Quick Answer — Seller’s Stamp Duty (SSD) in Singapore

SSD is a tax payable by the seller of a Singapore residential property if it is sold within 3 years of purchase.

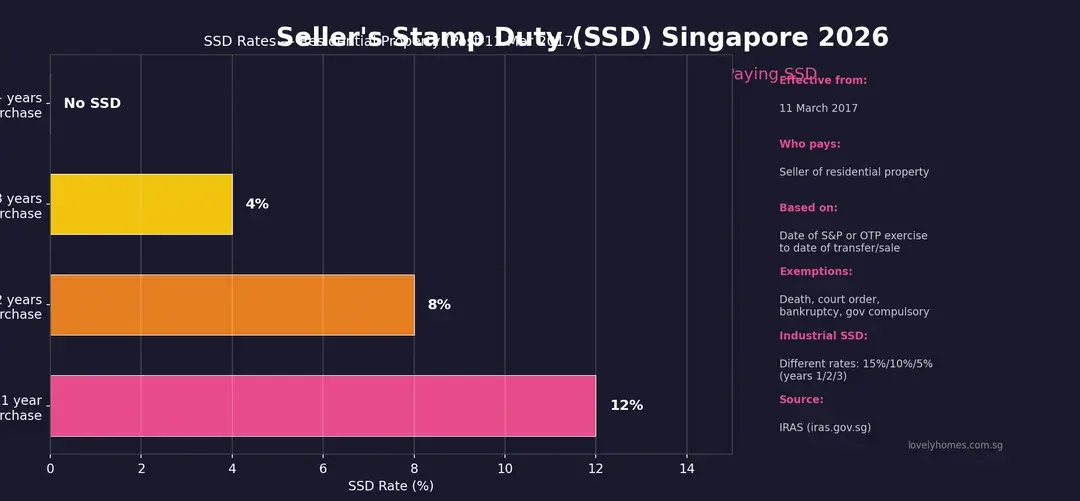

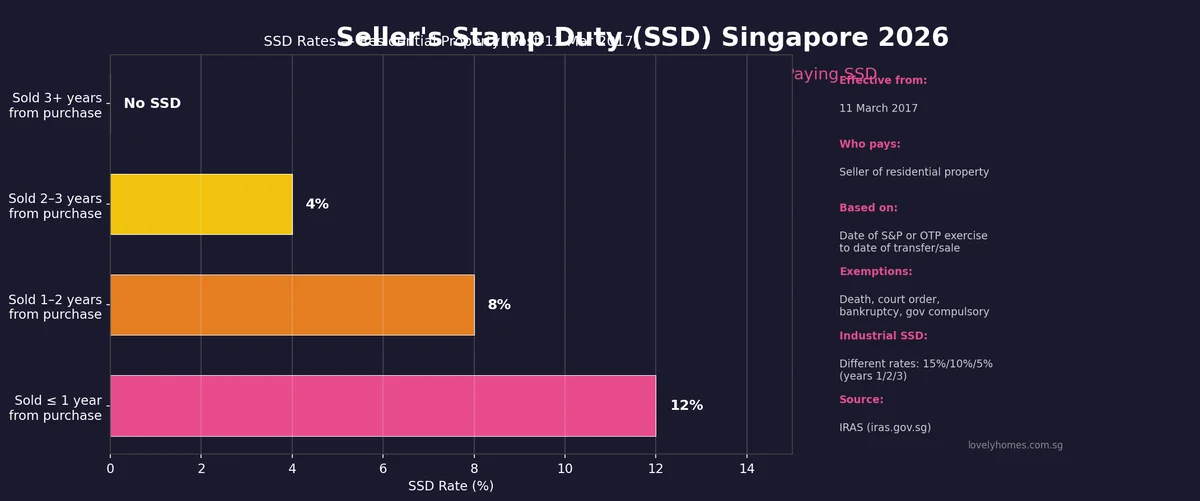

Rate is 12% if sold within 1 year, 8% if sold in Year 2, and 4% if sold in Year 3. No SSD after 3 years.

SSD is calculated on the higher of the sale price or the property’s market value at the time of sale.

Current rates have been in force since 11 March 2017 — unchanged through multiple rounds of cooling measures since.

Key exemptions: disposal by court order, bankruptcy proceedings, Government compulsory acquisition, and transfer due to death of owner.

Industrial property has different SSD rates: 15% (Year 1), 10% (Year 2), 5% (Year 3) — and a 3-year holding period applies.

Figure 1: Seller’s Stamp Duty (SSD) Singapore 2026 — rates by holding year for residential property. Source: IRAS.

What is Seller’s Stamp Duty (SSD)?

Seller’s Stamp Duty is a property transaction tax introduced by the Singapore Government as a property market cooling measure. It targets short-term speculators and property flippers — buyers who purchase residential property intending to sell quickly for a profit. The SSD creates a disincentive to sell within the first three years of purchase by imposing a tax on the sale proceeds, calibrated to be punishing in Year 1 (12%), moderately deterring in Year 2 (8%), and mildly deterring in Year 3 (4%), with no penalty after Year 3.

SSD was first introduced on 20 February 2010 during the first wave of post-Global Financial Crisis cooling measures. Since then, the rates and holding period have been revised multiple times. The current regime — 12%/8%/4% across a 3-year holding period — was established on 11 March 2017, when the Government eased the rules from the previous 16%/12%/8%/4% four-year regime. This easing was the last SSD adjustment to date; despite multiple ABSD increases in 2021, 2022 and 2023, SSD has remained unchanged.

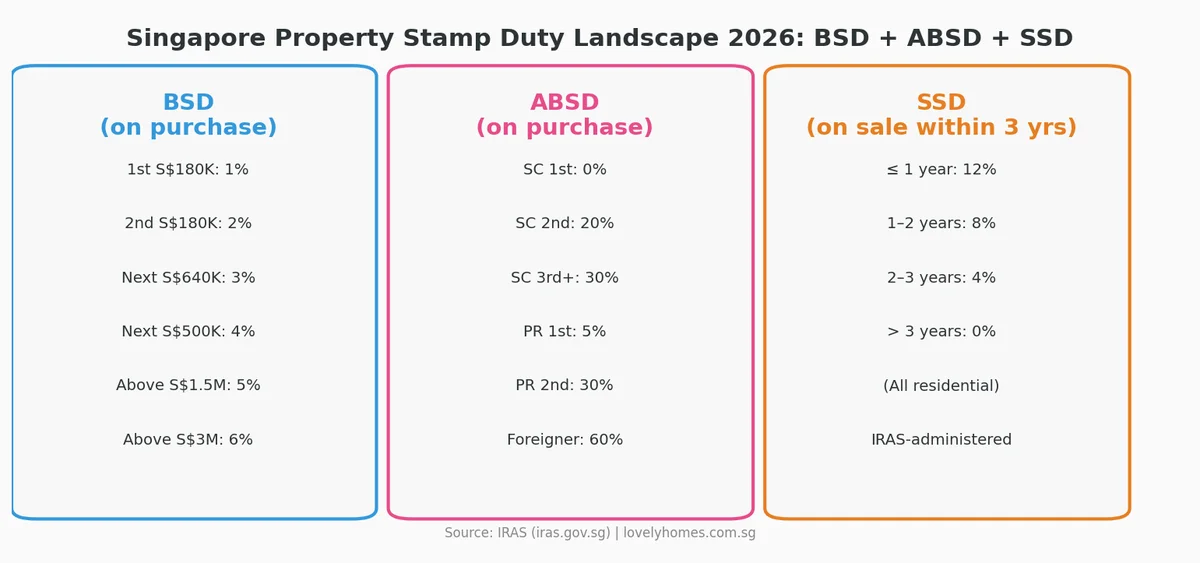

Figure 3: Singapore’s three property stamp duties at a glance — BSD (purchase), ABSD (purchase, ownership-count dependent), and SSD (sale within 3 years). Source: IRAS.

SSD rates for residential property — current (from 11 March 2017)

Holding Period

SSD Rate

Example (S$1.5M property)

Year 1 (sold within 12 months of purchase)

12%

~S$180,000 on a S$1.5M property

Year 2 (sold 12–24 months after purchase)

8%

~S$120,000 on a S$1.5M property

Year 3 (sold 24–36 months after purchase)

4%

~S$60,000 on a S$1.5M property

After 3 years (sold 36+ months after purchase)

0%

No SSD payable

SSD is calculated on the higher of the sale price or the market value at the date of sale. Assessed by IRAS. Must be paid within 14 days of signing the Option to Purchase (OTP) or Sales and Purchase Agreement (S&P).

How the holding period is calculated — critical details

The SSD holding period is measured from the date of purchase (date of execution of the OTP or S&P by the buyer) to the date of disposal (date of execution of the OTP or S&P by the seller to the next buyer). It is not measured from the date of completion, the date of lodging the caveat, or the date of transfer at the Land Titles Registry. This creates a practical implication: if you sign an OTP on 10 April 2023 and you sign another OTP granting your buyer an option on 11 April 2026 — that is exactly 3 years and 1 day — no SSD is payable.

For properties purchased under a building-under-construction (BUC) scheme (new launches where payment is tied to construction progress), the date of purchase is the date of the S&P agreement, not the date of TOP or legal completion. This means buyers who bought at the launch of a 4-year construction project — say, in 2022 for a 2026 TOP — have already been holding for 4 years by TOP and are SSD-free from the day of collection.

SSD base value — sale price vs market value

SSD is charged on the higher of: (a) the sale price, or (b) the property’s market value at the time of sale. This prevents sellers from artificially understating the sale price to reduce SSD liability. IRAS has the power to assess market value independently. In practice, for arm’s-length transactions in the open market, the sale price and market value will typically be equivalent or very close. SSD is assessed by IRAS based on the stamp duty valuation and must be paid within 14 days of the date of signing the instrument (OTP or S&P).

SSD exemptions — when you do not have to pay

IRAS recognises several circumstances where SSD is waived or not applicable:

Transfer upon death — if the property is transferred to a beneficiary under a will or intestacy, SSD is not payable by the estate.

Court-ordered transfer — divorce proceedings that result in a court-ordered transfer of residential property are exempt from SSD.

Government compulsory acquisition — if the Government acquires the property under the Land Acquisition Act, no SSD applies.

Bankruptcy proceedings — a sale by a trustee in bankruptcy is exempt from SSD.

Housing developers — a licensed housing developer that sells residential units as part of its development business is not subject to the residential SSD regime (they are subject to ABSD remission conditions instead).

HDB flat transfers within family — certain intra-family HDB flat transfers are exempt, subject to HDB approval.

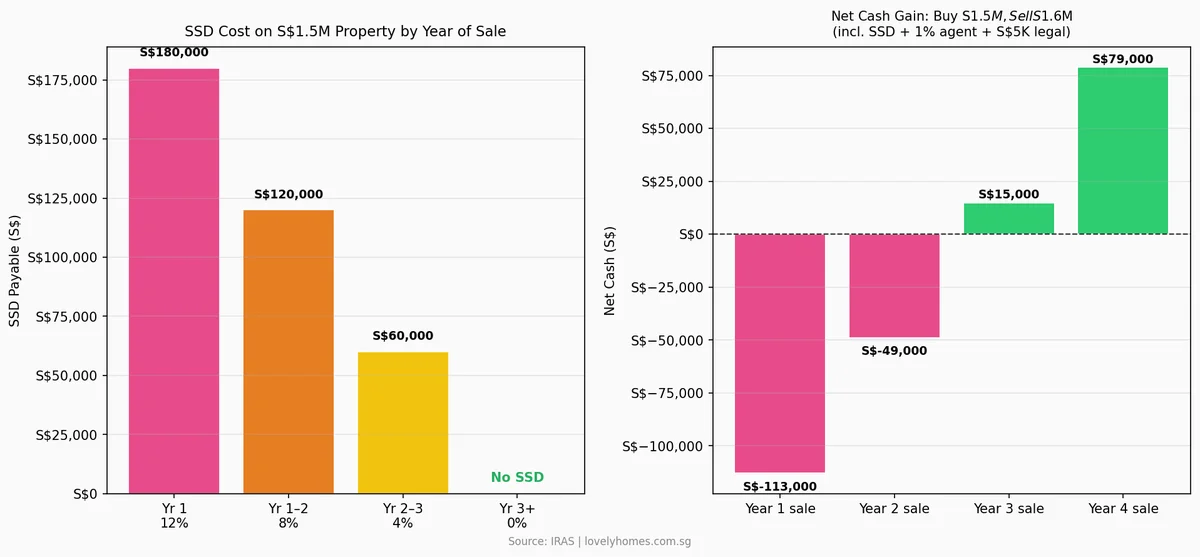

Worked example — the cost of selling early

Figure 2: Net cash outcome for a seller who buys at S$1.5M and sells at S$1.6M — showing how SSD eliminates profit in Years 1–2 and reduces it significantly in Year 3.

Consider a Singapore Citizen (first property) who buys a private condominium at S$1,500,000 on 1 April 2024 and sells at S$1,600,000 (a 6.7% gain). Assuming a 1% agent commission (S$16,000) and S$5,000 in legal fees, the net cash outcome varies dramatically by year of sale:

Sell Year 1

Sell Year 2

Sell Year 3

Sell Year 4+

Gross sale proceeds

S$1,600,000

S$1,600,000

S$1,600,000

S$1,600,000

SSD payable

S$192,000 (12%)

S$128,000 (8%)

S$64,000 (4%)

S$0

Agent commission (1%)

S$16,000

S$16,000

S$16,000

S$16,000

Legal fees (est.)

S$5,000

S$5,000

S$5,000

S$5,000

Net cash before mortgage clearance

S$−213,000 net loss

S$−149,000 net loss

S$15,000 net gain

S$79,000 net gain

Including S$100K CPF + accrued interest (8 yrs @ 2.5%)

—

—

~S$−105,000 after CPF refund

~S$−29,000 after CPF refund (10 yrs)

The example is clear: at a 6.7% gain (S$100,000 appreciation), selling in Year 1 or Year 2 produces a net loss after SSD and transaction costs. Year 3 produces a modest net gain. Year 4 and beyond is when the full gain materialises in cash. The implication for property investors: unless the property appreciates by more than 12–13% in the first year (covering SSD at 12% plus transaction costs), there is no financial case for selling within the SSD window.

SSD history — from 2010 to today

Date

Change

Detail

20 Feb 2010

SSD introduced

Holding period: 1 year; Rate: 1%

30 Aug 2010

SSD tightened

Holding period extended to 3 years; Rates: 3%/2%/1%

14 Jan 2011

SSD tightened further

Holding period extended to 4 years; Rates: 16%/12%/8%/4%

11 Mar 2017

SSD relaxed (current)

Holding period reduced to 3 years; Rates: 12%/8%/4%

27 Sep 2022

ABSD increased (SSD unchanged)

SSD rates held; ABSD for SC 2nd property raised to 20%

26 Apr 2023

ABSD increased again (SSD unchanged)

ABSD for foreigners raised to 60%; SSD unchanged

Industrial property SSD — different rules

For industrial properties (factories, warehouses, business parks, but not offices), a separate SSD regime applies with more punishing rates over a longer holding period. The current industrial SSD was introduced on 12 January 2013:

Holding Period

SSD Rate

Year 1 (≤ 12 months)

15%

Year 2 (12–24 months)

10%

Year 3 (24–36 months)

5%

Year 4+ (> 36 months)

0%

Industrial SSD is particularly relevant for buyers of strata industrial units (factories, LB1 mixed-use units) and commercial investors who may be considering the industrial sub-market as an alternative to residential. The 3-year holding period is the same as residential, but the Year 1 rate of 15% makes early disposal very costly.

SSD and decoupling — interaction with ABSD avoidance strategies

A common property structuring question is whether decoupling (transferring a jointly-owned property to one spouse, then using the other spouse’s clean slate to buy a second property without ABSD) triggers SSD. The answer: yes, if the decoupling transfer occurs within the 3-year SSD holding period. The date of the initial purchase is the reference date; if a couple purchased in 2024 and decouples (transfers one owner’s share to the other) in 2025, SSD at 8% applies on the half-share transferred. This is a significant deterrent to decoupling young properties and must be factored into any ABSD avoidance calculation. For detailed analysis of decoupling economics, see our Decoupling Property Guide.

SSD vs ABSD vs BSD — when each applies

Tax

Who Pays

When

Rate

Holding Rule

Buyer’s Stamp Duty (BSD)

Buyer

On purchase

All residential (graduated: 1%–6% on purchase price)

No holding period

Additional Buyer’s Stamp Duty (ABSD)

Buyer

On purchase

0–60% depending on citizenship and property count

No holding period (once paid, non-refundable for most)

Seller’s Stamp Duty (SSD)

Seller

On sale (if sold within 3 years)

12%/8%/4% of sale price or market value

Holding period: 3 years

Practical implications for Singapore property investors in 2026

The SSD regime fundamentally shapes Singapore’s residential property investment horizon. Here is what investors should factor into every decision:

Minimum 3-year holding period strategy — most experienced Singapore property investors budget for a minimum 3-year hold on any residential acquisition. Not because of SSD alone, but because BSD, legal fees, agent commissions and CPF accrued interest together mean you need meaningful appreciation (typically 10–15%) just to break even, and SSD on top of that makes any sub-3-year exit financially painful.

