The HDB Minimum Occupation Period (MOP) is the mandatory period you must physically occupy your HDB flat before you can sell it on the open market, rent out the entire flat, or purchase a second private residential property without incurring the full ABSD burden. MOP is administered by HDB (Housing and Development Board).

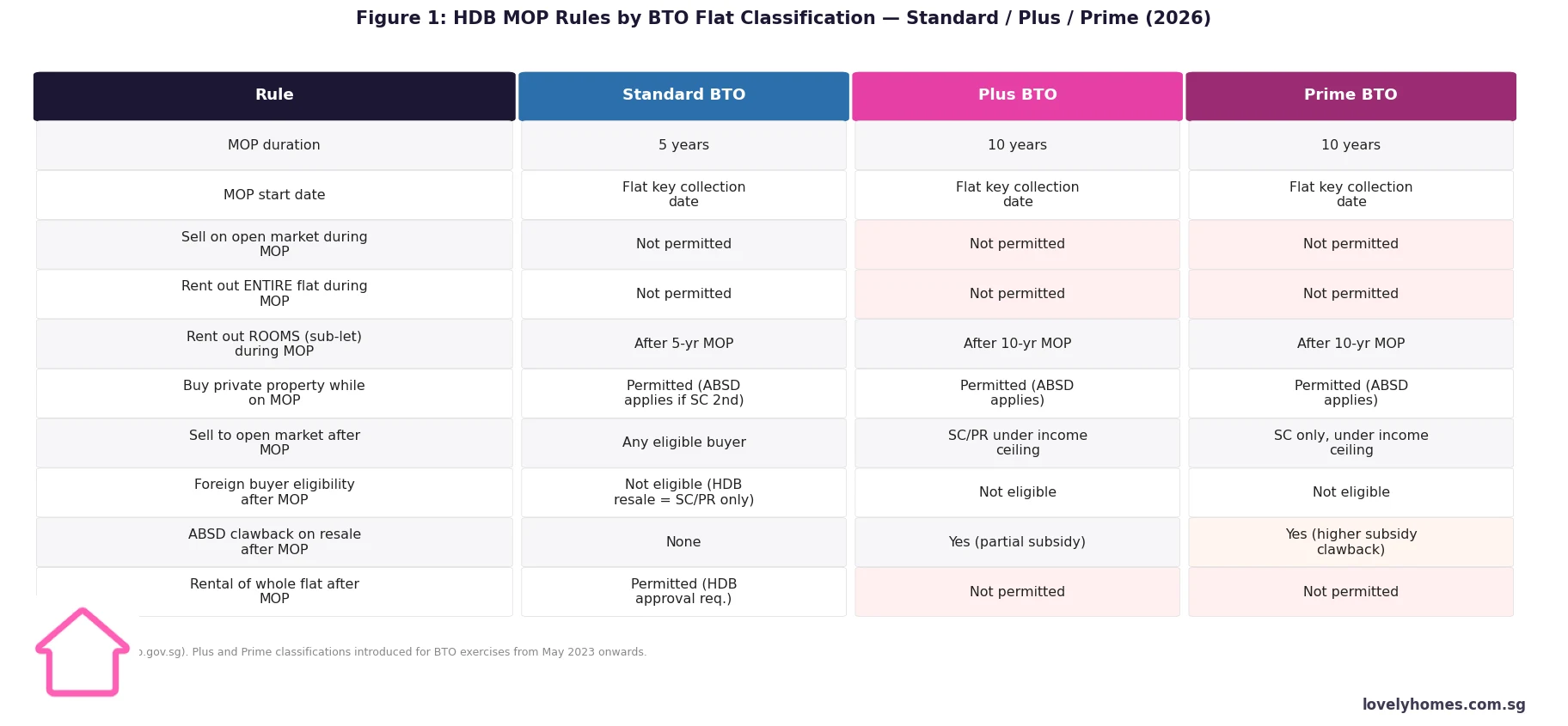

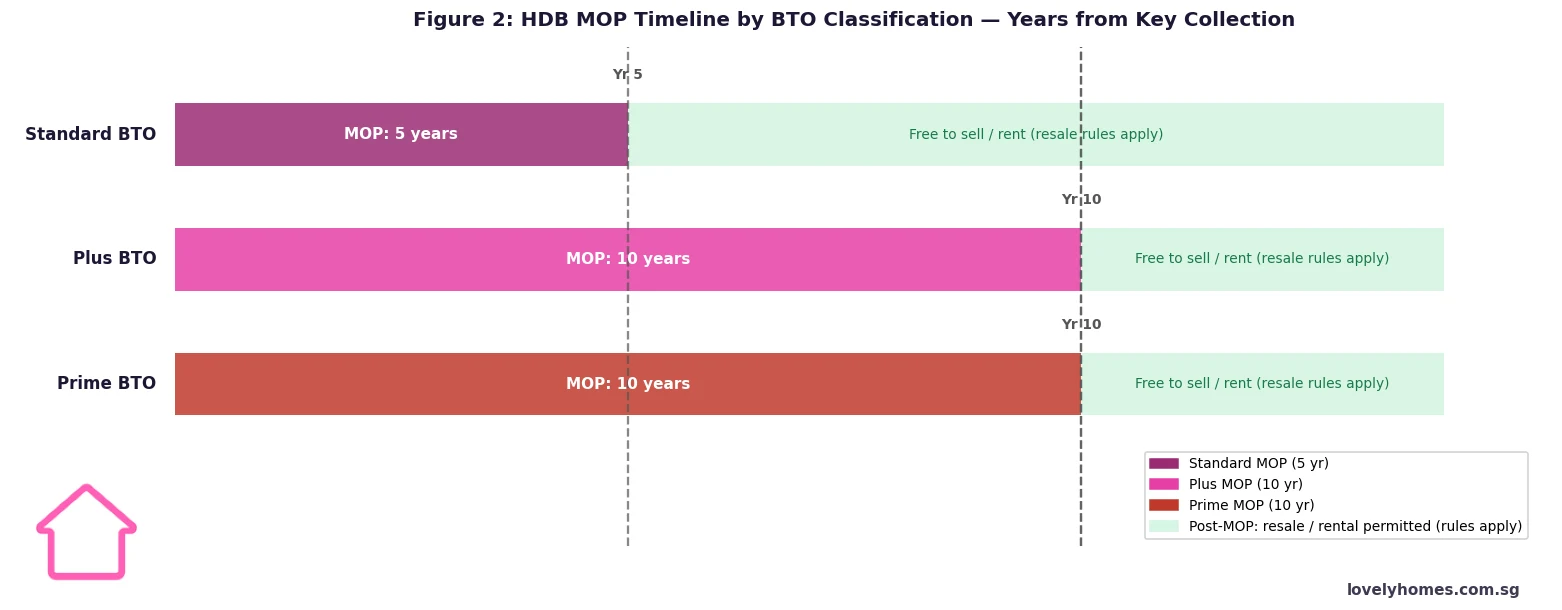

For Standard BTO flats, the MOP is 5 years from the date of key collection. For Plus and Prime BTO flats (introduced for BTO exercises from May 2023), the MOP is 10 years.

