Singapore Property Checklist for First-Time Buyers 2026: Complete Step-by-Step Guide

Singapore Property Checklist for First-Time Buyers 2026: Complete Step-by-Step Guide

- Singapore Citizens buying their first residential property pay 0% ABSD — only BSD applies

- Maximum grants for HDB buyers: EHG S$120,000 + CPF Housing Grant S$80,000 = up to S$200,000 combined

- Bank loan LTV: 75% (private property); HDB concessionary loan: 90% — but you must not own other property and meet income ceiling

- TDSR ceiling: 55% of gross monthly income; MSR ceiling for HDB/EC: 30%

- BSD on S$700k HDB resale: ~S$17,400; on S$1.4M condo: ~S$44,600 — payable within 14 days of OTP

- Always sell your current home before buying a second one to avoid triggering the 20% SC second-property ABSD

- Conveyancing lawyer and IPA (In-Principle Approval) should be secured before you commit to an OTP

Buying your first property in Singapore is one of the largest financial decisions you will ever make — and one of the most bureaucratically complex. Between eligibility rules, grant calculations, loan approvals, stamp duties, and legal processes, first-time buyers in 2026 face a matrix of decisions that can take months to navigate correctly. The cost of getting it wrong — particularly on ABSD, CPF rules, or MOP requirements — can run into the hundreds of thousands of dollars.

This checklist is designed to walk you through every step of the Singapore property buying process in the right sequence. Whether you are planning to buy an HDB flat (BTO or resale), an executive condominium, or a private condo or landed property, the framework below applies — with notes on where the process diverges for each property type.

