Freehold or 99-year leasehold? It is the single most-asked question on every Singapore condo viewing — and the most-misunderstood. The freehold premium is real but smaller than most buyers think. Lease decay is real but slower in the early years than buyers fear. Whether the freehold premium is worth paying depends almost entirely on your holding period, not your gut feeling.

This guide unpacks how Singapore property tenure actually works in 2026 — the four tenure types you will encounter, the maths behind Bala’s Curve (the lease-relativity table the Singapore Land Authority uses internally), the financing and CPF rules that bite as a lease shortens, and a worked 20-year hold comparison on a S$1.8 million condo in the same district. Where useful, we cross-link to the underlying frameworks at IRAS and CPF.

Quick Answer — Freehold vs 99-Year Leasehold at a glance

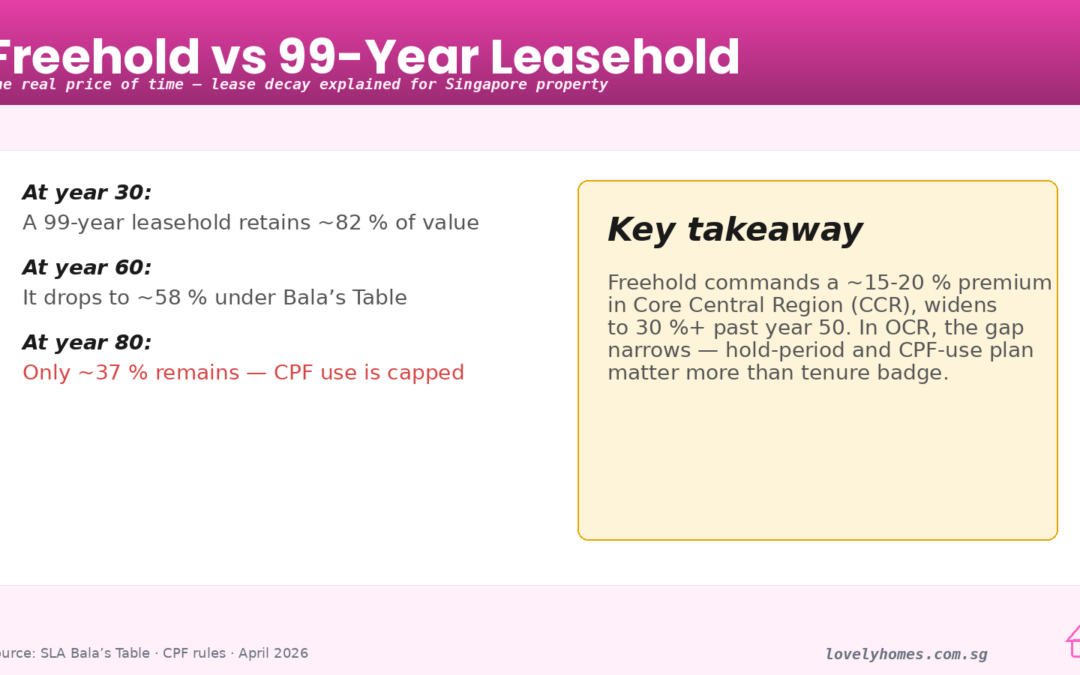

Freehold premium in comparable locations: typically 10–20% over 99-year leasehold