During the MOP, you cannot sell the flat, rent out the entire unit, or transfer ownership. You can, however, rent out individual rooms with HDB approval, and you may purchase private property (subject to ABSD).

After the MOP, Standard flat owners may sell to any eligible HDB buyer (SC or SPR). Plus flat owners must sell to SC or SPR buyers whose household income is within the prevailing income ceiling. Prime flat owners may only sell to Singapore Citizens whose household income is within the income ceiling.

Whole-flat rental after MOP is permitted for Standard flats (subject to HDB approval). It is not permitted at any time for Plus or Prime flats.

A subsidy clawback applies when Plus and Prime flats are sold on the open market — HDB recovers a portion of the housing grant and pricing subsidy. The clawback amount is higher for Prime flats.

The MOP clock starts from the date of key collection — not the date of BTO application, booking fee payment, or Temporary Occupation Permit (TOP). A flat collected in June 2024 has its Standard MOP expiry in June 2029.

What Is the MOP and Who Administers It?

The Minimum Occupation Period (MOP) is a statutory requirement under the Housing and Development Act, administered by the Housing and Development Board (HDB). It requires owners of HDB flats to physically occupy their flat for a minimum period before certain rights become available — primarily the right to sell on the open market, rent out the entire unit, or purchase a second private residential property.

The MOP exists for two complementary policy reasons. First, it ensures that subsidised HDB flats are used as genuine owner-occupied homes rather than short-term investment instruments. Second, it moderates the supply of resale HDB flats that enter the market at any one time, which helps to stabilise resale prices. The requirement has been part of Singapore’s public housing policy for decades, and HDB enforces it through its ownership records, which are cross-referenced against the buyer’s NRIC address for SC/SPR buyers.

Figure 1: HDB MOP Rules by BTO Classification — Standard, Plus and Prime (2026) | Source: HDB

Standard, Plus and Prime: The Three BTO Classifications

From the May 2023 BTO exercise onwards, HDB classifies all new BTO flats into one of three tiers based on location and subsidy level. This classification directly determines MOP length, post-MOP resale eligibility, rental rights, and subsidy clawback:

Standard flats are located in non-central, typically suburban estates (such as Tengah, Woodlands, Sembawang, and Punggol). They carry the lowest subsidies relative to market value and have the most permissive rules: 5-year MOP, resale to any eligible SC/SPR buyer, and whole-flat rental allowed after MOP with HDB approval.

Plus flats are located near transport nodes or commercial hubs, in estates that would otherwise be too pricey for first-timer buyers without additional subsidy. They come with a 10-year MOP, resale restricted to SC/SPR buyers within the prevailing income ceiling, and no whole-flat rental at any time.

Prime flats are located in the choicest sites — city-fringe, waterfront, or mature central estates like Kallang, Toa Payoh, and Marina South — where HDB provides the heaviest subsidies. They carry a 10-year MOP, SC-only resale (SPR buyers are ineligible), income ceiling restrictions, no whole-flat rental at any time, and the highest clawback rate.

Buyers are told which classification a flat falls under at the time of BTO application. The classification is permanently attached to the flat and does not change over time, even after resale. A Prime flat remains a Prime flat in every subsequent transaction.

Figure 2: HDB MOP Timeline by BTO Classification — Years from Key Collection (Singapore 2026)

What You Can and Cannot Do During the MOP

The MOP does not mean you are locked away from all activity — it specifically restricts disposal and whole-unit rental. The table below summarises key permitted and prohibited actions:

Activity

During MOP

After MOP (Standard)

After MOP (Plus/Prime)

Sell flat on open market

Not permitted

Permitted (SC/SPR buyers)

SC/PR (Plus); SC only (Prime); income ceiling applies

Rent out entire flat

Not permitted

Permitted (HDB approval)

Not permitted (ever)

Rent out rooms (sub-let)

Not permitted during MOP

Permitted (HDB approval)

Permitted (HDB approval)

Buy private property

Permitted (ABSD applies if SC 2nd property: 20%)

Permitted

Permitted

Transfer ownership (gift / divorce / death)

HDB approval case-by-case

Yes

Yes (subject to Plus/Prime resale rules)

Renovate / alter the flat

Permitted (HDB renovation permit)

Permitted

Permitted

Buying Private Property During the MOP

One of the most common questions from HDB flat owners is whether they can buy a private condominium before their MOP is up. The answer is yes — you are allowed to purchase private residential property in Singapore while your MOP is running. However, there are important financial consequences to consider.

If you are a Singapore Citizen owning an HDB flat (which counts as your first residential property) and you buy a private condo during the MOP, you are buying a second property. This means you pay 20% ABSD on the private property purchase. If you are an SPR, your second-property ABSD is 30%. The HDB flat itself remains subject to the MOP and cannot be sold until the MOP expires.

This means you will be servicing two housing loans simultaneously until the HDB can be sold — which requires careful TDSR planning. The TDSR cap of 55% applies across all outstanding loans. HDB loans (from HDB directly) and bank loans on HDB flats are both counted in TDSR. If the combined debt servicing ratio exceeds 55% when adding the private mortgage, financing for the private property may be declined.

What Happens When You Sell After the MOP

Once the MOP is fulfilled, the key restrictions are lifted — but resale rules still apply, especially for Plus and Prime flats:

Standard flats: May be sold to any eligible HDB resale buyer — SC or SPR, subject to standard HDB eligibility criteria (Ethnic Integration Policy quotas, family nucleus requirements, etc.). No income ceiling on the buyer.

