Snapshot of the three Lakeview and Shunfu BTO projects announced for the June 2026 sales exercise.

Quick take

HDB confirmed on 17 April 2026 that three new Build-To-Order (BTO) projects at Lakeview and Shunfu will be launched from the June 2026 sales exercise, delivering about 1,600 new homes when completed. Two of the projects sit in Lakeview and one in Shunfu — the first time in more than four decades that public housing is being introduced on this stretch of Upper Thomson Road. The first Lakeview project, with about 1,200 units across five blocks, headlines the June 2026 launch.

What’s launching in June 2026

The first Lakeview BTO comprises five residential blocks ranging from 18 to 40 storeys. Unit mix is approximately 470 × 2-Room Flexi flats, 740 × 4-Room flats, and 50 × public rental flats — a deliberately family-skewed mix that reflects the precinct’s school catchment (Catholic High, Raffles Institution, Ai Tong) and its Circle Line accessibility via Marymount MRT.

Indicative pricing

HDB has anchored Lakeview pricing to recent comparables in the Bishan Terraces and Mount Pleasant Crest cohorts:

2-Room Flexi: ~S$230,000 to S$370,000 (depending on lease term and flat size)

4-Room: ~S$500,000 to S$750,000+ (high floor and stack premiums add ~S$60k–S$80k)

This places Lakeview firmly in the upper Standard / Plus band — these are not Prime-class flats (the precinct sits outside the 5km central radius), but the central-fringe location and Circle Line proximity justify the premium over a comparable Punggol or Tengah BTO.

Connectivity and amenity

The site sits within walking distance of Marymount MRT (CC16, Circle Line), two stops from Bishan Interchange (NS17/CC15) and four stops from Caldecott (CC17/TE9). Covered linkways will connect the project to the bus stop along Upper Thomson Road, while the existing park connector along the same road is being realigned to give residents direct walking access to MacRitchie Reservoir Park and the Central Catchment Nature Reserve.

The other two BTO projects

The second Lakeview project and the Shunfu project together add about 130 × 3-Room flats and 290 × 4-Room flats — roughly 420 units. HDB has indicated both will launch within the next two years (i.e. through the October 2026, February 2027 and June 2027 sales exercises). Final unit counts and storey heights are subject to detailed planning consent.

What it means for buyers

For first-timer applicants in the Plus / Standard band looking for a central-fringe location, this is one of the most compelling June 2026 ballots — Marymount-area flats trade at a 30–40% discount to equivalent CCR private condos but enjoy similar access to the central catchment and the same school basket. Application-to-flat (ATF) ratios at the last comparable Bishan Terraces launch were close to 4× for 4-Room, so families should expect competitive ballots and prepare HFE (HDB Flat Eligibility) documentation in advance. The 5-year Minimum Occupancy Period applies, with resale levy implications for previous flat owners.

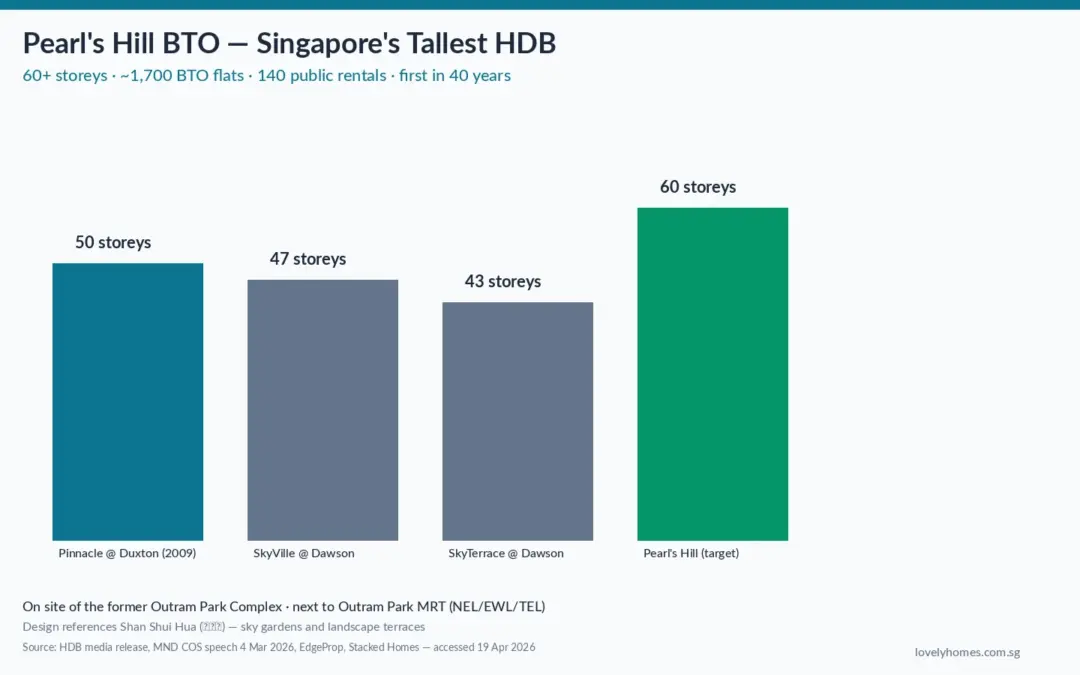

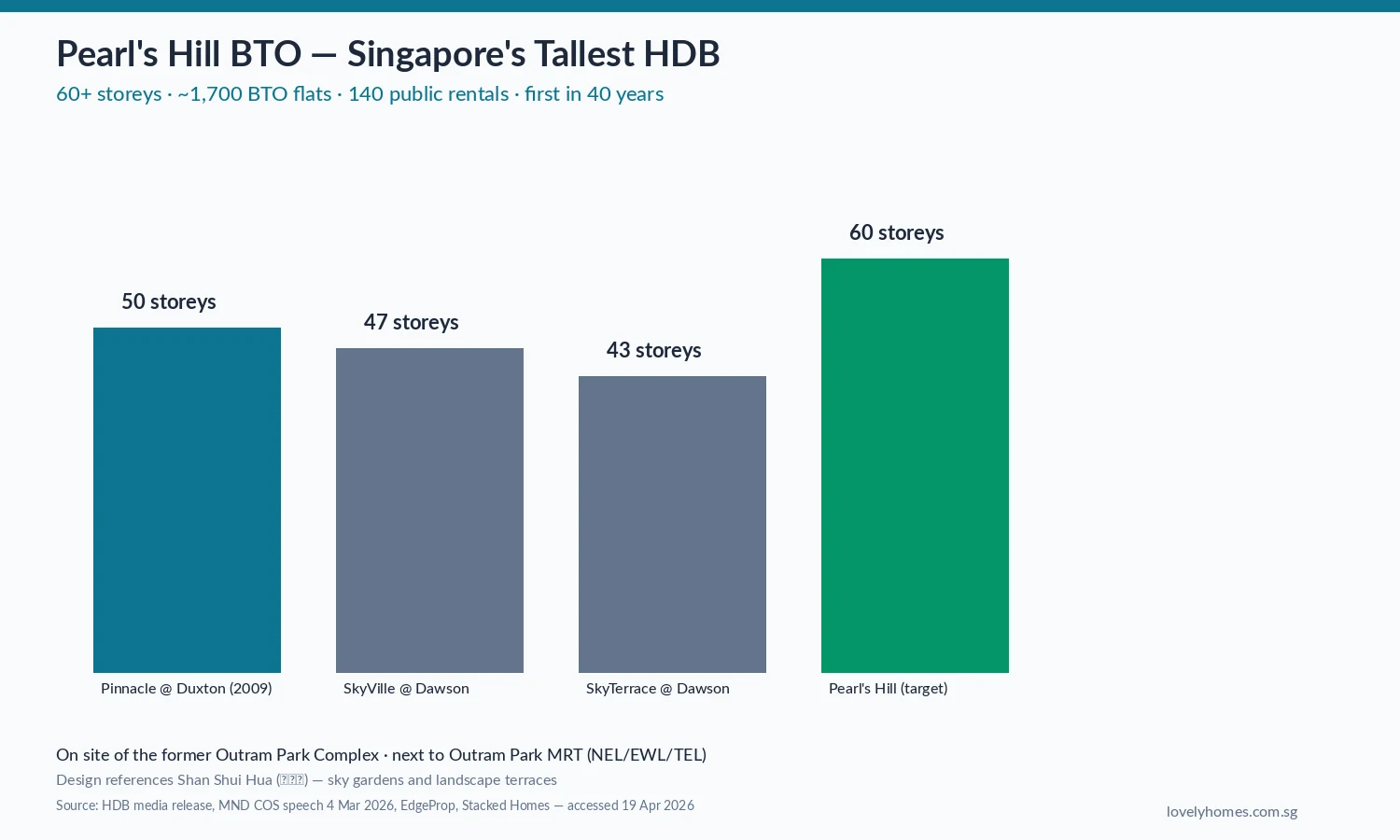

The Pearl’s Hill BTO will exceed 60 storeys, edging past Pinnacle @ Duxton (50 storeys) as Singapore’s tallest public-housing project.

Quick take

HDB has confirmed that a new BTO project at Pearl’s Hill in Outram will rise to more than 60 storeys — overtaking Pinnacle @ Duxton (50 storeys) as Singapore’s tallest public-housing project. The development sits on the site of the former Outram Park Complex, next to Outram Park MRT (NEL/EWL/TEL interchange), and will deliver approximately 1,700 BTO flats across 2-Room Flexi, 3-Room and 4-Room formats, plus over 140 public rental flats. It is the first new public housing in Pearl’s Hill in more than four decades.

