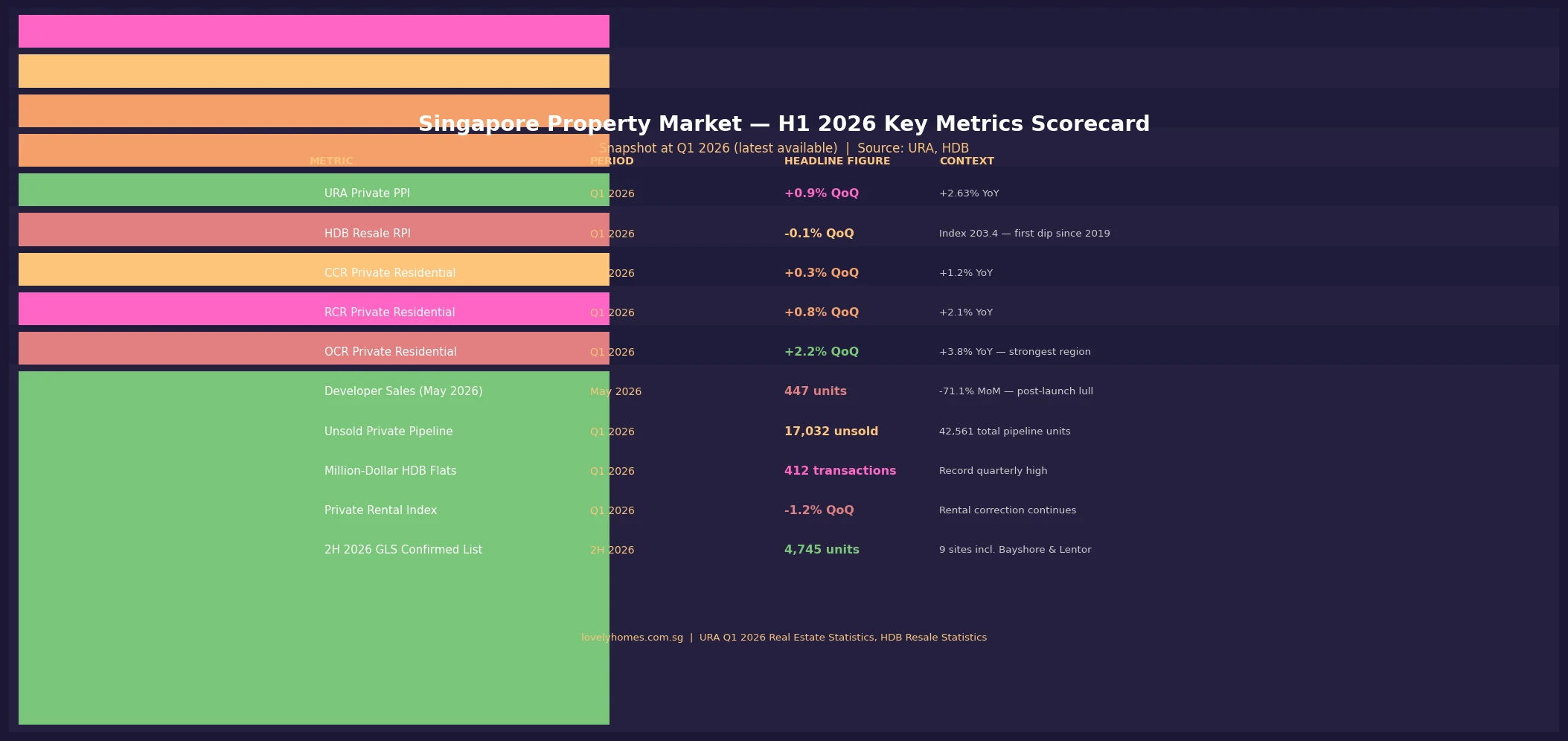

Private residential prices rose 0.9% QoQ and 2.63% YoY in Q1 2026, with the Outside Central Region (OCR) leading at +2.2% QoQ — price growth is positive but moderating.

HDB resale recorded its first quarterly dip (-0.1% QoQ) since Q2 2019; index sits at 203.4. Not a crash — more of a pause after a five-year run.

2H 2026 GLS launches 9 confirmed-list sites (4,745 units), adding meaningful supply to OCR and RCR. Pricing discipline from developers is expected.

Key risk: interest rates remain elevated at 3.0–3.5% for bank mortgages; affordability is stretched for many first-time buyers.

Key catalyst: any US Federal Reserve rate cut signals would unlock significant pent-up demand — watch the September and December 2026 Fed meetings.

For buyers: fundamentals remain sound — Singapore’s employment is near-full, rental demand supports investment yield, and supply is finite. Timing the market is less reliable than time in the market.

URA Q2 2026 Flash Estimates are expected in early July 2026 and will be the next major data point.

H1 2026 in Review: Where the Singapore Property Market Stands

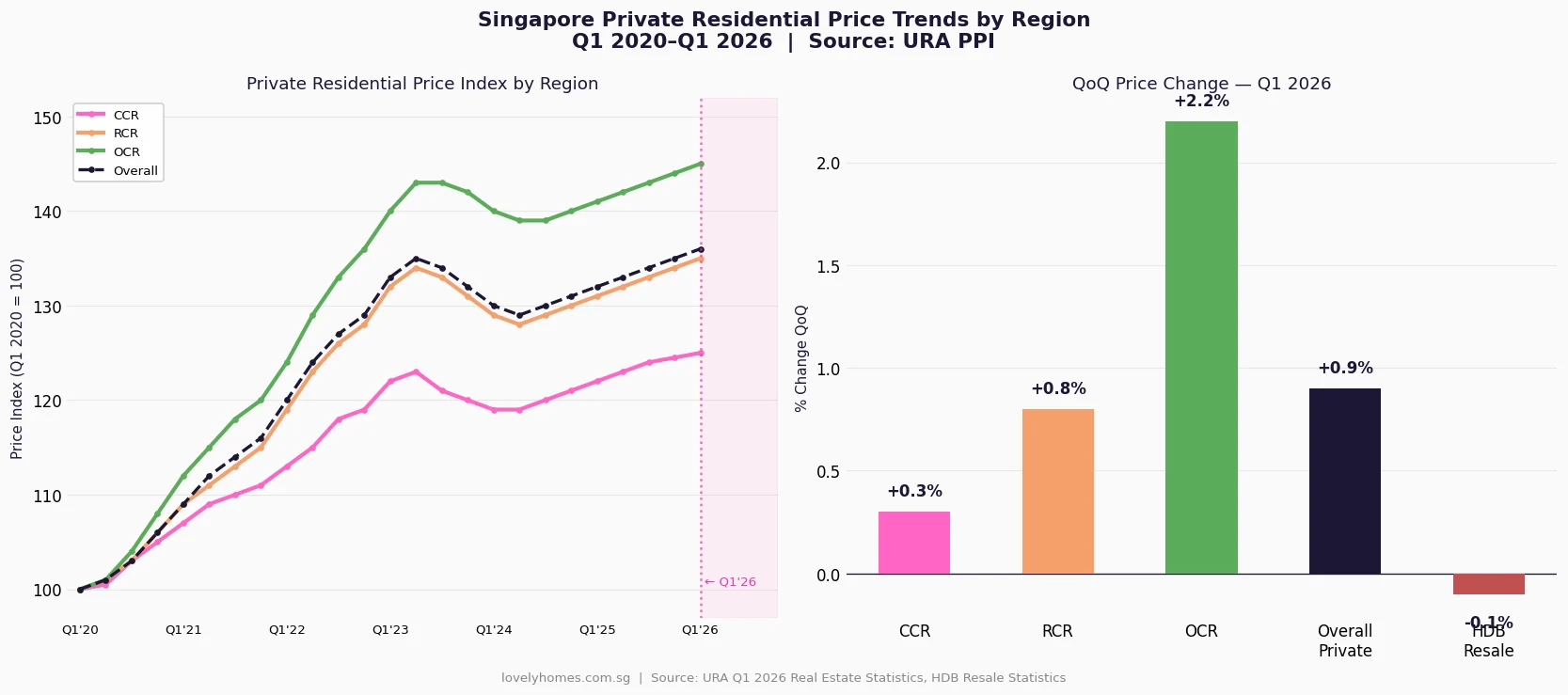

As the calendar turns to the second half of 2026, Singapore’s property market presents a nuanced picture. Private residential prices continued their gradual upward trajectory in Q1 2026, with the Urban Redevelopment Authority (URA) reporting a Property Price Index (PPI) increase of 0.9% quarter-on-quarter — a modest but consistent gain that extends a trend stretching back to the post-pandemic recovery that began in mid-2020. On a year-on-year basis, the private residential index is up 2.63%, a pace that is firm but well below the double-digit growth seen during the post-pandemic surge of 2021 to 2023.

