Singapore Property Agent Commission Guide 2026

Click anywhere to close

⚡ Quick Answer: Property Agent Commission Singapore 2026

- Agent commission is negotiable — there are no legally fixed rates in Singapore. Industry benchmarks exist but are not mandated.

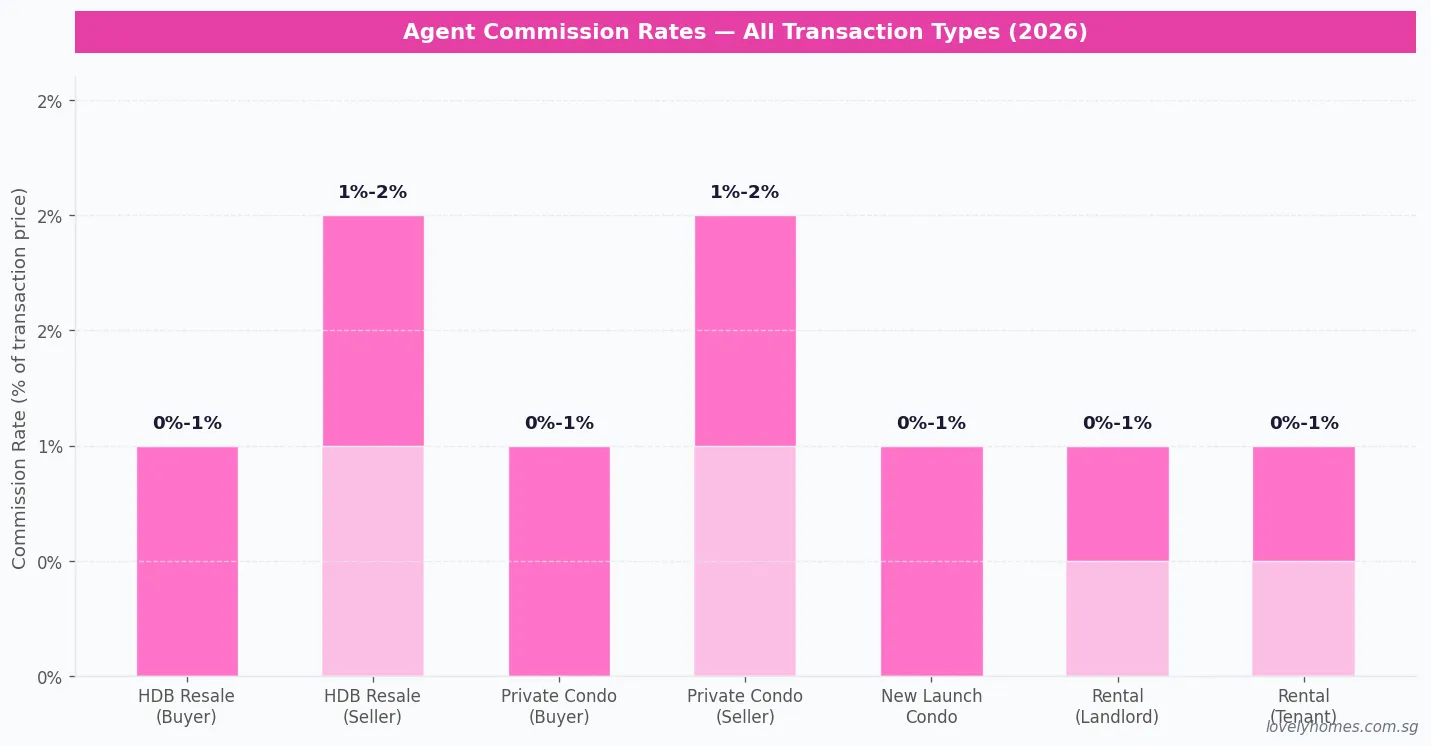

- HDB resale sellers typically pay 1%–2%; HDB resale buyers typically pay 0%–1% of purchase price, plus 9% GST.

- Private property sellers typically pay 1%–2%; private property buyers typically pay 0%–1%, plus 9% GST.

- New launch condo buyers pay nothing — the developer pays the buyer’s agent commission directly (typically 1%–3% of purchase price).

- Rental transactions: landlords and tenants each typically pay half a month’s rent for leases under 24 months; one month’s rent for longer leases.

- All agents must be CEA-licensed and must sign a Client’s Agreement (CA) with you before conducting any work on your behalf — mandated under the Estate Agents Act.

