Singapore Property Rental Income Tax Guide 2026: IRAS Deductions, Rates and How to File

Quick Answer: Singapore Rental Income Tax 2026

- All rental income from Singapore property is taxable under the Income Tax Act (Cap 134), administered by IRAS.

- You may deduct allowable expenses — mortgage interest, property tax, fire insurance, routine repairs, agent fees — to arrive at net taxable rental income.

- Capital costs cannot be deducted — no claims for renovations, major upgrades, furniture depreciation, or loan principal repayments.

- Tax is levied at personal income tax rates — Singapore tax-resident rates (0–24%) apply; non-residents pay a flat 22% on net rental income.

- Filing deadline: 18 April annually — declare via myTax Portal; IRAS auto-includes known data where available.

- Late filing or non-declaration attracts penalties — up to 200% of tax undercharged plus potential prosecution under s.96 Income Tax Act.

- HDB flat rental has slightly different rules — HDB room rental income is also taxable but sub-let approval and NCQ limits still apply (see our HDB Room Rental Guide 2026).

Owning an investment property in Singapore comes with one certainty beyond market cycles: your rental income is taxable. Whether you own a one-bedroom condominium in Tiong Bahru, a shophouse unit in Tanjong Pagar, or a landed property in Upper Bukit Timah that you lease out whilst residing abroad, the Inland Revenue Authority of Singapore (IRAS) expects you to declare that rental income each year.

Yet many Singapore landlords — especially first-time investors who upgraded from an HDB flat — under-declare or over-pay because they misunderstand which deductions IRAS allows. This guide sets out the complete picture: what qualifies as rental income, which expenses are deductible, how the tax is calculated, and how to file correctly by 18 April each year.

What Counts as Rental Income in Singapore?

Under section 10(1)(f) of the Income Tax Act, rental income includes all amounts received or receivable by a person in respect of the letting of any property located in Singapore. This covers:

- Gross rent — the monthly or annual sum paid by your tenant under the tenancy agreement.

- Lease premiums — any upfront lump-sum payment to secure the tenancy is spread over the lease term and taxed proportionately.

- Furniture and fittings rent — if your tenancy agreement splits the total into “base rent” and a “furniture allowance”, both components are taxable rental income.

- Reimbursed expenses — if your tenant pays your utility bills or property tax and these are included in the rent, the gross amount is your rental income (before the deduction).

- Compensation for early termination — amounts received from tenants for breaking a tenancy early are treated as rental income for the period the tenancy was broken.

Rental income from overseas property is generally not taxable in Singapore (as Singapore uses a territorial tax system), provided the funds are not remitted into Singapore. From 1 January 2024, certain foreign-sourced income remitted to Singapore by individuals is taxable; consult a licensed tax adviser if you hold overseas investment property.

