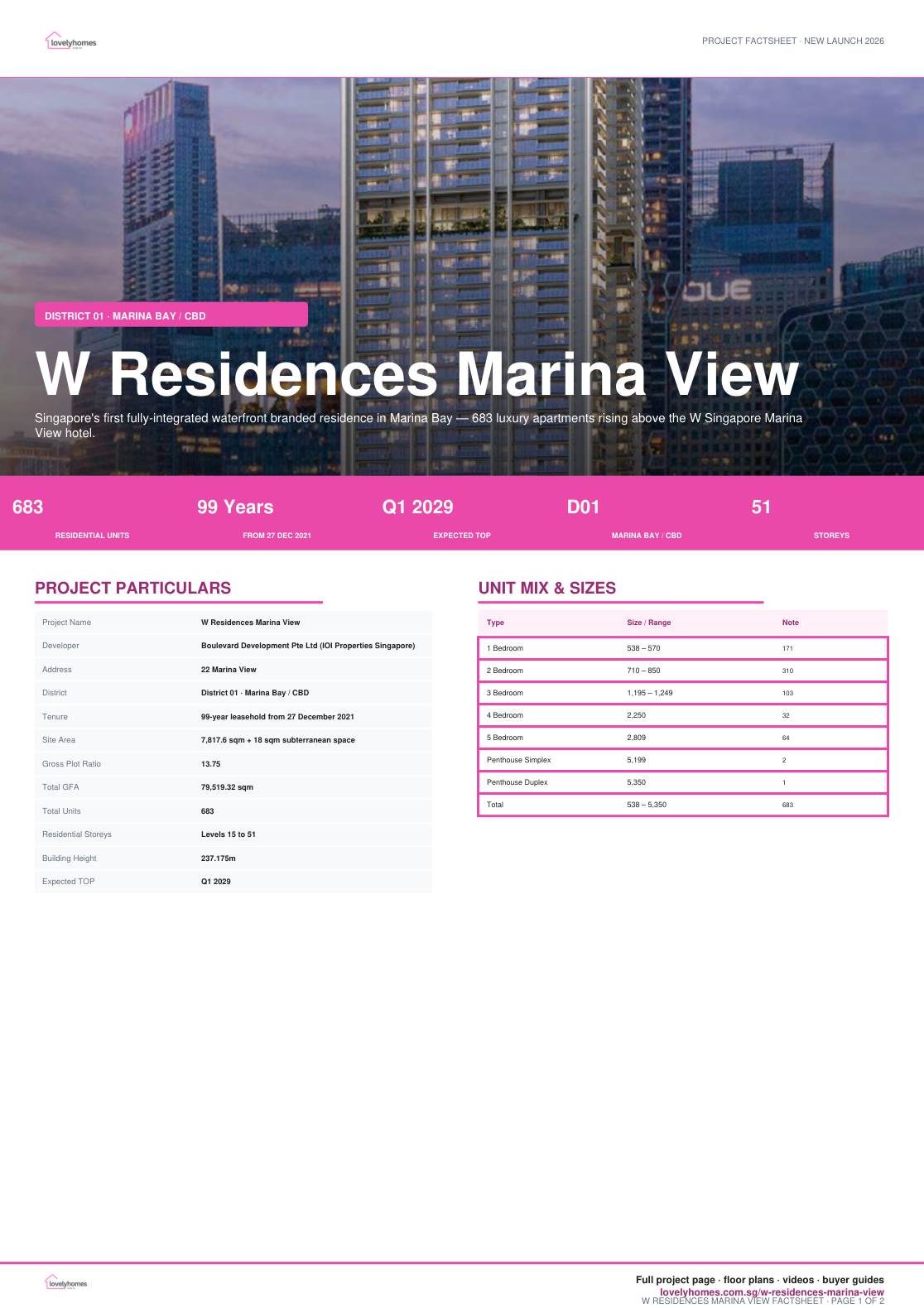

W Residences Marina View is a 99-year leasehold branded residence at 22 Marina View, developed by Boulevard Development Pte Ltd under IOI Properties Singapore. Project documents describe it as the first integrated development in Singapore with 683 residences sitting above a 360-room W Singapore hotel.

The key appeal is the combination of a Marina Bay address, managed branded-residence services, a large 683-unit amenity base, and the long-term transformation of Marina Bay / Greater Southern Waterfront.

01 · Address

Marina Bay new downtown

Located at the junction of Union Street and Marina View, within walking reach of Shenton Way, Downtown, Marina Bay, Raffles Place and Tanjong Pagar MRT stations.

02 · Branded Living

W hotel-managed lifestyle

Developer buyer notes position the residence around W’s hotel-style services, concierge support and branded hospitality environment.

03 · Scale

683 luxury units

Unit sizes span 1-bedroom suites through 5-bedroom apartments and three penthouses, supporting multiple sky and club facilities.

Project At-a-Glance

Project Name

W Residences Marina View

Developer

Boulevard Development Pte Ltd (IOI Properties Singapore)