Design — Shan Shui Hua

The blocks vary in height, with sky gardens and landscape terraces stepping up the hillside. The architecture references Shan Shui Hua (山水画) — the traditional Chinese ink-painting tradition that depicts mountains and flowing water in harmonic balance. The reference is more than aesthetic: the project sits at the base of Pearl’s Hill City Park, one of Singapore’s least-visited central parks, and the design language is intended to extend the park’s contour line up into the residential elevation rather than impose a rectilinear slab profile.

Location and connectivity

Pearl’s Hill sits between Chinatown and Outram, immediately adjacent to Outram Park MRT — a triple-line interchange (North-East Line, East-West Line, Thomson-East Coast Line) opened to the TEL extension in 2022. From Outram Park, residents reach Raffles Place in two stops, Marina Bay in three, and Orchard in five. SGH (Singapore General Hospital) is a five-minute walk; Tiong Bahru Market and the Pearl’s Hill heritage cluster sit on either side of the park.

Prime BTO classification

Pearl’s Hill is unambiguously in the central five-kilometre radius and will almost certainly be launched under the Prime BTO framework. Practically, that means: a 10-year MOP (vs the standard 5-year), a subsidy clawback on resale (the percentage to be confirmed at launch but is currently 8% for Prime flats), and tighter resale eligibility (Singaporean families, with a household income ceiling on resale buyers). Foreign buyers and investors are excluded from the resale pool. Indicative pricing has not been published, but commentators have flagged the S$700,000+ band for 4-Rooms as plausible — in line with the 2024 Pearl’s Hill GLS land tender benchmarks.

When does it launch?

HDB has indicated the Pearl’s Hill BTO will launch within the next few years — i.e. across the 2026–2028 sales exercises, with Minister Chee Hong Tat confirming the project in his Committee of Supply 2026 speech on 4 March 2026. The Toa Payoh West BTO at the former Caldecott site is the parallel central announcement, scheduled for the October 2026 sales exercise.

Why it matters

The Pearl’s Hill BTO is the most prominent confirmation yet that HDB is willing to build vertically and centrally — going beyond the SkyVille and SkyTerrace experiments at Dawson and Pinnacle’s 50-storey precedent. For homebuyers, it offers a rare chance to access genuinely central living at HDB prices, with the trade-off of Prime BTO restrictions. For the broader market, it signals a deliberate reweighting of public housing supply back into the central planning areas after two decades dominated by the Tengah-Punggol-Tampines new-town axis.

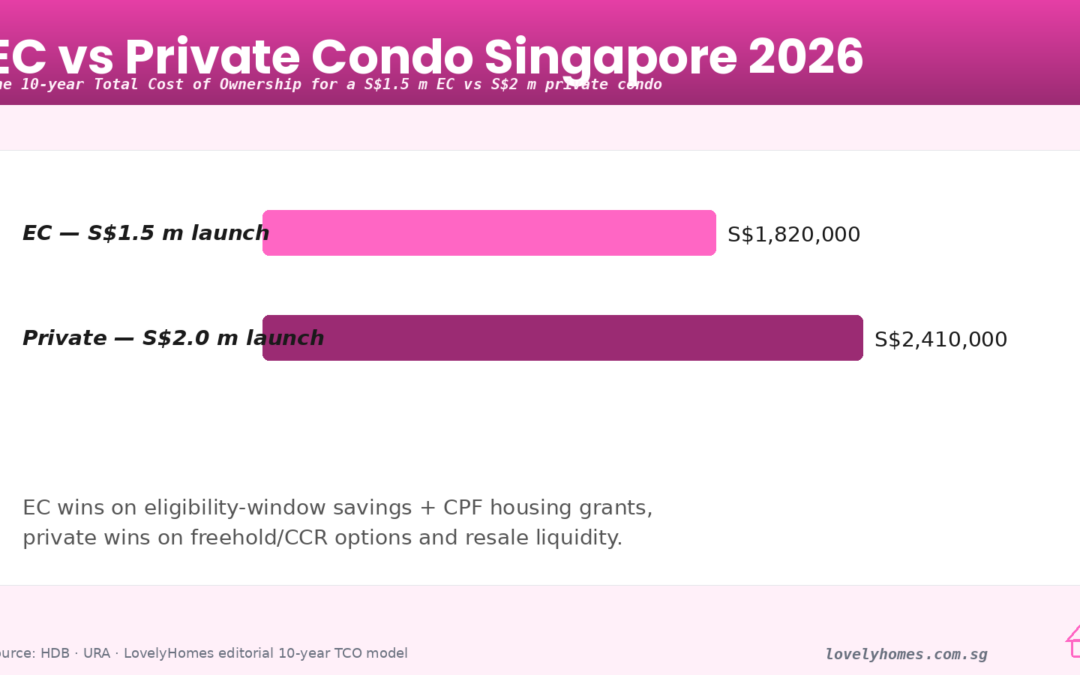

Stacked-bar TCO comparison for a Singaporean couple buying in 2026 — EC saves roughly S$0.9m over 10 years before post-MOP uplift.

Quick answer

For an eligible first-time Singaporean couple with household income under S$16,000/month, an Executive Condominium (EC) wins on almost every financial metric over a 10-year horizon. The purchase price is typically 25–30% lower than a comparable private condo, CPF grants can add up to S$30,000, mortgage interest savings compound, and the historical post-MOP capital gain has been 40–60% versus 18–28% for private condos. The trade-offs are the five-year Minimum Occupancy Period (MOP), restricted resale pool, and the 10-year wait before foreigners can buy.

What makes an Executive Condominium different

Executive Condominiums are a hybrid scheme introduced in 1996 to serve the “sandwich class” — households whose income exceeds the HDB Build-To-Order (BTO) ceiling of S$14,000/month but who cannot comfortably afford a private condo. ECs are built to identical specifications as private condos (same facilities, same PPVC construction, same architects and interior designers) but are sold under HDB rules for the first 10 years: buyers must meet income and citizenship eligibility, the Minimum Occupancy Period is five years, and resale during years five to ten is limited to Singapore Citizens and Permanent Residents. On year 10, the project is “privatised” and trades as a fully open-market private condo.

Who qualifies — the eligibility matrix

EC eligibility is gated on citizenship, family nucleus and the S$16,000/month Executive Income Scheme (EIS) ceiling — revised 1 January 2025.

The most common disqualifier in 2026 is income. HDB’s Executive Income Scheme ceiling was raised from S$14,000 to S$16,000 per month on 1 January 2025 — 28% higher than in 2019. This captures households where, for example, both spouses earn S$8,000 each. But for dual-income professional couples in their early thirties, it remains a binding constraint: bonus-laden earners in tech, legal and finance quickly cross the ceiling, and HDB uses a 12-month average.

Opening-day price gap — why ECs undercut private condos

The Government Land Sales price for EC sites is deliberately lower than equivalent private condo sites, reflecting the embedded subsidy in the scheme. In 2025 Otto Place EC (Tengah) and Novo Place EC (Plantation Close) launched at psf bands of S$1,450–S$1,650, while the closest private comparables (Parktown Residence in Tampines North, J’den in Jurong) transacted at S$2,200–S$2,550. That is a 30–35% discount before grants.

Cost component (10-yr)

Executive Condo (S$1.5m)

Private Condo (S$2.0m)

Difference

Purchase price

1,500,000

2,000,000

+500,000

Buyer’s Stamp Duty

44,600

64,600

+20,000

CPF grant (Family)

(30,000)

0

+30,000

Renovation + legal

60,000

70,000

+10,000

Mortgage interest (3.5% × 25 yr, 75% LTV)

310,000

470,000

+160,000

Maintenance (S$400 × 120 mo)

48,000

84,000

+36,000

Property tax (AV S$32k vs S$45k, owner-occupier)

36,000

72,000

+36,000

10-year all-in TCO

~1.968m

~2.761m

+793,000

Illustrative TCO. Maintenance, property tax and renovation are modelled at OCR-level ranges. Private condo assumes a typical 99-year OCR launch at S$2,000 psf for 1,000 sq ft.

