Pasir Ris Neighbourhood Guide Singapore 2026: Property Prices, Schools, MRT and Investment Outlook

Pasir Ris Neighbourhood Guide Singapore 2026: Property Prices, Schools, MRT and Investment Outlook

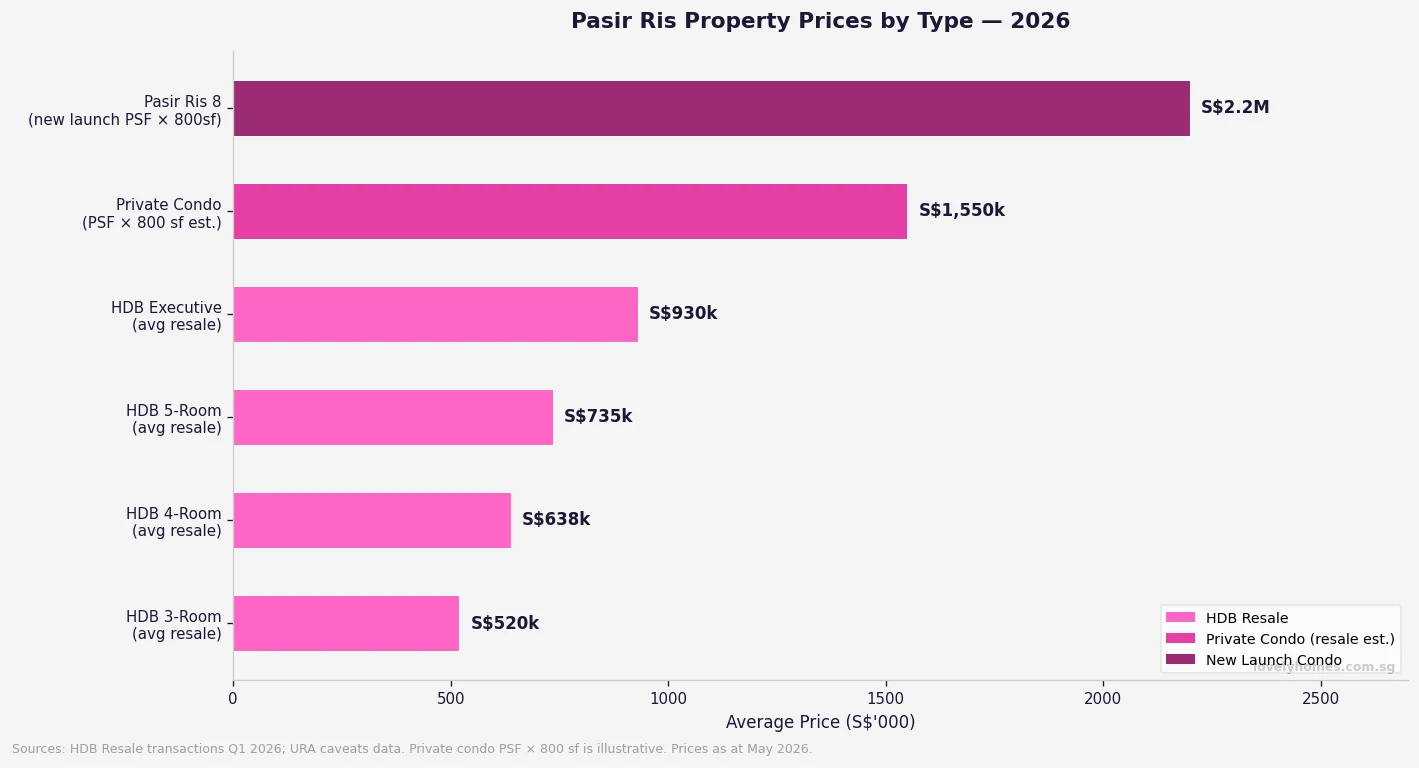

- HDB 4-room resale: median S$638,000; 5-room: S$735,000; Executive: S$930,000

- Private condo (resale): S$1,550–S$1,900 psf; Pasir Ris 8 (new launch): S$1,934–S$3,728 psf

- MRT: EW1 Pasir Ris on East West Line today; Elias MRT on Cross Island Line (Punggol Extension) expected ~2032

