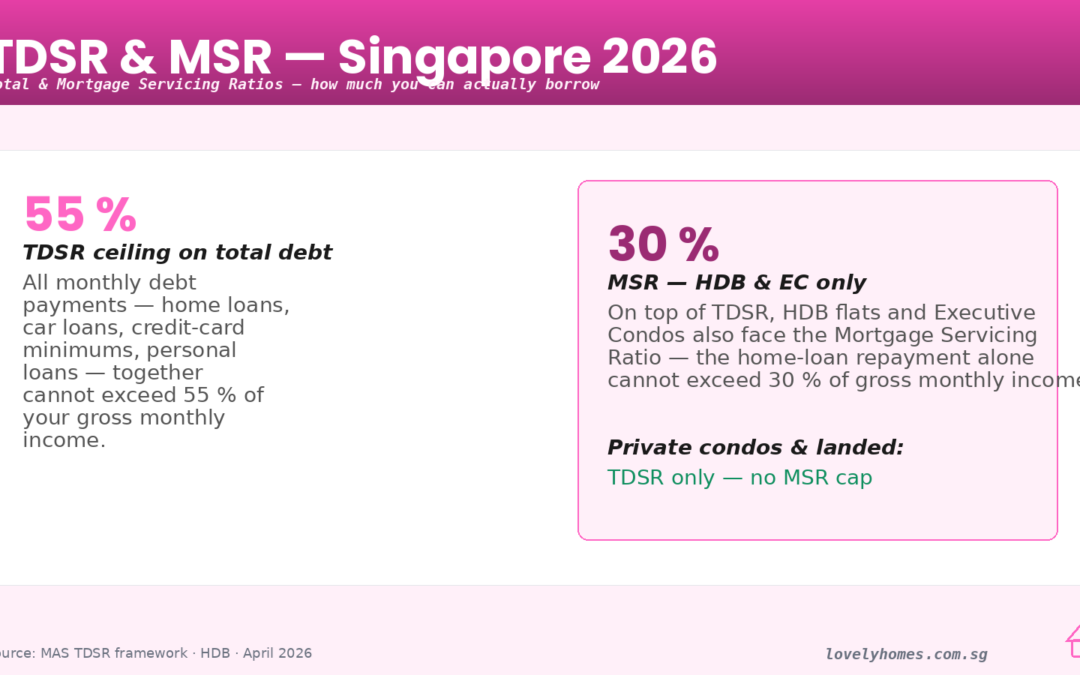

Figure 1: The two numbers that decide every Singapore home loan — TDSR at 55% of income and MSR at 30% for HDB and EC purchases.

If you have ever wondered why the bank’s pre-approval letter gave you a smaller loan than you budgeted for — or why a friend on the same salary can borrow noticeably more than you — the answer almost always comes down to two acronyms: TDSR and MSR. These are the two borrowing limits the Monetary Authority of Singapore (MAS) bakes into every residential mortgage, and in 2026 they are the single biggest determinants of how much home you can actually finance.

This guide is the 2026 edition. It covers exactly how TDSR and MSR are calculated, how they interact with the loan-to-value (LTV) cap, where the 4.0% stress-test rate comes from, what counts as income, what doesn’t, and — crucially — how to game the numbers in your favour without breaking any rules. We walk through a fully-worked Singapore example end-to-end and finish with the policy trajectory so you know what to watch for next.

Quick Answer: The 10 Things Every Singapore Borrower Should Know

TDSR is 55%. Total monthly debt repayments — including the new mortgage — cannot exceed 55% of your gross monthly income. Applies to every residential property loan.

MSR is 30%. Mortgage repayments on an HDB flat or Executive Condominium (EC) bought from the developer cannot exceed 30% of gross monthly income. Private condos and landed property have no MSR.

Stress-test rate is 4.0%. TDSR and MSR are calculated at a medium-term interest rate of 4.0% for residential loans, regardless of the rate you actually pay today.

LTV caps layer on top. First housing loan: up to 75% of purchase price. Second housing loan: up to 45%. Third and beyond: up to 35%.

Age and tenure matter. If the loan tenure pushes past age 65, or exceeds 30 years (25 for HDB), the LTV cap drops by 20 percentage points.

Variable income is haircut by 30%. Commission, bonus, rental and freelance earnings are only counted at 70% of the proven figure.

Existing debts eat into headroom. Car loans, credit-card minimum payments, student loans, and other mortgages all hit your TDSR ceiling before the new home loan does.

Guarantors are counted too. If you guarantee a sibling’s loan, it may sit in your TDSR — not theirs.

Cash down-payment rules mirror LTV. The first 5% (25% at higher LTV tiers) must be paid in cash; the balance can be CPF Ordinary Account funds.

Refinancing carve-out. Borrowers refinancing an owner-occupied property with no cash-out may be exempted from TDSR — a narrow but useful escape hatch.

What Is TDSR — The Framework That Underpins Every Home Loan

The Total Debt Servicing Ratio was introduced in June 2013 as part of MAS’s cooling-measures programme (see our full cooling measures timeline for the wider context). Its purpose is simple: to stop households from levering up to a level where a modest rise in interest rates would push them into negative cash flow. The 2010s saw Singapore’s household debt-to-GDP ratio climb past 70%, and MAS wanted a circuit-breaker that worked the same way regardless of which bank a buyer walked into.

TDSR caps all monthly debt obligations at 55% of gross monthly income. “All debt” is deliberately broad: it includes the prospective home-loan instalment (calculated at the stress-test rate), existing mortgages, car loans, personal loans, renovation loans, student loans, credit-card minimum repayments and any loans you have personally guaranteed. Even a dormant credit card with a S$20,000 limit is counted if the bank uses the 3% minimum-payment convention.

The ratio was originally set at 60% in 2013 and tightened to 55% in December 2021, where it remains in 2026. That three-percentage-point shave looks small on paper but at a typical Singapore household income removes roughly S$150,000–S$200,000 of borrowing capacity.

What Is MSR — The Second Ratio You Cannot Ignore for HDB and EC Buyers

The Mortgage Servicing Ratio is narrower but stricter. Introduced for HDB loans in 2011 and extended to bank loans on HDB flats in 2013, MSR caps the mortgage portion alone at 30% of gross monthly income for purchases of HDB flats and Executive Condominiums bought directly from the developer.

MSR is a subset of TDSR, not a substitute. HDB and new-EC buyers must clear both ratios — the tighter of the two binds. In practice MSR is almost always the binding constraint for HDB buyers because existing debt rarely adds up to the 25-percentage-point gap between MSR (30%) and TDSR (55%). For EC buyers the numbers narrow as the project moves through its 10-year maturation period — after the five-year minimum occupation period and the ten-year privatisation, a resale EC is treated like a private condo for borrowing-limit purposes, so TDSR alone applies.

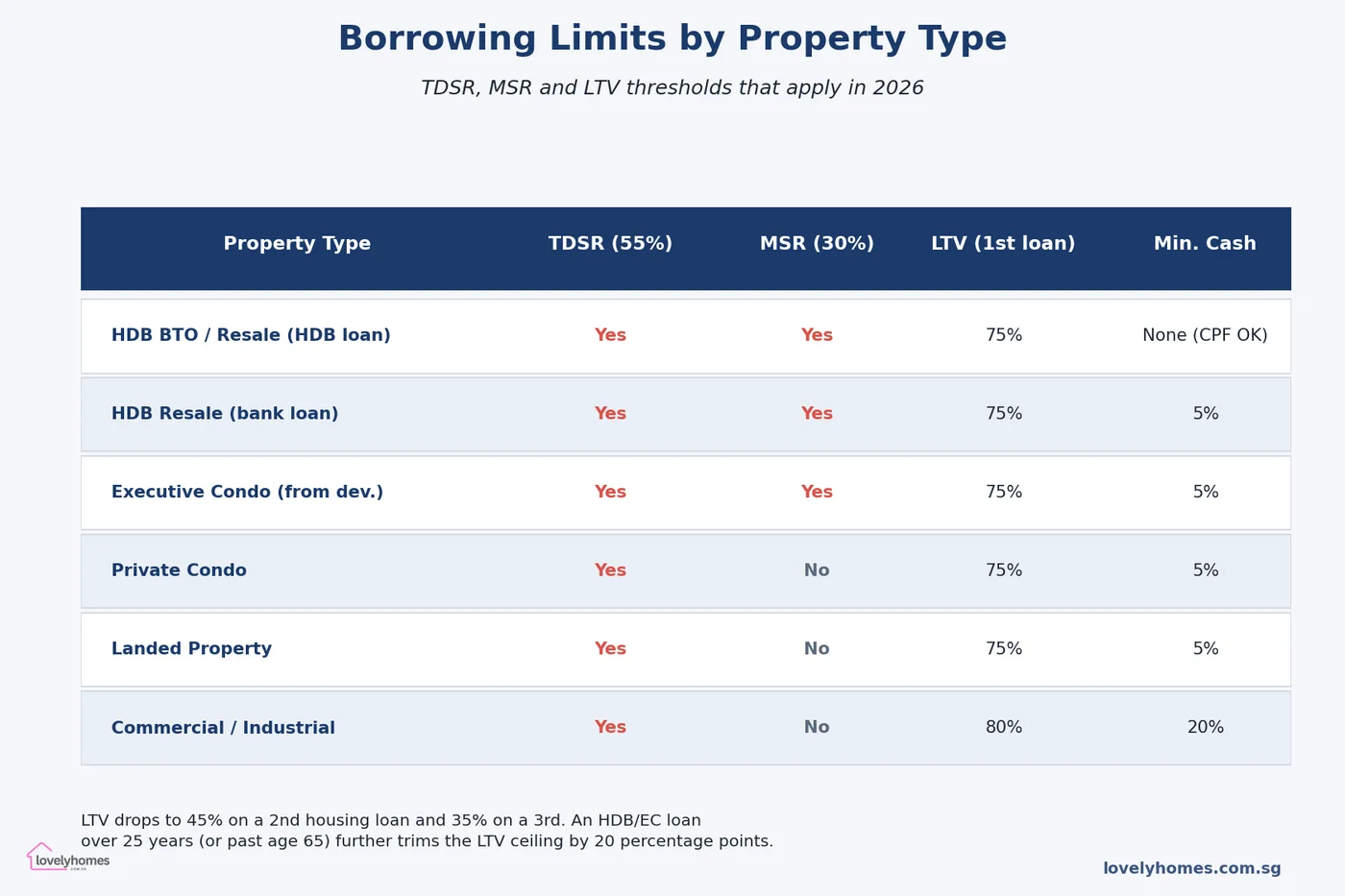

For a side-by-side look at which ratios hit which property type, the matrix below summarises 2026 rules.

Figure 2: 2026 borrowing limits by property type. HDB flats and ECs face both MSR and TDSR; private condos, landed property and commercial assets only face TDSR.

How the 4.0% Stress-Test Rate Works — And Why It Matters More Than Your Actual Rate

Here is the trap that catches most first-time buyers: banks must calculate your monthly instalment using an assumed rate of 4.0% for residential mortgages, even if your actual rate is 2.5% or 3.0%. This is the medium-term interest rate, set by MAS and reviewed from time to time. It was revised upward from 3.5% to 4.0% in September 2022 and has not moved since.

Why 4.0%? The rate is designed to approximate the long-run average that Singapore floating-rate loans have oscillated around over a 30-year horizon. It is deliberately punitive — regulators would rather have borrowers told “you qualify for less” at origination than have the same borrowers go into arrears when rates spike. Anyone who lived through the 2022–2023 rate cycle, when three-month SORA went from 0.2% to 3.8% in 18 months, will appreciate the logic.

The mechanic: the bank plugs a 4.0% rate into the standard amortisation formula using your chosen loan tenure, derives an assumed monthly instalment, and tests that figure against your TDSR (55%) and, if applicable, MSR (30%). Your actual repayment — calculated at whatever rate the bank is offering — will be lower in most cases, leaving you with a margin of safety that MAS consciously engineered.

What Counts as Income — And Why Variable Pay Is Penalised

Income for TDSR/MSR purposes is not what you see on your IRAS tax statement. MAS prescribes a structured treatment:

Fixed salary. Counted at 100%. Evidenced by payslips (usually three to six months) and the latest CPF contribution history.

Variable income. Commission, bonus, overtime, and freelance earnings are haircut by 30%, so only 70% of the verified average is recognised. The haircut applies to the entire variable component, even if you can show multiple years of steady track record.

Rental income. Counted at 70% of the gross rent receivable, net of void periods. A two-year tenancy agreement is strong evidence; month-to-month leases are viewed more sceptically.

Self-employed / business income. Two years of Notice of Assessment (NOA) are the default evidentiary bar, with the 30% haircut applied.

Allowances and AWS. Typically 100% if contractual and evidenced; otherwise haircut.

This is where the seemingly simple 55% number becomes surprisingly individual. A banker earning S$12,000 monthly but with 40% of that as variable gets assessed on S$7,200 fixed + S$3,360 post-haircut variable = S$10,560 — so the TDSR ceiling drops to S$5,808 per month rather than the nominal S$6,600.

What Counts as Debt — The Items Borrowers Miss

The other half of the equation is debt. The headline items — the new home loan instalment, existing mortgages, and car loans — are obvious. Less obvious items often catch borrowers out:

Credit-card minimum payments. Banks use a 3% minimum convention on the outstanding balance (or sometimes on the total credit limit). If you carry S$30,000 revolving credit across cards, that is a S$900 monthly hit on your TDSR — shaving S$192,000 off your loan ceiling at a 4.0% stress rate over 30 years.

Renovation and personal loans. Unsecured loan instalments count in full.

Student loans. Included in TDSR from the date repayments begin.

Guarantor obligations. If you have co-signed a relative’s loan and there is no formal debt-transfer, some banks will count the full instalment against you. Others use 50%. Ask the relationship manager explicitly.

Outstanding ABSD remission obligations. If you are on a remission schedule (e.g. from selling a prior property to claim remission on a new purchase), the existing loan remains in TDSR until the sale completes.