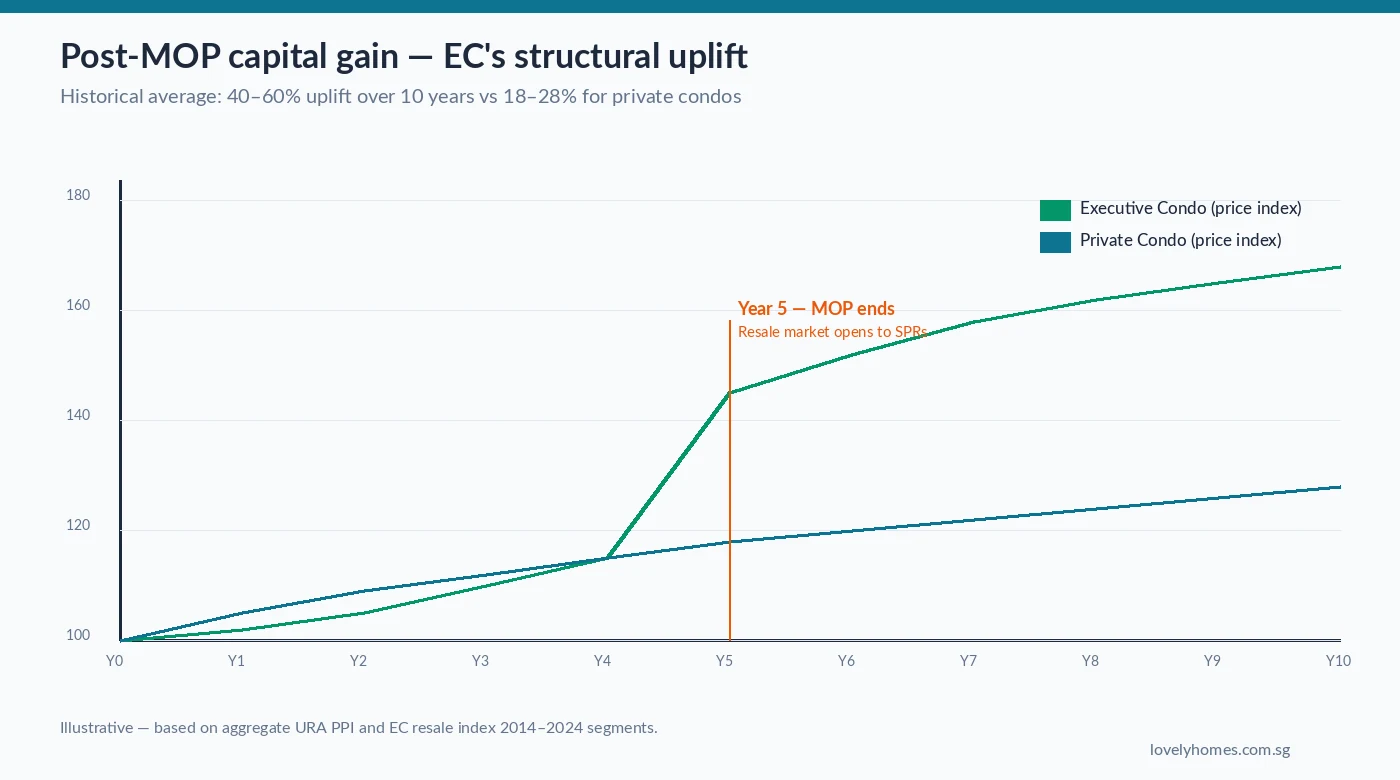

Post-MOP capital gain — the real alpha

Illustrative EC vs private-condo 10-year price index. Year 5 is the MOP inflection point — the resale pool opens to SPRs.

The structural advantage of ECs is that they cross-read into the private condo market on privatisation (Year 10). Because opening-day EC buyers paid a subsidised GLS price, the market gap closes as the scheme matures. URA resale data from 2014–2024 shows EC resale indices gaining 40–60% over a 10-year hold versus 18–28% for equivalent-vintage private condos, although the private condo sample is biased towards already-appreciated central assets. The Y5–Y7 window is where the step-change happens because the SPR resale pool opens after MOP.

MOP, resale restrictions and the 10-year staircase

Years 1–5 (MOP): Must occupy. Cannot rent the entire flat (room rentals allowed subject to HDB rules). Cannot sell.

Years 5–10: Resale open to Singapore Citizens and Permanent Residents. Cannot sell to foreigners or companies. Must still meet HDB resale conditions (no ABSD on the SPR buyer is the key attraction).

Year 10 onwards (privatisation): The project is fully privatised. Foreigners can buy. Project becomes indistinguishable from a regular private condo.

Most owners who flip for capital gain do so at Year 5.5 to Year 7 — post-MOP when the discount to private condos is widest and demand from upgrader SPRs peaks. Owners who hold through privatisation also do well, but market timing matters more because the privatisation often coincides with one of the 7–10 year macro cycles.

When the private condo is the better choice

Income over S$16,000/month — you are ineligible for EC, no further analysis needed.

You value liquidity — private condos can be sold anytime. ECs cannot be sold during MOP, even in emergencies, without HDB consent.

You want a CCR / RCR address — ECs are only built on OCR GLS sites (Tengah, Plantation Close, Tampines, Punggol, Woodlands). If you need Orchard, Bukit Timah or the Southern Waterfront, you must go private.

You plan to rent the whole unit early — ECs forbid full-unit rental during MOP. Private condos can be rented from Day 1.

You want to buy under a company / trust — not allowed for ECs.

You are buying as an investment, not a home — the EC scheme is designed for owner-occupation. The MOP makes pure-investment arithmetic work poorly.

Forward view for 2026 launches

Two 2026 EC launches anchor the calendar: Otto Place EC (Tengah Garden Walk, ~600 units) and Novo Place EC (Plantation Close, ~500 units). Both are priced into the S$1,500–S$1,700 psf band for quality-finished units and have benefited from the EIS ceiling increase to S$16,000 — the pre-booking registrations at both projects reportedly exceed available unit counts by 4–5×. Private comparables in the same 2026 window include ELTA (Clementi Avenue 1, OCR) and Promenade Peak (Zion Road, CCR) — both at S$2,300–S$2,800 psf. The 2026 market therefore offers a cleaner-than-usual EC vs private A/B test.

FAQ

1. Can a single Singaporean buy an EC?

Not under the Public Scheme. Singles aged 35+ can only buy an EC under the Joint Singles Scheme with another single, or under the Fiancé/Fiancée Scheme with a Singaporean partner.

2. Is there an ABSD on an EC purchase?

No, not for the buyer — EC is treated as a first property (provided you sell your existing HDB within six months and do not own any other residential). BSD applies at the standard slabs.

3. What is the resale levy on moving from HDB to EC?

A resale levy of S$50,000 (3-room), S$45,000 (4-room), S$55,000 (5-room) or S$60,000 (Executive) applies if you previously enjoyed a first-timer HDB benefit. The levy is deducted from sale proceeds at the EC purchase.

4. How much CPF can I use for an EC?

Subject to the Valuation Limit (100% of the lower of purchase price or valuation) and the Withdrawal Limit (120% of VL). TDSR caps total monthly debt at 55% of gross income; MSR caps EC-specific mortgage at 30% of gross income — whichever is tighter applies.

5. What happens if our income exceeds S$16k/month during MOP?

Nothing — the ceiling applies at the point of application. You will not lose the unit if your income grows after the OTP is exercised.

6. Can the EC grant be refunded if I sell?

The grant plus CPF accrued interest (2.5% p.a. notional) must be returned to your CPF-Ordinary Account at resale. It is a timing friction, not a permanent loss.

7. Do ECs qualify for the Enhanced Housing Grant (EHG)?

Yes, for first-timer households earning under S$9,000/month (up to S$30,000 in EHG tiers). Above that band, EC buyers receive only the CPF Housing Grant if eligible.

8. Is the 5-year MOP counted from key collection or from OTP?

From key collection (TOP), not OTP. So a 2026-booked EC with a 2029 TOP hits MOP in 2034 and privatises in 2039.

9. Can I rent out rooms during MOP?

Yes, subject to HDB rules: maximum 6 occupants including the owner, registered subletting arrangements, no short-term stays. The entire unit cannot be rented.

10. How does the 10-year privatisation affect value?

Privatisation removes the buyer-eligibility restrictions, widening the pool to foreigners and entities. Historically this produces a small upward step (3–5%) in resale psf on privatisation week, but the bulk of the EC-vs-private gap closes between Years 5 and 8.

This article is general information, not personal financial or tax advice. CPF rules, HDB eligibility criteria, EHG amounts, BSD slabs and Green Mark certification pathways change. Figures are illustrative and based on HDB, CPF Board and IRAS published rules as at February 2025 (Budget 2025). Always verify the current position at hdb.gov.sg, cpf.gov.sg and iras.gov.sg before acting.