The Housing Development Board’s Resale Price Index (RPI), however, told a slightly different story. At 203.4 in Q1 2026, the HDB resale market recorded a 0.1% quarterly decline — the first such dip since Q2 2019. This is not alarming in isolation: the index had surged more than 54% since its 2019 trough, and a modest pause is consistent with natural market digestion. What it does signal is that the exceptional run of HDB resale price appreciation is transitioning into a more measured phase.

Figure 1: Singapore Property Market H1 2026 Key Metrics Scorecard — URA Q1 2026 Real Estate Statistics and HDB Resale Statistics.

Private Residential Market: A Three-Speed Story

The defining characteristic of Singapore’s private residential market in 2026 is regional divergence. The three planning zones administered by URA — the Core Central Region (CCR), Rest of Central Region (RCR), and Outside Central Region (OCR) — have performed at markedly different speeds in 2026.

The OCR is the undisputed pace-setter. A 2.2% quarterly gain in Q1 2026, following similar momentum in late 2025, reflects genuine demand from HDB upgraders — a cohort whose Minimum Occupation Period (MOP) clears in waves and who target mass-market new launches in the S$1.3M–S$1.8M range. The 2H 2026 GLS programme deliberately concentrates supply here (Tampines Street 94, Bayshore Road), which should moderate any further sharp price acceleration without causing a price correction.

The RCR recorded 0.8% QoQ growth — solid mid-field performance driven by a mix of first-time private buyers, professionals, and some foreign-related buying in the city-fringe. River Valley Green Parcel C (awarded June 2026 at a top bid of approximately S$1,730 psf ppr) is the headline indicator of developer confidence in this zone.

The CCR grew just 0.3% QoQ, a subdued reading that reflects several headwinds: the 60% Additional Buyer’s Stamp Duty (ABSD) on foreigners that has been in place since April 2023 continues to suppress international transaction volumes; and the global macro uncertainty discussed in the risk section below has weighed on ultra-high-net-worth discretionary buying. That said, CCR is not in distress — it remains a long-term beneficiary of Singapore’s family office growth and wealth inflows.

Figure 2: Singapore Private Residential Price Index by Region (Q1 2020–Q1 2026) and QoQ Change for Q1 2026. Source: URA Q1 2026 Real Estate Statistics.

HDB Resale Market: A Healthy Pause, Not a Reversal

Singapore’s HDB resale market has been one of the defining investment stories of the 2020s. From a low point in 2019 (RPI ≈ 132), prices surged to an index of 203.4 by Q1 2026 — a 54% cumulative increase. The Q1 2026 dip of 0.1% QoQ is, in that context, the market catching its breath after an exceptional run rather than a structural reversal.

Two counterintuitive data points reinforce this view. First, million-dollar HDB transactions reached a record quarterly high of 412 in Q1 2026 — indicating that at the premium end of the resale market (large mature-estate flats, high-floor units in sought-after towns), demand remains fierce. Second, overall HDB resale transaction volumes for Q1 2026 remained healthy, with four-room flats accounting for the largest share (approximately 2,690 transactions in Q1 2026 alone) at a median price of around S$575,000.

For 2H 2026, the HDB resale market is likely to remain range-bound rather than sharply appreciating or correcting. MOP cohorts from the 2016–2019 BTO launches are gradually clearing, releasing units back to the resale market — but supply from this channel is relatively thin compared to the 2013–2016 peak cycle. Demand remains supported by couples who cannot access BTO (due to income ceiling, citizenship mix, or urgency) and Permanent Residents who remain ineligible to buy BTO directly.

Developer Sales and the New Launch Pipeline

Developer sales activity is the indicator most directly shaped by new launch timing. The monthly data tells a story of feast and famine: January to April 2026 saw 1,120, 895, 1,348 and 1,548 units sold respectively — solid months driven by a cluster of project launches. May 2026 crashed to 447 units (-71.1% month-on-month), not because demand evaporated, but because there were few projects launching that month.

The pipeline going into 2H 2026 remains substantial. URA data shows 17,032 unsold units in the private pipeline as of Q1 2026 (total pipeline including units not yet launched: 42,561). The 2H 2026 GLS Confirmed List adds nine further sites including Lentor Gardens Parcel A and B, Bayshore Road, Tampines Street 94, and an EC site at Jurong East. These launches are phased across 2H 2026 into 2027, so the impact on completed supply will be felt primarily in 2028–2030.

Singapore’s private residential rental market began correcting in 2024 after a record two-year surge and that correction extended into 2026. The URA rental index fell 1.2% QoQ in Q1 2026, following declines across 2024 and 2025. In absolute terms, rents remain significantly above their pre-pandemic levels — a 2BR in D15 that rented for S$2,800/month in 2019 may still command S$4,200–S$4,800/month in 2026 depending on specification — but the exceptional post-pandemic pricing has normalised.

For investors, this rental correction compresses gross yields. A S$1.5M 2BR in the RCR yielding S$4,500/month gross generates a gross yield of approximately 3.6%, which is broadly comparable to bank deposit rates in 2026. Net yield after management fees, property tax, and maintenance is lower — making the case for property investment in 2026 primarily a capital appreciation thesis rather than a pure income play.

2H 2026 Market Outlook Summary

Segment

Base Case

Bull Case

Bear Case

Private Residential (Overall)

+1%–2% for full year 2026

+3%–4% if rates ease and demand recovers

Flat to -1% if global recession deepens

OCR (Mass Market)

Continues outperforming; +2%–3% YoY

+4%–5% with strong HDB upgrader demand

Supply pressure from GLS launches moderates gains

RCR (City Fringe)

Steady +1%–2% YoY

+3% with new launch interest

Flat if affordability ceiling is hit

CCR (Core Central)

Sideways to +1%; foreign buyer ABSD drag

+2%–3% if ABSD reviewed or wealth inflows surge

-1%–2% if global HNW sentiment deteriorates

HDB Resale

±0.5% QoQ; range-bound in H2

+1%–2% if upgrader demand stays robust

-1% if affordability stress bites flat demand

Private Rental

Further -2%–4% as supply catches up

Stabilises if employment influx resumes

Deeper correction if expat headcount falls

Worked Example: The Chen Family — Buy in 2H 2026 or Wait?

Mr and Mrs Chen are Singapore Citizens in their early 30s. They have cleared their HDB MOP on their Bishan 4-room flat and are looking to upgrade to a 3-bedroom OCR condo. They have combined income of S$13,500 per month, CPF OA savings of S$180,000, and cash of S$120,000.

They are eyeing a 3BR at an upcoming OCR launch in Q3 2026 priced at S$1.65M. Under the ABSD SC couple remission scheme, they can purchase the new condo and claim a full refund of the 20% ABSD (S$330,000) provided they sell their HDB flat within six months of the condo purchase date.

Key numbers: BSD S$47,600 (payable from CPF); ABSD S$330,000 (cash, but refundable within six months of HDB sale); 5% cash S$82,500; legal fees ~S$5,500. Bank loan: 75% LTV = S$1,237,500 at 3.2% over 30 years → monthly repayment approximately S$5,338. TDSR = S$5,338 ÷ S$13,500 = 39.5% (PASS, under 55%). Total cash needed upfront: ~S$208,000 (cash component + ABSD float pending HDB sale).

