Property decoupling is the restructuring of joint ownership between spouses so that one of them becomes the sole owner of the existing property, freeing the other to buy a second home at first-timer ABSD rates (0% for SCs, 5% for PRs). In 2026, with ABSD at 20% for SCs on a second property, the savings can be substantial — but HDB flats cannot be decoupled except in divorce, and IRAS scrutinises obviously tax-avoidance arrangements.

This guide walks through how decoupling works mechanically, the costs involved, a worked example, and when IRAS is likely to push back.

Quick Answer — Decoupling at a Glance

Who: Joint owners of a private property (spouses typically).

What: One party transfers their share to the other so that the other becomes sole owner.

Why: The transferring party is now property-free and can buy a second home at first-timer ABSD rates.

HDB flats: Cannot be decoupled except under divorce court order.

IRAS risk: If the arrangement is clearly contrived, IRAS can reassess as tax avoidance.

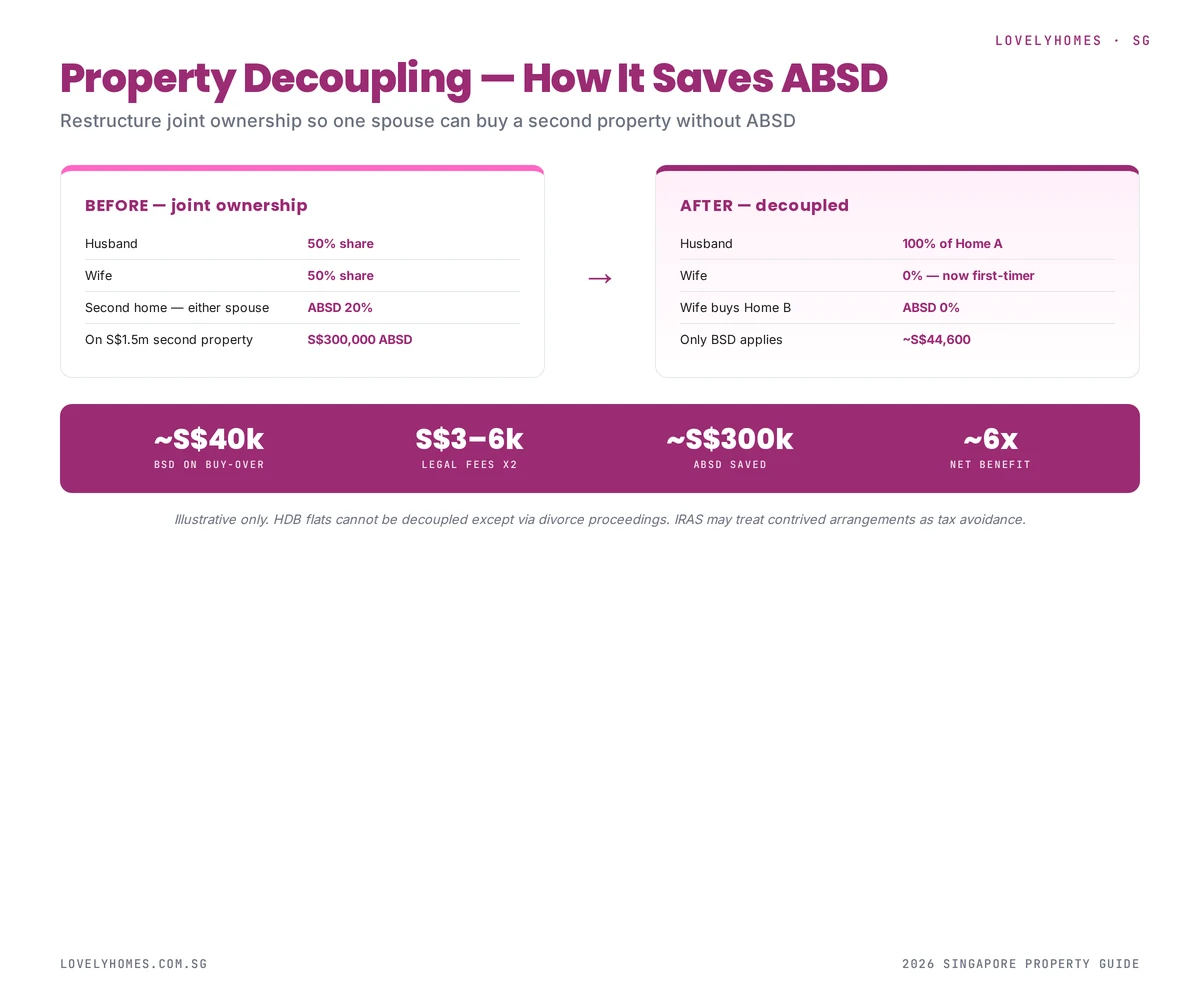

A worked before/after on a S$1.5m second property — roughly S$300k of ABSD saved for a ~S$50k restructuring cost.

How Decoupling Works Mechanically

There are two legal pathways to decouple a property:

1. Part-purchase

One spouse buys the other spouse’s share via a sale and purchase agreement. The price must be at market value (to satisfy IRAS), and Buyer’s Stamp Duty is paid on the share being transferred. If there is a mortgage, the buying spouse typically refinances the loan in their sole name.

2. Transfer-of-ownership

Less common and typically used only in genuine gift scenarios or divorce. The share is transferred via a Deed of Transfer. Stamp duty still applies based on the market value of the share.

The common pathway is Part-purchase, because it creates a clear arms-length commercial record (helpful if IRAS later asks questions).

Costs of Decoupling

Decoupling a typical S$1.5m condo with joint ownership structured as 50:50:

Component

Amount

Property value

S$1,500,000

Share being transferred (50%)

S$750,000

BSD on S$750,000 transfer

~S$17,100

Legal fees (2 parties, separate lawyers)

S$4,000–S$6,000

Mortgage refinancing costs

S$1,000–S$3,000

CPF refund (to transferring spouse’s CPF)

Full principal + accrued interest

Total cost (excluding CPF flows)

~S$22,000–S$26,000

The CPF refund is a cash flow, not a cost — the transferring spouse’s CPF OA is topped up with their original contributions plus 2.5% annual accrued interest. They can then redeploy that CPF for the second property purchase.

Worked Example: Buying a S$1.5m Second Property

A married couple owns a S$2.5m Orchard-area condo jointly. They want to buy a S$1.5m investment unit.