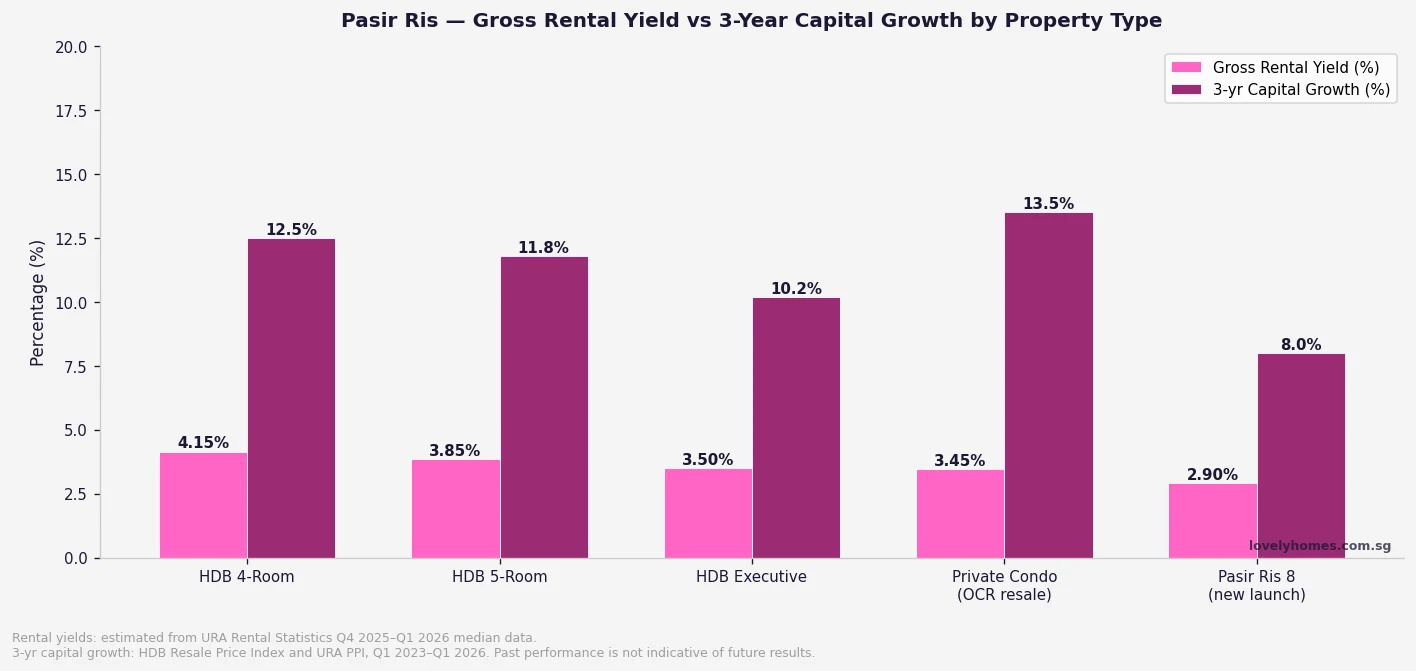

- Gross rental yield (HDB 4-room): ~4.1–4.2% — among the higher-yielding OCR estates

- ~1,200–1,400 HDB flats reaching MOP in Pasir Ris during 2026 — creating upgrader demand

- Pasir Ris Park (70 ha), White Sands, Downtown East and Changi General Hospital all within the estate

- Investment catalyst: Elias MRT, Neighbourhood 8 precinct development, and growing CRL network

Pasir Ris sits at the far east of Singapore — coastal, spacious, and historically associated with family living rather than prestige addresses. But in 2026, that picture is changing. Cross Island Line infrastructure is being built, a new Neighbourhood 8 precinct is taking shape around the former MINDEF land near Elias Road, and Pasir Ris 8 — the integrated development at the MRT station — has firmly repriced what private property in this estate can command. For HDB upgraders watching MOP numbers and investors hunting yield in the Outside Central Region, Pasir Ris is an estate worth examining carefully.

This guide covers everything you need to know about buying, renting, or investing in Pasir Ris in 2026 — from exact resale prices by flat type, to the MRT connectivity timeline, to a worked upgrader cost analysis.