A Fully-Worked Example: A S$10,000-a-Month Household Buying a Private Condo

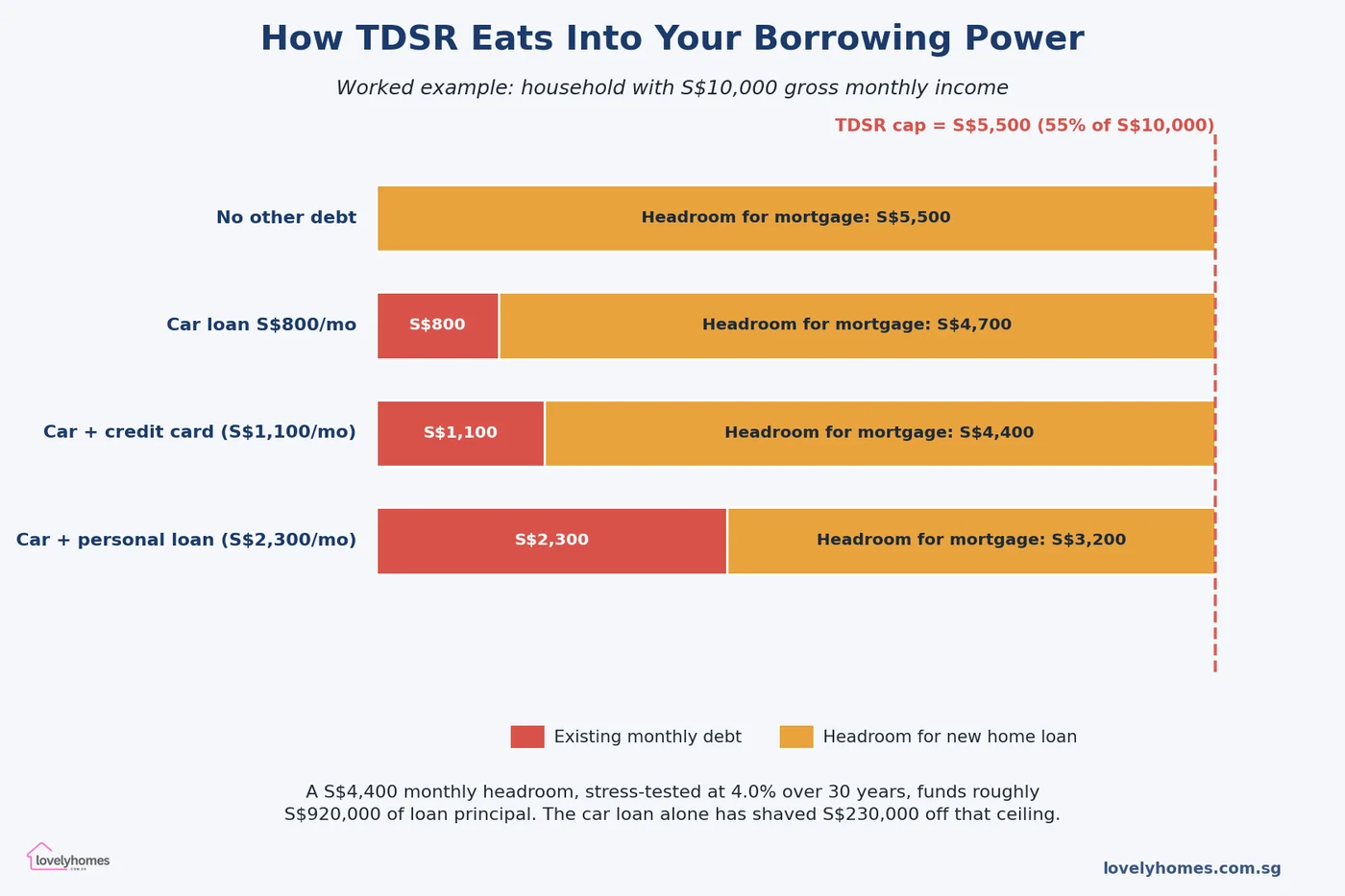

Figure 3: How different existing-debt profiles crater the monthly headroom available for a new mortgage, given a household earning S$10,000 gross.

Consider a dual-income couple: combined gross monthly salary S$10,000, both on fixed pay, no variable component. They are looking at a S$1.8 million resale private condo in District 15.

Step 1 — TDSR cap. 55% × S$10,000 = S$5,500. No MSR applies because this is a private condo.

Step 2 — Existing debts. One car loan at S$800/month and revolving credit balances generating a S$300/month minimum payment. Total existing obligations: S$1,100.

Step 3 — Headroom for the new mortgage. S$5,500 − S$1,100 = S$4,400 per month available for the new home loan instalment.

Step 4 — Maximum loan principal. At the 4.0% stress rate over a 30-year tenure, S$4,400 monthly funds approximately S$922,000 of loan principal (standard amortisation formula: P = M × [(1 − (1 + r)^(−n)) / r]).

Step 5 — LTV cap. At 75% LTV on an S$1.8m purchase, the bank could lend up to S$1,350,000 — but TDSR limits them to S$922,000 here, so TDSR binds, not LTV. The couple needs S$878,000 of combined cash and CPF equity.

Flip the same household to an HDB flat at S$700,000: now MSR binds first. 30% × S$10,000 = S$3,000 maximum mortgage instalment. That fundamentally funds roughly S$628,000 — well below the 75% LTV ceiling of S$525,000… wait. In this case the 75% LTV actually binds below MSR, because S$525,000 of loan needs only about S$2,500/month at 4.0% over 25 years, comfortably inside MSR. So the couple’s CPF-plus-cash needs to fill the remaining S$175,000.

These two scenarios show the recurring pattern: for HDB/EC buyers, MSR or LTV usually binds; for private/landed buyers, TDSR usually binds. The flow of the calculation matters, and every added dollar of existing debt has a disproportionate impact through the 30-year amortisation lever.

How to Legitimately Maximise Your Borrowing Ceiling

Nothing below involves gaming the system — each lever is recognised by banks and MAS. Together they can add S$200,000–S$400,000 to a buyer’s loan ceiling.

Close dormant credit facilities. A S$50,000 unused overdraft or a clutch of credit cards still hits TDSR via the 3% minimum rule. A week of admin before you apply for pre-approval can move the needle.

Pay down the car loan. High-instalment vehicle finance is the single most common TDSR killer. A S$1,000 monthly car note costs you roughly S$210,000 of home-loan capacity at 4.0%/30yr.

Lengthen the tenure (cautiously). A 30-year tenure beats a 25-year one on headline TDSR because the stress-rate instalment is lower — but watch the age-65 and 30-year triggers that knock the LTV down 20 points.

Co-apply with a higher earner. Joint applications aggregate income and debt. If spouses have different debt loads, consider which combination maximises the pooled headroom.

Formalise variable income. A commissioned sales professional with one year of written contracts may be haircut more heavily than one with two years of NOAs. Waiting one tax cycle can unlock meaningful capacity.

Use a Loan Assessment before committing. Banks in Singapore offer in-principle approval (IPA) at no cost. Three IPAs from different banks let you benchmark the figure.

How Singapore’s Framework Compares Globally

Singapore is not alone in prescribing debt-service ratios, but its combination is unusually strict. Hong Kong applies a 50% debt-service ratio with a 70% LTV cap for first-time owner-occupiers — broadly comparable but no separate MSR for public housing. The United Kingdom uses a 4.5× income loan-to-income ratio at most lenders (soft cap), with affordability stress-tested at 3 percentage points over the reversion rate. Australia’s prudential regulator APRA applies a serviceability buffer of 3 percentage points over the contracted rate — a rule-of-thumb approach rather than a hard ratio.

The common thread in all four jurisdictions is a stress-test mechanism designed to withstand a rate spike. Singapore’s 4.0% medium-term rate is higher (more conservative) than the contracted-rate buffers used in the UK and Australia, which is one reason Singaporean household debt has been more resilient through recent cycles than peers. MAS has been explicit that this is by design: household leverage is viewed as a systemic risk, not purely a consumer-protection issue.

What Might Come Next — The Forward View

The 4.0% stress rate has held since September 2022. Three scenarios could prompt a revision in the next 12–18 months:

Sustained higher long-term rates. If three-month SORA settles above 3.5% on a durable basis, MAS may nudge the medium-term rate to 4.25% or 4.5% to preserve the buffer it represents.

Renewed leverage in the private condo segment. If luxury-segment TDSR headroom is being used aggressively to bid up prime-district prices, expect tighter LTV on second/third loans rather than a TDSR change.

Public housing affordability stress. If HDB resale prices outrun wage growth materially, MSR could tighten from 30% to 25%. This would be the single most consequential move for first-time buyers.

None of the above is signalled by MAS at the time of writing (April 2026) — but the Financial Stability Review due in November 2026 is the data release to watch. Historically MAS has adjusted TDSR and MSR in the December statement that accompanies the cooling-measures package.

Frequently Asked Questions

1. Does TDSR apply to refinancing my existing mortgage?

For owner-occupied properties, a clean refinance without any cash-out and without extending the principal is generally exempted from TDSR under a carve-out MAS introduced to avoid penalising existing borrowers. If you take a cash-out top-up or increase the principal, the full TDSR test applies. For investment-property refinancing, TDSR applies in full regardless of cash-out status, so build in a review of your current debt profile before signing any refinance Letter of Offer.

2. How is TDSR calculated if I am self-employed with irregular income?

Banks use two years of Notice of Assessment (NOA) as the primary evidentiary source, take the simple average, apply the 30% haircut, and treat the resulting figure as your recognised gross monthly income. A particularly strong year — say a bumper bonus — will be smoothed. If you have less than two years of NOAs the bank will often decline or require a significantly larger down-payment. Incorporating yourself through a Pte Ltd does not change this; director’s remuneration drawn as salary is still subject to the haircut.

3. Can I borrow more by stretching the loan tenure?

Up to a point, yes. A 30-year tenure reduces the stress-rate instalment versus a 25-year tenure, increasing how much loan principal S$4,400 (in our worked example) can support. But two triggers cap the benefit: if your loan extends past age 65 or exceeds 30 years (25 for HDB), the LTV cap drops by 20 percentage points — from 75% to 55% on a first loan. The net effect is usually worse, not better. Most brokers recommend landing the tenure such that the loan concludes at or just before age 65.

4. Are joint-borrower applications better than going solo?

Usually, because they aggregate income while both parties still share the TDSR ceiling. The nuance is “income-weighted average age” for tenure calculations — if a 55-year-old and a 35-year-old co-apply, the bank blends their ages by income share to determine the maximum allowable tenure. Adding a much older co-applicant to a younger borrower can shorten the tenure and reduce the headroom on paper. Structured correctly, joint applications reliably produce higher approvals than solo for dual-income households.

5. What happens to TDSR if interest rates fall sharply?

Nothing, in the short run. The 4.0% stress rate is a regulatory input, not a market rate. Falling SORA means your actual monthly instalment shrinks and your actual debt-service ratio improves, but the ceiling at which MAS sets the TDSR bar is unchanged. Over a multi-year horizon, if rates settle well below 4.0% on a sustained basis, MAS may consider lowering the stress rate — but the precedent is that adjustments are infrequent (the last move was September 2022).

6. Does CPF Ordinary Account balance count as income for TDSR?

No. CPF OA is treated as equity (part of the down-payment and subsequent instalments), not as income. The monthly CPF contribution inflow also does not count as additional income — your CPF contributions are already a reduction from your gross pay, and gross pay is what banks use. The only way CPF affects borrowing capacity indirectly is through the Home Protection Scheme (for HDB loans) and through the cash-CPF split in the down-payment.

7. I was denied because of TDSR — what are my options?

First, get the denial reasoning in writing and compare it with a second IPA at a different bank — underwriting interpretations vary on edge cases, particularly around variable income and guarantor obligations. Second, tackle the debt side: clear a car loan, consolidate or close credit cards, discharge a guarantor role. Third, stretch the timeline: a fresh NOA next April may unlock the variable-income shortfall. Fourth, reduce the target property price — a 10% lower purchase price typically requires a proportionally smaller loan and therefore a smaller headroom. Finally, consider a joint application with a fixed-income parent (though this binds their future TDSR too).

This article is an editorial guide for general information only and does not constitute financial, legal or mortgage advice. The figures quoted reflect rules in force on the date of publication (April 2026) and may change. Confirm the authoritative position with the Monetary Authority of Singapore (MAS), the Housing & Development Board (HDB), your bank’s credit officer and a licensed mortgage broker before committing to any loan or property purchase. Interest-rate scenarios and worked examples are illustrative; your actual borrowing ceiling depends on the full underwriting review at application.

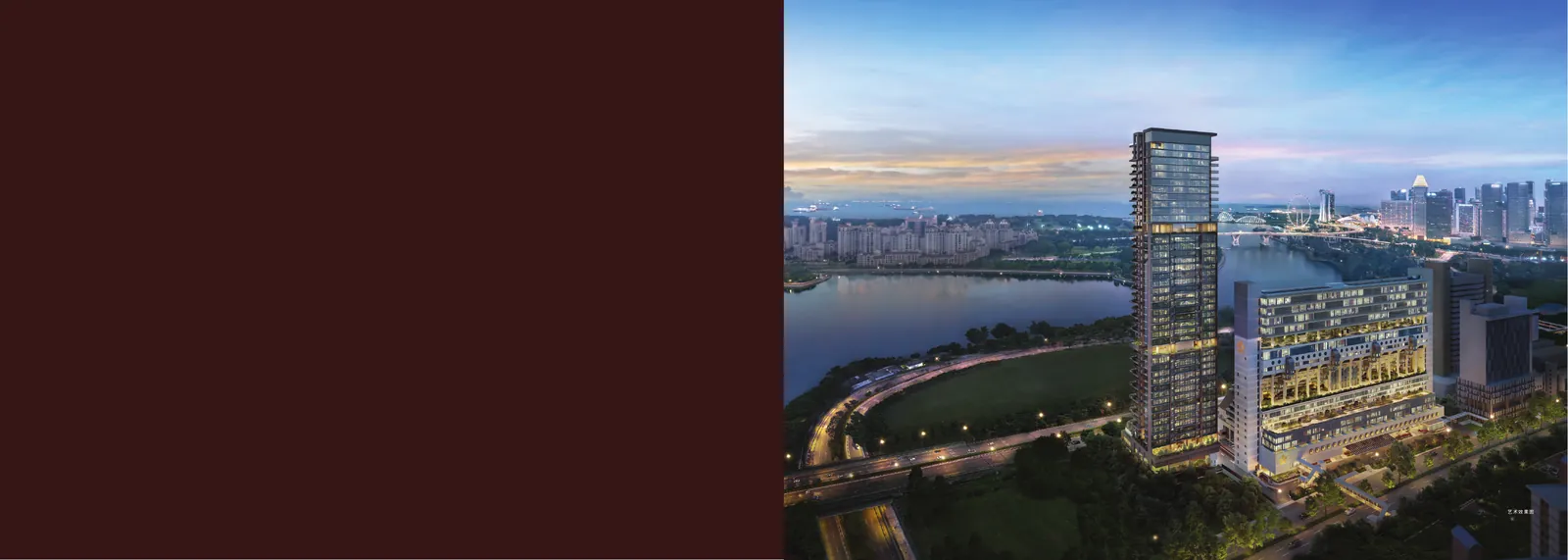

Aurea — Latin for golden — is the residential crown of The Golden Mile, the once-in-a-generation restoration of Golden Mile Complex, Singapore’s first large-scale modernist building to be gazetted for conservation. Developed by GMC Property Pte Ltd (a joint venture between Perennial Holdings and Far East Organization), Aurea rises 45 storeys above the heritage-listed 1973 terraced podium, delivering 188 homes in Singapore’s prime city-fringe District 7.

What sets Aurea apart is not one feature but the layering of four rarely-combined advantages: a District 7 address on Beach Road, the cultural pedigree of a nationally conserved modernist icon, a 5-minute covered walk to Nicoll Highway MRT (CC5) and a sky-rise programme that concentrates all 188 homes on a single tower — giving every unit light, view and amenity on a scale the city-fringe rarely offers.