Should they wait? If OCR prices rise another 2% by Q1 2027, the same unit would cost S$1,683,000 — an additional S$33,000. If interest rates fall 50 bps by then, monthly repayments fall by ~S$300/month. The calculus slightly favours acting when they are ready rather than trying to time the market precisely, provided the ABSD remission window can be managed. See our guide on ABSD remission for SC couples for the full rules.

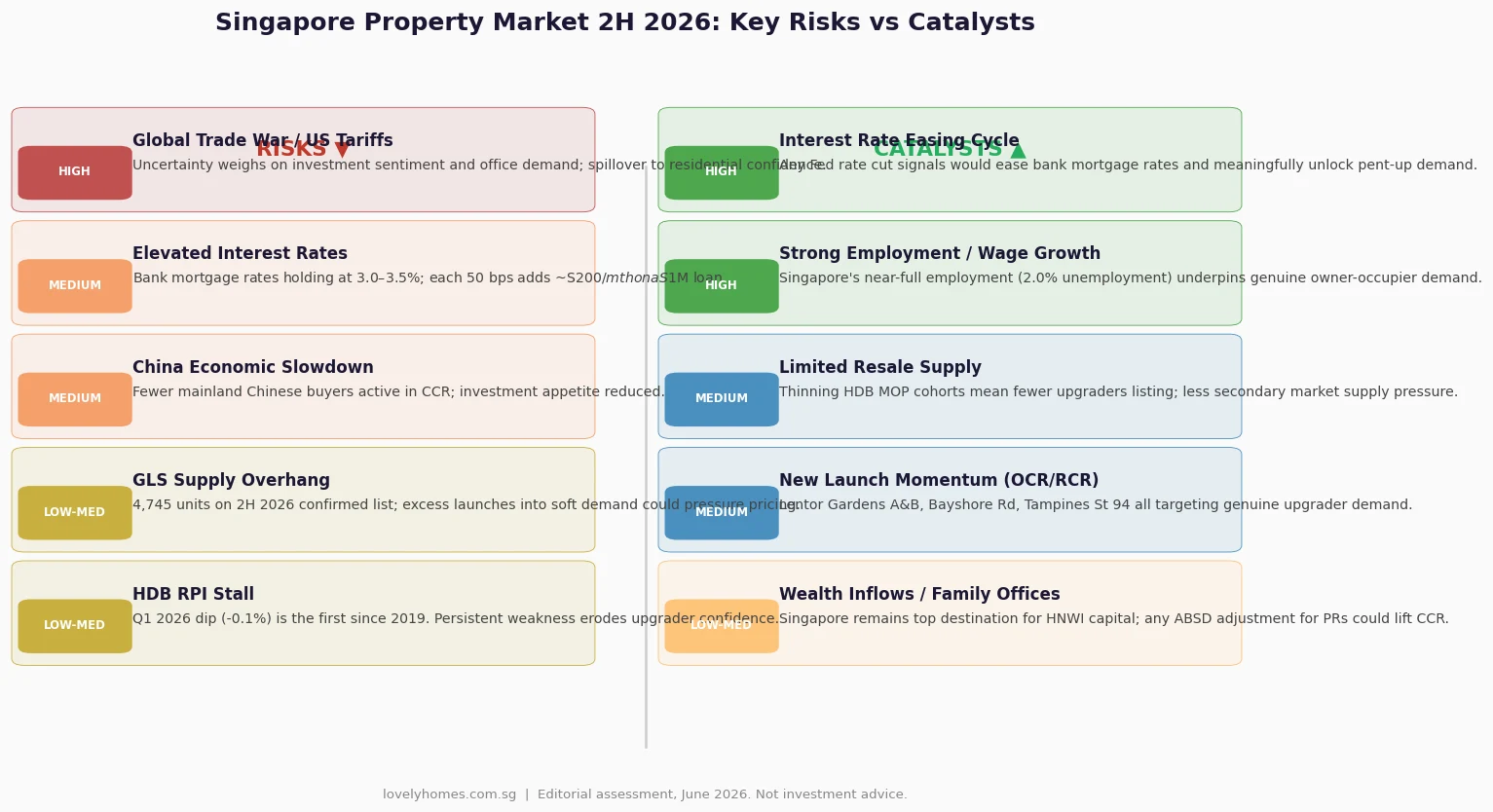

What Might Come Next: Risks and Catalysts for 2H 2026

The Singapore property market operates at the intersection of domestic fundamentals (employment, wage growth, HDB upgrader cohorts) and global macro forces (US interest rates, geopolitical risk, capital flows). For the second half of 2026, both sides of that equation are in play.

Key downside risks include the persistence of elevated interest rates — if the US Federal Reserve holds rates through 2026 without cutting, Singapore bank mortgage rates (which track SORA and swap rates) will remain in the 3.0–3.5% range, keeping affordability stretched. Continued global trade disruptions from US tariff policy create a dampening effect on business investment sentiment and, indirectly, on expatriate headcounts and rental demand. China’s economic slowdown reduces the pool of Chinese-origin buyers who were historically active in the CCR.

Key upside catalysts include the prospect of Fed rate cuts in September or December 2026 — even one 25-basis-point cut would move Singapore’s forward rates and boost buyer confidence. Singapore’s own fundamentals remain strong: the unemployment rate is approximately 2.0%, wage growth is positive, and the Government’s managed-supply approach via the GLS programme means developers are not flooding the market with distressed inventory. Any relaxation of ABSD for permanent residents (which has been debated, though there is no official signal) would be an immediate CCR and RCR catalyst.

Figure 3: Singapore Property Market 2H 2026 — Key Risks vs Catalysts. Editorial assessment as at June 2026. Not investment advice.

Frequently Asked Questions

Will Singapore property prices drop in 2H 2026?

A broad price correction in 2H 2026 is not the base-case scenario for most analysts. Singapore’s property market is underpinned by limited land supply, robust employment, and the Government’s disciplined GLS programme which calibrates supply to demand. The most likely outcome for 2H 2026 is modest positive growth in the private residential segment (0%–2% for the full year in a base case) and range-bound movement in HDB resale. A sharp correction would require a confluence of events unlikely to materialise simultaneously: a major spike in unemployment, a severe global financial shock, and a government decision to release large additional land supply. None of these is the current outlook.

When will the URA Q2 2026 Flash Estimates be released?

Based on URA’s established release pattern, the Q2 2026 Flash Estimates for the private residential property price index are expected in the first week of July 2026 — likely 1 or 2 July. The full Q2 2026 real estate statistics (including detailed regional breakdowns, rental index, and developer sales data) typically follow approximately three to four weeks later. The flash estimate gives a preliminary QoQ price change figure; the full release provides granular transaction and rental data. LovelyHomes will publish a dedicated analysis article as soon as the data is available.

What does the HDB resale -0.1% dip in Q1 2026 actually mean for sellers?

A -0.1% quarterly change in the HDB Resale Price Index is, in practical terms, negligible. On a S$600,000 flat, it represents a S$600 notional price movement — far smaller than the typical negotiation buffer in any individual transaction. What it signals is a shift in market psychology: buyers are less willing to pay premiums above valuation (Cash-Over-Valuation, or COV), and the exceptional seller’s market conditions of 2021–2024 have normalised. Sellers should still expect good prices — the index is 54% above its 2019 trough — but they should set realistic expectations and price to comparable transactions rather than aspirationally. For guidance on reading HDB data, see our HDB Resale Price Index Guide.

Is this a good time to buy a private property in Singapore?

This depends entirely on your personal financial circumstances, intended holding period, and purpose. If you are buying for genuine owner-occupation (primary home or long-term family residence), timing the market precisely is less important than buying within your means — ensuring your TDSR is comfortable, that you have adequate cash reserves, and that your loan tenor is appropriate. If you are buying as an investment (rental yield or capital appreciation), you need to stress-test the numbers at current mortgage rates (3.0–3.5%) and assess whether the rental yield justifies the carrying cost. For a personalised assessment, consult a licensed financial adviser and a property professional. See also our Singapore Property Financing Guide for a full breakdown of LTV, TDSR, and MSR rules.

