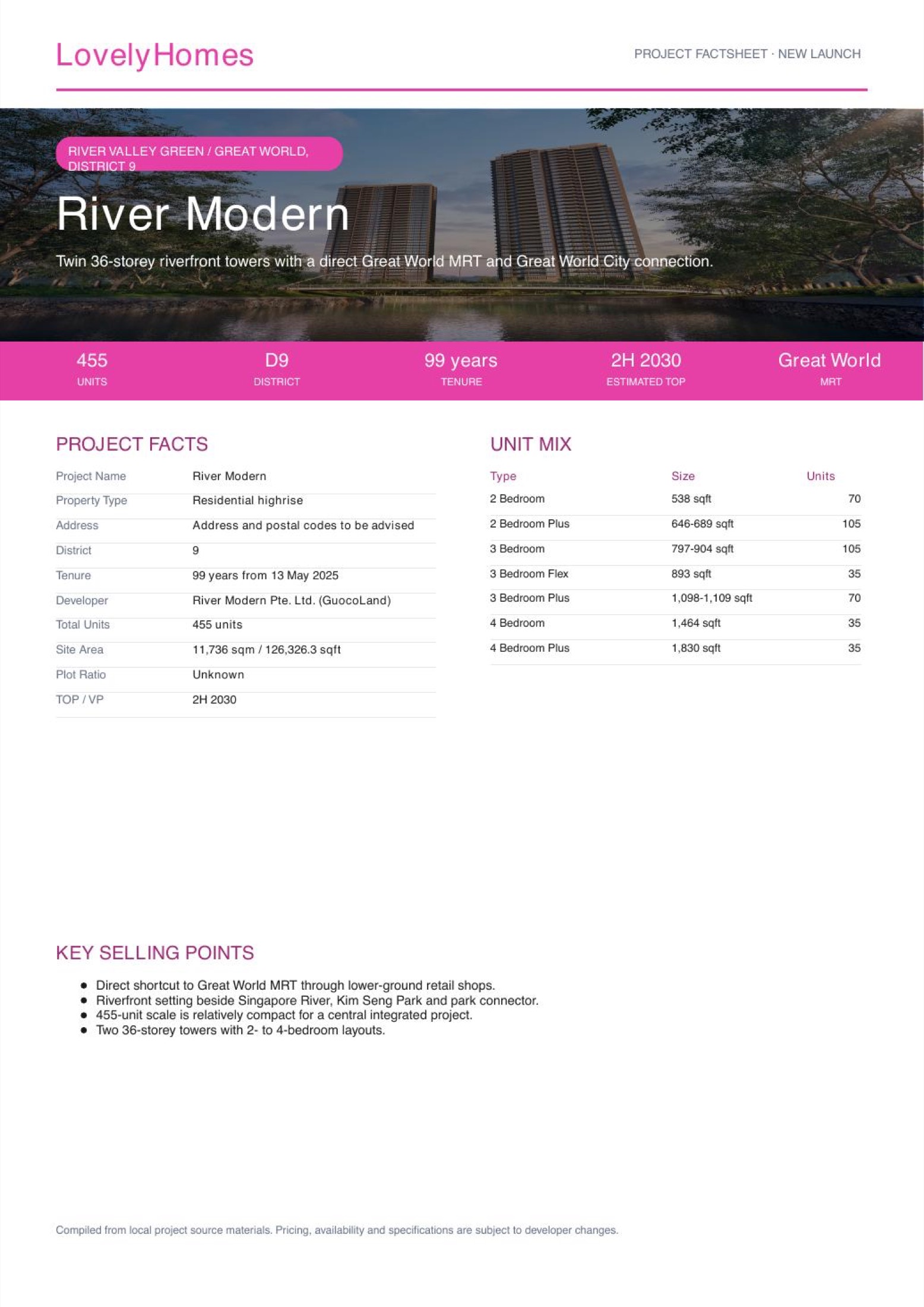

Twin 36-storey riverfront towers with a direct Great World MRT and Great World City connection.

01

Direct shortcut to Great World MRT through lower-ground retail shops

Direct shortcut to Great World MRT through lower-ground retail shops.

02

Riverfront setting beside Singapore River, Kim Seng Park and park connector

Riverfront setting beside Singapore River, Kim Seng Park and park connector.

03

455-unit scale is relatively compact for a central integrated project

455-unit scale is relatively compact for a central integrated project.

Project At-a-Glance

Project Name

River Modern

Property Type

Residential highrise

Address

Address and postal codes to be advised

District

9

Tenure

99 years from 13 May 2025

Developer

River Modern Pte. Ltd. (GuocoLand)

Total Units

455 units

Site Area

11,736 sqm / 126,326.3 sqft

Plot Ratio

Unknown

TOP / VP

2H 2030

River Modern in brief

Direct shortcut to Great World MRT through lower-ground retail shops.

Riverfront setting beside Singapore River, Kim Seng Park and park connector.

Unit Mix and Sizes

Unit Type

Size Range

Units

2 Bedroom

538 sqft

70

2 Bedroom Plus

646-689 sqft

105

3 Bedroom

797-904 sqft

105

3 Bedroom Flex

893 sqft

35

3 Bedroom Plus

1,098-1,109 sqft

70

4 Bedroom

1,464 sqft

35

4 Bedroom Plus

1,830 sqft

35

Source note: Unit mix and sizes are compiled from local project factsheet/floor-plan materials. Buyers should verify latest units and strata details before booking.

Indicative Pricing

Price Guide

Latest official price list

Availability

Available on request

Status

Subject to developer release

The local source materials do not provide a publishable current unit-by-unit price list for this post. Request the latest developer price matrix before making a purchase decision.

Why Buyers Are Watching

1Direct shortcut to Great World MRT through lower-ground retail shops.

2Riverfront setting beside Singapore River, Kim Seng Park and park connector.

3455-unit scale is relatively compact for a central integrated project.

4Two 36-storey towers with 2- to 4-bedroom layouts.