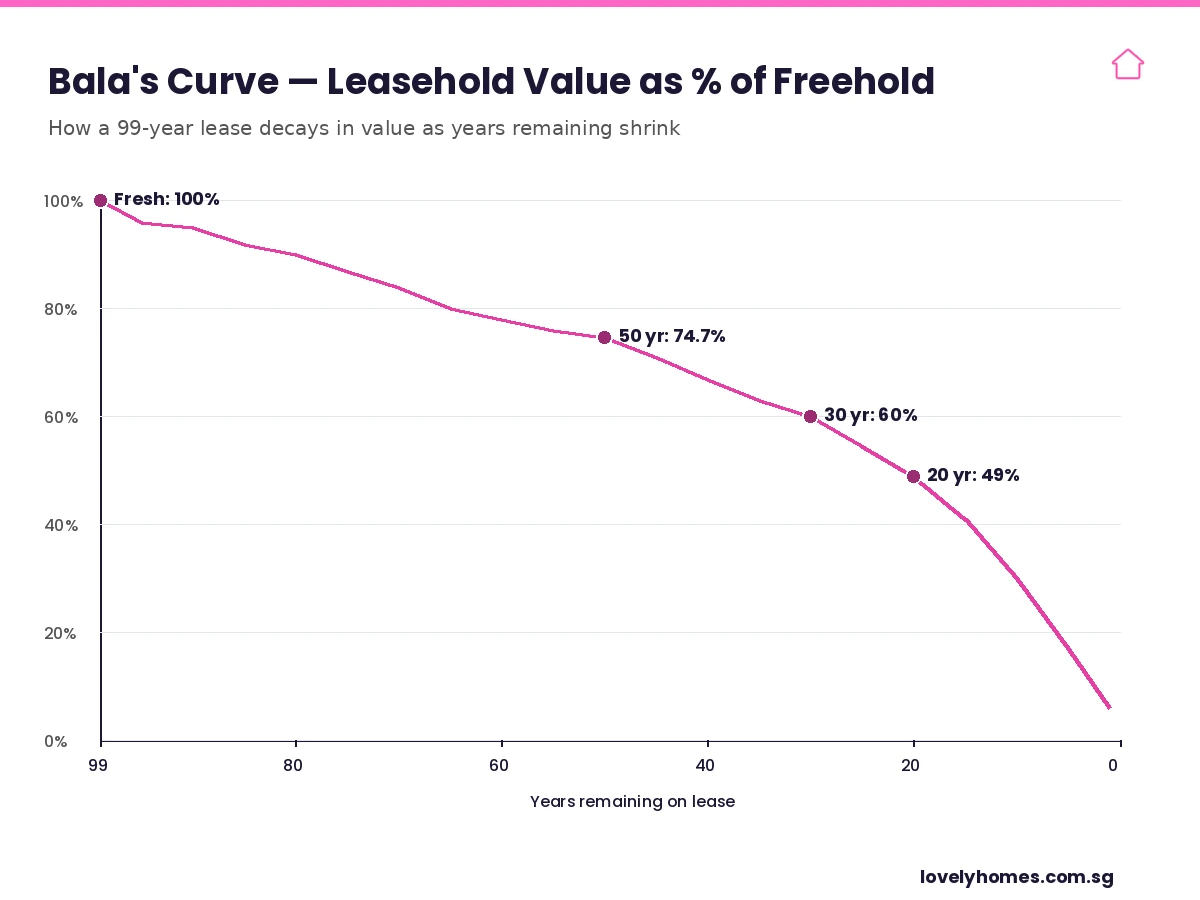

Bala’s Curve sets leasehold value at ~74.7% of freehold at 50 years remaining; ~60% at 30 years; ~49% at 20 years

CPF restrictions kick in when remaining lease is below 60 years; cannot use CPF at all if lease falls below 30 years for the next buyer

Bank financing tightens when remaining lease is below 40 years

Lease must cover the youngest applicant’s age + 95 for full CPF usage

Most new-launch condos and ECs are 99-year leasehold; freehold supply is fixed at ~5% of Singapore’s land area

For holding periods under 20 years in good locations, leasehold often outperforms freehold on a return-on-capital basis

For multi-generational holds (40+ years), the freehold premium pays for itself

What Are You Actually Buying? The Four Tenure Types

Singapore property comes with four main tenure types — and the difference between them is more legal than emotional. Tenure determines how long the State (or your descendants) recognises your interest in the land beneath your unit. Strata-Title in your condo gives you ownership of your apartment and a share in the land — for as long as the land tenure runs.

Figure 1: The four tenure types you will encounter in Singapore.

Freehold (Estate in Fee Simple)

You own the land in perpetuity, with the right to sell, lease or pass it to heirs without time limit. About 5% of Singapore’s land area is freehold — concentrated in the prime districts (D9, D10, D11) and pockets of D15. The State has not generally released new freehold land since 1965; almost all freehold supply today is from pre-1965 grants. This is why freehold supply is functionally fixed and cannot be created.

999-Year Leasehold

Issued mostly under pre-1900 colonial grants. Functionally identical to freehold for any sensible holding period — banks and valuers treat 999-year as a freehold equivalent. About 1% of Singapore’s land area sits on 999-year tenure. When you read a marketing brochure that says “freehold equivalent”, this is what is meant.

99-Year Leasehold

By far the most common tenure for new condos, Executive Condominiums, HDB flats, and almost every site released through the Government Land Sales (GLS) programme. The lease starts running on the date of issuance — which for a new launch is typically 1–2 years before TOP. Land reverts to the State at the end of the 99 years, with the building demolished or redeveloped. Subject to Bala’s Curve depreciation, which we cover next.

60-Year and 30-Year Leases

Unusual outside specific commercial or industrial sites. Some HDB shophouses sit on 60-year leases; certain industrial GLS plots are 30-year. CPF, bank-financing and resale rules are sharply restricted on these — not the tenure for a typical residential buyer.

Bala’s Curve — The Maths Behind Lease Decay

The single most important framework for understanding 99-year leasehold pricing is Bala’s Table (sometimes called Bala’s Curve, after Mr V K Balasubramaniam who developed it for the Singapore Land Authority in the 1990s). Bala’s Table sets out the value of a leasehold property as a percentage of its equivalent freehold value, indexed to the years remaining on the lease.

Figure 2: Bala’s Curve — non-linear lease decay across the 99-year lease. Steepest depreciation falls in the final 30 years.

Two features of the curve matter most:

The depreciation is non-linear. A fresh 99-year lease is worth roughly the same as freehold — the curve sits at 100%. After 50 years remaining (i.e. ~half-life), value is still ~74.7% of freehold — a far gentler decay than the simple linear “halfway = 50%” intuition. The steep portion of the curve falls in the last 30 years, when value drops from ~60% (30 years remaining) to ~17% (5 years remaining).

Bala’s Table is the floor, not the market. Real-world transactions rarely match the table exactly. Local demand, building condition, en-bloc potential, and lease topping-up rumours can push prices well above (or below) the Bala line. The table is what SLA uses to price lease top-ups and to convert tenure for tax purposes — not what the open market necessarily pays.

For a buyer, the practical implication is that the first 30–40 years of a 99-year lease behave very like freehold. A 99-year condo at TOP today is essentially “freehold for two generations”. The depreciation problem is real for buyers planning to hold past Year 60 or thinking about en-bloc redevelopment as the exit strategy.