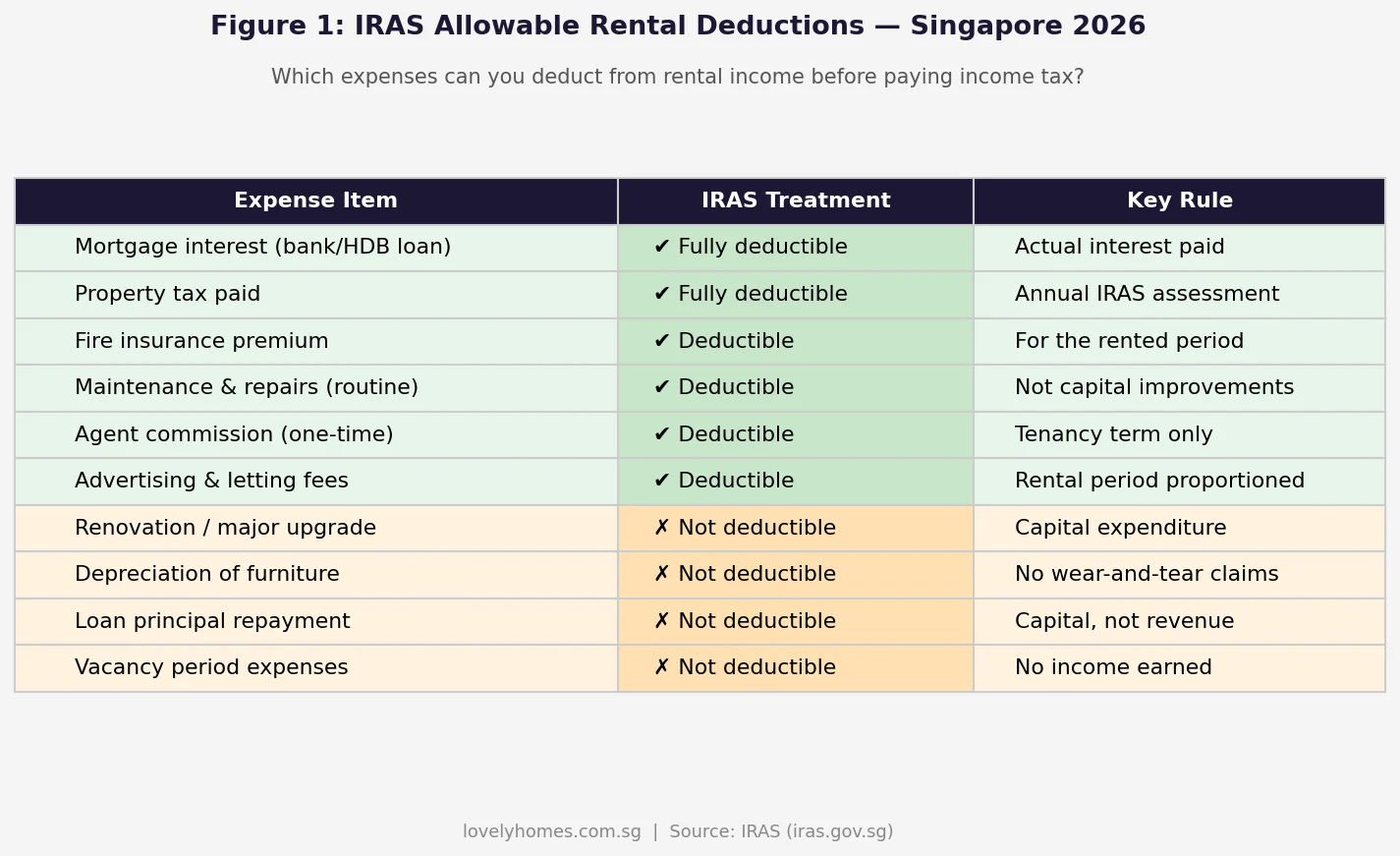

Allowable Deductions: What You Can Claim Against Rental Income

IRAS allows landlords to deduct expenses that are wholly and exclusively incurred in the production of rental income and are revenue in nature (not capital). The following are the main allowable deductions in 2026:

1. Mortgage Interest

The interest portion of your monthly bank or HDB loan repayment is fully deductible. Only the interest element qualifies — loan principal repayments are capital and cannot be deducted. If you have a floating-rate loan, use the actual interest charged each year. Most banks issue an annual statement splitting principal and interest for your records.

2. Property Tax

Annual property tax paid to IRAS on the investment property is deductible. Note: you are claiming the tax as an expense against rental income — this is separate from your residential property tax obligation on your own home. The deduction is for the property tax assessed on the rented property for the year.

3. Fire Insurance Premium

Fire insurance premiums covering the property during the rental period are allowable. If your policy covers a period spanning two tax years (e.g., July 2025 to July 2026), apportion the premium to the relevant year.

4. Routine Maintenance and Repairs

Costs of maintaining the property in its existing condition — plumbing repairs, repainting, replacing faulty fixtures — are deductible. Improvements that enhance the property’s value or extend its life (a new built-in wardrobe, a replacement air-conditioning system that upgrades the previous one) are capital expenditure and not deductible.

5. Agent Commission and Advertising

Letting fees paid to a licensed property agent, including a one-time commission upon signing the tenancy agreement, are deductible. Advertising costs (online listings, print advertisements) for finding tenants are similarly allowable. These are expenses incurred in earning the rental income.