BUC purchases are already 3-4 years old at TOP — buyers of new launches in 2024–2025 with a 2028–2030 TOP will have cleared their 3-year SSD hold by the time they take possession. This means the first opportunity to sell is already SSD-free. For new launch buyers who plan to flip at TOP or shortly after, SSD is usually not a concern.

Resale condo purchases require a date check — buyers of 3-year-old or younger resale condominiums should check the prior owner’s original purchase date before assuming no SSD issue. As a resale buyer, your own 3-year SSD clock starts fresh from your purchase date.

Decoupling timing is critical — never decouple a property that is still within its 3-year SSD window without first modelling the SSD cost and comparing it to the ABSD saving from using a clean-slate buyer.

Market downturns can trap short-hold buyers — during the 2022–2023 rate-rise cycle, sellers who bought in 2020–2021 and needed to sell found themselves simultaneously facing SSD (if within 3 years) and a softer market. The SSD deterrent reduced distressed selling, which helped support Singapore property prices.

The SSD clock starts from the date of purchase — specifically, the date the buyer executes the Option to Purchase (OTP) or signs the Sales & Purchase Agreement (S&P). It does not start from legal completion, TOP, or the date of mortgage drawdown. When calculating whether you are out of the SSD window, count from the date you signed the purchase documents, not the date you got the keys.

Is SSD payable on the full sale price or only the profit?

SSD is payable on the full sale price (or market value if higher), not just the profit. This is what makes SSD so punishing: on a S$1.5M property sold at 12% SSD, you pay S$180,000 regardless of whether the property appreciated or depreciated. There is no offset for your purchase costs, stamp duties paid, or renovation expenditure.

Can SSD be avoided by gifting the property instead of selling?

No. A gift (transfer for no consideration) is still treated as a disposal by IRAS, and SSD is assessed on the market value of the property at the time of the gift. Similarly, transferring a property to a company, a trust, or a related party at below-market price does not avoid SSD — IRAS will assess based on market value.

Is SSD deductible against income tax?

For individuals holding investment properties, SSD paid is generally deductible as a cost of disposal when computing any capital gains — but since Singapore does not have a capital gains tax for individuals, this is largely academic. If a property is held as trading stock in a business (rare for individuals), SSD would be a deductible business expense. Always consult an accountant for your specific tax position.

Are HDB flat sales subject to SSD?

Yes. HDB resale flat sellers are subject to SSD if they sell within 3 years of purchase. However, HDB has its own Minimum Occupation Period (MOP) of 5 years — meaning you cannot sell a BTO or resale HDB flat on the open market for the first 5 years anyway. In practice, this means HDB resale sellers are always beyond their 3-year SSD window by the time they are legally allowed to sell, making SSD a non-issue for most HDB resale transactions.

What rate of appreciation is needed to break even after SSD?

To break even on a Year 1 sale, you need the property to appreciate enough to cover: SSD (12%) + BSD paid at purchase (~3–4% on a S$1.5M property) + agent fees (~1–2%) + legal fees (~0.3%) = approximately 17–18% appreciation in under 12 months. This is why property flipping in Singapore is economically unfeasible under the current SSD/BSD regime — the combined transaction costs are simply too high for any reasonable short-term gain.

What if I cannot afford to hold and must sell within 3 years?

If you face genuine financial hardship and must sell within the SSD window, you have limited options: (a) accept the SSD cost as the price of liquidity; (b) explore renting out the property (if permitted and the rental income covers carrying costs while you wait out the 3-year period); (c) approach IRAS for hardship consideration — in very limited circumstances (confirmed financial distress, not just suboptimal market timing), IRAS may consider remission, but this is rare and there is no formal remission channel for SSD. The best mitigation is to model your exit scenarios before purchasing.

Disclaimer: This article provides general information only and does not constitute financial, legal, or tax advice. SSD rates, holding periods, and exemptions are set by the Singapore Government and administered by the Inland Revenue Authority of Singapore (IRAS). Always verify the latest rules directly with IRAS (iras.gov.sg) or consult a licensed property agent, solicitor, and/or tax adviser before making any property transaction decision. LovelyHomes.com.sg is an independent editorial publication and is not an agent or adviser.

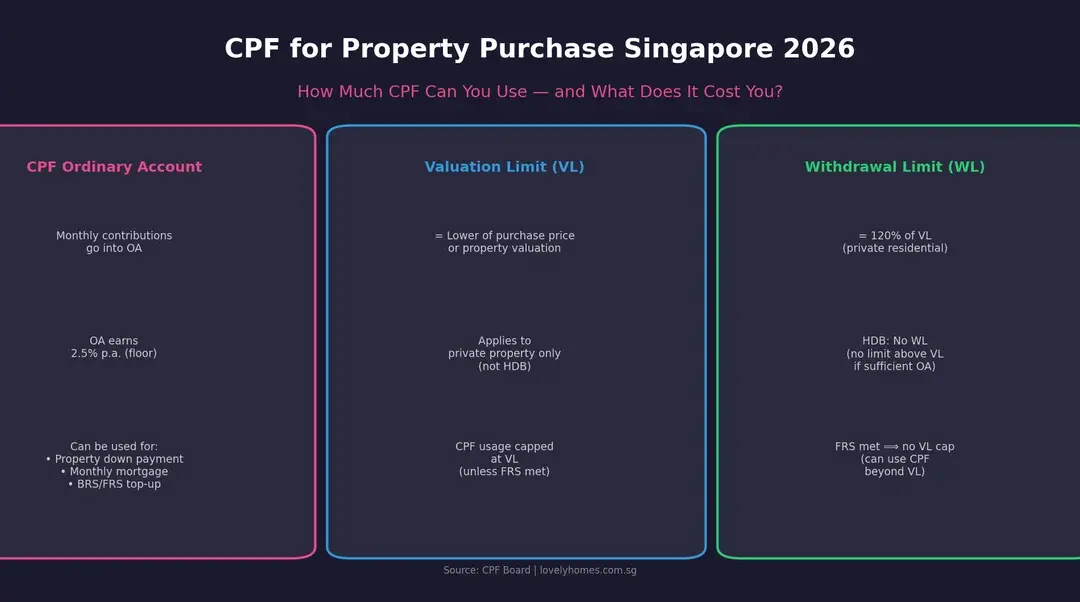

You can use your CPF Ordinary Account (OA) to pay the down payment and monthly mortgage instalments on a Singapore residential property.

For HDB flats, there is no Valuation Limit cap — you can use CPF up to the property value.

For private residential properties, CPF is capped at the Valuation Limit (VL) — the lower of purchase price or market valuation — unless your CPF Full Retirement Sum (FRS) is met.

There is a Withdrawal Limit (WL) of 120% of the VL for private residential properties — the absolute maximum you can ever withdraw for one property.

Accrued interest (2.5% per annum on all CPF used) must be refunded to your CPF account when you sell the property — this is not a cost, but a return to your retirement savings.

Remaining lease must be at least 20 years for CPF usage; for buyer’s age + remaining lease to satisfy the 80-year rule for properties with shorter leases.

Figure 1: CPF for Property Purchase — the three pillars: Ordinary Account (OA), Valuation Limit (VL) and Withdrawal Limit (WL). Source: CPF Board.

What is CPF OA and how does it accumulate?

The CPF Ordinary Account (OA) is one of three CPF accounts (alongside the Special Account and MediSave Account) that Singapore Citizens and Permanent Residents contribute to throughout their working lives. The OA is the account used for housing — and it is also the one that earns the lowest base interest rate of 2.5% per annum (floor rate). As of 2026, CPF contribution rates for employees below 55 are 37% of wages (23% employer + 17% employee = 20% to OA, 6% to Special Account, 8% to MediSave, approximately, depending on wage bracket). A Singaporean earning S$7,500/month will see approximately S$1,250 flow into their OA every month — a meaningful housing war chest that accumulates fast if untouched.

The OA earns 2.5% per annum, guaranteed by the Singapore Government. Additional 1% interest is paid on the first S$60,000 of combined balances (with OA capped at S$20,000 of this). This means a S$50,000 OA balance earns effectively 3.5% p.a. on the first S$20,000 and 2.5% on the rest. When you use CPF for property, you lose this compounding — which is why CPF Board requires accrued interest to be refunded to your account on sale, effectively restoring the retirement savings as if you had never withdrawn.

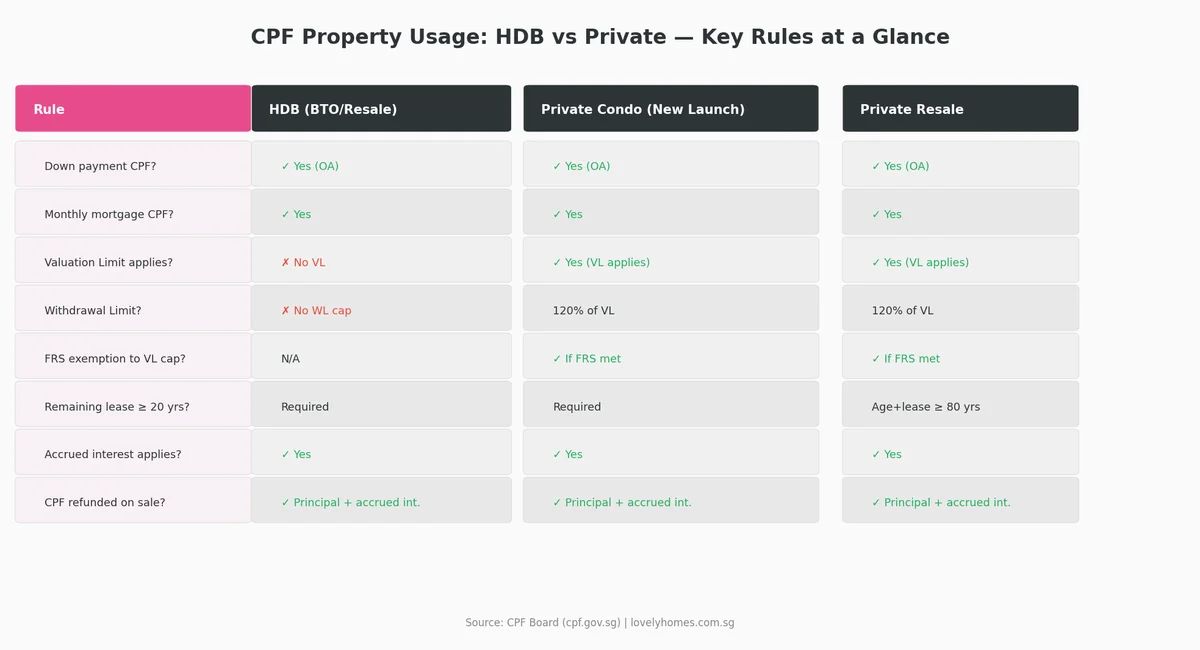

Which properties can you use CPF for?

CPF OA funds can be used for residential properties in Singapore only. This covers HDB BTO flats, HDB resale flats, Executive Condominiums (ECs) during the first 5 years (developer payment), private condominiums (new launch and resale), and landed property. You cannot use CPF for commercial properties, industrial units, overseas properties, or short-term leasehold properties with insufficient remaining lease.

Figure 3: CPF property usage rules — HDB vs private residential at a glance. The Valuation Limit and Withdrawal Limit apply to private property only.

Valuation Limit (VL) — the private property CPF ceiling

For private residential properties (condominiums, landed homes, ECs post-privatisation), CPF OA usage is capped at the Valuation Limit (VL). The VL is defined as the lower of: (a) the purchase price, or (b) the property’s valuation at the time of purchase. In practice, this means if you buy a condominium at S$1.5M and it is independently valued at S$1.45M, your VL is S$1.45M — and CPF usage is capped there, unless you meet the Full Retirement Sum (FRS) exemption.

The FRS exemption: if you have set aside the Full Retirement Sum (FRS) — which is S$213,000 for persons turning 55 in 2026 — in your CPF Special Account and Retirement Account (or pledged the property for half the FRS), then the VL cap does not apply. You can continue withdrawing OA funds beyond the VL, up to the Withdrawal Limit (WL) of 120% of the VL. This is a significant incentive for older buyers (approaching 55) who have built up a substantial CPF SA balance.

Concept

Definition

Applies to

Example

Valuation Limit (VL)

Lower of purchase price or valuation

Private residential only

S$1.45M (if valuation < purchase price of S$1.5M)

Withdrawal Limit (WL)

120% of VL

Private residential only

S$1.74M (if VL = S$1.45M)

Full Retirement Sum (FRS)

S$213,000 (2026)

Set aside in CPF SA/RA

Exempts buyer from VL cap

How CPF accrued interest works — the most misunderstood part

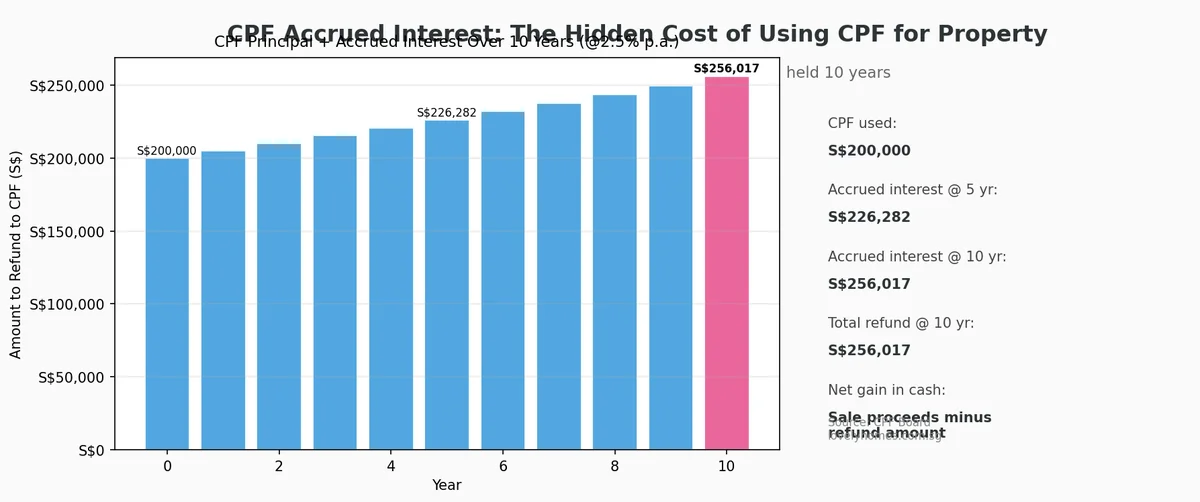

When you use CPF OA money for your property, the CPF Board charges accrued interest — 2.5% per annum — on all CPF withdrawn, from the date of withdrawal until the date of refund (on sale or full loan repayment). This is not an additional cost; it is a notional return that your CPF OA would have earned had the money remained there. On sale of the property, the gross proceeds must first be used to refund the CPF principal withdrawn plus the accrued interest, before you receive any cash.

The implication is profound: a buyer who uses S$200,000 of CPF for their property and sells 10 years later must refund approximately S$256,000 back to CPF (S$200,000 × 1.025^10). If the property has appreciated significantly, this is a rounding error. If the property has not appreciated, the refund obligation can reduce or eliminate the cash proceeds from the sale.

Figure 2: Accrued interest on S$200,000 CPF used for property over 10 years at 2.5% p.a. — the refund obligation grows to S$256,018 by Year 10.

Worked example — CPF usage for an S$800,000 HDB resale purchase

Item

Amount

Note

HDB resale purchase price

S$800,000

Cash component (Option fee + exercise)

S$40,000 (min 5% for resale HDB with bank loan)

From savings

Down payment via CPF OA

S$120,000 (15%)

Drawn from CPF OA

Bank loan (80% LTV)

S$640,000

Monthly mortgage (25 yr, 3.2% p.a.)

~S$3,085/month

Can be paid from CPF OA monthly

CPF used in Year 1 (down + 12 months)

~S$157,000

Accrued interest if sold at Year 10 on full CPF drawn (~S$450,000)

Cash proceeds: S$0 (bank loan must be cleared first)

This illustrative example assumes the entire HDB mortgage is serviced by CPF OA over 10 years and the full OA drawdown accumulates accrued interest. Actual figures depend on monthly payment, valuation and prevailing rates. Always use the CPF Board’s online calculator for your specific scenario.