Without decoupling

Both already own property → ABSD 20% applies to the second purchase

ABSD on S$1.5m = S$300,000

Plus BSD on S$1.5m = S$44,600

Total stamp duty: S$344,600

With decoupling

Husband buys out wife’s 50% share of the Orchard condo → BSD on S$1.25m = ~S$35,600

Plus legal fees and refinancing: ~S$6,000

Wife now has zero property → first-timer status

Wife buys the S$1.5m second property → ABSD 0%, BSD only

BSD on S$1.5m = S$44,600

Total stamp duty + decoupling costs: S$86,200

Net saving

S$344,600 – S$86,200 = S$258,400 saved.

HDB Flats Cannot Be Decoupled

Since 2016, HDB explicitly prohibits decoupling of HDB flats except under court order (usually in the context of divorce). The rule was introduced specifically to close the ABSD-avoidance loophole that decoupling had opened for HDB flat owners looking to buy private property.

If you own an HDB flat and want to buy a private unit without paying ABSD, the only legitimate paths are:

Sell the HDB first, buy the private unit as a first-timer (subject to MOP being fulfilled)

Dispose of HDB within 6 months of buying the private unit — the ABSD Remission Scheme refunds the ABSD you initially paid

IRAS Scrutiny: When Decoupling Becomes Tax Avoidance

Decoupling is legitimate when it reflects a genuine change in ownership. IRAS begins asking questions when the arrangement is obviously contrived for tax savings alone. Red flags include:

Back-to-back decoupling and second purchase — decouple today, OTP tomorrow

The transferring spouse had no means to be a genuine buyer (income too low to have qualified for the original loan alone)

Multiple decouplings in sequence — decouple to buy property A, decouple again to buy property B

Artificial “loan” structures where the buying spouse’s share payment is obviously funded by the transferring spouse

Under the Stamp Duties Act and the general anti-avoidance provision, IRAS can reassess the arrangement as tax avoidance and claw back the saved ABSD with a surcharge. The 99-to-1 arrangement scrutinised in 2023–2024 was a related pattern — see our 99-to-1 guide.

Is Decoupling Still Worth It in 2026?

For genuine cases — where one spouse actually wants to become a sole owner, and the other actually has the income and savings to buy a second property independently — yes. The ABSD savings on a mid-market second property (S$1m–S$2m) typically far exceed the cost of decoupling by a factor of 6 to 10.

For arrangements that are transparently tax-motivated — where the transferring spouse has no genuine interest in becoming a sole property owner — the risk calculus has changed. IRAS has shown a real willingness to reassess such arrangements, and the 1.5x clawback means a failed attempt costs more than just paying the ABSD upfront.

Practical Considerations

Timing: Complete the decoupling fully before the second property’s OTP. Back-to-back transactions draw IRAS attention.

Separate legal counsel: Each spouse should use a different lawyer. Joint counsel can be a red flag.

Market-value pricing: The share must be sold at market value, supported by a professional valuation.

Mortgage servicing: The buying spouse must independently qualify for the refinanced loan in their sole name.

CPF flows: The transferring spouse’s CPF must be refunded in the correct amount, including accrued interest.

FAQ — Decoupling 2026

Can I decouple a condo I own with my parent?

Yes, the same mechanisms apply (Part-purchase or Transfer-of-ownership). The stamp duty rates depend on the parent’s relationship, and IRAS may look more closely if the decoupling pattern is unusual.

Does decoupling affect the existing bank loan?

Yes. The bank will need to refinance the loan in the sole name of the buying spouse. If the buying spouse cannot service the full loan independently, decoupling is not viable.

How long does decoupling take?

Typically 8–12 weeks from engagement to completion. Both lawyers, the bank, and CPF must all coordinate.

Can unmarried partners decouple?

They can, but the original joint ownership would need to have had a clear commercial basis (co-investors, for instance). IRAS is more likely to scrutinise an unmarried joint ownership that decouples immediately before a second purchase.

What if IRAS does reassess?

Expect the original ABSD saved plus a 50% surcharge (1.5x clawback). On our S$300k ABSD example, that would be S$450k payable — plus interest and legal costs.

Disclaimer: This is general guidance, not legal or tax advice. Decoupling has significant tax, legal and CPF consequences specific to your household. Always engage a qualified conveyancing lawyer and a tax advisor before proceeding.

The Minimum Occupation Period (MOP) is the single most important HDB rule for any flat owner. It governs when you can sell, when you can rent out the whole unit, and even when you can buy a second property. This 2026 guide explains the 5-year standard rule, how the clock starts and when it can pause, the rare exceptions, and exactly what unlocks once MOP is fulfilled.

For the official rules, see the HDB MOP page. This article explains what those rules mean in practice.