How does the 2H 2026 GLS supply affect new launch prices?

The 2H 2026 Government Land Sales Confirmed List adds nine sites capable of yielding approximately 4,745 private and EC units. This is a substantial supply injection, particularly into the OCR and RCR. In theory, more supply means developers compete harder for buyers, which moderates launch prices. In practice, Singapore developers rarely slash prices — they tend to phase launches to match demand and hold firm on pricing. The more likely outcome is that new launches in 2H 2026 are priced at modest premiums (5%–8%) to recent comparables rather than at exceptional premiums. Buyers interested in specific sites such as Lentor Gardens Parcels A and B, Bayshore Road, or Tampines Street 94 should monitor the URA tender awards and developer launch announcements as they are made throughout 2H 2026. Full details of all 2H GLS sites are in our 2H 2026 GLS Programme Guide.

What is the ABSD rate for Singapore Citizens buying a second property in 2026?

A Singapore Citizen purchasing a second residential property pays 20% ABSD on the purchase price or market value, whichever is higher. This is paid in cash (CPF cannot be used for ABSD). For SC couples who own an HDB flat, the 20% ABSD on their second private property can be refunded under the SC Couple ABSD Remission Scheme, provided the HDB flat is sold within six months of the completion of the private property purchase. The full rules are detailed in our ABSD Remission Guide and Complete ABSD Singapore 2026 Guide.

How do I track the Singapore property market between official URA releases?

Between URA quarterly releases, you can monitor real-time trends through several free sources. The URA REALIS portal (accessible via My SingPass) provides transaction-level data for private residential properties. The HDB Resale Flat Prices portal shows individual HDB transactions. SRX Property and EdgeProp Singapore publish weekly market commentaries based on caveats lodged. The Business Times Real Estate section and Channel NewsAsia Property cover major announcements and tender results. For a guide on how to interpret the data you find, see our HDB Resale Price Index Guide and CCR RCR OCR Property Guide.

Disclaimer: This article is for general informational purposes only and does not constitute financial, investment, or property advice. All property market data is sourced from the Urban Redevelopment Authority (URA) and Housing Development Board (HDB) official releases as at Q1 2026. Property prices, interest rates, and government policies can change — readers should refer to the latest official URA (ura.gov.sg), HDB (hdb.gov.sg), MAS (mas.gov.sg), and IRAS (iras.gov.sg) publications and consult a licensed financial adviser or property professional before making any property-related decision. Past price performance is not indicative of future results.

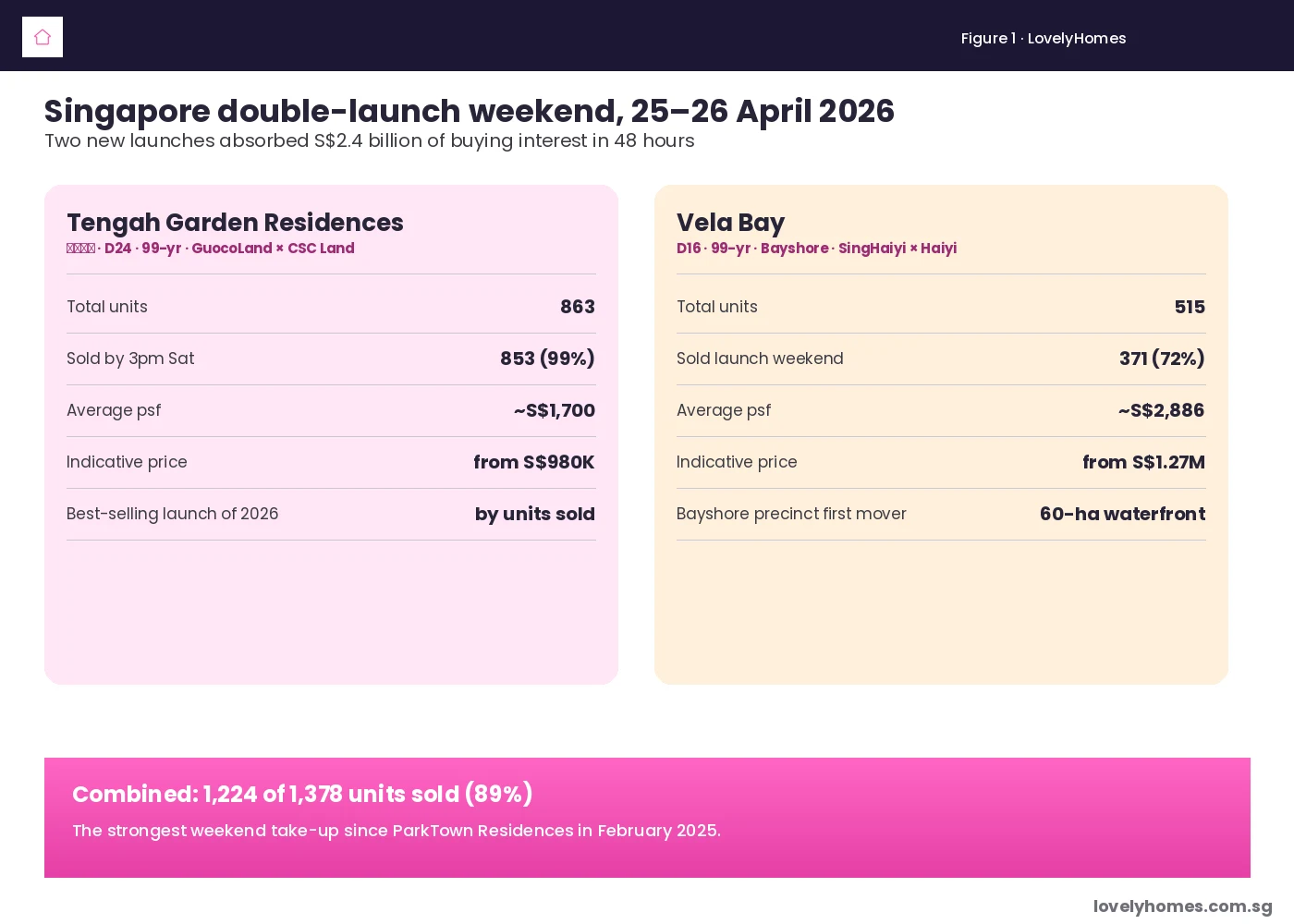

Published 28 April 2026. Reflects developer launch-weekend announcements and Singapore property press coverage of 25–26 April 2026.

Quick Answer — what happened

Two major Singapore new condo launches went live on the weekend of 25–26 April 2026: Tengah Garden Residences (863 units, 99-yr leasehold, GuocoLand × CSC Land) and Vela Bay (515 units, 99-yr leasehold, SingHaiyi × Haiyi Holdings).

Combined, the two projects sold 1,224 of 1,378 units (89%) over the launch weekend.

Tengah Garden Residences cleared 853 of 863 units (~99%) by Saturday afternoon, the strongest launch-day take-up since ParkTown Residences in February 2025.

Vela Bay sold 371 of 515 units (~72%), becoming the first private launch in the 60-hectare Bayshore waterfront precinct.

Average prices: Tengah Garden Residences ≈ S$1,700 psf, with units from S$980,000. Vela Bay ≈ S$2,886 psf, with units from S$1.27 million.

The weekend’s combined gross sales value is approximately S$2.4 billion, the largest dual-launch weekend on record for Singapore residential property.

The headline numbers

Singapore’s primary condo market has been described as “thin but priced firm” through Q1 2026. The weekend of 25–26 April 2026 ended that narrative with a single set of launch figures. By close of business Sunday, two new projects in different parts of the island had between them moved more units than the entire month of February 2026.

Tengah Garden Residences, the first private condominium launched inside the Tengah HDB-led new town, registered 853 sales out of 863 units — a 99% sell-through rate. Vela Bay, the first private residential launch in the Bayshore precinct in the East, sold 371 of 515 units. The two projects together absorbed buyer demand worth roughly S$2.4 billion in 48 hours.

Figure 1: 1,224 of 1,378 units sold across the two projects — roughly 89% of available stock cleared in two days.