The development is designed by DP Architects with conservation specialist Studio Lapis, targets BCA Green Mark Platinum, and is scheduled for TOP in Q2 2029, with vacant possession by 31 March 2030.

Pillar 01

Heritage reborn

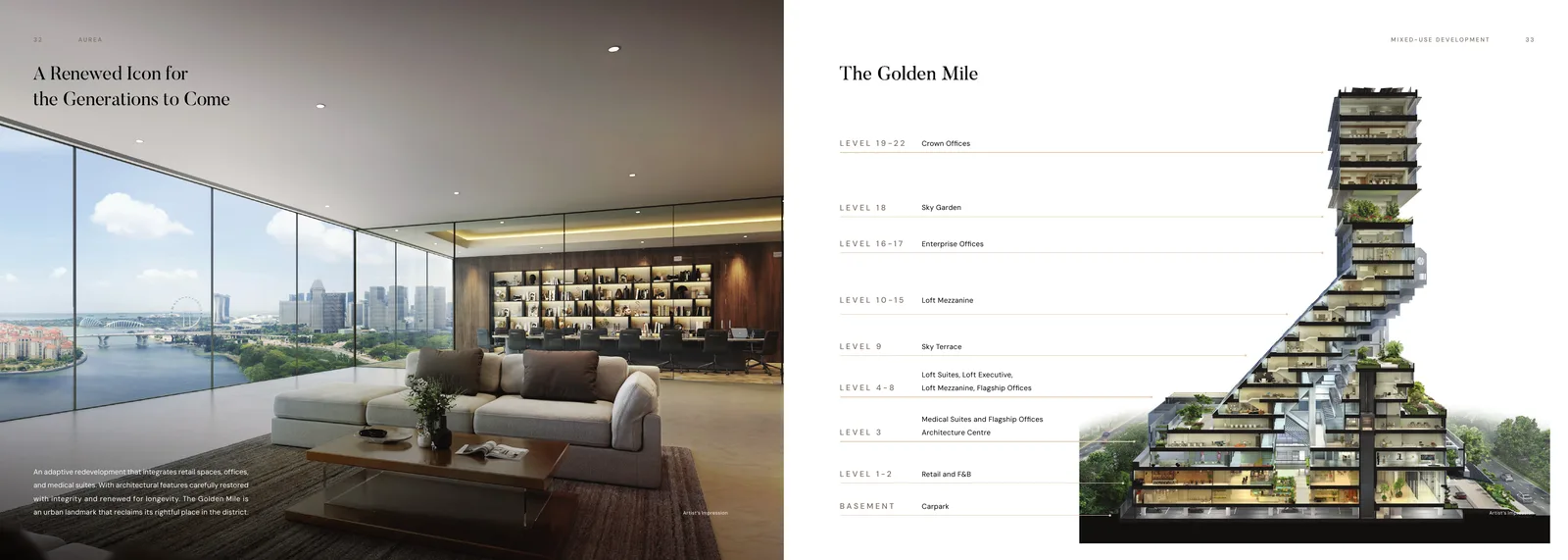

Aurea sits atop Singapore’s first large-scale conserved modernist building — the 1973 Golden Mile Complex by Design Partnership — now reimagined as The Golden Mile with retail, offices and medical suites.

Pillar 02

District 7 city-fringe

A 5-minute covered walk to Nicoll Highway MRT (CC5), 9 minutes to Lavender MRT (EWL), and short drives to Bugis Junction, Suntec City, Raffles City and Marina Bay Sands.

Pillar 03

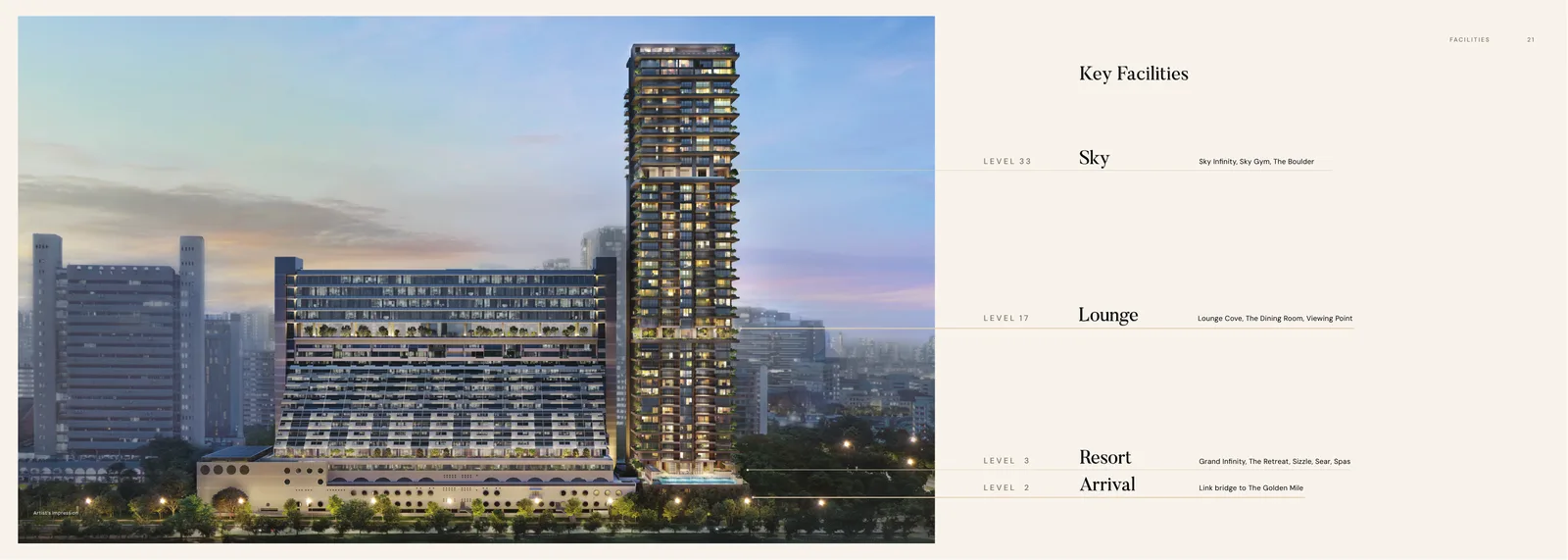

Sky-rising design

All 188 units in a single 45-storey tower. Three themed sky-terrace decks at Levels 17 and 33 bring gym, lounge and dining above Singapore’s Central Area skyline.

Project At-a-Glance

Developer

GMC Property Pte Ltd JV — Perennial Holdings and Far East Organization

Address

802 Beach Road Singapore 199980

District

7 · Golden Mile / Beach Road

Tenure

99-year leasehold from 18 Nov 2024

Site Area

13,462.30 sqm (≈ 144,908 sqft)

Total GFA

75,388.88 sqm · Plot Ratio 5.6

Blocks and Storeys

1 residential tower · 45 storeys and 3 basements

Total Units

188 residential

Carpark

129 lots + 3 accessible · 4 EV · 48 bicycle

Expected TOP

Q2 2029 (Residential)

Vacant Possession

31 March 2030

Architect

DP Architects Pte Ltd

Conservation Specialist

Studio Lapis Conservation

Landscape Architect

DP Green Pte Ltd

Civil and Structural Engineer

KCL Consultants Pte Ltd

Mechanical and Electrical Engineer

Rankine & Hill (Singapore) Pte Ltd

Quantity Surveyor

Rider Levett Bucknall Consultancy

Sustainability Target

BCA Green Mark Platinum

Unit Mix and Sizes

Type

Size (sqft)

Units

% of Total

2-Bedroom (B1 / B2 / B3)

635 – 710

84

44.7%

3-Bedroom (C1)

1,001

28

14.9%

4-Bedroom Signature (D1)

1,442

28

14.9%

4-Bedroom Premium Signature (D2)

1,798

28

14.9%

5-Bedroom Skyliving (E1 / E2)

2,863 – 3,251

18

9.6%

Penthouse (PH1 / PH2)

5,608 – 8,816

2

1.1%

Total

635 – 8,816

188

100%

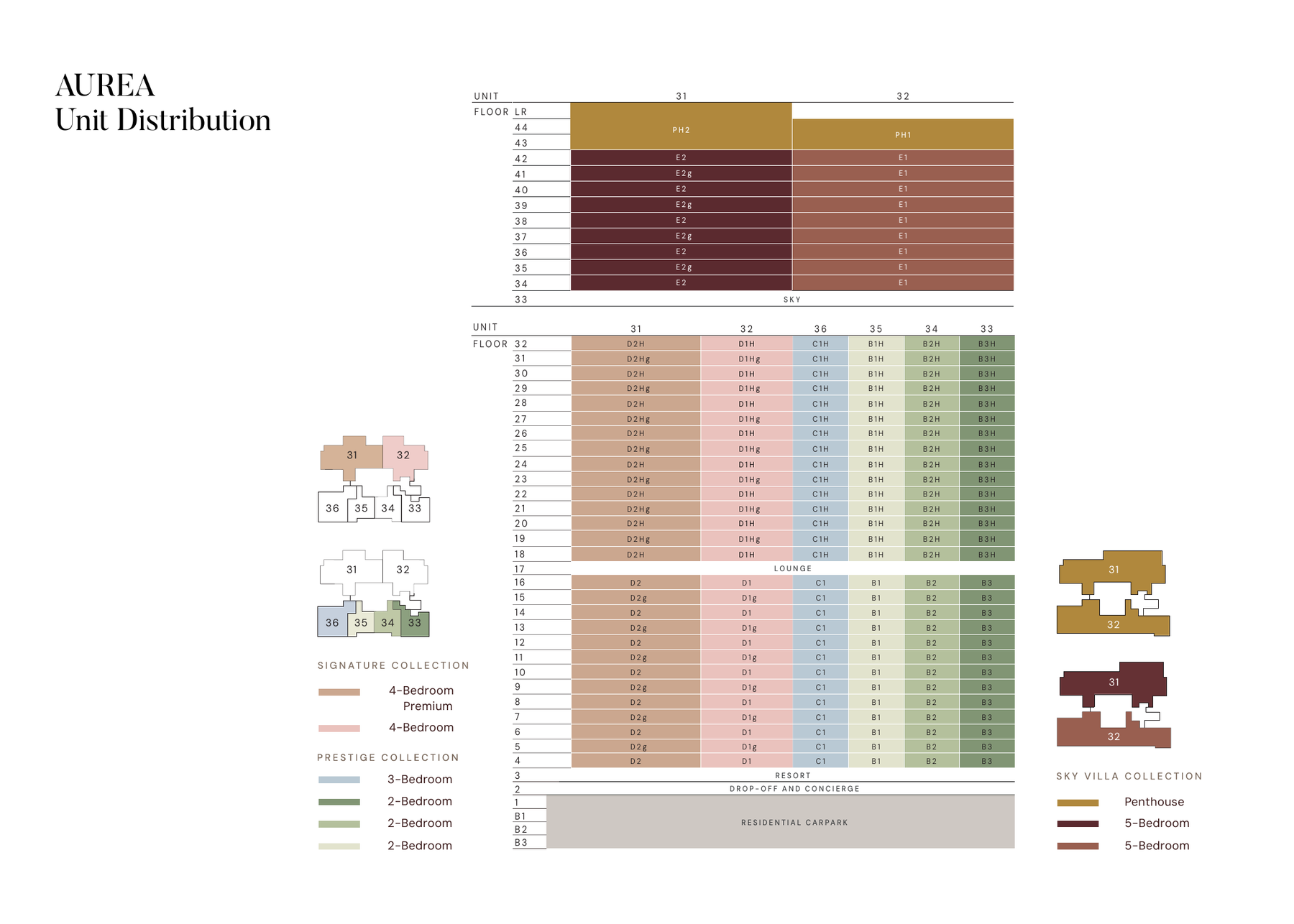

Collections:Prestige Collection (Levels 4–32, 2- to 4-Bedroom, 168 units) · Signature Collection (Levels 34–42, 5-Bedroom Skyliving, 18 units) · Penthouse Collection (Levels 43–45, 2 units). Units with the H suffix sit on Levels 18–32 with higher ceilings.

Indicative Pricing

2-Bedroom from

S$1.76M

3-Bedroom from

S$2.89M

4-Bedroom Signature from

S$4.23M

4-Bedroom Premium from

S$5.48M

5-Bedroom Skyliving from

S$9.20M

Penthouse

POA

PSF benchmark: Prestige Collection mid-S$2,700 to mid-S$2,900 psf; Signature Collection S$3,100–S$3,250 psf at launch. Prices indicative only and subject to developer confirmation at booking — speak to LovelyHomes for the current live price list.

Why Buyers Are Watching

1A national conserved landmark — the only new-build residence physically integrated with Singapore’s first large-scale modernist conservation site. A design story that cannot be replicated elsewhere.

2District 7 address — a freshly-minted prime city-fringe postcode on Beach Road, within walking distance of Kampong Glam, Bugis and the Ophir–Rochor corridor.

3Nicoll Highway MRT at 5 minutes — covered walk to Circle Line, plus Lavender MRT (EWL) at 9 minutes and the entire CBD, Marina Bay and Orchard within a 10-minute commute.

4188 units, one tower — a sky-rise scale that concentrates all amenities, views and light across a single 45-storey form, not multiple low blocks sharing boundary space.

5Three sky-terrace decks — The Sky Club and Sky Gardens at Levels 17 and 33 deliver elevated gym, lounge, dining and wellness above the Central Area skyline.

6Prestige, Signature and Penthouse tiers — from compact 2-Bedroom Prestige homes to 8,816 sqft Penthouses, the unit mix spans one of the widest quantum ranges of any current launch.

7Mixed-use precinct on your doorstep — The Golden Mile retail, offices and medical suites next door, linked by an elevated Public Pedestrian Link on the 2nd storey.

8DP Architects × Studio Lapis — lead architect of Marina Bay Sands and Esplanade, with Singapore’s most active conservation specialist consultancy. A pedigree matched by very few city-fringe launches.

Location and Connectivity

Transport

Nicoll Highway MRT (CC5)

5-minute covered walk. Direct Circle Line to Marina Bay, Bayfront, Dhoby Ghaut and Paya Lebar. Lavender MRT (EWL) is 9 minutes on foot.

Lifestyle

Kampong Glam · Kallang Riverside

Heritage dining and boutiques at Kampong Glam on one side; Kallang Riverside Park, Sports Hub and Marina Reservoir on the other.

Retail

Bugis · Suntec · Marina

Bugis Junction, Raffles City, Suntec City and The Shoppes at Marina Bay Sands all within a 3–6 minute drive.

Work

Bugis · Beach Road · CBD

Bugis/Beach Road business cluster at 2 minutes; Shenton Way, Raffles Place and MBFC at 7 minutes; Orchard Road at 8 minutes.