Address

22 Marina View

District

District 01 · Marina Bay / CBD

Tenure

99-year leasehold from 27 December 2021

Site Area

7,817.6 sqm + 18 sqm subterranean space

Gross Plot Ratio

13.75

Total GFA

79,519.32 sqm

Total Units

683

Residential Storeys

Levels 15 to 51

Building Height

237.175m

Expected TOP

Q1 2029

Carpark

342 lots + 4 accessible lots; EV provision

Bicycle Lots

171 residential bicycle lots

Architect

Architects61 Pte Ltd

Landscape Architect

Coen Design International Pte Ltd

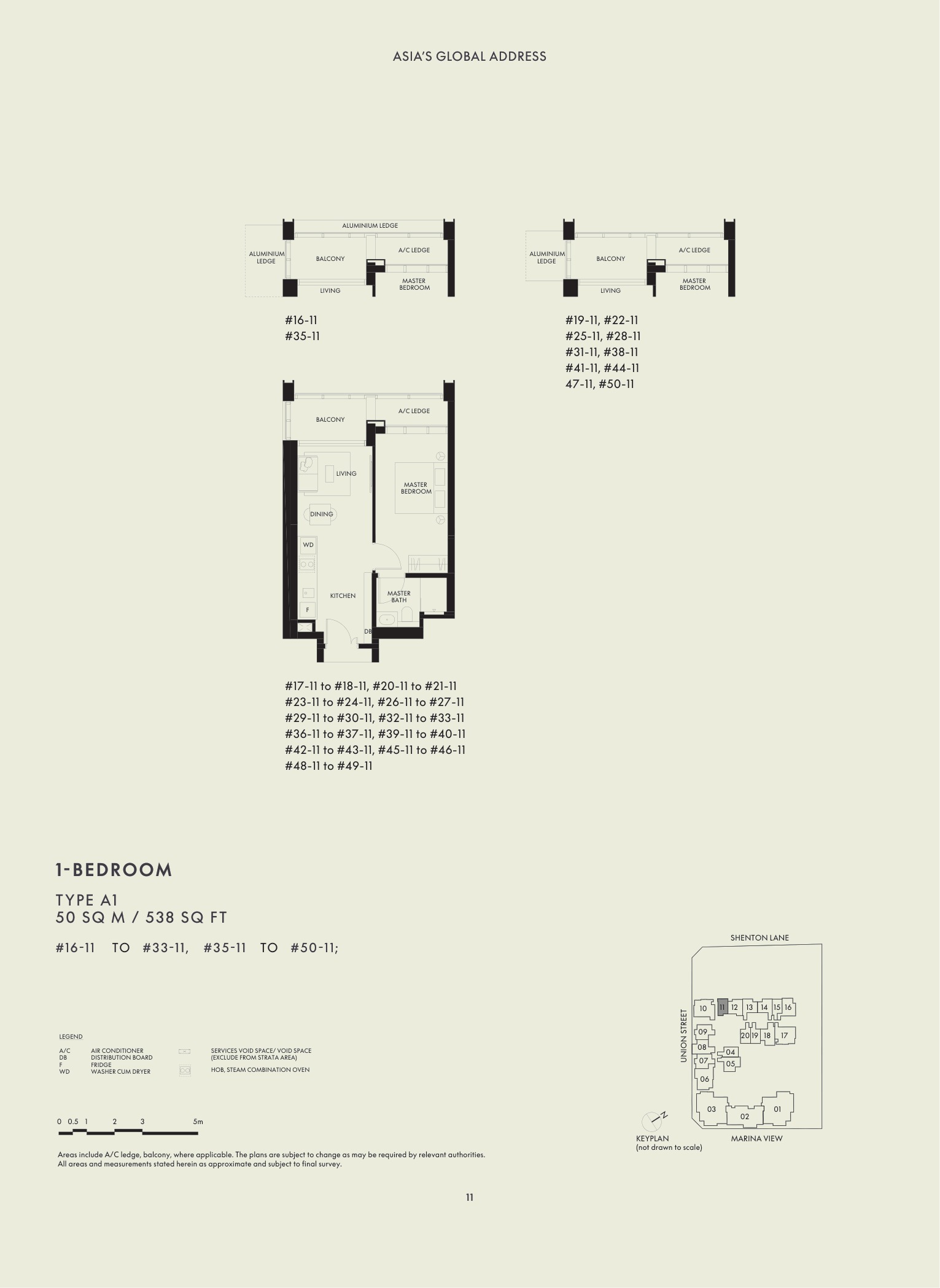

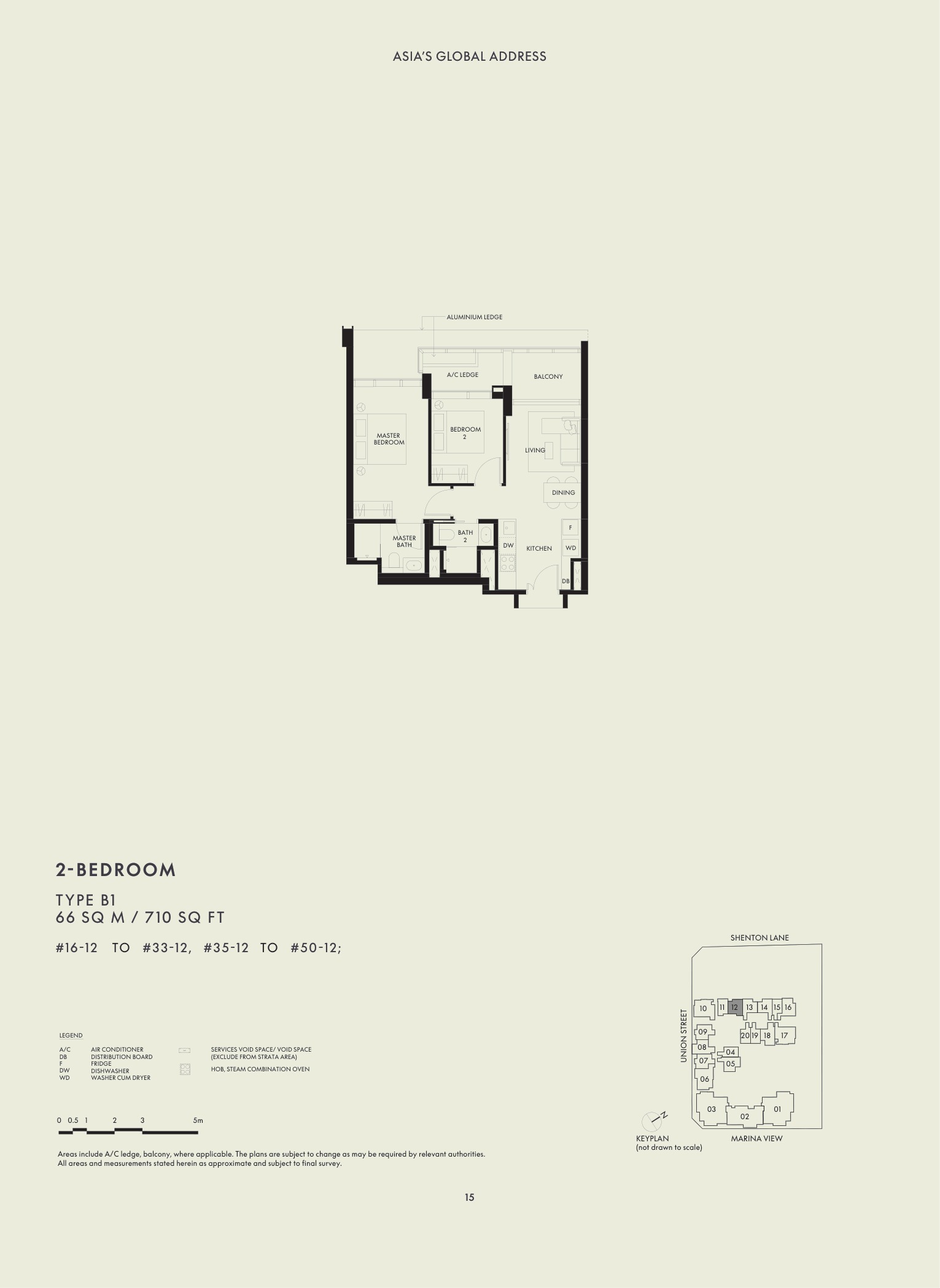

Unit Mix and Sizes

Bedroom Type

Size (sqft)

Units

% of Total

1 Bedroom

538 – 570

171

25.0%

2 Bedroom

710 – 850

310

45.4%

3 Bedroom

1,195 – 1,249

103

15.1%

4 Bedroom

2,250

32

4.7%

5 Bedroom

2,809

64

9.4%

Penthouse Simplex

5,199

2

0.3%

Penthouse Duplex

5,350

1

0.1%

Total

538 – 5,350

683

100%

Unit mix and sizes are taken from the abridged project factsheet dated 7 October 2024. Areas are approximate and subject to final survey.

Indicative Pricing

1BR

From S$1.778M

538-570 sqft

2BR

From S$2.383M

710 sqft

5BR

From S$11.360M

2,809 sqft

Current public balance-unit snapshot shows 1BR from S$1.778M, 2BR from S$2.383M, 3BR from S$3.860M, 4BR from S$8.740M and 5BR from S$11.360M. Source: W Residences Marina View NewLaunches price list updated 27 Jan 2026, accessed 29 Apr 2026.

Why Buyers Are Watching

1

First waterfront branded residence in Marina Bay — source USP notes frame the project as an early mover in Marina Bay’s new downtown.

2

Integrated W hotel living — residences sit above W Singapore Marina View, with hotel-style managed services and branded-residence positioning.

3

Five MRT stations nearby — buyer notes reference Shenton Way, Downtown, Marina Bay, Raffles Place and Tanjong Pagar MRT within walking reach.

4

Large branded-residence scale — 683 apartments enable a broad facilities programme across Levels 15, 34 and 51.

5

Views and future transformation — USP material references marina waterfront, city, Greater Southern Waterfront and Sentosa views, plus Marina Bay masterplan upside.

6

Green Mark Platinum — project document positions the project as a BCA Green Mark Platinum certified development.

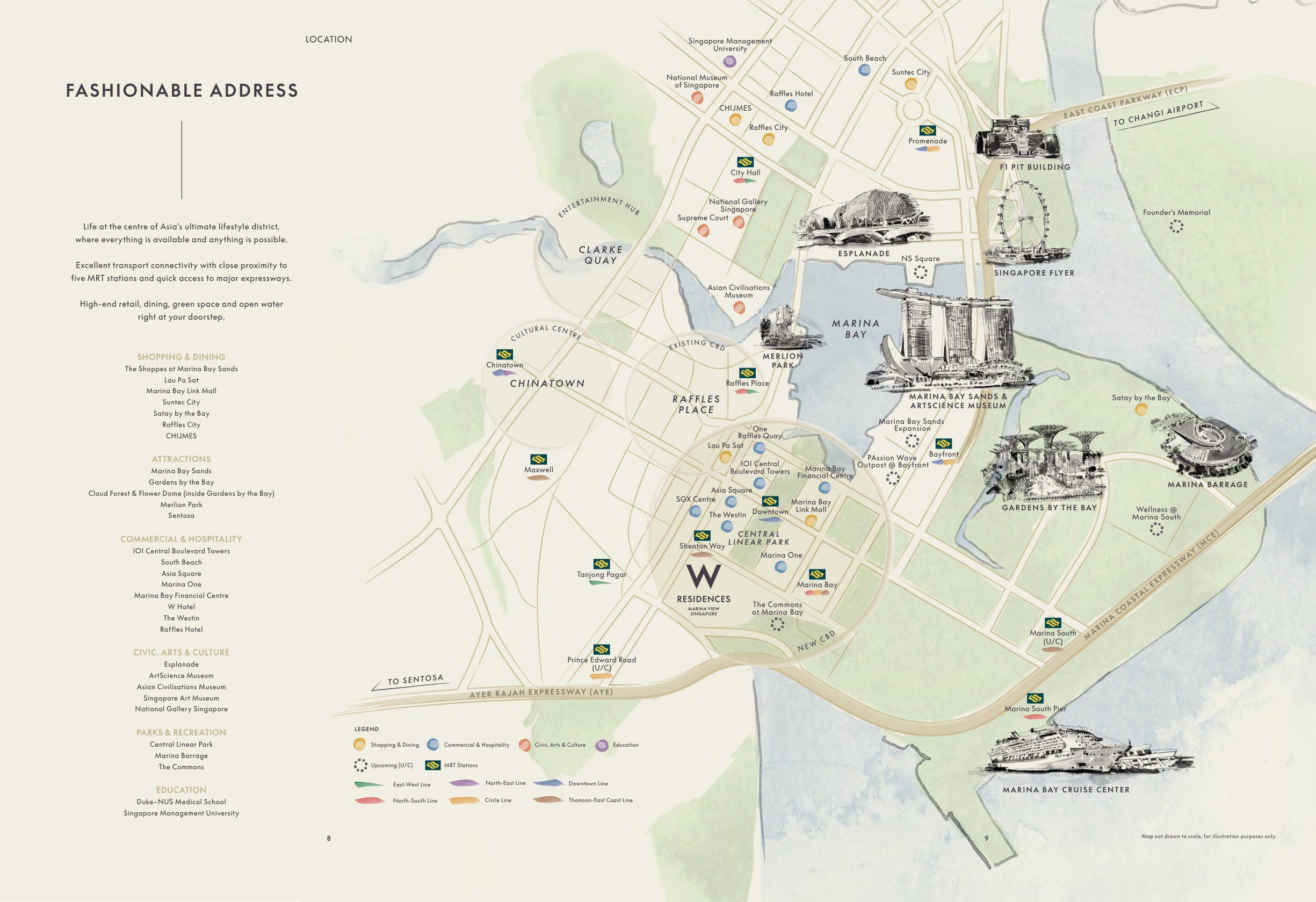

Location and Connectivity

MRT

Five station options

Shenton Way TEL is cited as a 2-minute walk; Downtown, Marina Bay, Raffles Place and Tanjong Pagar MRT are also referenced nearby.