Quick Answer — MOP in 60 Seconds

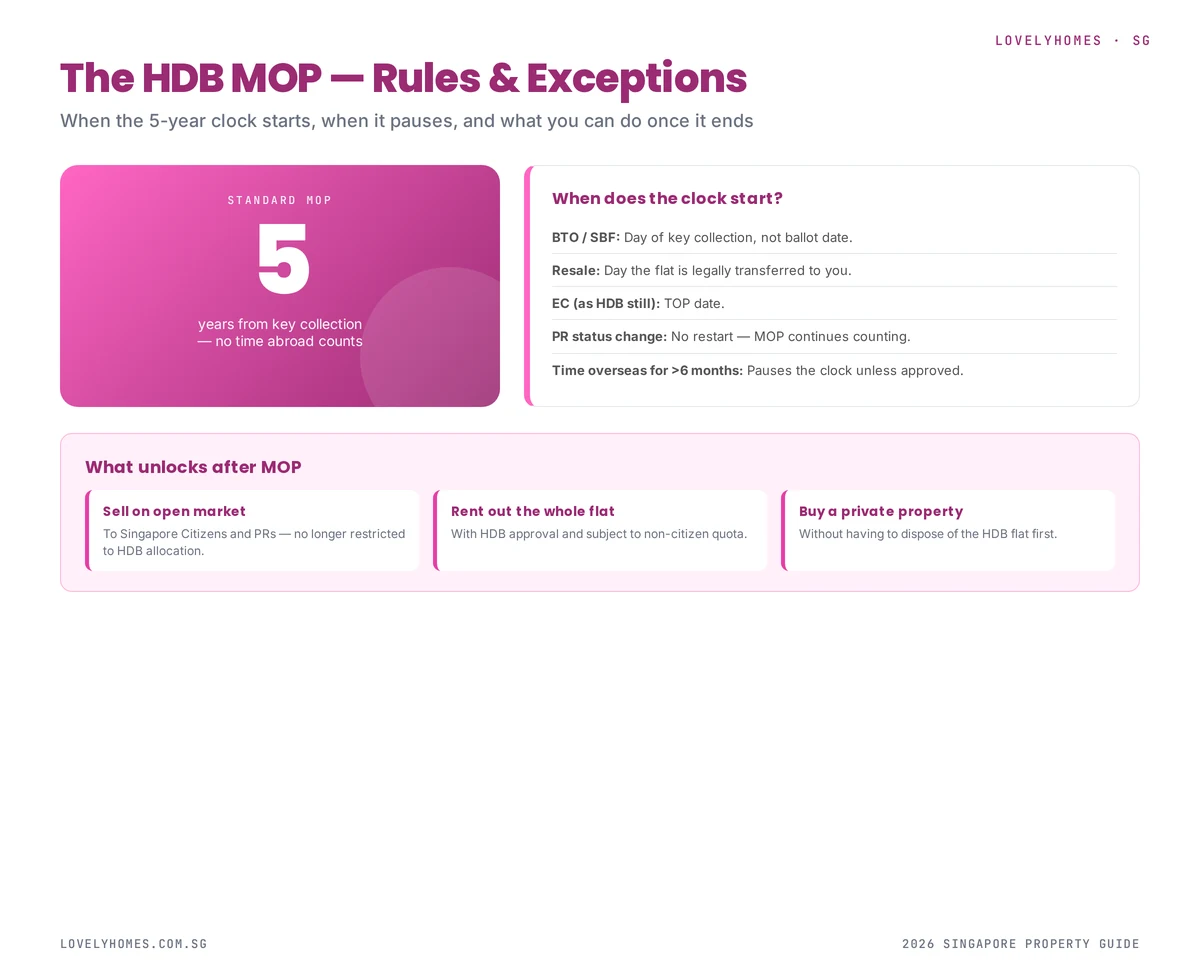

Standard MOP: 5 years from key collection — applies to most BTO, SBF, and resale flats.

Plus and Prime flats: 10 years MOP (introduced 2024).

Clock starts the day you legally take possession, not the day you apply or ballot.

Clock pauses when you are overseas for 6 months or more continuously.

Exceptions: divorce, death of spouse, financial hardship — case by case with HDB.

MOP unlocks the right to sell, rent the whole flat, and buy private property without disposing of the HDB.

The standard MOP is 5 years — the clock pauses for extended time overseas, and the consequences of breach are severe.

What Is MOP?

The Minimum Occupation Period is the number of years you must live in your HDB flat before you can sell it, rent it out as a whole unit, or use it to qualify for a second home purchase. It is HDB’s tool for ensuring public housing subsidies flow to people who actually need a home — not to speculators who buy and flip.

MOP is personal: it is the owner who must have occupied the flat for the period, not just anyone. If all listed owners have moved out within MOP (say, for overseas work), the clock pauses until at least one owner returns.

The 5-Year Standard

For most HDB flats — standard BTO, resale, SBF — the MOP is 5 years. This applies to:

All BTO flats except Plus and Prime

SBF (Sale of Balance Flats) purchases

Resale flats purchased on the open market

Executive Condominiums (for the EC-as-HDB period)

DBSS (Design, Build, Sell Scheme) flats

The 10-Year MOP: Plus and Prime Flats

Introduced in 2024, the revised BTO classification creates two new categories with extended MOP:

Plus flats

Plus flats are located in choice mature-estate areas that are not classified as “core central”. They have:

10-year MOP from key collection

Future-buyer income ceiling applied on resale (restricts buyer pool)

Subsidy clawback at resale computed by HDB

Prime flats

Prime flats are in genuinely core central locations (Tanjong Pagar, Queenstown, Rochor, etc.). They have all of the Plus restrictions, plus an even higher subsidy clawback at resale.

When Does the Clock Start?

The MOP clock starts on the day of key collection, not on:

The ballot date of your BTO application

The signing of the Lease Agreement

The purchase completion date (for resale, these are the same day)

The date you actually move in (if different from key collection)

You can verify the exact date on your HDB My Home record via Singpass. It is worth noting the date somewhere — the 5th anniversary is the earliest you can register Intent to Sell.

When Does the Clock Pause?

MOP is an occupation requirement. If no one who owns the flat is actually living in it for an extended period, the clock pauses. The standard trigger is 6 continuous months overseas by all listed owners.

How HDB tracks overseas status

Under the Income and Property Declaration required during resale applications, HDB cross-references ICA travel records. If your records show you were overseas for a year during MOP, your effective MOP date is pushed back by a year.

What counts as “overseas”

Overseas employment (with or without HDB approval)

Study overseas

Extended travel or sabbatical

Caring for family overseas

Short trips (weeks), business travel, holidays, and study leave that total less than 6 months per calendar year generally do not pause the clock.

Exceptions to the 5-Year Rule

HDB permits early disposal in a narrow set of circumstances:

1. Divorce

If the owners divorce within MOP, HDB may approve early disposal if neither party can afford to keep the flat. Ownership can also be transferred to one party under a court order.

2. Death of a spouse or co-owner

Surviving owner(s) can retain the flat without breach. If the surviving household falls below the minimum family nucleus requirement, HDB may require the flat to be sold.

3. Severe financial hardship

Documented financial distress (bankruptcy, serious illness, prolonged unemployment) may qualify for early disposal. Case-by-case with HDB’s Financial Assistance team.

4. Change in family circumstances

Marriage resulting in ineligibility under the original scheme, or purchase of a new flat under a scheme that requires disposal of the existing flat, may qualify.

What Unlocks Once MOP Is Fulfilled

1. Sell on the open market

You can register Intent to Sell and market the flat to Singapore Citizens and PRs (subject to the block’s EIP cap).

2. Rent out the whole flat

Previously you could only rent individual rooms while occupying the flat. After MOP, with HDB approval, you can rent the entire unit. Subletting quota rules (e.g. 1 non-citizen cap for non-Malaysian foreigners) still apply.

3. Buy private property without disposal

Before MOP, if you wanted to buy a private property, you would need to dispose of the HDB within 6 months of TOP of the new property. After MOP, you can hold both — subject to ABSD and TDSR implications. See our ABSD guide.

4. Apply for a second BTO or resale

Post-MOP, if you sell the original flat, you can re-enter the BTO / resale market as a second-timer buyer (with reduced grant eligibility but still eligible).

Consequences of Breaching MOP

Breaching MOP is treated seriously by HDB. Possible consequences include:

Compulsory acquisition of the flat at HDB’s administered price — typically below market value.