Property Prices in Pasir Ris — 2026 Overview

Pasir Ris is predominantly an HDB estate, with approximately 50,600 public housing flats across the town. Private residential supply is anchored by Pasir Ris 8 (the integrated development directly above Pasir Ris MRT station) and a small number of older condominiums and landed houses along the coastal and park-fronting streets.

| Property Type | Typical Price Range | Median / Avg | Notes |

|---|---|---|---|

| HDB 3-Room (resale) | S$400k – S$620k | ~S$520k | Older stock; strong rental demand from singles |

| HDB 4-Room (resale) | S$548k – S$720k | ~S$638k | Most traded flat type; strong median |

| HDB 5-Room (resale) | S$650k – S$850k | ~S$735k | Larger format; MOP supply wave lifting liquidity |

| HDB Executive / Jumbo (resale) | S$800k – S$1.08M | ~S$930k | Limited supply; strong demand from large families |

| Private Condo (resale, OCR) | S$1,200 – S$1,900 psf | ~S$1,550 psf | Older projects; limited resale stock |

| Pasir Ris 8 (new launch) | S$1,934 – S$3,728 psf | ~S$2,600 psf est. | Integrated development above MRT; luxury positioning |

The wide range within Pasir Ris 8 reflects its mixed product offering — from studio-format units to spacious 4-bedroom penthouses. For buyers focused on yield, the older resale condominiums at S$1,200–S$1,600 psf offer a more favourable entry point relative to rental demand, though they come with shorter remaining lease durations.

HDB Resale Market Dynamics

Pasir Ris has approximately 700 HDB resale transactions per year across all flat types, placing it in the mid-tier for transaction volume among OCR estates. Of these, 4-room flats account for roughly 40% of transactions, making them the most liquid asset class in the estate.

A notable dynamic in 2026 is the MOP wave. Nationally, around 13,480 HDB flats are reaching the end of their five-year (or ten-year Plus/Prime) minimum occupation period this year. Of these, Pasir Ris contributes an estimated 1,200–1,400 flats — primarily 4-room and 5-room units from developments built in 2019–2021. Sellers from these developments are typically younger upgraders, and their exit into the resale market is creating both additional supply and, indirectly, upgrader demand for private condominiums within and around the estate.

MRT Connectivity — Today and Tomorrow

Pasir Ris’s connectivity story is defined by two chapters: today’s East West Line (EWL) coverage and tomorrow’s Cross Island Line (CRL) expansion.