HWA International School (MSQ) · Invictus International School (Centrium) · EtonHouse International (Orchard)

Primary

Farrer Park Primary · Hong Wen School · St Margaret’s Primary · Kong Hwa School · Anglo-Chinese School (Junior)

Secondary

Outram Secondary · Dunman High School · future Singapore Sports School (Kallang relocation)

Tertiary and Arts

Singapore Management University (SMU) · LASALLE College of the Arts · Nanyang Academy of Fine Arts (NAFA) · School of the Arts (SOTA) · Kaplan City campuses

International Business

Financial / business district — Bugis and Beach Road at 2 minutes’ drive; Shenton Way / Raffles Place / MBFC at 7 minutes

Lifestyle and Amenities

Heritage dining

Kampong Glam’s Arab Street, Haji Lane and Bussorah Street — plus Golden Mile Food Centre at 2 minutes’ walk and North Bridge Road Market at 6 minutes.

Waterfront and parks

Kallang Riverside Park and the Park Connector Network at 3 minutes’ walk. Gardens by the Bay and the Marina Bay waterfront at a short drive.

Icons on your doorstep

Esplanade – Theatres on the Bay, Sands Expo and Convention Centre, Singapore Indoor Stadium and the upcoming Future Indoor Arena — all within 9 minutes’ drive.

Retail belt

Bugis Junction, Raffles City, Suntec City, Marina Square and Shaw Towers — a complete retail and F&B belt within a 3–5 minute drive.

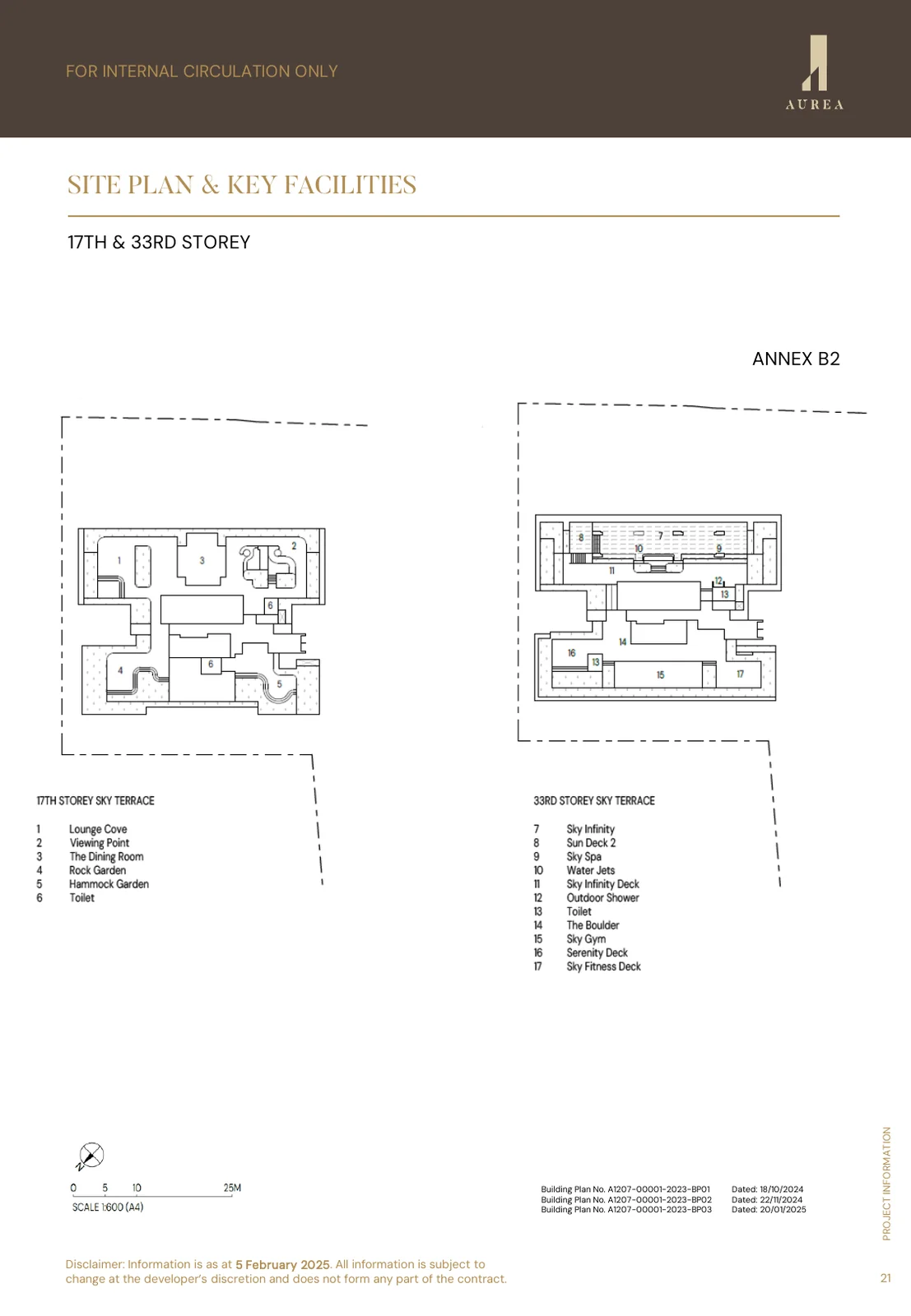

Sky-rise wellness

The Sky Club (Level 17) and Sky Gardens (Level 33) house the gym, yoga pavilion, function rooms and dining pavilions — with panoramic views over Marina Bay and the city.

Medical and education

Raffles Hospital at 2 minutes’ drive and Farrer Park Hospital at 4 minutes. SMU, LASALLE, NAFA and SOTA within the same short-drive radius.

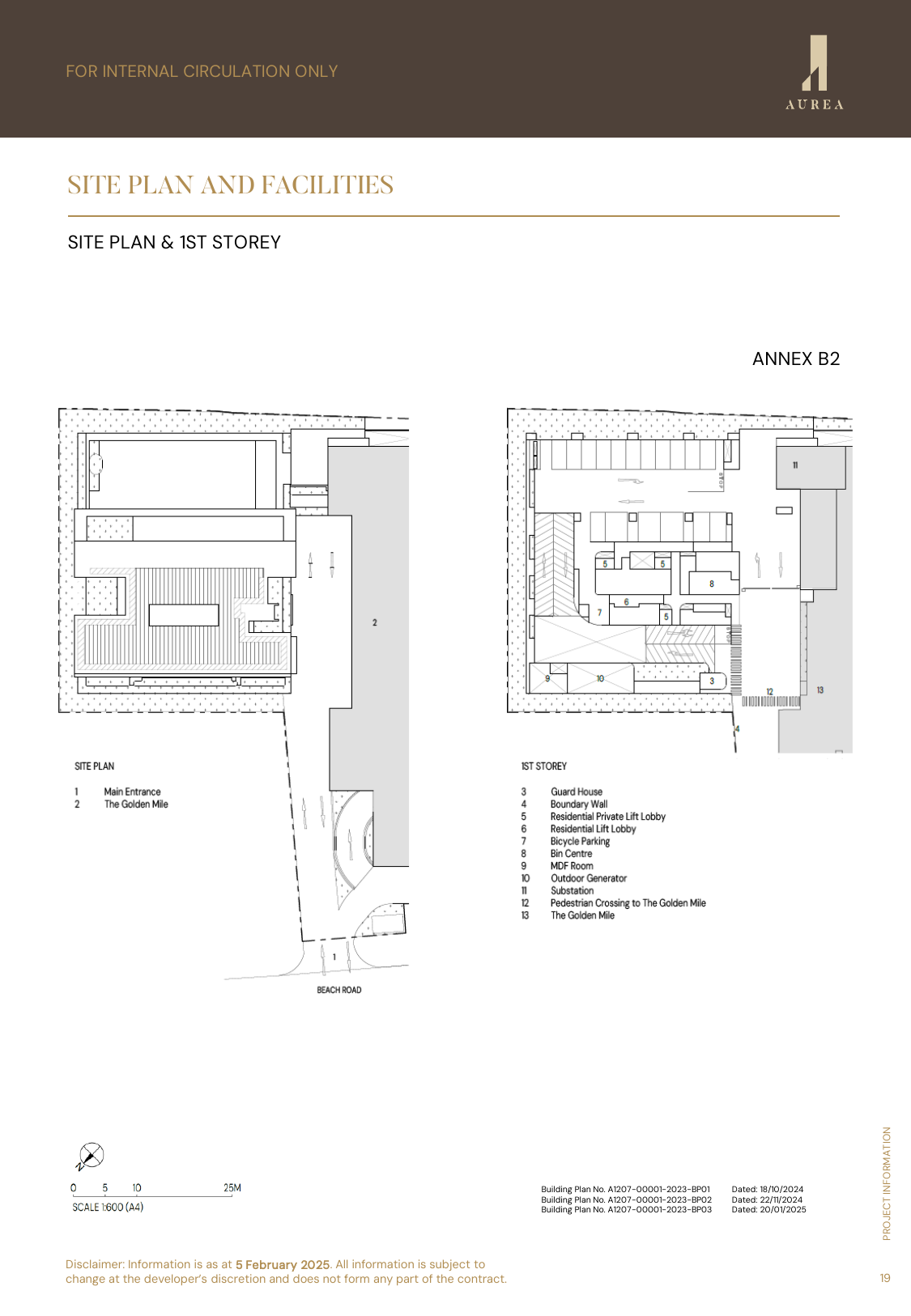

Site Plan

Site plan · 1st storey · indicative only · subject to developer confirmation

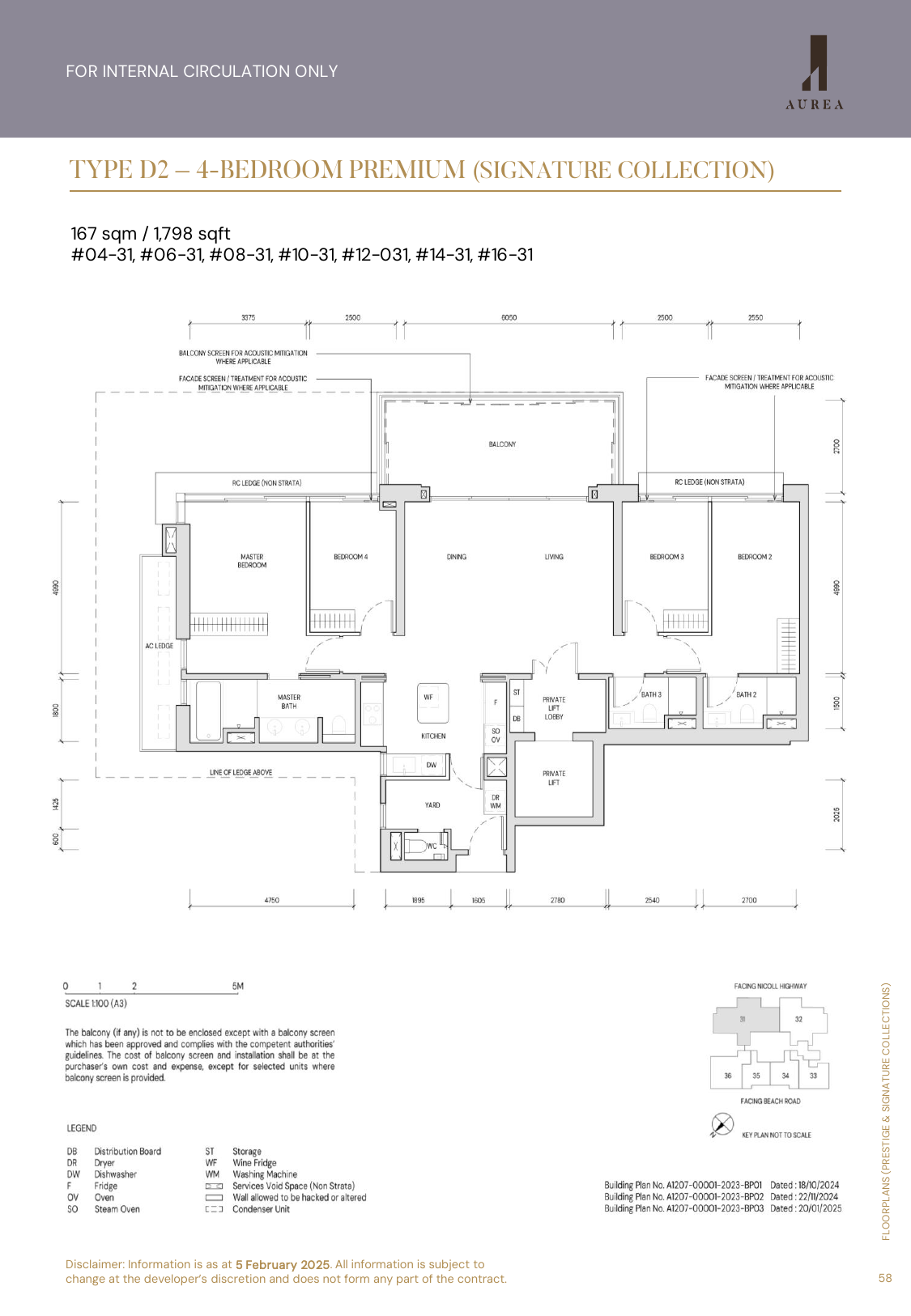

Floor Plans (Selected)