Roads

CBD expressway access

Source connectivity notes reference quick access to MCE, AYE and KPE.

Lifestyle

Marina Bay landmarks

Gardens by the Bay, Marina Bay Sands, Esplanade, Singapore Flyer, Clarke Quay and CBD lifestyle nodes sit in the broader precinct.

Growth

New Downtown / GSW

URA Marina Bay and Greater Southern Waterfront planning remains the long-term precinct story.

Schools Nearby

School Planning

Confirm current school distance bands and eligibility with OneMap and MOE before relying on any school-distance claim.

Lifestyle and Amenities

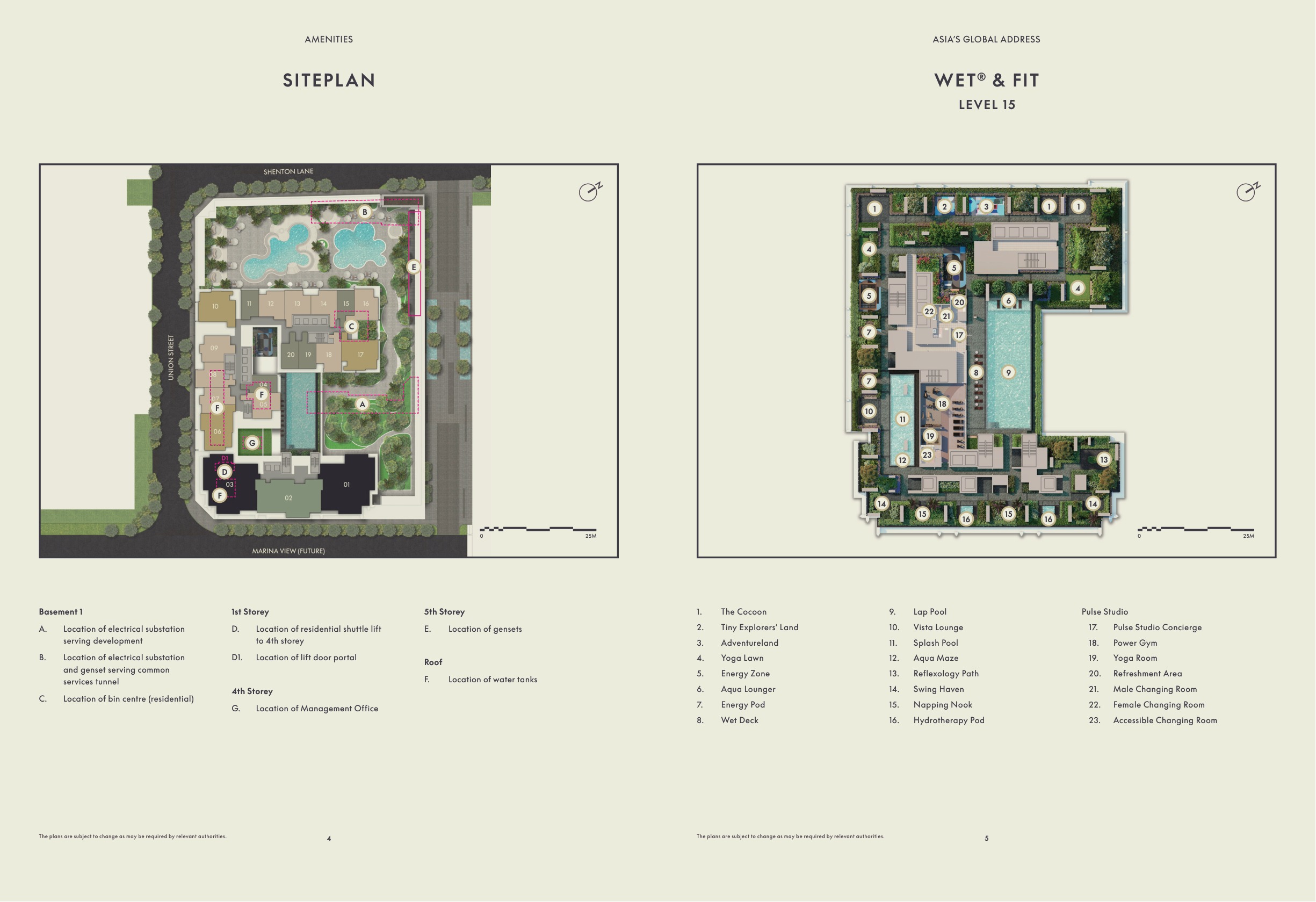

Level 15 · WET & FIT

Infinity Tranquillity Pool, sun deck, wet deck, kids’ pool, hydrotherapy pool, Power Gym, yoga room and outdoor fitness.

Level 34 · Living Room

Gourmet Pavilions, Sommelier Lounge, home cinema room, Oasis Lounge, private dining lounge and golf simulator.

Level 51 · AWAY

Sky Pool, chill deck, The Hangout, Club 51, onsen, steam room, sauna, meditation room, treatment room and Zen Garden.

Site Plan

Actual Level 15 facilities/site plan from W Residences Marina View floor-plan project document · indicative and subject to developer confirmation