CPF usage for private property — worked example (S$1.5M condo)

Item

Amount

Note

Purchase price

S$1,500,000

Valuation (assumed equal)

S$1,500,000

VL = S$1,500,000

Withdrawal Limit (WL)

S$1,800,000 (120% of VL)

Absolute maximum CPF

Minimum cash down payment (25% LTV)

S$375,000

Of which 5% (S$75K) must be cash

CPF used for down payment

S$300,000 (remaining 20%)

From OA

Bank loan (75% LTV)

S$1,125,000

Monthly CPF for mortgage (TDSR test passed)

~S$5,100/month

From OA

FRS met? (Age 50 buyer with S$250K in SA)

Yes — VL cap waived

Can draw up to WL of S$1.8M

Remaining lease rules — the age-lease equation

CPF Board introduced lease-based restrictions in 2019 to prevent buyers from over-leveraging their retirement savings on properties with declining lease values. The key rules are:

Minimum lease of 20 years remaining at time of purchase for any CPF usage.

Buyer’s age + remaining lease ≥ 80 years: If this condition is not met, CPF usage is prorated based on the lease remaining at age 55.

HDB flats: If remaining lease is 20–59 years, CPF usage is limited to the amount that covers the flat from age of purchase to age 95. If lease is 60+ years, full CPF usage allowed.

Private property: Same age + lease formula applies. A 45-year-old buyer purchasing a condo with 30 years remaining (age 45 + 30 = 75 < 80) will face a prorated CPF withdrawal limit.

Implication: older buyers considering older 99-year leasehold condos should model their CPF eligibility carefully. A 50-year-old buyer buying a 30-year-old 99-year condo with 69 years remaining: 50+69=119 ≥ 80, so full CPF available. No issue. But a 55-year-old buying a 1990-vintage 99-year condo with only 64 years left: 55+64=119 ≥ 80. Still fine.

HDB vs private — what is different?

Rule

HDB Flat

Private Property

Valuation Limit?

No (HDB grants and valuations handled separately)

Yes — critical for private property

Withdrawal Limit?

No — can draw from OA as long as lease/age rule met

120% of VL (hard cap)

Accrued interest?

Yes — 2.5% p.a., refunded on sale

Yes — same

CPF Housing Grant?

Yes (EHG, PHG, AHG available for resale HDB)

No CPF housing grants for private

Minimum cash outlay?

0–5% depending on loan type (HDB/bank)

5% in cash + up to 20% CPF (bank loan)

CPF for monthly mortgage?

Yes (HDB loan or bank loan)

Yes (bank loan; must pass TDSR)

Top 5 CPF property strategies for Singapore buyers in 2026

Max out OA before drawing CPF for property — the OA earns a guaranteed 2.5%–3.5% p.a. For buyers who can service the mortgage in cash, keeping CPF untouched preserves retirement savings and eliminates accrued interest obligations. This makes sense for investors who expect property appreciation to outrun 2.5% by a wide margin.

Use CPF for HDB, save cash for private — for HDB upgraders, using CPF for the HDB monthly mortgage is common practice and sensible (no VL cap, no WL). On upgrading to a private property, the HDB sale refund restores CPF and the proceeds fund the new purchase. Plan the refund timeline carefully to avoid a cash-flow gap.

Meet FRS before buying private property — buyers approaching 55 who have sufficient CPF SA balance can meet the FRS and unlock CPF usage beyond the VL on private property. This is particularly valuable for high-value CCR purchases where the loan quantum alone may not cover the purchase price.

Model the accrued interest in every resale scenario — before deciding how much CPF to use, run the numbers on your break-even price. If you use S$300,000 CPF today and sell in 8 years, you will owe ~S$362,000 back. Your property must appreciate enough to cover: (a) accrued CPF refund, (b) ABSD (if applicable), (c) legal and agent fees, (d) SSD (if within 3-year hold), before you see any net cash profit.

Check CPF eligibility for older resale condos early — if you are buying a 20+ year old condominium, verify that the remaining lease satisfies the age+lease ≥ 80 rule before making an offer. Properties that fail this test may require a larger cash component than budgeted.

Frequently asked questions — CPF for property

Can I use CPF to buy a second property in Singapore?

Yes. You can use your CPF OA balance for a second private residential property, but the Valuation Limit and Withdrawal Limit apply, and you must set aside the Basic Retirement Sum (BRS) in your CPF Retirement Account before using the excess CPF for the second property (if you are aged 55 or above). For buyers below 55, there is no BRS deduction requirement — you can use available OA funds for the second property subject to normal VL/WL rules. Note that ABSD on a second property (20% for Singapore Citizens, 30% for PRs as of 2026) must be paid in cash and cannot be covered by CPF.

Does accrued interest mean I pay more to buy my property?

No — accrued interest is not an additional cost. It is the interest your CPF OA would have earned had the money not been withdrawn for property. When you sell, the principal and accrued interest are refunded to your CPF account, restoring your retirement savings. The cost implication is opportunity cost: if you had not used CPF, your OA would be larger. The practical effect on your net cash from sale depends entirely on property appreciation versus the 2.5% accrual rate.

Can I use CPF to pay for renovation or stamp duties?

No. CPF OA can only be used for the purchase price, legal fees (in limited circumstances), and monthly mortgage instalments. It cannot be used to pay for renovations, Buyer’s Stamp Duty (BSD), Additional Buyer’s Stamp Duty (ABSD), property tax, or maintenance fees. All stamp duties must be paid in cash.

What happens to CPF if my property goes into negative sale?

If the sale proceeds are insufficient to cover the outstanding bank loan and the CPF refund obligation, the CPF Board allows a shortfall arrangement in limited circumstances — but you must still settle the bank loan in full from other funds. You are not released from the CPF accrued interest obligation simply because the property lost value. This is a key risk for buyers who use maximum CPF leverage and purchase at the market peak.

Is CPF usage different for an Executive Condominium (EC)?

EC purchase rules vary by phase. During the initial launch and construction phase (developer payment), ECs are treated like HDB flats — the VL does not apply and you can use CPF freely for the down payment and progress payments, plus any CPF housing grants you are eligible for. After TOP and during the Minimum Occupation Period (MOP), the EC is still treated as public housing for CPF purposes. After the 5-year MOP, if you sell, CPF rules transition to private property rules for the buyer.

Can foreigners use Singapore CPF for property?

No. CPF is exclusively for Singapore Citizens and Permanent Residents. Foreigners working in Singapore on an Employment Pass or other work pass do not contribute to CPF and have no CPF OA to draw on for property purchases. They must fund 100% of the purchase price (minus any bank loan) in cash.

What is the CPF accrued interest rate and is it subject to change?

The OA accrued interest rate is pegged to the CPF OA interest rate — currently 2.5% p.a. (floor rate set by the Government). The actual rate is the higher of 2.5% or the 3-month SIBOR average. Since SIBOR has been below 2.5% for most of the past decade, 2.5% has been the effective floor. If Singapore rates normalise materially higher, the accrued interest rate would increase accordingly, making the refund obligation on sale larger.

Disclaimer: This article provides general information only and does not constitute financial, legal, or CPF-specific advice. CPF rules, interest rates, FRS amounts and withdrawal limits are subject to change by the CPF Board and the Singapore Government. Always verify the latest rules and limits directly with the CPF Board (cpf.gov.sg) or consult a licensed financial adviser before making any property or CPF withdrawal decision.

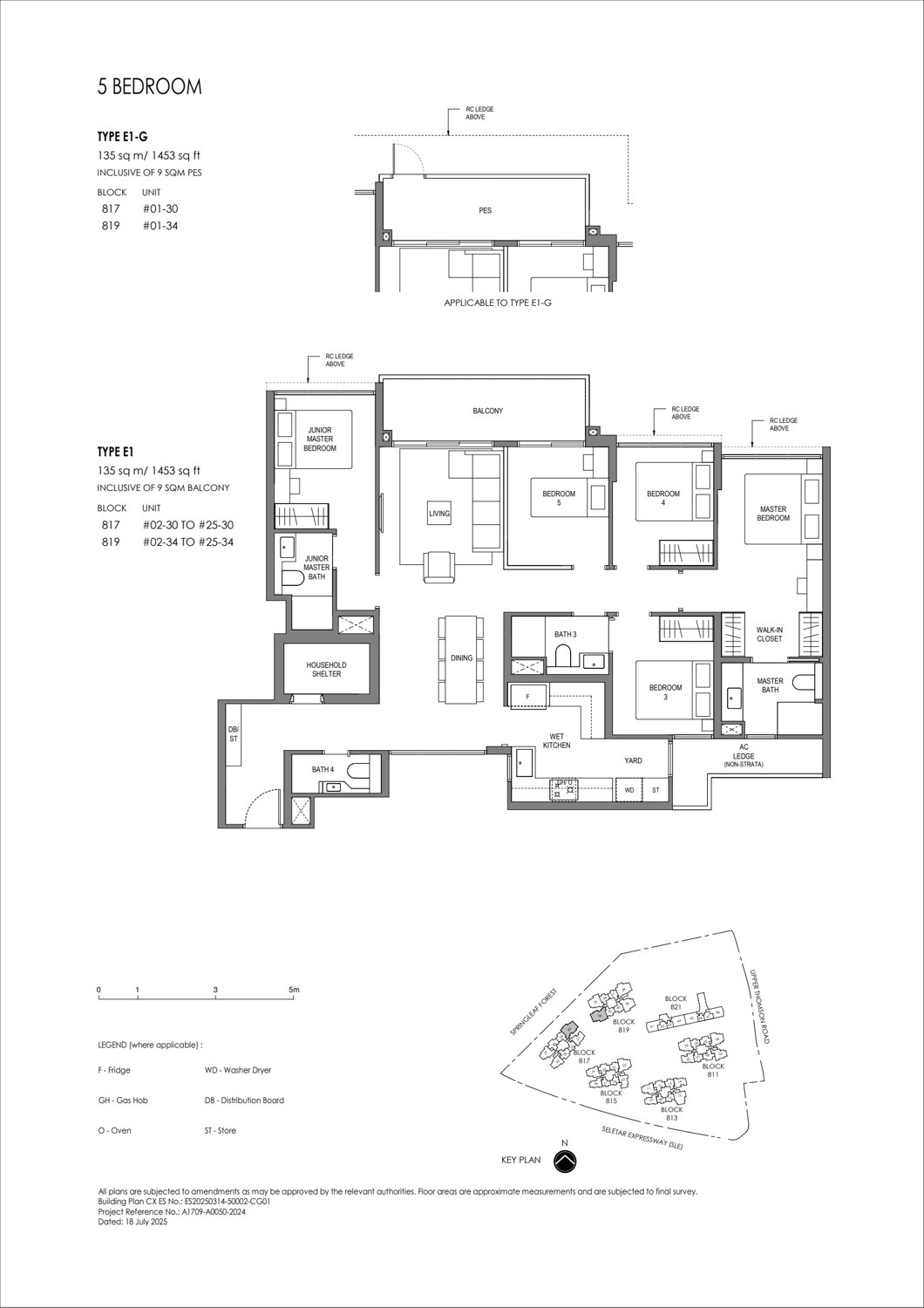

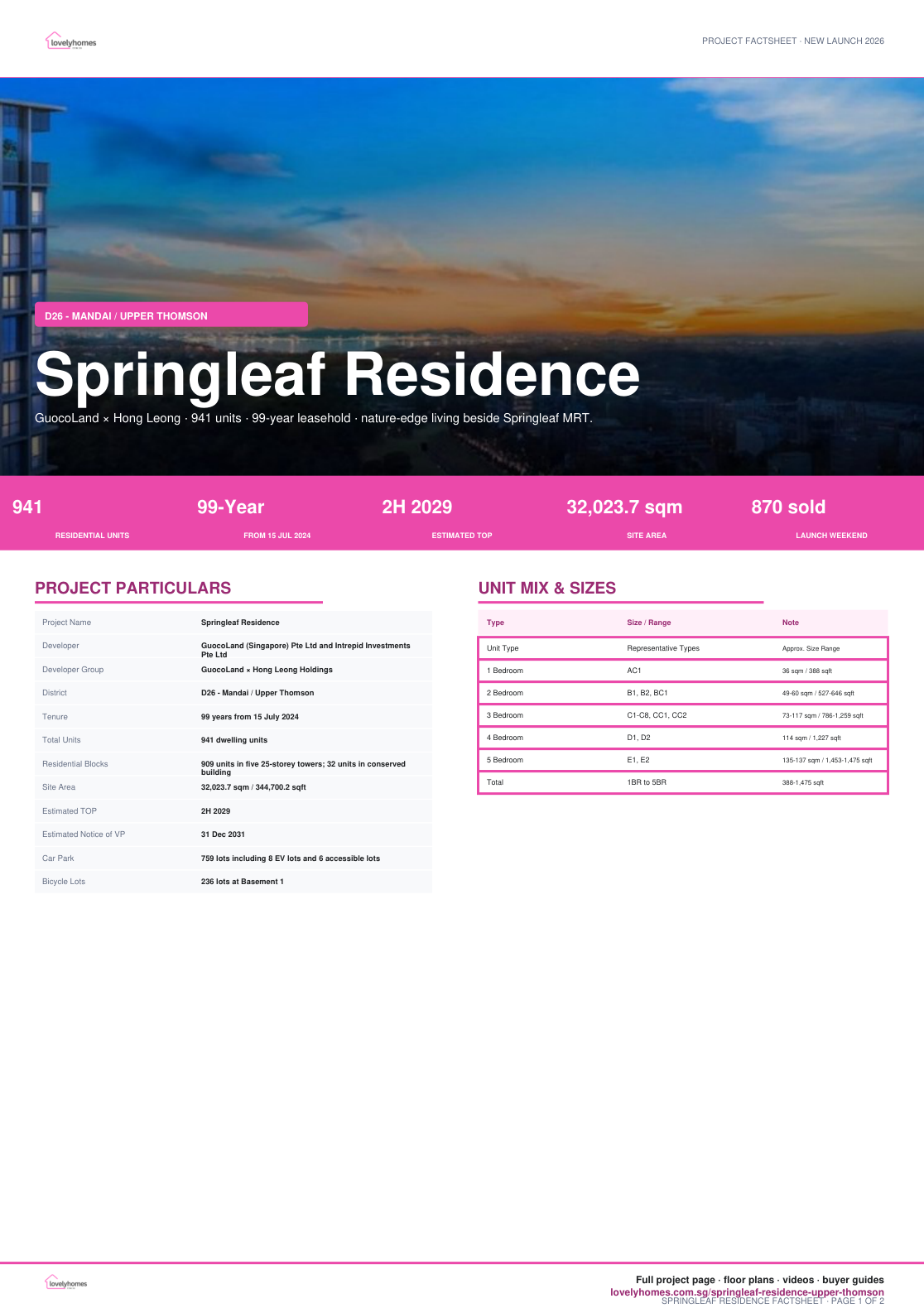

Springleaf Residence is a 941-unit nature-edge new launch at Upper Thomson Road, jointly developed by GuocoLand and Hong Leong. Local project documents list five 25-storey towers with 909 homes plus 32 homes in the conserved former school building.