Financial penalty equivalent to the subsidy or concessionary loan received.

Banning from future HDB purchases for a period of years.

Referral for prosecution in cases of fraudulent misrepresentation (e.g. fake tenancy agreements).

The most common accidental breach is renting out the whole flat before MOP. If you must be overseas during MOP, sublet only individual rooms with HDB approval.

MOP and Your Financial Planning

Knowing your exact MOP date lets you plan key life decisions:

Upgrading to a condo? Target MOP + condo launch cycle for maximum CPF refund and minimum ABSD complexity.

Moving for work? Understand how overseas time pauses the clock so you don’t miss MOP by years.

Family expansion? Post-MOP flexibility (sell, rent, or buy additional property) enables better choices.

Rental income? Model the income stream against the HDB subletting quota rules.

FAQ — HDB MOP 2026

What is the shortest possible MOP?

5 years for standard flats. Plus and Prime flats are 10 years. There is no way to reduce the MOP shorter than these limits through any scheme.

Does becoming a PR after buying restart my MOP?

No. Citizenship status changes do not restart the MOP clock. The 5 years begin from key collection regardless.

Can I count time spent at my parents’ house toward MOP?

No. MOP requires occupation of your specific flat. Time spent elsewhere, even with family, does not count.

Does the MOP transfer to a new co-owner I add later?

Adding an owner does not restart the clock, but the added owner’s MOP is measured from the date they become an owner. This matters if they intend to use MOP completion for their own eligibility (e.g. to apply for a second property).

Can I sell the flat through a private sale after MOP, to avoid HDB involvement?

No. All HDB flat transactions must go through HDB’s resale process. Private sales of HDB flats outside the HDB framework are not permitted.

Disclaimer: This is general information, not legal advice. HDB evaluates MOP edge cases on a case-by-case basis — if your situation is unusual, contact HDB directly before making any plans.

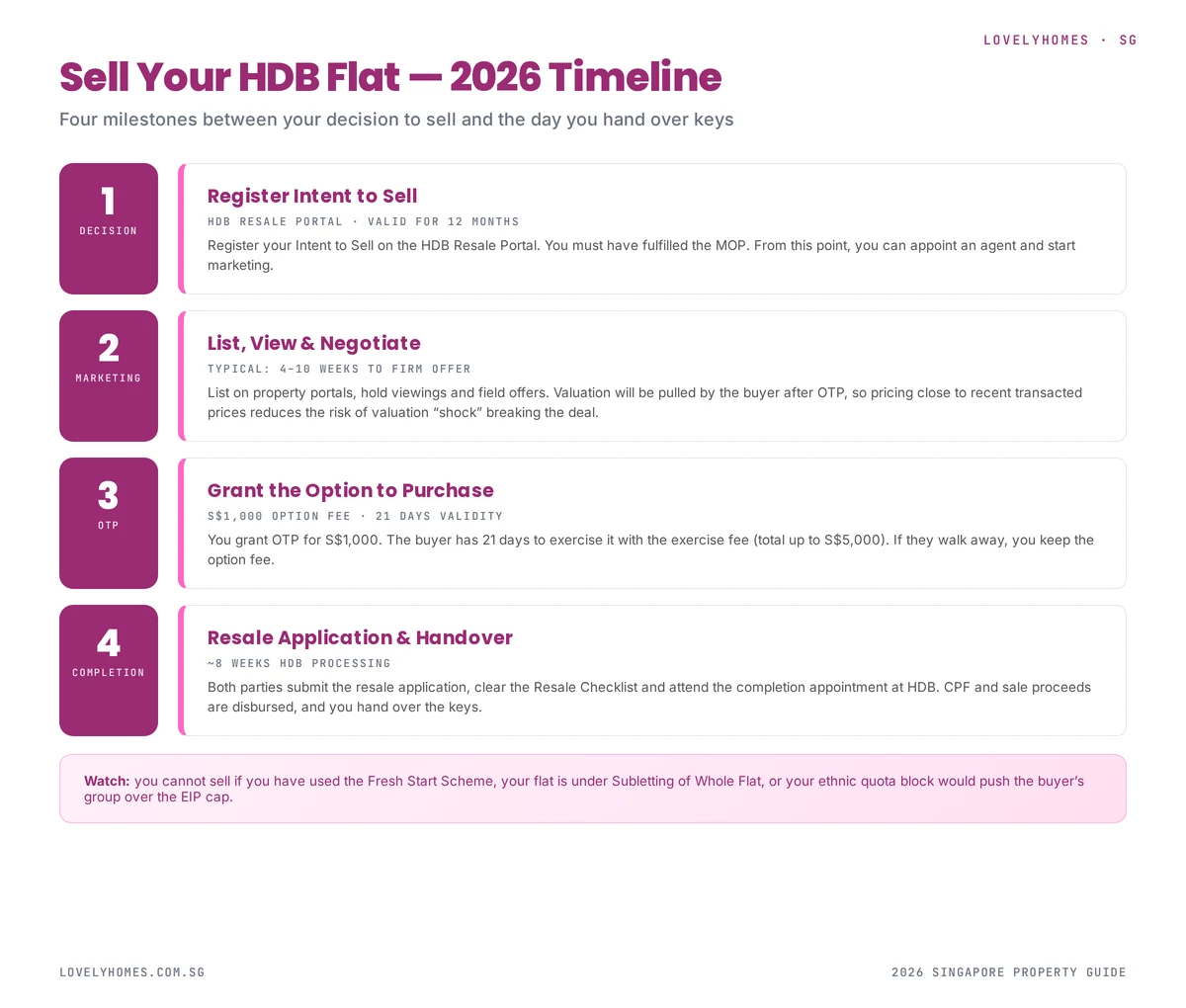

Selling your HDB flat in Singapore is a four-stage process — Intent to Sell, marketing and negotiation, OTP, and completion. Each stage has its own legal document, its own timing constraints, and its own price-breaking pitfalls. This 2026 guide walks through the full sequence from the seller’s side.

See HDB’s official selling page for the regulatory details. This guide explains the practical mechanics.

Quick Answer — Selling an HDB Flat

Check your MOP — 5 years from key collection for most flats.

Register Intent to Sell on the HDB Resale Portal.

List, view, negotiate — typically 4–10 weeks.

Grant the Option to Purchase (OTP) — S$1,000 option fee, 21-day validity.

Both parties submit the resale application — ~8 weeks HDB processing.