Plus flats: May only be sold to buyers whose household income does not exceed the prevailing income ceiling (currently S$14,000/month for families, S$7,000 for singles). SPR buyers are eligible. A subsidy clawback is deducted from the sale proceeds on the first open-market resale.

Prime flats: May only be sold to Singapore Citizen buyers (SPR buyers are not eligible) whose household income does not exceed the income ceiling. The subsidy clawback rate is higher than for Plus flats and is also deducted from the first open-market resale proceeds.

The subsidy clawback is calculated as a percentage of the resale price (or market value, whichever is higher) and is paid to HDB at the point of resale. HDB has not publicly released a fixed clawback percentage table; the exact rate is determined and communicated at the time of application. This is intended to recover some of the subsidy advantage enjoyed by Plus/Prime buyers while still allowing them a fair profit on genuine capital appreciation.

The MOP and CPF Accrued Interest

When you sell an HDB flat after the MOP, any CPF funds used to purchase the flat (including the option fee, downpayment, and monthly mortgage instalments paid from your CPF Ordinary Account) must be refunded to your CPF accounts — along with accrued interest at the CPF OA interest rate (currently 2.5% per annum). This accrued interest represents what your CPF savings would have earned had they not been used for housing. On a long MOP (10 years), accrued interest can be substantial and reduces the net cash proceeds from the sale.

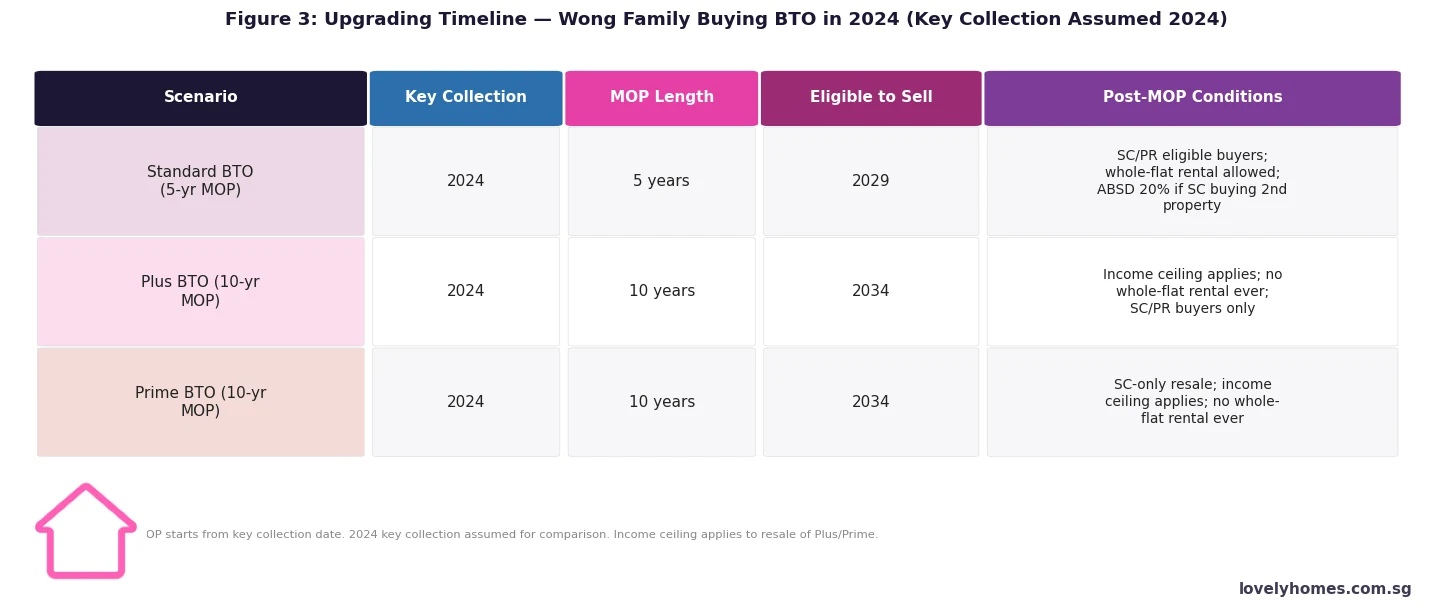

Worked Example: The Wong Family and the MOP Decision

Mr and Mrs Wong, both Singapore Citizens, purchase a 4-room BTO flat in Bishan (classified as a Plus flat) in June 2024. Key collection is in June 2024. Their household income is S$9,000/month. The purchase price is S$550,000.

Over the 10-year MOP, if the flat appreciates from S$550,000 to S$800,000 (a not unreasonable assumption for a Plus-classified Bishan flat), the Wongs would make a nominal gross gain of S$250,000. From this, HDB deducts the clawback (amount TBD at point of sale), plus CPF refund with accrued interest. On a S$550,000 purchase with 25% CPF downpayment (S$137,500) at 2.5% CPF OA rate over 10 years, accrued interest alone would be approximately S$38,700 — reducing net cash-in-hand from the sale. This is still a solid return, but buyers should model it carefully before factoring in the Plus flat subsidy as pure profit.

What This Means for HDB Buyers in 2026

The 10-year MOP for Plus and Prime flats is a significant commitment. A buyer collecting keys in 2026 cannot sell their Plus or Prime flat until 2036 at the earliest. Over that decade, Singapore’s property market will go through multiple cycles, interest rate shifts, and policy changes. Buyers who select Plus or Prime flats primarily because of the lower purchase price — and not because they genuinely intend to occupy the flat for 10 years — may find themselves in a difficult position if circumstances change (job relocation overseas, family expansion, divorce).

For those who do plan to stay, the Plus and Prime schemes deliver real value. A Prime flat in a central location at a subsidised price, occupied for 10 years with a no-rental restriction, is likely to appreciate meaningfully in absolute terms even after clawback. The restriction is the price of the subsidy.

What Might Come Next

The May 2023 introduction of Plus and Prime classifications represented a significant shift from the old Mature/Non-Mature estate binary. The April 2023 announcement also removed the ability of EC buyers to use the Deferred Payment Scheme from May 2026 — suggesting the government continues to tighten across all public and quasi-public housing tiers. Any further changes to MOP duration are unlikely in the near term given that the 10-year Plus/Prime MOP is relatively new and the government will want to assess its impact before adjusting. The resale income ceiling may, however, be revised upwards over time to track median income growth in Singapore.