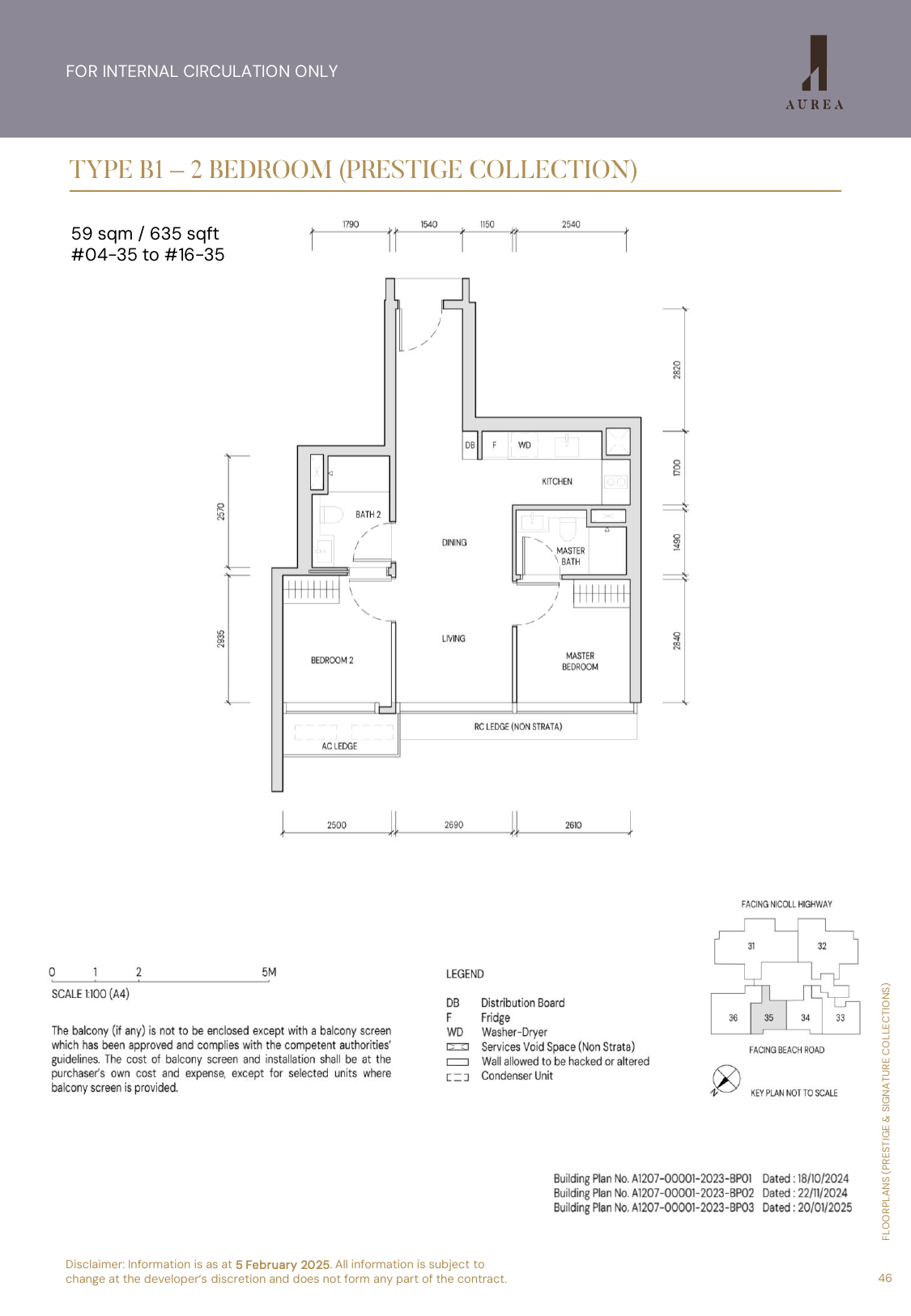

Type B1 · 2-Bedroom · 635 sqft

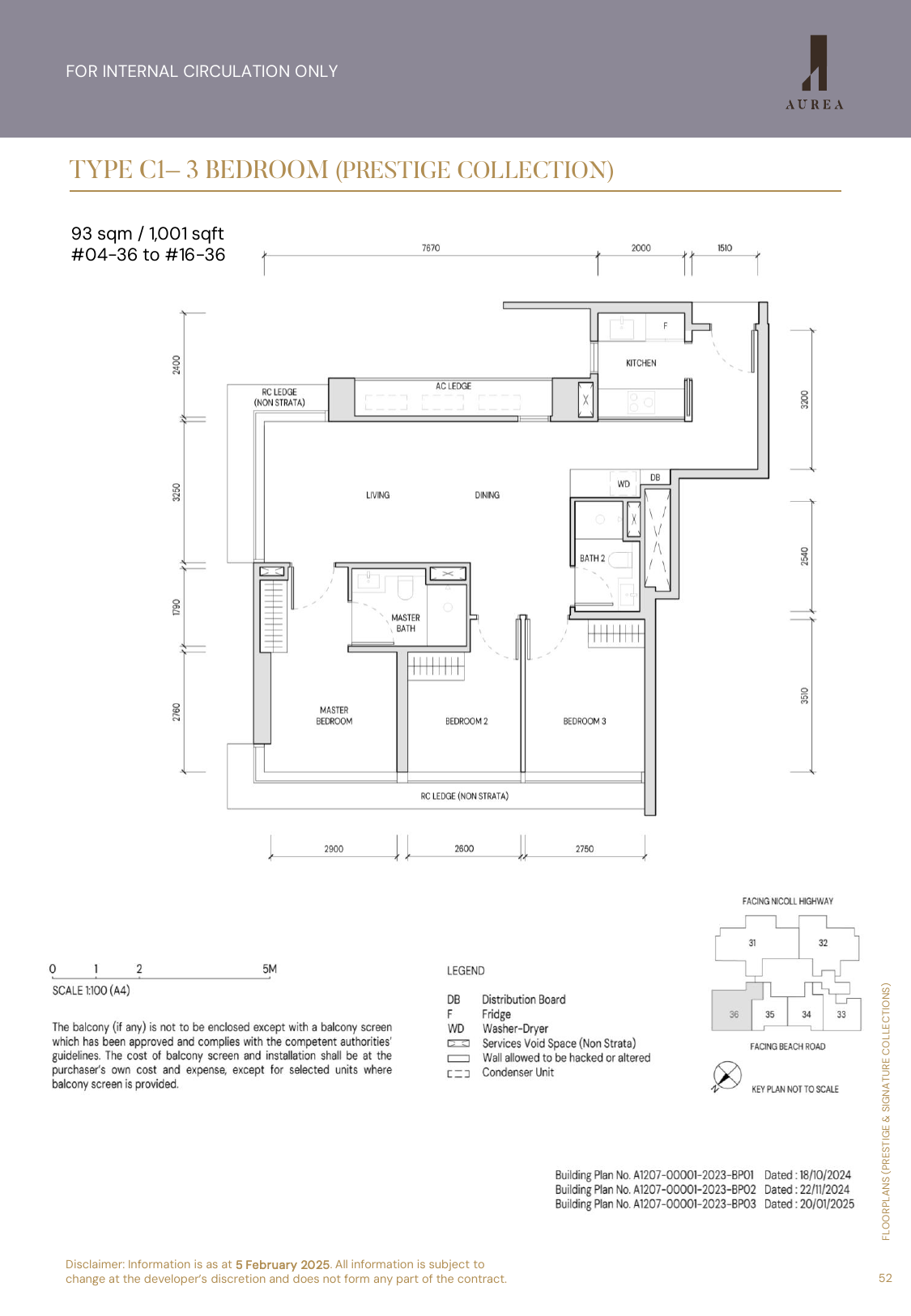

Type C1 · 3-Bedroom · 1,001 sqft

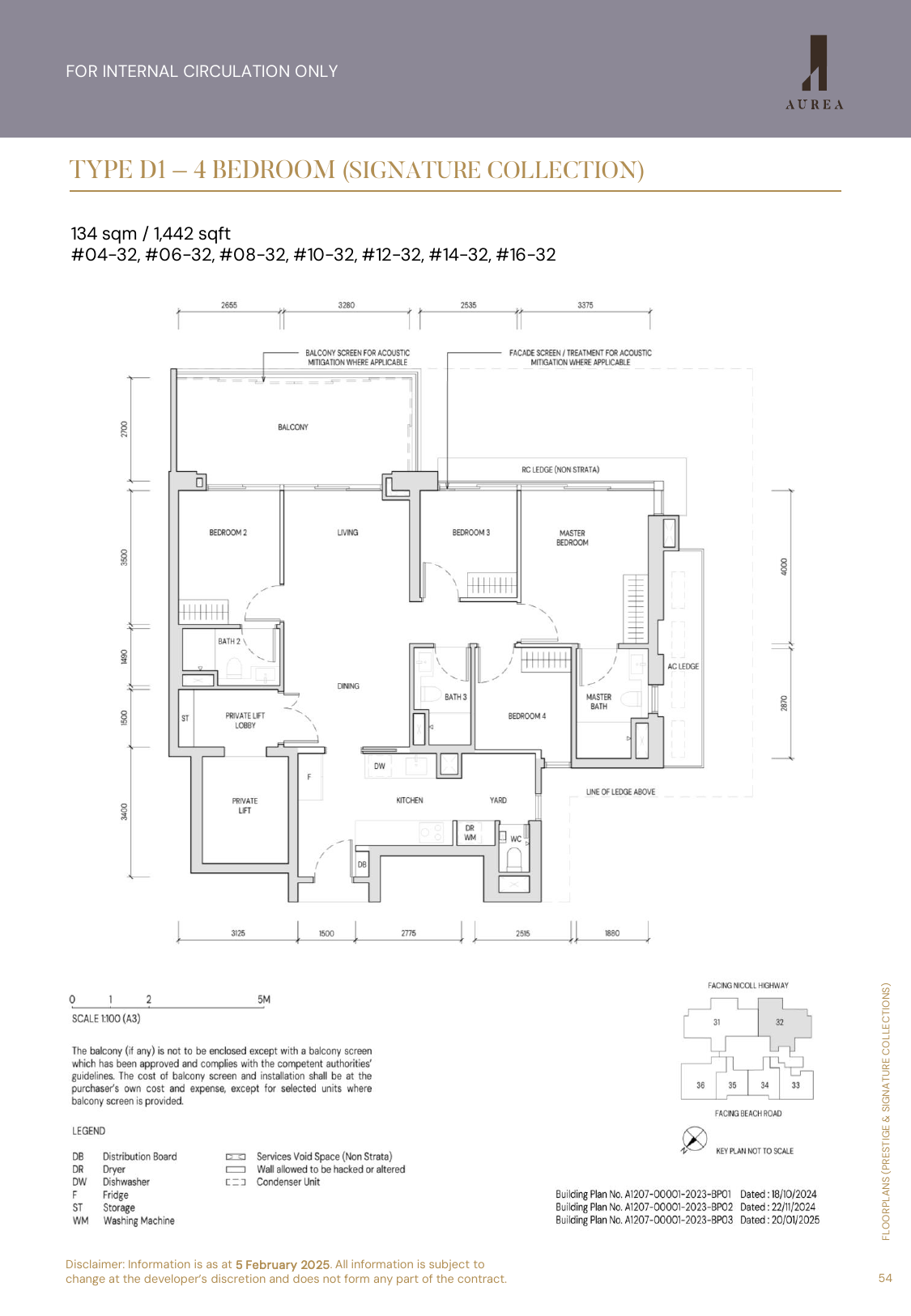

Type D1 · 4-Bedroom Signature · 1,442 sqft

Type D2 · 4-Bedroom Premium Signature · 1,798 sqft

Source note: The available Aurea floor-plan source begins at 2-bedroom Prestige layouts; no 1-bedroom plan is included in the local source set, so selected thumbnails show 2-bedroom, 3-bedroom and 4-bedroom Signature/Premium layouts.

Full Floor Plans PDF

All stack-by-stack floor plans across Prestige, Signature and Penthouse collections.

Arrival ForecourtGrand LobbyGuardhouse50m Lap PoolSpa PoolKid’s PoolPool DeckPoolside PavilionsSky Club (L17)Sky GymSky LoungeSky Function RoomYoga PavilionSteam RoomSky Garden (L33)Dining PavilionBBQ PavilionTea GardenReading CornerFitness CornerChildren’s PlaygroundWellness DeckCommunity LawnElevated Pedestrian Link to The Golden MileEV Charging (4 lots)Bicycle Parking (48 lots)

Gallery

Developer and Consultant Team

GMC Property Pte Ltd — a Perennial Holdings and Far East Organization joint venture

GMC Property Pte Ltd (Developer’s Licence C1497) is the special-purpose vehicle behind Aurea and the wider Golden Mile rejuvenation. It is a joint venture between Perennial Holdings Pte Ltd — one of Asia’s most active mixed-use and healthcare real-estate platforms — and Far East Organization, Singapore’s largest private property developer. The JV acquired the iconic Golden Mile Complex through a collective sale and is leading its conservation-first redevelopment into The Golden Mile with retail, offices, medical suites and Aurea residences.

Architect

DP Architects Pte Ltd

Conservation Specialist

Studio Lapis Conservation Pte Ltd

Landscape Architect

DP Green Pte Ltd

Civil and Structural Engineer

KCL Consultants Pte Ltd

Mechanical and Electrical Engineer

Rankine & Hill (Singapore) Pte Ltd

Quantity Surveyor

Rider Levett Bucknall Consultancy Pte Ltd

Acoustic Consultant

Arup Singapore Pte Ltd

ESD (Sustainability) Consultant

DP Sustainable Design Pte Ltd

Facade Consultant

Building Facade Group

Conveyance Solicitor

Allen & Gledhill LLP

Sustainability and Specifications

Aurea is designed to Singapore’s highest tier of environmental certification and integrates adaptive-reuse of a nationally conserved 1973 modernist landmark — one of the country’s most sustainable design propositions.

BCA Green Mark Platinum targeted — the top tier of Singapore’s residential green-building scheme

Heritage conservation — the 1973 Golden Mile Complex facade, terraced podium and structural language are retained under URA guidance

Low-emissivity glass curtain-wall and window systems for thermal performance

Precast and prefabricated construction with prefabricated bathroom units where applicable — faster, lower waste

EV-ready — 4 EV charging lots for the residential tower

Micro-mobility — 48 bicycle lots and end-of-trip provisions to support a car-lite city-fringe lifestyle

Acoustic and facade engineering — Arup and Building Facade Group engaged to manage noise ingress from Beach Road and Nicoll Highway

Project Timeline

18 Nov 2024

99-year lease commencement

Feb 2025

Sales launch

2026 – 2028

Ongoing sales phases

Q2 2029

Expected TOP

31 Mar 2030

Expected vacant possession

Project Factsheet

A shareable 2-page PDF snapshot of everything on this page — bring it to viewings, forward it to family.

Aurea is located at 802 Beach Road in Singapore’s prime District 7, sitting atop the conserved Golden Mile Complex. It is a 5-minute covered walk to Nicoll Highway MRT (CC5, Circle Line) and 9 minutes to Lavender MRT (EWL), with Marina Bay, Orchard and the CBD all within a 10-minute ride.

Who is the developer?

The developer is GMC Property Pte Ltd — a joint venture between Perennial Holdings and Far East Organization. Perennial is one of Asia’s most active mixed-use and healthcare real-estate platforms, and Far East Organization is Singapore’s largest private property developer. Developer’s Licence No. C1497.

When is Aurea expected to be completed?

The expected Temporary Occupation Permit (TOP) date is Q2 2029 for the residential tower. Expected vacant possession is 31 March 2030, and expected legal completion is 31 March 2033. The 99-year leasehold commenced on 18 November 2024, so buyers get a near-full fresh lease at completion.

What unit types are available?

Aurea offers 188 residential units across three collections: Prestige Collection (Levels 4–32) with 2-Bedroom (635–710 sqft), 3-Bedroom (1,001 sqft), 4-Bedroom Signature (1,442 sqft) and 4-Bedroom Premium Signature (1,798 sqft); Signature Collection (Levels 34–42) with 5-Bedroom Skyliving (2,863 or 3,251 sqft); and the Penthouse Collection (Levels 43–45) with two penthouses at 5,608 and 8,816 sqft.

What are indicative prices at Aurea?

Indicative starting prices at launch were from S$1.76M for a 2-Bedroom, S$2.89M for a 3-Bedroom, S$4.23M for a 4-Bedroom Signature, S$5.48M for a 4-Bedroom Premium Signature and S$9.20M for a 5-Bedroom Skyliving. PSF benchmarks range from the mid-S$2,700s for the Prestige Collection to S$3,100–S$3,250 psf for the Signature Collection. Penthouses are price-on-application. All figures are indicative and subject to developer confirmation at booking.

How close is Nicoll Highway MRT?