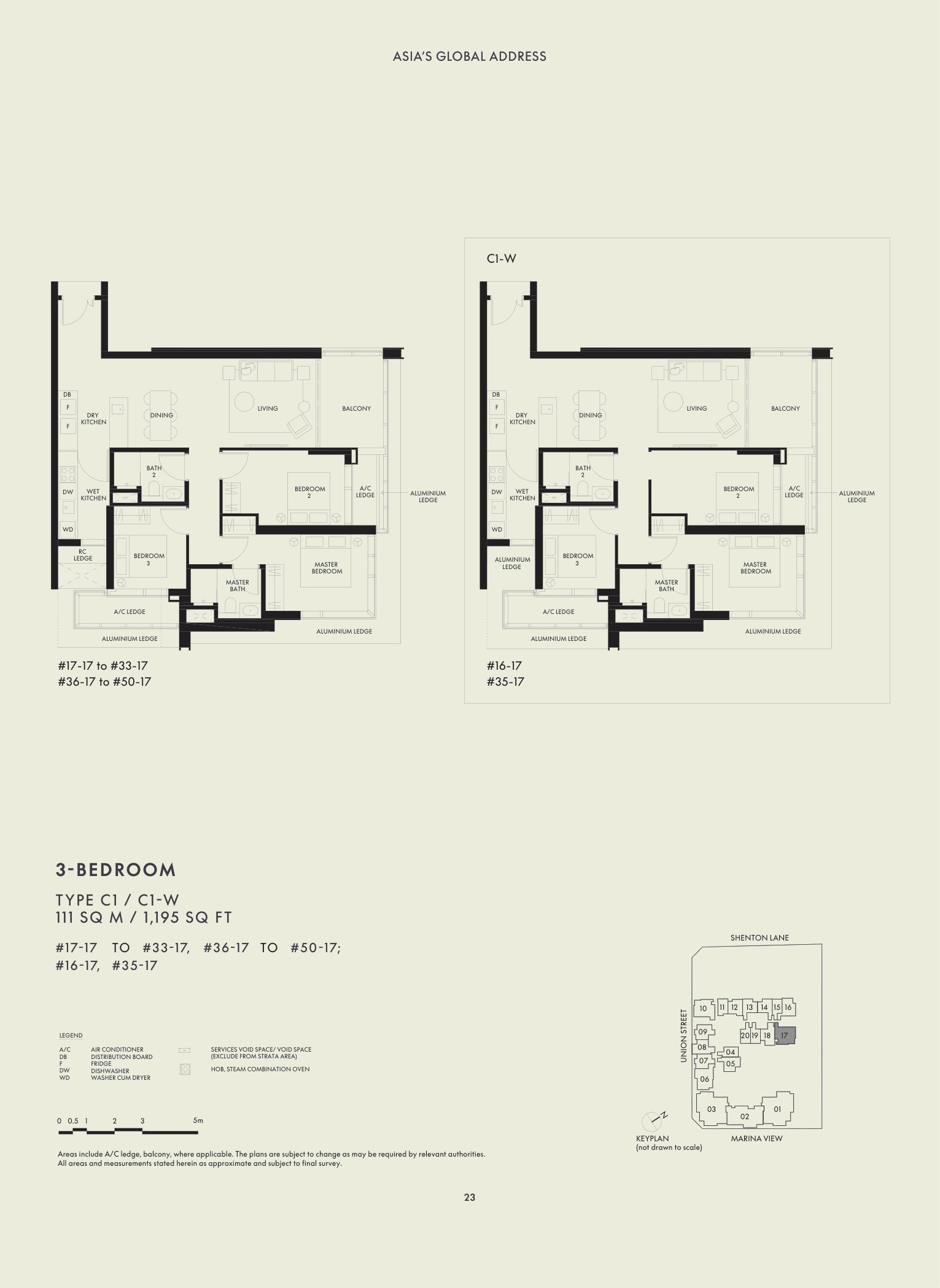

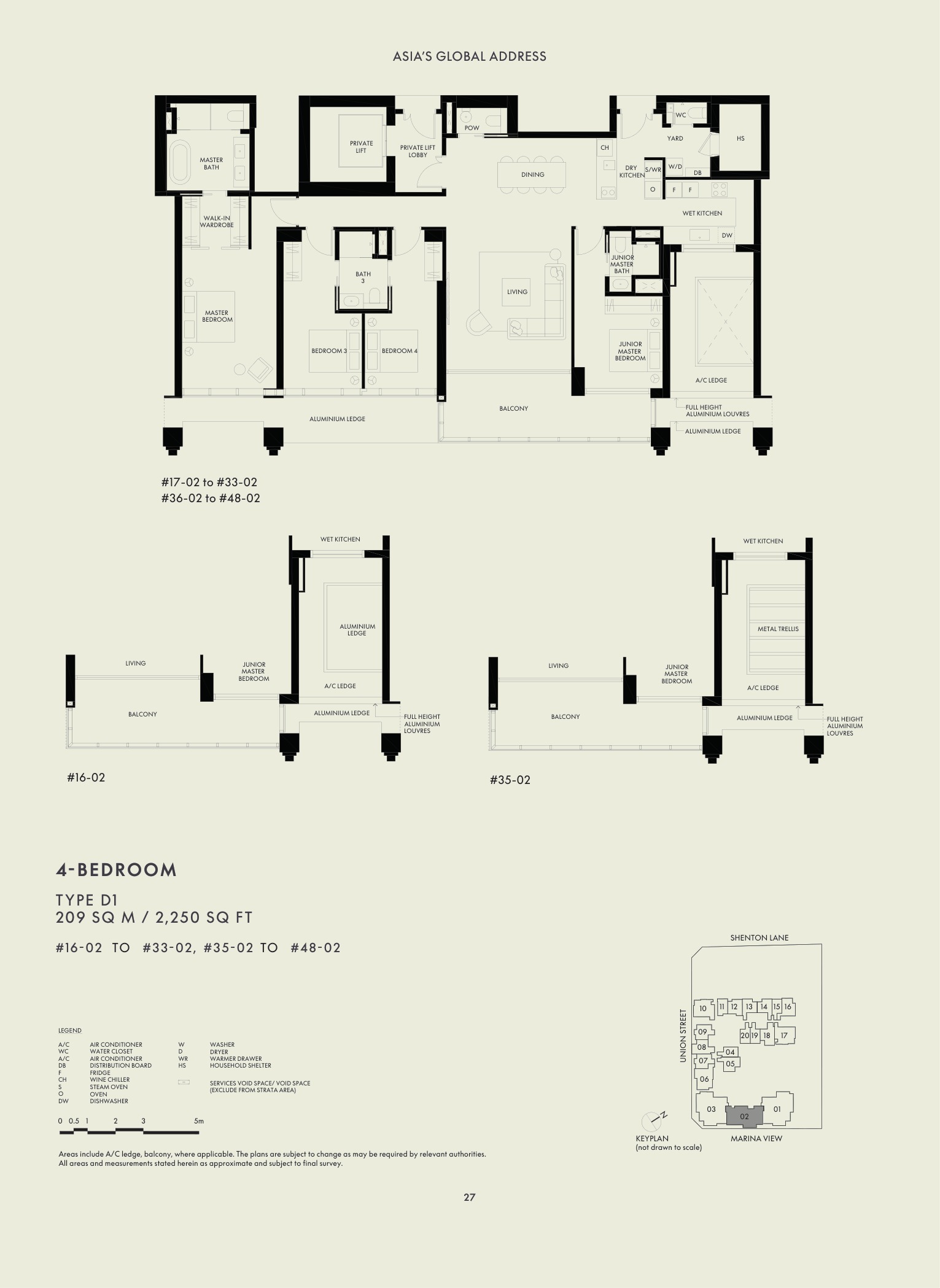

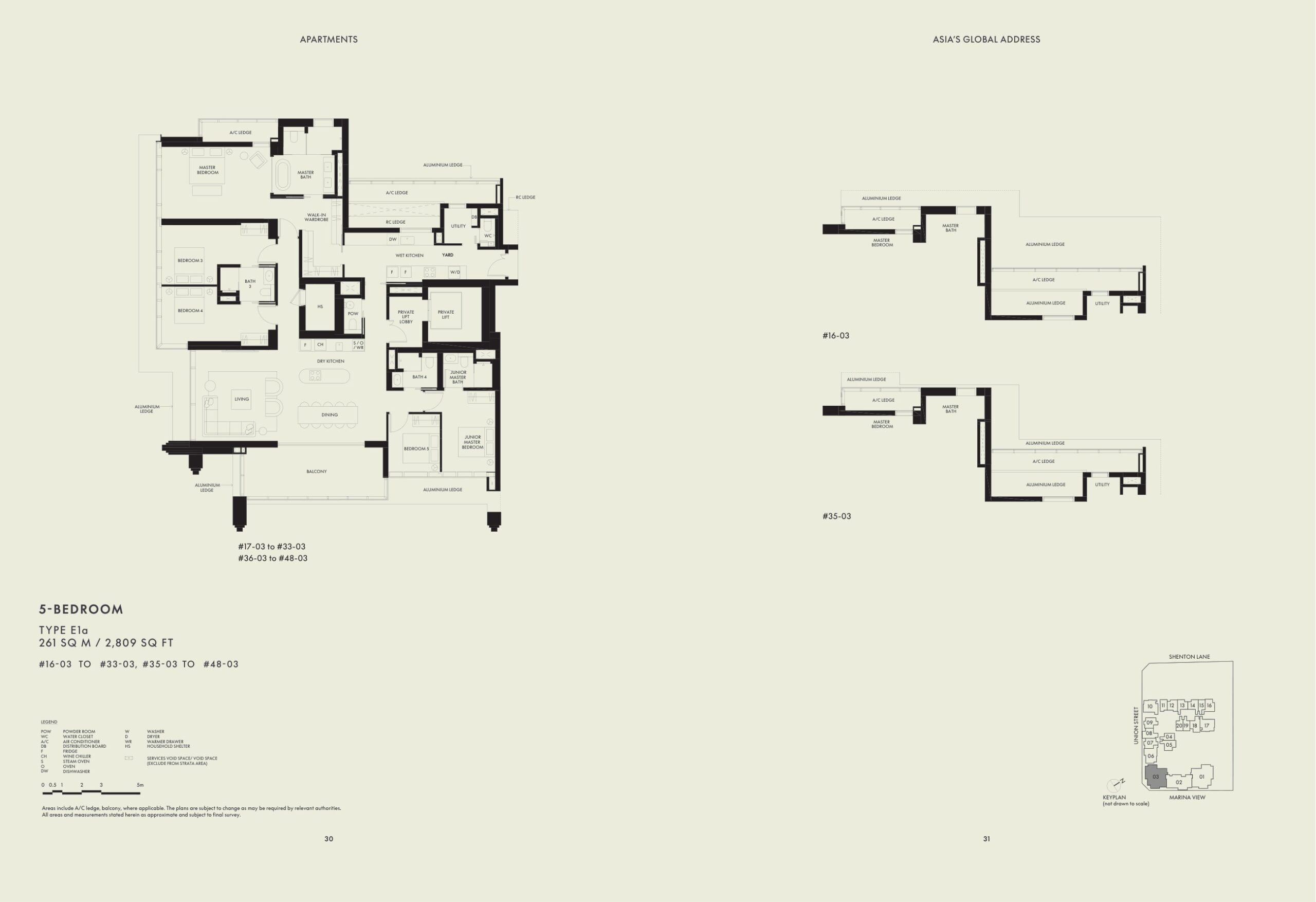

Floor Plans (Selected)

Representative actual plans by unit type. Download the clean full floor-plan PDF below for the complete selected plan pack.

1 Bedroom Type A150 sqm / 538 sqft

2 Bedroom Type B166 sqm / 710 sqft

3 Bedroom Type C1111 sqm / 1,195 sqft

4 Bedroom Type D1209 sqm / 2,250 sqft

5 Bedroom Type E1a261 sqm / 2,809 sqft

Penthouse Type PH1483 sqm / 5,199 sqft

Full Floor Plans PDF

Clean plan pack extracted from the source floor-plan PDF, excluding agency appendix pages.

The project address is 22 Marina View, near the junction of Union Street and Marina View in District 01.

Who is the developer?

The source factsheet lists Boulevard Development Pte Ltd as developer, under IOI Properties Singapore.

What is the tenure?

99-year leasehold commencing from 27 December 2021.

How many units are there?

683 residential units, with types from 1-bedroom to 5-bedroom and three penthouses.

When is the expected TOP?

The abridged source factsheet states Q1 2029, subject to developer and authority confirmation.

What is the current from-price?

Current public balance-unit snapshot shows 1BR from S$1.778M, 2BR from S$2.383M, 3BR from S$3.860M, 4BR from S$8.740M and 5BR from S$11.360M. Source: W Residences Marina View NewLaunches price list updated 27 Jan 2026, accessed 29 Apr 2026.

Ready to see W Residences Marina View in person?

Request the latest availability, price guide, floor plans and stamp-duty estimate before shortlisting.

Progressive payment, ABSD timing, and resale comparison.

DISCLAIMER: All information is compiled from developer-issued project documents and public references for informational purposes only. Prices, unit mix, specifications and timelines are indicative and subject to change without notice. This page does not constitute an offer to buy or sell. Seek advice from a licensed property agent and legal counsel. LovelyHomes.com.sg is an independent editorial platform. Agency Licence: L3010858B.