When does the MOP start — from key collection or from BTO ballot application?

The MOP starts from the date of key collection — not the date of BTO application, not the ballot exercise date, and not the date you pay the option fee or sign the lease agreement. The key collection date is when you physically receive the keys to your flat and formally take possession. This date is recorded by HDB and serves as the MOP commencement date. For a Standard flat collected in July 2024, the MOP expires in July 2029. For a Plus or Prime flat collected in the same month, it expires in July 2034.

Can I rent out rooms in my HDB flat while the MOP is running?

No. During the MOP, you may not rent out any part of your flat — neither the entire unit nor individual rooms. Room rental (sub-letting) is only permitted after the MOP has been fulfilled and only with HDB’s prior written approval. After the MOP, Standard flat owners may rent out rooms or the entire flat (with HDB approval); Plus and Prime flat owners may rent out rooms after the MOP but may never rent out the entire flat under any circumstances.

What happens if I need to move overseas for work during the MOP?

If you need to work overseas temporarily, you must continue to maintain your HDB flat as your Singapore residence — meaning a family member must continue to reside in the flat, and you must return periodically. You cannot rent out the flat during the MOP even if you are overseas. If your overseas stint is long-term and the flat will genuinely be unoccupied, you should consult HDB directly. Abandoning the occupancy requirement during the MOP can result in HDB compulsorily acquiring the flat at a below-market price under the Housing and Development Act — a severe consequence that buyers should be aware of.

Can I buy a private condo while my HDB MOP is still running?

Yes. Purchasing a private residential property while your HDB MOP is outstanding is permitted. However, since your HDB flat counts as your first residential property, the private condo purchase is classified as a second property for ABSD purposes. A SC pays 20% ABSD on the private condo. An SPR pays 30%. You must also have the financial capacity to service both housing loans simultaneously and remain within the 55% TDSR cap. Many HDB owners choose to exercise this option a year or two before their MOP expires, so the HDB can be sold shortly after the MOP milestone — reducing the period of dual-loan exposure.

What is the subsidy clawback for Plus and Prime flats, and when is it paid?

The subsidy clawback for Plus and Prime flats is paid to HDB at the point of the first open-market resale (i.e., the first resale transaction after the MOP). It is deducted from the sale proceeds before any balance is paid to the seller. The clawback is calculated as a percentage of the resale price or market valuation (whichever is higher). HDB has not published a fixed percentage table publicly; the exact rate is communicated in the flat purchase document at the time of BTO booking and is specific to the flat’s classification and location. The clawback only applies to the first open-market resale — subsequent owners of a Plus or Prime flat do not face an additional clawback when they eventually sell.

Do MOP rules apply to HDB flats purchased on the open resale market?

Yes. When you purchase an HDB resale flat — whether Standard, Plus, or Prime — the MOP requirement applies afresh from the date you collect the keys. A Standard resale flat has a 5-year MOP from your key collection date; a Plus resale flat has a 10-year MOP; and a Prime resale flat has a 10-year MOP. The classification (Standard, Plus, Prime) of the flat follows it through all transactions. You cannot shorten the MOP on a resale flat because the previous owner already fulfilled their MOP.

Can an SPR buyer purchase a Plus or Prime HDB flat on the open resale market?

For Plus flats: yes, subject to the income ceiling (S$14,000/month household income) and standard SPR eligibility criteria. For Prime flats: no — Prime flats may only be resold to Singapore Citizens (not SPR). This restriction applies to every resale of a Prime flat in perpetuity, not just the first resale. SPR buyers wishing to purchase Plus flats must also form an eligible family nucleus (e.g., SC/SPR family or SPR household of two or more) to qualify under HDB’s resale eligibility framework.

Disclaimer: This article is for general information only and does not constitute legal or financial advice. HDB rules, MOP durations, clawback rates, and eligibility criteria are subject to change by HDB and the Ministry of National Development. Always verify the latest requirements at hdb.gov.sg and consult HDB directly or a licensed HDB resale agent for guidance specific to your situation. All figures and scenarios are illustrative and based on publicly available data as at 16 May 2026.