6. Legal Fees for Tenancy

Solicitor’s fees for drafting or reviewing a tenancy agreement are deductible. Legal costs for acquiring or disposing of the property are capital and not deductible.

What You Cannot Deduct

IRAS explicitly disallows: renovation costs, capital improvements, furniture and fittings depreciation (Singapore has no wear-and-tear allowance for residential property), loan principal repayments, mortgage protection insurance premiums, costs incurred during vacancy periods when no rent is being earned, and any expense that is not wholly connected to earning the rental income.

How Singapore Income Tax Applies to Rental Income

Rental income does not attract a separate tax — it is added to your other assessable income (employment income, trade income, director’s fees) and taxed at your marginal personal income tax rate under the resident progressive rate schedule, effective Year of Assessment (YA) 2024 onwards:

| Chargeable Income (SGD) | Rate on Band | Cumulative Tax |

|---|---|---|

| First $20,000 | 0% | $0 |

| Next $10,000 ($20K–$30K) | 2% | $200 |

| Next $10,000 ($30K–$40K) | 3.5% | $550 |

| Next $40,000 ($40K–$80K) | 7% | $3,350 |

| Next $40,000 ($80K–$120K) | 11.5% | $7,950 |

| Next $40,000 ($120K–$160K) | 15% | $13,950 |

| Next $40,000 ($160K–$200K) | 18% | $21,150 |

| Next $40,000 ($200K–$240K) | 19% | $28,750 |

| Next $40,000 ($240K–$280K) | 19.5% | $36,550 |

| Next $40,000 ($280K–$320K) | 20% | $44,550 |

| Above $320,000 | 22% – 24% | progressive |

Non-resident landlords pay a flat 22% on net rental income with no personal reliefs available. This applies to individuals not ordinarily resident in Singapore for 183 days or more in the relevant year. Non-residents must also file a Singapore tax return and may be required to appoint a local tax agent.