Nicoll Highway MRT (CC5, Circle Line) is approximately 0.4 km away — a 5-minute covered walk from the residential tower via an elevated Public Pedestrian Link at the 2nd storey that connects Aurea to The Golden Mile. Lavender MRT (EWL) is approximately 0.8 km (a 9-minute walk).

Is Aurea freehold or leasehold?

Aurea is a 99-year leasehold development. The lease commenced on 18 November 2024, so a buyer in 2026 effectively takes on a fresh near-full lease.

What is the link-bridge to Golden Mile Complex?

An elevated Public Pedestrian Link (EPL) at the 2nd storey connects Aurea to The Golden Mile. The EPL is required by the authorities to remain publicly accessible 24 hours a day and gives residents direct sheltered access to the retail, office and medical suites in the conserved podium.

What makes Aurea different from other city-fringe launches?

Aurea combines four rarely co-located advantages: a District 7 Beach Road address, physical integration with Singapore’s first large-scale modernist conservation site, a 5-minute covered walk to Nicoll Highway MRT, and a single 45-storey tower concentrating amenities and sky-terraces. It also targets BCA Green Mark Platinum — the top tier of Singapore’s residential green-building scheme.

Where is the sales gallery?

The developer’s sales gallery is at 10A Central Lane 1, Singapore 019927. To arrange a private viewing, receive the full developer e-brochure, or request the latest live price list, message LovelyHomes on WhatsApp at +65 8222 2556.

Ready to see Aurea at Golden Mile in person?

Speak to our LovelyHomes concierge on WhatsApp for the latest unit availability, e-brochures and showflat bookings. We’ll connect you with the developer’s in-house team, not an agency.

Every major round of Singapore property cooling measures and what they did to prices.

Disclaimer. Prices, unit mix, specifications, site plans, floor plans and facility lists on this page are indicative only and subject to change by the developer without notice. All information has been compiled from developer sales material (brochures, project factsheet dated 5 February 2025 and sales kits) and verified as at 19 April 2026. LovelyHomes.com.sg is not the project developer. Prospective buyers should consult an accredited salesperson and the developer’s official sales kit before committing to any purchase. Artist impressions are for illustrative purposes only and may differ from the final built product.

Figure 1: The three tenure classes in Singapore real estate — with freehold at ~4% of the housing stock, 999-year a rare pre-1960s relic, and 99-year the dominant form.

Every Singapore property conversation eventually turns to tenure. Is the extra 10–15% for a freehold condo actually worth it? Will a 99-year leasehold unit hold its value if I plan to hold for 20 years? Do banks and CPF really pull the plug on an ageing lease? These are not academic questions. The tenure decision shapes your long-run return more than almost any other call you make at the point of purchase, and the rules that govern it — CPF usage, bank LTV caps, HDB loan eligibility, lease-top-up policy — change in sharp steps rather than smoothly.

This is the 2026 edition of our tenure guide. It walks through the legal substance of freehold, 999-year and 99-year titles; the SLA “Bala’s Table” that dictates how lease-decay is valued; the financing cliffs at 95, 60 and 30 years remaining; and a Singapore-specific worked example that puts a dollar figure on the freehold premium. We close with a forward view on what the SERS / VERS pipeline means for older leaseholds.

Quick Answer: The 10 Things Every Tenure-Sensitive Buyer Should Know

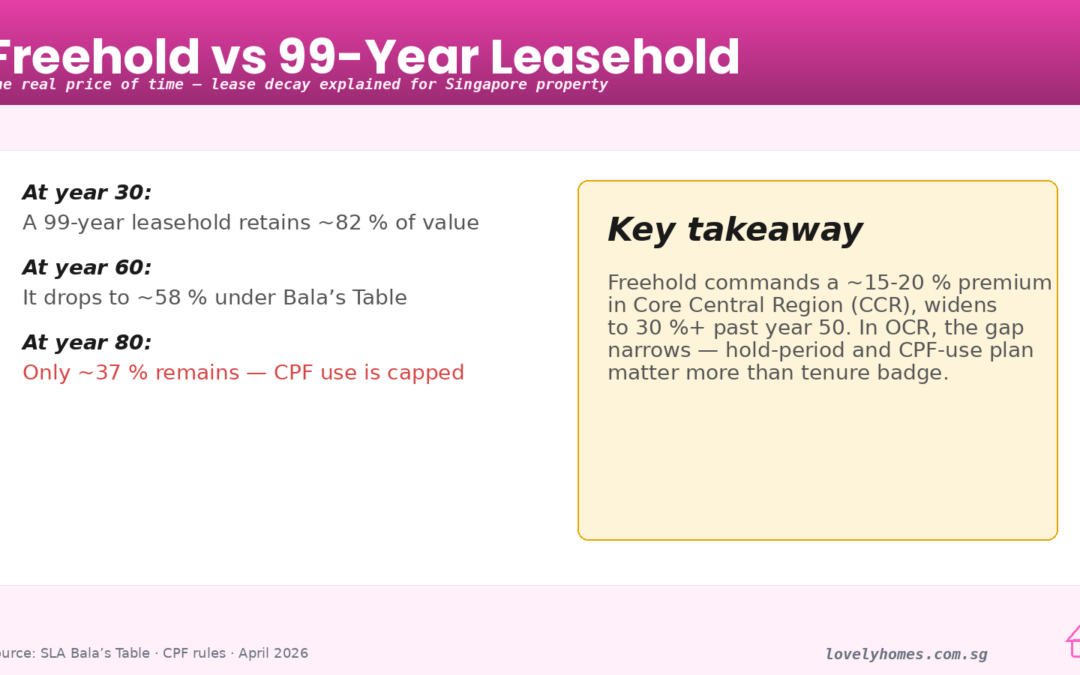

Freehold ≈ ~4% of SG residential stock. The vast majority of private homes and all HDB flats are 99-year leasehold. 999-year titles are a rare pre-1960 relic but, in valuation terms, behave like freehold.

The freehold premium is ~10–15%. In comparable micro-markets, a fresh-lease 99-year condo typically trades at 85–90% of the freehold equivalent — a narrower gap than many buyers expect.

Bala’s Table is the ruler. SLA’s published valuation table is the single authoritative source for how a leasehold interest is valued at any years-remaining. It is a non-linear curve, steepening materially below 60 years.

60 years is the financing cliff. CPF usage and bank LTVs compress sharply once a lease drops below 60 years remaining.

30 years is the exit wall. Below 30 years remaining, almost no bank will finance the unit and CPF usage is effectively nil — the buyer pool collapses to cash-rich owner-occupiers.

SERS is discretionary, not guaranteed. HDB’s Selective En bloc Redevelopment Scheme is offered to a very small minority of ageing flats; the 99 years ends and the land reverts regardless.

VERS is the policy hedge. The Voluntary Early Redevelopment Scheme (legislated 2018, rolling out for the oldest HDB towns in the late 2020s) gives residents a vote on early redevelopment in exchange for a lower pay-out than SERS.

Lease top-ups exist for private land. URA allows lease extensions via upgrading premium payments for selected private freehold/leasehold sites — used routinely by en-bloc developers.

HDB’s 99-year clock starts at award. A BTO completed in 2018 will, in 2117, revert to the state regardless of whether the flat has been sub-sold or renovated.

Tenure affects renter demand less than you’d think. Rental yields on comparable freehold and 99-year properties tend to be within 10–20 basis points of each other; the rental market is insensitive to tenure in a way the sales market is not.

What Tenure Actually Means in Singapore Law

Under the Land Titles Act, freehold in Singapore is what the Common Law calls an “estate in fee simple” — the fullest form of private ownership available, running in perpetuity and capable of being transmitted by will or gift without reverting to the state. 999-year leasehold is functionally indistinguishable from freehold during the lifetime of anyone reading this article; valuers treat it at par with freehold for discounting purposes, and both CPF and bank lenders do the same. Its rarity reflects early colonial-era land grants, most of them pre-1960.

99-year leasehold is the modern default. The State (via the Singapore Land Authority, SLA) retains reversionary title; the leasehold owner holds what is technically a “term of years absolute”. When the lease expires, title reverts without compensation unless the land is re-granted. This is the deal that underpins every HDB flat, every Executive Condominium (from its initial sale onwards), and the majority of private condos and landed properties released from the Government Land Sales (GLS) programme since the 1970s.

How Lease Decay Is Valued: Bala’s Table

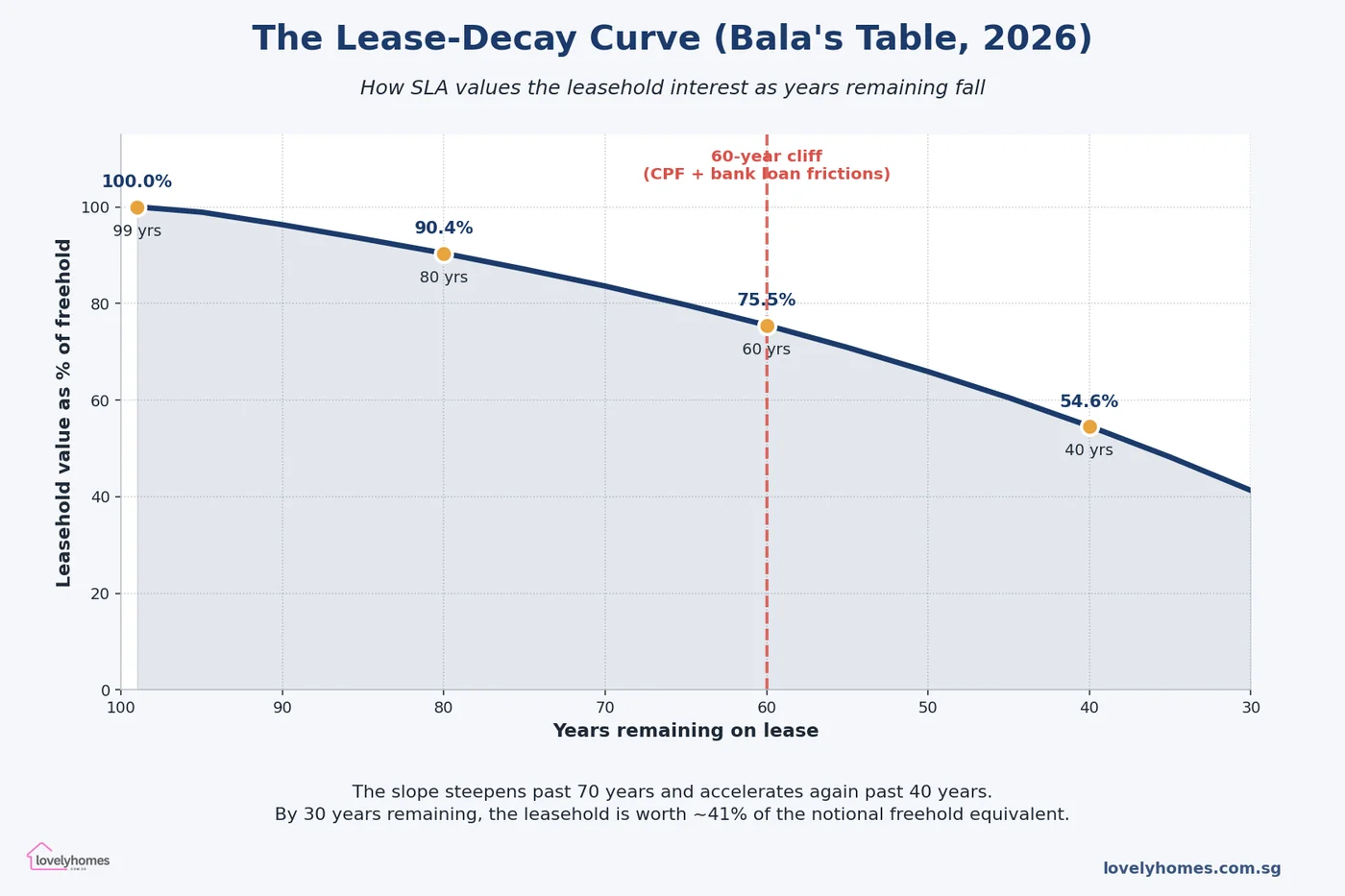

Figure 2: The Bala’s Table lease-decay curve as maintained by SLA. A 99-year leasehold retains 90% of its freehold-equivalent value at 80 years remaining, but only 75% at 60 years and 55% at 40 years.

Every Singapore valuer — including IRAS, SLA, CPF, banks and private surveyors — uses the SLA’s “Bala’s Table” as the reference for lease-hold-to-freehold value conversion. The table was named after Mr. Bala Subramaniam, then Chief Valuer, who introduced it in the early 1980s. It expresses the leasehold interest as a percentage of the equivalent freehold value at each remaining-years figure from 99 down to zero. The curve is not linear — depreciation accelerates as years remaining shrinks.

Key reference points from the 2026 version of the table:

99 years remaining: 100.0% of freehold

80 years remaining: ~90.4%

70 years remaining: ~83.6%

60 years remaining: ~75.5%

50 years remaining: ~65.9%

40 years remaining: ~54.6%

30 years remaining: ~41.3%

20 years remaining: ~26.6%

Two practical implications flow from this curve. First, the “depreciation drag” on a 99-year lease over the first 20 years is only about 10 percentage points — which in a market where underlying land values are rising 2–3% annually is easy to out-run. Second, the drag compounds rapidly past the 40-year mark, and by the time a lease is under 30 years remaining the leasehold interest is a fraction of the notional freehold and financing options have all but disappeared.