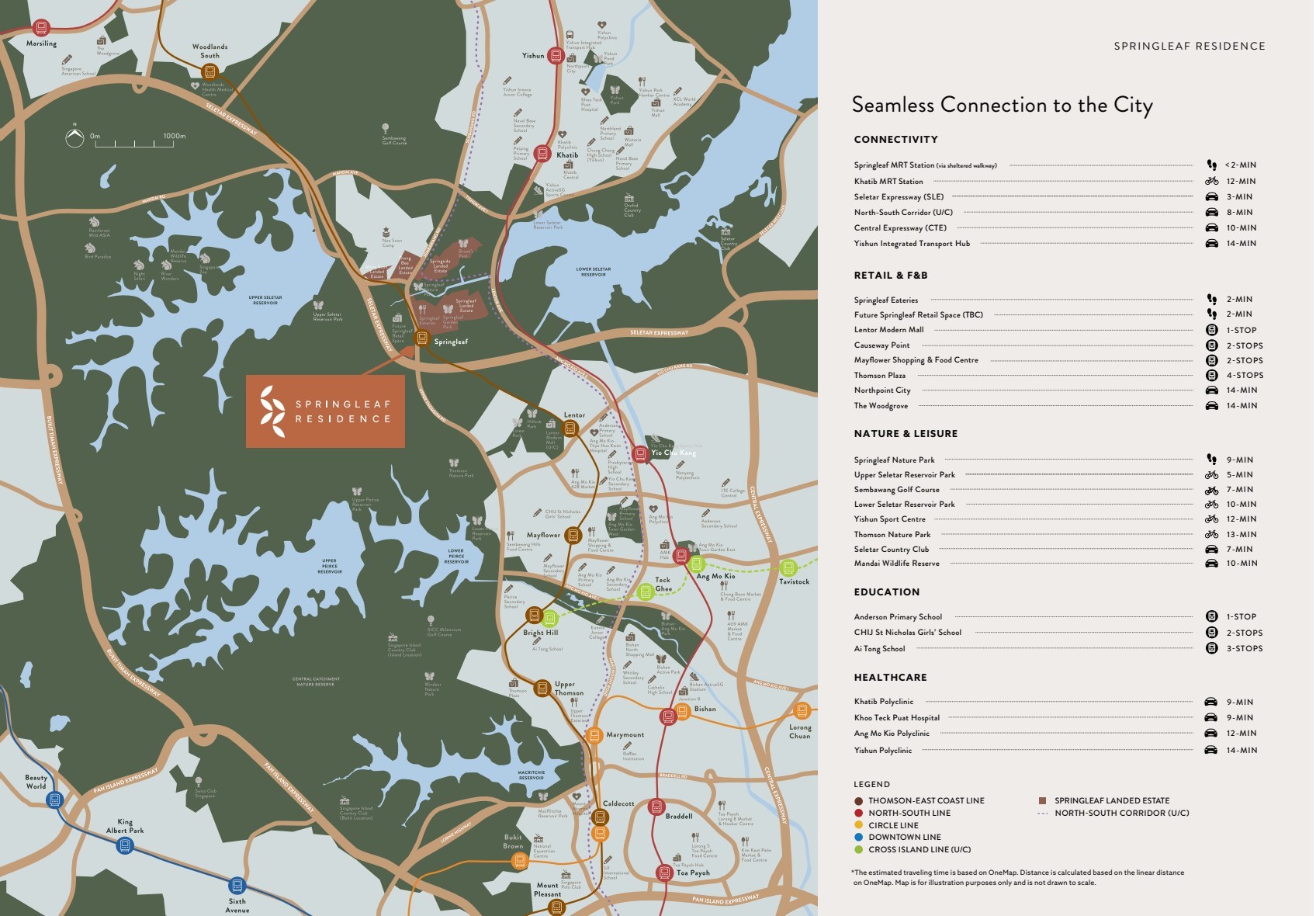

01 · Connectivity

MRT at the doorstep

Project documents place Springleaf MRT on the Thomson-East Coast Line within a sheltered walk of under two minutes, with SLE and the future North-South Corridor close by.

02 · Nature

Forest-edge living

The large 3.2-hectare site sits beside Springleaf Forest and the Central Catchment Nature Reserve, with biodiversity-sensitive landscape planning.

03 · Heritage

Modern towers plus conservation

Five new residential towers are paired with a conserved four-storey former school block adapted into homes and communal spaces.

