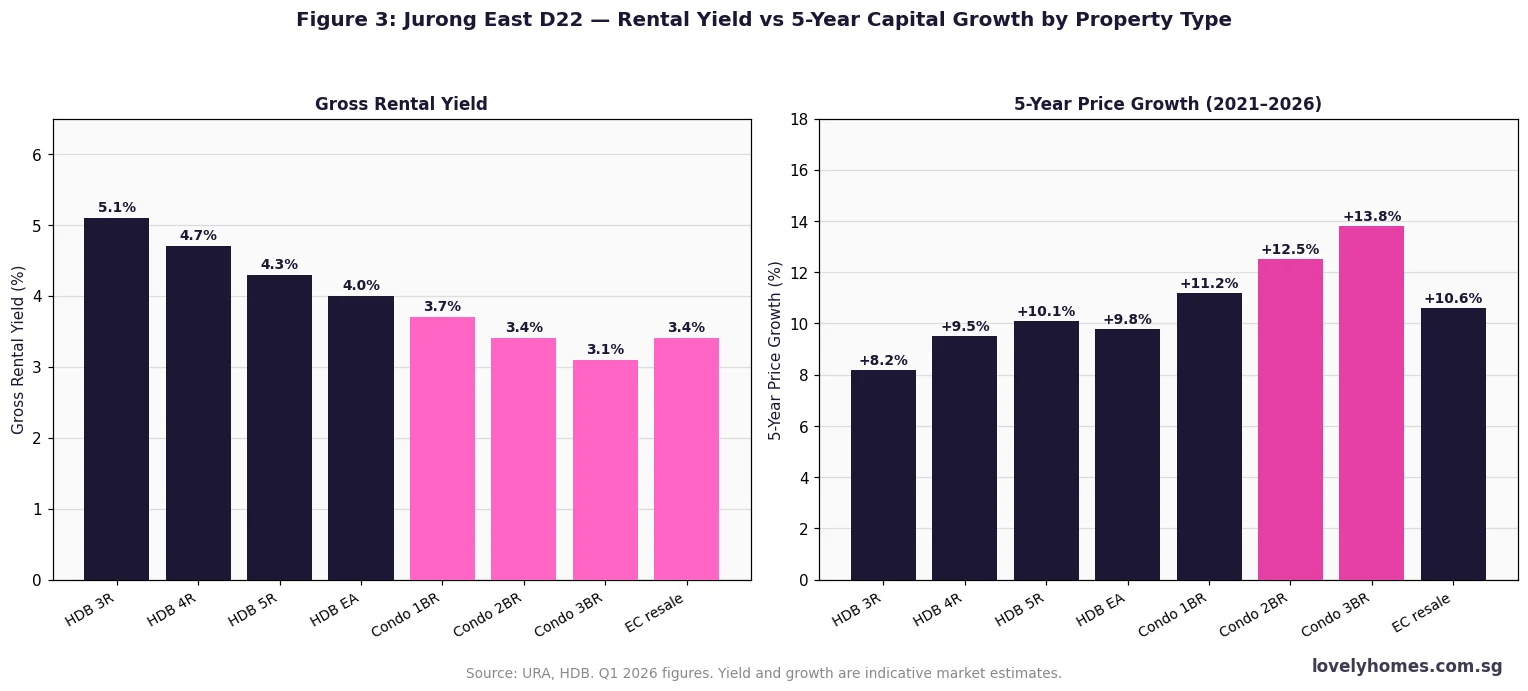

As at Q1 2026, gross rental yields in D22 are approximately: HDB 3-room 5.1%, HDB 4-room 4.7%, HDB 5-room 4.3%, condo 1BR 3.7%, condo 2BR 3.4%, EC resale 3.4%. These are modest compared to D11 medical cluster or D19 student-driven markets, but they are supported by genuine occupational demand rather than speculative vacancy churn. Vacancy rates in D22 private condos are estimated at approximately 4–6%, consistent with the national OCR private average of approximately 5% in Q1 2026.