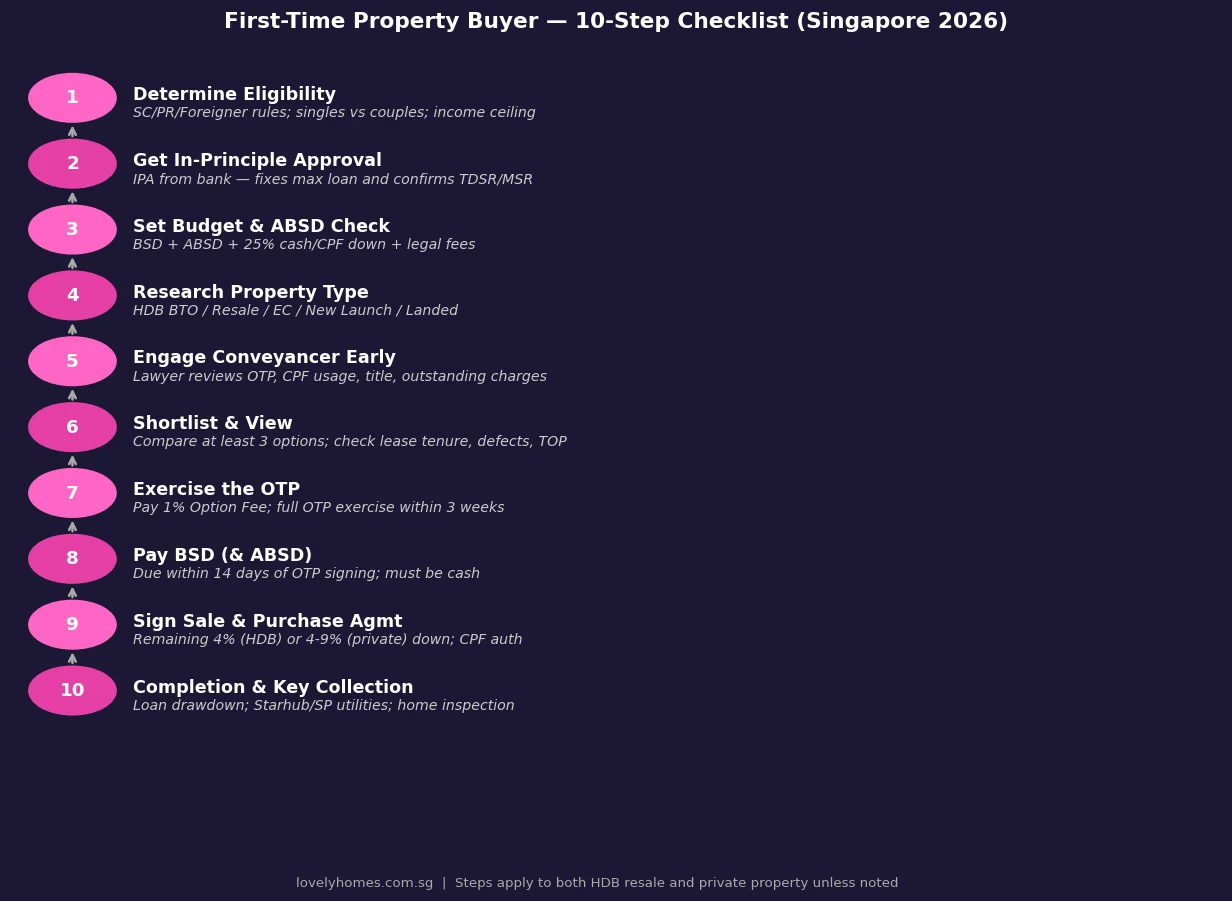

The 10-Step Singapore Property Buying Checklist

Step 1 — Determine Your Eligibility

Before browsing listings, you need to know what you are legally allowed to buy. Singapore’s property eligibility framework is citizenship-dependent and property-type-specific.

Singapore Citizens (SC) have the broadest access: they can purchase HDB flats (BTO, resale, EC), private condominiums, and (with restrictions) landed property. There is no property ownership limit per se, but each additional residential property increases your ABSD exposure significantly — from 0% on the first to 20% on the second.

Singapore Permanent Residents (SPR) may purchase resale HDB flats (with a family nucleus and after three years of PR), private condominiums, and certain ECs on the open market. SPRs pay 5% ABSD on their first residential property purchase. They cannot buy new BTO flats directly and face additional HDB Ethnic Integration Policy (EIP) restrictions on resale flats.

Foreigners (non-PR) are restricted to private condominiums and certain commercial properties. They pay 60% ABSD on any Singapore residential property. Nationals from Iceland, Liechtenstein, Norway, Switzerland, and the United States are treated as Singapore Citizens for ABSD purposes under FTA provisions.

If you are buying a BTO HDB flat, additional eligibility conditions apply: income ceiling (S$7,000/mth for 2-room Flexi, S$14,000/mth for 3-room and above), family nucleus requirement for most schemes, first-timer status, and the Ethnic Integration Policy quota at the block and neighbourhood level.

Step 2 — Secure Your In-Principle Approval (IPA)

An IPA (also called an AIP — Approval In Principle) from a bank or, for HDB loans, HDB itself, is your preliminary loan commitment. It is not the final loan offer, but it tells you — and the seller’s agent — how much you can borrow, which in turn defines your maximum purchase price.

For bank loans, the key constraints are the Total Debt Servicing Ratio (TDSR) at 55% of gross monthly income, and the Loan-to-Value (LTV) limit of 75% for private property. For HDB concessionary loans, the Mortgage Servicing Ratio (MSR) of 30% applies (your monthly loan repayment cannot exceed 30% of gross income), and the LTV is 90%. However, to qualify for a HDB loan, your household income must not exceed S$14,000/mth, and you must not own any private residential property.

Secure your IPA before viewing seriously or making any offers. An IPA is typically valid for 30 days (bank) or 6 months (HDB HLE), and it will save you from falling in love with a property you cannot actually finance.