Completion appointment at HDB Hub — hand over keys.

Total: 3–4 months from listing to completion.

Four milestones between listing decision and handing over keys.

Step 1: Check Your MOP

You cannot sell an HDB flat until the Minimum Occupation Period (MOP) has been fulfilled. For most modern flats this is 5 years from key collection; for Plus and Prime flats it is 10 years. See our MOP guide for the exceptions and consequences of breach.

Time spent overseas for more than 6 months at a stretch does not count. If you have been posted abroad, verify with HDB that your effective MOP is what you think it is.

Step 2: Register Intent to Sell

Log into the HDB Resale Portal with Singpass and submit Intent to Sell. This is valid for 12 months. It:

Confirms your eligibility to sell (MOP, ethnic quota impact)

Allows you to appoint a licensed property agent

Triggers HDB’s valuation pipeline when an OTP is later granted

Gives buyers assurance that the flat is legitimately for sale

Step 3: Price, List and Negotiate

HDB resale is now in a tight market with COV back on the table. Price correctly:

Pricing benchmarks

Recent transacted prices on the HDB Resale Portal for the same block, type, and floor

Recent COV spread — has the estate been transacting above or below valuation?

Remaining lease — a shorter lease narrows the buyer pool considerably

Block-level ethnic quota — a block that is “closed” to major ethnic groups has a reduced buyer pool and attracts weaker offers

Agent vs no-agent

The HDB Resale Portal is designed to let sellers transact without an agent. However, a good agent will:

Run marketing on PropertyGuru, 99.co, and Facebook/IG for 2–4 weeks

Coordinate viewings (typically evenings and weekends)

Shepherd both parties through resale application submission

Typical seller-side commission in 2026 is 2% of the transacted price. See our agent commission guide.

Step 4: Grant the OTP

Once you and the buyer agree on a price, you grant the OTP. The option fee is fixed at S$1,000. The buyer then has 21 calendar days to exercise by paying the exercise fee (up to S$4,000 more, so total S$5,000 maximum). Key points:

If the buyer fails to exercise, you retain the S$1,000 option fee.

If the buyer does exercise, the sale becomes unconditional. You cannot then grant an OTP to another buyer.

Valuation is requested at this point — if it comes in below the agreed price, the buyer must pay the shortfall in cash (COV).

Step 5: Resale Application

Within 7 days of OTP exercise, both seller and buyer log into the HDB Resale Portal and jointly submit the resale application. You will:

Confirm the agreed price and terms

Select your conveyancing solicitor (HDB Legal or private)

Complete the Resale Checklist — a set of confirmations from both parties

Pay the administrative fee (S$80 for 1-2 room, S$120 for 3-room and above)

HDB then processes the application, targeted at 8 weeks. During this time, HDB will audit your ownership, verify the buyer’s eligibility, compute CPF refunds, and arrange the completion appointment.

Step 6: Completion Appointment

Typically 8–12 weeks after the resale application, you attend the completion appointment at HDB Hub. Both parties sign the transfer documents, CPF refund is credited to your Ordinary Account, the buyer’s loan is disbursed, and you hand over the keys.

What Happens to Your CPF and Sale Proceeds

The sale proceeds flow in this sequence:

Outstanding HDB or bank loan is repaid in full from the proceeds.

CPF refund — the principal you used from CPF, plus accrued interest, is refunded back into your CPF Ordinary Account. This can be substantial on a flat you have lived in for 10+ years.

Balance — what remains is your cash-in-hand from the sale.

If the flat has appreciated slowly or you used a large CPF component, the CPF refund may consume most of the proceeds, leaving little cash. This is the “negative sale” scenario and a real risk for short-lease resale.

Worked Example: Selling a S$680k 4-Room Flat

You bought the flat 9 years ago for S$420k, paid using S$100k CPF (principal) and a S$300k HDB loan, and have S$150k outstanding on the loan:

Item

Amount

Sale price

S$680,000

Less: outstanding HDB loan

(S$150,000)

Less: CPF refund (principal + 9yr accrued @ 2.5%)

(S$125,000)

Less: agent commission (2%)

(S$13,600)

Less: legal fees

(S$500)

Net cash in hand

S$390,900

CPF Ordinary Account now holds

S$125,000 more

Common Pitfalls

Accepting an offer before verifying buyer HFE status — if the buyer cannot get HFE, the deal collapses.

Ethnic quota surprise — HDB rejects the application because the sale would push the block over its EIP cap for the buyer’s ethnic group.

Valuation shortfall — the buyer walks away if the valuation is too low and they cannot fund the cash COV.

Underestimating CPF accrued interest — many sellers find far less cash in hand than expected.

Overestimating the flat — overpricing leads to extended listing periods and ultimately a lower final transacted price.

FAQ — Selling an HDB Flat 2026

Can I sell my flat before MOP is fulfilled?

Only under exceptional circumstances (divorce, death, financial hardship) and with HDB’s explicit approval. Otherwise, sale before MOP is not permitted.

How much cash will I actually get from the sale?

Sale price minus outstanding loan minus CPF refund minus agent commission minus legal fees. For most owners 5–10 years in, cash in hand is 40–60% of sale price.

Do I pay Seller Stamp Duty on an HDB resale?

Only if you have owned the flat for less than 3 years (very rare because of MOP). See our SSD guide.

Can I reject a buyer after accepting their OTP offer?

No. Once the OTP is granted and the buyer has paid the option fee, you are legally bound to sell to them if they exercise within 21 days.

What if the buyer’s HDB loan gets denied?

The buyer can walk away from the OTP, forfeiting the option fee (and exercise fee if already paid). You are then free to re-list and sell to another buyer.

Disclaimer: HDB processes, fees and scheme rules change over time. Verify the current rules with HDB before committing to sale. Consult your conveyancing lawyer for advice on your specific situation.