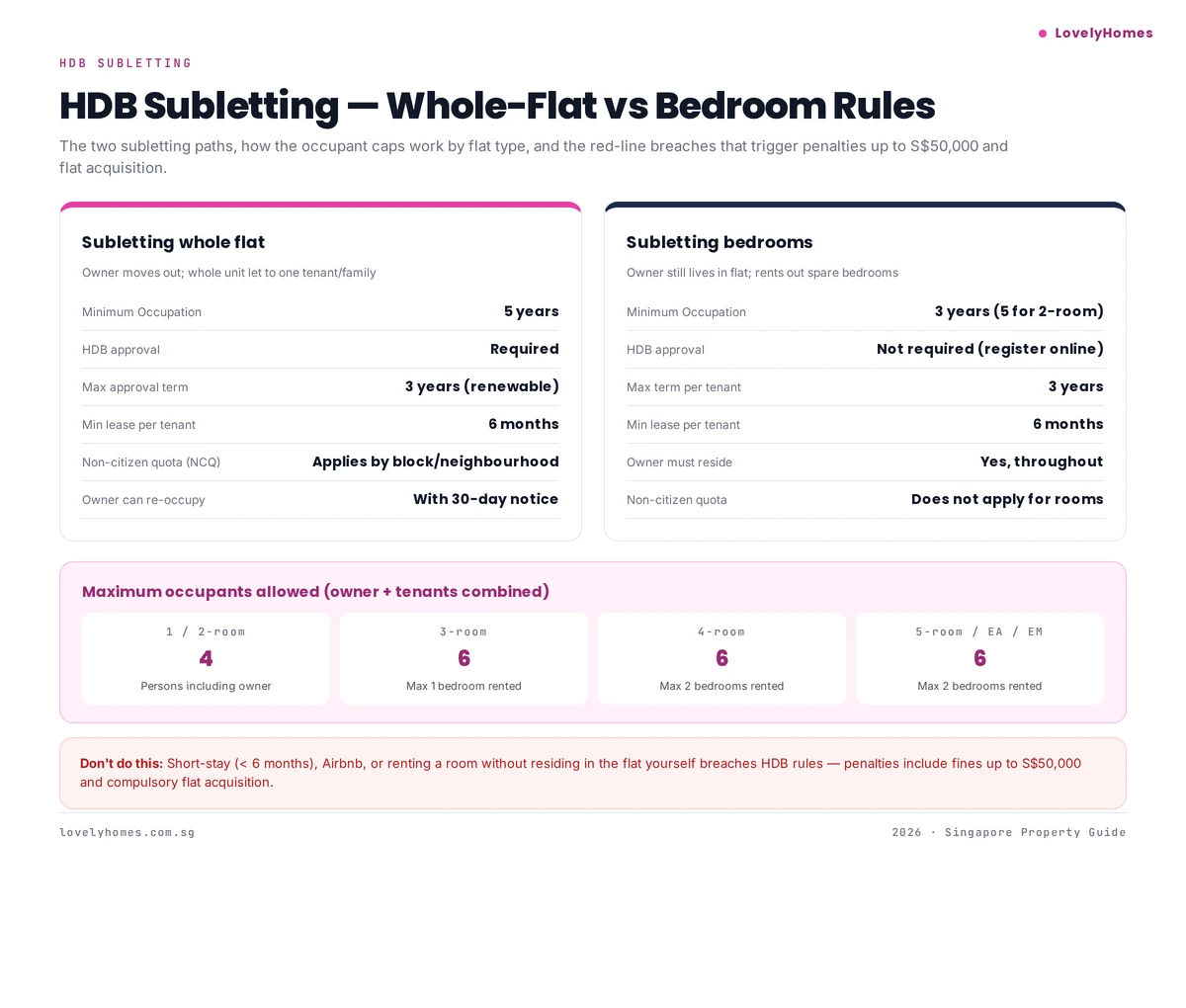

HDB owners can sublet whole flat after 5-year MOP (HDB approval required, max 3 years per approval, non-citizen quota applies) or sublet bedrooms after 3-year MOP (5 years for 2-room, no HDB approval needed but online registration required, owner must still live in the flat). Minimum lease is 6 months per tenant — no Airbnb, no short-stay. Breaches risk fines up to S$50,000 and compulsory flat acquisition.

HDB subletting is the single most rule-bound corner of the Singapore rental market. The policies exist because HDB is public housing, funded by subsidies and grants, and subletting concessions try to balance owner flexibility with social objectives (owner-occupation, ethnic integration, housing supply). The rules are enforced — HDB audits tenanted flats and compulsory acquisition is a real outcome for breaches.

This guide lays out the two subletting paths (whole flat vs bedrooms), the occupant caps, and the red lines you cannot cross.

For broader landlord obligations (licensing, tax, TA clauses), see our landlord’s guide. For more context on HDB rules generally, read our MOP rules guide.

Whole-flat vs bedroom subletting, occupant caps, and breach penalties

The two subletting paths at a glance

Rule

Whole-flat subletting

Bedroom subletting

MOP required

5 years (all flat types)

3 years (5 yrs for 2-room)

HDB approval

Required before tenancy

Register online; no approval needed

Owner must occupy

No — owner can live elsewhere

Yes — owner must still live in the flat

Max approval term

3 years per renewal

3 years per tenant

Min lease per tenant

6 months

6 months

Non-citizen quota

Applies (block + neighbourhood)

Does not apply

Ethnic quota (EIP/SPH)

Applies

Applies in certain cases

Whole-flat subletting in depth

Whole-flat subletting is allowed only after the full 5-year Minimum Occupation Period from key collection. Apply via HDB InfoWEB with:

Tenant’s NRIC/FIN and work/student/dependent pass

Proposed tenancy term and rent

S$20 non-refundable admin fee

Declaration of the owner’s temporary residential address

HDB typically approves within 2–3 weeks. The approval is valid for up to 3 years and can be renewed. Non-Citizen Quota (NCQ) may block some rentals if the block or neighbourhood has already reached its foreigner cap.

Bedroom subletting in depth

Bedroom subletting is simpler because the owner stays — HDB treats it more like house-sharing than a full rental. Register the tenant’s details on HDB InfoWEB within 7 days of the tenancy starting. No formal approval needed.

Key constraint: the occupant cap includes both the owner’s household and any subletted bedroom tenants.

Maximum occupants by flat type

Flat type

Max occupants

Max bedrooms rented

1-room / 2-room

4

1 bedroom

3-room

6

1 bedroom

4-room and above

6

2 bedrooms

Where the occupant cap used to be based on flat size, HDB moved to a hard cap of 6 persons in 2024 for most flat types to curb overcrowding and nuisance complaints.

What counts as a breach

Red-line breaches that trigger HDB enforcement:

Short-stay rentals under 6 months — includes Airbnb, Booking.com short lets, weekend stays, room-by-night.

Subletting the whole flat before MOP.

Subletting rooms before 3-year MOP, or 5-year for 2-room flats.

Subletting rooms without the owner residing in the flat.

Exceeding the occupant cap (even by one person).

Letting to tenants without a valid pass or to unauthorised nationalities.

Not registering bedroom subletting on HDB InfoWEB.

Accepting rental payments in cash without records (complicates dispute resolution and IRAS audits).

Penalties

HDB’s enforcement ladder, from lightest to most severe:

Written warning for minor paperwork lapses.

Financial penalty — fines up to S$50,000.

Compulsory acquisition of the flat for serious or repeated breaches. Owner receives compensation at HDB’s determined valuation — typically below market.

Debarment from buying another HDB flat or applying for HDB rental.

Frequently asked questions

Can I rent my HDB flat on Airbnb even if it’s for friends only?

No. The 6-month minimum lease rule applies regardless of who the tenant is. Any stay below 6 months is a breach, even if unpaid.

Can I sublet while I’m overseas for work?

Yes — this is a common use case for whole-flat subletting after MOP. You need HDB approval and must notify HDB of your overseas address. You can return any time.

Does bedroom subletting affect my PR sponsorship or home loan?

No direct effect on PR or citizenship applications. It may affect your TDSR if banks treat rental income as supplementary (they typically use 70–80% of the rent in TDSR calculations).

What’s the non-citizen quota?

HDB caps the percentage of non-Malaysian foreigners who can occupy flats in a block and neighbourhood. If your block has hit the cap, HDB will reject your subletting application until a spot opens up.