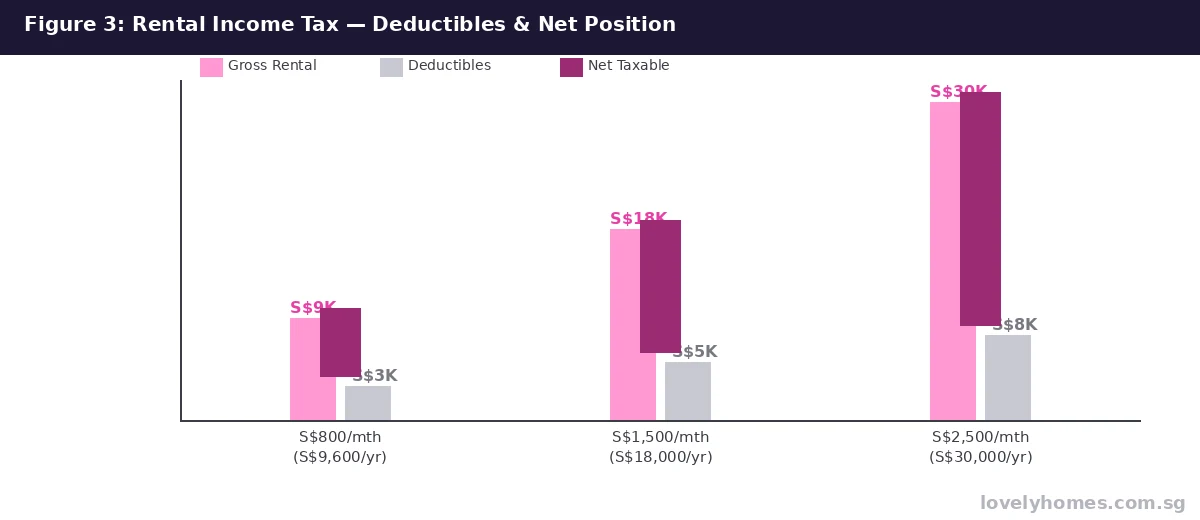

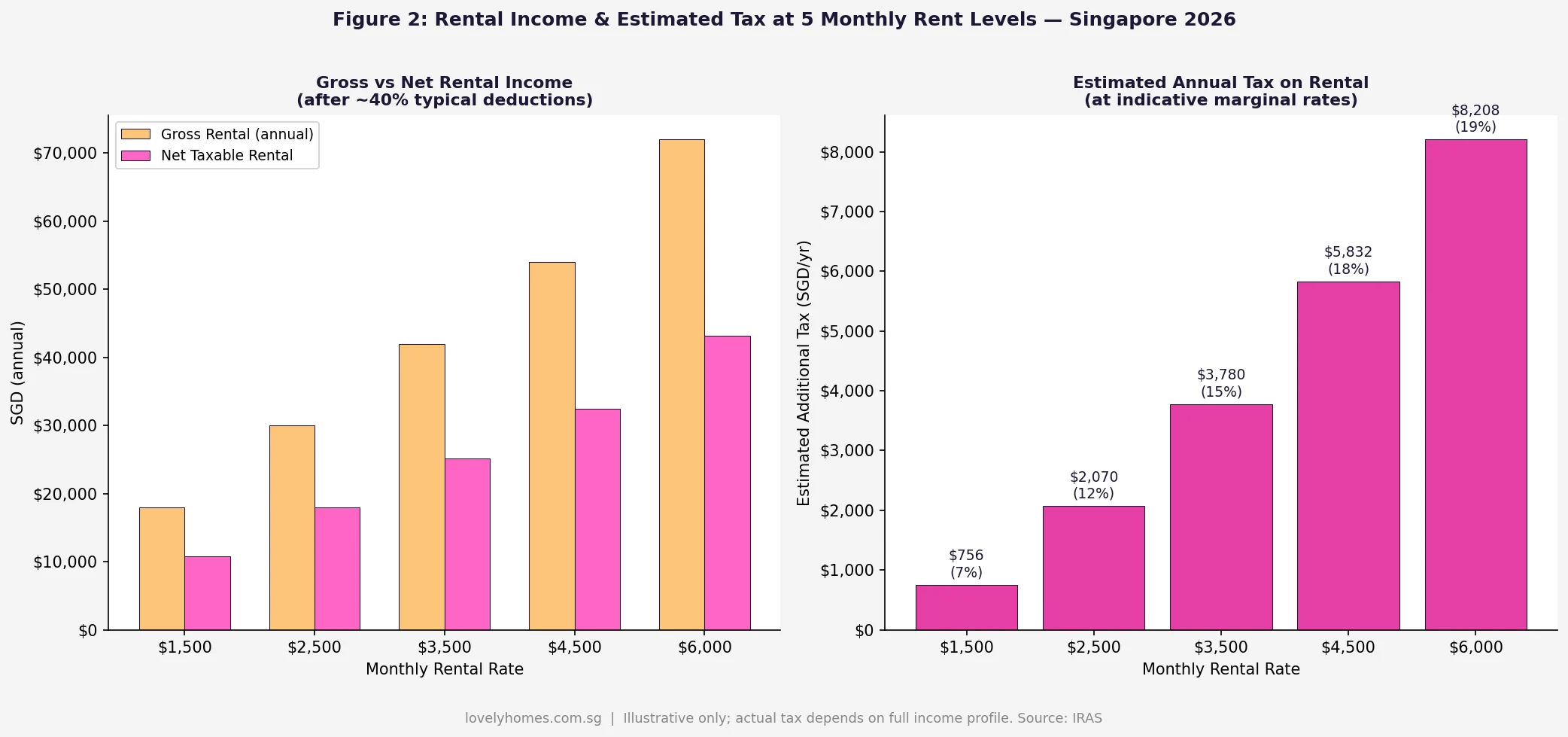

Worked Example: Renting Out a Private Condo in 2026

The Wong family — Singapore Citizens, joint owners of a 2-bedroom condominium in Kallang. Gross monthly rent: $3,200. Mr Wong earns $9,500/mth in employment income.