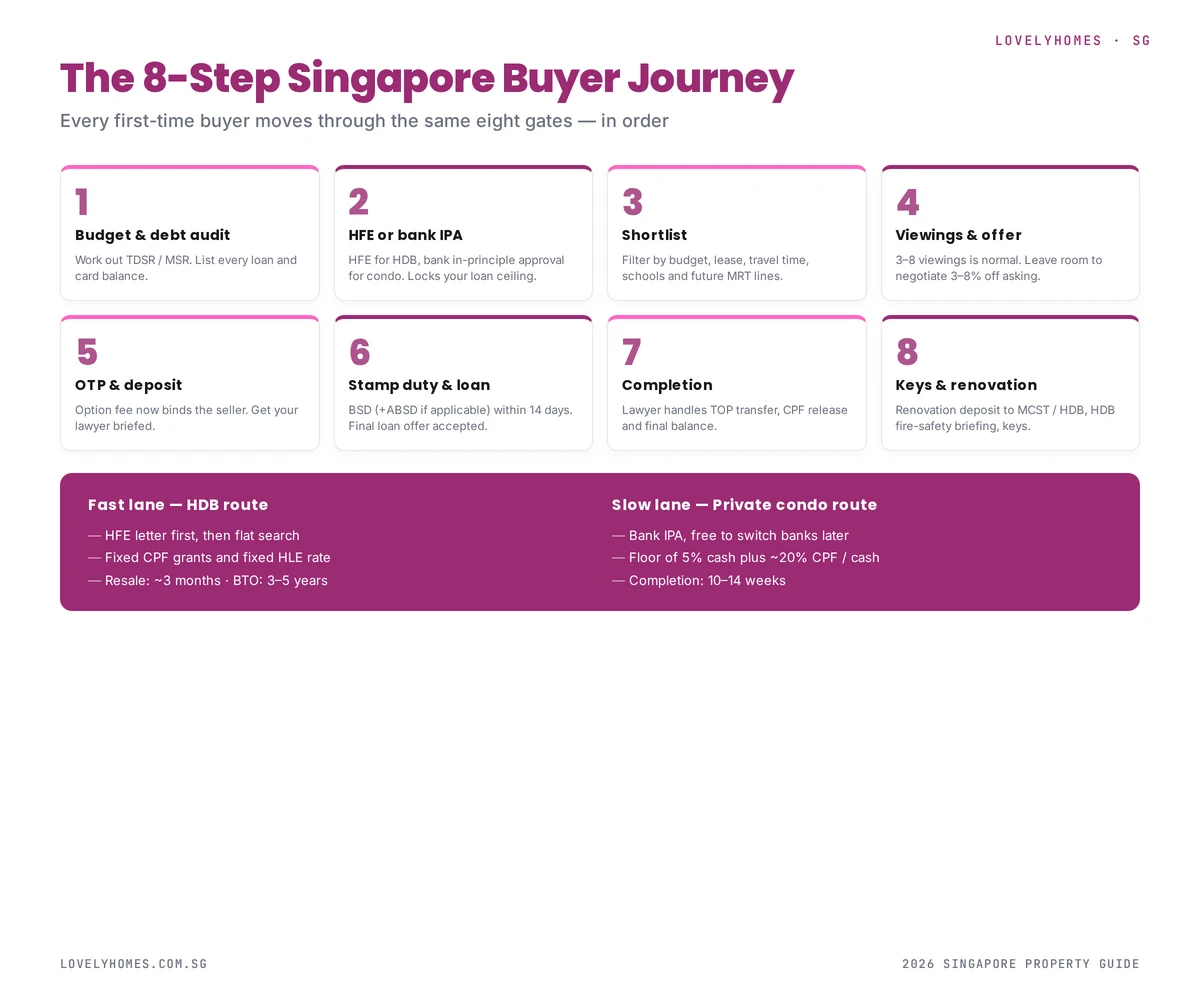

Buying your first home in Singapore is the single largest financial decision most people ever make. It has regulatory gates (HFE, TDSR, MSR), financial gates (downpayment, stamp duty, renovation), and procedural gates (OTP, resale application, completion). This 2026 walkthrough moves through all eight gates in the order you will actually encounter them.

If you are still deciding between flat types, read our comparison of BTO, resale and EC first. This article assumes you know roughly what you want to buy, and are ready to work out how.

Quick Answer — The 8 Gates

Budget and debt audit — work out TDSR and MSR.

HFE letter or bank IPA — locks your loan ceiling.

Shortlist and compare — narrow to 3–5 options.

Viewings and offer — expect 3–8 viewings before firming.

OTP and option fee — commits both parties.

Stamp duty and loan drawdown — the money phase.

Completion — legal transfer and final balance.

Keys and renovation — you own a home.

Every Singapore first-time buyer moves through the same eight gates — in order.

Gate 1: Budget and Debt Audit

Before you look at a single listing, sit down with your household income and debt obligations. Two ratios govern what banks will lend you:

TDSR 55%: All monthly debts (existing loans, minimum credit-card payments, new home loan) must be at or below 55% of gross income.

MSR 30%: For HDB and EC buyers only — home loan alone is capped at 30% of gross income.

With the maths squared away, you need a financing lock:

HDB route: Apply for an HFE letter via the HDB Flat Portal. Takes ~2 weeks. Valid 6 months.

Private condo route: Apply for Bank IPA (in-principle approval). Typically 3–5 working days. Valid 30 days.

An HFE or IPA is the document a seller or developer will ask to see before engaging seriously. It also tells you how much you can actually borrow, which constrains your flat search.

Gate 3: Shortlist and Compare

Use the HDB Resale Portal (for HDB), 99.co, PropertyGuru, and our own LovelyHomes listings (for private) to narrow a shortlist. Criteria that matter:

Transport: Walking distance to MRT, commute to work, future Cross Island Line / Jurong Region Line stations.

Schools: 1km and 2km catchment for primary schools if you have young children.

Remaining lease (HDB): Affects loan tenure and CPF usage.

Maintenance fees (private): Check the strata table for the monthly MCST fee.

Gate 4: Viewings and Offer

Expect 3–8 viewings before you firm on a unit. At each viewing, check:

Water pressure and drainage (run taps, flush toilets)

Ceiling for water staining (upstairs leaks)

Door frames for termite damage

Window seals for water ingress

Electrical outlet locations and DB box condition

Noise during the day and evening

When you are ready to offer, recognise that asking prices are typically 3–8% above the agreed-on transaction price for HDB resale, and 5–10% for private condos. Start below asking.

Gate 5: OTP and Option Fee

Once price is agreed, the seller issues the Option to Purchase:

HDB resale: S$1,000 option fee (fixed by HDB). 21 days to exercise.

Private resale: 1% of purchase price. 14 days to exercise.

New launch condo: 5% on booking, then S&P Agreement within 8 weeks.

This is the commitment point. Engage a conveyancing lawyer during this window, and if buying private with a bank loan, lock the loan offer now.

Gate 6: Stamp Duty and Loan Drawdown

Within 14 days of OTP exercise, you must pay Buyer Stamp Duty via IRAS. If ABSD applies (second or subsequent property, PR, or foreigner), it is due at the same time. Your lawyer will handle the filing and remittance.