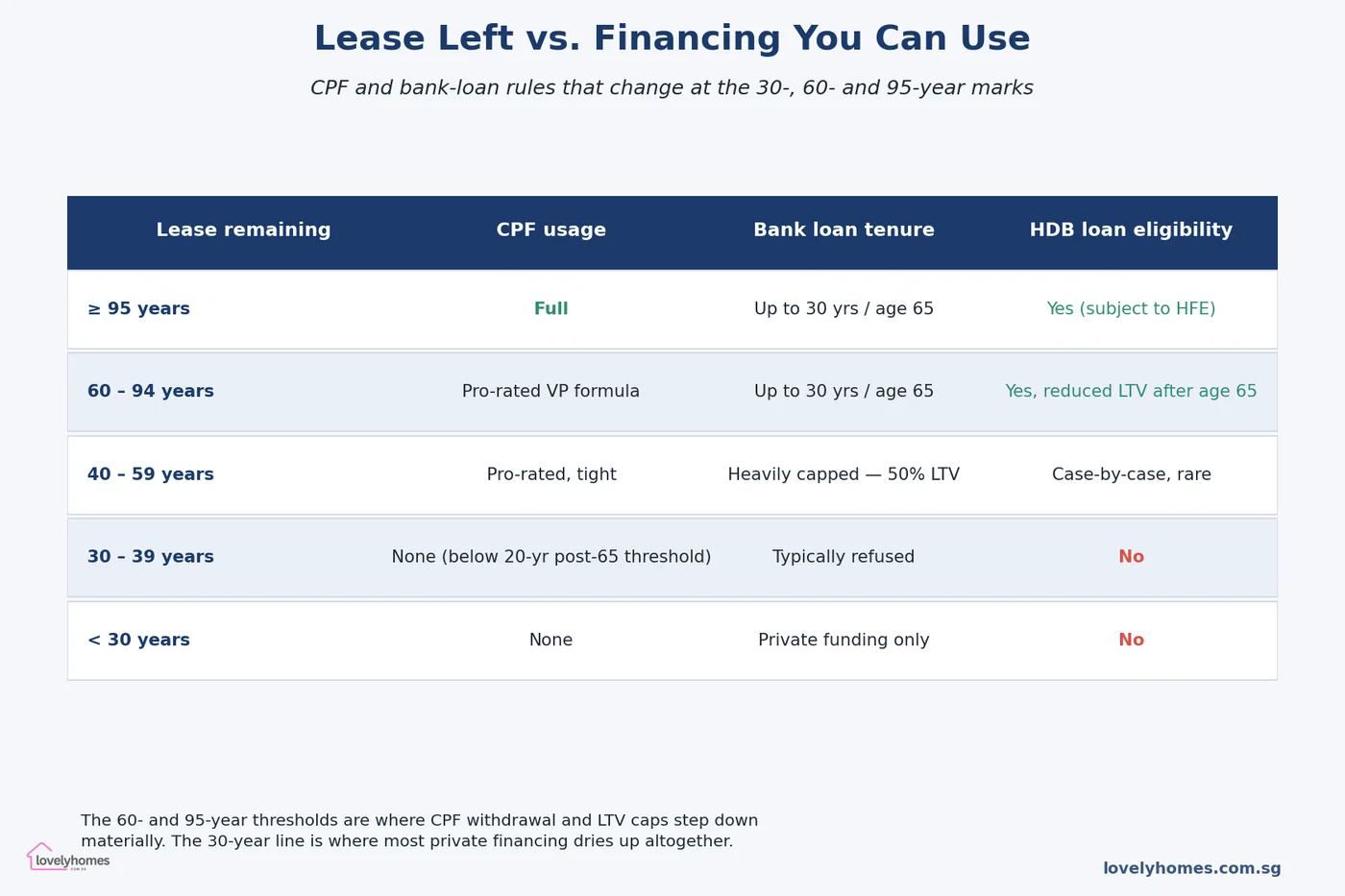

The CPF and Financing Cliffs — When Lease Decay Starts to Bite

Bala’s Curve is the underlying valuation framework, but two regulatory cliffs determine when lease decay actually starts to hurt resale liquidity:

The CPF Usage Rules

CPF can be used in full only if the remaining lease covers the youngest buyer’s age plus 95 years. For a 35-year-old buying a property today, the remaining lease must be at least 60 years for full CPF use; otherwise CPF usage is pro-rated and capped. If the remaining lease is below 30 years, CPF cannot be used at all by your next buyer — which collapses the buyer pool to cash buyers only.

The Bank Financing Rules

Bank loan tenure cannot exceed (lease remaining minus a buffer; typically 5 years). If the remaining lease is below 40 years, banks will quote shorter loan tenures, lower LTVs, and higher rates — and some banks will decline outright. When this happens, your effective buyer pool narrows further.

Together, these two cliffs mean that the Bala’s Curve depreciation is amplified in the secondary market by liquidity contraction. A 40-year-remaining lease may be worth 67% of freehold in pure Bala terms, but the smaller buyer pool means actual transactions can clear at a steeper discount. This is why the “sweet spot” for selling a 99-year leasehold is usually before Year 50, not after.