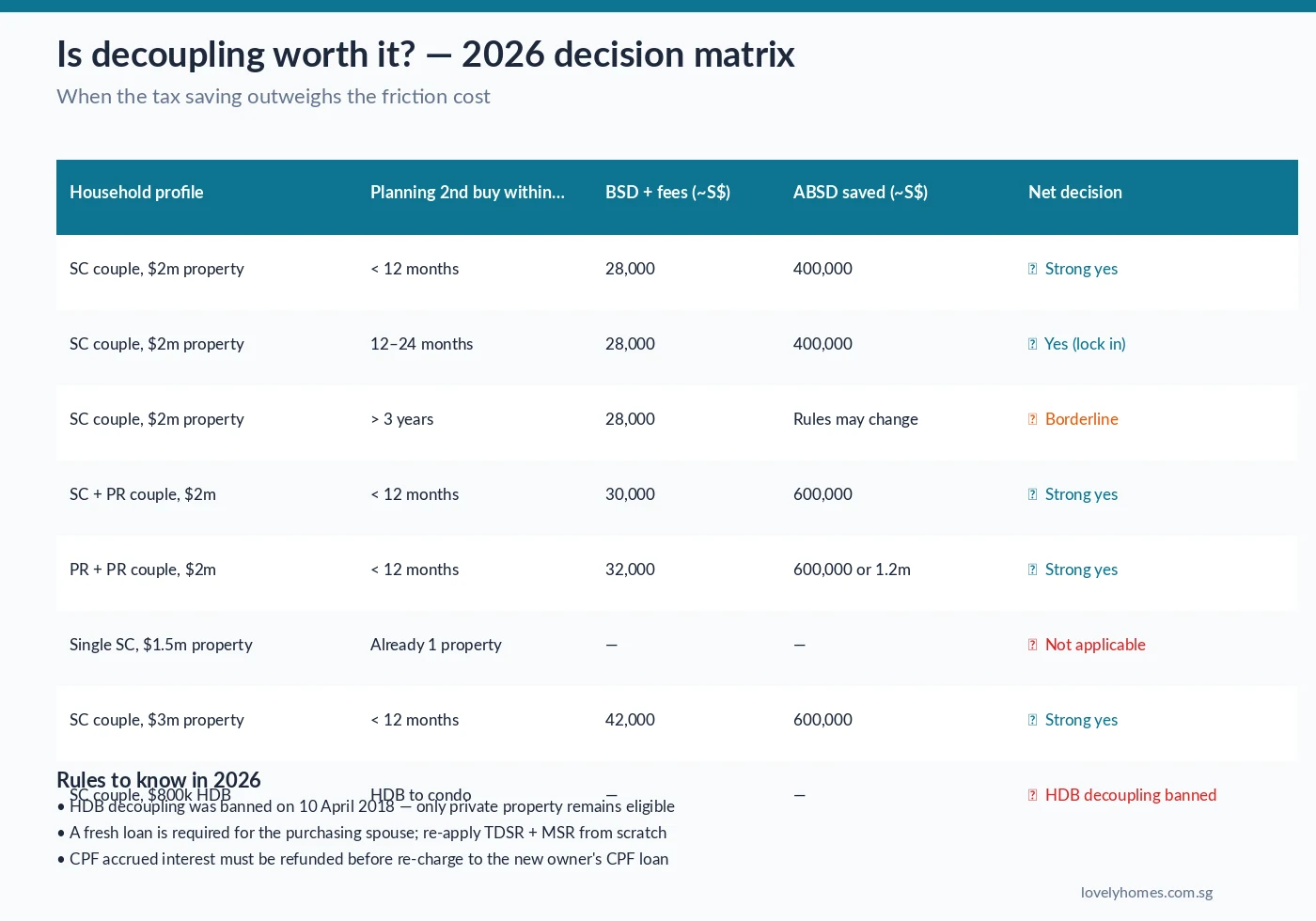

Worked example — same S$2m property, same half-share transfer, different ABSD era.

Quick answer

Yes — decoupling still pencils out in 2026 for most Singaporean couples planning a second property within two years. The Buyer’s Stamp Duty (BSD) on a half-share transfer is typically S$24,000–S$44,000 all-in, while the Additional Buyer’s Stamp Duty (ABSD) saving on a ~S$2m second property runs S$400,000–S$600,000 depending on citizenship. What has changed is the tolerance window: with ABSD now at 60% for foreigners (from 30%) and 20% for a Singapore citizen’s second property (from 17%), decoupling only makes sense if the second purchase is imminent and funded; otherwise you are paying the BSD upfront for an option you may never exercise.

What “decoupling” actually means

In Singapore property practice, decoupling is the act of transferring one spouse’s share in a jointly-owned private residential property to the other spouse, so that the selling spouse is legally recorded as owning zero properties and can therefore buy a second home without paying the punitive ABSD rate that applies to a Singapore citizen’s second property (20% since 15 February 2025, up from 17%). The buying spouse takes full title to the original home and refinances the mortgage in their own name.

Importantly, decoupling has been banned for HDB flats since 10 April 2018 — the Housing & Development Board will not register a share transfer between owners unless one of the narrow exceptions applies (divorce, financial hardship, renunciation of citizenship). The strategy only works on fully-paid or refinanceable private residential property: condominiums, executive condominiums that have crossed the 10-year privatisation mark, cluster houses, and landed homes.

Why the calculus changed in 2023–2025

Before the 27 April 2023 ABSD hike, the arithmetic was straightforward. A Singaporean couple buying a second S$2m property would pay 17% ABSD (S$340,000). Decoupling the first home cost S$24,600 of BSD plus ~S$5,000 in legal and valuation fees — a net saving of roughly S$310,000. Every tax-literate married couple who could decouple did decouple.

Then the cooling measures stacked up:

27 April 2023 — ABSD for Singapore citizens’ 2nd property raised from 17% to 20%; PR 2nd property from 25% to 30%; foreigner flat rate from 30% to 60%; entities from 35% to 65%.

14 August 2024 — Mortgage Servicing Ratio and Total Debt Servicing Ratio floors tightened, eroding the loan quantum the buying spouse can re-underwrite.

15 February 2025 — the ABSD 6-year remission window for couples was clarified but not broadened; BSD upper marginal rate raised to 6% on the portion above S$1.5m and 5% on S$1.5m–S$3m, making decoupling more expensive than before even though the ABSD saving also grew.

The absolute saving from decoupling in 2026 is larger than it was in 2022 (because 20% of S$2m is more than 17% of S$2m). But the friction cost is also higher, and the optionality risk — paying BSD for a second purchase you end up not making — has become the decisive variable.

Worked example: S$2m property held 50/50 by a Singaporean couple

Spouse A transfers her 50% share to Spouse B for the market value of S$1,000,000. Spouse B takes out a fresh loan for his portion, CPF is refunded to Spouse A, and the title is updated by the Singapore Land Authority.

Break-even at a second-property purchase price of ≈ S$165,000

Break-even on decoupling is reached if Spouse A ever buys a second property worth more than ~S$165k — effectively any private property.

The 2026 decision matrix

Eight household profiles mapped against timing. The green checkmarks cluster where the second purchase is within 12 months.

Two patterns emerge from the matrix. First, timing is now the most sensitive variable. The longer the window between decoupling and the second purchase, the higher the chance that new cooling measures, ABSD rate changes, or personal circumstances (a promotion bumping household income, a medical event, a relocation) invalidate the plan. Second, higher-quantum households benefit more — the BSD on a half-share of a S$3m property is about S$42,000, but the ABSD saving on an equivalent S$3m second purchase is S$600,000. The saving-to-friction ratio is most attractive in the S$2m–S$4m property band.

The 10- to 14-week process

From engaging separate conveyancers to completion of CPF charge discharge.

A clean decoupling — where the buying spouse has the loan capacity and CPF on hand — takes ten weeks end-to-end. The critical path is the fresh loan underwriting: the purchasing spouse’s TDSR and MSR are re-evaluated from scratch, which can trip up households where one spouse holds most of the CPF or bank-qualified income. Couples should get an in-principle approval from the chosen bank before committing to the decoupling, not after.

What can go wrong

IRAS anti-avoidance challenge — Section 33A of the Stamp Duties Act allows IRAS to recharacterise a transaction it considers tax-motivated without commercial substance. In the 2024 Boon Suan decision, the taxpayer’s decoupling was upheld as legitimate, but the bar was set higher for sham pricing and circular-loan structures. Stick to market valuations.

Second purchase never happens — if the buying spouse loses income or the target property does not materialise, the BSD paid on decoupling is sunk cost.

CPF accrued interest shortfall — Spouse A must refund the CPF used plus notional 2.5% accrued interest; if the half-share valuation is below the original CPF contribution, the shortfall must be topped up in cash.

New cooling measure tightens ABSD further — the strategy protects against the current 20% rate but not against future ones. Most practitioners think the 2023 hike is the ceiling for this cycle, but the 2011 / 2013 / 2018 precedents warn against assuming rates only go up in one direction.

Alternatives that work better for some households

Decoupling is not the only way to buy a second property as a married couple. Consider:

Buy under one spouse’s name from day one — if you are still house-hunting for the first property, avoid joint ownership unless CPF or loan structure requires it. This sidesteps the decoupling cost entirely.

Buy under an adult child’s name — ABSD still applies at the child’s citizenship rate, but there is no decoupling friction. Watch the implications for estate planning and HDB eligibility.

Pay the ABSD and claim remission on subsequent sale of the first home within 6 years — the ABSD remission for married Singaporean couples (IRAS e-Tax Guide, Feb 2025) returns the full 20% if the first home is sold within 6 years of the second purchase.

Switch to commercial property or REITs — no ABSD applies, at the cost of a different tax and yield profile.

Forward view — what could change the calculus again

The two biggest “regime change” risks to a 2026 decoupling plan are (a) a further ABSD hike on SC second properties above 20%, which would deepen the saving but also lengthen the tolerance window on BSD paid today, and (b) IRAS pattern-matching against half-share transfers. The Ministry of Finance’s February 2025 Budget maintained the current ABSD structure and signalled that policy attention had moved to the supply side — BTO, GLS and EC launches — rather than further demand-side measures. Practitioners expect stability through 2026, which is also the planning horizon most couples need.

FAQ

1. Can we decouple our HDB flat?

No — HDB decoupling was banned on 10 April 2018 except in narrow circumstances (divorce, bankruptcy, renunciation of citizenship).

2. How long after decoupling must we wait before buying the second property?

There is no minimum waiting period — the second purchase can complete the day after the decoupling completes. Many couples schedule the OTP for the second property within two weeks.

3. Does decoupling trigger Seller’s Stamp Duty (SSD) on the original property?

Yes if the original property was bought less than three years ago. The half-share transfer counts as a “disposal” for SSD purposes: 12% of value in Year 1, 8% in Year 2, 4% in Year 3, 0% thereafter.

4. Can we pay for the half-share transfer using CPF?

Yes, subject to CPF Withdrawal Limits and Valuation Limit rules. The buying spouse’s CPF-OA can pay the half-share consideration exactly as if it were a resale purchase.

5. What’s the BSD rate on a S$1m half-share?

Applying the current BSD slabs: 1% on the first S$180k + 2% on the next S$180k + 3% on the next S$640k + 4% on the final S$0 of the first S$1m = S$24,600 total. On a S$1.5m half-share it would be S$44,600.

6. Is legal advice mandatory?

Not mandatory, but two independent conveyancers are strongly recommended — one for the transferring spouse, one for the receiving spouse — because their interests diverge even within a marriage.

7. Can we decouple a property still under its 3-year SSD window?

Technically yes, but the SSD charge usually wipes out the ABSD saving. Wait until the property has crossed the 3-year SSD threshold.