| Item | Amount |

|---|---|

| Gross annual rent (Jan–Dec 2025) | $38,400 |

| Less: Mortgage interest (POSB Home Loan statement) | ($9,600) |

| Less: Annual property tax (non-owner-occupied) | ($3,200) |

| Less: Fire insurance premium | ($520) |

| Less: Routine maintenance / A/C servicing / plumbing | ($1,100) |

| Less: Agent commission (1 month’s rent) | ($3,200) |

| Net taxable rental income (YA 2026) | $20,780 |

| Mr Wong’s employment income (declared separately) | $114,000 |

| Total chargeable income (after personal reliefs ~$37,000) | ~$97,780 |

| Incremental tax on rental income at ~11.5% marginal rate | ~$2,389/yr |

| Net rental income after tax (monthly) | ~$1,516/mth |

Key takeaway: after deductions and tax, Mr Wong nets approximately $1,516 per month from the $3,200 gross rent. This is not a criticism of property investment — the capital appreciation on the condo adds significantly to total returns — but it illustrates why landlords who model only gross rent make poor investment decisions.

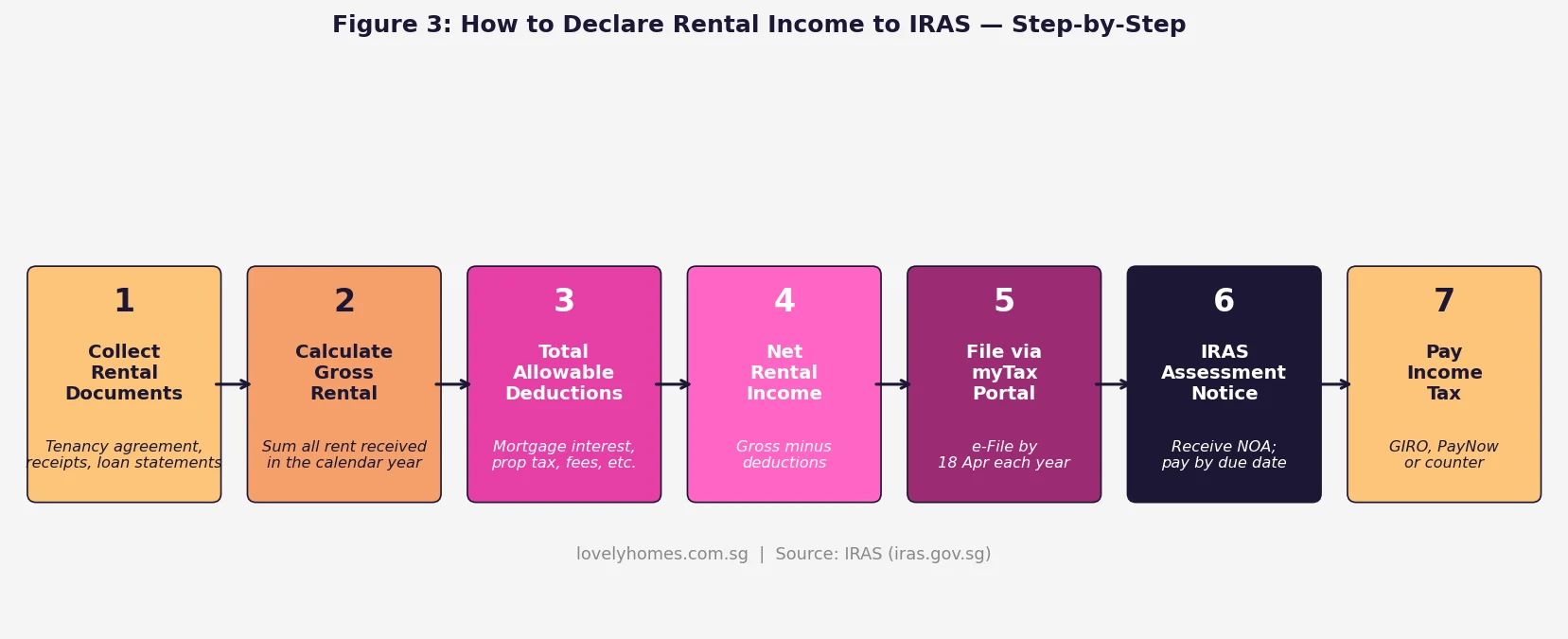

How to File: IRAS myTax Portal Step by Step

IRAS auto-populates most employment income figures via the Auto-Inclusion Scheme (AIS), but rental income is not auto-included — landlords must declare it manually. The process in practice:

- Gather your documents by January of the filing year: tenancy agreement, bank loan annual statement (splitting principal and interest), IRAS property tax assessment, insurance policy, receipts for maintenance and agent fees.