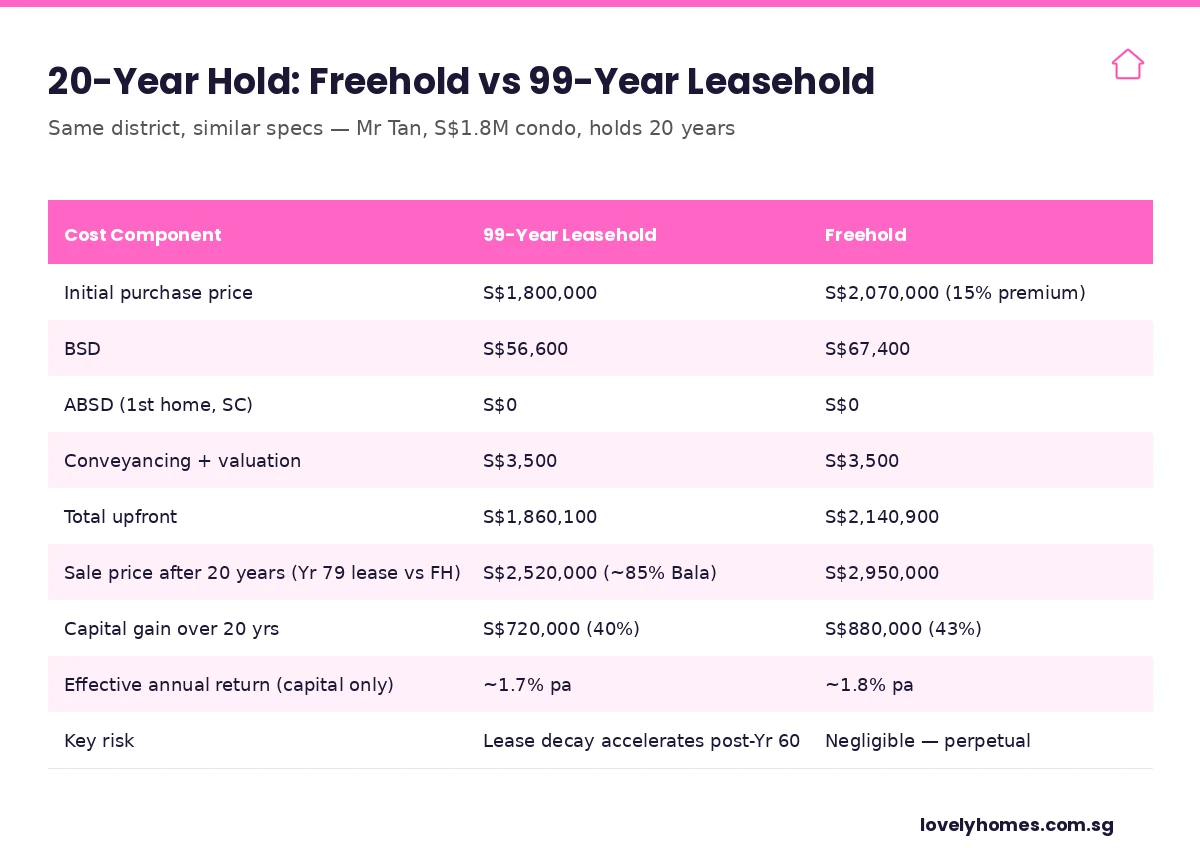

Worked Example — 20-Year Hold, Same District, Same Specs

Let’s strip out emotion and compare on the maths. Mr Tan is 40, a Singapore Citizen first-time buyer. He is choosing between two condos in the same District 15 micro-market: a brand-new 99-year leasehold at S$1,800,000 and a 999-year (freehold-equivalent) unit at S$2,070,000 — a 15% freehold premium, which is roughly the historic norm. He plans to hold 20 years.

Figure 3: 20-year hold — freehold vs 99-year leasehold, identical-district worked example.

Cost / Outcome

99-Year Leasehold

Freehold

Year 0 purchase price

S$1,800,000

S$2,070,000

Year 0 BSD

S$56,600

S$67,400

Year 0 ABSD (1st home, SC)

S$0

S$0

Year 0 conveyancing

S$3,500

S$3,500

Total upfront outlay

S$1,860,100

S$2,140,900

Year 20 sale price (assume 2.0% pa district appreciation, freehold; leasehold capped at Yr 79 Bala factor ~92% of freehold)

S$2,520,000

S$2,950,000

Capital gain

S$720,000 (40%)

S$880,000 (43%)

Effective annual return (capital only)

~1.7% pa

~1.8% pa

Return on incremental S$280,800

~3.4% pa — the marginal freehold premium implies a ~3.4% annualised return on the extra capital tied up

The headline finding: in this worked example, the freehold buyer earns a ~3.4% annualised return on the extra S$280,800 tied up in the freehold premium — modest, and below typical bond returns. For a 20-year hold, the leasehold often comes out marginally ahead on a return-on-capital basis, especially if the freed-up capital can earn 4–5% in conservative investments.

Where the maths flips is at longer holding periods. Repeat the calculation across 40 years — with the leasehold now at Yr 59 remaining (~78% Bala) versus a still-perpetual freehold — and the freehold premium starts compounding strongly. By Year 50 of holding, the freehold has typically earned a meaningful spread.

When Freehold Wins, When Leasehold Wins

The framework most experienced Singapore buyers use is to match tenure to holding period and exit strategy:

Hold under 15 years: 99-year leasehold typically wins on return-on-capital. Lease decay is too gentle in this window to matter, and the freed-up capital can earn elsewhere. This is the typical short-to-medium hold investor case.

Hold 15–30 years: A toss-up. Outcome turns on (a) the actual freehold premium paid and (b) the district’s underlying appreciation rate. In high-growth districts, leasehold often wins; in slow-growth districts, the freehold premium does its job.

Hold 30+ years or multi-generational: Freehold wins. Lease decay enters its accelerating zone, and the freehold becomes a meaningfully stronger compounding asset. This is the family-legacy or trust-held case.

Buying for own-stay, expecting to en-bloc: Leasehold can win if the project has clear redevelopment upside (high plot ratio uplift, supportive URA zoning, agreeable owner mix). The collective sale becomes the “lease top-up” you couldn’t buy directly.

Buying for rental yield: Leasehold typically yields more — lower entry price for the same rent. Yield-focused investors generally prefer leasehold.

Owners and developers occasionally apply to SLA to top up a depleting lease — restoring it to a fresh 99 years for a payment based on the difference between the current and the topped-up value. The cost is calculated against Bala’s Table. In practice, lease top-ups are most often initiated as part of an en-bloc / collective sale, where the developer negotiates the top-up alongside the redevelopment approval.

An individual owner cannot reliably plan for a private top-up. The Government’s VERS (Voluntary Early Redevelopment Scheme), announced in 2018 for selected HDB precincts, is a separate framework from private leasehold top-ups and applies only to public-housing estates. There is no equivalent statutory framework for private leasehold properties — which means private leasehold owners cannot count on lease top-ups as part of their long-term plan.

What This Means for You

If you take only five things away from this guide, take these:

Match tenure to holding period. Under 15 years, leasehold typically wins. Over 30 years, freehold typically wins. In between, run the maths on the actual freehold premium versus the capital-cost spread.

Don’t pay more than ~15–20% premium for freehold. Above this, the maths almost never works for typical holding periods. Some new-launch freehold projects have asked for 25–30% premiums — treat those with caution.

Watch the lease-remaining number when buying resale. 60 years is the CPF cliff for buyers in their late 30s. Below that, you start losing CPF eligibility for your next buyer — which compresses your exit price more than Bala’s Table would suggest.