Project At-a-Glance

Project Name

Springleaf Residence

Developer

GuocoLand (Singapore) Pte Ltd and Intrepid Investments Pte Ltd

Developer Group

GuocoLand × Hong Leong Holdings

District

D26 – Mandai / Upper Thomson

Tenure

99 years from 15 July 2024

Total Units

941 dwelling units

Residential Blocks

909 units in five 25-storey towers; 32 units in conserved building

Site Area

32,023.7 sqm / 344,700.2 sqft

Estimated TOP

2H 2029

Estimated Notice of VP

31 Dec 2031

Car Park

759 lots including 8 EV lots and 6 accessible lots

Bicycle Lots

236 lots at Basement 1

Construction Method

APCS

Source Date

Local factsheet accurate as at 11 July 2025

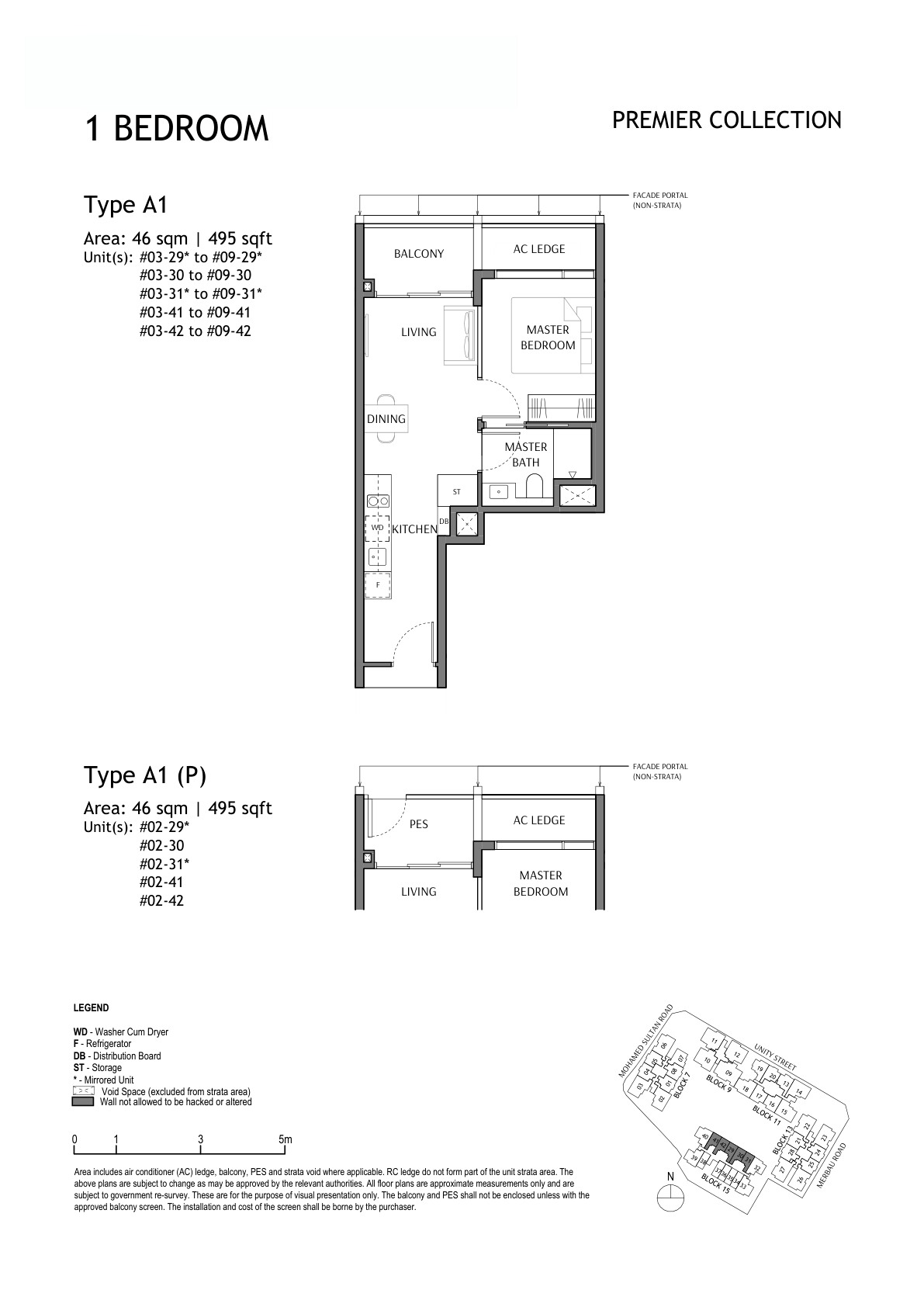

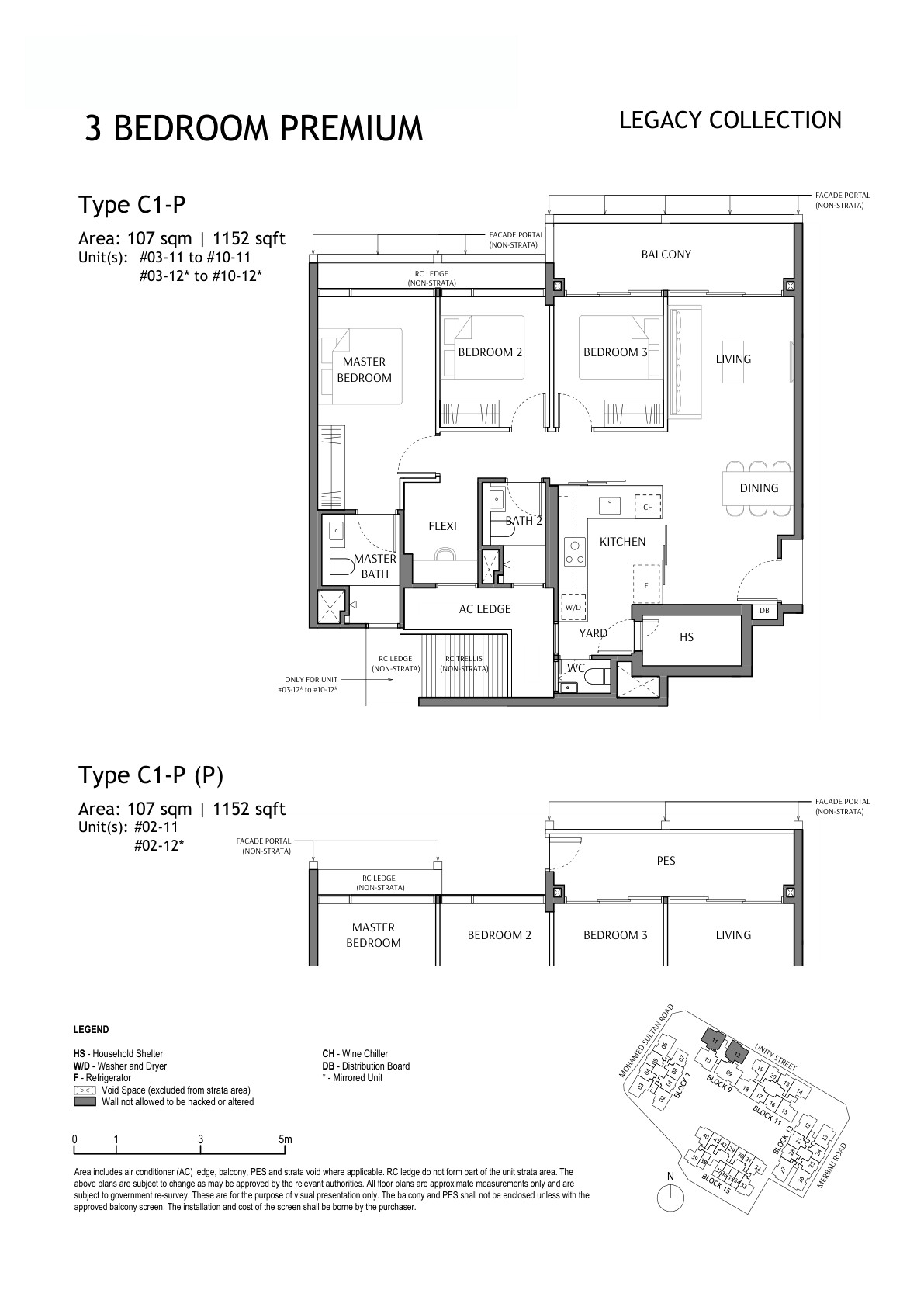

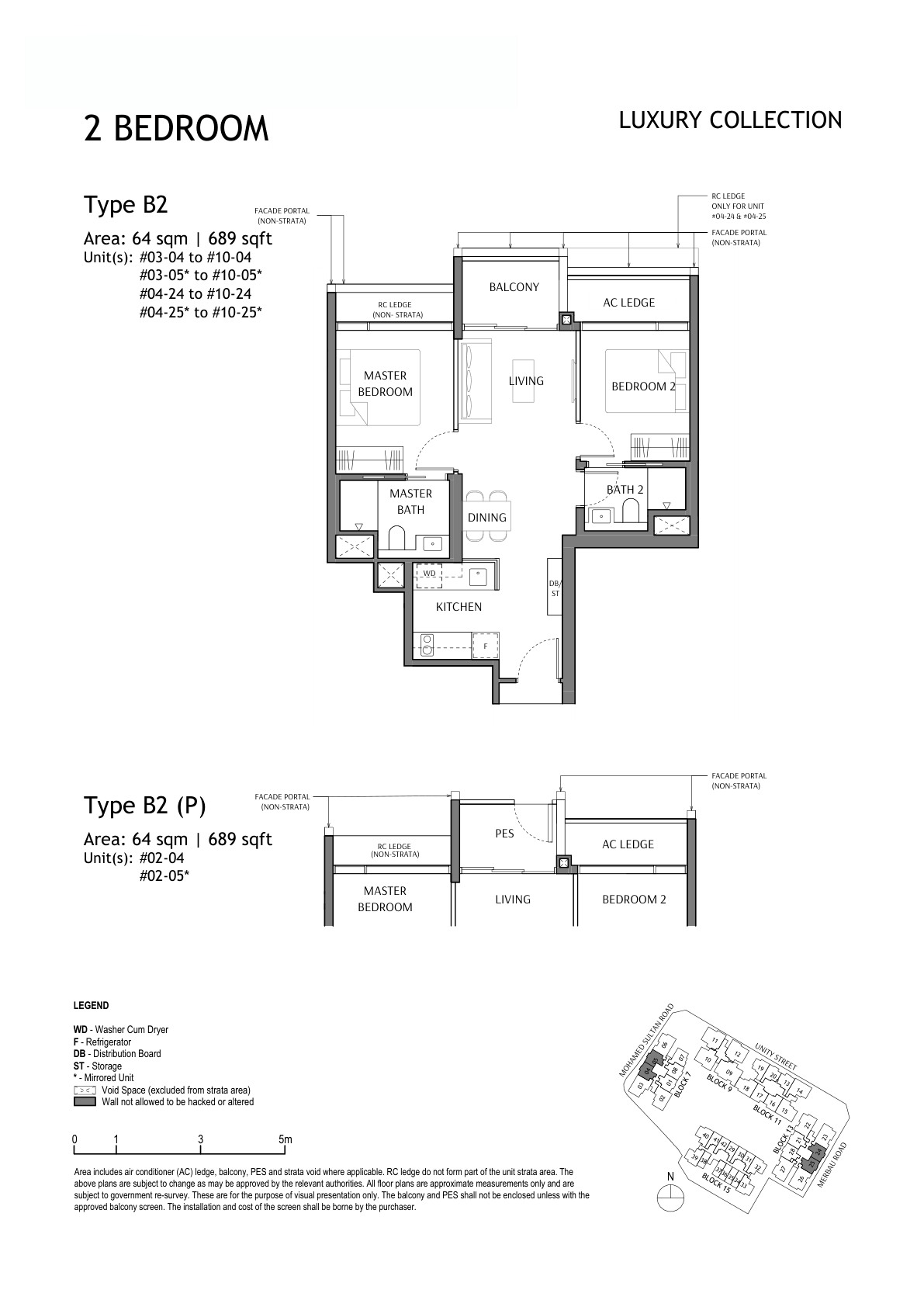

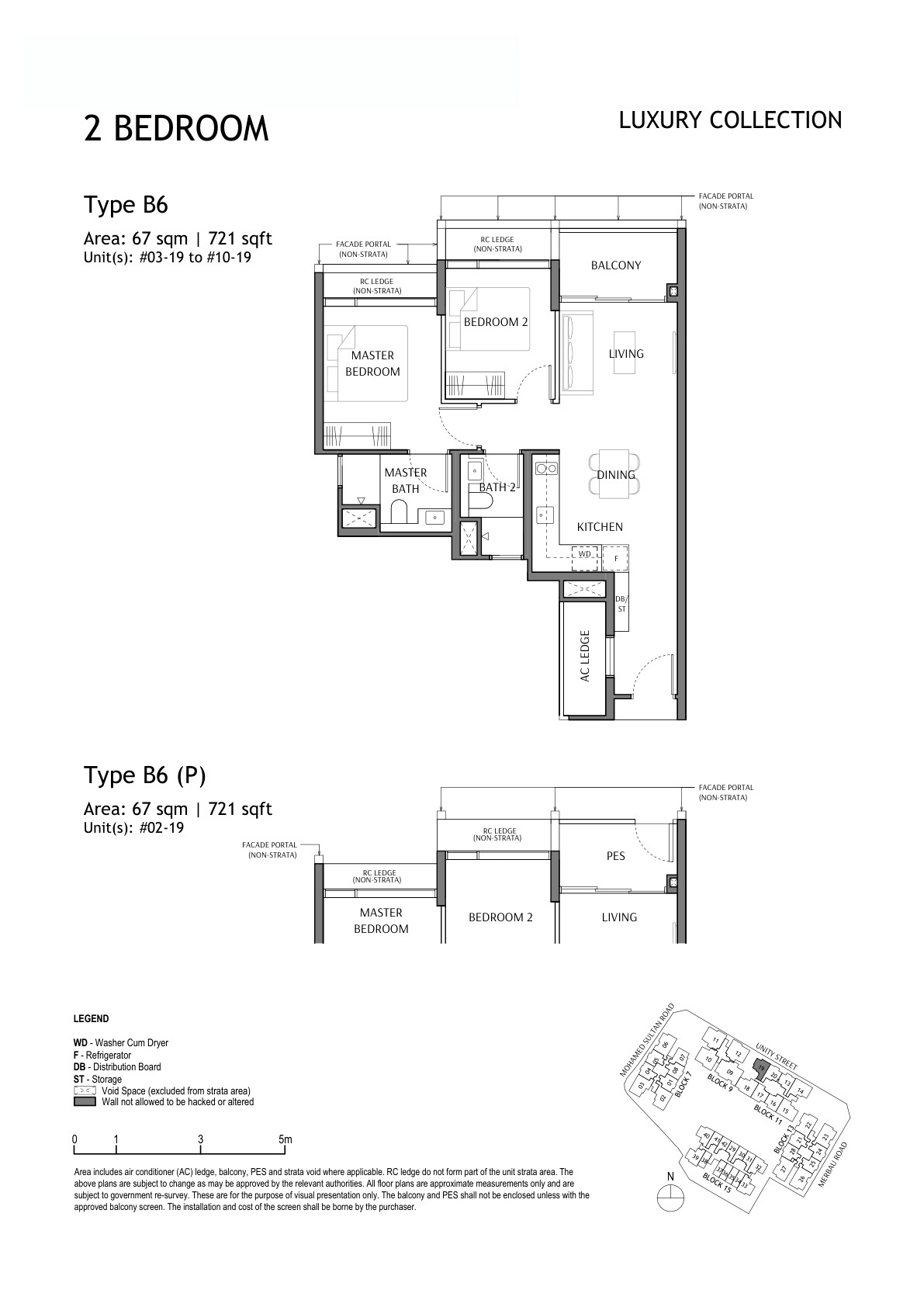

Unit Mix and Sizes

Unit Type

Representative Types

Approx. Size Range

Units

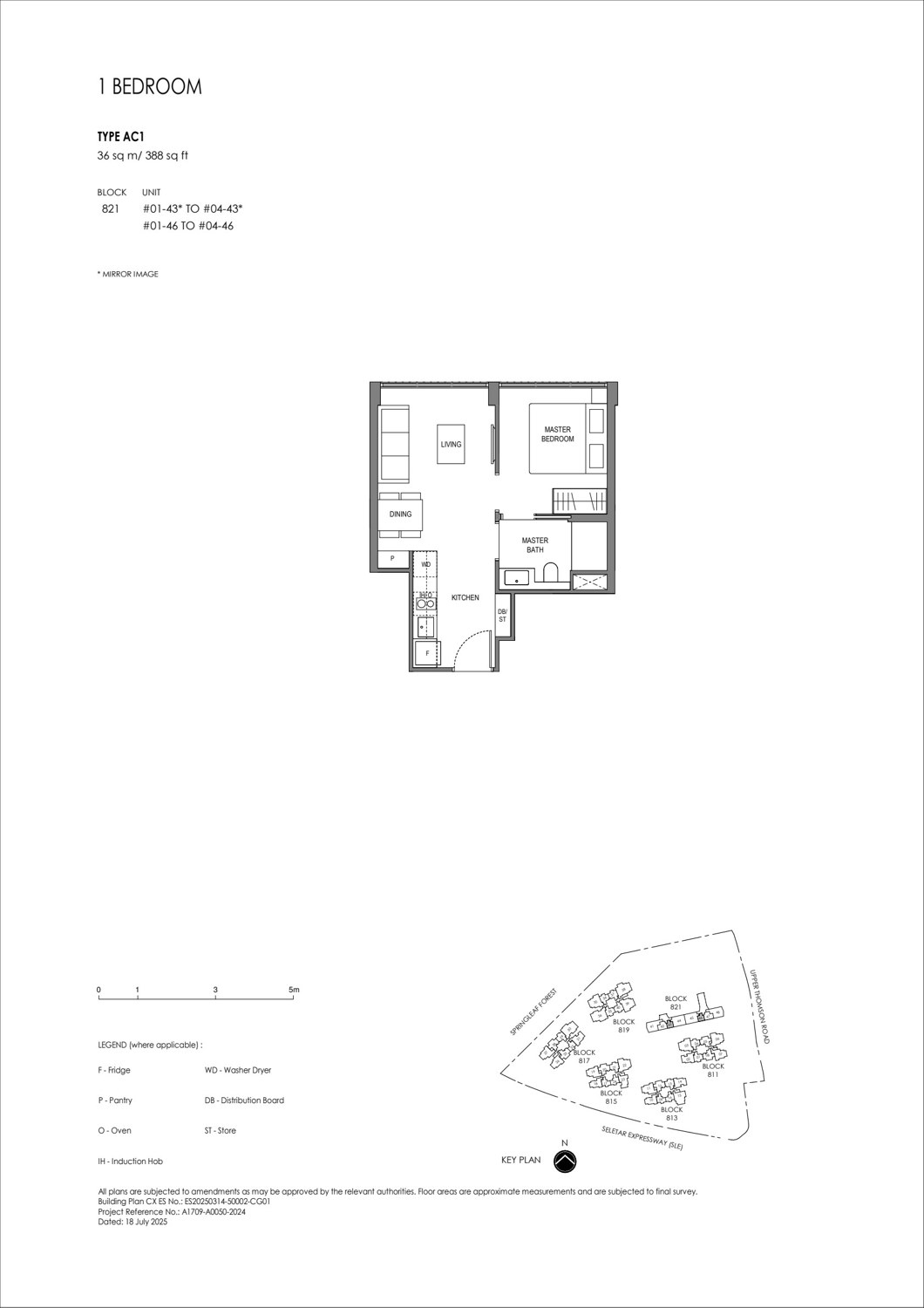

1 Bedroom

AC1

36 sqm / 388 sqft

8

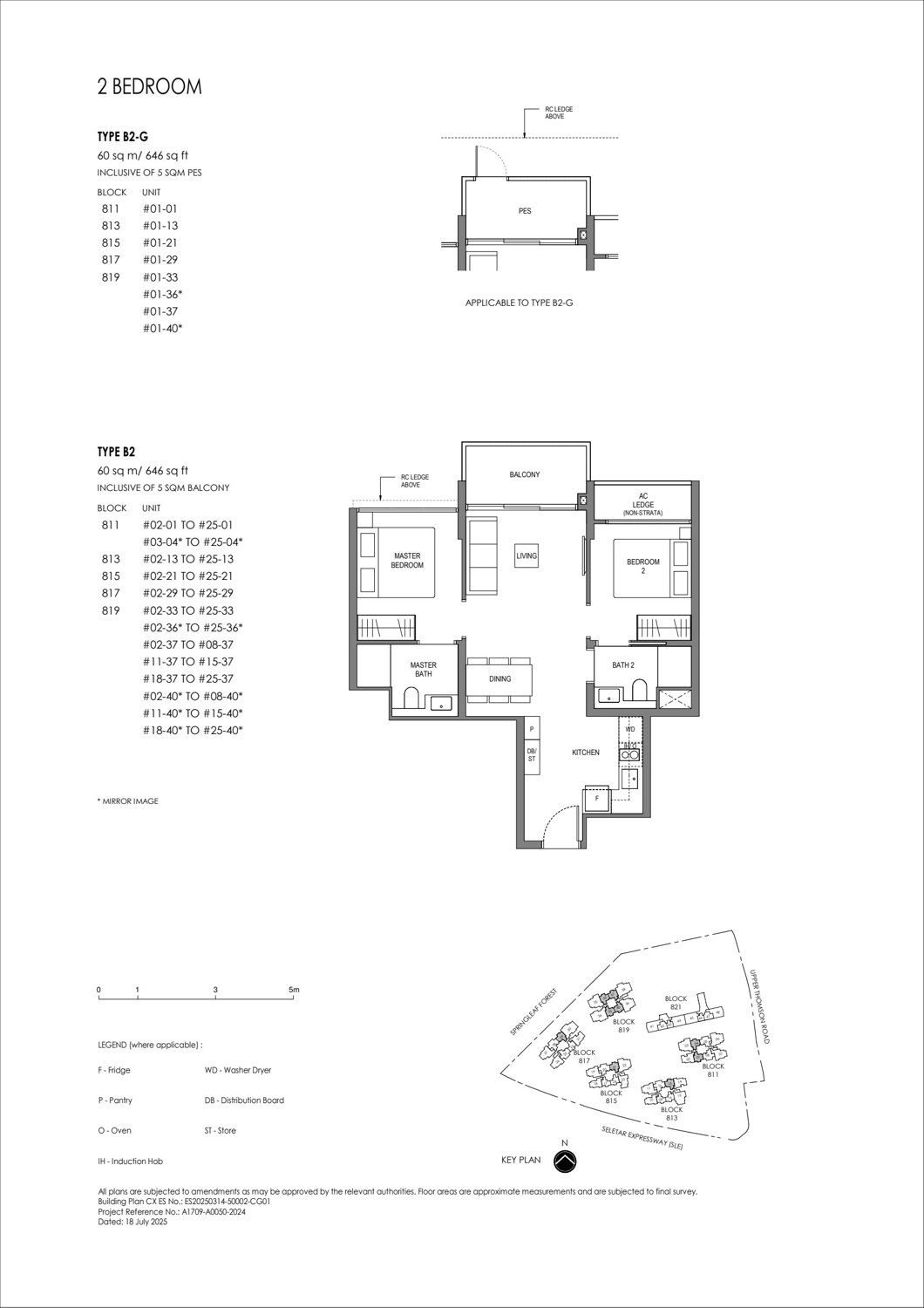

2 Bedroom

B1, B2, BC1

49-60 sqm / 527-646 sqft

340

3 Bedroom

C1-C8, CC1, CC2

73-117 sqm / 786-1,259 sqft

384

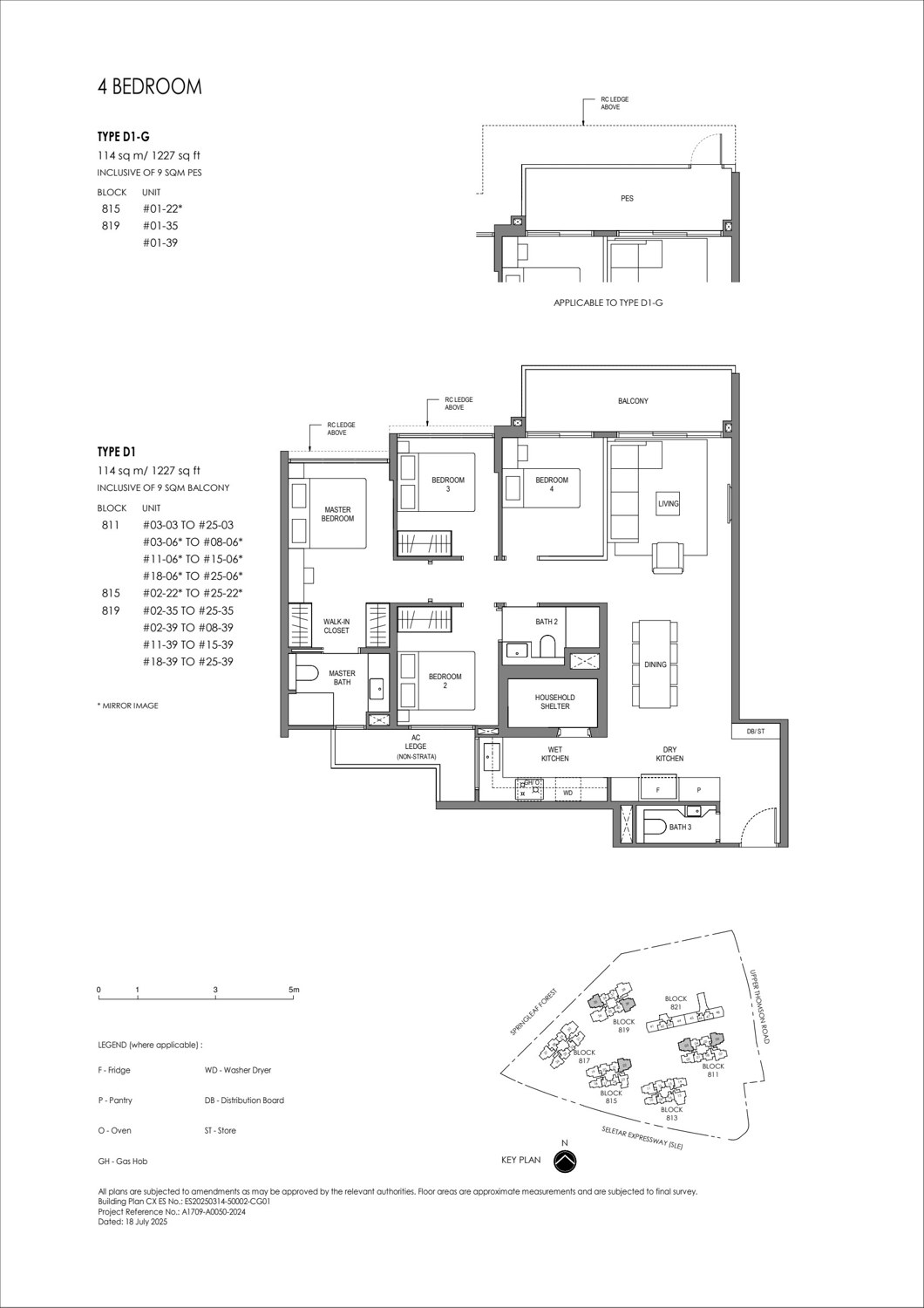

4 Bedroom

D1, D2

114 sqm / 1,227 sqft

138

5 Bedroom

E1, E2

135-137 sqm / 1,453-1,475 sqft

71

Total

1BR to 5BR

388-1,475 sqft

941

Unit mix is taken from available available project information. Download the full floor-plan PDF below for all layout notes and keyplan references.

Indicative Pricing

Preview Guide

From S$1,995 psf

Launch Average

~S$2,175 psf

1BR Launch Ref.

From ~S$860k

Pricing is indicative and time-sensitive. Confirm current availability, stack, floor, facing and incentives against the latest developer sales documents before booking.

Why Buyers Are Watching

1MRT doorstep access – Springleaf MRT is described in project documents as under two minutes sheltered walk away.

2Large nature-edge site – the project sits beside Springleaf Forest and the Central Catchment Nature Reserve.

3High launch take-up – public reporting cited 870 homes sold over launch weekend.

4Conserved building story – a former school building is conserved and adapted for homes and amenities.

5Broad family-size mix – layouts range from compact 1-bedroom to 5-bedroom homes.

Location and Connectivity

Transport

Springleaf MRT

Thomson-East Coast Line station within sheltered walking distance from project documents.

Roads

SLE and NSC

Quick access to Seletar Expressway and the future North-South Corridor.

Nature

Forest Edge

Springleaf Forest, Springleaf Nature Park and Central Catchment Nature Reserve nearby.

Retail

Thomson / Lentor

Springleaf eateries, Thomson Plaza, Lentor Modern Mall and Northpoint City are in the broader catchment.

Schools Nearby

Primary / Nearby

Anderson Primary School, CHIJ St Nicholas Girls’ School, Ai Tong School, Mayflower Primary School

Secondary / Tertiary

Yishun Junior College and Nanyang Polytechnic are listed in local page materials.

Lifestyle and Amenities

Nature and parks

Springleaf Nature Park, Upper Seletar Reservoir Park, Lower Seletar Reservoir Park, Mandai Wildlife Reserve and Thomson Nature Park.

Retail and dining

Springleaf eateries, future Springleaf retail space, Lentor Modern Mall, Thomson Plaza, Causeway Point and Northpoint City.

Wellness and recreation

50m lap pool, spa and hydrotherapy pools, tennis court, lounges, reading room, craft room and sky terraces.

Site Plan

Actual site plan from Springleaf Residence project documents · indicative and subject to developer confirmation

Floor Plans (Selected)

Representative actual plans by unit type. Download the full PDF below for all variants and keyplan notes.

1 Bedroom Type AC136 sqm / 388 sqft

2 Bedroom Type B260 sqm / 646 sqft

3 Bedroom Type C384 sqm / 904 sqft

4 Bedroom Type D1114 sqm / 1,227 sqft

5 Bedroom Type E1135 sqm / 1,453 sqft

Full Floor Plans PDF

Official Springleaf Residence floor-plan PDF with all selected bedroom types and keyplan references.

Springleaf Residence is jointly developed by GuocoLand and Hong Leong, with project documents naming GuocoLand (Singapore) Pte Ltd and Intrepid Investments Pte Ltd as developer entities.

Architect

ADDP Architects LLP

Landscape Architect

Ortus Design Pte Ltd

Main Contractor

China Construction (South Pacific) Development Co Pte Ltd

Conservation Consultant

Studio Lapis Conservation Pte Ltd

Biodiversity Specialist

Camphora Pte Ltd

Green Mark Consultant

DP Sustainable Design Pte Ltd

Sustainability and Specifications

The source factsheet describes biodiversity-sensitive design with a forest buffer zone, native planting, ecological corridors, educational trails and adapted conservation use. The four-storey former school block is conserved and converted into residential homes and communal spaces.