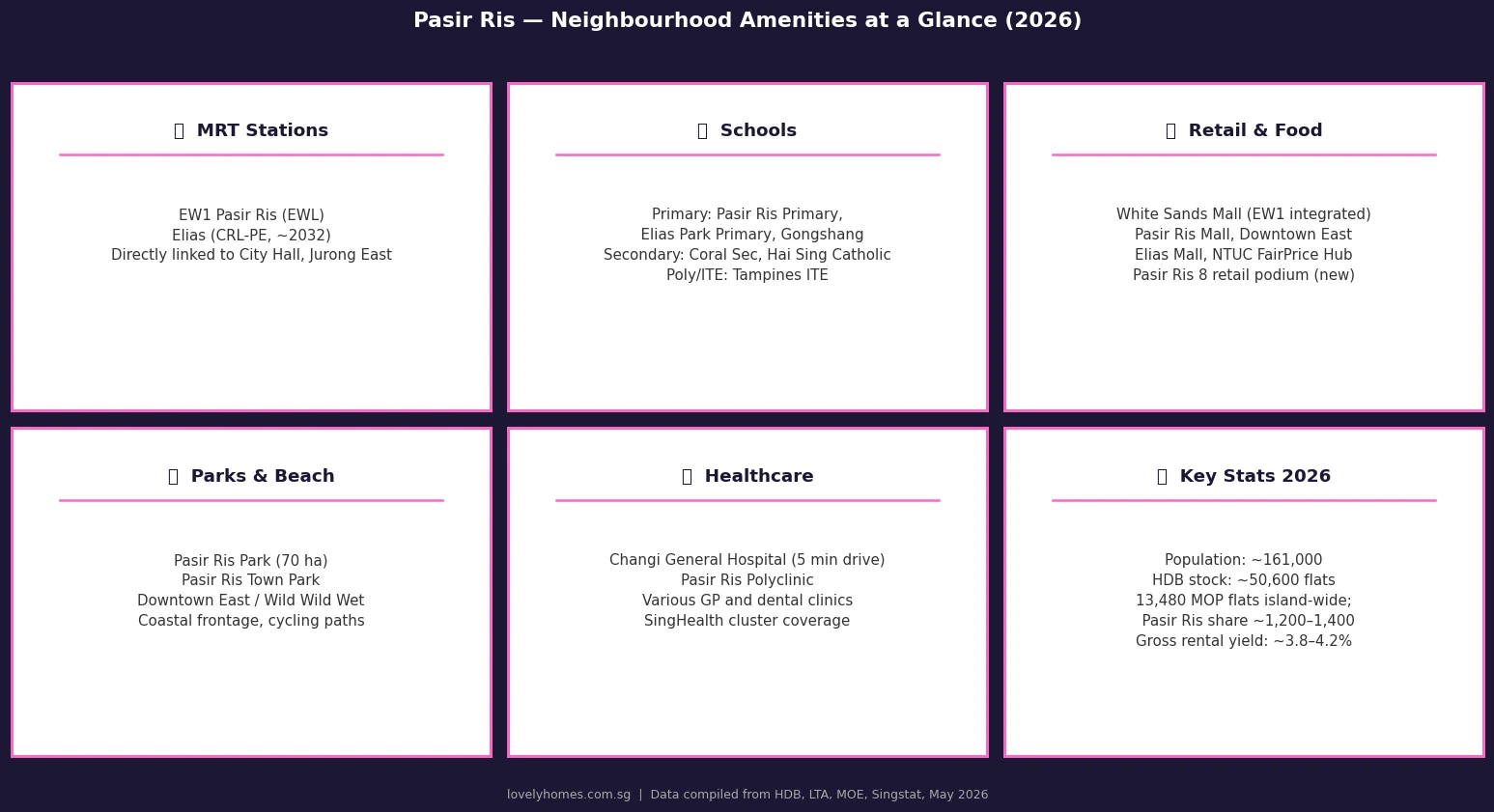

Today, Pasir Ris MRT station (EW1) is the eastern terminus of the East West Line — one of Singapore’s busiest rail corridors. From Pasir Ris, commuters can reach Raffles Place in approximately 38 minutes and Jurong East in roughly 55 minutes. The station is integrated with Pasir Ris 8, White Sands shopping centre, and a bus interchange, making it one of the better-connected suburban interchanges in the east.

By approximately 2032, the Cross Island Line’s Punggol Extension will add a second MRT station to the estate: Elias MRT, located at the junction of Pasir Ris Drive 10 and Pasir Ris Drive 3. Pasir Ris main station itself will also become an interchange with the CRL Punggol Extension, creating a direct link to Punggol, Sengkang, and the broader north-eastern corridor without requiring a change at Tampines. This dual-line connectivity, when realised, would meaningfully reduce Pasir Ris’s current perceived remoteness for residents commuting to the north-east.

Neighbourhood Amenities at a Glance

Schools and Education

Pasir Ris is well-served for primary education, with several schools within 1–2 km of most residential blocks. Pasir Ris Primary School, Elias Park Primary School, and Gongshang Primary School are the main feeder schools for the estate. For secondary education, Coral Secondary School and Hai Sing Catholic School sit within the town’s boundaries, while Dunman High School (an autonomous school offering the Integrated Programme) is accessible via a short bus or car journey near the Tampines–Pasir Ris border.

The MOE School Finder shows that families seeking a primary school within 1 km of popular Pasir Ris residential streets — particularly around Pasir Ris Drive 1, 3, and 6 — generally have strong in-zone admission chances at Pasir Ris Primary and Elias Park Primary. This factor alone drives family buyer demand for 5-room and executive HDB flats in those streets.

For post-secondary and tertiary education, the ITE College East and Tampines Meridian Junior College are both accessible within 20 minutes by bus or rail.

Retail, Food and Lifestyle

White Sands (integrated with Pasir Ris MRT) is the estate’s anchor mall, offering a full suite of food courts, supermarkets, pharmacies, and lifestyle retailers. Downtown East — one of Singapore’s largest lifestyle and entertainment hubs — sits adjacent to Pasir Ris Park and provides a Wild Wild Wet waterpark, indoor sports facilities, hotel accommodation, and an extensive food and beverage offering. Elias Mall and Pasir Ris Mall serve the internal town areas.

The upcoming Pasir Ris 8 development adds a retail podium above the MRT station, expanding the commercial offering with higher-end dining and lifestyle options that have historically been absent in the estate.