- Log in to myTax Portal at mytax.iras.gov.sg using Singpass MFA.

- Navigate to “File Individual Income Tax (Form B1)” (for employees with rental income) or Form B (for self-employed) — complete the rental income section under “Other Income”.

- Enter gross rental income and each allowable deduction separately. IRAS will compute net rental income automatically.

- Submit by 18 April (e-filing; paper returns are due 15 April).

- Receive your Notice of Assessment (NOA) by post or via myTax Portal. Review for accuracy — you have 30 days from the NOA date to object if there is an error.

- Pay by the due date on the NOA — via GIRO, PayNow, internet banking, or at AXS/SingPost counters.

Tip: IRAS’s Rental Relief Framework introduced during the COVID-19 period (2020–2021) has fully expired. No rental income relief is available in YA 2026 under COVID measures.

Why Rental Income Tax Matters for Singapore Property Investors

Singapore has relatively low income tax rates compared with most developed markets — the top marginal rate of 24% (above $1M) is far below the UK’s 45%, Australia’s 47%, or Hong Kong’s 17% salaries tax. Even at the 15–18% band that most mid-income investors land in, the after-tax rental yield for a well-located condo is typically positive. However, failing to account for IRAS obligations when underwriting a property purchase leads to three common errors:

- Overestimating net yield — a $3,200/mth gross rent may look like a 3.2% yield on a $1.2M property, but after allowable deductions and tax, the true cash yield is closer to 1.8–2.2%.

- Missing deductions — many landlords forget to claim mortgage interest (the largest deductible item) because they use CPF OA funds for repayment and assume no cash changes hands. IRAS allows the interest deduction regardless of whether the repayment comes from CPF or cash.

- Commingling ABSD strategy with tax strategy — if you held your HDB flat and purchased a condo (20% ABSD, with remission on HDB sale within 6 months), you must still declare rental income on the condo during the period you hold both properties. The ABSD framework and the rental income tax regime are entirely separate systems administered by different IRAS divisions.

For investors holding multiple properties, maintaining a separate rental income tracker for each property and reconciling it quarterly against bank statements is strongly recommended. This significantly simplifies April filing.

What Might Come Next: Rental Income Tax Outlook

The following is forward-looking speculation based on publicly available commentary and budget signals — it does not constitute tax advice.

IRAS has signalled no changes to the rental income tax framework for YA 2026 or YA 2027. However, two areas bear watching:

- Foreign-sourced income changes: Following the 2022 changes that brought certain foreign passive income (dividends, interest) into the Singapore tax net when remitted, there is ongoing policy debate about whether foreign rental income should similarly be taxable upon remittance. As at June 2026, rental income from overseas properties remains outside Singapore’s tax net if not remitted, but high-net-worth landlords with overseas portfolios should monitor any Budget 2027 announcements.

- Non-owner-occupied property tax alignment: The graduated non-owner-occupied property tax rates (10–20%, increased in 2023) may be reviewed in future budgets to further discourage speculative holding. Higher property tax would paradoxically increase allowable deductions for landlords, but would also compress investment yields.

- Platform reporting: IRAS has been expanding its data-matching capabilities via MAS and regulatory partnerships. Rental income declared through platforms like 99.co, PropertyGuru, and Airbnb may eventually be subject to third-party reporting obligations similar to the GST framework for digital services.

Rental Income Tax in Context: Singapore vs Regional Peers

Singapore’s approach to taxing rental income is broadly aligned with other developed economies, but its relatively modest rates and clear deduction framework make it more landlord-friendly than most. In Malaysia, rental income above RM70,000 is taxed at 24%; in Australia, negative gearing laws allow interest losses to offset other income but the effective capital gains tax erodes returns on sale; in Hong Kong, property tax is levied as a flat 15% on net rental income (gross rent less 20% statutory allowance) regardless of actual expenses. Singapore’s expense-based deduction regime — whilst requiring more documentation — is generally more accurate and beneficial for highly leveraged investors with large mortgage interest deductions.