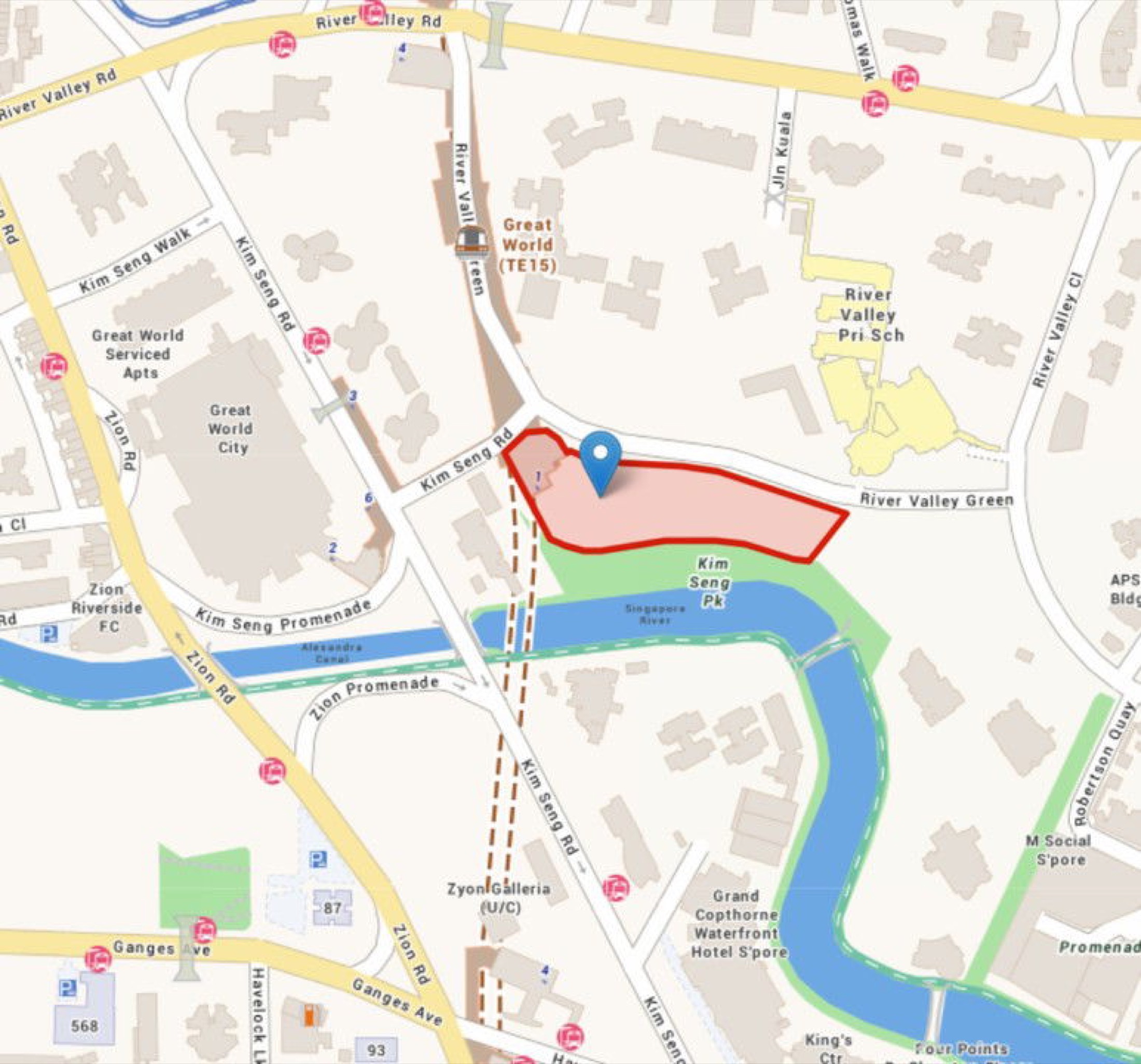

Location and Connectivity

Link 1

Great World MRT Exit 1

Connectivity detail from local project materials; travel times should be independently verified.

Link 2

Great World City mall

Connectivity detail from local project materials; travel times should be independently verified.

Link 3

Singapore River park connector

Connectivity detail from local project materials; travel times should be independently verified.

Link 4

Short drive to Orchard, CBD and Marina Bay

Connectivity detail from local project materials; travel times should be independently verified.

Location details are source-derived and should be verified against current transport maps.

Schools Nearby

Nearby schools

River Valley Primary, ACS Junior, St Margaret's School (Primary), Alexandra Primary

Note

School proximity and eligibility should be checked against the latest MOE OneMap school-query data.

Lifestyle and Amenities

Great World City

Neighbourhood amenity highlighted in the local source pack and surrounding-area notes.

Singapore River dining

Neighbourhood amenity highlighted in the local source pack and surrounding-area notes.

Orchard Road

Neighbourhood amenity highlighted in the local source pack and surrounding-area notes.

Kim Seng Park

Neighbourhood amenity highlighted in the local source pack and surrounding-area notes.

Marina Bay

Neighbourhood amenity highlighted in the local source pack and surrounding-area notes.