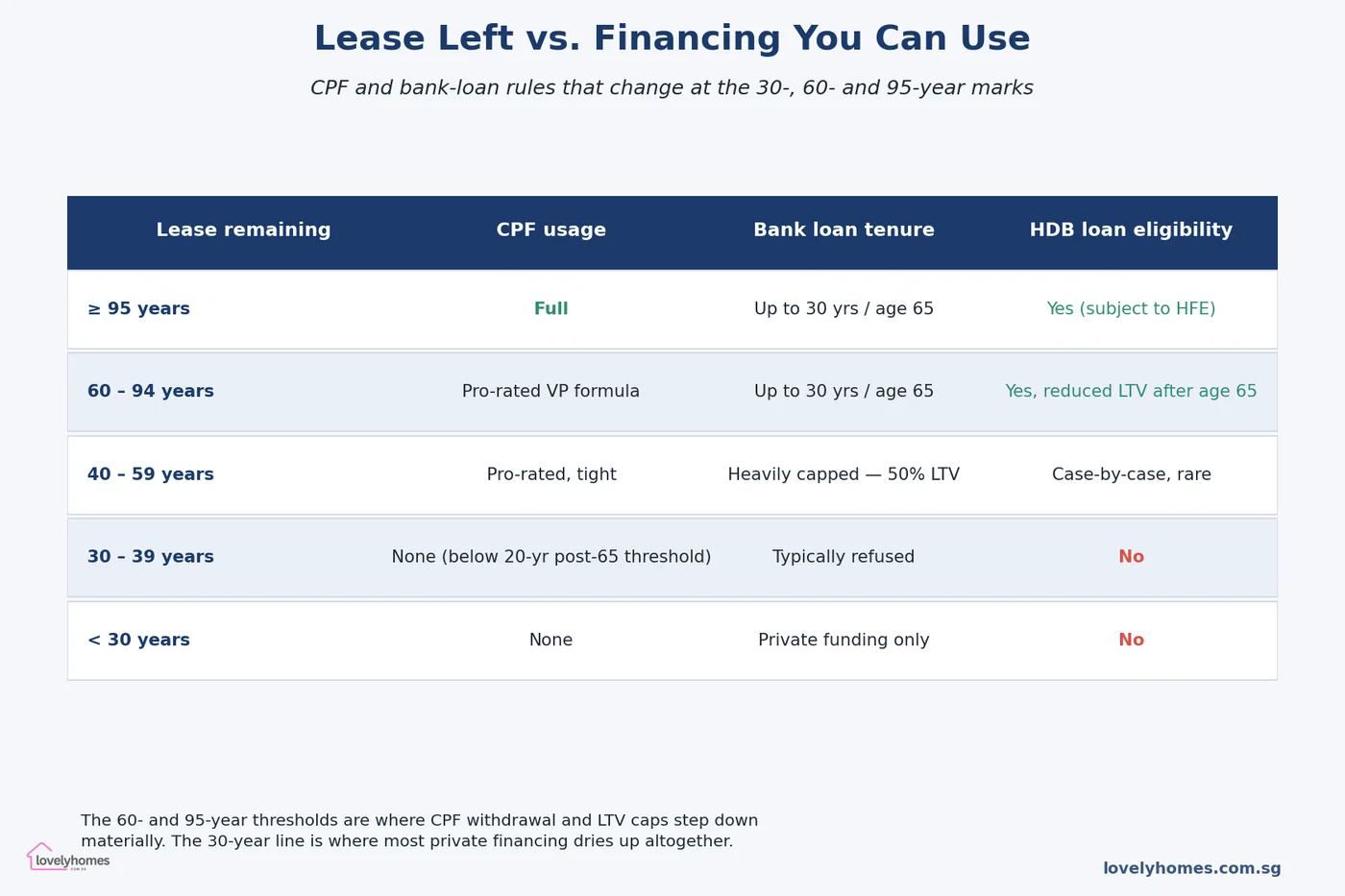

The Financing Cliffs: 95, 60 and 30 Years

Figure 3: The step changes in CPF usage, bank-loan tenure and HDB-loan eligibility as the years remaining on the lease decline.

Financing rules, not sentiment, drive most of the tenure-based price gap. CPF and bank underwriting both step down abruptly rather than smoothly. The three thresholds every buyer should know:

95 years remaining and above — Full CPF Ordinary Account usage, bank loan tenure up to 30 years or age 65, HDB loan eligible (subject to HDB Flat Eligibility letter). This is the baseline scenario for any brand-new launch.

60 years remaining — The first major cliff. CPF switches to a pro-rated Valuation Limit formula (the property must last the buyer until at least age 95, otherwise CPF usage is capped proportionally). Banks remain willing to lend but the 75% LTV may compress to 55% if the tenure extends past age 65. HDB loans remain available but with reduced LTV for older buyers.

30 years remaining — The exit wall. Most banks will decline to finance the purchase; those that do offer sub-50% LTV at punitive rates. CPF usage is effectively nil. HDB loans are not available. The market for the unit shrinks to cash-rich, typically older, buyers who are treating the purchase as a lifestyle-until-death asset.

The non-linearity is what makes tenure so consequential. A leasehold condo at 65 years remaining looks like a bargain on a pure price-per-square-foot basis — until the buyer realises they have a 5-year runway before the 60-year CPF cliff begins biting, which compresses the future pool of buyers who can take the unit off their hands.

A Fully-Worked Example: Freehold vs 99-Year in District 15

Consider two comparable 3-bedroom condo units in the Marine Parade area, both completed in 2026:

Unit A (99-year leasehold): S$2.3 million purchase price. 99 years at award — so the buyer gets 99 years of tenure starting from 2024 (when the plot was awarded).

Unit B (freehold): S$2.65 million purchase price. 15% premium to Unit A.

Assume both appreciate at 3% per annum nominal (a rough median for the Marine Parade submarket over a 20-year horizon). What does the tenure decision look like at the 20-year mark (2046)?

Unit A (now 79 years remaining): On Bala’s curve at 79 years, the leasehold interest is worth ~90% of the notional freehold equivalent. If the freehold equivalent has compounded at 3% for 20 years, it would be worth S$2.3m × 1.03^20 = S$4.15 million. The leasehold interest is then 90% of that “freehold equivalent” — but wait: the Bala curve already expresses value relative to freehold. So the 99-year unit in 2046 is worth roughly S$2.3m × 1.03^20 × (90%/100%) = S$3.74 million. Gain: ~63% over 20 years.

Unit B (still freehold): S$2.65m × 1.03^20 = S$4.79 million. Gain: ~81% over 20 years.

At the 20-year mark, the freehold unit has outperformed by about S$1.05 million in absolute terms and 18 percentage points in percentage gain. Adjust for the S$350,000 premium paid upfront (which could alternatively have earned ~4% in risk-free assets: S$350k × 1.04^20 = S$767k of opportunity cost), and the net advantage of the freehold is closer to S$300,000–S$400,000 over the period.

Is that worth it? For a buyer with a 20-year hold and no liquidity pressure, plausibly yes. For a buyer whose realistic hold is 8–10 years, the freehold premium may not recoup — the decay drag on a fresh 99-year lease is small over that horizon and the opportunity cost on the premium is live. This is the central trade-off: tenure mattered most for very long holds, very aged leases, or illiquid micro-markets.

SERS, VERS and the End-of-Lease Question

The elephant in the room for ageing 99-year stock is what happens at expiry. Three scenarios exist:

Lease runs its full 99 years and reverts. This is the default. The land returns to the state and the leasehold owner receives no compensation. For HDB flats the owner-occupier gets to live there until expiry (subject to upkeep and lease conditions). For private condos the same applies but the economic value in the final years approaches zero.

SERS (Selective En bloc Redevelopment Scheme). HDB identifies a small number of ageing blocks with high redevelopment potential and offers residents a replacement flat plus ex gratia compensation. Fewer than 5% of HDB blocks have been selected for SERS since the programme began in 1995. The policy framing is deliberately narrow — SERS is a planning tool, not a tenure safety net.

VERS (Voluntary Early Redevelopment Scheme). Legislated in 2018 and first offered to flats around the 70-year-remaining mark in the late 2020s, VERS is an opt-in mechanism: residents of an eligible precinct vote on whether to accept a negotiated pay-out in exchange for early redevelopment. Payouts are explicitly flagged as lower than SERS compensation. Our full VERS guide walks through the mechanics.

For private leaseholds, the equivalent mechanism is the en bloc (collective) sale, where 80% of owners by value (90% if the development is less than 10 years old) can force a sale to a developer who pays SLA a topping-up premium to reset the 99-year clock. The economics of en bloc sales change materially once a development crosses 60 years remaining — the topping-up premium escalates and developer IRRs tighten.

What Might Come Next — Policy Signals to Watch

Three forward-looking data points to monitor over 2026–2028:

The first VERS offers. The first precincts eligible for VERS are the 1970s HDB estates in Tiong Bahru, Queenstown and Marine Parade, now crossing the 55-year-remaining mark. The terms of the first offer (how much is paid, how much choice the resident has in replacement housing) will set the template for the next two decades. HDB has signalled a 2027–2028 rollout window.

Bala’s Table updates. SLA reviews the table periodically. The last meaningful revision was in 2019, when decay rates were nudged upward to reflect data from transactions in older leases. Another revision would have knock-on effects on CPF and bank LTV decisions.

Lease top-up policy for older private estates. A handful of pre-1970s private freehold estates have approached URA for lease-top-up schemes to extend or recalibrate tenure. If a standardised top-up mechanism emerges, the value of ageing 99-year private leaseholds could rise materially.

How Singapore’s Tenure System Compares Globally

Singapore is not alone in using long leaseholds for residential land. Hong Kong’s typical residential lease is also 99 years, with far more aggressive lease-modification and top-up activity (land premiums are a major source of government revenue). London uses a mix of long leaseholds (typically 99 or 125 years) on ex-local-authority and conversion flats, and reformed the Leasehold Reform, Housing and Urban Development Act in 2002 to allow leaseholders to compel freehold purchase (a process called “enfranchisement”) under specific conditions. Vancouver has true freehold in most of the metro area but faces its own lease-renewal issues with First Nations reserve land.

The distinctive feature of Singapore’s framework is the tightness of its financing-tenure coupling: HDB and CPF rules shape the buyer pool in a way that is more formulaic than in most peer jurisdictions. That makes Singapore’s Bala-Table decay an underwriting reality, not just a valuation convention — which is why it moves prices in step-changes around the 60- and 30-year thresholds.

Frequently Asked Questions

1. Is paying a 15% premium for a freehold condo ever worth it?

It depends almost entirely on your holding period and the opportunity cost of the premium. For a 25+ year hold in a supply-constrained micro-market, the math usually favours freehold — the Bala decay on the 99-year unit starts to bite after year 20, the buyer pool for the freehold unit remains wider, and the reinvested-premium scenario struggles to keep pace with property inflation. For a 5–10 year hold, the 99-year unit will typically outperform net of the premium: the Bala decay over that window is less than the opportunity cost of parking an extra S$300,000–S$500,000 in a lower-yielding asset.

2. Can I get a bank loan for a flat with less than 30 years remaining?

In practice, very rarely. Two or three private banks specialising in high-net-worth lending will consider it on bespoke terms — typically capped at 50% LTV, premium rates, short tenure and often secured against other assets. For standard retail buyers, the answer is effectively no. This is why the 30-year mark is called the exit wall: the market shrinks to a niche of cash-rich buyers and the price discount can be severe. The same logic drives why a 99-year unit sold at year 65 clocks a bigger-than-Bala discount — the market is already pricing in the financing thinning that bites at 60.

3. Does CPF allow me to buy an ageing leasehold flat?

Yes, but pro-rated. The CPF Board’s rule of thumb is that the property must be able to last the owner until at least age 95. If the remaining lease does not cover that, CPF usage is capped proportionally via the Valuation Limit/Withdrawal Limit formula. A 40-year-old buyer looking at a 65-year lease on a flat can usually still use full CPF. The same buyer at 55 looking at a 50-year lease will face a material haircut. Always run the CPF calculator before committing.

4. Are all HDB flats 99-year leasehold?

Yes. Every HDB flat — BTO, resale, SBF, DBSS — is 99-year leasehold from the date the block was first awarded (or in some older blocks, re-dated for the current lease commencement). The 99-year clock is set in stone; HDB does not sell freehold, and there is no mechanism to convert an HDB flat to freehold. The compensation schemes (SERS, VERS) are the only policy routes around the expiry, and they are discretionary.

5. How does tenure affect rental yields?

Less than most people expect. Rental markets price comparable units on amenity, location and unit quality; tenure is a distant factor because tenants are paying for the right to occupy, not to own. Comparable freehold and 99-year condos in the same submarket typically show rental yields within 10–20 basis points of each other. The yield difference is usually in favour of the leasehold (because the leasehold trades at a lower capital value), but the gap is small enough that investors optimising for yield rarely pick tenure as the decision variable.

6. What is the difference between lease commencement date and Temporary Occupation Permit (TOP) date?

The lease commencement date is the date on which the 99-year clock begins — typically when the land was awarded to the developer via the GLS programme. The TOP date is when the building is ready for occupation, usually 3–5 years after lease commencement for a condo and 6–8 years for an HDB BTO. The lease clock does not reset at TOP; a buyer moving into a newly-completed 2026 condo may already have only 95 years remaining on the lease because the plot was awarded in 2022. Always check the lease commencement date in the Sale & Purchase Agreement, not just the TOP.

7. Can a 99-year lease be extended?

For private residential land, yes — via the URA’s lease top-up scheme, which en bloc developers use routinely. The developer pays a topping-up premium to SLA and the lease resets to 99 years. Individual flat owners cannot unilaterally request a top-up; it must be done at the collective/development level. For HDB flats there is no top-up mechanism available to flat owners; the 99 years runs to expiry with only the SERS/VERS escape hatches as exceptions.

This article is an editorial guide for general information only and does not constitute legal, financial or valuation advice. The Bala’s Table figures and policy references used are illustrative and reflect the position as published by the Singapore Land Authority (SLA) and the Housing & Development Board (HDB) at the time of writing (April 2026); figures are periodically revised. For authoritative guidance consult the Singapore Land Authority, the HDB, the URA, a licensed property valuer and a qualified conveyancing lawyer before any property decision. Worked-example numbers are illustrative; actual outcomes depend on market conditions, the specific property, and financing available at the time of purchase.

Property agent commission in Singapore is never a published rate — it is negotiated on a case-by-case basis, constrained by market convention and the Council for Estate Agencies (CEA) framework. This 2026 guide walks through what is conventional, what is negotiable, who actually pays, and how to choose an agent worth the fee.

For the regulator’s side, the CEA website is authoritative on registration, disciplinary actions, and agent obligations.

Quick Answer — Typical 2026 Rates

HDB resale — sale: 2% (seller pays).

HDB resale — buy: 1% (buyer pays, optional).

Private condo — sale: 1–2% (seller pays).

Private condo — buy (resale): 0–1%; commonly covered by the seller via co-broke.

New launch condo: ~1% paid by the developer to the agent (buyer pays nothing).

Rental (1-year lease): 0.5–1 month’s rent, typically paid by landlord; split by custom.

Typical 2026 commission rates across HDB resale, private condo, new launch and rental transactions.

The CEA Framework

Every practising property agent in Singapore must be registered with the Council for Estate Agencies (CEA) and affiliated with a licensed estate agency. Key CEA rules:

Registration: Agents have a 6-digit CEA registration number. Check it on the public register before engaging.

One-party rule: The same agent cannot represent both buyer and seller in the same transaction. An agency can have different agents for each side, but not the same person.

Estate Agency Agreement (EAA): Every formal engagement must be documented in an EAA specifying the service scope, exclusivity, and commission structure.

Continuing education: CEA mandates continuing education each year, which is why you should check registration is current.

HDB Resale Commissions

Seller-side commission

The standard HDB resale seller-side commission in Singapore is 2% of the transacted price. On a S$600,000 flat, that is S$12,000 + GST, payable at completion.

For this fee, a competent agent typically delivers:

Coordination with the buyer’s agent, lawyers, and HDB

Buyer-side commission

HDB buyer-side commission is 1% of the transacted price, where paid. Many buyers use the HDB Resale Portal directly without an agent, in which case no commission applies. Where an agent is used on the buyer side, 1% is the market norm.

Private Condominium Commissions

Seller-side

Private condo sellers pay between 1% and 2% of transacted price, with 2% being common and 1.5% negotiable for larger sale values. The higher fee reflects stronger marketing requirements (larger buyer pool, more luxury property presentation).