Check the lease commencement date carefully. A new-launch 99-year condo often has a lease that started 1–2 years before TOP, so a buyer at TOP only gets ~97–98 years remaining, not 99.

If en-bloc is your exit strategy, leasehold can win. The collective-sale premium effectively converts the 99-year lease into a one-time cash payout that bypasses Bala’s Curve. But en-bloc success rates vary — do not assume your project will get there.

What Might Come Next

Three policy and market variables to watch in 2026–2027:

Bala’s Table revision. SLA last refreshed Bala’s Table several years ago. A revision — especially one that flattens the curve or pushes the steep zone closer to lease end — would mark up secondary leasehold values across the board. There is no current signal of revision in 2026.

Freehold premium compression. Several recent freehold launches have struggled to clear meaningful premiums over comparable leasehold launches in the same district. If this trend continues, the structural freehold premium may compress towards the 5–10% range, weakening the case for paying up.

VERS or analogous private-lease scheme. If the Government extends a VERS-style framework to private leaseholds (an idea floated occasionally by industry figures), the long-tail risk of holding past Year 60 reduces sharply — and the freehold premium loses some of its insurance value.

Frequently Asked Questions

Is freehold always better than leasehold?

No. Freehold is structurally lower-risk for very long holds (30+ years) and multi-generational holds. For shorter holds (under 15 years), the capital tied up in the freehold premium often earns a lower return than the same capital deployed elsewhere. The right answer depends entirely on your holding period.

What happens at the end of a 99-year lease?

The land reverts to the State. Owners typically receive no compensation unless a private collective-sale or a public scheme (e.g. VERS for HDB) intervenes earlier. In practice, almost every 99-year property in Singapore exits via en-bloc or major redevelopment well before the lease expires — full lease expiry is rare for residential land.

Can CPF be used for any leasehold property?

Only if the remaining lease covers the youngest applicant’s age plus 95. For full CPF withdrawal limits to apply, the lease must run at least to that age. Where the lease is shorter, CPF usage is pro-rated. Below 30 years remaining, CPF cannot be used at all by the next buyer.

How is Bala’s Curve different from straight-line depreciation?

Straight-line depreciation would assume the leasehold loses 1/99 of its value every year. Bala’s Curve recognises that the early years of a long lease have negligible depreciation (because the buyer pool is large and time-to-expiry is far away), while the final 20–30 years see steep depreciation (because financing and CPF rules compress the buyer pool sharply). Bala’s Table is non-linear and far more accurate for real-world pricing.

Are HDB flats freehold or leasehold?

All HDB flats are 99-year leasehold. The lease starts when the block is completed and the title issued. By the time most BTO buyers move in, the lease typically has between 96 and 99 years remaining. HDB resale flats from the 1970s and 1980s have far less remaining lease — some now under 60 years — which is why CPF eligibility for older HDB resale is increasingly tight.

Does freehold matter for rental yield?

Not really. Tenants pay for liveability, location and amenities — not for tenure. Rental yield is therefore a function of the lower entry price, which favours leasehold. Yield-focused investors typically prefer leasehold because the same rent against a lower entry price gives a higher gross yield.

Can I top up a 99-year lease privately?

An individual owner cannot reliably do so. SLA does process lease top-up applications, but they are typically in the context of an en-bloc / collective sale where the developer pays for the top-up as part of the redevelopment approval. A private owner asking SLA to extend their personal 99-year lease should not assume approval — nor should they assume the cost would be commercially reasonable.

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. Bala’s Table and CPF / financing rules are administered by the Singapore Land Authority, the Central Provident Fund Board, and the Monetary Authority of Singapore respectively, and may be revised from time to time. Always verify the current position with the Singapore Land Authority, the CPF Board, and a licensed conveyancing lawyer before signing any Option to Purchase.

Figure 1: The three tenure classes in Singapore real estate — with freehold at ~4% of the housing stock, 999-year a rare pre-1960s relic, and 99-year the dominant form.

Every Singapore property conversation eventually turns to tenure. Is the extra 10–15% for a freehold condo actually worth it? Will a 99-year leasehold unit hold its value if I plan to hold for 20 years? Do banks and CPF really pull the plug on an ageing lease? These are not academic questions. The tenure decision shapes your long-run return more than almost any other call you make at the point of purchase, and the rules that govern it — CPF usage, bank LTV caps, HDB loan eligibility, lease-top-up policy — change in sharp steps rather than smoothly.

This is the 2026 edition of our tenure guide. It walks through the legal substance of freehold, 999-year and 99-year titles; the SLA “Bala’s Table” that dictates how lease-decay is valued; the financing cliffs at 95, 60 and 30 years remaining; and a Singapore-specific worked example that puts a dollar figure on the freehold premium. We close with a forward view on what the SERS / VERS pipeline means for older leaseholds.

Quick Answer: The 10 Things Every Tenure-Sensitive Buyer Should Know

Freehold ≈ ~4% of SG residential stock. The vast majority of private homes and all HDB flats are 99-year leasehold. 999-year titles are a rare pre-1960 relic but, in valuation terms, behave like freehold.

The freehold premium is ~10–15%. In comparable micro-markets, a fresh-lease 99-year condo typically trades at 85–90% of the freehold equivalent — a narrower gap than many buyers expect.

Bala’s Table is the ruler. SLA’s published valuation table is the single authoritative source for how a leasehold interest is valued at any years-remaining. It is a non-linear curve, steepening materially below 60 years.

60 years is the financing cliff. CPF usage and bank LTVs compress sharply once a lease drops below 60 years remaining.

30 years is the exit wall. Below 30 years remaining, almost no bank will finance the unit and CPF usage is effectively nil — the buyer pool collapses to cash-rich owner-occupiers.

SERS is discretionary, not guaranteed. HDB’s Selective En bloc Redevelopment Scheme is offered to a very small minority of ageing flats; the 99 years ends and the land reverts regardless.