Tengah Garden Residences — the suburb story

Developed jointly by GuocoLand and CSC Land Group on a 99-year leasehold parcel along Tengah Garden Avenue (District 24), Tengah Garden Residences was launched at indicative prices from S$980,000 for one-bedroom units. Average pricing landed at roughly S$1,700 per square foot, slotting in between recent Outside-Central-Region (OCR) launches and the older Bukit Batok mass-market resale stack.

Key drivers of the near-sellout:

Pent-up Tengah demand. Tengah’s residential identity has been HDB-led since 2018, with no private launches inside the estate. The opening of the first private project tested an aspirational segment that had been waiting four years.

Pricing that read as “below ParkTown”. ParkTown Residences in Tampines launched at a higher OCR psf in February 2025; the Tengah price point felt restrained by comparison.

Singapore-Citizen-heavy buyer mix. Over 90% of buyers are reported to be Singapore Citizens, consistent with the post-2023 ABSD regime where foreign demand at OCR price points has thinned.

Connectivity story. Future Tengah MRT (Jurong Region Line, opening 2027–2028) and the proximity of the new Tengah town centre supported the long-hold buyer thesis.

Vela Bay — the Bayshore opener

Vela Bay, by SingHaiyi Group and Haiyi Holdings, launched at average prices of around S$2,886 psf, with one-bedroom units from S$1.27 million. The 515-unit project sits inside the Bayshore precinct, an emerging 60-hectare master-planned waterfront on the East Coast.

The Vela Bay take-up of 72% is more modest than Tengah Garden Residences’ 99%, but no less interesting:

Higher absolute price point. A typical 2-bedroom Vela Bay unit lands above S$2 million; that is a different buyer profile from Tengah.

First-mover premium. As the only private launch in a precinct still under construction, Vela Bay’s price had to absorb the discount buyers usually demand for “go-first” risk on infrastructure delivery.

Nine new sites in 1H 2026 GLS. URA’s 1H 2026 Government Land Sales programme released nine confirmed-list sites with capacity for ~9,185 units. The sequencing of those sites — including the Bayshore Drive mixed-use plot whose tender closes 15 July 2026 — is shaping how buyers price first-mover Bayshore stock.

SingHaiyi balance-sheet narrative. SingHaiyi has been a heavy participant in en-bloc and GLS bids in 2026 (it was also part of the consortium that won Loyang Valley en-bloc at S$880 million); its Bayshore launch is a clear conviction trade by the developer.

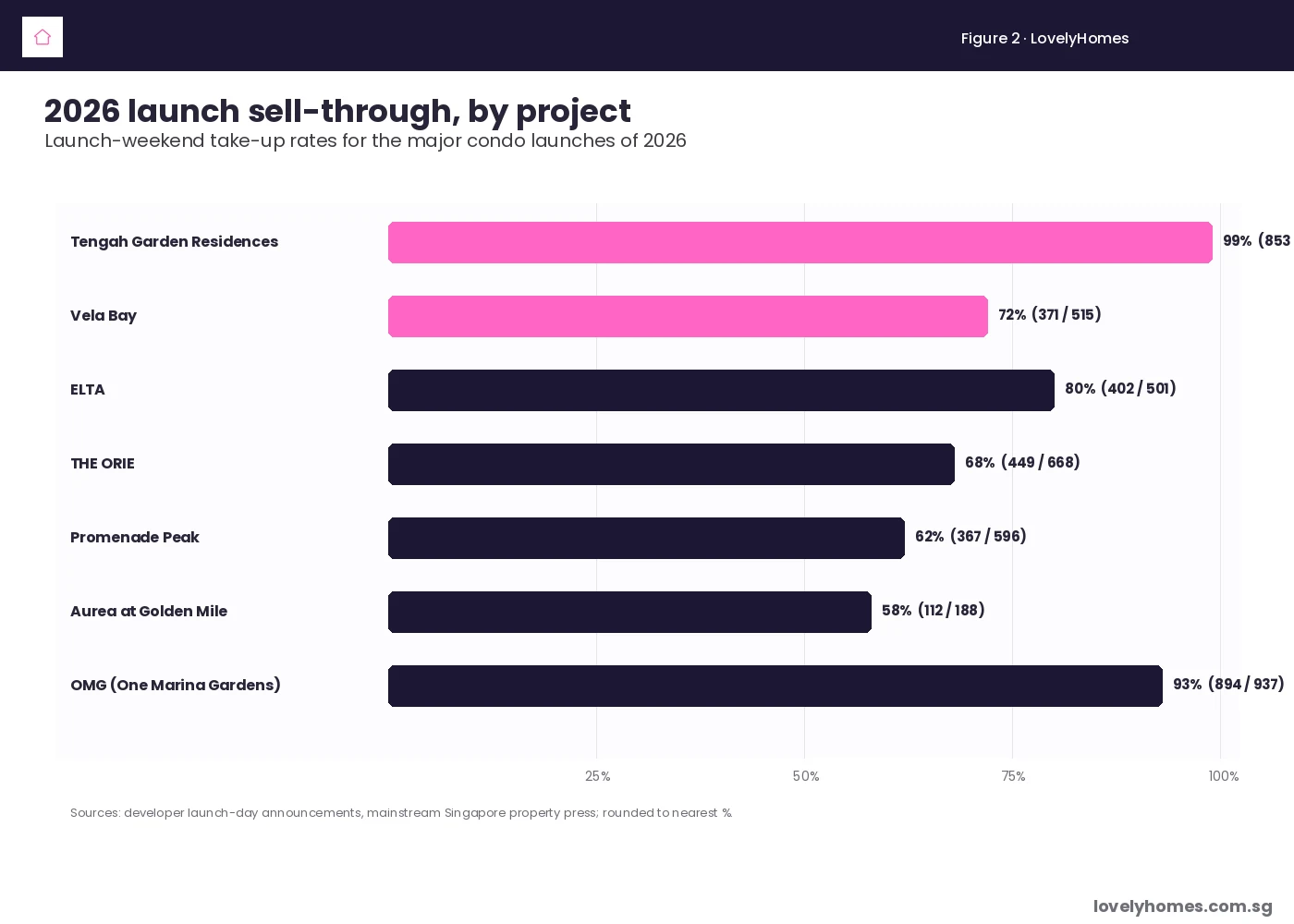

Figure 2: Tengah Garden Residences sits at the top of the 2026 launch sell-through table. Vela Bay’s 72% is also above the 2026 OCR/RCR average.

What the weekend tells us about 2026 demand

Metric

Reading

Implication

Combined launch-weekend take-up

1,224 / 1,378 units (89%)

Latent demand absorbing strongly when supply opens at the right price

OCR launch psf — Tengah

~S$1,700

Below recent comparable OCR launches; a “value” anchor for 2026 OCR pricing

RCR/East launch psf — Vela Bay

~S$2,886

Setting the benchmark for the Bayshore precinct ahead of the Bayshore Drive GLS tender

Buyer mix

Predominantly Singapore Citizen

Foreign demand still suppressed by the 60% ABSD; the market is local-driven

2026 launch pipeline

~17 projects, ~8,100 units

30% lower than 2025 — supply scarcity supports launch-day pricing power

What this means for buyers

For prospective Tengah buyers who missed the launch ballot, the resale option will likely sit at a 3–7% premium once units start changing hands — typical for a near-sellout launch. Tengah Garden Residences will not have additional release tranches for some months given the sell-through.

For Vela Bay, with 144 units (28%) still available, the post-launch phase remains accessible at launch pricing. Buyers should monitor whether units in Towers 1 and 2 are released before infrastructure milestones in the Bayshore precinct — first-mover units historically appreciate as the precinct fills out, but only if pricing on later launches doesn’t undercut them.

For the broader market, the weekend confirms that well-priced, well-located new launches in Singapore can still clear at speed in 2026, against the narrative of cooling-measure overhang. The discipline is on launch-day pricing: Tengah’s near-sellout came at a psf below what some industry watchers had projected for an OCR launch this cycle. Vela Bay’s slower (but still strong) take-up suggests that buyers in the higher-price RCR segment remain willing to pay up only for clearly differentiated locations.