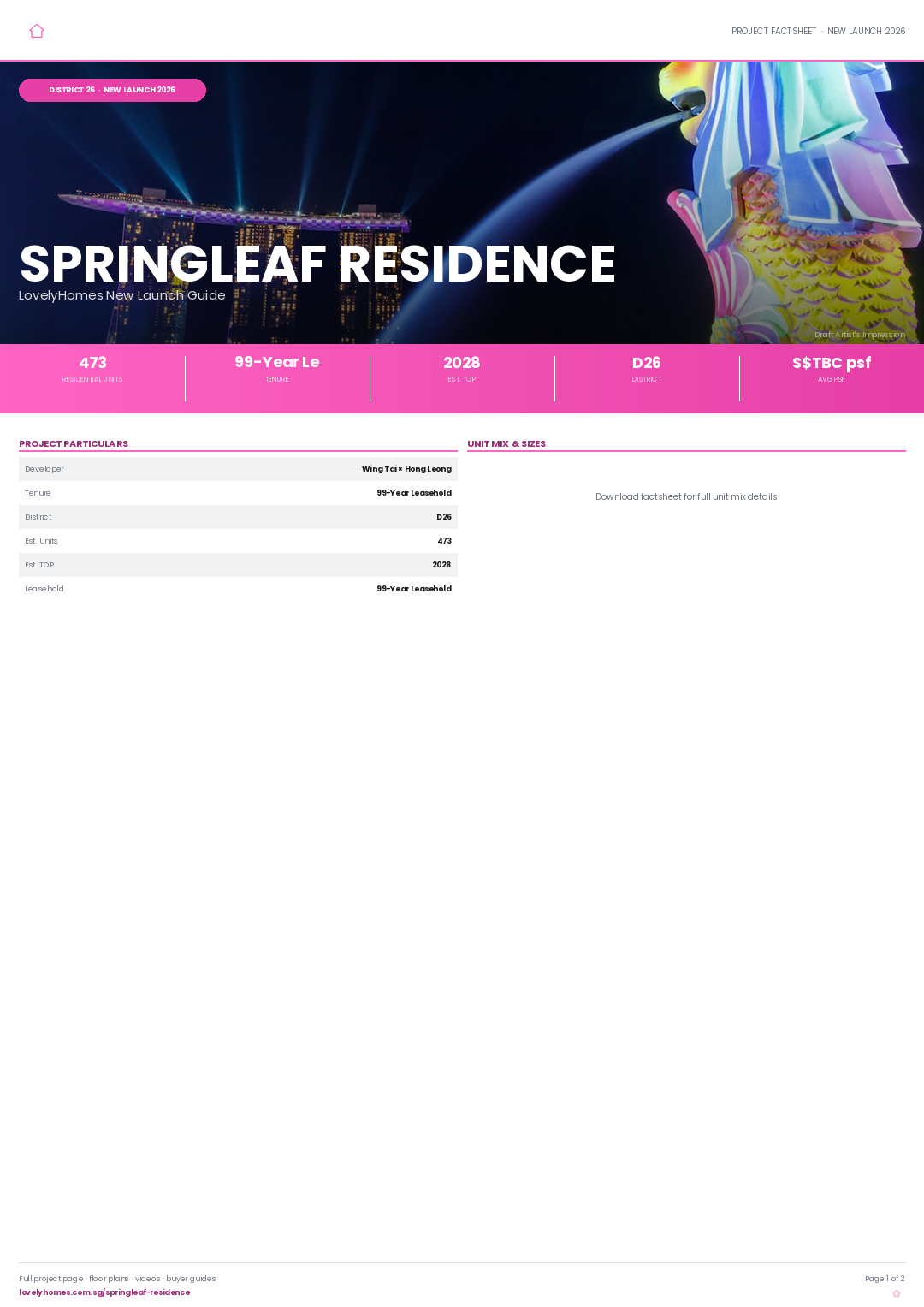

Springleaf Residence is a 473-unit 99-year leasehold residential development in District 26, Singapore, developed by Wing Tai × Hong Leong with an estimated TOP of 2028.

01 · Location

District 26 Address

Well-connected neighbourhood with access to public transport, schools, and lifestyle amenities.

02 · Scale

473 Residences

99-Year Leasehold development with quality fittings, smart-home provisions, and full condominium facilities.

03 · Value

New-Launch Advantage

Progressive payment schedule, 12-month Defects Liability Period, and modern specifications throughout.

Project At-a-Glance

Project Name

Springleaf Residence

Developer

Wing Tai × Hong Leong

District

D26

Tenure

99-Year Leasehold

Total Units

473

Est. TOP (VP)

2028

Est. Legal Completion

2031

Unit Mix and Sizes

Bedroom Type

Size (sqft)

Units

% of Total

Download the project factsheet for the full unit mix breakdown and confirmed sizes.

Refer to the developer’s official sales kit for confirmed unit types, sizes, and availability. Download factsheet (PDF).

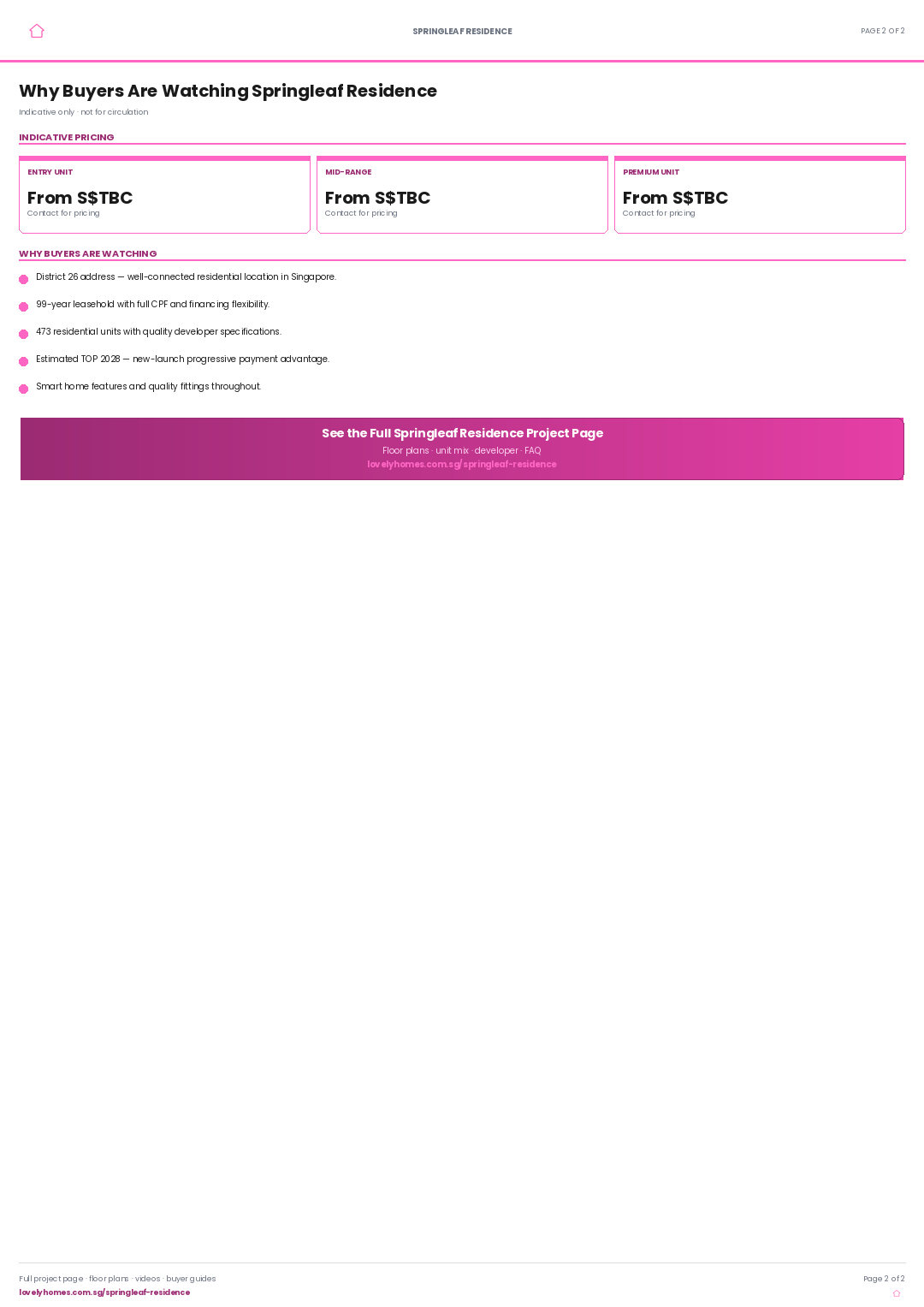

Indicative Pricing

Entry Units

S$TBC

Mid-Range Units

S$TBC

Premium Units

S$TBC

Prices are indicative and subject to change. Before ABSD, BSD, and legal fees. See our ABSD guide for stamp duty rates.

Why Buyers Are Watching

1

District 26 location — well-connected address with MRT access, expressways, and lifestyle amenities in an established residential corridor.

2

99-Year Leasehold — 99-year leasehold enabling full CPF usage and bank financing from day one.

3

473 residential units — comprehensive development with full condominium facilities and an active resident community.