Disclaimer

This guide is for general information only. Singapore’s rental rules, HDB policies, and IRAS stamp duty rates change periodically. Always verify against the HDB, URA and IRAS websites before signing a lease or filing with IRAS. LovelyHomes is not a licensed property agent or tax adviser. For personalised advice, please engage a registered CEA agent or a qualified tax professional.

Fresh Start Housing Scheme gives second-timer families with at least one child (aged 16 or below) who are living in rental or transitional housing a pathway to buy a 2-room Flexi short-lease BTO flat with up to S$75,000 of Fresh Start Grant. The scheme comes with a 20-year Minimum Occupation Period and mandatory financial counselling.

Fresh Start is Singapore’s second-chance scheme: a narrow but meaningful door back into HDB ownership for families who have already owned a flat, fallen out of ownership, and are raising children in rental housing. It is small in numbers — HDB allocates only a few hundred flats to it each year — but it is consequential for the families who qualify.

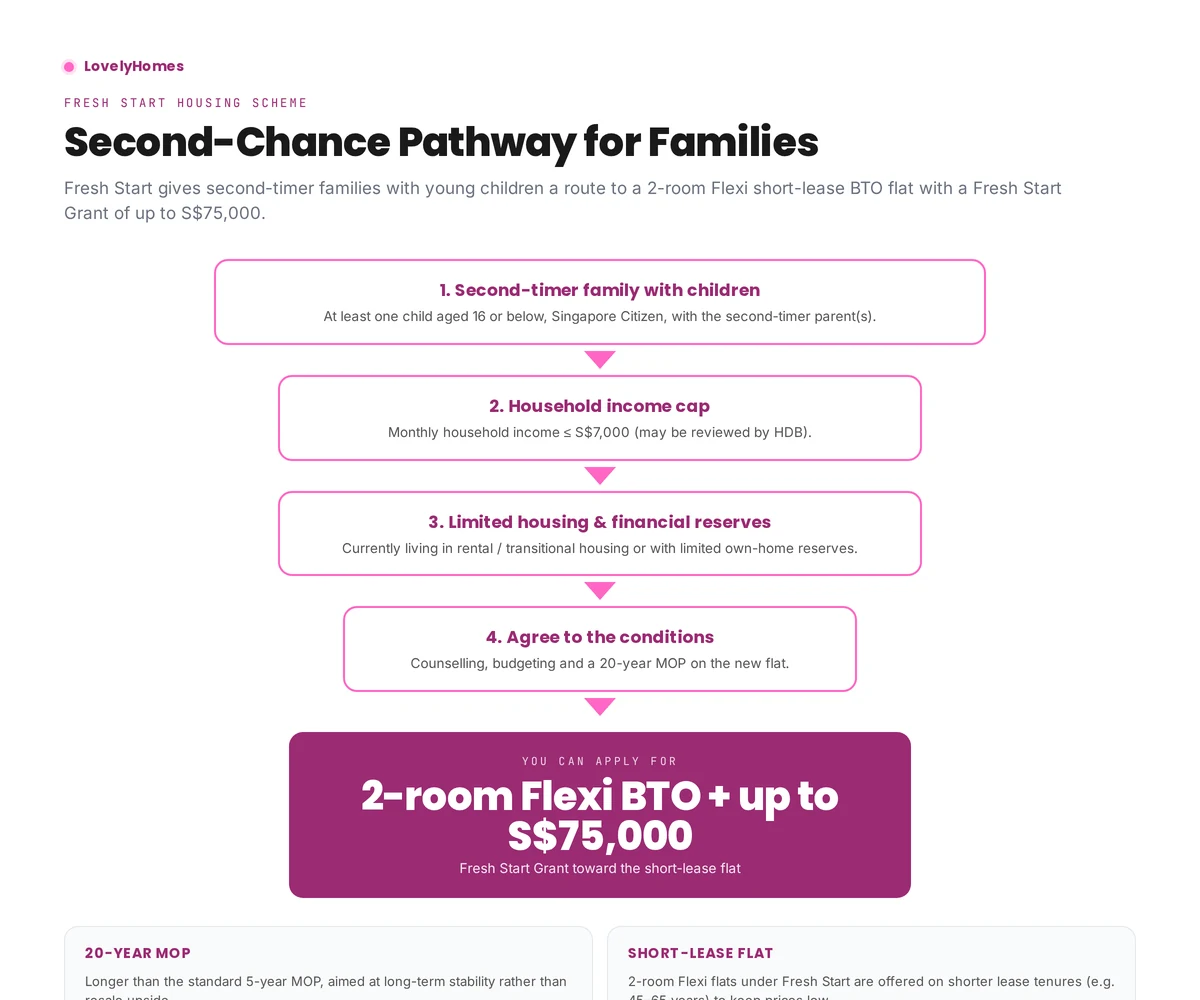

The four eligibility gates and the 2-room Flexi + S$75,000 Fresh Start Grant outcome.

Who Fresh Start is designed for

The scheme is aimed at low-income, second-timer families with young children who are currently in public rental flats or transitional housing under HDB’s schemes like the Interim Rental Housing Programme. HDB’s intention is to help the family stabilise rather than to offer a general upgrade path, so the scheme comes with heavier conditions than standard BTO.

The four eligibility gates

Second-timer family with children. At least one SC child aged 16 or below, living with the applicant family nucleus. Both parents — or a single-parent applicant — must have previously owned a flat.

Household income cap. Monthly household income is typically ≤ S$7,000 (HDB reviews this on a case-by-case basis).

Limited housing & financial reserves. The family is currently in public rental, transitional housing, or otherwise living with very limited financial and housing reserves.

Agree to the conditions. Mandatory counselling, a budgeting programme, and a 20-year MOP on the new flat.

The Fresh Start Grant

The grant is up to S$75,000, disbursed in stages rather than all at once. The structure HDB has published:

Disbursement stage

Amount

On key collection

S$25,000

Over the following years (as the family remains in the flat)

Up to S$50,000

Total

Up to S$75,000

The phased structure is intentional: it nudges families to stay in the flat long enough to stabilise, rather than viewing Fresh Start as a quick cash-out.

What you actually buy

Fresh Start families buy a 2-room Flexi flat on a short-lease tenure (often 45 to 65 years, depending on the applicant’s age and the precinct). Short leases keep prices affordable, but they also mean that the flat does not carry the same long-term resale upside as a standard 99-year flat.