Summary: Jurong East Investment Snapshot by Property Type

| Property Type | Price Range | Gross Yield | 5-Yr Growth | Tenure |

|---|---|---|---|---|

| HDB 3-Room | S$280k–S$410k | ~5.1% | +8.2% | 99yr (HDB) |

| HDB 4-Room | S$370k–S$530k | ~4.7% | +9.5% | 99yr (HDB) |

| HDB 5-Room / EA | S$490k–S$880k | ~4.2% | +9.9% | 99yr (HDB) |

| Condo 1BR | S$760k–S$1,050k | ~3.7% | +11.2% | 99yr (leasehold) |

| Condo 2BR | S$1,050k–S$1,480k | ~3.4% | +12.5% | 99yr (leasehold) |

| Condo 3BR | S$1,400k–S$2,000k | ~3.1% | +13.8% | 99yr (leasehold) |

| EC (resale) | S$850k–S$1,250k | ~3.4% | +10.6% | 99yr (privatised) |

Worked Example: First-Time Buyer Purchasing a Jurong East HDB 4-Room Resale

Case Study — Mr & Mrs Lim, Singapore Citizens, first-time HDB buyers

Household profile: Mr & Mrs Lim, both Singapore Citizens, joint gross income S$8,500/month. First-time HDB buyers (no prior property ownership). Target: purchase a 4-room HDB resale flat in Jurong East at S$490,000.

Grants: Joint income S$8,500/month qualifies for Enhanced Housing Grant (EHG) of S$25,000 (family income S$7,001–9,000 bracket); Proximity Housing Grant (PHG) of S$30,000 if purchasing within 4 km of parents. Total grants: S$55,000.

Effective purchase price after grants: S$490,000 − S$55,000 = S$435,000 (for CPF/loan computation purposes).

Stamp duties: BSD on S$490,000 = (S$180,000 × 1%) + (S$180,000 × 2%) + (S$130,000 × 3%) = S$1,800 + S$3,600 + S$3,900 = S$9,300. ABSD: nil (SC first property).

Financing: HDB Loan LTV 80% on S$490,000 = S$392,000 loan @ 2.6% p.a. 25 years → monthly instalment S$1,776. MSR check: S$1,776 ÷ S$8,500 = 20.9% — within 30% PASS.

Upfront cash required: 5% cash downpayment on S$490,000 = S$24,500. BSD S$9,300 (payable via CPF). Legal/valuation ~S$2,500. Total cash outlay: approximately S$27,000.

Monthly household finances: Mortgage S$1,776 (20.9% MSR) + conservancy charges ~S$80 + property tax ~S$120 = approximately S$1,976/month total property cost. At S$8,500 gross income, net take-home after CPF (employee contribution 20% = S$1,700) is approximately S$6,800/month, leaving comfortable headroom.

Why Jurong East Matters to Property Investors in 2026

The JLD story is the most compelling single narrative in Singapore’s western residential market. No other OCR town has a comparable government-backed catalyst: a designated second CBD, a new MRT interchange (JRL J1), a landmark GLS white site under active tender, and the surrounding Jurong Lake Gardens — Singapore’s third national garden after Botanic Gardens and Gardens by the Bay — as a lifestyle anchor. Comparable transformations in Singapore’s history — the Marina Bay build-out from 2005 to 2018, the Dhoby Ghaut Circle Line opening in 2009 — consistently delivered residential price appreciation in the 8–20% range over a 3–5 year period following the key infrastructure milestones.

The practical investment case for most buyers today is straightforward: entry-level pricing in D22 remains accessible by OCR standards, yields are supportable, tenant demand is real, and the infrastructure spend committed by the government is unprecedented for any suburban town. The key risks are timeline slippage (JLD’s full development has a 20–30 year horizon) and interest rate sensitivity (a sustained SORA above 3.5% would compress condo yields to less than 2% net, making servicing costs uncomfortable).

What Might Come Next for Jurong East

The July 2026 JLD white site tender result will be the single most watched event in the Singapore western property market for the second half of 2026. A high bid — say S$1,800+ psf ppr — would signal developers’ confidence in JLD pricing and likely prompt a re-rating of existing D22 private condos. A below-expectation result could dampen enthusiasm but would not alter the structural story. The JRL’s opening in phases from approximately 2028, with J1 Jurong East as the key interchange, is widely expected to be the catalytic event for near-station premium appreciation. Investors monitoring the situation should also watch the Tengah New Town development (42,000 HDB flats planned, JRL-served) — as Tengah launches into the market from 2026 onwards, it will compete with Jurong East for western upgrader demand and may moderate Jurong East’s immediate-term HDB resale momentum.

Frequently Asked Questions: Jurong East Neighbourhood Guide 2026

Is Jurong East a good area to buy property in 2026?