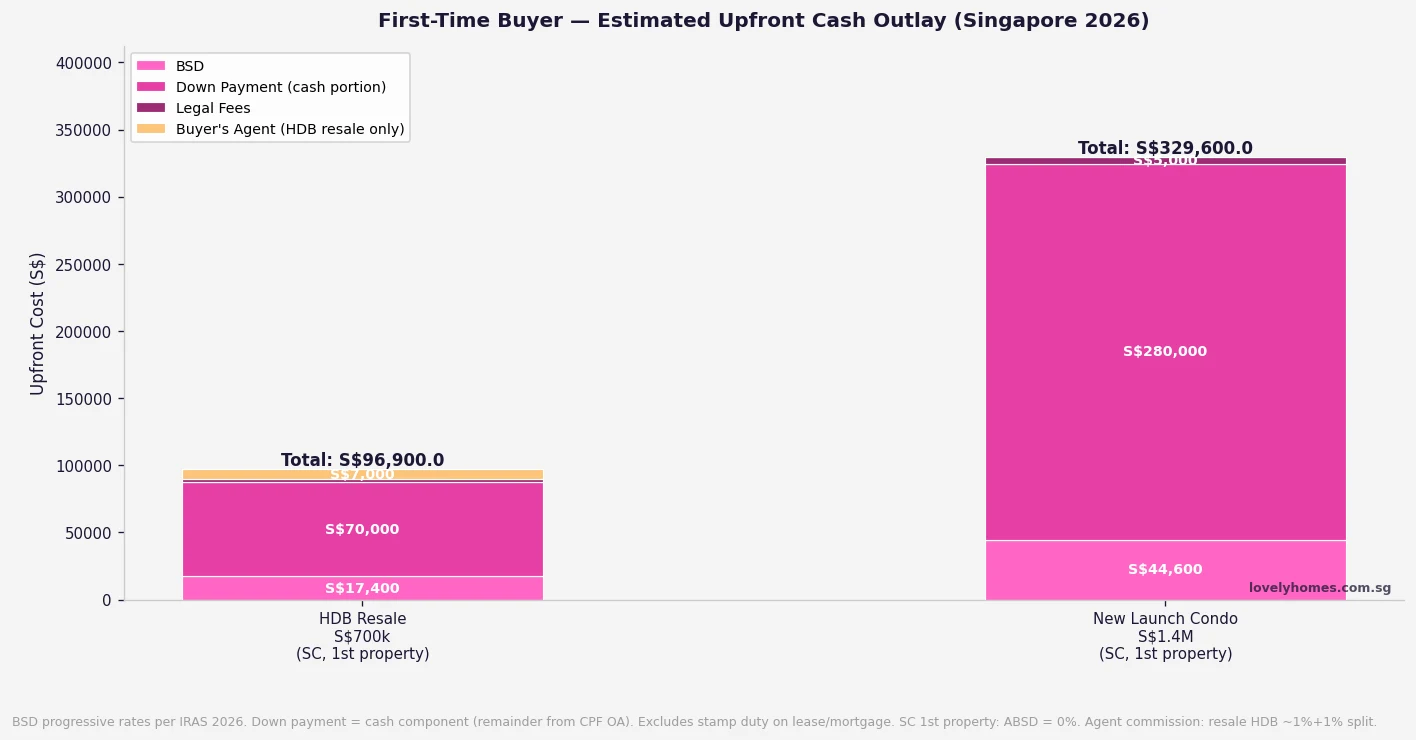

Step 3 — Set Your Total Budget Including All Costs

Your headline property price is just the beginning. The full upfront cost of purchasing includes Buyer’s Stamp Duty (BSD), the down payment (with a mandatory cash component), legal fees, and in some cases agent commission. For a first-time SC buyer, ABSD is zero — but BSD is unavoidable.

| Cost Item | HDB Resale S$700k | Private Condo S$1.4M | Notes |

|---|---|---|---|

| Buyer’s Stamp Duty (BSD) | S$17,400 | S$44,600 | Payable in cash within 14 days of OTP |

| ABSD (SC, 1st property) | S$0 | S$0 | 0% for SC first property — confirm ownership count |

| Down Payment (cash portion) | S$70,000 (10%) | S$280,000 (20% of 25%) | Minimum 5% cash for HDB; 5% cash for private (rest CPF) |

| Legal Fees (conveyancing) | ~S$2,500 | ~S$5,000 | Includes title search, CPF charge registration |

| Agent Commission (buyer side) | ~S$7,000 (1%) | S$0 | New launch: developer pays; resale private: negotiated |

| Total Estimated Cash Outlay | ~S$96,900 | ~S$329,600 | Remainder of down payment can use CPF OA |

Note that for private property, only the first 5% of the purchase price must be paid in cash (before or at OTP exercise). The remaining 20% of the 25% down payment can come from CPF Ordinary Account. For HDB loans, only 5% cash is required upfront — the remaining 85% is funded by the HDB concessionary loan.

Steps 4–6 — Research, Engage Your Lawyer Early, and View Properties

The biggest mistake first-time buyers make is viewing properties extensively before understanding their financing ceiling and legal standing. The reverse sequence — finance and legal first, then view — saves both time and negotiating leverage.

Property type selection (Step 4) depends on your income, CPF balance, timeline, and lifestyle priorities. The decision matrix in Figure 3 below compares HDB, private condo, and EC across the key dimensions first-time buyers care about most.

Engaging a conveyancing lawyer early (Step 5) is advice most first-time buyers receive too late. A good conveyancing lawyer will review the OTP before you sign it, not after. They will flag title issues, outstanding mortgages on the property, caveat searches, and CPF charge implications — all of which affect whether and at what price you should proceed. Legal fees for a straightforward purchase are modest (S$2,500–S$5,000) relative to the transaction value; do not treat them as a cost to defer.

When viewing properties (Step 6), check the remaining lease tenure carefully — especially for HDB flats and older freehold condominiums. CPF Ordinary Account funds cannot be used if the remaining lease does not cover the youngest buyer to age 95. A 60-year-old resale HDB flat may look attractively priced, but the financing and CPF limitations will materially alter your actual cost of acquisition.