Pasir Ris Park and Outdoor Living

One of Pasir Ris’s most tangible lifestyle advantages is its greenery. Pasir Ris Park covers 70 hectares of managed parkland abutting the coastline — featuring cycling paths, mangrove boardwalks, a family-friendly beach, and barbecue pits. Singaporeans who value nature proximity will find Pasir Ris among the more green-affluent estates in the OCR, comparable to Bishan’s proximity to Bishan-AMK Park but with the added dimension of coastal access.

Investment Outlook — Rental Yield and Capital Growth

For HDB landlords, Pasir Ris delivers gross rental yields of approximately 3.8–4.2% on 4-room and 5-room flats — above the HDB island-wide average and driven by proximity to Changi Airport, Changi Business Park, and the wider east industrial corridor. Median monthly rents for a 4-room flat in Pasir Ris were approximately S$2,600–S$2,900 as at Q1 2026, according to HDB rental data.

For private condo investors, the older resale condominiums in Pasir Ris generate gross yields of approximately 3.4–3.6%, while Pasir Ris 8’s premium pricing means net yields will be tighter. The investment case for Pasir Ris 8 buyers rests more on capital appreciation (from MRT connectivity, new-launch premium, and precinct gentrification) than on near-term rental income cover.

Over the three years from Q1 2023 to Q1 2026, HDB resale prices in Pasir Ris have appreciated approximately 11–13% on a total-return basis across 4-room and 5-room flats, in line with broader OCR HDB trends as tracked by the HDB Resale Price Index.

Worked Example — HDB Upgrader Buying a Pasir Ris Condo in 2026

Consider Mr and Mrs Lim, a Singapore Citizen couple aged 38 and 36, with a combined monthly income of S$14,500. They own a 5-room HDB flat in Pasir Ris that cleared its five-year MOP in early 2026. They purchased the flat as a BTO for S$350,000; it is now transacting at S$750,000 on the resale market. They have S$260,000 in CPF Ordinary Account used for the flat, with accrued interest of S$48,000 (at 2.5% p.a. over six years).

Step 1 — Sale proceeds: Gross sale S$750,000 → outstanding bank loan S$220,000 → CPF principal refund S$260,000 → accrued interest S$48,000 → legal and agent costs S$12,000. Estimated cash-in-hand: approximately S$210,000.

Step 2 — Buying a S$1.60M Pasir Ris condo: As they are selling first, they hold zero residential properties at OTP signing. ABSD: 0% (Singapore Citizens, first property). BSD on S$1.60M = 1%×S$180k + 2%×S$180k + 3%×S$640k + 4%×S$600k = S$1,800 + S$3,600 + S$19,200 + S$24,000 = S$48,600.

Step 3 — Financing: 75% LTV (bank loan on private property, SC first property) = S$1,200,000 loan. 25% down = S$400,000 (S$308,000 CPF OA re-deposited after refund + S$92,000 cash). Legal and miscellaneous costs: ~S$7,000 cash. Total immediate cash outlay: S$48,600 (BSD) + S$92,000 (cash top-up on down payment) + S$7,000 = ~S$147,600.

Step 4 — Monthly repayment: S$1,200,000 at a fixed rate of 1.80% over 25 years = approximately S$4,930/mth. TDSR check: S$4,930 ÷ S$14,500 = 34.0% — comfortably within the 55% TDSR ceiling. The couple’s post-purchase cash reserve is approximately S$62,000, providing a meaningful liquidity buffer.

What Might Come Next for Pasir Ris

The 2032 completion of Elias MRT is the most significant near-term catalyst for the estate. New MRT stations in Singapore have historically generated price premium expansion in the two-to-four years leading up to opening, as market participants anticipate connectivity improvements. Areas within 600–800 metres of the future Elias station — particularly the emerging Neighbourhood 8 precinct — will be worth tracking.

The former MINDEF training land adjacent to Elias Road is earmarked for public and private housing development as part of Neighbourhood 8. While no definitive URA masterplan details or GLS tenders have been announced for this precinct as at May 2026, it represents a potential supply of several thousand new homes on relatively underutilised land in an estate where new private supply has historically been scarce.

On the rental side, Changi Airport’s continued expansion (Terminal 5, expected post-2030) and the growth of Changi Business Park as a technology and financial services hub both support sustained rental demand in the eastern corridor, benefiting Pasir Ris landlords.

Frequently Asked Questions

Is Pasir Ris a good place to buy property in 2026?