Project Timeline

15 Jul 2024

99-year lease commencement

29 Jul 2025

Preview pricing from S$1,995 psf

15-16 Aug 2025

Launch weekend; 870 units reported sold

2H 2029

Estimated TOP

31 Dec 2031

Estimated notice of VP

Project Factsheet

A shareable 2-page PDF snapshot of everything on this page — bring it to viewings, forward it to family.

Disclaimer. Prices, unit mix, specifications, site plans, floor plans and facility lists on this page are indicative only and subject to change by the developer without notice. Information has been compiled from available developer materials and verified for this LovelyHomes page update on 28 April 2026. LovelyHomes.com.sg is not the project developer. Prospective buyers should verify the latest developer sales kit, availability and pricing before committing to any purchase. Artist impressions are for illustrative purposes only and may differ from the final built product.

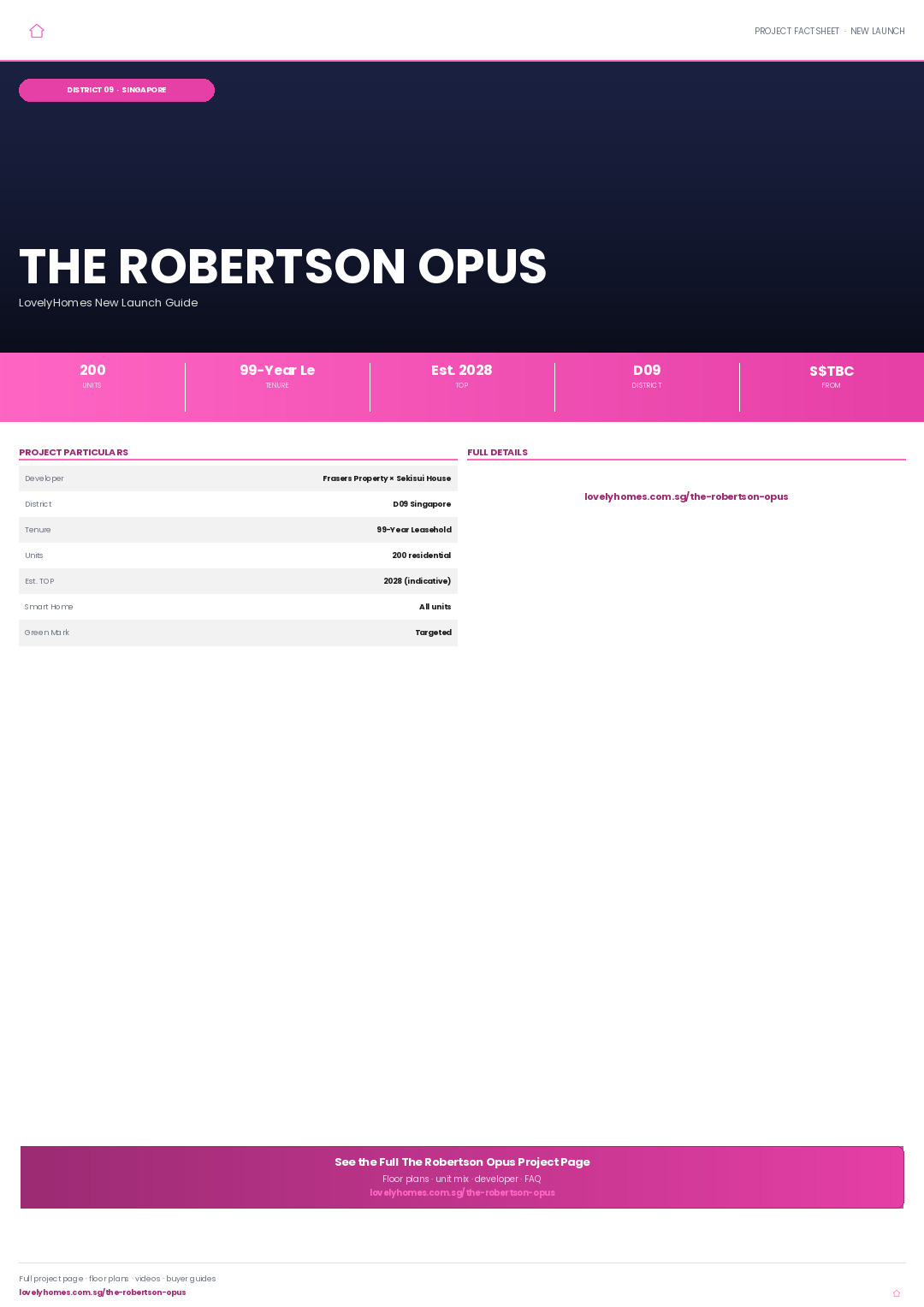

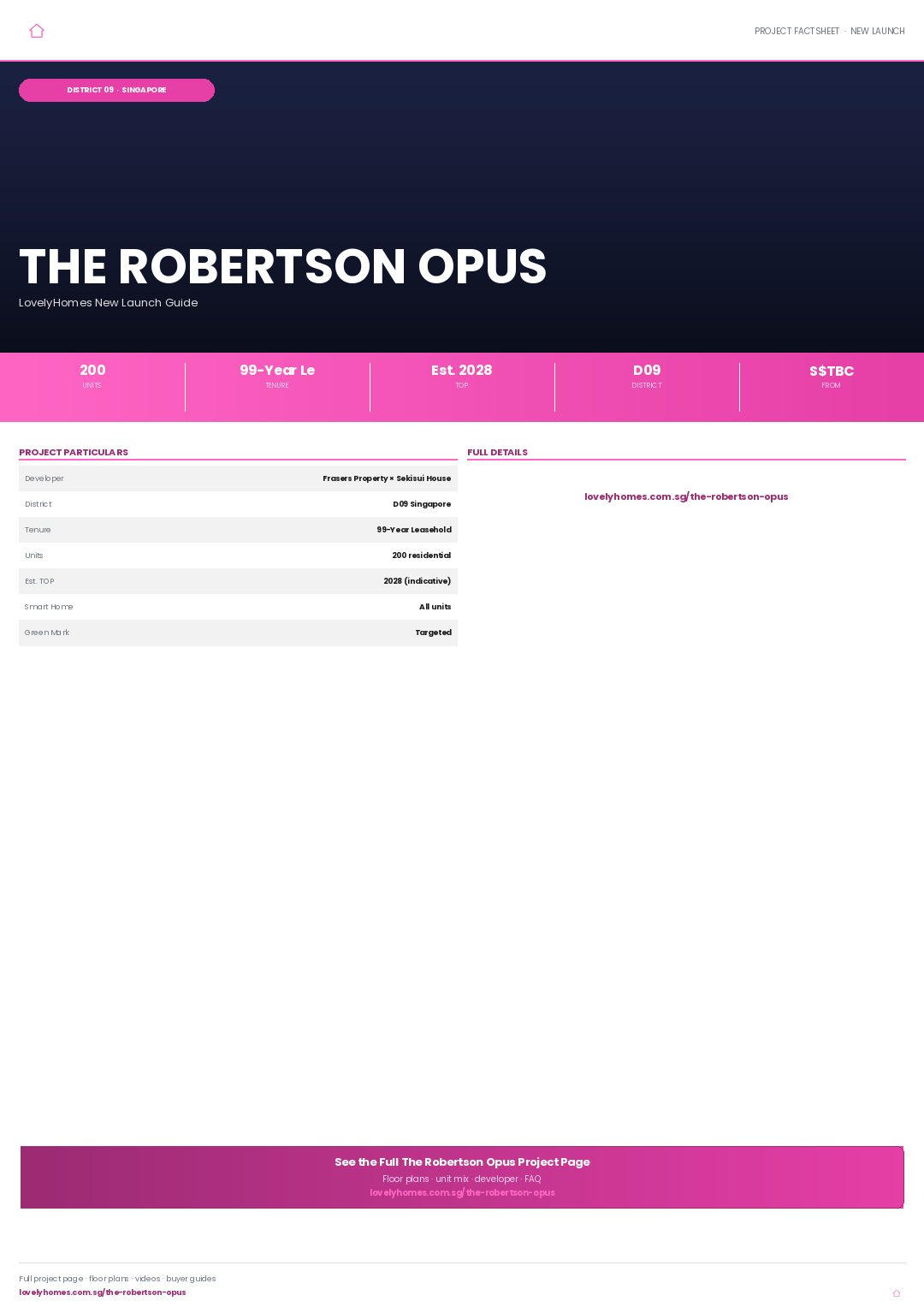

The Robertson Opus is a 200-unit 99-year leasehold residential development in District 09, Singapore, developed by Frasers × Sekisui House with an estimated TOP of 2028.

01 · Location

District 09 Address

Well-connected neighbourhood with access to public transport, schools, and lifestyle amenities.

02 · Scale

200 Residences

99-Year Leasehold development with quality fittings, smart-home provisions, and full condominium facilities.

03 · Value

New-Launch Advantage

Progressive payment schedule, 12-month Defects Liability Period, and modern specifications throughout.

Project At-a-Glance

Project Name

The Robertson Opus

Developer

Frasers × Sekisui House

District

D09

Tenure

99-Year Leasehold

Total Units

200

Est. TOP (VP)

2028

Est. Legal Completion

2031

Unit Mix and Sizes

Bedroom Type

Size (sqft)

Units

% of Total

Download the project factsheet for the full unit mix breakdown and confirmed sizes.

Refer to the developer’s official sales kit for confirmed unit types, sizes, and availability. Download factsheet (PDF).

Indicative Pricing

Suite

From S$1.388M

431 sqft

1BR

From S$1.598M

495 sqft

3BR DuoFlex

From S$3.213M

990-1,023 sqft

Current public balance-unit snapshot shows suites from S$1.388M, 1BR from S$1.598M, 2BR from S$2.317M and 3BR DuoFlex from S$3.213M. Source: The Robertson Opus NewLaunches price list updated 20 Mar 2026, accessed 29 Apr 2026.

Why Buyers Are Watching

1

District 09 location — well-connected address with MRT access, expressways, and lifestyle amenities in an established residential corridor.

2

99-Year Leasehold — 99-year leasehold enabling full CPF usage and bank financing from day one.

3

200 residential units — boutique scale ensuring exclusivity and a curated ownership community.

4

Developer pedigree — Frasers × Sekisui House brings a track record of quality residential development across Singapore’s private property market.

5

Progressive payment advantage — staggered cash outlay during construction typically saves S$30,000–S$60,000 in loan interest compared to a full resale drawdown.

6

12-month Defects Liability Period — legally binding developer obligation to rectify defects at no cost within 12 months of TOP.

Location and Connectivity

Transport

MRT Access

Conveniently located near MRT stations connecting to the wider Singapore rail network.

Expressways

Road Connectivity

Access to major expressways for quick connections to the CBD, Changi Airport, and key destinations.

Lifestyle

Shopping & Dining

Nearby malls, hawker centres, supermarkets, and F&B within the immediate neighbourhood.

Schools

Education Belt

Primary and secondary schools within 1–2 km, with tertiary institutions in the broader district.

Elevation overview · indicative only · refer to developer’s official stack chart for confirmed positions

Facilities (30+)

Swimming PoolGymnasiumFunction RoomsBBQ PavilionsChildren’s PoolJacuzziClub LoungeGarden PavilionSky TerraceYoga LawnSmart Home SystemEV Charging24-Hour SecurityBicycle BaysPneumatic Waste System

Gallery

Developer and Consultant Team

Frasers × Sekisui House

Developer of The Robertson Opus with residential development expertise in Singapore’s private property market. Consultant team details are available in the project factsheet.

Developer

Frasers × Sekisui House

District

D09

Estimated TOP

2028

Sustainability and Specifications

BCA Green Mark: Designed to meet BCA Green Mark standards with energy-efficient envelope and water-efficient fittings.

Smart Home: Smart home management provisions across all units for access control and utilities.

EV Infrastructure: Electric vehicle charging provisions in basement carpark.

Quality Finishes: Premium materials and fittings in line with developer specifications throughout.

Project Timeline

2023–2024

Land Award & Licence

2024–2025

Sales Launch

2025–2028

Construction Phase

2028

Estimated TOP (VP)

2031

Legal Completion

Project Factsheet

A shareable 2-page PDF snapshot — bring it to viewings, share with family.

DISCLAIMER: All information is compiled from publicly available sources and developer-issued materials for informational purposes only. Prices, unit mix, specifications, and timelines are indicative and subject to change without notice. This page does not constitute an offer to buy or sell. Seek advice from a licensed property agent and legal counsel. LovelyHomes.com.sg is an independent editorial platform. Agency Licence: L3010858B.

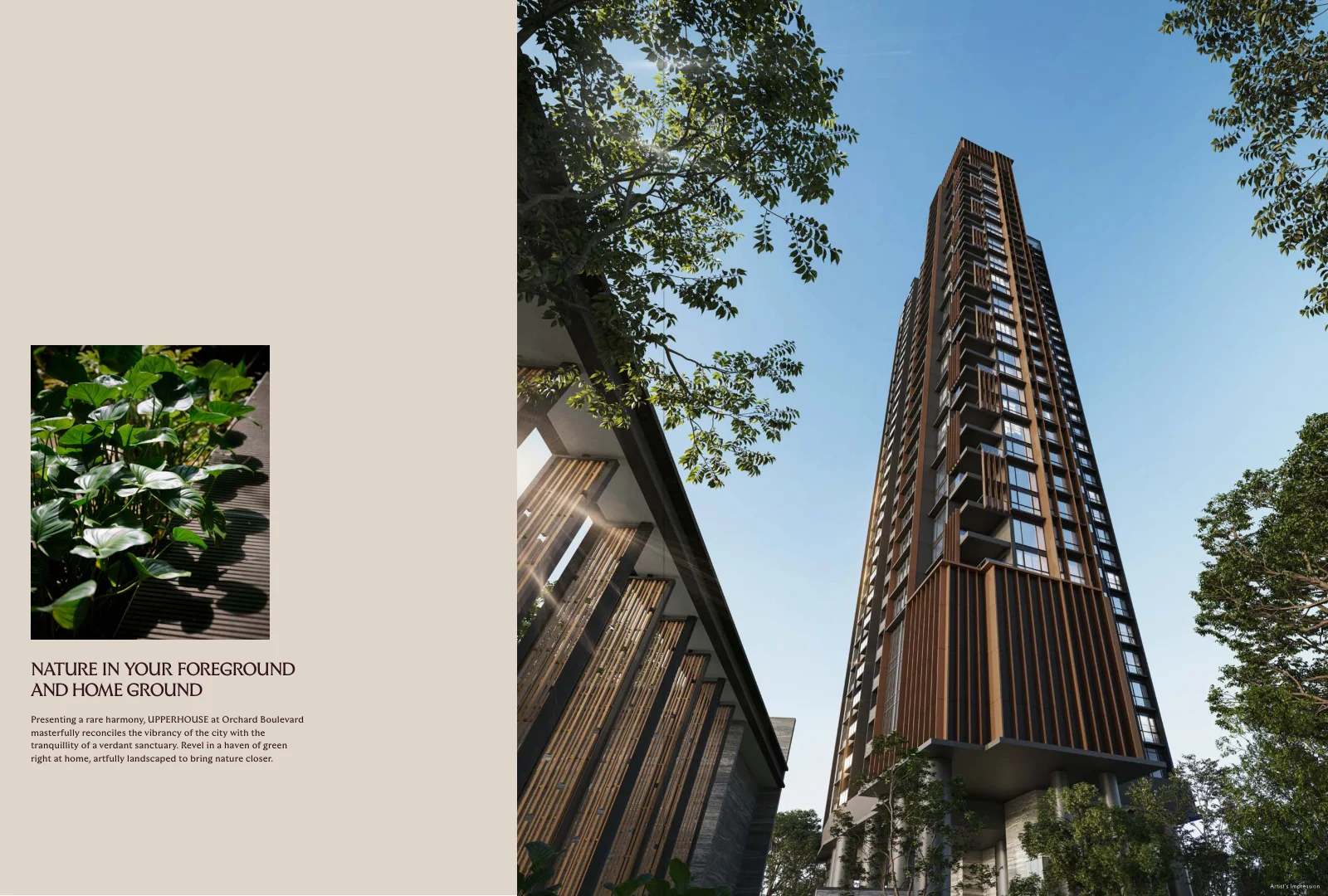

UPPERHOUSE at Orchard Boulevard (傲杰嘉苑) is a 301-unit luxury condominium at 22 Orchard Boulevard, District 10 — jointly developed by UOL Group Limited and Singapore Land Group Limited, launched in July 2025 at an average of S$3,350 psf. A single 35-storey tower on a 7,031 sqm site, it sits a one-minute walk from Orchard Boulevard MRT (Circle Line) and within arm’s reach of Singapore Botanic Gardens, the Tanglin Club and the Orchard Road shopping belt. UOL’s flagship ‘Masterpiece Collection’ — the same lineage as Meyer House and Watten House — UPPERHOUSE targets affluent owner-occupiers who want the prestige of an Orchard address without the transience of a shoebox. This page captures the developer-confirmed facts, launch performance data, and our own analysis of why District 10 remains Singapore’s most resilient residential market in 2026.