Steps 7–8 — Exercise the OTP and Pay Stamp Duty

When you have identified your property, the seller will issue an Option to Purchase (OTP) in exchange for an option fee (typically 1% of the purchase price). You have a defined window — 21 calendar days for private property under the standard Law Society OTP — to exercise the option by paying the exercise price (typically another 4–9% for private, with the first 1% option fee credited) or walk away (forfeiting the 1% option fee).

Within 14 days of the OTP signing date, you must pay Buyer’s Stamp Duty (and ABSD if applicable) to IRAS via e-Stamping. Late payment attracts penalties starting at 5% of the duty payable. BSD cannot be paid from CPF — it must be in cash. This is why ensuring you have sufficient liquidity before signing the OTP is essential.

Steps 9–10 — Sale & Purchase Agreement and Completion

After exercising the OTP, your lawyer will coordinate the formal Sale and Purchase (S&P) Agreement, CPF Ordinary Account authorisation, and the loan drawdown with your bank. For new launch condominiums, the payment schedule follows the Progressive Payment Scheme (NPS) — where each tranche is tied to construction milestones — or the full lump-sum payment at completion for resale. The Deferred Payment Scheme (DPS) for executive condominiums was abolished on 8 May 2026 — all new EC purchases now follow the Normal Payment Scheme (NPS).

At completion (or key collection for BTO), your lawyer discharges their obligations and you register as the new owner at the Singapore Land Authority. Arrange for SP Group and StarHub connectivity, conduct a thorough defects inspection, and retain the developer’s or seller’s maintenance obligations where applicable.

Worked Example — SC First-Time Buyer, S$700k HDB Resale in Tampines

Ms Tan, a 31-year-old Singapore Citizen, is buying her first home — a 4-room HDB resale flat in Tampines listed at S$700,000. She earns S$6,800 per month. She has applied for an Enhanced Housing Grant (EHG) and CPF Housing Grant (CHG), and has S$120,000 in her CPF Ordinary Account.

Grants calculation: At S$6,800/mth (singles scheme), EHG = S$35,000 (approximately, based on the singles-rate EHG table at ~S$6,500–S$7,000 bracket). If she buys with a co-applicant (e.g. her mother, Singles scheme not applicable — assuming she buys as a single first-timer), or as a couple. For simplicity, assume Ms Tan buys jointly with her fiancé (combined income S$10,500/mth): EHG = S$40,000 + CHG = S$80,000 = S$120,000 total grants applied to the purchase price, reducing the effective cost.

BSD: On S$700,000 = (1%×S$180k) + (2%×S$180k) + (3%×S$340k) = S$1,800 + S$3,600 + S$10,200 = S$15,600 (payable in cash within 14 days).

Financing: Grants reduce the purchase price for grant disbursement, but BSD is still calculated on the full S$700,000 transaction price. HDB concessionary loan: 90% LTV on S$700,000 – grants S$120,000 = net S$580,000 → 90% = S$522,000 loan. Monthly repayment at 2.6% over 25 years: approximately S$2,370. MSR check: S$2,370 ÷ S$10,500 = 22.6% — within the 30% MSR ceiling.

Cash outlay at purchase: BSD S$15,600 + 10% down payment S$70,000 (min S$35,000 cash; balance from CPF OA) + legal S$2,500 + agent S$7,000 = approximately S$95,100 total, of which a minimum S$57,600 must be in cash (with the rest from CPF OA).

What to Watch in 2H 2026

Singapore’s property market for first-time buyers in the second half of 2026 will be shaped by three key developments. First, the June 2026 BTO exercise offering 6,900 flats across Bishan, Ang Mo Kio, Bukit Merah, Sembawang, and Woodlands will open for applications in mid-June — this is the largest BTO exercise of the year and the first to include Bishan Lakeview units in over four decades. First-timers with strong ballot positioning should register their interest before the application window closes.

Second, bank interest rates continue to ease in Singapore: the three-month SORA fell to approximately 1.20% as at May 2026, and major banks’ fixed-rate packages (2-year) now sit in the 1.75–1.85% range. For first-time buyers with long planning horizons, locking a rate now before any policy shift is worth discussing with a mortgage broker.

Third, the EC market is adjusting to the 8 May 2026 changes: the Deferred Payment Scheme is gone, the MOP is 10 years (up from five), and the first-timer quota has expanded to 90%. First-timers with the income and budget to qualify for an EC now have a higher allocation probability than at any point in the past five years — but they also face a longer hold requirement before they can monetise the property.

Frequently Asked Questions

Do I need to pay ABSD as a first-time Singapore Citizen buyer?