VERS is the policy hedge. The Voluntary Early Redevelopment Scheme (legislated 2018, rolling out for the oldest HDB towns in the late 2020s) gives residents a vote on early redevelopment in exchange for a lower pay-out than SERS.

Lease top-ups exist for private land. URA allows lease extensions via upgrading premium payments for selected private freehold/leasehold sites — used routinely by en-bloc developers.

HDB’s 99-year clock starts at award. A BTO completed in 2018 will, in 2117, revert to the state regardless of whether the flat has been sub-sold or renovated.

Tenure affects renter demand less than you’d think. Rental yields on comparable freehold and 99-year properties tend to be within 10–20 basis points of each other; the rental market is insensitive to tenure in a way the sales market is not.

What Tenure Actually Means in Singapore Law

Under the Land Titles Act, freehold in Singapore is what the Common Law calls an “estate in fee simple” — the fullest form of private ownership available, running in perpetuity and capable of being transmitted by will or gift without reverting to the state. 999-year leasehold is functionally indistinguishable from freehold during the lifetime of anyone reading this article; valuers treat it at par with freehold for discounting purposes, and both CPF and bank lenders do the same. Its rarity reflects early colonial-era land grants, most of them pre-1960.

99-year leasehold is the modern default. The State (via the Singapore Land Authority, SLA) retains reversionary title; the leasehold owner holds what is technically a “term of years absolute”. When the lease expires, title reverts without compensation unless the land is re-granted. This is the deal that underpins every HDB flat, every Executive Condominium (from its initial sale onwards), and the majority of private condos and landed properties released from the Government Land Sales (GLS) programme since the 1970s.

How Lease Decay Is Valued: Bala’s Table

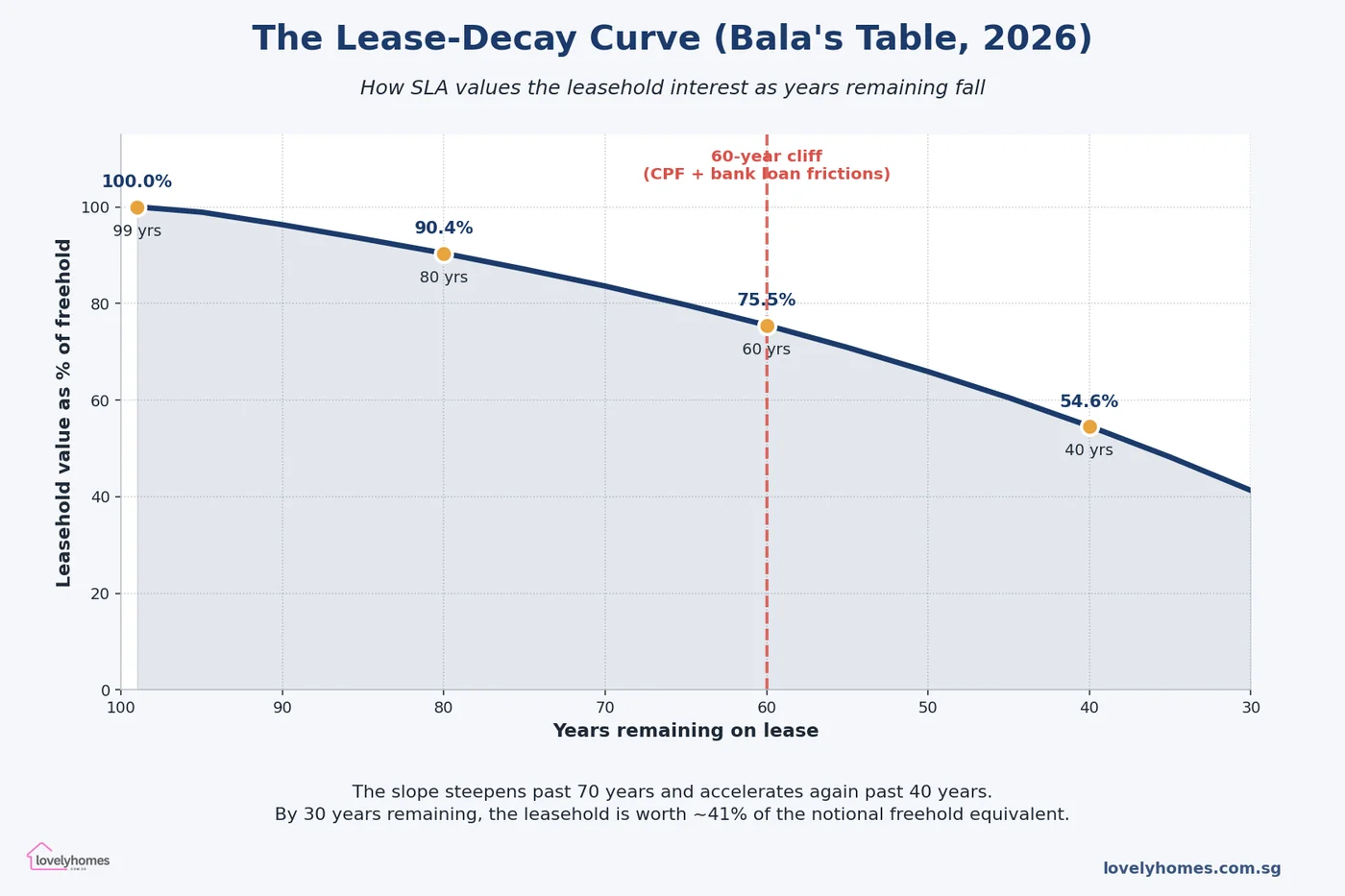

Figure 2: The Bala’s Table lease-decay curve as maintained by SLA. A 99-year leasehold retains 90% of its freehold-equivalent value at 80 years remaining, but only 75% at 60 years and 55% at 40 years.