4

Developer pedigree — Wing Tai × Hong Leong brings a track record of quality residential development across Singapore’s private property market.

5

Progressive payment advantage — staggered cash outlay during construction typically saves S$30,000–S$60,000 in loan interest compared to a full resale drawdown.

6

12-month Defects Liability Period — legally binding developer obligation to rectify defects at no cost within 12 months of TOP.

Location and Connectivity

Transport

MRT Access

Conveniently located near MRT stations connecting to the wider Singapore rail network.

Expressways

Road Connectivity

Access to major expressways for quick connections to the CBD, Changi Airport, and key destinations.

Lifestyle

Shopping & Dining

Nearby malls, hawker centres, supermarkets, and F&B within the immediate neighbourhood.

Schools

Education Belt

Primary and secondary schools within 1–2 km, with tertiary institutions in the broader district.

Elevation overview · indicative only · refer to developer’s official stack chart for confirmed positions

Facilities

Swimming PoolGymnasiumFunction RoomsBBQ PavilionsChildren’s PoolJacuzziClub LoungeGarden PavilionSky TerraceYoga LawnSmart Home SystemEV Charging24-Hour SecurityBicycle BaysPneumatic Waste System

Gallery

Developer and Consultant Team

Wing Tai × Hong Leong

Developer of Springleaf Residence with residential development expertise in Singapore’s private property market. Consultant team details are available in the project factsheet.

Developer

Wing Tai × Hong Leong

District

D26

Estimated TOP

2028

Sustainability and Specifications

BCA Green Mark: Designed to meet BCA Green Mark standards with energy-efficient envelope and water-efficient fittings.

Smart Home: Smart home management provisions across all units for access control and utilities.

EV Infrastructure: Electric vehicle charging provisions in basement carpark.

Quality Finishes: Premium materials and fittings in line with developer specifications throughout.

Project Timeline

2023–2024

Land Award & Licence

2024–2025

Sales Launch

2025–2028

Construction Phase

2028

Estimated TOP (VP)

2031

Legal Completion

Project Factsheet

A shareable 2-page PDF snapshot — bring it to viewings, share with family.

DISCLAIMER: All information is compiled from publicly available sources and developer-issued materials for informational purposes only. Prices, unit mix, specifications, and timelines are indicative and subject to change without notice. This page does not constitute an offer to buy or sell. Seek advice from a licensed property agent and legal counsel. LovelyHomes.com.sg is an independent editorial platform. Agency Licence: L3010858B.

HDB’s May 2026 Build-To-Order launch is expected to open for application in the first week of May, the second launch of the year after the February 2026 exercise. Based on the sites gazetted through URA Government Land Sales in late 2024 and 2025, and on pre-launch developer briefings released by HDB, we preview the likely site mix, expected application rates, and the first-timer vs second-timer allocation picture.

At a glance

May 2026 BTO is expected to launch approximately 6,800 flats across Standard, Plus and Prime categories.

Confirmed launch sites include Bukit Merah (Henderson), Tampines (Tampines North), Tengah (Garden District) and Woodlands (Woodlands North Coast).

Bukit Merah Henderson is the category headliner — Prime location classification; expect application rates above 10x for 4-room.

Family grant framework (Enhanced CPF Housing Grant, Family Grant, Proximity Housing Grant) applies; first-timer ballot weights unchanged.

Applications typically close 7 days after opening; ballot results announced 4–6 weeks later.

What a Plus / Prime BTO classification means for May buyers

The Plus and Prime classifications — introduced under the revised 2024 HDB framework — replace the legacy Mature / Non-Mature framework for new BTO launches. Standard flats follow the traditional BTO rules. Plus flats, typically in choice non-mature locations, carry a 10-year Minimum Occupation Period (up from 5) and subsidy clawback on resale. Prime flats, in the most central and amenity-rich locations, carry the same 10-year MOP plus a resale income ceiling that applies when the flat is eventually sold.

Buyers should model the full hold cycle before ballot. A Prime classification delivers an under-market purchase price and exceptional location, but the 10-year MOP plus resale-income-ceiling combination narrows the eventual buyer pool at exit. For households expecting to stay in the flat 15–20 years, the Prime route is straightforward. For households planning a shorter trade-up, the Standard category is typically the better fit.

Site-by-site expectations

Bukit Merah (Henderson) — Prime classification

Estimated launch: approximately 1,200 flats, 4-room and 5-room mix. The site sits on Henderson Road, about a 5-minute walk from Redhill MRT (East-West Line) and within walking distance of Dawson Estate and Bukit Merah Central. The Prime designation is expected to deliver a substantial price discount vs the adjacent resale market, where four-room flats are transacting in the S$850–S$1,050k band. Expect application rates for 4-room flats above 10x on the first-timer pool.

Tampines (Tampines North) — Plus classification

Estimated launch: approximately 1,600 flats, full mix from 2-room Flexi to 5-room. The site is adjacent to the Tampines North MRT (Cross Island Line Stage 1, opened late 2024) and sits in a growing mixed-use district bracketed by Tampines Regional Centre and Tampines North Park. The Plus classification carries a 10-year MOP but no resale-income ceiling. Expect application rates of 4–6x on 4-room flats.

Tengah (Garden District) — Standard classification

Estimated launch: approximately 2,400 flats, the largest single-site batch of the May 2026 launch. The Tengah Garden District is the western master-planned town pioneered as Singapore’s first car-free town centre. The Jurong Region Line MRT is under construction with stations expected to open progressively from 2027 through 2029. Expect application rates of 2–3x on 4-room flats given the larger supply and the longer MRT wait.

Woodlands (Woodlands North Coast) — Standard classification

Estimated launch: approximately 1,600 flats. The Woodlands North Coast site benefits from the recently opened Thomson-East Coast Line terminus at Woodlands North, cross-border connectivity via the under-construction Johor Bahru-Singapore Rapid Transit System, and the still-developing Woodlands Regional Centre. Expect application rates of 2–3x on 4-room flats.

First-timer, second-timer and quota mechanics

HDB ring-fences a majority of every launch for first-time applicant families — specifically, at least 85% of four-room and larger Standard flats are reserved for first-timer families. Two-timer applicants (families who already own or have previously owned an HDB flat, EC or private property) compete for the remaining quota and typically face ballot odds 2–4x longer than first-timers. Singles and first-timer families under the joint application framework are balloted separately under the 2-Room Flexi scheme.

Prime and Plus flats have the same general first-timer preference but with a further stratification: households with household income under the relevant bracket receive the CPF Housing Grant stack, which can add up to S$80,000 in grants depending on income-group position.

Application tactics for a strong ballot position

Three behavioural points the HDB system rewards. First, ballot entry across multiple launches does not compound — each launch is a fresh lottery. But second-timers who roll over their application to a next launch do receive a small priority-weighting uplift, capped at two rollovers. Second, the Proximity Housing Grant (S$30,000 for applying to live with or near parents) is a strong signal to the ballot system and materially improves odds at Bukit Merah Henderson and Tampines North. Third, the Enhanced CPF Housing Grant is income-tiered — the lowest income tier receives the largest grant, which influences eligibility for Standard categories.

Expected timeline

What May 2026 means for the resale market

A May launch of approximately 6,800 flats is a moderate supply pulse into the BTO pipeline, but the immediate effect on resale is indirect. In the short term, first-timer applicants who commit to a BTO ballot typically withdraw from active resale viewings while waiting for the result, which softens resale transaction volume for 4–6 weeks. If ballot rates are high (as expected for Bukit Merah Henderson), disappointed applicants often re-enter the resale market in late June, which typically produces a small transaction bounce in July. This pattern has been consistent across the last six BTO launch cycles.

Frequently asked questions

When exactly does the May 2026 BTO open for application?

HDB typically announces the exact launch window approximately two weeks before applications open. Based on past May launches, the window usually falls in the first 10 days of May, with applications closing roughly 7 days after opening.

Can I apply for both a BTO and a resale flat at the same time?

You can apply for a BTO while viewing resale flats, but you cannot hold a BTO booking and simultaneously enter a resale HDB agreement. Most applicants use the BTO ballot window to continue resale research; successful balloters decline at booking if they have already committed to a resale.

How much is the ABSD and BSD on a BTO flat?

BTO flats are sold directly by HDB under the Housing & Development Act. Buyers’ Stamp Duty applies on the purchase price at the standard schedule. Additional Buyer’s Stamp Duty does not apply to first-timer BTO applicants buying their first residential property.

What is the difference between Plus and Prime?

Both carry a 10-year MOP and subsidy clawback on sale. Prime adds a resale-income-ceiling constraint at exit — the eventual resale buyer must meet an income ceiling. Plus has no such eventual-buyer constraint.

Can PRs apply for BTO flats?

PR-only households cannot apply for a BTO. A Singapore Citizen applying with a PR spouse or family nucleus can apply under the HDB Fiancé/Fiancée, Family or Joint Singles scheme.

What happens if I decline the allocated BTO flat?

Declining a BTO selection appointment has consequences for future applications: after two non-selections in a 12-month period, HDB may debar the applicant from applying for BTO for a period of up to 12 months. Plan your ballot portfolio carefully.

Source

Source: HDB public information on the BTO launch framework and 2024 revised category system, URA GLS announcements, and public site-gazetting records. Full documentation: HDB BTO flat selection and URA GLS current sites.