8. Does the buying spouse need to physically move in?

No — the buying spouse becomes sole legal owner but occupancy of a spouse is not disturbed. The property remains the matrimonial home.

9. If the second property is a new launch, when is the ABSD paid?

Within 14 days of the Option to Purchase being exercised (at booking), regardless of TOP date. IRAS stamps the OTP — not the later SPA — for ABSD purposes.

10. What if we want the second property to be joint-name?

Then decoupling does not help — ABSD applies at the rate of the highest-owning party in a joint purchase (20% for an SC who already owns a property). You would need to buy the second in the selling spouse’s sole name.

This article is general information, not personal tax, financial or legal advice. Stamp duty rates, CPF rules and ABSD remission criteria are subject to change without notice. Always obtain advice from an IRAS-registered conveyancer and tax professional before executing a decoupling. Figures are illustrative and based on IRAS e-Tax Guide on Stamp Duties published February 2025; see iras.gov.sg for the current position.

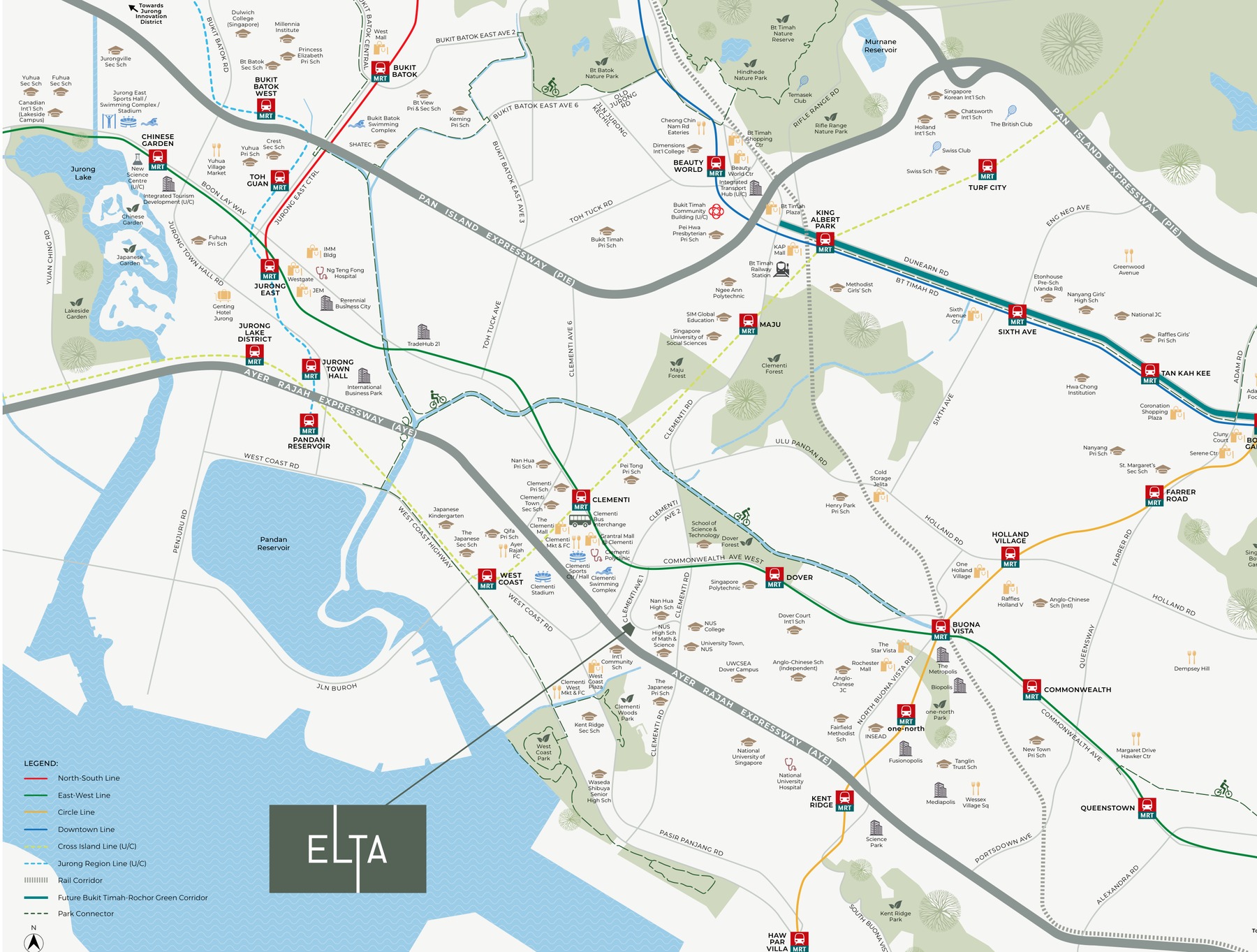

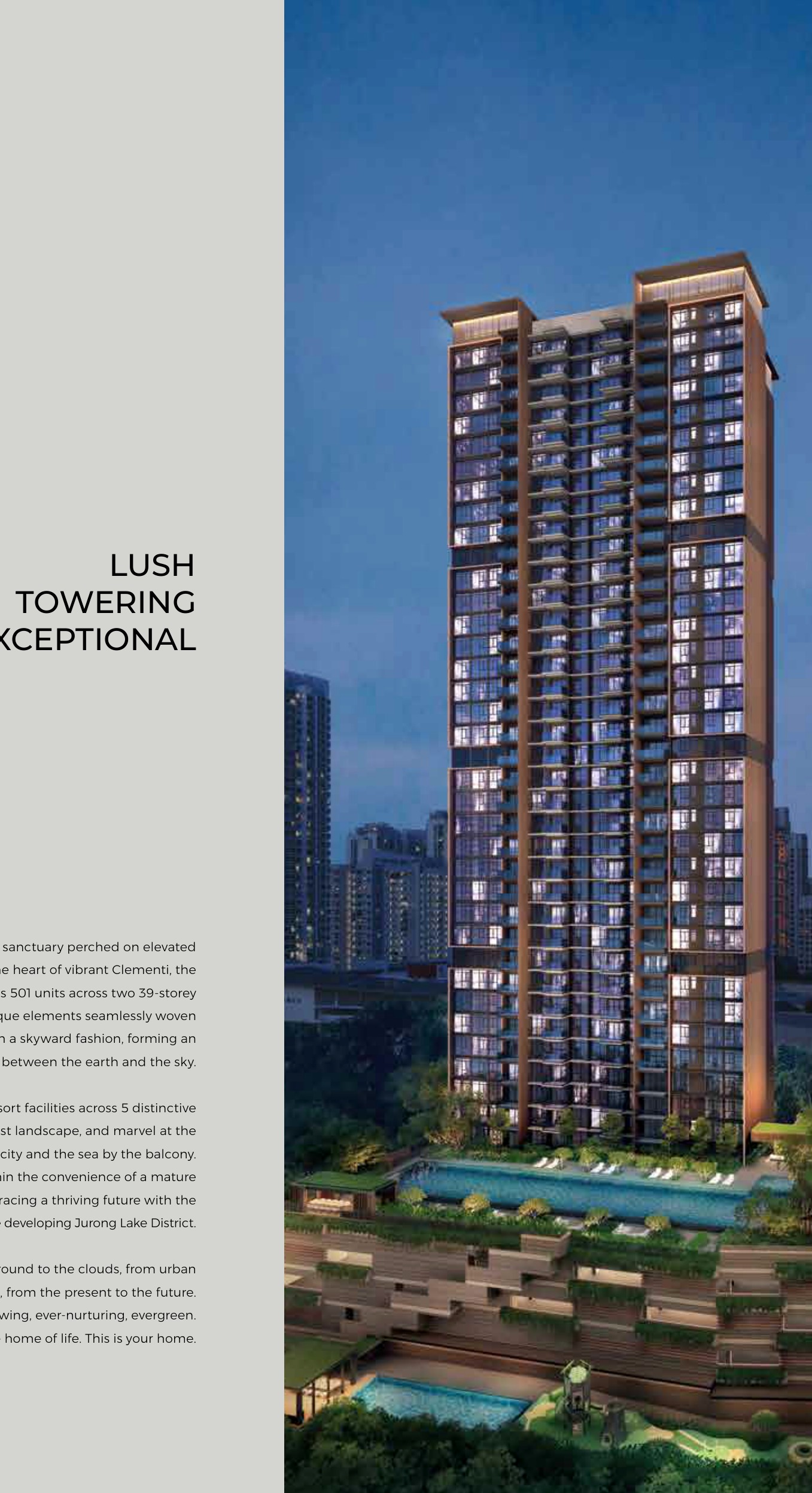

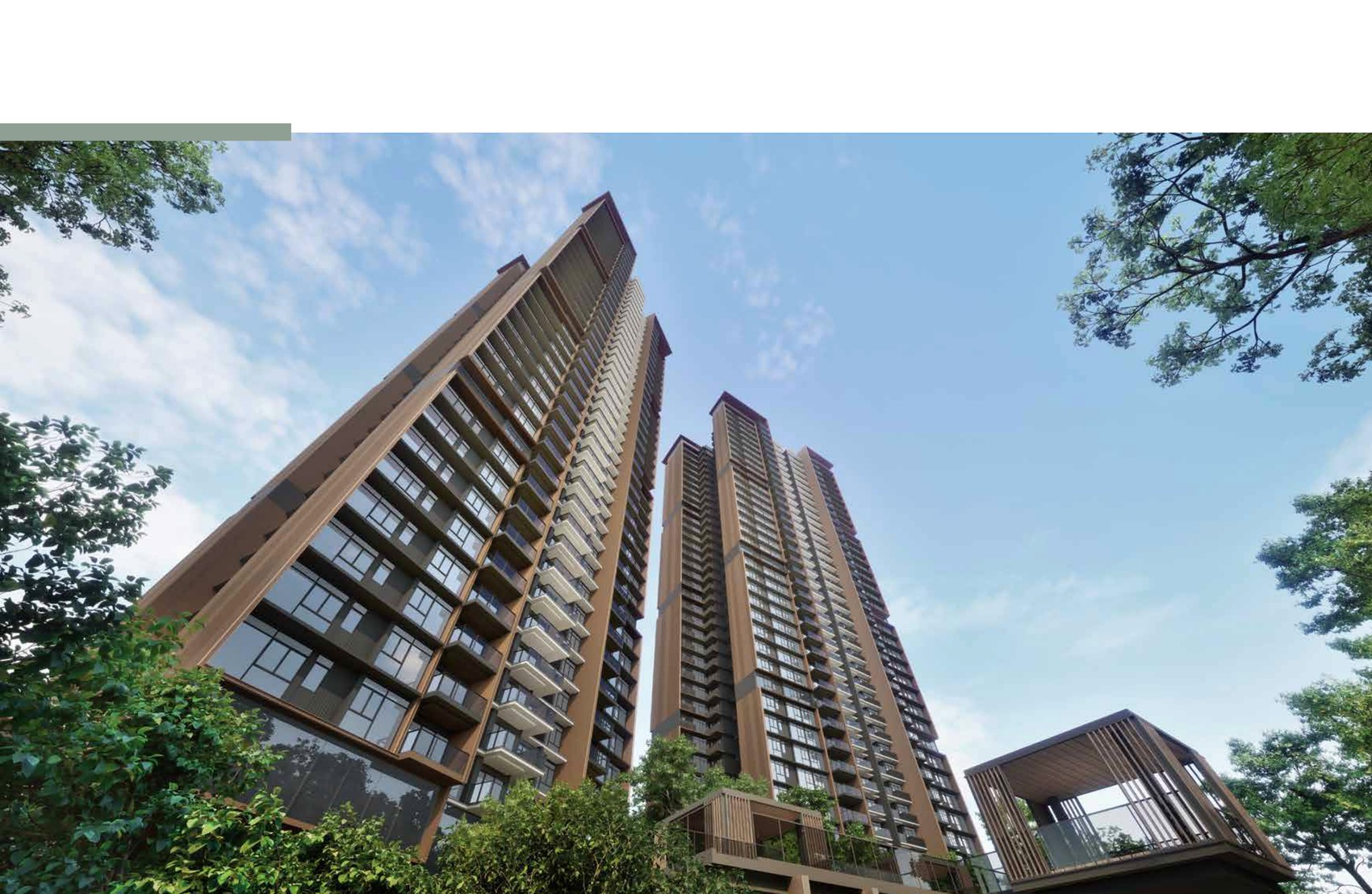