Every Singapore valuer — including IRAS, SLA, CPF, banks and private surveyors — uses the SLA’s “Bala’s Table” as the reference for lease-hold-to-freehold value conversion. The table was named after Mr. Bala Subramaniam, then Chief Valuer, who introduced it in the early 1980s. It expresses the leasehold interest as a percentage of the equivalent freehold value at each remaining-years figure from 99 down to zero. The curve is not linear — depreciation accelerates as years remaining shrinks.

Key reference points from the 2026 version of the table:

99 years remaining: 100.0% of freehold

80 years remaining: ~90.4%

70 years remaining: ~83.6%

60 years remaining: ~75.5%

50 years remaining: ~65.9%

40 years remaining: ~54.6%

30 years remaining: ~41.3%

20 years remaining: ~26.6%

Two practical implications flow from this curve. First, the “depreciation drag” on a 99-year lease over the first 20 years is only about 10 percentage points — which in a market where underlying land values are rising 2–3% annually is easy to out-run. Second, the drag compounds rapidly past the 40-year mark, and by the time a lease is under 30 years remaining the leasehold interest is a fraction of the notional freehold and financing options have all but disappeared.

The Financing Cliffs: 95, 60 and 30 Years

Figure 3: The step changes in CPF usage, bank-loan tenure and HDB-loan eligibility as the years remaining on the lease decline.

Financing rules, not sentiment, drive most of the tenure-based price gap. CPF and bank underwriting both step down abruptly rather than smoothly. The three thresholds every buyer should know:

95 years remaining and above — Full CPF Ordinary Account usage, bank loan tenure up to 30 years or age 65, HDB loan eligible (subject to HDB Flat Eligibility letter). This is the baseline scenario for any brand-new launch.

60 years remaining — The first major cliff. CPF switches to a pro-rated Valuation Limit formula (the property must last the buyer until at least age 95, otherwise CPF usage is capped proportionally). Banks remain willing to lend but the 75% LTV may compress to 55% if the tenure extends past age 65. HDB loans remain available but with reduced LTV for older buyers.

30 years remaining — The exit wall. Most banks will decline to finance the purchase; those that do offer sub-50% LTV at punitive rates. CPF usage is effectively nil. HDB loans are not available. The market for the unit shrinks to cash-rich, typically older, buyers who are treating the purchase as a lifestyle-until-death asset.

The non-linearity is what makes tenure so consequential. A leasehold condo at 65 years remaining looks like a bargain on a pure price-per-square-foot basis — until the buyer realises they have a 5-year runway before the 60-year CPF cliff begins biting, which compresses the future pool of buyers who can take the unit off their hands.

A Fully-Worked Example: Freehold vs 99-Year in District 15

Consider two comparable 3-bedroom condo units in the Marine Parade area, both completed in 2026:

Unit A (99-year leasehold): S$2.3 million purchase price. 99 years at award — so the buyer gets 99 years of tenure starting from 2024 (when the plot was awarded).

Unit B (freehold): S$2.65 million purchase price. 15% premium to Unit A.

Assume both appreciate at 3% per annum nominal (a rough median for the Marine Parade submarket over a 20-year horizon). What does the tenure decision look like at the 20-year mark (2046)?

Unit A (now 79 years remaining): On Bala’s curve at 79 years, the leasehold interest is worth ~90% of the notional freehold equivalent. If the freehold equivalent has compounded at 3% for 20 years, it would be worth S$2.3m × 1.03^20 = S$4.15 million. The leasehold interest is then 90% of that “freehold equivalent” — but wait: the Bala curve already expresses value relative to freehold. So the 99-year unit in 2046 is worth roughly S$2.3m × 1.03^20 × (90%/100%) = S$3.74 million. Gain: ~63% over 20 years.

Unit B (still freehold): S$2.65m × 1.03^20 = S$4.79 million. Gain: ~81% over 20 years.

At the 20-year mark, the freehold unit has outperformed by about S$1.05 million in absolute terms and 18 percentage points in percentage gain. Adjust for the S$350,000 premium paid upfront (which could alternatively have earned ~4% in risk-free assets: S$350k × 1.04^20 = S$767k of opportunity cost), and the net advantage of the freehold is closer to S$300,000–S$400,000 over the period.

Is that worth it? For a buyer with a 20-year hold and no liquidity pressure, plausibly yes. For a buyer whose realistic hold is 8–10 years, the freehold premium may not recoup — the decay drag on a fresh 99-year lease is small over that horizon and the opportunity cost on the premium is live. This is the central trade-off: tenure mattered most for very long holds, very aged leases, or illiquid micro-markets.

SERS, VERS and the End-of-Lease Question

The elephant in the room for ageing 99-year stock is what happens at expiry. Three scenarios exist:

Lease runs its full 99 years and reverts. This is the default. The land returns to the state and the leasehold owner receives no compensation. For HDB flats the owner-occupier gets to live there until expiry (subject to upkeep and lease conditions). For private condos the same applies but the economic value in the final years approaches zero.

SERS (Selective En bloc Redevelopment Scheme). HDB identifies a small number of ageing blocks with high redevelopment potential and offers residents a replacement flat plus ex gratia compensation. Fewer than 5% of HDB blocks have been selected for SERS since the programme began in 1995. The policy framing is deliberately narrow — SERS is a planning tool, not a tenure safety net.

VERS (Voluntary Early Redevelopment Scheme). Legislated in 2018 and first offered to flats around the 70-year-remaining mark in the late 2020s, VERS is an opt-in mechanism: residents of an eligible precinct vote on whether to accept a negotiated pay-out in exchange for early redevelopment. Payouts are explicitly flagged as lower than SERS compensation. Our full VERS guide walks through the mechanics.

For private leaseholds, the equivalent mechanism is the en bloc (collective) sale, where 80% of owners by value (90% if the development is less than 10 years old) can force a sale to a developer who pays SLA a topping-up premium to reset the 99-year clock. The economics of en bloc sales change materially once a development crosses 60 years remaining — the topping-up premium escalates and developer IRRs tighten.