Pasir Ris offers a compelling combination of yield (HDB gross yields of 4%+), greenery, family-friendly infrastructure, and a clear near-term catalyst in the Cross Island Line’s Elias station (~2032). It is not a prestige address and will not command the PSF of Bishan, Queenstown, or the CCR — but for owner-occupiers seeking space and affordability, and for investors prioritising yield, it performs well within the OCR category. The key risk is the estate’s current single-line MRT exposure (EWL only) until the CRL Punggol Extension is operational.

Which MRT stations serve Pasir Ris?

Currently, Pasir Ris MRT (EW1) on the East West Line is the sole station. It is the eastern terminus of the EWL and is integrated with the Pasir Ris Bus Interchange. By approximately 2032, the Cross Island Line’s Punggol Extension will add Elias MRT within the estate (at Pasir Ris Drive 10 / Drive 3), and Pasir Ris station itself will become an interchange with the CRL Punggol Extension — enabling direct connectivity to Punggol, Sengkang, and Bishan without changing trains.

What is the HDB resale record in Pasir Ris?

The highest recorded HDB resale transaction in Pasir Ris, as at our research date, is an Executive flat that transacted at approximately S$1.08M — reflecting the scarcity of large-format flats in the estate. For 5-room flats, transactions in excess of S$850,000 have been recorded for well-located blocks near Pasir Ris Park and the MRT. These represent outlier premium transactions; the estate-wide median for 5-room flats remains approximately S$735,000 as at Q1 2026.

How does Pasir Ris compare to Tampines and Bedok for property investment?

Compared to Tampines, Pasir Ris tends to offer slightly higher HDB rental yields (4%+ vs Tampines’ ~3.8%) but lower private condo capital growth potential in the short term, as Tampines benefits from more established commercial infrastructure and multiple MRT lines. Compared to Bedok, Pasir Ris offers lower entry prices for similar flat types but lacks Bedok’s three-MRT-line advantage. The upcoming Elias MRT and Neighbourhood 8 development are Pasir Ris-specific catalysts that neither Tampines nor Bedok can replicate on the same timeline.

Can HDB upgraders avoid ABSD when buying Pasir Ris 8?

Yes — if the HDB flat is sold before (or simultaneously with) the OTP signing for the private property. When a Singapore Citizen sells their only existing residential property before acquiring a new one, they hold zero properties at the point of OTP and therefore pay 0% ABSD. This is the standard “sell-first, then buy” upgrader route. The key constraint is timing: you will need to arrange bridging accommodation between your HDB sale completion and your new condo’s TOP date. See our Upgrading from HDB to Private Property guide for the full timeline and cost analysis.

Are there BTO flats available in Pasir Ris in 2026?

As at May 2026, no standard BTO launch has been announced specifically for Pasir Ris in the June 2026 BTO exercise, which covers Bishan, Ang Mo Kio, Bukit Merah, Sembawang, and Woodlands. However, the emerging Neighbourhood 8 precinct (former MINDEF land near Elias Road) is expected to yield future BTO launches — likely announced in the 2027–2028 BTO exercise window once planning and land clearance is completed. Prospective buyers wanting to live in Pasir Ris in the near term should look at the resale market, the Sale of Balance Flats (SBF) exercises, or the Pasir Ris EC at Jalan Loyang Besar for qualifying buyers.

Related Articles

- Bedok Neighbourhood Guide Singapore 2026: Property Prices, Schools and Investment Outlook

- Tampines Neighbourhood Guide Singapore 2026: Property Prices, Schools and Investment Outlook

- Upgrading from HDB to Private Property Singapore 2026: Step-by-Step Guide, Costs and Timing

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Minimum Occupation Period (MOP) Singapore 2026: HDB, EC and Private Property Rules

- 13,480 HDB Flats Reaching MOP in 2026: What the Supply Wave Means for Buyers and Sellers

- Rental Yield Singapore 2026: Complete Guide to Gross, Net and Location-Adjusted Yields

Disclaimer: This neighbourhood guide is for general informational purposes only and does not constitute financial, investment, or property advice. All prices, yields, and market data cited are drawn from publicly available sources including HDB Resale Statistics, URA Caveats Lodged, LTA announcements, and SingStat as at May 2026, and are subject to change without notice. Past performance and historical price trends are not indicative of future results. Always conduct independent verification and consult a licensed property agent, financial adviser, or conveyancing lawyer before making any property decision. For official data, refer to HDB, URA, LTA, SingStat, and MAS.