The 20-year MOP trade-off

The 20-year Minimum Occupation Period is the biggest non-monetary cost. You cannot sell the flat on the open market or rent out the whole flat for 20 years. That is four times the standard MOP and is a clear signal that the scheme is designed for long-term stability, not trading.

Breaking the MOP without HDB’s approval has serious consequences, including the possibility of HDB repossessing the flat. HDB does allow sale back to HDB in genuine hardship cases, with grant clawback.

How to apply

Applications run through HDB’s Housing & Development Office (HDO) rather than the usual BTO portal. The process is more involved than a regular BTO application:

Approach HDB via your rental flat officer or a Family Service Centre.

Counselling & budgeting assessment over several sessions — non-negotiable.

Flat offer once HDB confirms eligibility and matches you to an available 2-room Flexi unit.

Financial plan signed off — HDB makes sure the family can afford the mortgage plus utilities.

Key collection with the first S$25,000 disbursed into CPF.

Frequently asked questions

Can Fresh Start applicants apply for other HDB grants?

The Fresh Start Grant is designed as the main support for this scheme. Stacking with other grants (like EHG) is generally not available — HDB consolidates the support into the Fresh Start Grant.

What happens if circumstances improve after I move in?

The phased disbursements continue as long as you remain in the flat and comply with the scheme conditions. Rising income does not trigger clawback.

Is the 20-year MOP negotiable?

No. It is a scheme condition, not a default. HDB considers early sale only in genuine hardship cases.

Can single parents qualify?

Yes. A single-parent household with a SC child qualifies subject to the same income and reserves tests.

This guide is for general information only and is accurate as of April 2026. CPF grants, scheme quantum and eligibility rules are set by HDB / the Ministry of National Development and can change. Always confirm current rules on the HDB Flat Portal or with an HDB officer before committing. We are not a financial or legal advisor.

The Minimum Occupation Period (MOP) is the single most important HDB rule for any flat owner. It governs when you can sell, when you can rent out the whole unit, and even when you can buy a second property. This 2026 guide explains the 5-year standard rule, how the clock starts and when it can pause, the rare exceptions, and exactly what unlocks once MOP is fulfilled.

For the official rules, see the HDB MOP page. This article explains what those rules mean in practice.

Quick Answer — MOP in 60 Seconds

Standard MOP: 5 years from key collection — applies to most BTO, SBF, and resale flats.

Plus and Prime flats: 10 years MOP (introduced 2024).

Clock starts the day you legally take possession, not the day you apply or ballot.

Clock pauses when you are overseas for 6 months or more continuously.

Exceptions: divorce, death of spouse, financial hardship — case by case with HDB.

MOP unlocks the right to sell, rent the whole flat, and buy private property without disposing of the HDB.

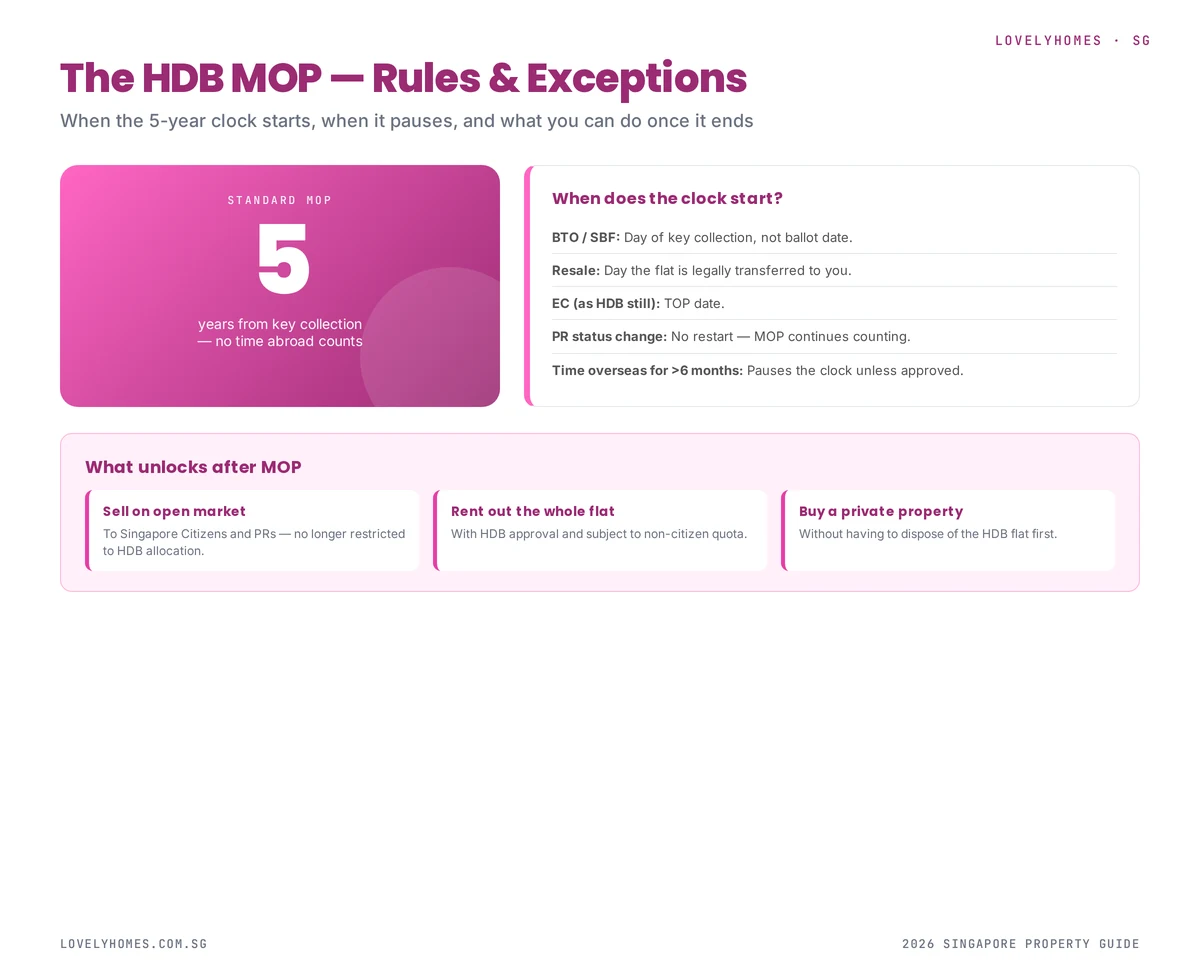

The standard MOP is 5 years — the clock pauses for extended time overseas, and the consequences of breach are severe.