- Verify your agent at cea.gov.sg before signing anything. An unlicensed “agent” cannot legally claim commission and may expose you to fraud risk.

Property Agent Commission in Singapore: Who Pays What and Why

In Singapore’s property market, agent commission is one of the largest transaction costs after stamp duties — yet it remains one of the least understood. Unlike stamp duty, which is set by law and published in IRAS schedules, agent commission has no statutory fixed rate. The Council for Estate Agencies (CEA), which regulates all property agents under the Estate Agents Act (Cap. 95A), has never mandated a specific commission percentage. Instead, it publishes broad guidelines and requires that all commissions be agreed in writing via a Client’s Agreement before an agent begins work.

This means that the rates you see quoted — 1% for HDB buyers, 2% for private sellers — are industry convention rather than law. In practice, they are widely observed but negotiable, particularly for high-value transactions or where a single agent represents both buyer and seller (co-broking arrangements).

Understanding the standard rates, who pays whom, and what the commission covers can help you plan your transaction budget accurately and negotiate confidently.

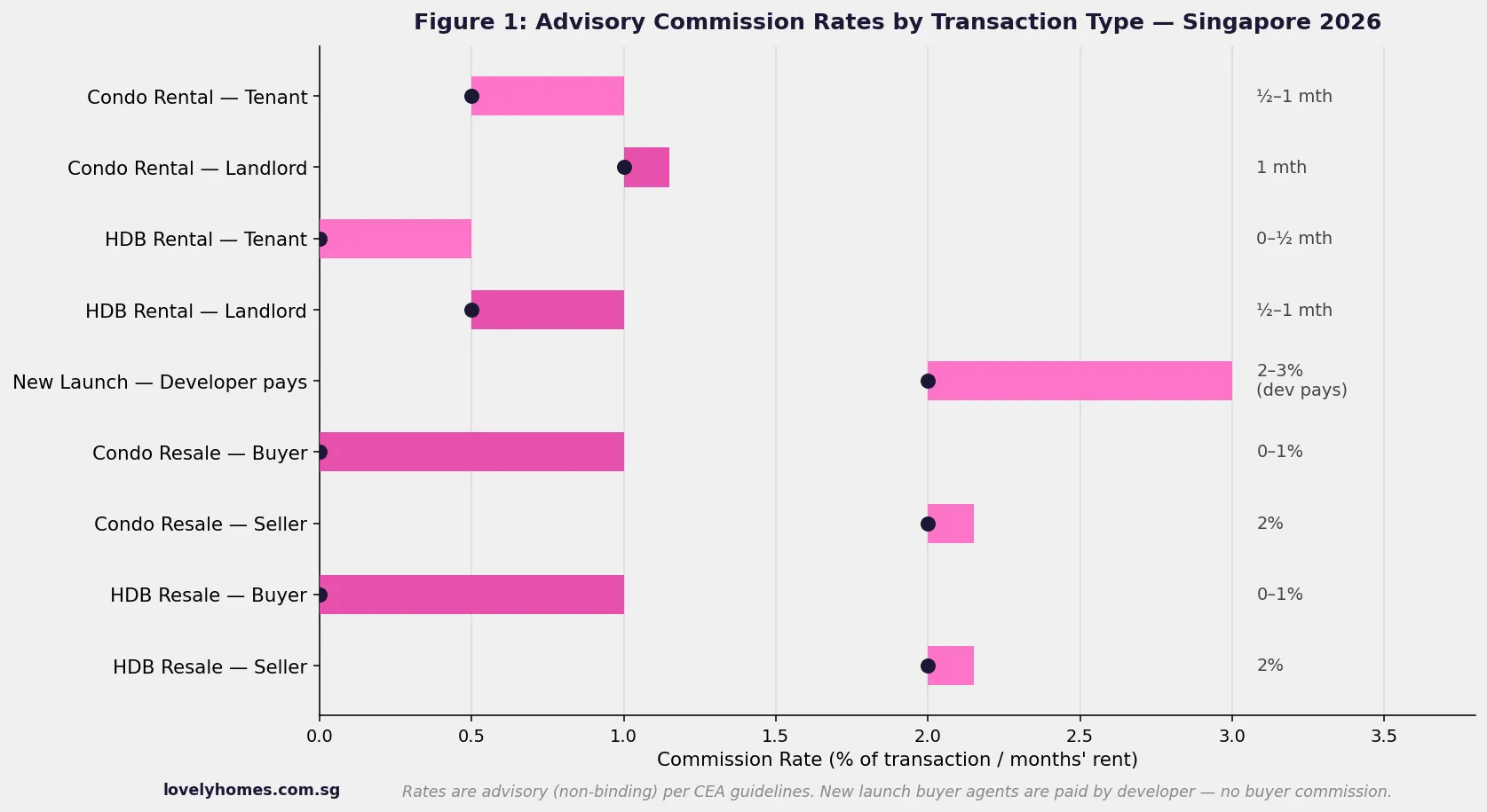

Commission Rates by Transaction Type

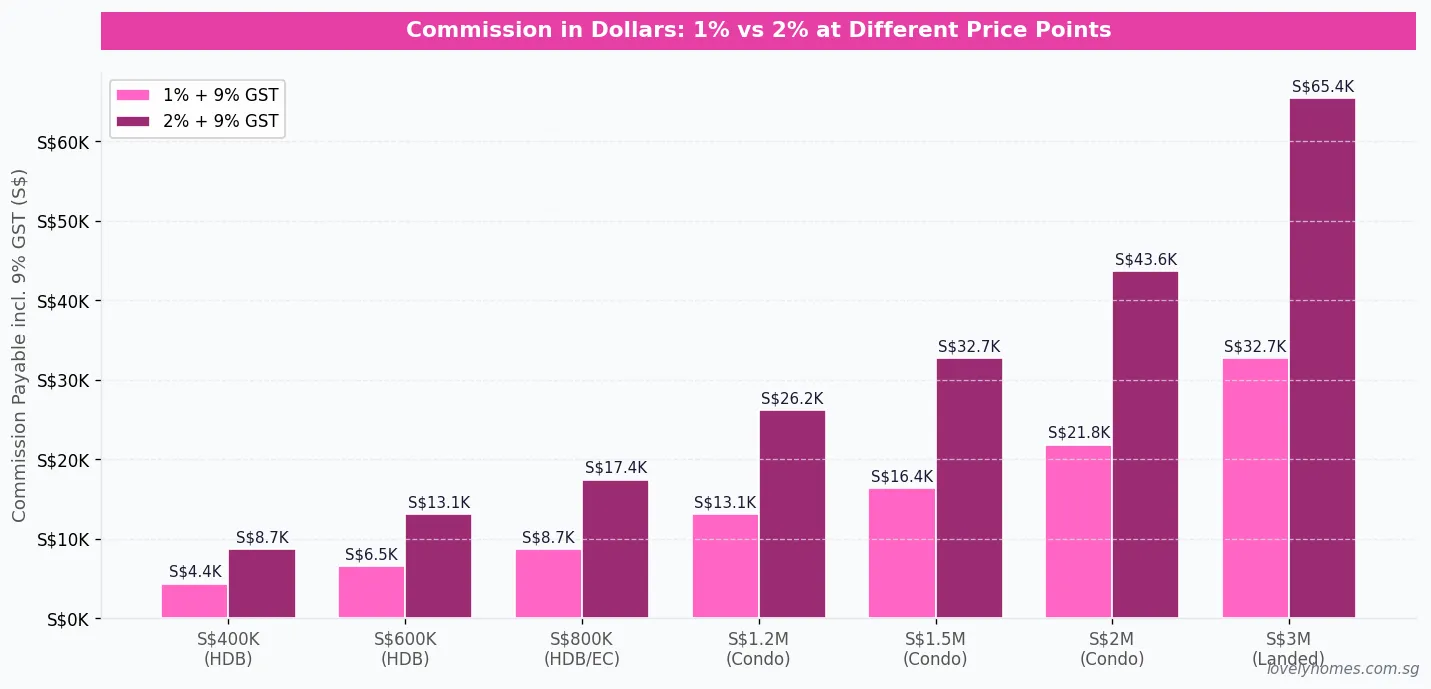

HDB resale transactions: For buyers, the industry benchmark is 0% to 1% of the purchase price; many HDB buyers negotiate the buyer-side commission down or even to zero, since developers do not incentivise buyer agents the way new-launch projects do. For sellers, the benchmark is 1% to 2%. A seller paying 2% on an S$620,000 HDB flat will pay S$12,400 plus 9% GST = S$13,516.

Private residential (resale condominiums, apartments, landed): For buyers, 0%–1% is typical. For sellers, 1%–2% is typical. Co-broking is standard — each agent receives their respective commission from their own client. At S$2,000,000, a seller paying 2% pays S$43,600 inclusive of GST.