What might come next

Two near-term watchpoints:

Bayshore Drive mixed-use GLS tender (closes 15 July 2026). The land bid will be read against Vela Bay’s launch psf as a price discovery point for the precinct.

BTO June 2026 ballot (~6,900 flats). If HDB pricing continues to compress against private OCR pricing, the substitution effect supports a second wave of OCR private demand later in 2026.

The next major private launches in the calendar — Bayshore Drive (if the tender awards in 1H 2026), Sembawang Drive EC, and a likely 2H 2026 District 5 OCR launch — will tell us whether the 25–26 April weekend was a one-off catch-up after a thin Q1, or the start of a measurably stronger primary market.

Frequently asked questions

Why did Tengah Garden Residences sell so much faster than Vela Bay?

Three reasons. First, price: at ~S$1,700 psf, Tengah’s entry price of S$980,000 sits below the typical OCR launch and is reachable for HDB upgrader couples. Vela Bay at ~S$2,886 psf and S$1.27 million entry sits in a different affordability cohort. Second, Tengah is a four-year-old new town with a built-out HDB community already in occupation; Vela Bay is the first launch in a precinct still under construction. Third, Tengah was the first private launch in the new town — a one-off scarcity premium that Vela Bay does not enjoy because more Bayshore launches will follow.

Is this evidence that cooling measures aren’t working?

Not necessarily. Cooling measures (the April 2023 ABSD hike, the September 2022 LTV / TDSR tightening) have visibly suppressed foreign demand and kept investor flows thin. The April 2026 launches were powered overwhelmingly by Singapore Citizen owner-occupier and upgrader demand, which is exactly the segment policy-makers wanted to remain active. The strong take-up reflects pent-up local demand meeting limited new supply, not a re-acceleration of speculative buying.

Should buyers chase a near-sellout launch like Tengah?

Generally no. Once a launch clears 90%+, the remaining stock is typically the less attractive layouts or units, and the resale market opens at a premium. The discipline for buyers is to be at the front of the queue at launch — or wait for the resale market to settle 6–9 months later when the urgency premium has softened.

What does this mean for the Bayshore Drive GLS tender?

Vela Bay’s 72% sell-through at ~S$2,886 psf gives bidders a reference point for what a Bayshore launch can absorb at price. If the Bayshore Drive GLS tender bids land at above S$1,400 psf ppr, the implied launch psf for the next Bayshore project would be approximately S$3,000+, which is testable against Vela Bay’s revealed demand curve.

How does this compare to historical strong launches?

The 99% Tengah figure is the highest launch-weekend take-up since ParkTown Residences in February 2025, which moved 87% on launch day. Going further back, Lentor Mansion (2024), Amo Residence (2022), and Treasure at Tampines (2019) all booked similar 90%+ launch-day percentages. Each of those projects shared the same ingredients as Tengah: a clear price-point anchor, an underserved sub-market, and a strong upgrader cohort.

Will more units be released?

For Tengah Garden Residences, the developer has not announced a second tranche; with only 10 units unsold, there is little to release. For Vela Bay, the remaining 144 units (28%) will be released in batches over the coming weeks at the same indicative price band; movements above launch pricing typically follow demonstrated take-up of 80%+.

Disclaimer. All sales figures, prices and dates are based on developer launch-day announcements and public reporting in the Singapore property press. Final transaction figures will be reflected in URA Realis caveats over the coming weeks. This article is general market commentary and does not constitute investment, legal or financial advice. Buyers should always verify current pricing and availability with the developer’s appointed sales gallery and consult a licensed Singapore conveyancing lawyer before exercising any Option to Purchase. Cooling-measure thresholds and ABSD rates are administered by the Inland Revenue Authority of Singapore and the Monetary Authority of Singapore.

New Launch Tengah Garden Residences Vela Bay Singapore Property Market Property News OCR Bayshore Tengah SingHaiyi GuocoLand

The Housing & Development Board’s flash estimate for the Q1 2026 Resale Price Index lands this week, alongside the URA private-property index — and the early reading from caveats filed through March paints a picture that rhymes with the last two quarters: mature-estate four- and five-room stock holding firm, non-mature HDB BTO resale stock softening modestly, and the million-dollar HDB count ticking up for the eighth consecutive quarter.

At a glance

HDB’s Q1 2026 flash RPI print is expected to come in at +0.9% QoQ, following +1.1% in Q4 2025 and +1.4% in Q3.

Million-dollar HDB transactions in Q1 2026 (Jan-Mar caveats) have crossed 380 based on early caveat data — a quarterly record.

Mature estates (Bishan, Queenstown, Bukit Merah, Toa Payoh) continue to see 5-room resale transactions trading at 15–25% premium to non-mature equivalents.

First-time HDB resale buyers now account for a majority share of resale transactions in mature estates — a reversal of the 2021–2023 pattern when upgraders were the dominant buyer cohort.

Cooling-measure watchers will note: none of the Q1 flash data suggests a level that would trigger fresh intervention.

The headline: deceleration, not decline

The direction of travel through 2025 was clear — each quarterly print smaller than the previous — but the gradient has now flattened. The Q1 2026 +0.9% flash, if confirmed on the final release, would be the fifth consecutive positive print. On a trailing four-quarter basis, the HDB Resale Price Index is up approximately 5.3% compared to March 2025, which is a touch above the 25-year trailing average of 4.1% per annum and well below the 10.7% CAGR of the post-pandemic recovery window from 2021 to 2023.

The deceleration pattern is most visible in non-mature estates. Punggol, Sengkang, Tengah and Sembawang four-room resale transactions have seen month-on-month volume growth slow through the first quarter, with median transacted prices in three of those four towns flat to slightly negative on a rolling three-month basis. Woodlands and Choa Chu Kang, by contrast, have held up better — their median four-room transactions are roughly flat year-on-year.

The mature-estate premium keeps widening

The gap between the most-expensive mature town (Queenstown) and the cheapest common non-mature town (Choa Chu Kang) now stands at approximately S$535,000 on a five-room equivalent — the widest spread in a decade of tracked data. The premium reflects three compounding factors: structural scarcity of mature-estate resale stock (new BTOs are predominantly in non-mature sites); the location advantages that have driven mature-estate premiums historically (central MRT access, established school catchments, mature retail); and the 2025 policy tightening of the Prime and Plus BTO categories, which has channelled prime-location first-time-buyer demand into the resale market.

Million-dollar HDB transactions cross 380

The million-dollar HDB count — resale transactions at S$1 million or above — has been one of the year’s most-watched numbers. Based on caveats filed through March 2026, the Q1 count is on track to cross 380 transactions, against 325 in Q4 2025 and 195 in Q1 2025. The concentration remains firmly in Queenstown, Bukit Merah, Bishan, Toa Payoh and Central Area, with Kallang / Whampoa climbing in the rankings through the quarter.

Why million-dollar HDB matters

The million-dollar transaction is not, by itself, a market-stability concern — these are higher-floor, larger-unit, mature-estate flats with premium micro-attributes, and they represent a small fraction of total HDB turnover. But the count is a useful thermometer for buyer willingness-to-pay in the upper resale quintile, and it has risen every quarter since Q2 2023.

The buyer mix has quietly inverted

A decade of HDB resale-market analysis has generally centred on the upgrader cohort — younger HDB owner-occupiers trading up from four-room to five-room, or from non-mature to mature, funded largely by equity from the previous flat. That cohort dominated the 2021–2023 market.

The composition has quietly inverted through 2025 and into Q1 2026. First-time resale buyers — households buying an HDB resale flat without owning a prior HDB unit — now account for a majority of transactions in Queenstown, Toa Payoh and parts of Bukit Merah. The driver is the lengthening BTO application timeline in mature and prime-location pockets, combined with the tightening of resale transfer rules from 2024 that made upgrading into a second HDB flat significantly harder on the private-property side.