No. Singapore Citizens purchasing their first residential property pay 0% ABSD. You pay only Buyer’s Stamp Duty (BSD), which is a progressive tax starting at 1% on the first S$180,000 and rising to 6% on the portion above S$3,000,000. However, if you own any residential property at the time of OTP signing — including inherited property or a share in a property — you will be treated as a second-property buyer and face 20% ABSD. Always verify your property ownership profile via the IRAS myTax Portal before signing any OTP.

Can I use CPF to pay Buyer’s Stamp Duty?

No. BSD (and ABSD, if applicable) cannot be paid from your CPF Ordinary Account. These duties must be paid in cash within 14 days of the OTP signing date. CPF OA funds can, however, be used toward the property’s down payment (subject to the Valuation Limit), monthly mortgage instalments, and certain legal fees. Ensure you have sufficient cash liquidity to cover stamp duties before you exercise any OTP.

What is the difference between HDB loan and bank loan for first-time buyers?

An HDB concessionary loan charges a fixed rate of 2.6% per annum (0.1% above CPF OA rate), allows up to 90% LTV, and can be refinanced to a bank later (irreversibly — you cannot switch back to HDB loan once moved to a bank). A bank loan currently offers fixed rates of approximately 1.75–1.85% for a two-year lock-in (as at May 2026), requires a minimum 25% down payment with 5% in cash, and requires a stress test. For buyers who prioritise certainty and lower initial cash outlay, the HDB loan is simpler. For those who want to minimise total interest over a long loan tenure, a bank loan often saves significantly more — but exposes you to rate refixing risk every 2–3 years. See our Home Loan Comparison Singapore 2026 guide for a detailed worked comparison.

How long does the HDB BTO process take from ballot to key collection?

The full BTO cycle — from launch ballot to key collection — typically takes four to five years for standard construction timelines, though some projects take longer. The sequence is: Launch (application window) → Ballot result (2–3 months) → Flat selection queue (typically 6–12 months) → Sign S&P Agreement (within the selection window) → Construction period (3–4 years typically) → Temporary Occupation Permit (TOP) → Key collection. For buyers who need housing sooner, resale HDB flats, Sale of Balance Flats (SBF), or private property are the alternatives. See our HDB BTO Ballot System 2026 guide for full ballot probability data by flat type and estate classification.

What happens if I sign an OTP and then cannot secure a loan?

If your bank does not approve the final loan (distinct from the IPA, which is only in-principle), you will forfeit the option fee (typically 1% of the purchase price) and potentially face claims from the seller if the failure to complete is attributable to financing. This is why securing a firm IPA before signing the OTP is essential. Most conveyancing lawyers will recommend including a financing condition in the OTP for resale transactions, which allows you to withdraw and recover the option fee if you cannot secure financing by a specified date — though sellers do not always agree to such conditions in competitive markets.

Can foreigners buy HDB flats or ECs in Singapore?

No. Foreigners (non-PR) cannot purchase HDB flats (BTO or resale) or new ECs from developers. They are restricted to private condominiums and most commercial/industrial property. A foreign national would pay 60% ABSD on any Singapore residential property purchase. The only exception is citizens of the five FTA countries (Iceland, Liechtenstein, Norway, Switzerland, USA) who are treated as Singapore Citizens for ABSD purposes — but even these buyers cannot purchase HDB flats or new ECs, as that restriction is based on citizenship/PR status, not on ABSD rates.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty (BSD) Singapore 2026: Complete Guide to Rates, Calculation and Exemptions

- Home Loan Comparison Singapore 2026: HDB Loan, Fixed vs Floating and the SORA Explained

- HDB Grants Singapore 2026: EHG, CPF Housing Grant, Proximity Grant and Step-Up Grant Explained

- HDB BTO Application and Ballot System Singapore 2026: Priority Schemes and Ballot Odds

- Private Condo Buying Process Singapore 2026: Complete Step-by-Step Guide

- Enhanced Housing Grant (EHG) Singapore 2026: Full Guide with Worked Examples

Disclaimer: This checklist is for general informational purposes only and does not constitute financial, legal, or property advice. All figures, grant amounts, BSD rates, LTV limits, and loan terms cited are based on publicly available sources including IRAS, HDB, MAS, and CPF Board as at May 2026, and are subject to change. Past performance is not indicative of future results. Consult a licensed conveyancing lawyer, financial adviser, and HDB/CEA-registered property agent before making any property transaction. Verify current grants, rates, and eligibility conditions at HDB.gov.sg, IRAS.gov.sg, and MAS.gov.sg.