New launch condominiums: Buyers pay nothing — developer commission structures compensate the buyer’s agent directly, typically at 1%–3% of the purchase price depending on developer marketing budget. This is why agents are often more enthusiastic about showing new launches than resale properties. The commission comes from the developer’s marketing spend, which is embedded in the developer’s pricing model.

Rental transactions: The standard for leases of 24 months or less is one month’s rent split equally between the landlord’s agent and the tenant’s agent (0.5 months each, plus GST). For leases longer than 24 months, the benchmark rises to one month’s rent each. Short-term rentals or corporate leases may attract different structures negotiated case by case.

GST note: Property agents are GST-registered if their annual turnover exceeds the GST registration threshold. As of 1 January 2024, GST is charged at 9%. Always confirm whether a quoted commission is inclusive or exclusive of GST.

Commission Summary Table

| Transaction Type | Buyer Pays | Seller / Landlord Pays | Basis | Notes |

|---|---|---|---|---|

| HDB resale flat | 0%–1% of purchase price | 1%–2% of sale price | % of transacted price | Both + 9% GST. Negotiable. |

| Private condo / apartment resale | 0%–1% of purchase price | 1%–2% of sale price | % of transacted price | Both + 9% GST. Negotiable. |

| Landed property resale | 0%–1% of purchase price | 1%–2% of sale price | % of transacted price | Both + 9% GST. Negotiable. |

| New launch condominium | Nil (paid by developer) | Developer pays buyer agent 1%–3% | Developer marketing budget | Buyer incurs no direct commission cost. |

| Residential rental (≤24 mths) | 0.5 mth rent + GST | 0.5 mth rent + GST | Per-lease | Split 50/50 between landlord agent and tenant agent. |

| Residential rental (>24 mths) | 1 mth rent + GST | 1 mth rent + GST | Per-lease | Higher commission for longer commitments. |

CEA Licensing and the Client’s Agreement

Every person conducting estate agency work in Singapore must hold a valid salesperson registration or estate agency licence issued by the Council for Estate Agencies (CEA), established under the Estate Agents Act 2010. The CEA maintains a public register at cea.gov.sg where anyone can look up an agent’s registration number, licence status, agency affiliation, and disciplinary history.

Before an agent may commence any work on your behalf — searching for properties, arranging viewings, submitting offers — they are required by the CEA Code of Practice to provide and have you sign a Client’s Agreement (CA). The CA specifies the scope of work, the agreed commission rate, and the duration of the engagement. Signing the CA creates a binding contract. Without a signed CA, any commission claim by the agent is difficult to enforce.

If an agent pressures you to make an offer or view properties without first providing a CA, this is a CEA breach and a red flag. You should decline and find another agent.

Worked Example: The Nair Family Sells Their D15 Condo

Mr and Mrs Nair decide to sell their freehold 3-bedroom condominium in District 15 (East Coast area). The property is listed at S$2,200,000 and eventually transacts at S$2,150,000.

They engage a seller’s agent at a negotiated commission of 1.5% (rather than the 2% upper benchmark), inclusive of marketing costs. Their buyer transacts through a separate buyer’s agent at 1% (paid by the buyer).

Commission calculation for the Nairs (sellers): S$2,150,000 × 1.5% = S$32,250. Add 9% GST = S$32,250 × 1.09 = S$35,152.50.

Commission calculation for the buyer: S$2,150,000 × 1% = S$21,500. Add 9% GST = S$21,500 × 1.09 = S$23,435.

The Nairs save S$10,750 pre-GST by negotiating from 2% to 1.5%. The saving is meaningful — equivalent to roughly one additional monthly mortgage payment.

Why Agent Commission Matters: Singapore in Context

At first glance, 1%–2% might sound modest. But on a S$2,000,000 private condominium, the combined buyer and seller commission (at 1% + 2%) totals S$60,000 before GST — S$65,400 inclusive of GST. That is a material transaction cost, often comparable to two to three months of gross household income for many Singapore buyers.

Unlike in some markets where buyer agents are paid from a shared commission pool, Singapore’s market structure is transparent: each side typically pays their own agent. This reduces conflicts of interest but means buyers who forgo representation on new launches (where they pay nothing for a buyer’s agent) are effectively subsidising the developer’s marketing cost through the purchase price.