ELTA is a 501-unit Clementi Avenue 1 condominium across two 39-storey towers with a basement, 3-storey multi-storey carpark, swimming pool and communal facilities.

01 · Location

D05 Address

10 and 12 Clementi Avenue 1, Singapore 129633 / 129632

02 · Scale

501 residential units

2 blocks of 39-storey residential towers

03 · Pricing

From S$1.397M

Available units from S$1.397M; 1BR+Study from S$1.397M, 3BR from S$2.622M, 4BR from S$3.286M, 5BR from S$3.906M (16 Apr 2026 public balance-unit snapshot).

Project At-a-Glance

Project Name

ELTA

Address

10 and 12 Clementi Avenue 1, Singapore 129633 / 129632

District

D05

Tenure

99 years commencing from 13 February 2024

Developer

HC Land (Clementi) Pte. Ltd. (JV between MCL Land and CSC Land Group)

Total Units

501 residential units

Site Area

Approx. 13,451.10 sqm / 144,788 sqft

Plot Ratio

3.5

Blocks

2 blocks of 39-storey residential towers

Expected TOP

31 March 2029

Legal Completion

31 March 2032

Current Price

Available units from S$1.397M; 1BR+Study from S$1.397M, 3BR from S$2.622M, 4BR from S$3.286M, 5BR from S$3.906M (16 Apr 2026 public balance-unit snapshot).

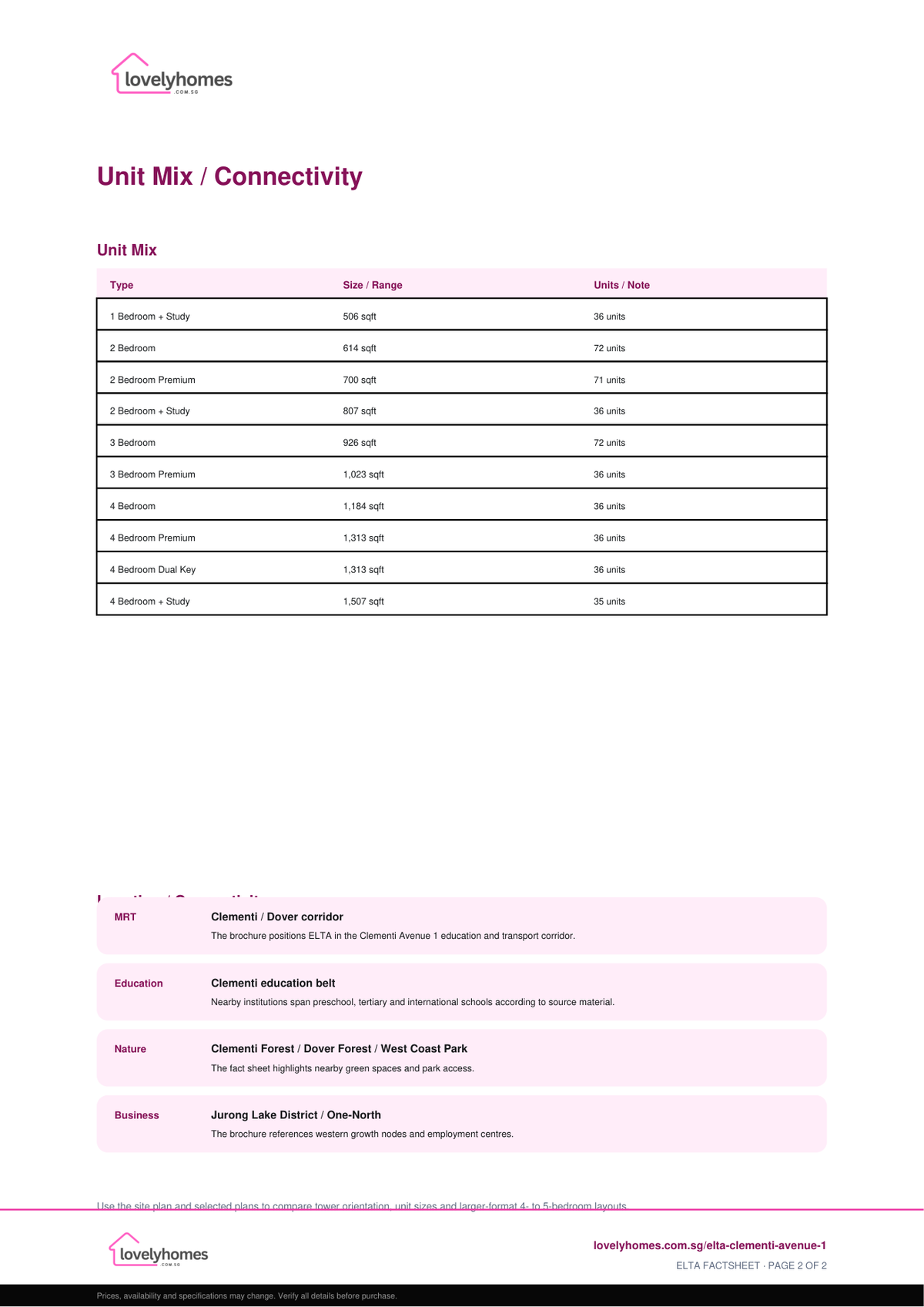

Unit Mix and Sizes

Bedroom Type

Size (sqft)