Buyer-side (resale)

Buyers rarely pay a separate commission in private resale transactions. The seller’s 2% agent typically co-brokes with the buyer’s agent, splitting the seller’s 2% (typically 1%–1% but sometimes 1.2%–0.8% if the listing agent did most of the marketing work). The buyer pays nothing additional.

New launch

In a new launch condo, the developer pays the agent’s commission. Conventional market rates are 1% from the developer, though some luxury launches pay more to attract top agents. The buyer pays nothing for agent services.

Rental Commissions

The norm for residential rentals is a full month’s rent commission on a 2-year lease, split by custom:

2-year lease (standard): 1 month’s rent, paid by landlord.

1-year lease: 0.5 month’s rent, typically paid by landlord.

Expat rental ≥ S$5,000/month: landlord typically pays, as the rental amount justifies it.

Rental below S$3,500/month: the tenant’s agent may ask the tenant to pay the commission directly.

What Is Negotiable?

Commission rates are not fixed by CEA or by any regulation. They are market conventions, and everything is negotiable:

When you have leverage

Large transaction value. 1.5% on a S$3m condo (S$45,000) can be discussed.

Multiple properties under one engagement. Selling two units with one agent can justify a reduced rate on each.

Repeat business. An agent who has represented you before should reflect that.

Short timeline with minimal marketing. If the agent is simply facilitating a deal you already have, a flat fee rather than percentage commission is reasonable.

When you have less leverage

Short-dated MOP-edge flats. These require more marketing effort to attract rare eligible buyers.

Ethnic-quota-closed blocks. Narrowed buyer pool means harder selling.

Luxury condos in quiet markets. Agents may push for higher rates to justify the effort.

How to Choose a Good Agent

Commission rate is only part of the calculus. A 2% agent who sells at 2% above valuation out-performs a 1.5% agent who sells at 5% below. What actually matters:

1. Track record in your estate or property type

Ask for the agent’s recent transacted listings in the same estate and flat type. Most agents have a concentrated specialty — lean into that.

2. Responsiveness

Do they return calls and messages within 2 hours during working hours? If not, imagine trying to coordinate viewings with them.

3. Marketing approach

What listings will they use? Will they pay for PropertyGuru premium placement, professional photography, Facebook/IG ads? For sale-side, marketing budget matters.

4. Negotiation style

A good agent negotiates hard for your side, not for a quick commission. Ask how they handle price objections.

5. CEA registration and standing

Verify the CEA number is current. Check the public register for any disciplinary actions or complaints.

Estate Agency Agreement Essentials

Every engagement needs a written EAA. Key clauses to review:

Exclusivity: Sole agency (exclusive) vs non-exclusive. Sole agency typically gets more effort but you cannot switch easily during the term.

Term: 3 months is common, 6 months for private condo. Always specify an end date.

Commission rate: State the percentage and the basis (transacted price) clearly.

Marketing expenses: Whether the agent or the seller bears marketing costs.

Termination clause: Under what conditions either party can terminate before the term ends.

Post-termination tail: A common clause says the agent earns commission if the property is sold to a buyer the agent had introduced even after termination, for a period of 3–6 months.

Red Flags to Avoid

Agent without CEA number — illegal to transact.

Requests for upfront cash for marketing expenses — should be bundled in the commission.

Reluctance to sign a written EAA — a CEA violation.

Agent suggesting they represent both sides — also a CEA violation.

Pressure to sign OTP quickly without letting you consult a lawyer — a sign the agent is pushing for commission, not your interests.

Promise of guaranteed sale price — no agent can guarantee this in a market-driven transaction.

FAQ — Property Agent Commission 2026

Do I have to pay a commission if the deal falls through?

Typically no. Commission is earned on completion, not on introduction. The EAA should say this explicitly — ensure it does.

Can I use different agents for buying and selling the same property?

Yes. Many sellers use one agent for the sale and a different one for the onward purchase. There are no CEA restrictions on this.

Are commission rates negotiable even for new launches?

Not really — the developer sets the agent’s fee structure, and the buyer pays nothing either way. What is negotiable is which agent to use, as different agents may offer different rebates back to the buyer (check CEA rules on rebates).

Who pays the commission in a cash sale of a private condo?

The same parties as any other sale: the seller pays the seller-side commission, and the buyer-side commission (if any) depends on the co-broke arrangement. Cash vs financed makes no structural difference.

Can I file a complaint against an agent?

Yes, through the CEA complaints process at cea.gov.sg. Complaints about fees, conduct, misrepresentation or CEA rule violations are taken seriously.

Disclaimer: Commission rates are market conventions, not regulated minimums. Rates and customs may shift over time. Always document your engagement in an Estate Agency Agreement and verify your agent’s CEA status before engagement.

99-to-1 property ownership is a structure where one party holds a 99% interest in a property and another holds 1%. It came under intense IRAS scrutiny in 2023–2024 when the tax authority identified a specific pattern being used to sidestep Additional Buyer’s Stamp Duty (ABSD). This 2026 guide separates legitimate 99-to-1 arrangements from the red-flag pattern IRAS has been reassessing, and explains how it differs from classic decoupling.

For the official IRAS guidance, see IRAS’s stamp duty page. This article explains the practical picture.

Quick Answer — 99-to-1 in 2026

The structure: one party holds 99% of a property, another holds 1%.

Legitimate uses: loan eligibility, succession planning, investment allocation among co-owners.

The flagged pattern: sole buyer signs OTP, then transfers 1% to another party within weeks.

Clawback: original ABSD + 50% surcharge = 1.5x the amount saved.

Different from decoupling: 99-to-1 happens at original purchase; decoupling happens long after purchase.

The red-flag pattern: a two-stage transfer executed within weeks of the original OTP.

Why 99-to-1 Became Attractive

A standard 99-to-1 structure lets two parties co-own a property with minimal share for one. In isolation this is unremarkable — people use it for tax planning, succession, and pooled investment.

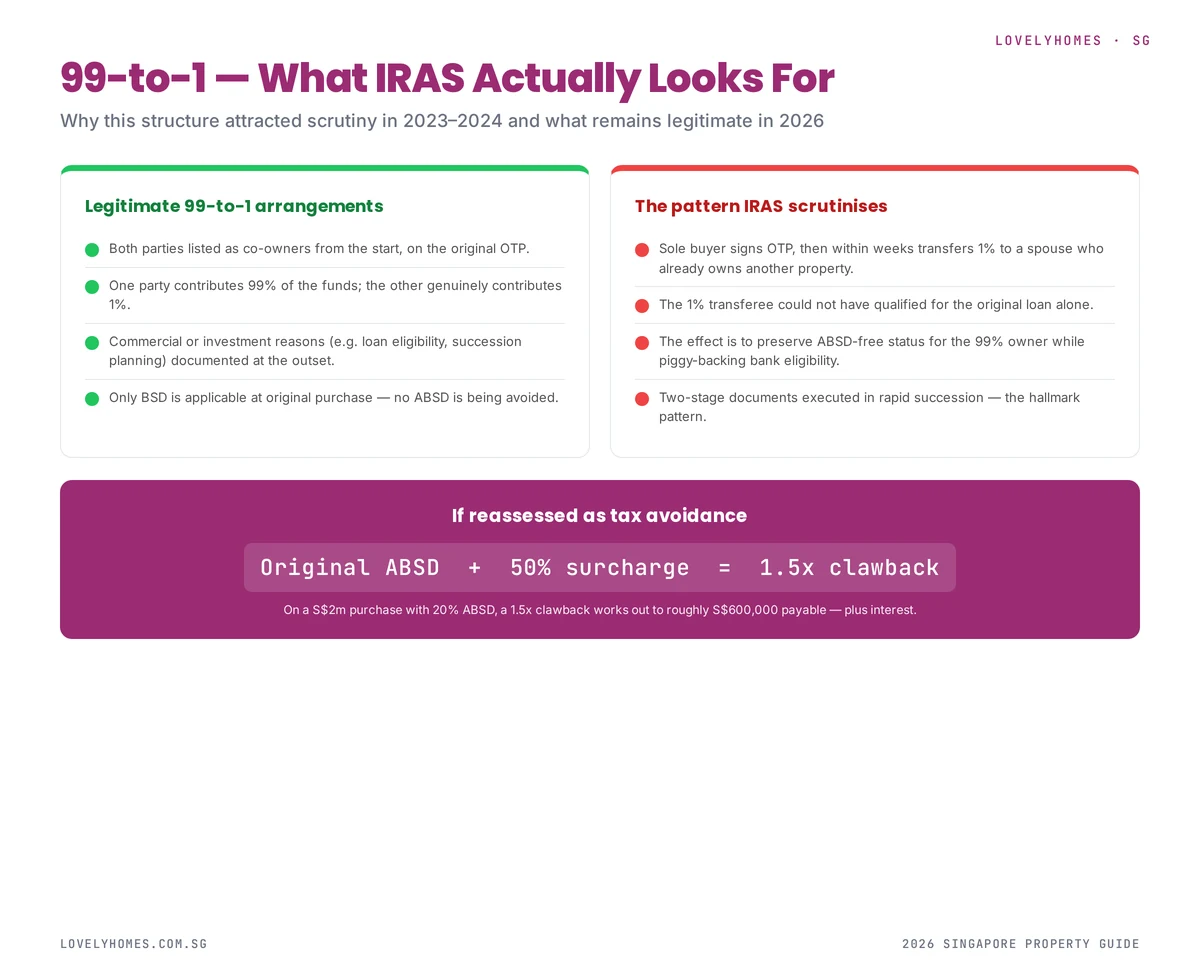

Under Singapore’s ABSD framework, though, it can also function as a loan-qualification tool. Here is the pattern IRAS identified:

A buyer without enough income to qualify for a large bank loan wants to buy a S$2m condo.

A family member with high income but who already owns a property agrees to be named on the loan.

The high-income family member was added as a co-owner at 1%, while the main buyer takes 99%.

The bank was willing to lend based on both incomes because the family member is a co-owner.

But because the family member only owned 1%, the buyer’s main ownership would have qualified for first-timer ABSD treatment.

The effect: a high-income co-owner who already owned property was piggybacking on a first-timer buyer’s ABSD rate. IRAS identified this as a tax-avoidance pattern under the general anti-avoidance provision.

The IRAS Audit Pattern

IRAS has been targeting a specific variant of 99-to-1:

Sole buyer signs the OTP and pays BSD on the full purchase price at first-timer rates.

Within weeks of OTP, a 1% share is transferred to a second party (often a spouse or parent).

The 1% transferee already owns another property — they would have triggered ABSD if they had been on the OTP from day one.

The two-stage structure avoids the ABSD that a direct joint purchase would have incurred.

IRAS reviewed approximately 300–400 such cases in its 2023–2024 sweep. Where the pattern matched, IRAS reassessed the transaction as if the 1% transferee had been a co-owner from the start, and issued an ABSD bill plus surcharge.

The 1.5x Clawback

When IRAS reassesses a 99-to-1 arrangement as tax avoidance, the remedy is:

The full ABSD that would have applied had the transferee been on the OTP from day one

Plus a 50% surcharge on that ABSD

On a S$2m purchase where avoided ABSD was 20% = S$400,000, the clawback works out to S$400,000 + S$200,000 surcharge = S$600,000 payable, plus any interest and legal costs. This is materially more punitive than simply paying the ABSD upfront.

Legitimate 99-to-1 Arrangements

Not every 99-to-1 is a red flag. IRAS has explicitly acknowledged the pattern is legitimate when:

Both parties are co-owners from day one

If both parties sign the original OTP and are named as co-owners in the Sale & Purchase Agreement at the 99:1 split, this is a single transaction and the full ABSD applies on the 1% transferee’s share from the outset. No two-stage manoeuvre, no IRAS issue.

Genuine investment-pooling

Multiple family members pooling funds for an investment property, with each contributing in proportion to their share, is legitimate — provided the shares reflect actual contribution.

Succession planning

A parent retaining 99% and transferring 1% to a child for succession reasons is legitimate, subject to the normal BSD on the 1%. Timing is usually far removed from any property transaction, which is itself a credibility signal.

Commercial co-ownership

Business partners sharing an investment property where one partner provides 99% of the capital and the other provides 1% (perhaps in exchange for operational management) is legitimate under normal commercial logic.

How 99-to-1 Differs from Decoupling

Aspect

99-to-1

Decoupling

Timing

At or near original purchase

Years after purchase, before a new purchase

Ownership after

99:1 split persists

One party becomes sole owner

What it enables

Two parties on loan

Freed spouse buys second home

ABSD mechanism

Avoided on the 99% party

Avoided on the transferring party’s next purchase

IRAS scrutiny

2023–2024 sweep

Reviewed case-by-case

Put simply: decoupling restructures an existing joint ownership; the flagged 99-to-1 pattern manipulates a fresh purchase to sidestep ABSD that would otherwise have applied.

If You Already Have a 99-to-1 Arrangement

If you set up a 99-to-1 before 2023–2024 and have not heard from IRAS, it is almost certainly not in the audit scope. However, if you receive an IRAS query letter:

Do not respond on an informal basis. Engage a tax-focused solicitor immediately.

Compile the documentary evidence for the legitimate commercial purpose of the arrangement.

Be ready to pay the full clawback + surcharge if the pattern matches the flagged type. Appealing is expensive and the success rate has been low.

Consider restructuring if the arrangement is ongoing — though retrospective fixes rarely help once IRAS has engaged.

Current Status in 2026

As of 2026, IRAS continues to monitor two-stage transfers with a 1% residual. The 2023–2024 sweep was not a one-off — it set a precedent that routine transaction audits now look for. Structures that superficially resemble the flagged pattern are far riskier than they were before 2023.

For buyers with legitimate pooling or succession reasons, the arrangement remains viable — but put the co-owner on the original OTP, keep documentation of commercial intent, and avoid the tell-tale timing pattern.

FAQ — 99-to-1 2026

Is 99-to-1 illegal?

No. The ownership structure itself is legal. What is scrutinised is whether the specific arrangement amounts to tax avoidance under the general anti-avoidance provision.

Can I still use 99-to-1 today?

Yes, provided both parties are on the original OTP and the arrangement has a genuine commercial purpose. The risky pattern is the two-stage transfer executed soon after OTP.

How does IRAS identify flagged arrangements?

By cross-referencing stamp duty records with property ownership data. If you owned property before the 1% transfer date, IRAS’s system will flag the transaction for review.

What about 95-to-5 or 90-to-10?

The same anti-avoidance principle applies. IRAS has focused on 99-to-1 because it is the most extreme variant, but the logic extends to any split where a high-income party with existing property takes a minor share to piggyback ABSD rates.

Can I unwind an existing 99-to-1 to avoid IRAS attention?

Possibly, but consulting a tax lawyer before any action is essential. Unwinding can itself trigger stamp duty and CPF complications, and retrospective “fixes” are often viewed as evidence of avoidance intent.

Disclaimer: This article explains a complex and evolving area of Singapore tax law. Specific cases require qualified legal and tax advice. IRAS enforcement practice may shift further.