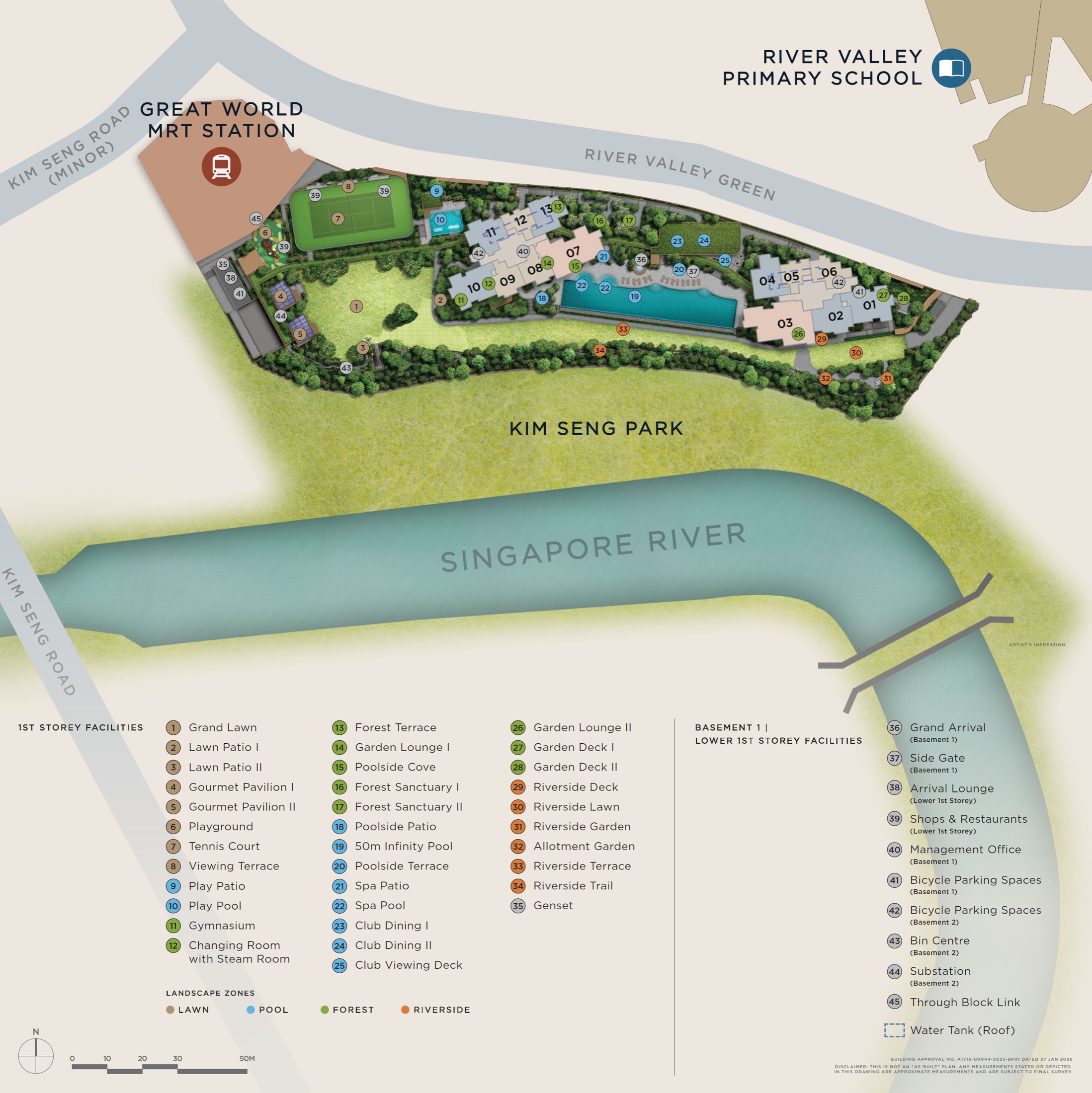

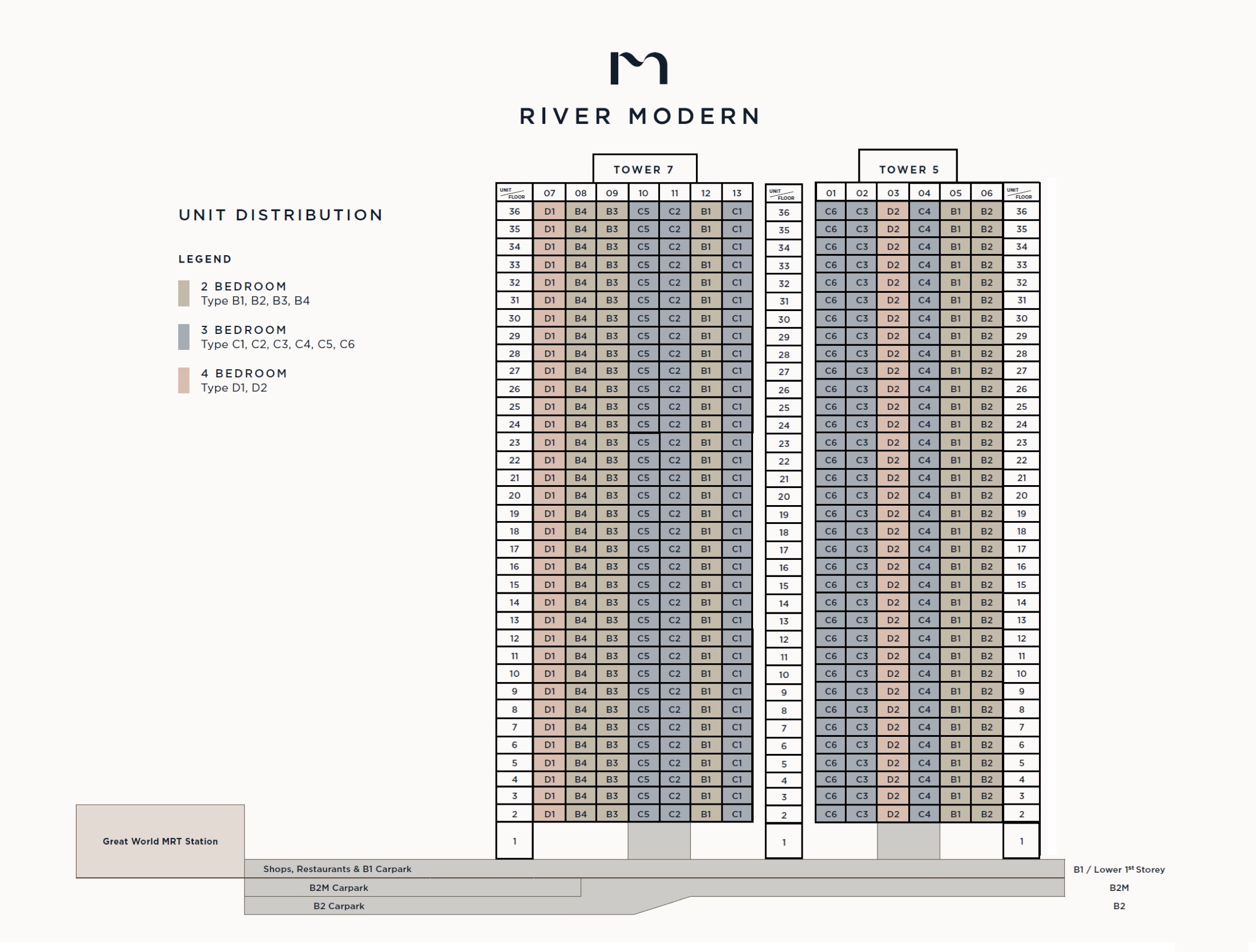

Site Plan

River Modern actual site plan from source material

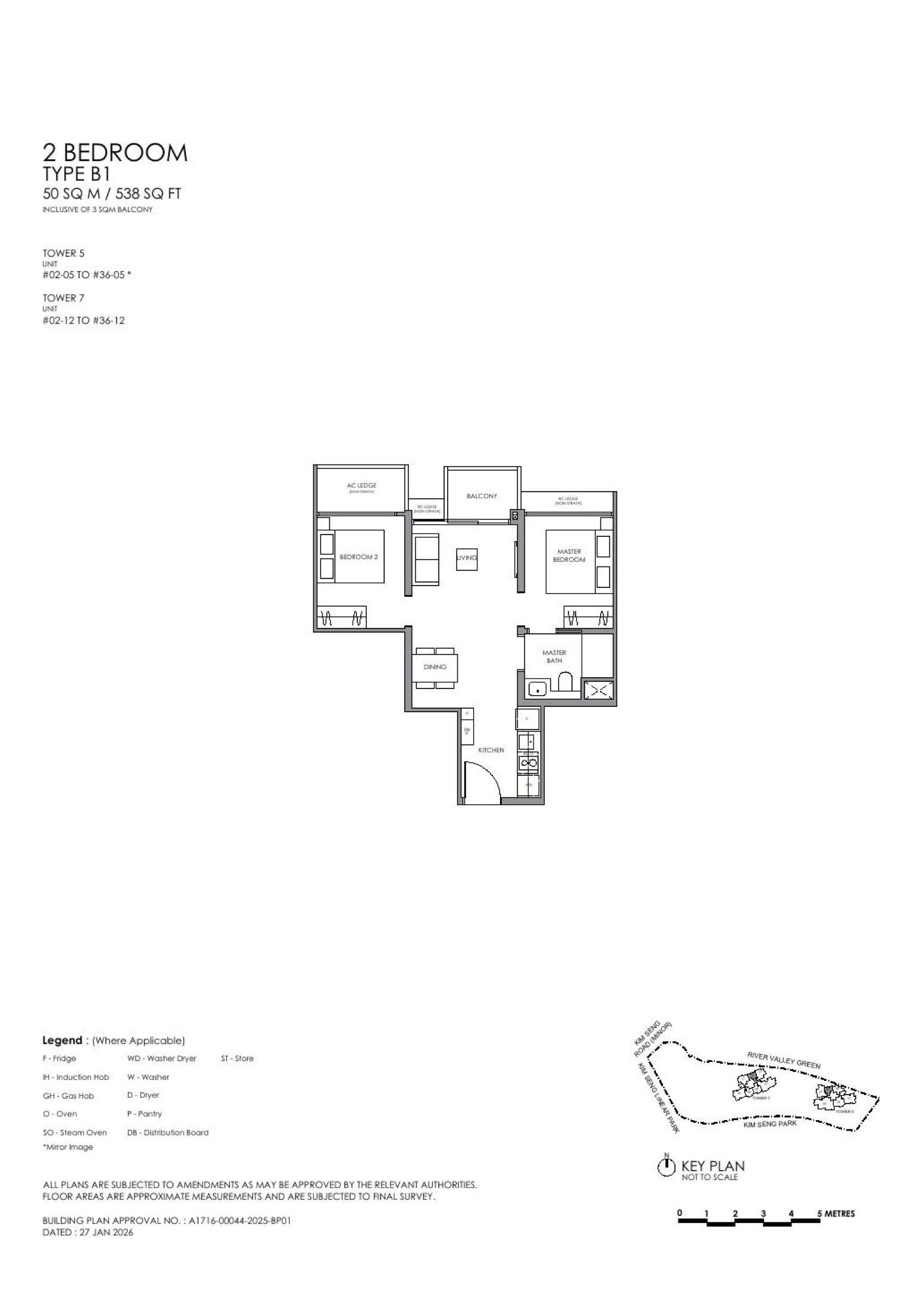

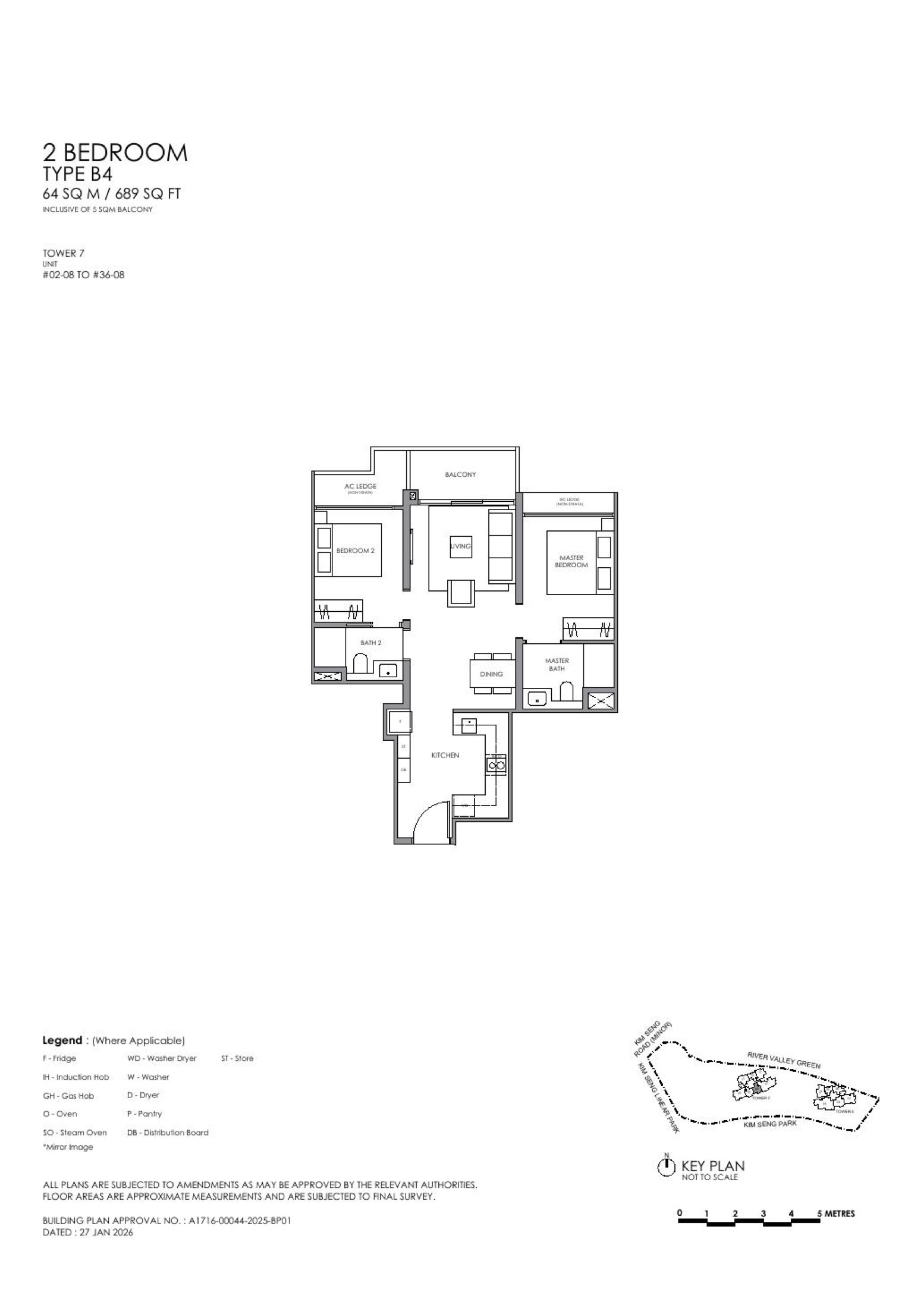