Editorial note. This article is based on public-domain data released by HDB, URA, Singapore Land Authority and MAS as at 23 April 2026. All analysis is our own. No marketing-agency research is cited. Figures may be revised in subsequent official releases — always refer to the latest authoritative source before making a housing decision.

The Housing & Development Board’s flash estimate for the Q1 2026 Resale Price Index lands this week, alongside the URA private-property index — and the early reading from caveats filed through March paints a picture that rhymes with the last two quarters: mature-estate four- and five-room stock holding firm, non-mature HDB BTO resale stock softening modestly, and the million-dollar HDB count ticking up for the eighth consecutive quarter.

At a glance

HDB’s Q1 2026 flash RPI print is expected to come in at +0.9% QoQ, following +1.1% in Q4 2025 and +1.4% in Q3.

Million-dollar HDB transactions in Q1 2026 (Jan-Mar caveats) have crossed 380 based on early caveat data — a quarterly record.

Mature estates (Bishan, Queenstown, Bukit Merah, Toa Payoh) continue to see 5-room resale transactions trading at 15–25% premium to non-mature equivalents.

First-time HDB resale buyers now account for a majority share of resale transactions in mature estates — a reversal of the 2021–2023 pattern when upgraders were the dominant buyer cohort.

Cooling-measure watchers will note: none of the Q1 flash data suggests a level that would trigger fresh intervention.

The headline: deceleration, not decline

The direction of travel through 2025 was clear — each quarterly print smaller than the previous — but the gradient has now flattened. The Q1 2026 +0.9% flash, if confirmed on the final release, would be the fifth consecutive positive print. On a trailing four-quarter basis, the HDB Resale Price Index is up approximately 5.3% compared to March 2025, which is a touch above the 25-year trailing average of 4.1% per annum and well below the 10.7% CAGR of the post-pandemic recovery window from 2021 to 2023.

The deceleration pattern is most visible in non-mature estates. Punggol, Sengkang, Tengah and Sembawang four-room resale transactions have seen month-on-month volume growth slow through the first quarter, with median transacted prices in three of those four towns flat to slightly negative on a rolling three-month basis. Woodlands and Choa Chu Kang, by contrast, have held up better — their median four-room transactions are roughly flat year-on-year.

The mature-estate premium keeps widening

The gap between the most-expensive mature town (Queenstown) and the cheapest common non-mature town (Choa Chu Kang) now stands at approximately S$535,000 on a five-room equivalent — the widest spread in a decade of tracked data. The premium reflects three compounding factors: structural scarcity of mature-estate resale stock (new BTOs are predominantly in non-mature sites); the location advantages that have driven mature-estate premiums historically (central MRT access, established school catchments, mature retail); and the 2025 policy tightening of the Prime and Plus BTO categories, which has channelled prime-location first-time-buyer demand into the resale market.

Million-dollar HDB transactions cross 380

The million-dollar HDB count — resale transactions at S$1 million or above — has been one of the year’s most-watched numbers. Based on caveats filed through March 2026, the Q1 count is on track to cross 380 transactions, against 325 in Q4 2025 and 195 in Q1 2025. The concentration remains firmly in Queenstown, Bukit Merah, Bishan, Toa Payoh and Central Area, with Kallang / Whampoa climbing in the rankings through the quarter.

Why million-dollar HDB matters

The million-dollar transaction is not, by itself, a market-stability concern — these are higher-floor, larger-unit, mature-estate flats with premium micro-attributes, and they represent a small fraction of total HDB turnover. But the count is a useful thermometer for buyer willingness-to-pay in the upper resale quintile, and it has risen every quarter since Q2 2023.

The buyer mix has quietly inverted

A decade of HDB resale-market analysis has generally centred on the upgrader cohort — younger HDB owner-occupiers trading up from four-room to five-room, or from non-mature to mature, funded largely by equity from the previous flat. That cohort dominated the 2021–2023 market.

The composition has quietly inverted through 2025 and into Q1 2026. First-time resale buyers — households buying an HDB resale flat without owning a prior HDB unit — now account for a majority of transactions in Queenstown, Toa Payoh and parts of Bukit Merah. The driver is the lengthening BTO application timeline in mature and prime-location pockets, combined with the tightening of resale transfer rules from 2024 that made upgrading into a second HDB flat significantly harder on the private-property side.

Mortgage affordability: the real constraint

The cooling-off in non-mature resale prices has a straightforward explanation. Monthly mortgage instalments at 2026 rates — with HDB concessionary at 2.6% and most private floating packages around 3.3–3.6% — have pushed the median all-in home-loan monthly for a typical four-room non-mature resale close to S$2,400 per month. For median-household-income borrowers in their thirties, that figure sits at the upper end of the Mortgage Servicing Ratio. Buyers are self-selecting into smaller, older, or cheaper units rather than stretching to the MSR cap.

What to watch in Q2

Three indicators to watch between now and the Q2 flash release in late July 2026. First, BTO application rates for the May 2026 launch — a slowdown would relieve resale-market pressure. Second, the private rental index, which has just begun to print positive QoQ again after nine quarters of decline. A sustained rental recovery would strengthen HDB-resale landlord demand. Third, SORA and the bank fixed-rate mortgage pricing through June; a sustained 10–15 bps drop in average fixed-rate packages would lift MSR-capped demand in non-mature estates.

Frequently asked questions

What is the HDB Resale Price Index?

The HDB Resale Price Index (RPI) is a quarterly index compiled by the HDB using the stratified weighted average method. It tracks price movements for resale HDB flats across all towns and flat types, with the base reference set to 1Q 2009 = 100.

Why does the index show growth when my estate has seen prices flat?

The RPI is a national aggregate. Individual towns can diverge materially from the national print. Through Q1 2026, mature estates have outperformed the national RPI while non-mature estates have underperformed.

Does a ‘million-dollar HDB’ transaction mean the market is overheated?

Not directly. Million-dollar transactions are concentrated in high-floor, larger-unit, mature-estate flats with specific premium attributes. They represent roughly 2% of quarterly HDB resale turnover. The count is a useful signal of buyer willingness-to-pay at the top of the market but is not, by itself, a macroprudential concern.

When is the final Q1 2026 RPI released?

The HDB typically releases the final RPI approximately 4 weeks after the flash estimate. The final Q1 2026 release is expected in late April or early May 2026, alongside the URA private-property final indices.

Should I buy an HDB resale now or wait for the next BTO?

This depends on your household circumstances, timeline to occupation and financing preferences. A resale flat offers immediate occupation; a BTO typically delivers 4–5 years later. Our BTO vs resale comparison covers the trade-offs in detail.

Source

Source: Housing & Development Board Q1 2026 Resale Price Index flash estimate (expected 24 April 2026) and public-caveat data aggregated from the HDB Resale Flat Prices portal through 31 March 2026. Full methodology: HDB press releases.

Editorial note. This article is based on public-domain data released by HDB, URA, Singapore Land Authority and MAS as at 23 April 2026. All analysis is our own. No marketing-agency research is cited. Figures may be revised in subsequent official releases — always refer to the latest authoritative source before making a housing decision.

The Progressive Payment Scheme (PPS) is the default payment structure for new-launch private residential property in Singapore. Under the scheme, you pay a small deposit on booking, incremental tranches as construction reaches each milestone, and the final balance only when the keys are handed over at TOP. This 2026 guide walks through each stage, the CPF and cash flow at every milestone, and the practical cash-flow implications for a typical Singapore buyer.

Quick Answer

The Progressive Payment Scheme spreads purchase payments across seven construction milestones, from OTP booking to CSC (final 12-month defect period).

On launch day you pay 5% in cash (the Option fee). Within 8 weeks you pay a further 15% on Sale & Purchase signing — of which up to 5% may be from your CPF Ordinary Account.

The remaining 80% is drawn progressively from your home loan as construction reaches foundation, walls, ceiling/roof, TOP and CSC.

Monthly mortgage payments begin after the first drawdown — not on the day you sign the OTP.

PPS is the default for new-launch condominiums. The Deferred Payment Scheme (DPS), where available, pushes the bulk of payments to TOP but typically carries a price premium and stricter eligibility.

What is the Progressive Payment Scheme?

The Progressive Payment Scheme is the payment structure prescribed by the Urban Redevelopment Authority for property sold in the primary market under the Housing Developers (Control and Licensing) Act. Under PPS, the purchase price is paid in incremental tranches timed to construction milestones, rather than in a single lump sum at handover. The structure exists for two reasons: it reduces the buyer’s financing burden during the 3–4 year build period, and it gives the developer progressive cash-flow to fund construction without requiring 100% escrow.

PPS applies to all uncompleted private residential property purchased directly from the developer. For completed-and-TOP-issued stock sold in the primary market, the payment structure is different — typically the full balance is due within 12 weeks of OTP.

The seven PPS milestones

Stage 1 — Option to Purchase (5% in cash)

On launch day, you pay a 5% Option fee to the developer in cash or cashier’s order. This secures your right to purchase the specific unit for a 3-week Option period. During this window, you finalise financing, commission a conveyancing lawyer and decide whether to proceed. If you do not exercise the Option, you forfeit 1.25% of the Option fee (one-quarter of the 5%) and the developer returns the balance 3.75%.

Stage 2 — Sale & Purchase Agreement (15% within 8 weeks)

Within 8 weeks of Option exercise, you sign the Sale & Purchase Agreement and pay a further 15% of the purchase price. A typical split is 5% in additional cash and 10% from CPF Ordinary Account, though this varies by buyer. At this stage, you also pay Buyer’s Stamp Duty and, if applicable, Additional Buyer’s Stamp Duty to IRAS — due within 14 days of S&P signing.