Mortgage affordability: the real constraint

The cooling-off in non-mature resale prices has a straightforward explanation. Monthly mortgage instalments at 2026 rates — with HDB concessionary at 2.6% and most private floating packages around 3.3–3.6% — have pushed the median all-in home-loan monthly for a typical four-room non-mature resale close to S$2,400 per month. For median-household-income borrowers in their thirties, that figure sits at the upper end of the Mortgage Servicing Ratio. Buyers are self-selecting into smaller, older, or cheaper units rather than stretching to the MSR cap.

What to watch in Q2

Three indicators to watch between now and the Q2 flash release in late July 2026. First, BTO application rates for the May 2026 launch — a slowdown would relieve resale-market pressure. Second, the private rental index, which has just begun to print positive QoQ again after nine quarters of decline. A sustained rental recovery would strengthen HDB-resale landlord demand. Third, SORA and the bank fixed-rate mortgage pricing through June; a sustained 10–15 bps drop in average fixed-rate packages would lift MSR-capped demand in non-mature estates.

Frequently asked questions

What is the HDB Resale Price Index?

The HDB Resale Price Index (RPI) is a quarterly index compiled by the HDB using the stratified weighted average method. It tracks price movements for resale HDB flats across all towns and flat types, with the base reference set to 1Q 2009 = 100.

Why does the index show growth when my estate has seen prices flat?

The RPI is a national aggregate. Individual towns can diverge materially from the national print. Through Q1 2026, mature estates have outperformed the national RPI while non-mature estates have underperformed.

Does a ‘million-dollar HDB’ transaction mean the market is overheated?

Not directly. Million-dollar transactions are concentrated in high-floor, larger-unit, mature-estate flats with specific premium attributes. They represent roughly 2% of quarterly HDB resale turnover. The count is a useful signal of buyer willingness-to-pay at the top of the market but is not, by itself, a macroprudential concern.

When is the final Q1 2026 RPI released?

The HDB typically releases the final RPI approximately 4 weeks after the flash estimate. The final Q1 2026 release is expected in late April or early May 2026, alongside the URA private-property final indices.

Should I buy an HDB resale now or wait for the next BTO?

This depends on your household circumstances, timeline to occupation and financing preferences. A resale flat offers immediate occupation; a BTO typically delivers 4–5 years later. Our BTO vs resale comparison covers the trade-offs in detail.

Source

Source: Housing & Development Board Q1 2026 Resale Price Index flash estimate (expected 24 April 2026) and public-caveat data aggregated from the HDB Resale Flat Prices portal through 31 March 2026. Full methodology: HDB press releases.

Editorial note. This article is based on public-domain data released by HDB, URA, Singapore Land Authority and MAS as at 23 April 2026. All analysis is our own. No marketing-agency research is cited. Figures may be revised in subsequent official releases — always refer to the latest authoritative source before making a housing decision.

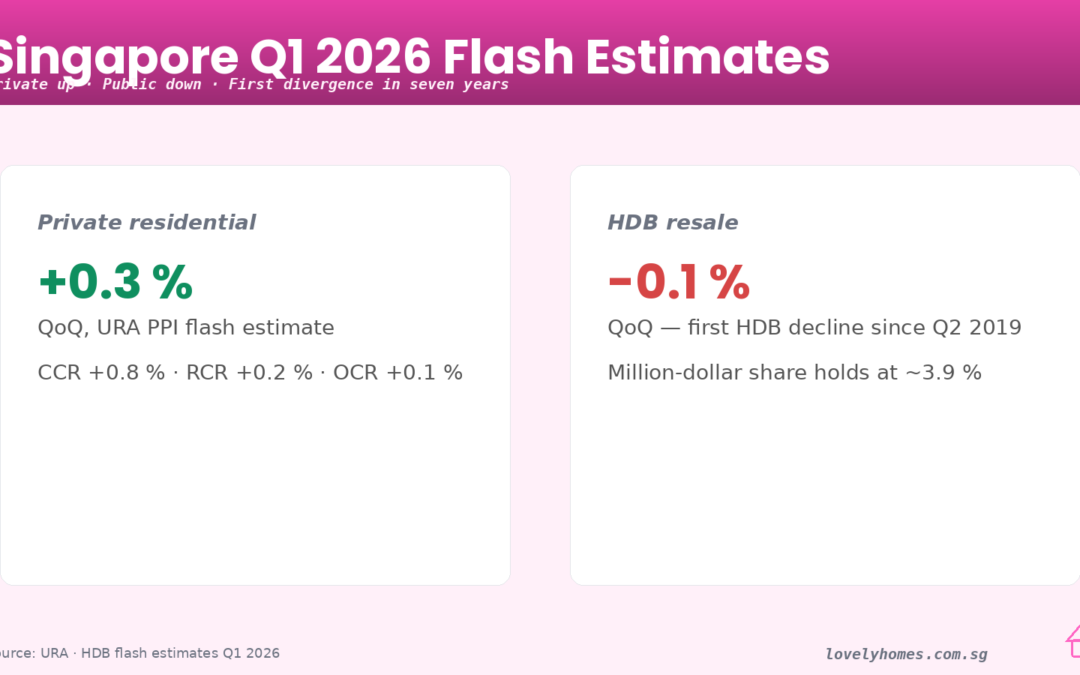

Private residential and HDB resale flash indices diverged for the first time in seven years. Source: URA and HDB flash estimates, 1 April 2026.

Quick take: On 1 April 2026, URA’s flash estimate showed the overall private residential price index rising 0.3% quarter-on-quarter in Q1 2026, while HDB’s flash estimate put the Resale Price Index at -0.1% quarter-on-quarter — the first public-housing decline since Q2 2019. The two segments have moved in the same direction almost every quarter since mid-2019. This quarter, they have not.

What the numbers actually say

URA’s flash estimate is a fast read on transactions caveated in the first ten weeks of the quarter. For Q1 2026, the non-landed segment carried the whole index: non-landed prices were up an estimated 1.0%, led by the Outside Central Region at +1.3%, followed by the Rest of Central Region at +0.8% and the Core Central Region at +0.4%. Landed homes pulled the headline the other way at about -2.4%, a reminder that the landed market trades thinly and can swing on a handful of deals.

The other private-market signal behind the flash is volume. New-sale launches collapsed to roughly 60% below Q4 2025. With only a thin slate of launches in January and February and most developers holding fire until after Chinese New Year, the bulk of Q1 price action came from resale and sub-sale transactions rather than showflat pricing power. When new launches return in strength from Q2, the price signal will widen again.

On the public side, HDB’s flash estimate at -0.1% is small in headline terms but large in narrative. The Resale Price Index has risen in every single quarter since Q3 2019 — twenty-six consecutive quarters of gains. A flash print at zero, or marginally below it, breaks that run. Final numbers, due in late April, may revise the estimate either way by a tenth or two, but the direction is the news.

Why the two markets are diverging now

Three forces are separating private and public prices this quarter.

1. The cooling measures have landed unevenly. The August 2024 LTV tightening for HDB loans (90% to 75%) and the continued 15-month wait-out rule for private downgraders have compressed HDB resale demand more than the private market. Private buyers financing with bank loans at lower LTV ceilings were already used to higher cash-and-CPF components; HDB resale buyers, many of whom are upgraders or first-timers, feel the tightening at the margin where deals close.

2. BTO supply has materially improved. HDB is pushing through roughly 50,000 flats across the 2025 and 2026 programmes. The June 2026 BTO exercise will offer about 6,900 flats across Ang Mo Kio, Bishan, Bukit Merah, Sembawang and Woodlands. When first-timers have a realistic shot at a BTO within 18 to 24 months, the urgency premium in resale prices eases. That is exactly the mechanism HDB publicly described when it reintroduced the Prime, Plus and Standard classification in late 2024.

3. The private market found a new OCR anchor. The OCR leading at +1.3% reflects the mass-market bid for newer freehold and 99-year projects where the price-per-square-foot still reads as a discount to the RCR. Buyers priced out of the core are not disappearing — they are rotating outward. HDB resale, by contrast, has no similar pressure valve; the product is the product.