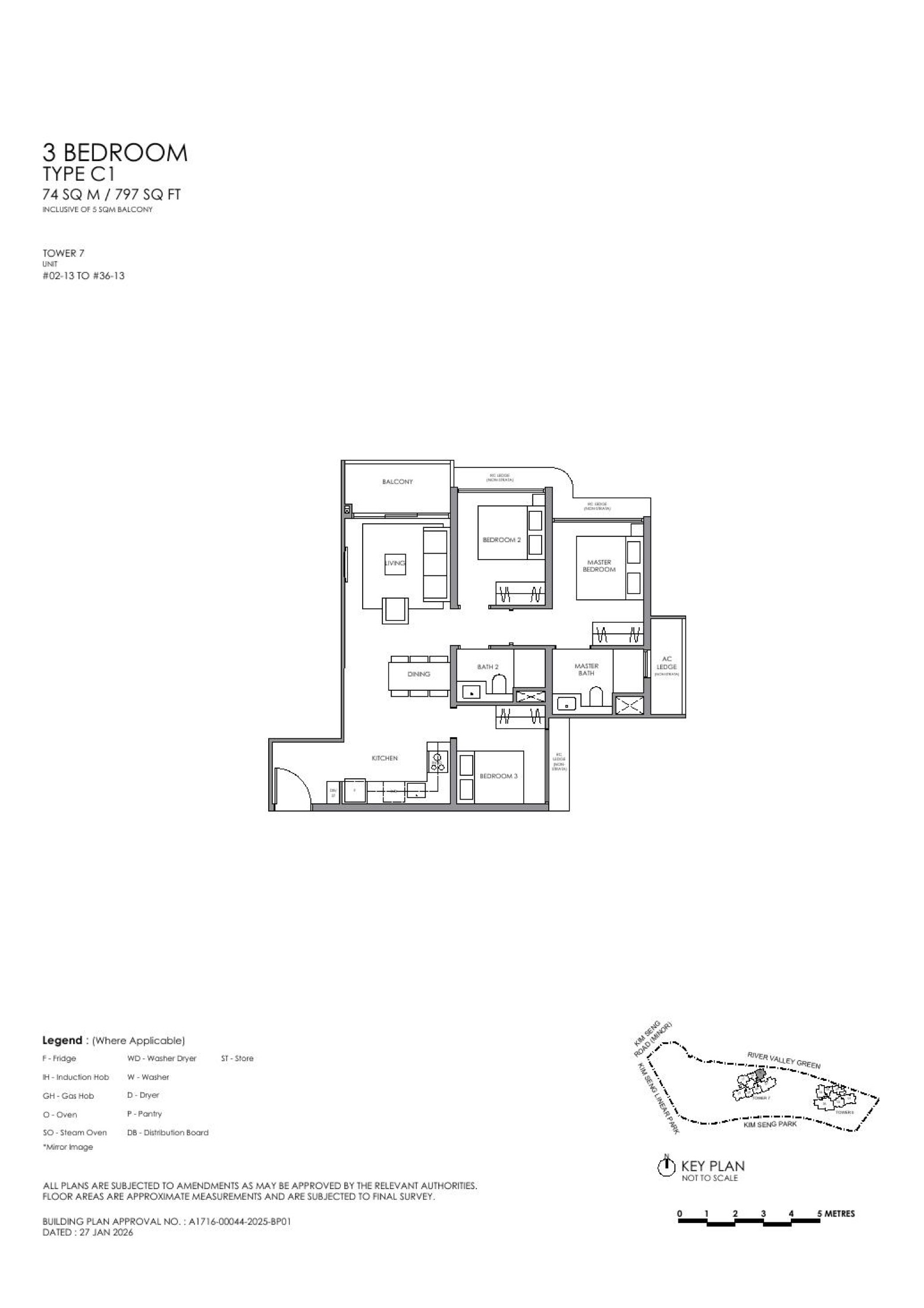

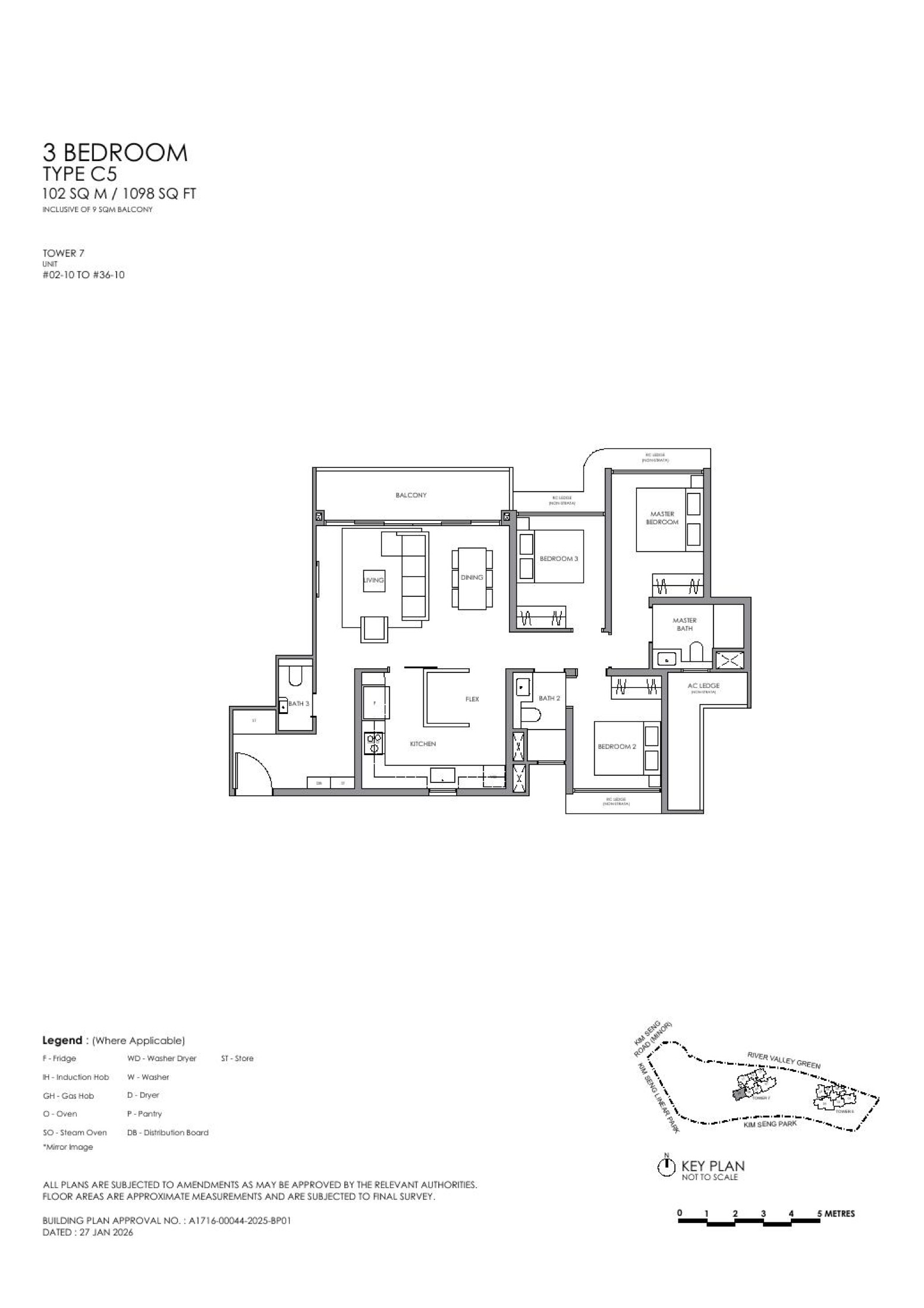

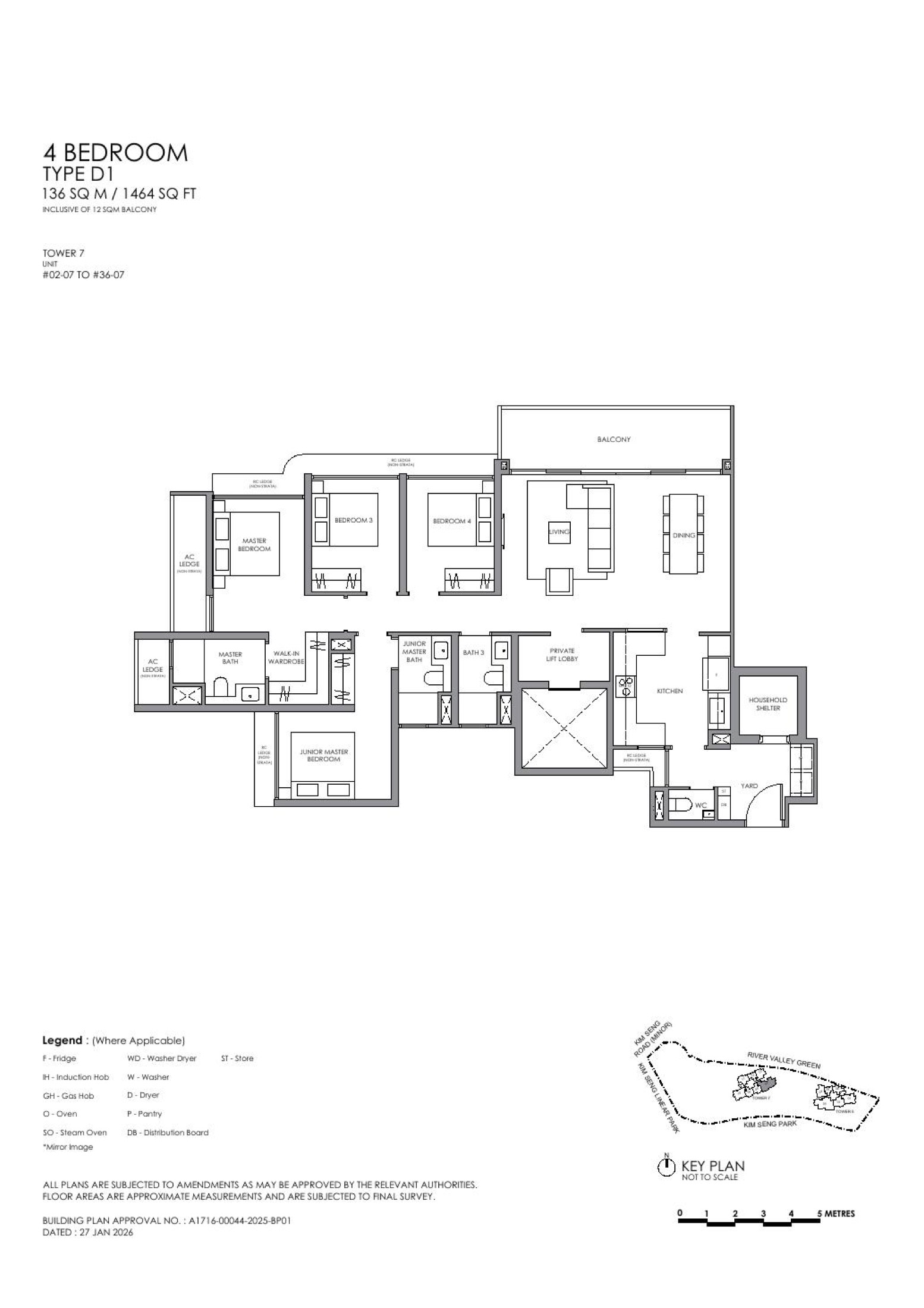

Floor Plans (Selected)

Representative actual floor plans by unit type. Download the full floor-plan PDF below for every available source layout.

2 Bedroom B1

2 Bedroom B4

3 Bedroom C1

3 Bedroom Plus C5

4 Bedroom D1

Need every stack and layout?

Download the full floor-plan PDF from the source pack.

Disclaimer: Information is compiled from local project source materials and may change without notice. Floor areas, travel times, pricing and availability must be verified with the developer sales team before purchase.