Your bank will now process the loan in earnest. They will send a valuer to the property, finalise the loan offer, and coordinate with your lawyer for completion.

Gate 7: Completion

For HDB, completion happens at the HDB Hub, typically 8–12 weeks after the resale application. For private, it happens at your lawyer’s office, typically 8–12 weeks after OTP exercise. At completion:

You pay the final cash balance

Your CPF is debited for the CPF portion

Your bank disburses the loan

The seller receives the proceeds

Legal title transfers to you

You receive the keys

Gate 8: Keys and Renovation

Congratulations — you own a home. From this point:

Apply for HDB renovation permit if structural changes (hacking, plumbing relocation).

Attend fire-safety briefing (HDB only) before renovation begins.

Budget realistically: 4-room HDB renovation runs S$50,000–S$80,000 on average in 2026.

MOP clock starts (HDB and EC) from the completion date.

Worked Example: S$780,000 BTO Flat, First-Timer Couple

A married couple, both SCs, combined monthly income S$9,500, buying a 4-room BTO in Tengah at S$380,000 (Standard flat):

Component

Amount

Purchase price

S$380,000

CPF Housing Grant (EHG)

S$55,000

Effective price

S$325,000

HDB loan @ 75%

S$244,000

Downpayment (cash + CPF)

S$81,000

Of which minimum cash

S$16,300 (5%)

Buyer Stamp Duty

S$5,700

Legal fees

~S$500

Minimum cash upfront

~S$23,000

Monthly HDB loan (25 yr, 2.6%)

~S$1,108

Against a household income of S$9,500, this represents an MSR of 11.7% — well inside the 30% limit. TDSR is also comfortable if there are no other debts.

Common Mistakes First-Timers Make

Viewing first, financing second. Without an HFE or IPA, you cannot make a binding offer.

Forgetting renovation cost. Budget S$50k–S$100k. It is often the second-largest cost after the downpayment.

Ignoring CPF accrued interest. The CPF you use will need to be returned with ~2.5% annual compounding when you sell. See our CPF guide.

Choosing HDB Legal for complex cases. HDB Legal is great for straightforward cases but offers no flexibility if your situation has quirks (trust ownership, divorce partial transfer, etc).

Maxing the loan tenure. The longest tenure minimises instalments but means vastly more interest over time.

FAQ — First-Time Buyer 2026

How long does the whole process take from first viewing to keys?

For HDB resale: 4–6 months. For private condo: 3–5 months. For BTO: add the 3–5 year build wait after selection.

Can I use my parents’ CPF to buy?

Yes, if they are named as co-applicants or under the Essential Occupier scheme. Their contribution becomes a charge on the flat like any other CPF usage.

Should I choose HDB loan or bank loan?

HDB loan: fixed 2.6% rate, forgiving on TDSR stress test, flexible on prepayment. Bank loan: potentially lower floating rates but exposed to SORA volatility. See our fixed vs floating guide.

Do I need a lawyer for my first home purchase?

Yes. For HDB, the HDB Legal service is low-cost. For private, you will need an external conveyancing firm. Expect to pay S$2,000–S$3,500 including disbursements.

What grants am I eligible for as a first-timer?

CPF Housing Grant (up to S$80k for families depending on income), Enhanced CPF Housing Grant, and Proximity Housing Grant if living near or with parents. Your HFE letter will compute your exact entitlement.

Disclaimer: Regulations, rates and grants change over time. Verify current rules with HDB, your bank, and IRAS before committing. Consider engaging a qualified financial advisor for tax and CPF planning on large purchases.