How the divergence compares historically

The last time HDB resale fell while the URA index rose was Q2 2019 — the final stretch of the post-2018-cooling-measures adjustment, when public housing was absorbing ABSD-driven demand shifts. Before that, divergence episodes clustered around the 2013-2014 tightening and the 2008-2009 cycle. Divergence is not unprecedented; what is unusual is how long the two markets have moved together. From Q3 2019 to Q4 2025, both indices posted gains in every single quarter.

One quarter is not a trend. The signal here is less “HDB is falling” and more “HDB has stopped rising.” That is still a meaningful shift after seven years of one-way pressure.

What this means for buyers and sellers

HDB resale buyers: The urgency is lower. If the June BTO ballot in a town you would consider is a serious option, running both tracks in parallel is now a more defensible strategy than it was 12 months ago. Million-dollar resale records will continue to happen in flagship locations, but the median flat in a mature estate is no longer compounding at 8-10% a year.

HDB sellers: Price realism matters. COV (cash-over-valuation) expectations set in 2024 no longer hold in most estates. Sellers who fix an asking price based on a neighbour’s Q3 2025 transaction are increasingly missing the window and sitting on the listing for two to three months before cutting.

Private buyers: The OCR is where the action is, and the Q2 launch slate will test how much pricing power developers actually have. Watch median PSF for OCR new launches in Q2 against late-2025 comparable projects. If developers push prices 3-5% above comparables and still clear 30% on launch weekend, the private cycle re-accelerates. If they stall, the flash estimate flatters a cooler underlying market.

Private sellers and sub-sale owners: The CCR-to-OCR spread narrowed again in Q1. Holders of older freehold CCR stock should benchmark against current RCR new-launch pricing rather than historical CCR premiums — the buyer pool has shifted.

What to watch between now and late April

Three things will sharpen the picture in the next three weeks:

Final Q1 numbers (late April): URA and HDB publish the full quarterly indices with sub-indices by region and flat type. The flash can revise by up to 0.2 percentage points in either direction.

April and May new-launch pricing: Two to three large OCR launches are pencilled in for Q2. Median PSF at launch will tell us whether developers are testing the ceiling or holding.

June 2026 BTO application rates: First-timer subscription ratios in Ang Mo Kio and Bishan will signal how much pressure is still in the resale market. Application rates above 3x in non-mature estates typically foreshadow resale strength; ratios closer to 1x suggest buyers are comfortable waiting.

The bigger frame

Singapore’s residential market has been remarkable for its synchronised climb since 2019. That era is pausing. Whether Q1 2026 turns out to be a one-quarter wobble or the start of a sustained rebalancing between public and private depends on three things: the new-launch pipeline in Q2 and Q3, the pace of BTO completions absorbing first-timer demand, and whether any further cooling measures are signalled in the mid-year review.

For now, the most honest read of the flash estimates is this: the private market is still advancing, the public market has stopped, and the gap between them is the most interesting number in Q1.

FAQ

How reliable is the URA flash estimate?

The flash estimate is based on the first ten weeks of caveated transactions and is typically revised by ±0.1 to ±0.2 percentage points when the final index is published three to four weeks later. Direction is usually preserved; magnitude can shift.

Is the HDB flash estimate the first decline since 2019?

Yes. HDB’s Resale Price Index last posted a quarter-on-quarter decline in Q2 2019. The Q1 2026 flash at -0.1% is the first negative print in twenty-seven quarters. The final number, due in late April, will confirm or revise this.

Why did private new launches drop 60% QoQ?

Q1 is seasonally slow because of Chinese New Year and because developers typically time launches to coincide with stronger post-Lunar-New-Year demand in Q2. Q1 2026 had a thinner launch slate than usual with most of the pipeline deferred to April onwards, which amplified the quarter-on-quarter drop.

Will the June 2026 BTO exercise affect resale prices?

At the margin, yes. 6,900 flats across five towns is a meaningful supply signal, especially in non-mature estates where first-timer application ratios drive most of the urgency pricing in resale. Towns included are Ang Mo Kio, Bishan, Bukit Merah, Sembawang and Woodlands.

Should I wait to buy?

Flash estimates are one input among many. If you have found the right unit at the right price relative to comparable transactions in the last 60-90 days, macro prints rarely change the calculus. If you are timing the cycle, wait for the final Q1 numbers and the Q2 launch pricing before committing.

Disclaimer: This article reports on URA and HDB flash estimates published on 1 April 2026 and is for general information only. Flash estimates are preliminary and subject to revision. Individual transactions vary by project, unit, tenure and timing. This is not financial, investment or property advice. Buyers and sellers should seek advice from qualified professionals and verify figures against the official URA and HDB releases before making decisions.

The Singapore government has announced its slate for the second half of 2025 under the closely watched Singapore GLS programme. This latest release makes eleven new sites available for private residential development. Moreover, this strategic move is pivotal in shaping the nation’s property landscape. It aims to ensure a stable and sustainable supply of private housing. Specifically, ten of these plots are on the confirmed list, signalling a definite sale within the period. In addition, a site in the Central Business District (CBD) for serviced apartments is on the reserve list. This means it can be triggered for sale based on developer demand. This curated list arrives amid cautious market sentiment, balancing new housing needs with economic uncertainties.

Consequently, market analysts are forecasting strong, and even fierce, competition. This is particularly true for prized sites in the Newton and Tanjong Rhu planning areas. Remarkably, these areas have not seen new state land offered for sale in nearly three decades. This long hiatus, therefore, makes them exceptionally rare opportunities for developers. They can establish a flagship presence in established, high-value residential enclaves.

Highly Anticipated Prime Locations: A Closer Look

The Newton site, a 0.59-hectare plot on Bukit Timah Road, is widely seen as the crown jewel. Slated for an August launch, it is poised to attract top-tier developers. The plot can be developed into approximately 340 exclusive homes. Furthermore, its history is notable; the land was previously used for transitional offices. The plot’s allure is now magnified by its prime location and excellent connectivity. For instance, it is near the Newton MRT interchange and the Orchard Road shopping belt. As a result, experts predict it will be highly sought after, potentially setting new price benchmarks.

Similarly, the Tanjong Rhu site is generating significant industry buzz. This substantial plot can accommodate around 525 residential units and is scheduled for a November tender. As the first GLS site in this waterfront precinct since 1997, it presents a unique chance. Developers can cater to the sustained upgrader demand for city-fringe living. The location’s appeal is also enhanced by its proximity to the Singapore Swimming Club. It is also near the future Katong Park MRT station, promising excellent connectivity.

Other Key Sites on the Confirmed List

In addition, developers can bid on a Dunearn Road site in the new Turf City housing estate. This 1.91-hectare plot will support 335 private homes and retail space. Its location near Sixth Avenue MRT and popular schools should ensure robust interest when it launches in December.

Furthermore, a large 1.35-hectare site along Dover Road is set to launch in November. It is expected to yield 625 units, making it the largest project on this list. Located near Singapore’s One-North R&D hub, this development provides much-needed housing. It brings residents closer to key employment centres for the area’s 50,000-strong workforce.

Meanwhile, a Bedok Rise plot for 380 units will likely see intense competition in September. This is a direct result of the limited supply of new homes in this mature estate. It also represents the last major development parcel near the Tanah Merah MRT interchange.

Increased Supply to Meet Strong EC Demand

In a clear response to robust demand, the government has included two executive condominium (EC) sites. The first, in Woodlands Drive 17, can be developed into 560 units. Consequently, a second site in Miltonia Close will yield around 430 EC units. This injection of supply brings the total of new EC units to its highest level since 2014. Therefore, experts believe increasing EC supply is crucial for providing more housing choices. It also helps mitigate the “fear of missing out” effect that can drive prices higher.

Reserve List and Overall Market Caution

Beyond the confirmed plots, a Cross Street site is available on the reserve list. It can yield 305 long-stay serviced apartments, which may appeal to certain investors. However, analysts remain uncertain if it will be triggered soon. This is because the asset class is a relatively untested concept in the Singapore market.

Overall, the government’s decision to place more supply on the reserve list reflects a measured approach. It acknowledges the recent slowdown in home sales and a cautious developer outlook. This caution stems from rising costs and an uncertain macroeconomic climate.