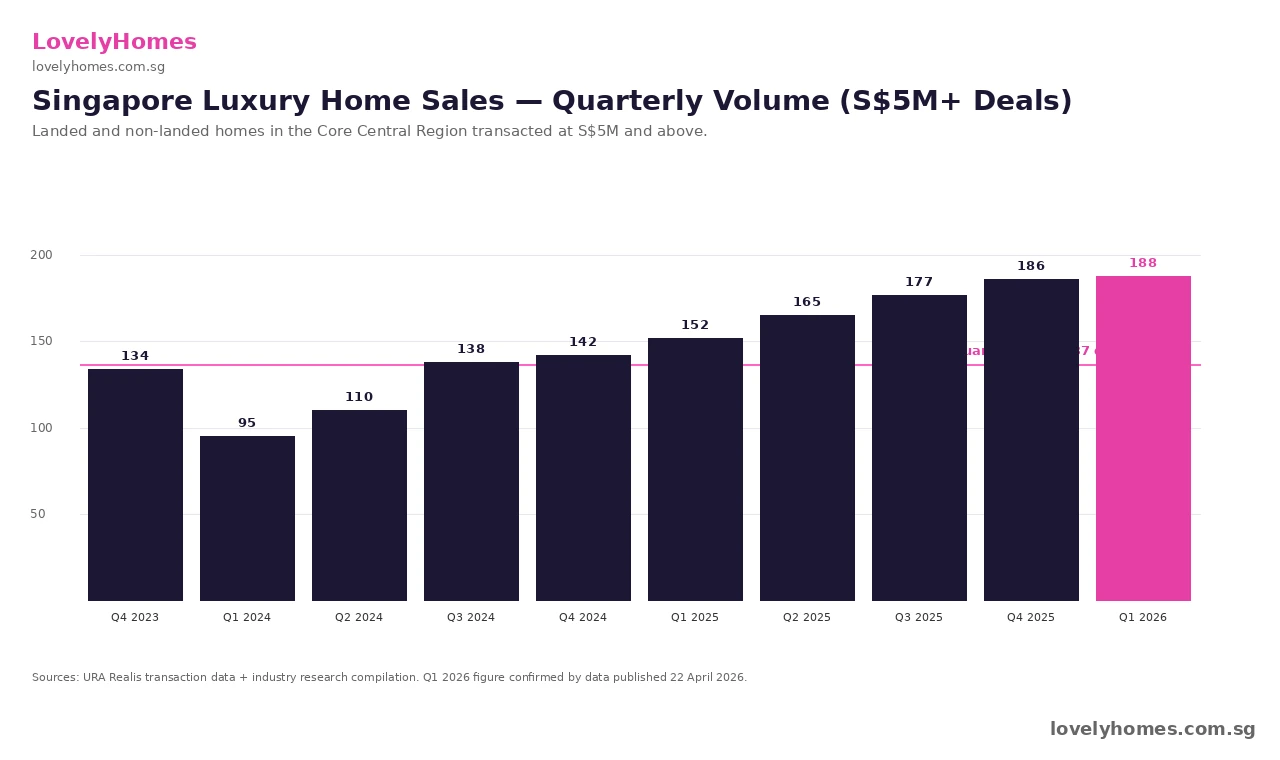

Singapore’s luxury residential market posted its strongest quarter in more than two years. 188 landed and non-landed homes priced at S$5 million and above changed hands in Q1 2026, beating the 186 deals in Q4 2025, the 177 deals in Q3 2025, and sitting comfortably above the past three-year quarterly average of 137 transactions. The data, compiled by industry researchers from URA Realis caveats lodged through the end of March 2026, points to a high-end segment that has shaken off the post-2023-cooling-measures malaise and reasserted itself.

Quick Answer — what just happened in Singapore’s luxury market

188 deals at S$5M and above in Q1 2026 — highest quarterly count since Q4 2023.

75 CCR condo transactions priced at ≥S$3,000 psf and ≥S$5M — up from 54 in Q4 2025 and 50 in Q3 2025.

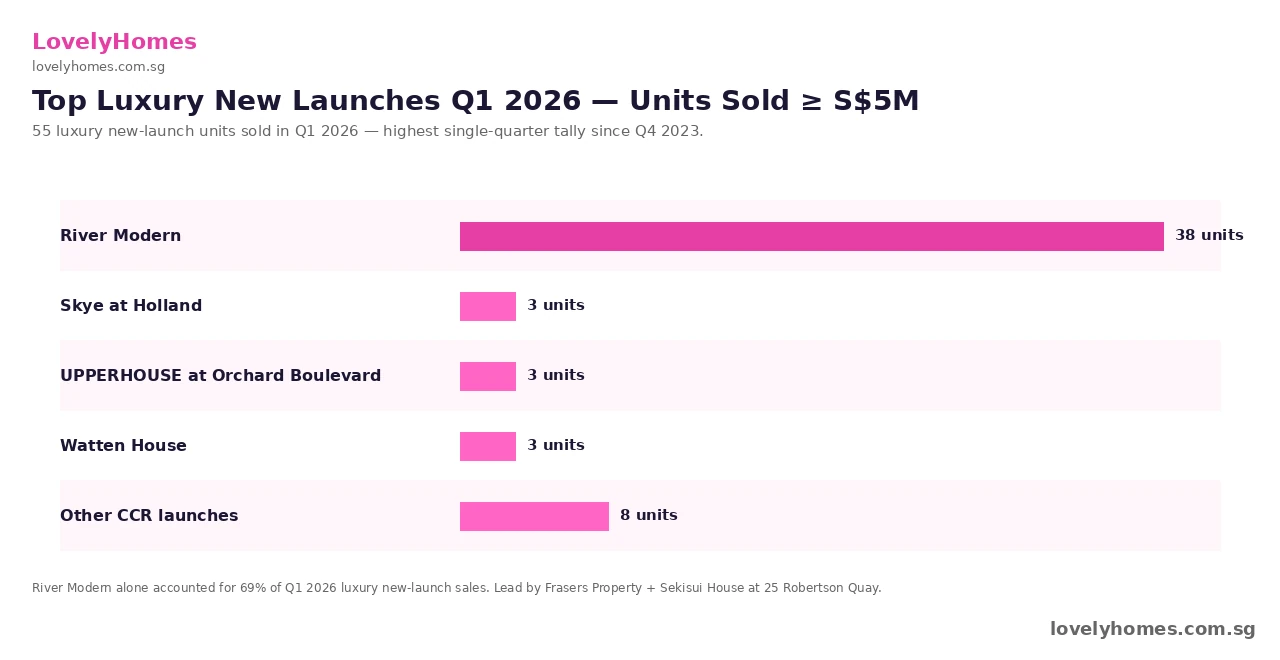

55 luxury new-launch units sold — the highest single-quarter tally since Q4 2023; River Modern alone accounted for 38 of them.

Ultra-luxury (≥S$10M) deals rose from 14 in Q4 2025 to 17 in Q1 2026.

Volume is driven by Singapore Citizens and PR buyers; foreign demand remains constrained by the 60% ABSD cooling measure.

The Headline Number — 188 Deals at S$5M and Above

The 188-deal print for Q1 2026 is the highest in nine quarters, and the third consecutive quarter of expansion in the absolute volume of luxury transactions. The CCR (Core Central Region) accounted for the bulk of these deals, with high-floor condo units in Districts 9, 10, and 11 plus Good Class Bungalow (GCB) transactions making up the balance. Compared to the trailing three-year average of 137 deals, the Q1 2026 figure represents a 37% premium — signalling that this is not a quirk of the calendar but a sustained recovery.

Figure 1: Quarterly luxury home transactions in Singapore (S$5M+). Q1 2026’s 188 deals top the past nine quarters.

The CCR Premium Segment — 75 Deals at S$3,000 psf+

Look one layer deeper and the picture sharpens. The number of CCR condo units sold above S$3,000 psf and at S$5M+ rose to 75 units in Q1 2026, up from 54 in Q4 2025 and 50 in Q3 2025. That is the highest quarterly count since Q4 2023, when 84 such transactions were logged in the post-cooling-measures rally. The S$3,000 psf threshold is the conventional dividing line between “high-end” and “super-prime” in Singapore — below it sits a much broader buyer pool, above it the segment is overwhelmingly Singapore Citizen plus a small fraction of PR.

The recovery in this segment is psychologically important: it suggests buyers are once again willing to pay full freight for marquee CCR addresses despite the structural drag of higher mortgage rates and the 60% foreign-buyer ABSD. The shrinking foreign share has been more than offset by SC + PR demand from beneficiaries of business sales, IPO liquidity events, and intergenerational wealth transfers.