Jurong East is one of the most strategically positioned OCR towns in Singapore for medium-to-long-term investors in 2026. The JLD development gives it a structural demand catalyst that most other OCR towns lack. Entry prices remain accessible (HDB 4-room resale at S$370k–S$530k; condo 2BR at S$1.05M–S$1.48M), yields are decent for the OCR, and the JRL interchange opening (~2028) provides a near-term price catalyst. The main caveat is that JLD is a very long-horizon project — buyers expecting a 1–2 year flip will likely be disappointed. The investment case is most compelling for buyers with a 5–10 year holding horizon who are simultaneously living in or near the area.

Which MRT stations serve Jurong East?

Jurong East is currently served by Jurong East MRT (EW24) on the East-West Line (EWL). It is an interchange station with a major bus hub. From July 2028 onwards (approximate), Jurong East will also be served by J1 Jurong East on the Jurong Region Line (JRL) — making it a two-line interchange. The JRL will connect Jurong East north to Choa Chu Kang and west to Boon Lay, significantly expanding the commuter catchment. A future Jurong–Sembawang Line (JSL) is referenced in URA’s Long-Term Plan Review but has no confirmed timeline. The EWL already connects Jurong East to the CBD (Raffles Place EW14) in approximately 32 minutes without a transfer.

Can PRs and foreigners buy property in Jurong East?

Singapore Permanent Residents (PRs) can purchase HDB resale flats in Jurong East subject to HDB eligibility criteria (PR households, no concurrent private property ownership, etc.) with a 5% ABSD on their first property. PRs cannot purchase new HDB BTO flats. For private condos (J Gateway, Vision, Lake Grandeur, Westwood Residences EC post-privatisation), PRs pay 5% ABSD on their first property and 30% on a second. Foreign nationals (non-PR) cannot own HDB flats at all, but may buy private condos at 60% ABSD. Given the 60% ABSD, foreign individual ownership of Jurong East condos is rare and concentrated among those using Singapore property as a long-term currency-diversification vehicle rather than a rental yield play.

What are the best condos to buy in Jurong East?

J Gateway (EW24 directly above station, 738 units, 99yr) is the most frequently cited for its unrivalled transport connectivity — with Jurong East MRT directly underfoot, rental demand from students and young professionals is among the strongest in D22. Vision (Boon Lay Way, 294 units, 99yr) offers a quieter residential setting with slightly lower psf and reasonable EWL access. Lake Grandeur (Jurong Lake area, 396 units, 99yr) is the best-positioned for JLD appreciation — walking distance to Jurong Lake Gardens and the future JLD commercial precinct. For buyers prioritising JLD capital upside over immediate rental yield, Lake Grandeur and the upcoming JLD GLS developments (once launched) represent the strongest bet. Note that all major D22 condos are leasehold (99-year), which affects long-term lease decay considerations for buyers with 30-year horizons.

How does Jurong East compare to Clementi and Bukit Batok for investment?

Clementi (D05 RCR boundary) benefits from NUS proximity, excellent CCL/EWL connectivity, and freehold land scarcity — it typically commands a 20–30% price premium over Jurong East for comparable property types. However, that premium already prices in much of the educational and transport uplift. Bukit Batok (adjacent OCR, D23) is more affordable — HDB 4-room resale at S$310,000–S$450,000 — and will benefit from the JRL Bukit Batok station, but lacks the JLD commercial anchor and has lower condo supply depth. For investors balancing yield, entry price, and structural upside, Jurong East sits in a superior position to Bukit Batok and offers better long-term appreciation potential than either D23 or the already-appreciated Clementi market.

Is there HDB BTO supply available in Jurong East in 2026?

Jurong East’s established HDB stock means BTO supply within the immediate town centre is limited. The 2026 HDB BTO exercise does not include a dedicated Jurong East precinct; the nearest June 2026 BTO projects are in Jurong West and Clementi. The primary acquisition route into Jurong East public housing is therefore the HDB resale market, which offers greater flexibility on flat type, floor, and move-in timeline but at market price (no BTO subsidy). Tengah New Town — a 42,000-flat new town directly adjacent to the JLD catchment — is receiving BTO allocations from 2024 onwards and represents an alternative for buyers seeking subsidised entry into the western corridor’s growth story, though at the cost of a longer wait time and MOP obligation.