What Might Come Next — Policy Signals to Watch

Three forward-looking data points to monitor over 2026–2028:

The first VERS offers. The first precincts eligible for VERS are the 1970s HDB estates in Tiong Bahru, Queenstown and Marine Parade, now crossing the 55-year-remaining mark. The terms of the first offer (how much is paid, how much choice the resident has in replacement housing) will set the template for the next two decades. HDB has signalled a 2027–2028 rollout window.

Bala’s Table updates. SLA reviews the table periodically. The last meaningful revision was in 2019, when decay rates were nudged upward to reflect data from transactions in older leases. Another revision would have knock-on effects on CPF and bank LTV decisions.

Lease top-up policy for older private estates. A handful of pre-1970s private freehold estates have approached URA for lease-top-up schemes to extend or recalibrate tenure. If a standardised top-up mechanism emerges, the value of ageing 99-year private leaseholds could rise materially.

How Singapore’s Tenure System Compares Globally

Singapore is not alone in using long leaseholds for residential land. Hong Kong’s typical residential lease is also 99 years, with far more aggressive lease-modification and top-up activity (land premiums are a major source of government revenue). London uses a mix of long leaseholds (typically 99 or 125 years) on ex-local-authority and conversion flats, and reformed the Leasehold Reform, Housing and Urban Development Act in 2002 to allow leaseholders to compel freehold purchase (a process called “enfranchisement”) under specific conditions. Vancouver has true freehold in most of the metro area but faces its own lease-renewal issues with First Nations reserve land.

The distinctive feature of Singapore’s framework is the tightness of its financing-tenure coupling: HDB and CPF rules shape the buyer pool in a way that is more formulaic than in most peer jurisdictions. That makes Singapore’s Bala-Table decay an underwriting reality, not just a valuation convention — which is why it moves prices in step-changes around the 60- and 30-year thresholds.

Frequently Asked Questions

1. Is paying a 15% premium for a freehold condo ever worth it?

It depends almost entirely on your holding period and the opportunity cost of the premium. For a 25+ year hold in a supply-constrained micro-market, the math usually favours freehold — the Bala decay on the 99-year unit starts to bite after year 20, the buyer pool for the freehold unit remains wider, and the reinvested-premium scenario struggles to keep pace with property inflation. For a 5–10 year hold, the 99-year unit will typically outperform net of the premium: the Bala decay over that window is less than the opportunity cost of parking an extra S$300,000–S$500,000 in a lower-yielding asset.

2. Can I get a bank loan for a flat with less than 30 years remaining?

In practice, very rarely. Two or three private banks specialising in high-net-worth lending will consider it on bespoke terms — typically capped at 50% LTV, premium rates, short tenure and often secured against other assets. For standard retail buyers, the answer is effectively no. This is why the 30-year mark is called the exit wall: the market shrinks to a niche of cash-rich buyers and the price discount can be severe. The same logic drives why a 99-year unit sold at year 65 clocks a bigger-than-Bala discount — the market is already pricing in the financing thinning that bites at 60.

3. Does CPF allow me to buy an ageing leasehold flat?

Yes, but pro-rated. The CPF Board’s rule of thumb is that the property must be able to last the owner until at least age 95. If the remaining lease does not cover that, CPF usage is capped proportionally via the Valuation Limit/Withdrawal Limit formula. A 40-year-old buyer looking at a 65-year lease on a flat can usually still use full CPF. The same buyer at 55 looking at a 50-year lease will face a material haircut. Always run the CPF calculator before committing.

4. Are all HDB flats 99-year leasehold?

Yes. Every HDB flat — BTO, resale, SBF, DBSS — is 99-year leasehold from the date the block was first awarded (or in some older blocks, re-dated for the current lease commencement). The 99-year clock is set in stone; HDB does not sell freehold, and there is no mechanism to convert an HDB flat to freehold. The compensation schemes (SERS, VERS) are the only policy routes around the expiry, and they are discretionary.

5. How does tenure affect rental yields?

Less than most people expect. Rental markets price comparable units on amenity, location and unit quality; tenure is a distant factor because tenants are paying for the right to occupy, not to own. Comparable freehold and 99-year condos in the same submarket typically show rental yields within 10–20 basis points of each other. The yield difference is usually in favour of the leasehold (because the leasehold trades at a lower capital value), but the gap is small enough that investors optimising for yield rarely pick tenure as the decision variable.

6. What is the difference between lease commencement date and Temporary Occupation Permit (TOP) date?

The lease commencement date is the date on which the 99-year clock begins — typically when the land was awarded to the developer via the GLS programme. The TOP date is when the building is ready for occupation, usually 3–5 years after lease commencement for a condo and 6–8 years for an HDB BTO. The lease clock does not reset at TOP; a buyer moving into a newly-completed 2026 condo may already have only 95 years remaining on the lease because the plot was awarded in 2022. Always check the lease commencement date in the Sale & Purchase Agreement, not just the TOP.

7. Can a 99-year lease be extended?

For private residential land, yes — via the URA’s lease top-up scheme, which en bloc developers use routinely. The developer pays a topping-up premium to SLA and the lease resets to 99 years. Individual flat owners cannot unilaterally request a top-up; it must be done at the collective/development level. For HDB flats there is no top-up mechanism available to flat owners; the 99 years runs to expiry with only the SERS/VERS escape hatches as exceptions.

This article is an editorial guide for general information only and does not constitute legal, financial or valuation advice. The Bala’s Table figures and policy references used are illustrative and reflect the position as published by the Singapore Land Authority (SLA) and the Housing & Development Board (HDB) at the time of writing (April 2026); figures are periodically revised. For authoritative guidance consult the Singapore Land Authority, the HDB, the URA, a licensed property valuer and a qualified conveyancing lawyer before any property decision. Worked-example numbers are illustrative; actual outcomes depend on market conditions, the specific property, and financing available at the time of purchase.