The CEA has discussed introducing more formal commission disclosure requirements in recent consultations, though no regulatory change had been announced as at June 2026. Buyers and sellers should nonetheless insist on a written, signed Client’s Agreement specifying the exact commission before any agent commences work on their behalf.

What Might Change in Agent Commission Rules

The CEA periodically reviews its Code of Practice for professional standards. Industry observers have noted ongoing discussion about whether a formal commission disclosure framework — similar to what exists in Australia — should be introduced to increase transparency. As at June 2026, commission rates remain entirely negotiable with no mandatory disclosure beyond what must appear in the Client’s Agreement. Buyers should monitor CEA announcements for any changes to co-broking standards or commission disclosure obligations.

Frequently Asked Questions

Is agent commission legally fixed in Singapore?

No. The Council for Estate Agencies (CEA) does not prescribe fixed commission rates. What it mandates is that any agreed commission must be documented in a signed Client’s Agreement before the agent commences work. The rates quoted throughout this article — 1%, 2%, half a month’s rent — are industry conventions that have become widely expected but are legally negotiable. An agent cannot demand a specific rate; the rate is whatever you and the agent agree and document.

Do I need a buyer’s agent when buying a new launch condo?

No, you do not — but having one costs you nothing because the developer pays the buyer’s agent commission directly. A buyer’s agent for a new launch can help you compare projects, assess floor plans, check price comparables, and advise on unit selection without charging you any fee. Using a buyer’s agent for new launches is therefore generally rational from a cost perspective.

Can one agent represent both buyer and seller (dual representation)?

Yes, but with restrictions. The CEA code permits an agent to act for both parties in a transaction (known as dual representation or co-broking by the same agent), but the agent must inform both parties, obtain their written consent, and act fairly to both sides. In practice, many experienced buyers and sellers prefer independent agents to avoid any conflict of interest. If a single agent represents both sides, it is common for the commission arrangement to be negotiated down to reflect the reduced workload.

What is the CEA Client’s Agreement and is it compulsory?

The Client’s Agreement (CA) is a written contract between you and your agent that specifies the scope of work (e.g., marketing your property, sourcing a tenant), the agreed commission, the duration of the engagement, and the agent’s obligations under the CEA Code of Practice. Signing the CA is compulsory under CEA rules before the agent may commence any estate agency activity on your behalf. Without a signed CA, the agent cannot legally enforce a commission claim if the transaction is completed.

What if I find a buyer myself — do I still owe commission?

It depends on your Client’s Agreement. If you signed an exclusive CA with an agent for a specified period, and you introduce a buyer yourself during that exclusive period, the agent may still be entitled to commission under the terms of the agreement. If you have a non-exclusive CA, and you find a buyer independently without the agent’s involvement, you may be able to argue no commission is owed — but the exact terms of your signed CA govern. Always read the CA carefully before signing, particularly the exclusivity clause.

How do I check if my agent is properly licensed?

Visit the CEA Public Register at cea.gov.sg/public-register and search by the agent’s name or registration number (which all agents are required to display on namecards, marketing materials, and messaging). Verify the status shows “Active”, check the estate agency affiliation matches what the agent told you, and review any disciplinary records. This takes under two minutes and is strongly recommended before signing any agreement.

Is agent commission subject to GST?

Yes, for GST-registered agents. As of 1 January 2024, GST in Singapore is charged at 9%. If your agent or their agency is GST-registered (mandatory once their annual turnover exceeds S$1 million), they will charge GST on top of the agreed commission. This means a 2% commission on a S$1,500,000 property becomes S$30,000 + 9% GST = S$32,700. Always clarify whether quoted commission rates are inclusive or exclusive of GST before signing the Client’s Agreement.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Private Property Buying Costs 2026: All-In Cost Guide

- How to Choose a Property Agent in Singapore 2026

- Private Property Resale Process 2026: Step-by-Step from OTP to Keys

- HDB Resale Process 2026: Step-by-Step Guide

- Singapore TDSR Guide 2026: Total Debt Servicing Ratio Explained

- Stamp Duty Remission Guide 2026: ABSD Upgrader Refunds

Disclaimer: This article is for general informational purposes only and does not constitute professional real estate, financial, or legal advice. Commission rates are industry benchmarks and are subject to negotiation. All agents must be CEA-licensed; verify at cea.gov.sg. For official guidance on estate agency regulation, refer to the Council for Estate Agencies at cea.gov.sg and the IRAS GST guidelines at iras.gov.sg.