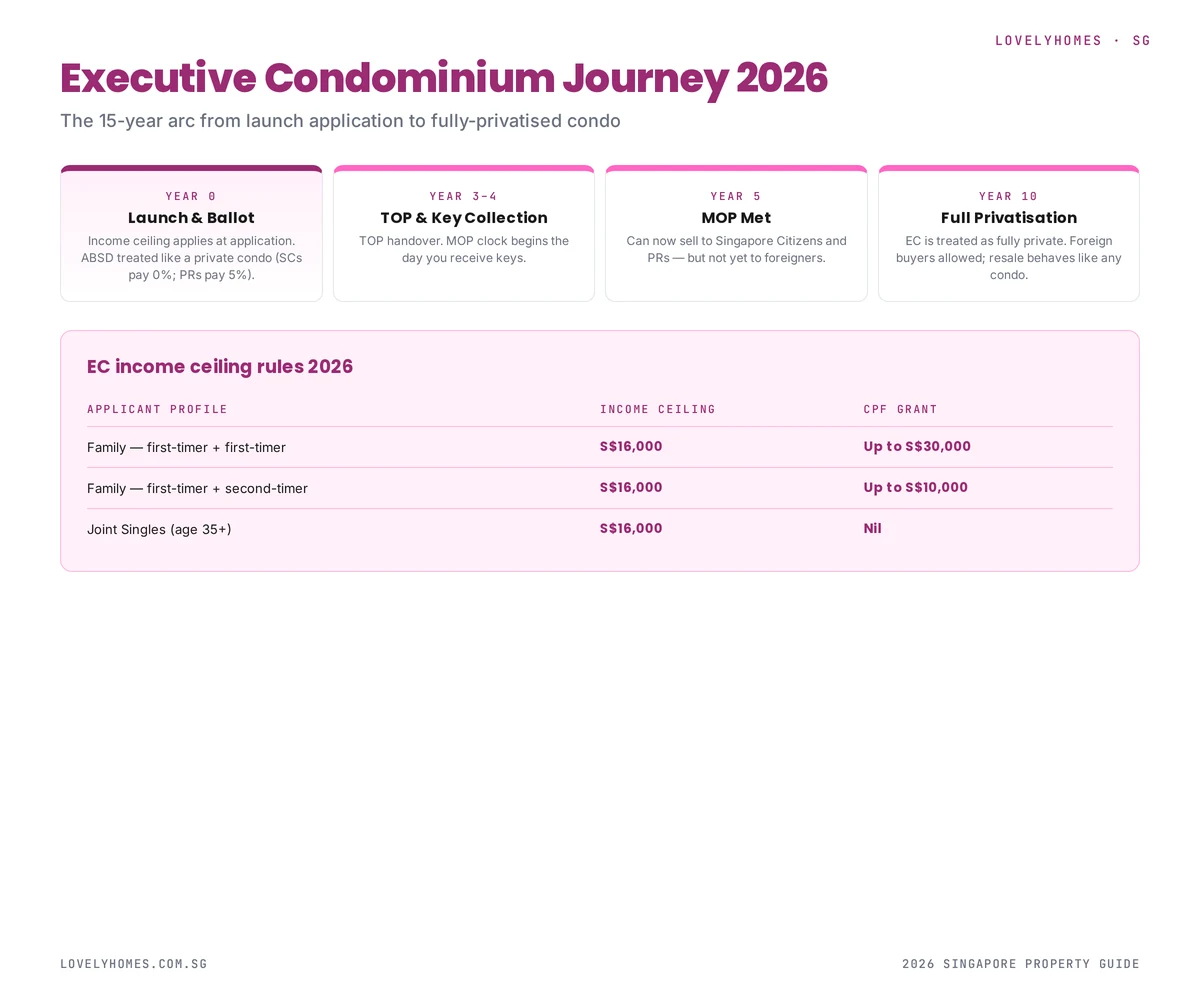

An Executive Condominium (EC) is Singapore’s middle-ground property — built by private developers like a condo, but sold initially with HDB-style eligibility rules and subsidies. Ten years after launch, it becomes indistinguishable from a private condo. This 2026 guide walks through the EC framework, eligibility rules, income ceiling, grants, and the full arc from application to full privatisation.

For the latest EC launches and rules, see the HDB EC page.

Quick Answer — EC Essentials

Hybrid flat: HDB-administered for the first 10 years, private after.

Income ceiling: S$16,000 gross monthly household income at application.

MOP: 5 years from TOP — during which you cannot sell or rent out the whole unit.

At year 5: sell to Singapore Citizens and PRs only.

At year 10: fully privatised — sell or rent to anyone, including foreigners.

CPF grants: up to S$30,000 for first-timer families.

ABSD: treated like private property — SCs 0% on first home, PRs 5%.

From launch to full privatisation — the EC follows a distinctive 15-year arc.

What Is an EC?

An Executive Condominium sits between public housing and private property. The Housing Development Board administers the launch and enforces early-stage rules, but the project itself is designed and built by a private developer, is freehold of its strata units, and has all the finishes and facilities of a regular condo — pool, gym, security, the full package.

The tradeoff is the resale restriction: for the first five years, you cannot sell the unit at all. Between year 5 and year 10, you can only sell to Singapore Citizens or PRs. Only from year 10 onwards is the EC fully privatised — at which point it is just like any other condo.

Eligibility Rules

EC eligibility sits in between BTO and private condo:

Applicant profile

Public Scheme (married couples): At least one SC, the other SC or PR.

Fiancé/Fiancée Scheme: Both parties intend to marry within 3 months of key collection.

Joint Singles Scheme: 2 singles aged 35+, both SCs.

No Single-Buyer Scheme — unlike BTO, ECs cannot be bought by a lone single applicant.

Income ceiling

The gross monthly household income must not exceed S$16,000 at application. This is tested at the time of booking, not at TOP. Once you have signed the sale and purchase agreement, subsequent income growth does not disqualify you.

Existing property ownership

Applicants cannot own any other property, local or overseas, within 30 months of the EC application. This is a stricter rule than private condos (where overseas property is fine) but less strict than BTO (which has complete no-tolerance for non-subsidised private property).

Financing and Grants

ECs are financed by bank loans only — HDB Concessionary Loans do not apply. That means:

LTV is bank-determined (max 75% for first property, falling to 45% for second).

Minimum 5% cash downpayment plus up-to-20% via CPF or cash.

TDSR and MSR both apply — whichever is tighter is binding. MSR caps the EC loan at 30% of gross monthly income.

CPF Housing Grants for ECs

First-timer families buying an EC can receive the CPF Housing Grant:

Household income

Family grant

Up to S$10,000

S$30,000

S$10,001–S$11,000

S$20,000

S$11,001–S$12,000

S$10,000

Above S$12,000

Nil

Second-timer + first-timer households receive progressively less; second-timer + second-timer couples receive no CPF grant for ECs.

Payment Schedule: Progressive Payments

ECs use a Progressive Payment Scheme because the unit is still under construction when you sign. You pay in stages as the project hits construction milestones:

Stage

% of price

When

Booking fee

5%

At booking

S&P Agreement

15%

~8 weeks after booking

Foundation

10%

Typically 6–12 months

Concrete structure

10%

Mid-construction

Further milestones

35%

Structure, walls, ceilings, M&E

TOP

25%

Key collection

CSC

15%

12 months after TOP

The 5-10-15 Journey

An EC’s economic and legal profile changes at three fixed points:

Year 0–5 (MOP period)

You cannot sell the unit at all. You can only sublet a single room, not the whole unit. The EC is, legally, treated as HDB for most purposes.

Year 5 (MOP achieved)

You can now sell, but only to Singapore Citizens and Permanent Residents. You can also now rent the whole unit out. Most EC owners who plan to upgrade do so at this point.

Year 10 (full privatisation)

The EC is now legally indistinguishable from a private condo. Foreign buyers are allowed. Resale prices typically see a step-up at this milestone, as the buyer pool widens significantly.

Income growth after booking is fine — but MOP stays at 5 years even if your income later exceeds the EC ceiling. You are not forced to sell.

Do not rent out the whole unit before MOP — this is the most common accidental breach, and HDB can compulsorily acquire the flat at the original price.

Don’t underestimate the progressive payment schedule — you need to service the loan as disbursements happen, not just at TOP.

Check the EC framework for your specific launch — rules on income ceiling, grants and MOP have been revised multiple times over the past decade.

FAQ — Executive Condominium 2026

Can I buy an EC if I already own a BTO?

You must dispose of the BTO before or within 6 months of the EC TOP date, and the MOP on the BTO must already have been fulfilled. Otherwise, you are not eligible.

What if my income goes above S$16k after booking?

No impact. The income ceiling is tested at booking only. Your future income is not relevant to your EC eligibility.

Can PRs buy an EC?

Only jointly with a Singapore Citizen, under the Public Scheme. A standalone PR applicant is not eligible.

Can I sublet individual rooms before MOP?

Yes, up to 3 rooms, provided you continue to occupy the unit. The whole unit cannot be sublet before MOP.

How is EC resale valued at year 5?

The open market determines the price, but the buyer pool is restricted to SCs and PRs only. Prices typically reflect this — liquidity step-ups further at year 10 when foreigners can also buy.

Disclaimer: EC rules have been revised multiple times; eligibility and grant amounts for your launch may differ. Always verify with the specific e-brochure for the project and consult a licensed property agent or HDB directly.