Frequently Asked Questions: Rental Income Tax Singapore 2026

Can I claim mortgage interest if I use CPF OA to pay my loan?

Yes. IRAS allows the deduction of mortgage interest regardless of whether you use CPF Ordinary Account funds or cash to service your loan repayments. You can obtain the annual mortgage interest figure from your bank’s annual statement or CPF Board’s online portal. Only the interest portion is deductible — not the principal reduction.

What if my property is vacant for part of the year? Can I still claim expenses?

Only expenses incurred during periods when the property is genuinely available for rent can be claimed. If the property is vacant between tenancies whilst you are actively seeking a new tenant, IRAS generally accepts a proportionate deduction. However, if the property is vacant because you are using it personally, renovating it, or simply leaving it idle, expenses during that period are not deductible. Keep records of advertising and agent correspondence to demonstrate active letting intent during vacancy.

Is rental income taxed if I rent out a room in my HDB flat?

Yes — all rental income from HDB flats and private property is taxable. For HDB flat room rentals, you must obtain HDB’s approval to sub-let, comply with the Non-Citizen Quota (NCQ), and declare the rental income to IRAS annually. You may deduct a proportionate share of allowable expenses (interest, property tax) corresponding to the rented portion. See our Singapore HDB Room Rental Guide 2026 for the full framework including NCQ limits and approval conditions.

Can I deduct renovation costs from rental income?

No. Renovation and improvement costs are capital expenditure and are not deductible against rental income under Singapore tax law. This applies even if the renovation was undertaken specifically to attract higher-paying tenants. IRAS distinguishes between revenue expenditure (maintaining the property in its existing state) and capital expenditure (enhancing or extending the property). Routine maintenance such as repainting, replacing like-for-like fixtures, and servicing appliances qualifies as revenue expenditure and is deductible; a full kitchen overhaul or bathroom extension does not.

What penalties apply if I under-declare rental income?

Under section 94 of the Income Tax Act, omitting income from a tax return without reasonable excuse attracts a penalty of twice the tax undercharged (200% penalty). Fraudulent under-declaration under section 96 can result in up to treble the tax undercharged plus a fine of up to $10,000 and imprisonment. IRAS has access to HDB records, URA caveats, and banking data — undeclared rental income identified through these channels is aggressively pursued. The most cost-effective approach is voluntary compliance and accurate declaration.

How does IRAS treat short-term rentals (e.g., Airbnb / serviced apartments)?

Short-term accommodation of private residential property — rentals shorter than three consecutive months per tenant — is generally not permitted under the Planning Act without URA approval, and HDB flats may not be sub-let on a short-term basis at all. Where such rentals are authorised (typically in government-approved short-stay projects), the income is taxable as rental income under the Income Tax Act. Platforms that facilitate short-stay bookings may be subject to IRAS data-matching. Unauthorised short-term rentals carry planning enforcement risk in addition to tax exposure.

Do joint owners each declare their share of rental income separately?

Yes. If a property is jointly owned, rental income and deductible expenses are allocated to each owner in proportion to their beneficial interest (ordinarily 50:50 for joint tenants, or as specified in a tenancy-in-common arrangement). Each owner declares their respective share independently in their personal income tax return. There is no joint filing option for property rental in Singapore. In practice, joint owner couples often find this beneficial if one spouse is in a lower tax bracket — the aggregate tax burden may be lower than if only the higher-earner declared the full rental income.

Related LovelyHomes Guides

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Annual Property Tax Guide 2026

- Singapore Private Property Buying Costs 2026: All-In Cost Guide

- CPF Accrued Interest for Property 2026

- Singapore HDB Room Rental Guide 2026

- Singapore Private Property Resale Process 2026

- Singapore Strata-Titled Landed Property Guide 2026

Click anywhere or press Esc to close