What Is MOP?

The Minimum Occupation Period is the number of years you must live in your HDB flat before you can sell it, rent it out as a whole unit, or use it to qualify for a second home purchase. It is HDB’s tool for ensuring public housing subsidies flow to people who actually need a home — not to speculators who buy and flip.

MOP is personal: it is the owner who must have occupied the flat for the period, not just anyone. If all listed owners have moved out within MOP (say, for overseas work), the clock pauses until at least one owner returns.

The 5-Year Standard

For most HDB flats — standard BTO, resale, SBF — the MOP is 5 years. This applies to:

All BTO flats except Plus and Prime

SBF (Sale of Balance Flats) purchases

Resale flats purchased on the open market

Executive Condominiums (for the EC-as-HDB period)

DBSS (Design, Build, Sell Scheme) flats

The 10-Year MOP: Plus and Prime Flats

Introduced in 2024, the revised BTO classification creates two new categories with extended MOP:

Plus flats

Plus flats are located in choice mature-estate areas that are not classified as “core central”. They have:

10-year MOP from key collection

Future-buyer income ceiling applied on resale (restricts buyer pool)

Subsidy clawback at resale computed by HDB

Prime flats

Prime flats are in genuinely core central locations (Tanjong Pagar, Queenstown, Rochor, etc.). They have all of the Plus restrictions, plus an even higher subsidy clawback at resale.

When Does the Clock Start?

The MOP clock starts on the day of key collection, not on:

The ballot date of your BTO application

The signing of the Lease Agreement

The purchase completion date (for resale, these are the same day)

The date you actually move in (if different from key collection)

You can verify the exact date on your HDB My Home record via Singpass. It is worth noting the date somewhere — the 5th anniversary is the earliest you can register Intent to Sell.

When Does the Clock Pause?

MOP is an occupation requirement. If no one who owns the flat is actually living in it for an extended period, the clock pauses. The standard trigger is 6 continuous months overseas by all listed owners.

How HDB tracks overseas status

Under the Income and Property Declaration required during resale applications, HDB cross-references ICA travel records. If your records show you were overseas for a year during MOP, your effective MOP date is pushed back by a year.

What counts as “overseas”

Overseas employment (with or without HDB approval)

Study overseas

Extended travel or sabbatical

Caring for family overseas

Short trips (weeks), business travel, holidays, and study leave that total less than 6 months per calendar year generally do not pause the clock.

Exceptions to the 5-Year Rule

HDB permits early disposal in a narrow set of circumstances:

1. Divorce

If the owners divorce within MOP, HDB may approve early disposal if neither party can afford to keep the flat. Ownership can also be transferred to one party under a court order.

2. Death of a spouse or co-owner

Surviving owner(s) can retain the flat without breach. If the surviving household falls below the minimum family nucleus requirement, HDB may require the flat to be sold.

3. Severe financial hardship

Documented financial distress (bankruptcy, serious illness, prolonged unemployment) may qualify for early disposal. Case-by-case with HDB’s Financial Assistance team.

4. Change in family circumstances

Marriage resulting in ineligibility under the original scheme, or purchase of a new flat under a scheme that requires disposal of the existing flat, may qualify.

What Unlocks Once MOP Is Fulfilled

1. Sell on the open market

You can register Intent to Sell and market the flat to Singapore Citizens and PRs (subject to the block’s EIP cap).

2. Rent out the whole flat

Previously you could only rent individual rooms while occupying the flat. After MOP, with HDB approval, you can rent the entire unit. Subletting quota rules (e.g. 1 non-citizen cap for non-Malaysian foreigners) still apply.

3. Buy private property without disposal

Before MOP, if you wanted to buy a private property, you would need to dispose of the HDB within 6 months of TOP of the new property. After MOP, you can hold both — subject to ABSD and TDSR implications. See our ABSD guide.

4. Apply for a second BTO or resale

Post-MOP, if you sell the original flat, you can re-enter the BTO / resale market as a second-timer buyer (with reduced grant eligibility but still eligible).

Consequences of Breaching MOP

Breaching MOP is treated seriously by HDB. Possible consequences include:

Compulsory acquisition of the flat at HDB’s administered price — typically below market value.

Financial penalty equivalent to the subsidy or concessionary loan received.

Banning from future HDB purchases for a period of years.

Referral for prosecution in cases of fraudulent misrepresentation (e.g. fake tenancy agreements).

The most common accidental breach is renting out the whole flat before MOP. If you must be overseas during MOP, sublet only individual rooms with HDB approval.

MOP and Your Financial Planning

Knowing your exact MOP date lets you plan key life decisions:

Upgrading to a condo? Target MOP + condo launch cycle for maximum CPF refund and minimum ABSD complexity.

Moving for work? Understand how overseas time pauses the clock so you don’t miss MOP by years.

Family expansion? Post-MOP flexibility (sell, rent, or buy additional property) enables better choices.

Rental income? Model the income stream against the HDB subletting quota rules.

FAQ — HDB MOP 2026

What is the shortest possible MOP?

5 years for standard flats. Plus and Prime flats are 10 years. There is no way to reduce the MOP shorter than these limits through any scheme.

Does becoming a PR after buying restart my MOP?

No. Citizenship status changes do not restart the MOP clock. The 5 years begin from key collection regardless.

Can I count time spent at my parents’ house toward MOP?

No. MOP requires occupation of your specific flat. Time spent elsewhere, even with family, does not count.

Does the MOP transfer to a new co-owner I add later?

Adding an owner does not restart the clock, but the added owner’s MOP is measured from the date they become an owner. This matters if they intend to use MOP completion for their own eligibility (e.g. to apply for a second property).

Can I sell the flat through a private sale after MOP, to avoid HDB involvement?

No. All HDB flat transactions must go through HDB’s resale process. Private sales of HDB flats outside the HDB framework are not permitted.

Disclaimer: This is general information, not legal advice. HDB evaluates MOP edge cases on a case-by-case basis — if your situation is unusual, contact HDB directly before making any plans.