Stage 3 to 5 — Construction-linked draws (45% total)

Once construction reaches each milestone, the developer issues a payment notice. Your home-loan bank draws down against your loan facility to pay the developer directly. Monthly mortgage instalments begin on the bank side after the first drawdown. The three construction-linked milestones are: foundation complete (10%); reinforced concrete framework, carpark and partition walls complete (10%); ceiling, roof and external wall complete with windows installed (25%). Typical elapsed time between Stage 2 and Stage 5 is 24–30 months for a mid-size project.

Stage 6 — TOP and key handover (25%)

When the Temporary Occupation Permit is issued, the developer notifies the buyer. You pay the next 25% tranche and receive the keys. You can now occupy the unit, lease it out, or commission renovation work. The MCST (management corporation strata title) is also constituted at or shortly after this milestone, and your monthly maintenance-fee obligation begins.

Stage 7 — Certificate of Statutory Completion (10%, within 12 months)

The final 10% is held back and released when the Certificate of Statutory Completion is issued — typically within 12 months of TOP. CSC confirms that all building works conform to the approved plans and that the defects-liability period has been honoured. This hold-back is the buyer’s main leverage during the first-year defects period, and you should work through your defects snag list methodically before authorising the final tranche.

How the CPF + cash + loan split actually works

The payment split varies by buyer, but a common structure for a Singapore Citizen first-time buyer is:

The 5%/15% split at the front of the scheme is not legally fixed — it is the default under URA rules. A buyer with additional CPF headroom may redirect more of Stage 2 from cash to CPF. A buyer with limited CPF but strong cash flow may pay Stage 2 entirely in cash. Your conveyancing lawyer will confirm the precise split on your S&P, and your bank’s mortgage specialist will coordinate the CPF withdrawal application.

Worked example — S$2,000,000 purchase

Consider a Singapore Citizen first-time buyer purchasing a S$2 million new-launch condominium under PPS. Total BSD is S$64,600, ABSD is nil on a first property.

BSD (paid in 14 days): S$ 64,600 (from cash or CPF)

Upfront total (weeks 0-8):

Cash required: S$ 200,000 – 264,600

CPF required: S$ 200,000 – 264,600

Stages 3-7 (24-48 months):

80% loan drawdown: S$1,600,000 (monthly instalment from first drawdown)

Approx. monthly mortgage at 3.5% / 30 yrs on S$1.6M:

Full-loan equivalent: S$ 7,184 per month

Starts: After Stage 3 first drawdown, scales as loan balance grows

Note two things. First, the BSD payment at Stage 2 is often overlooked in cash-flow planning. A S$2 million purchase carries approximately S$64,600 of BSD due within 14 days of S&P — a buyer who has budgeted only the 5% cash at OTP is likely to be caught short. Second, the monthly mortgage payment ramps up over the construction period: from roughly S$900 per month after Stage 3 (10% of loan drawn) to the full S$7,184 once all drawdowns are complete at TOP.

How monthly mortgage payments scale across milestones

This ramp is the single most important cash-flow feature of PPS. A buyer who qualifies on the full-loan TDSR check still has a much lighter monthly burden in the first 18–24 months of construction, which can be useful for offsetting stamp duty and renovation savings.

PPS vs Deferred Payment Scheme (DPS)

For completed inventory of some developments — particularly foreign-developer-owned assets and late-cycle unsold stock — developers sometimes offer a Deferred Payment Scheme as an alternative. Under DPS, the buyer pays 20% at OTP and S&P combined, defers the remaining 80% to TOP (or up to 3 years later for completed units), and takes no home-loan drawdowns during the deferral period.

DPS improves short-term cash flow at the cost of a slightly higher purchase price. For a buyer expecting a large cash event (bonus, asset sale, parental gift) at TOP, DPS can make sense. For a buyer with steady cash flow through the construction period, PPS is materially cheaper on a total-cost basis.

Common pitfalls to avoid

Pitfall 1 — Budgeting only the 5% at OTP

The 5% OTP is not the upfront cost. You need 20% plus BSD/ABSD in the first 8 weeks. Add renovation, agent, legal and moving costs and you are looking at 22–25% of purchase price in the first 12 weeks, not 5%.

Pitfall 2 — Forgetting BSD is due 14 days after S&P

BSD is not paid at TOP. It is due within 14 days of S&P signing. On a S$2M purchase that is S$64,600 — budgeted separately from the 20% downpayment.

Pitfall 3 — Mixing up loan disbursement schedule with own cash flow

The bank draws your loan on the developer’s notice — you do not pay the developer directly. But the bank’s monthly instalment on the drawn loan balance comes out of your account from the first drawdown.

Pitfall 4 — Releasing the CSC tranche before defects are fixed

The final 10% is your main leverage during the 12-month defects-liability period. Work through the snag list methodically and only authorise CSC release when outstanding defects are resolved or formally noted.

The PPS stamp-duty timing gotcha

Buyer’s Stamp Duty and Additional Buyer’s Stamp Duty are payable within 14 days of the dutiable instrument. For a new-launch PPS purchase, the dutiable instrument is the Sale & Purchase Agreement signed at Stage 2 — not the Option to Purchase signed at Stage 1. This timing nuance matters for three reasons.

First, you have a measurable planning window — roughly 10 weeks from launch day — to assemble the cash to pay both the Stage 2 downpayment and the stamp duty. Second, the ABSD exemption application window (for married couples claiming spousal ABSD remission, for example) opens at the S&P stage, not at OTP. Third, if the government announces a cooling-measure change between OTP and S&P, the stamp-duty rate that applies is the rate in force on the S&P date, not the OTP date. This has historically been a source of significant buyer anxiety during cooling-measure cycles.

Frequently asked questions

1. Do all new-launch private condominiums in Singapore follow PPS?

Yes. PPS is the default payment structure prescribed by URA for uncompleted private residential property sold in the primary market. Deferred Payment Scheme alternatives are available only for completed or late-cycle inventory at the developer’s discretion.

2. When does my monthly mortgage payment start?

Your monthly mortgage payment starts after the first loan drawdown — typically at Stage 3 (foundation complete), which is usually 6–12 months after S&P signing. Until the first drawdown, you pay no mortgage instalment.

3. Can I pay the whole purchase price upfront?

No. URA rules require the developer to collect payment against milestones under PPS, and a lump-sum upfront payment is not permitted on a new-launch uncompleted unit. You can, of course, make an agreed partial pre-payment on your home loan at any time once the loan has been drawn.

4. What happens if I cannot meet a progress-payment milestone?

Your loan facility covers the milestone drawdowns automatically — the bank pays the developer against your loan balance. The mortgage instalment comes out of your bank account monthly. A genuine default scenario would only arise if your monthly cash flow cannot service the mortgage instalment. Speak to your bank immediately if this looks likely; options typically include a short-term restructure or, in extreme cases, a resale exit.

5. Can I use CPF for the 5% OTP booking fee?

No. The 5% OTP must be paid in cash or cashier’s order. CPF can be used from Stage 2 onwards, subject to the Valuation Limit and Withdrawal Limit framework.

6. When is ABSD payable under PPS?

ABSD (and BSD) is payable within 14 days of signing the Sale & Purchase Agreement at Stage 2, not at OTP. Budget the stamp duty separately from the Stage 2 downpayment.

7. What is the Option fee forfeiture if I do not exercise the OTP?

One-quarter of the 5% Option fee — 1.25% of the purchase price — is forfeited to the developer. The remaining 3.75% is returned within a reasonable period. This is the standard URA-prescribed position and cannot be waived.

8. Does PPS apply to Executive Condominiums?

Yes. Executive Condominiums follow the same PPS milestones as private condominiums. The main EC-specific difference is eligibility and resale-restriction rules on the buyer side, not on the payment-schedule side.

9. Does PPS apply to HDB BTO flats?

No. HDB BTO flats follow a different payment schedule: 10% Option fee at booking (mostly from CPF), then the balance at key collection. Construction-linked progressive drawdowns do not apply to BTO.

10. How long does the full PPS cycle take?

Typically 3–4 years from OTP to CSC for a mid-size project: 2–3 months from OTP to S&P, then 24–36 months through construction to TOP, then a further 12 months to CSC.

11. Can I sell the unit before TOP?

Yes, subject to the standard resale rules for private property. You can sell the uncompleted unit to another buyer via a ‘sub-sale’ arrangement, with the original buyer’s obligations novated to the new buyer. The Seller’s Stamp Duty framework applies on the gain, and Additional Buyer’s Stamp Duty applies to the new buyer — both on the sub-sale price, not the original purchase price.

12. What happens if the developer delays TOP?

The Sale & Purchase Agreement specifies a contractual TOP deadline. If the developer misses it, liquidated damages are payable to the buyer per the S&P terms — typically a fraction of the purchase price per month of delay. Review your S&P clauses carefully; liquidated damages are not uniform across developers.

Disclaimer. This article is for general information only and does not constitute legal, financial or tax advice. Figures referenced reflect the position as at 23 April 2026 and are subject to change without notice. Always verify the latest rates and policies with the official authority — IRAS, HDB, URA, CPF or MAS — before making any property decision. Consult a qualified lawyer, mortgage broker or accountant for advice specific to your circumstances.