Units

% of Total

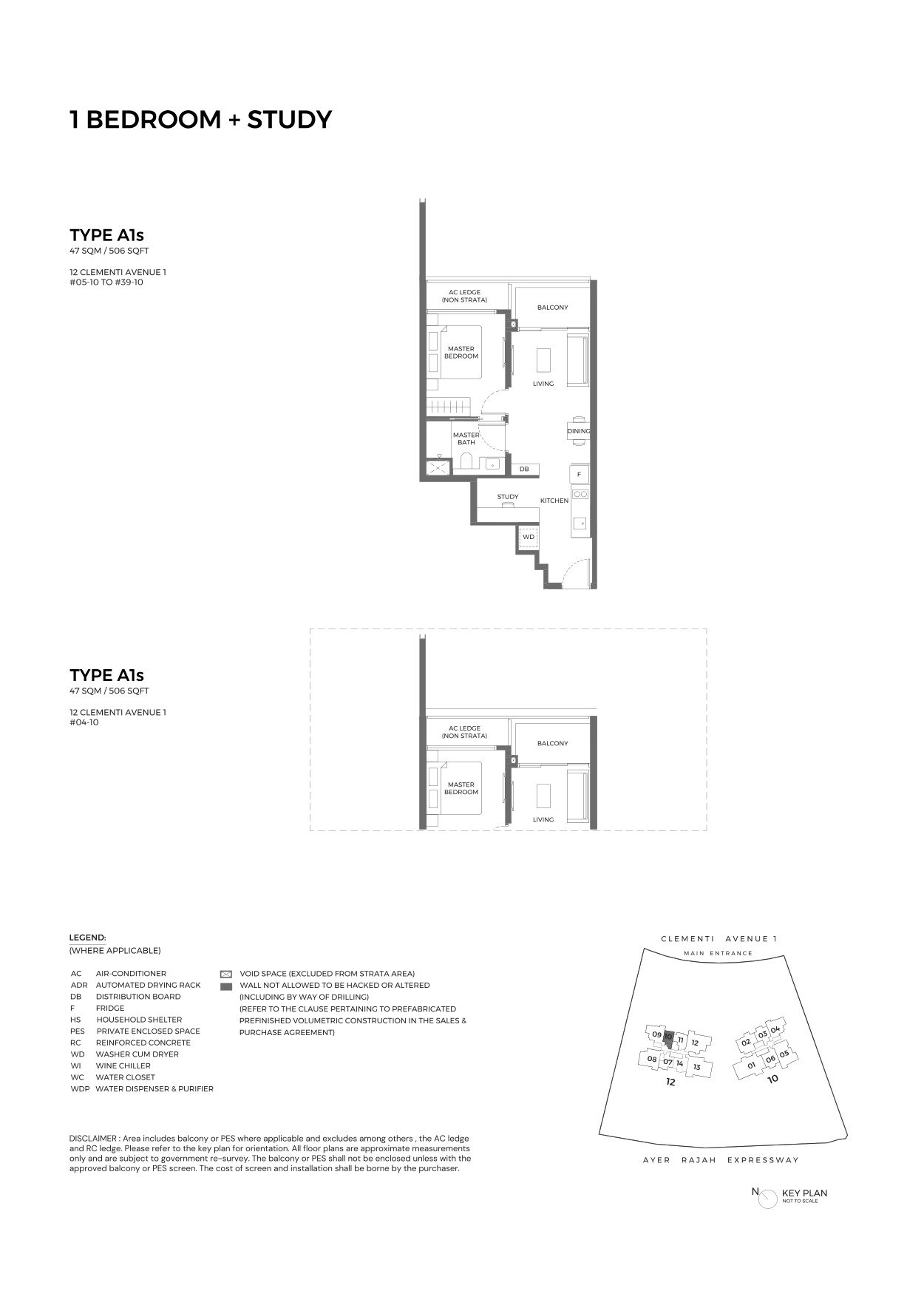

1 Bedroom + Study

506 sqft

36 units

7.2%

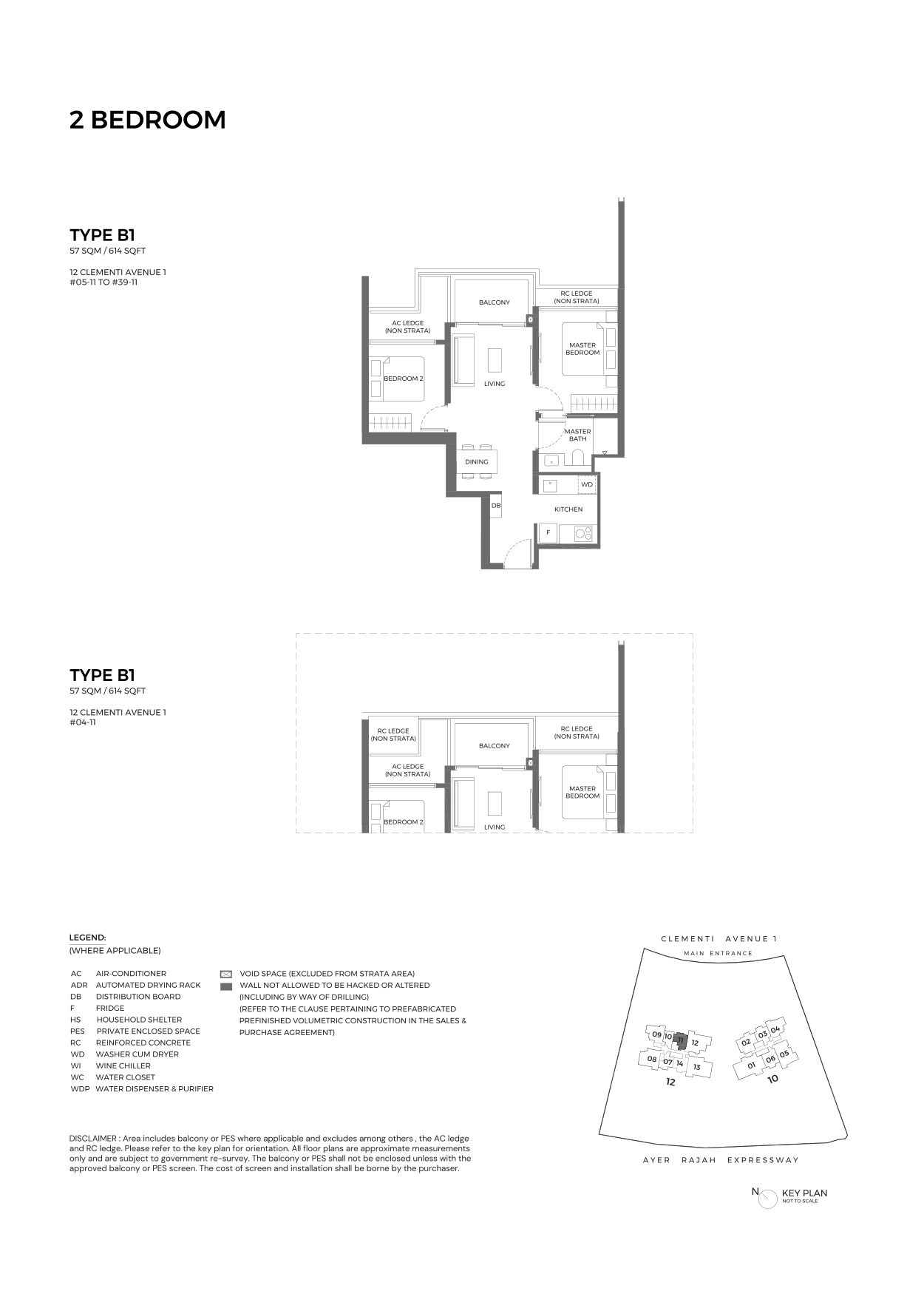

2 Bedroom

614 sqft

72 units

14.4%

2 Bedroom Premium

700 sqft

71 units

14.2%

2 Bedroom + Study

807 sqft

36 units

7.2%

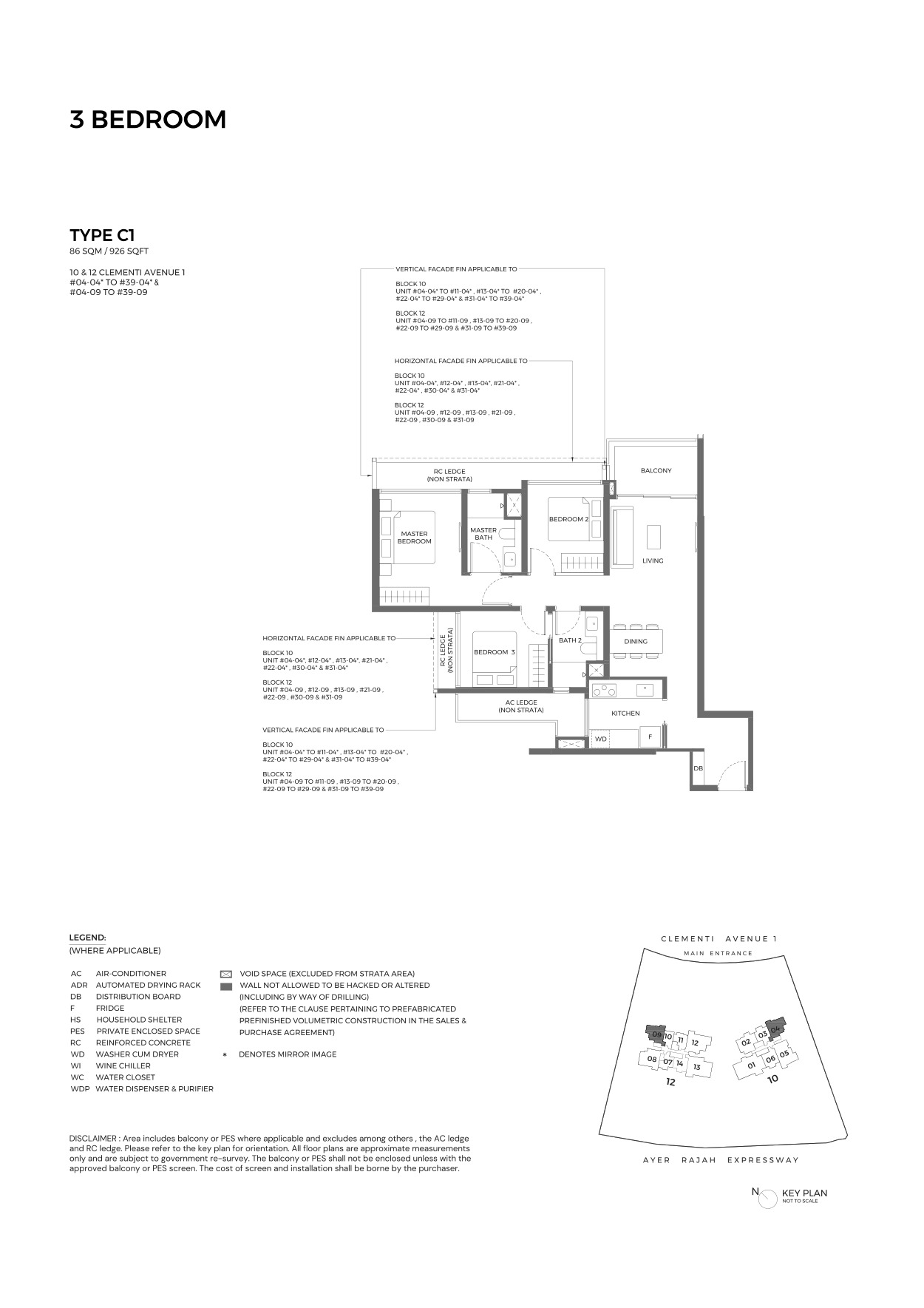

3 Bedroom

926 sqft

72 units

14.4%

3 Bedroom Premium

1,023 sqft

36 units

7.2%

4 Bedroom

1,184 sqft

36 units

7.2%

4 Bedroom Premium

1,313 sqft

36 units

7.2%

4 Bedroom Dual Key

1,313 sqft

36 units

7.2%

4 Bedroom + Study

1,507 sqft

35 units

7.0%

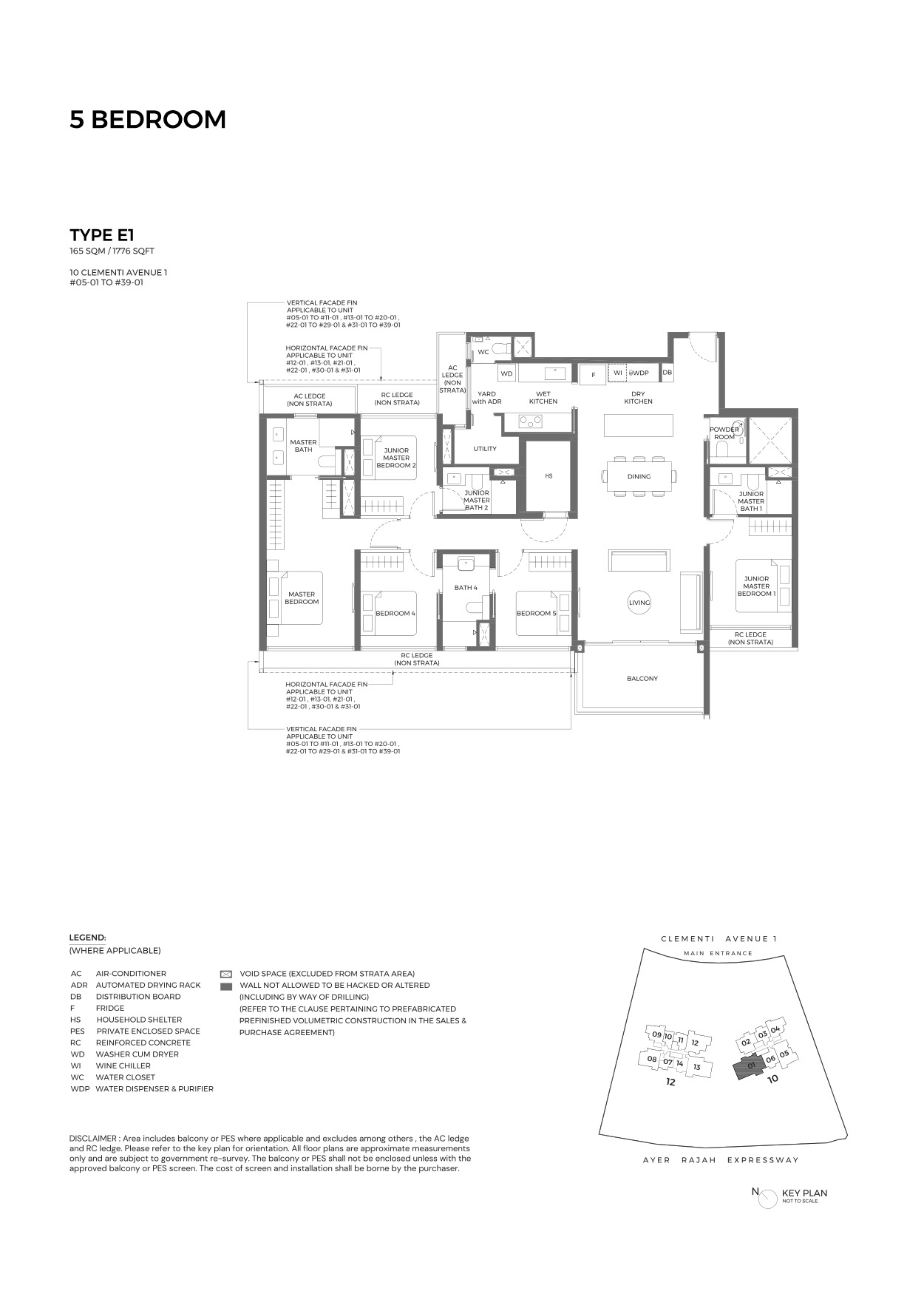

5 Bedroom

1,776 sqft

35 units

7.0%

Total

–

501 units

100%

Bedroom Type

Size / Range

Units

Current Indicative Price

1 Bedroom + Study

506 sqft

36 units

From S$1.397M

2 Bedroom

614 sqft

72 units

Sold out in checked balance snapshot

2 Bedroom Premium

700 sqft

71 units

Sold out in checked balance snapshot

2 Bedroom + Study

807 sqft

36 units

From S$2.263M

3 Bedroom

926 sqft

72 units

From S$2.622M

3 Bedroom Premium

1,023 sqft

36 units

From S$2.930M

4 Bedroom

1,184 sqft

36 units

From S$3.286M

4 Bedroom Premium

1,313 sqft

36 units

From S$3.476M

4 Bedroom Dual Key

1,313 sqft

36 units

From S$3.266M

4 Bedroom + Study

1,507 sqft

35 units

From S$3.495M

5 Bedroom

1,776 sqft

35 units

From S$3.906M

Pricing note: Pricing cross-checked against ELTA public balance-unit snapshot dated 16 Apr 2026, accessed 29 Apr 2026. Prices and availability can change without notice.

Indicative Pricing

Entry Units

From S$1.397M

1BR + Study, 506 sqft

3BR Units

From S$2.622M

3BR, 926 sqft

5BR Units

From S$3.906M

5BR, 1,776 sqft

Available units from S$1.397M; 1BR+Study from S$1.397M, 3BR from S$2.622M, 4BR from S$3.286M, 5BR from S$3.906M (16 Apr 2026 public balance-unit snapshot).

Why Buyers Are Watching

1

501 units across two 39-storey towers in Clementi.

2

Tenure is 99 years from 13 February 2024.

3

Fact sheet states over 50 resort-style facilities across five zones.

4

Near Clementi Forest, Dover Forest and West Coast Park.

5

Source fact sheet lists 401 car park lots, including 5 EV charging lots and 5 accessible lots.

6

Expected vacant possession is 31 March 2029.

Location and Connectivity

MRT

Clementi / Dover corridor

The brochure positions ELTA in the Clementi Avenue 1 education and transport corridor.

Education