Figure 1: UPPERHOUSE at Orchard Boulevard — 35-storey luxury condo rising above the prime Orchard Boulevard enclave. Artist’s impression by UOL Group and Singapore Land Group.

Why UPPERHOUSE matters for the 2026 District 10 market

The Orchard Boulevard corridor is the tightest pipeline in Singapore’s Core Central Region. Between 2015 and 2024, fewer than five new-launch private condominiums broke ground within a ten-minute walk of Orchard Boulevard MRT — the notable exceptions being the ultra-luxury 19 Nassim (2020) and Boulevard 88 (2019). Land supply here is structurally constrained: Good Class Bungalow Areas (GCBAs) hem the estate on three sides, the Singapore Botanic Gardens blocks the western perimeter, and Orchard Road’s commercial zoning limits residential conversion. Against this backdrop, UOL’s S$428 million GLS bid — S$1,617 per square foot per plot ratio (psf ppr) — secured the last meaningful Orchard Boulevard residential parcel for a decade.

The ‘Masterpiece Collection’ positioning is deliberate. UOL’s previous chapter was Watten House at Bukit Timah (2023, average S$3,230 psf); before that, Meyer House (2019). UPPERHOUSE is the third instalment — each project elevated slightly in PSF and address prestige. At an average launch price of S$3,350 psf, UPPERHOUSE sits above Watten House but below the ultra-luxury segment (Newport Residences, Nassim Hill Residences), occupying a ‘collectible luxury’ niche that targets returning global Singaporeans, high-net-worth investors seeking yield on 1-bed+Study units, and established families looking for a forever-home within one estate of everything.

Quick facts — UPPERHOUSE at a glance

Project Name

UPPERHOUSE at Orchard Boulevard (傲杰嘉苑)

Developer

United Venture Development (No. 7) Pte. Ltd. — JV of UOL Group Limited & Singapore Land Group Limited

Address

22 Orchard Boulevard, Singapore 249628

Region & District

CCR — District 10 (Tanglin / Orchard)

Tenure

99-year leasehold commencing 20 May 2024

Site Area

7,031.4 sqm / 75,689 sqft

Plot Ratio

3.5 (permissible GFA: 24,610 sqm)

Total Units

301 residential units (1 block, 35 storeys) + 6 commercial units at 1st storey

PPVC (Prefabricated Prefinished Volumetric Construction) with Cast-in-situ

Expected Vacant Possession (VP)

30 June 2029

Expected Legal Completion

30 June 2032

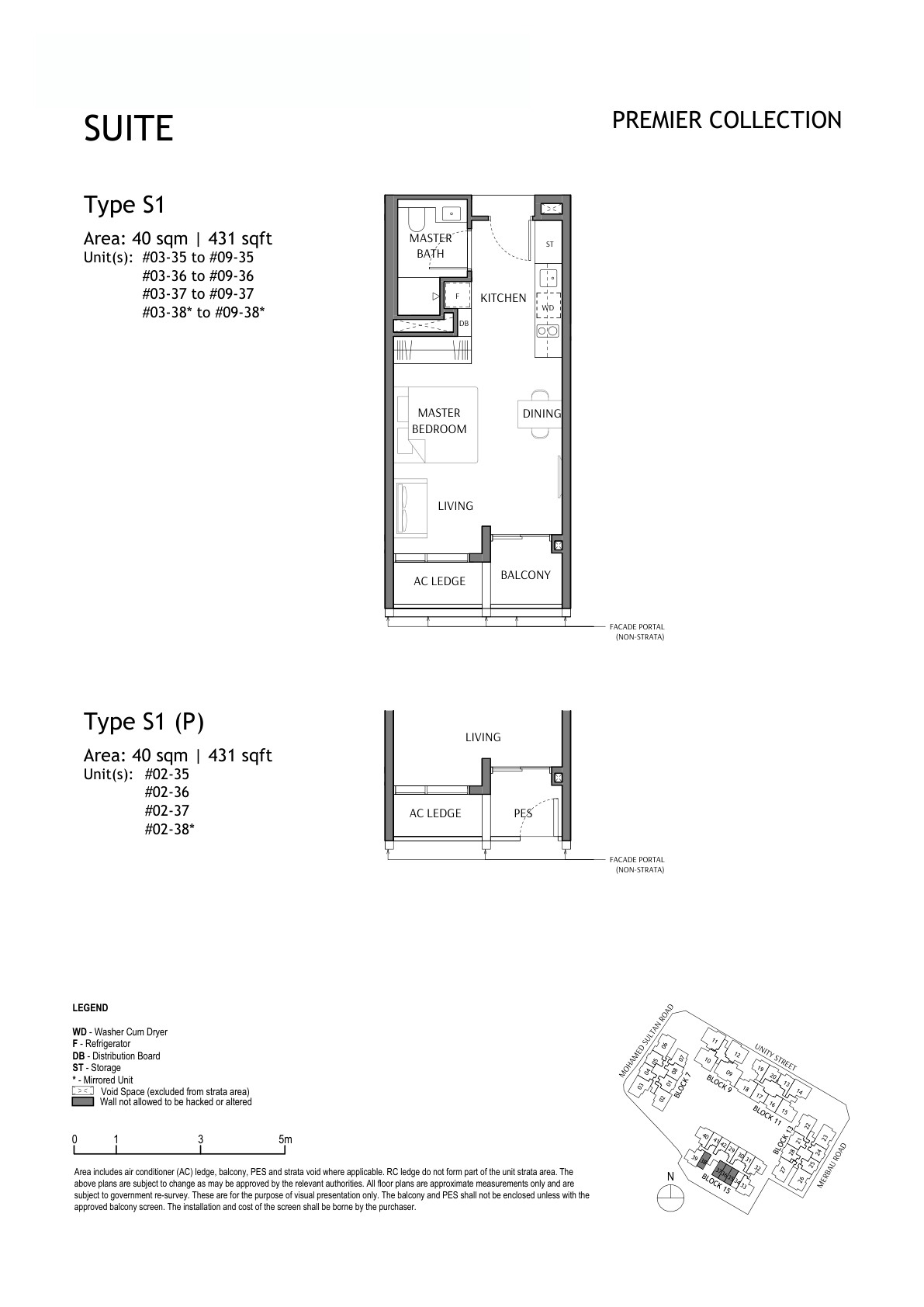

Unit mix — five layout types across 301 units

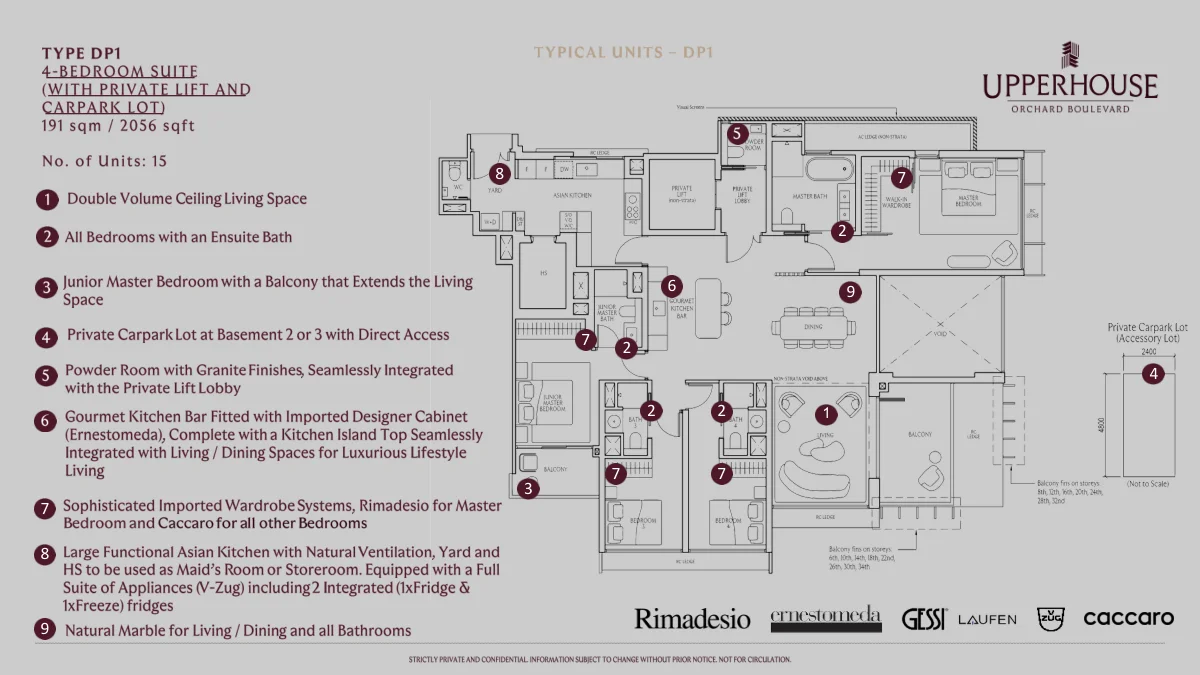

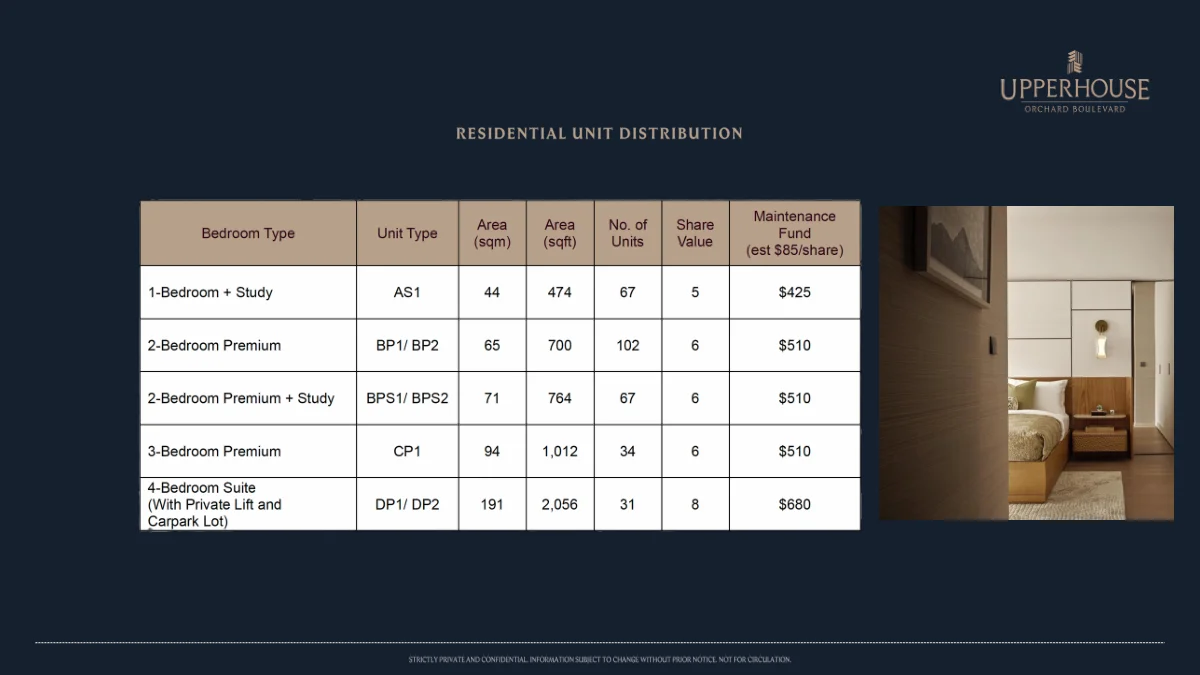

UPPERHOUSE’s unit mix is deliberately compact in breadth but rich in quality. There are no studio or micro units — the smallest footprint is 44 sqm (474 sqft), a 1-Bedroom + Study that still manages to include a study nook, silver-marble living floor, Caccaro wardrobe and a full suite of V-ZUG kitchen appliances. At the top end, the 31 four-Bedroom Suite units at 191 sqm (2,056 sqft) come with private lift access, private carpark lots, double-height living rooms (6.35m), Ernestomeda Italian kitchen cabinetry and Rimadesio wardrobes — a trophy-apartment specification rare outside the S$5M+ segment.

Bedroom Type

Unit Code

Size (sqm)

Size (sqft)

No. of Units

Est. Monthly Maintenance

1-Bedroom + Study

AS1

44

474

67

S$425 (5 shares @ S$85/share)

2-Bedroom Premium

BP1 / BP2

65

700

102

S$510 (6 shares)

2-Bedroom Premium + Study

BPS1 / BPS2

71

764

67

S$510 (6 shares)

3-Bedroom Premium

CP1

94

1,012

34

S$510 (6 shares)

4-Bedroom Suite (Private Lift + Carpark)

DP1 / DP2

191

2,056

31

S$680 (8 shares)

Total

301

Figure 4: Sample 1-Bedroom + Study floor plan (AS1, 44 sqm / 474 sqft) — the smallest unit still features silverite marble living floor and Caccaro wardrobe.

Pricing — S$3,350 psf average with S$2,950–S$3,890 psf range

UPPERHOUSE launched on 19 July 2025, moving 162 of 301 units (53.8%) on the first day at an average of S$3,350 psf — the strongest single-day take-up in the District 10 / Orchard corridor since Boulevard 88 in 2019. The most absorbed type was the 2-Bedroom Premium + Study (764 sqft): 60 out of 67 units sold on Day 1, at S$2.338M–S$2.72M (S$3,060–S$3,560 psf). The 4-Bedroom Suites were priced from approximately S$6.2M (around S$3,020 psf), representing strong absolute value for 2,056 sqft of Orchard District floor space.

Unit Type

Size (sqft)

Indicative Price From

Indicative PSF

1-Bedroom + Study

474

~S$1.40M

~S$2,950 psf

2-Bedroom Premium

700

~S$2.10M

~S$3,000 psf

2-Bedroom Premium + Study

764

S$2.338M–S$2.72M

S$3,060–S$3,560 psf

3-Bedroom Premium

1,012

~S$3.25M

~S$3,210 psf

4-Bedroom Suite

2,056

~S$6.20M

~S$3,020 psf

Note: Prices based on July 2025 launch data. Residual balance units may differ. Always verify current pricing directly with the developer or your appointed agent.

10 highlights of UPPERHOUSE at Orchard Boulevard

UOL Masterpiece Collection pedigree — the third release after Meyer House (2019) and Watten House (2023), each benchmarking a new quality standard for Singapore luxury residential.

1-minute walk to Orchard Boulevard MRT (Circle Line, Stage 6) — one of the fastest MRT-to-doorstep connections on any Orchard-area launch in recent years.

Steps from Singapore Botanic Gardens (UNESCO World Heritage Site, 82 hectares) — the only major new-launch condo that can legitimately claim Botanic Gardens urban-park adjacency.

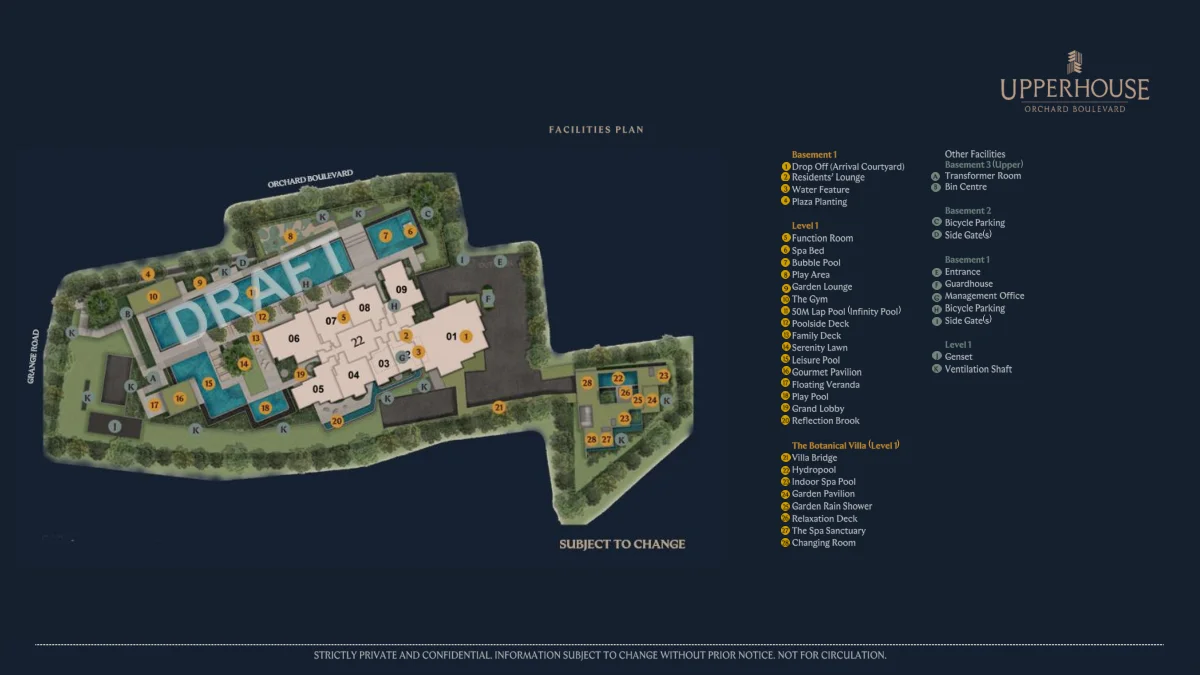

50m lap pool, 5 lanes (7.5m × 50m) — genuinely competition-length for a 301-unit development; rare at this scale in the CCR.