What Drove It — Three New Launches Did the Heavy Lifting

Luxury new-launch activity climbed for the fourth consecutive quarter, with 55 new units sold at S$5M+ in Q1 2026 — the highest single-quarter tally since Q4 2023’s 74. The skew was extreme. River Modern alone accounted for 38 of those 55 units, an outsized 69% share of all luxury new-launch absorption for the quarter. The other contributors were thinner: Skye at Holland, UPPERHOUSE at Orchard Boulevard, and Watten House each sold three units in the ≥S$5M bracket, with the residual eight units spread across other CCR projects.

Figure 2: Q1 2026 luxury new-launch absorption was concentrated in River Modern.

That concentration is a cautionary note. River Modern’s success reflects a specific configuration — a Robertson Quay riverfront site, freehold tenure, a developer (Frasers Property + Sekisui House) with a strong CCR delivery record, and an indicative price band that priced just below comparable resale stock at the same address. Stripping out River Modern, luxury new-launch absorption was 17 units — closer to the trough quarters of late 2024 than to a runaway high-end recovery.

Ultra-Luxury — The S$10M+ Cohort

At the very top of the market, the count of luxury condo transactions priced at S$10 million and above rose from 14 in Q4 2025 to 17 in Q1 2026. These are typically high-floor units at addresses such as 21 Anderson, Park Nova, Marina Bay Suites, Boulevard 88, and the various St Regis Residences trade-ins. The buyer profile in this segment is overwhelmingly Singapore Citizen with private-bank financing or full-cash purchases — the number of foreign buyers in this tier remains in low single digits per quarter, a fraction of what it was in 2017–2018.

Summary — The Q1 2026 Luxury Print at a Glance

Segment

Q3 2025

Q4 2025

Q1 2026

QoQ change

All luxury homes ≥ S$5M

177

186

188

+1.1%

CCR condos ≥ S$3,000 psf & ≥ S$5M

50

54

75

+38.9%

Luxury new-launch units ≥ S$5M

~30

~42

55

+31%

Ultra-luxury ≥ S$10M

12

14

17

+21%

Why This Matters for the Broader Market

Singapore’s luxury segment has historically led the broader market by 2–3 quarters at major inflection points. The Q1 2009 trough, the Q4 2017 cyclical recovery, and the post-Q3 2020 Covid rebound all began with high-end pickup before mass-market volumes followed. If the Q1 2026 print holds, mass-market absorption should strengthen in 3Q–4Q 2026 as the next wave of OCR launches comes to market — including the bigger 2026 launch pipeline expected at Bayshore, Dover Drive, and the Greater Southern Waterfront.

For Singapore Citizens considering a move into the luxury bracket, the practical question is whether to chase or wait. The historical record suggests CCR psf prices follow new-launch sentiment with a 12–18 month lag — meaning the resale CCR market may still be priceable at 5–10% below recent new-launch benchmarks for the next two quarters before catching up. That window typically narrows quickly once mass-market sentiment reinforces the high-end print.

What Might Come Next

Three watch-points for Q2 2026. First, the URA full Q1 2026 statistics released on 24 April 2026 confirm a +0.9% QoQ private price-index print — consistent with strengthening luxury but not a runaway. Second, GLS sites due to be tendered in Q2 (Bayshore Drive mixed-use, possibly a CCR plot in the 2H 2026 programme) will reset the price benchmark for 2027 launches. Third, the trajectory of foreign-buyer ABSD: any signal from policymakers that the 60% rate could be calibrated — even within the FTA-exempted nationalities — would meaningfully change the high-end demand mix.

Frequently Asked Questions

Does the Q1 2026 luxury print mean prices are rising fast?

Volume rose; price-per-square-foot was steadier. The URA private property price index rose just 0.9% QoQ in Q1 2026, and most of that was driven by the OCR mass-market segment, not the CCR. The CCR sub-index rose roughly 0.6% QoQ. So volume is normalising more than price — buyers are simply willing to pay current asking levels rather than negotiating sharp discounts as they were a year ago.

Are foreign buyers driving the recovery?

No. Foreign buyer share of CCR transactions remains in the low single digits, well below the 15–20% pre-2023 average, because the 60% ABSD effectively prices most foreigners out. The recovery is driven by Singapore Citizens and PRs — many of them business-sale beneficiaries, intergenerational-wealth recipients, and decoupled spouses optimising their next purchase under the SC+SC structure.

What is “River Modern” and why did it dominate?

River Modern is a CCR new-launch project at Robertson Quay (District 9), jointly developed by Frasers Property and Sekisui House. It launched in late 2025 with an indicative price from S$3,150 psf. Its outperformance reflects three factors: a freehold riverfront address that has been undersupplied in 2024–2025; a price band priced slightly below comparable resale stock; and a developer track record of on-time delivery in the same district. Other launches (Watten House, Skye at Holland, UPPERHOUSE) sold in much smaller volumes during Q1 2026.

Should I time a CCR resale purchase now or wait?

Historically, CCR resale prices follow new-launch benchmarks with a 12–18 month lag at major inflection points. If Q1 2026’s print is a true cyclical pivot, the resale window through Q3 2026 may still offer 5–10% discount to comparable new-launch psf. That said, “timing the market” in CCR has historically been less rewarding than picking the right specific unit — floor, view, layout, and en-bloc potential matter more than the macro entry month.

How does this compare to Hong Kong or Sydney’s luxury markets?

Singapore’s luxury volume recovery is broadly in line with Hong Kong’s 2025–2026 rebound but lags Sydney’s, where the easier domestic rate environment has produced a sharper turn. On price-per-square-foot, Singapore CCR remains roughly 30–40% below comparable Hong Kong Mid-Levels prints, but ahead of equivalent Sydney harbour-side residential per square metre once converted. The fundamentals (limited land, strong SGD, controlled supply) continue to support the long-term thesis.

Where is the Q2 2026 supply pipeline likely to land?

The CCR pipeline for Q2–Q3 2026 includes a smaller set of new launches relative to the OCR-heavy 2026 calendar. Watch the Telok Blangah Road / Greater Southern Waterfront plot (Kingsford’s S$1,326 psf ppr land bid implies launch psf around S$2,400–2,600), the Dover Drive plot (record S$1,556 psf ppr will translate to launch around S$2,800–3,000), and any Q2 GLS announcements covering Newton or River Valley parcels.

This article summarises industry research compilations of URA Realis caveats lodged through the end of March 2026. Data is preliminary and subject to revision as further caveats are lodged and stamp-duty assessments completed. Figures are illustrative as at April 2026. Always verify with primary sources — URA Realis, URA media releases, and the Inland Revenue Authority of Singapore — before making any property decision.