Clementi education belt

Nearby institutions span preschool, tertiary and international schools according to source material.

Nature

Clementi Forest / Dover Forest / West Coast Park

The fact sheet highlights nearby green spaces and park access.

Business

Jurong Lake District / One-North

The brochure references western growth nodes and employment centres.

Schools Nearby

School Notes

Nan Hua High, NUS High, Singapore Polytechnic, NUS and other Clementi-area institutions are referenced in source materials; verify distance bands.

Verification

Confirm current home-school distance bands with OneMap and MOE SchoolFinder before enrolment planning.

Lifestyle and Amenities

Transport

Use the location map and latest routing to compare MRT, bus and road access.

Daily Amenities

Review malls, supermarkets, food centres and services around the site.

Recreation

Compare nearby parks, clubs and leisure nodes against your household routine.

Site Plan

Site plan · indicative only · subject to developer confirmation

Floor Plans (Selected)

Representative plans from available bedroom types. Download the full PDF below for broader stack-by-stack layout review.

1 Bedroom + Study Type AS1

2 Bedroom Type B1

3 Bedroom Type C1

4 Bedroom Type D1

5 Bedroom Type E1

Full Floor Plans PDF

Selected layout pages and unit dimensions for buyer review.

10 and 12 Clementi Avenue 1, Singapore 129633 / 129632

What is the current from-price?

Available units from S$1.397M; 1BR+Study from S$1.397M, 3BR from S$2.622M, 4BR from S$3.286M, 5BR from S$3.906M (16 Apr 2026 public balance-unit snapshot).

How many units are there?

501 residential units

Where can I get the floor plans?

Use the selected thumbnails above or download the full floor-plan PDF.

Ready to see ELTA in person?

Request latest prices, balance-unit stacks, floor plans and viewing slots.

Disclaimer. Prices, unit mix, specifications, site plans, floor plans and facility lists on this page are indicative only and subject to change by the developer without notice. Pricing snapshots are compiled from public balance-unit/price-list references checked on 29 April 2026. LovelyHomes.com.sg is not the project developer. Prospective buyers should consult an accredited salesperson and the developer’s official sales kit before committing to any purchase. Artist impressions are for illustrative purposes only and may differ from the final built product.