The Botanical Villa wellness pavilion (320 sqm) — private spa sanctuary with hydropool (~28 sqm), indoor spa pool (~9 sqm, hot water), and curated nature-garden setting.

Full V-ZUG Swiss kitchen appliances across all unit types — combi steam ovens and integrated appliances standard from the 1-bed+Study.

4-Bedroom Suite private lift access — 31 units with private residential lifts from Basement 3 to the 35th storey, plus an assigned private carpark lot.

Double-height living room for 4BR Suites (6.35m ceiling) — a genuinely architectural moment that distinguishes these units from conventional high-floor condominiums.

PPVC construction with Italian and Turkish finishes — Silverite marble (Turkey), Caccaro/Rimadesio/Ernestomeda Italian cabinetry, engineered timber flooring, smart home management system throughout.

GCBA views from upper floors — the tower rises above neighbouring buildings; floors above roughly the 10th have unobstructed views across low-rise greenery to Marina Bay.

Connectivity — Orchard at your door, CBD in minutes

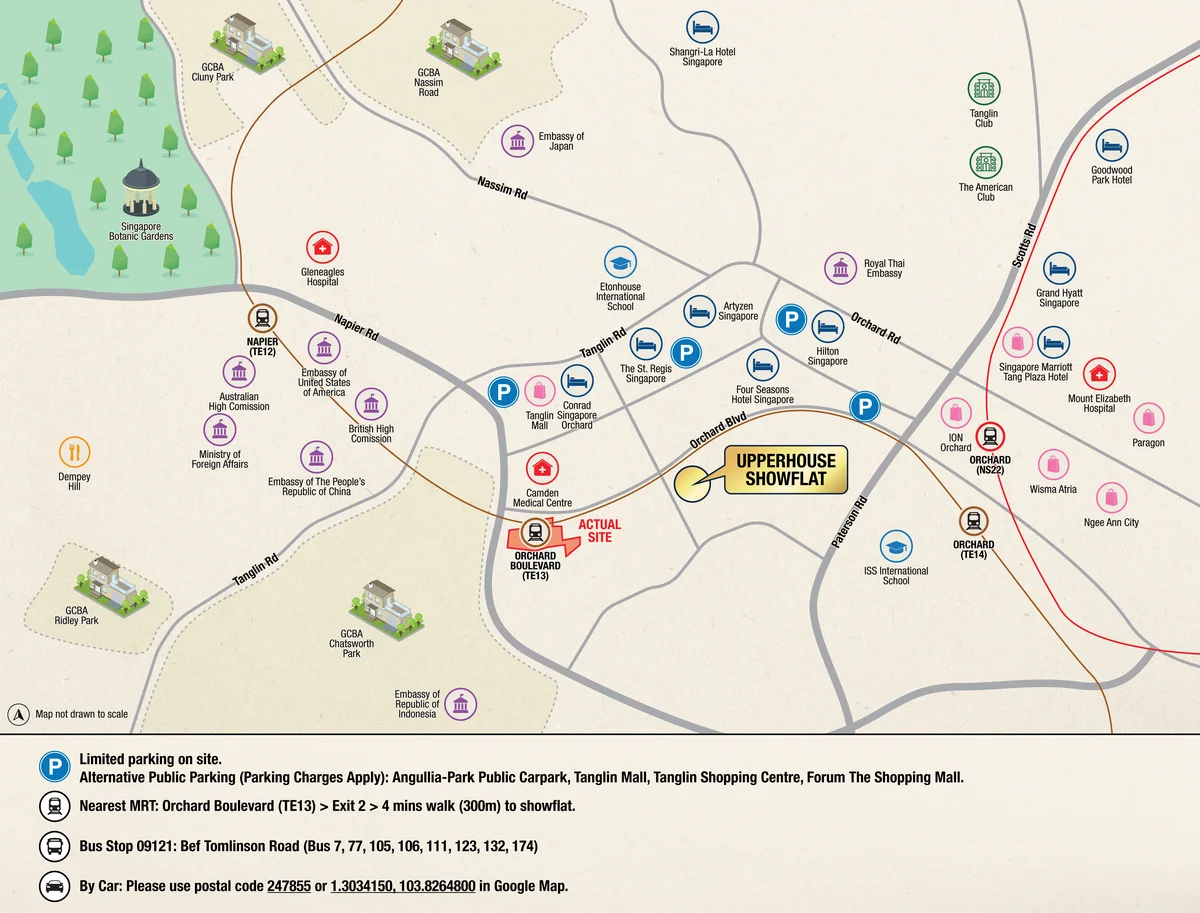

Figure 6: Location — UPPERHOUSE fronts Orchard Boulevard with Orchard Boulevard MRT (CCL) at 1-minute walk; the Botanic Gardens entrance gate is a 3-minute stroll.

UPPERHOUSE sits at the southern end of Orchard Boulevard, equidistant between Napier Road and Tanglin Road. Orchard Boulevard MRT (Circle Line, opened 2021) places residents one stop from Holland Village and two stops from Buona Vista — and gives direct CCL access to Bishan, Serangoon, Marina Bay, Harbourfront and Dhoby Ghaut (interchange to North-South and North-East Lines) without changing trains.

Destination

Distance / Time

Orchard Boulevard MRT (Circle Line)

1-minute walk

Singapore Botanic Gardens (UNESCO)

3-minute walk

Tanglin Mall

3-minute walk

ION Orchard / Ngee Ann City

6-minute drive

Great World Shopping Centre

4-minute drive

Dempsey Hill / Holland Village

6–8-minute drive

Central Business District

10-minute drive / 3 MRT stops

River Valley Primary School

6-minute drive

Anglo-Chinese School (Junior)

11-minute drive

NUS Bukit Timah Campus

9-minute drive

Lifestyle — Orchard, Tanglin and Botanic Gardens on your doorstep

The UPPERHOUSE catchment is arguably Singapore’s most complete urban lifestyle precinct. North along Orchard Boulevard leads to ION Orchard, 313@Somerset, Ngee Ann City, Tang Plaza and Paragon — international luxury brands, Michelin-starred dining and art galleries within a fifteen-minute walk. South along Tanglin Road opens Dempsey Hill’s weekend farmers’ market, Botanic Gardens bistros and the quiet lanes of the Tanglin Club and American Club. The Singapore Botanic Gardens — Singapore’s only UNESCO World Heritage Site — is three minutes on foot, a 82-hectare counter-balance to the urban energy of Orchard Road. For families, a strong belt of schools including Singapore Chinese Girls’ School, River Valley Primary and the ACS campuses is within comfortable daily-commute distance.

Figure 2: Rising above the GCBA belt, UPPERHOUSE commands sweeping views across botanical landscape and glittering cityscape. Artist’s impression.

Floor plans — curated finishes by bedroom tier

Figure 5: 4-Bedroom Suite floor plan (DP1/DP2, 191 sqm / 2,056 sqft) with private lift lobby, gourmet kitchen bar, Asian kitchen and double-height 6.35m living room.

UPPERHOUSE’s layout strategy is tiered: units from 1-Bed+Study to 3-Bedroom Premium share the same quality of marble, cabinetry and appliances in proportionate scale. The 4-Bedroom Suites step up to a separate specification tier — Ernestomeda (Italy) gourmet kitchen bar with Rosso Levanto marble island, Rimadesio walk-in wardrobe system, concealed ducted air-conditioning, and a dedicated Asian kitchen. Ceiling heights are 2.94m throughout, rising to 3.05m in 4BR dining/bedrooms and 6.35m double-height in the 4BR living room. Balconies are provided across all unit types with laminated glass railings at 1,050mm height.

Facilities — The Botanical Villa and 50m lap pool

Figure 3: Site plan — the 7,031 sqm landscaped deck features a 50m lap pool, leisure/bubble/play pools, Botanical Villa wellness pavilion, Gourmet Pavilion and The Gym.

Given UPPERHOUSE’s single-tower design on a 7,031 sqm footprint, the facility design is concentrated and curated rather than sprawling. The centrepiece is The Botanical Villa — a 320-sqm enclosed wellness sanctuary with a hydropool (28 sqm), indoor spa pool (9 sqm, heated), and two changing rooms. The main pool is a genuine 50m lap pool (7.5m × 50m, 5 lanes), complemented by a 113-sqm leisure pool, 84-sqm bubble pool (spa beds, bubble jets) and a 37-sqm play pool. Further amenities: Gourmet Pavilion (electric BBQ), Function Room (52 sqm, integrated appliances), Resident’s Lounge (33 sqm), and The Gym (45 sqm). Smart community control panels are provided at lift lobbies, and 76 bicycle lots are available at Basements 1 and 2.

Developer — UOL Group Limited & Singapore Land Group

United Overseas Land (UOL) Group Limited is one of Singapore’s largest publicly listed property developers, with a portfolio spanning residential, commercial and hospitality assets. Its celebrated Singapore residential launches include Watten House (2023), Amber 45 (2018), and Principal Garden (2015). Singapore Land Group (SingLand) is UOL’s listed subsidiary with extensive commercial holdings along Orchard Road and in the CBD. The two entities have co-developed numerous residential projects under the ‘United Venture Development’ JV structure. Both are ultimately controlled by the Wee family. Their track record on premium residential delivery is strong: Watten House reached TOP in 2025 with strong secondary-market demand and minimal buyer complaints, demonstrating consistent delivery quality.

Sustainability — PPVC construction and smart home integration

UPPERHOUSE uses PPVC (Prefabricated Prefinished Volumetric Construction) combined with conventional cast-in-situ elements — a hybrid that reduces on-site waste, shortens construction time, and produces more consistent quality for finishing. Smart home management system (covering access control, facilities booking and unit-level climate control) is standard across all 301 units. EV charging is provided at 5 residential lots. A Pneumatic Waste Conveyance System (PWCS) handles refuse disposal.

Timeline — key dates at a glance

GLS Site Awarded

2023

Land Tenure Commencement

20 May 2024

Developer’s Licence

C1528 (UEN: 202322557C)

VVIP Preview & Launch

July 2025 (sold 162/301 units on Day 1 at avg S$3,350 psf)

Expected Vacant Possession (VP)

30 June 2029

Expected Legal Completion

30 June 2032

Frequently asked questions — UPPERHOUSE at Orchard Boulevard

What is the tenure of UPPERHOUSE at Orchard Boulevard?

UPPERHOUSE is a 99-year leasehold development with the leasehold commencing on 20 May 2024. By the time a buyer takes vacant possession in mid-2029, approximately 5 years of the 99-year term will have elapsed. While a 99-year tenure in District 10 is less prestigious than a freehold or 999-year site, the scarcity of the Orchard Boulevard address historically supports strong price resilience — Orchard Road corridor 99-year condominiums consistently command psf premiums over equivalent tenure properties in other districts.

How far is UPPERHOUSE from Orchard Road shops and MRT?

Orchard Boulevard MRT (Circle Line, Stage 6) is a 1-minute walk from the lobby. Tanglin Mall is approximately 3 minutes on foot. The main Orchard Road retail belt — ION Orchard, Ngee Ann City, Paragon, 313@Somerset — is a 6-minute drive or a 15-minute walk north along Orchard Road. The Singapore Botanic Gardens main entrance is a 3-minute walk south.

What is the average price per square foot at UPPERHOUSE?

At the July 2025 launch, the average transacted price was S$3,350 psf, with a range of approximately S$2,950–S$3,890 psf across all unit types. The most popular unit — 2-Bedroom Premium + Study (764 sqft) — transacted at S$2.338M–S$2.72M (S$3,060–S$3,560 psf). Current availability and pricing should be confirmed directly; residual units may carry a premium depending on floor and orientation.

Are there any studio or micro units?

No. The smallest unit at UPPERHOUSE is the 1-Bedroom + Study (AS1) at 44 sqm / 474 sqft. UOL has deliberately avoided the micro-unit format to attract owner-occupiers and long-term holders rather than short-term rental investors — consistent with the Masterpiece Collection branding.

What are the schools near UPPERHOUSE?

Within driveable distance: River Valley Primary School (6-minute drive), Singapore Chinese Girls’ School (6-minute drive), Anglo-Chinese School (Junior) (11-minute drive), Anglo-Chinese School (Barker Road) (11-minute drive), and NUS Bukit Timah Campus (9-minute drive). UPPERHOUSE does not sit within the 1km primary school priority phase for most of these schools but is within comfortable upper-priority zone for River Valley Primary.

Does UPPERHOUSE have a private lift for all units?

Only the 31 four-Bedroom Suite units (DP1 and DP2) have private residential lifts running from Basement 3 to the 35th storey. All other units use the four common residential lifts. The private lift for 4BR units operates as a single-door, single-compartment lift — and comes paired with a private carpark lot.

What kitchen appliances are provided?

All units receive a full suite of V-ZUG (Swiss) kitchen appliances. The 1-Bed+Study and 2-Bedroom types get a 2-zone induction hob, hood, combi steam oven, integrated fridge-freezer, and washer-cum-dryer. 3-Bedroom Premium units step up to a 3-burner gas hob. The 4-Bedroom Suite (DP1/DP2) receives a 5-burner gas hob, conventional oven, steam oven, vacuum drawer, wine cooler, integrated dishwasher, and separate full-size fridge and freezer — a complete cook’s kitchen.

Is UPPERHOUSE suitable for rental investment?

The Orchard Boulevard corridor commands consistently strong rental demand from expatriate tenants in finance, law and technology. Monthly rents for comparable 700 sqft condominiums in the area range from approximately S$5,000–S$7,500 (based on 2025 URA caveats). At a purchase price of ~S$2.1M for a 700-sqft 2BR Premium, the gross rental yield at S$6,000/month is approximately 3.4% — below OCR yields (3.5%–4.5%) but Orchard Boulevard tenants tend to sign longer leases and provide more stable occupancy: the classic CCR yield-for-capital-growth trade-off.

When is the expected vacant possession (TOP) date?

The expected date of Notice of Vacant Possession is 30 June 2029, with legal completion on 30 June 2032. Buyers on a progressive payment scheme will make payments tied to construction milestones, with the final 15% payable on VP. Given the PPVC construction method, the 2029 VP date is considered achievable under normal construction conditions.

What is the maintenance fee for UPPERHOUSE units?

Based on the factsheet, the estimated maintenance fund rate is S$85 per share per month. Share values are: 5 shares (1BR+Study, S$425/month), 6 shares (2BR, 2BR+Study, 3BR Premium, S$510/month), and 8 shares (4BR Suite, S$680/month). These are estimates and the actual maintenance fee will be set by the Management Corporation at its first Annual General Meeting after TOP. Single-tier MCST management applies.

Is UPPERHOUSE eligible for CPF usage and bank loan?

Yes. As a 99-year leasehold private residential development, UPPERHOUSE is eligible for CPF Ordinary Account usage (subject to valuation limits and age-of-buyer / remaining-lease calculations under CPF Board rules). Bank loans up to 75% LTV (or 55% for second property) are available subject to TDSR limits. For the 2BR Premium at ~S$2.1M with 75% LTV, the loan quantum is S$1.575M; at approximately 3.2% p.a. (2026 prevailing rate) over 25 years, the monthly instalment is approximately S$7,600 — within TDSR limits for a combined household income of around S$17,000+/month.

B2B73; Enquire about UPPERHOUSE at Orchard Boulevard For balance units, floor selection, and pricing, send us a WhatsApp enquiry: WhatsApp us about UPPERHOUSE

Disclaimer: This article is for general informational purposes only and does not constitute financial, legal, or property advice. All facts, unit mix data, and pricing information are based on developer-released materials and publicly available URA/media sources as at April 2026 and may have changed. Prices, availability, and project details are subject to change without notice. Always verify current details directly with the developer or your appointed estate agent. LovelyHomes.com.sg is not the developer of UPPERHOUSE at Orchard Boulevard and is not authorised to sell units on the developer’s behalf. Consult a licensed property agent and an independent financial adviser before making any purchase decision.