Kallang Neighbourhood Guide Singapore 2026: HDB, Condos & the Kallang Alive Opportunity

📌 Quick Answer: Kallang Neighbourhood at a Glance

- District: D12 (Rest of Central Region — RCR)

- HDB resale median: S$420k (3-room) to S$820k (5-room) in 2025

- Private condo PSF: ~S$1,680 median; gross rental yield ~3.8%

- Key catalyst: Kallang Alive masterplan — Singapore Sports Hub, Kampong Bugis, waterfront promenade

- MRT access: Circle Line (Kallang, Bendemeer, Geylang Bahru) + East-West Line (Kallang)

- Best for: Young professionals, investors targeting rental demand from the sports/events corridor

- Upcoming supply: Peck Hay Road GLS tender (closes June 2026) — c.450 units near Farrer Park

- Caution: Geylang sub-market noise; heritage conservation constraints in Jalan Besar sub-area

Introduction: Why Kallang Deserves a Second Look

Kallang sits at the intersection of Singapore’s sporting ambitions and urban regeneration agenda. Administered as part of the Central Region under the Urban Redevelopment Authority (URA), District 12 spans Kallang, Whampoa, Bendemeer, Geylang Bahru, and the Tanjong Rhu waterfront — a corridor that the Government has been systematically transforming since 2014 under the Kallang Alive masterplan.

For buyers and investors in 2026, Kallang presents a classic mid-cycle RCR proposition: proximity to the CBD and Orchard at a meaningful PSF discount to Districts 9–11, anchored by a Government-backed precinct upgrade that is still mid-execution. The Kampong Bugis long-term development site — earmarked for a car-lite, waterfront mixed-use precinct — is expected to add thousands of residents and further commercial activity to the corridor over the next decade.

This guide covers the full picture: HDB and private market pricing, the Kallang Alive catalyst, schools, transport, worked acquisition costs, and the investment case.

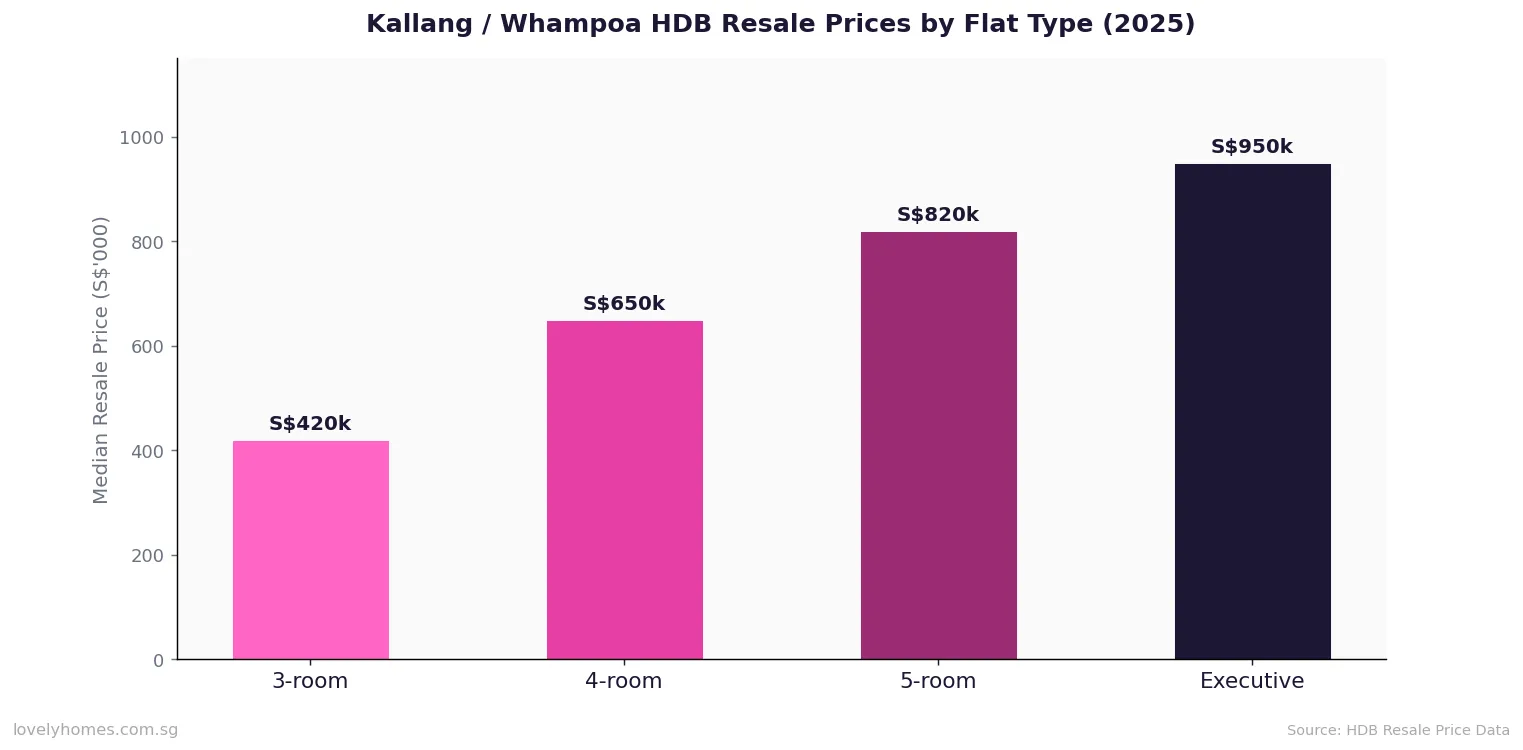

HDB Resale Market in Kallang / Whampoa

The Kallang and Whampoa housing estates sit under the Housing & Development Board (HDB) in the Central Region. Resale volumes in this sub-market are relatively low — fewer HDB blocks than OCR towns — which tends to keep prices supported. In 2025, median transacted prices ranged from approximately S$420,000 for a 3-room flat to over S$820,000 for a 5-room unit along the Tanjong Rhu or Whampoa Drive corridors. Executive flats are rare but command S$900k–S$1.0m when they appear.

Buyers should note that some Kallang HDB blocks are approaching or have crossed the 30-year MOP-plus threshold, and a handful of precincts have been earmarked for the Selective En-Bloc Redevelopment Scheme (SERS) — check the HDB portal before purchasing any resale flat in this area, as SERS selection changes the asset’s long-term value profile significantly.

CPF and HDB Loan Eligibility

Singapore Citizens and Permanent Residents purchasing HDB resale flats in Kallang may apply for HDB concessionary loans at 2.60% per annum (pegged at 0.1 percentage points above the CPF Ordinary Account rate of 2.50%). Enhanced CPF Housing Grants (EHG) of up to S$80,000 are available for first-timer families with a combined income at or below S$9,000 per month, subject to the flat’s remaining lease covering the youngest buyer to at least 95 years old. Given the older stock in Kallang, lease-decay must be carefully modelled for any flat with fewer than 70 years remaining.

Private Residential Market: Condos and PSF

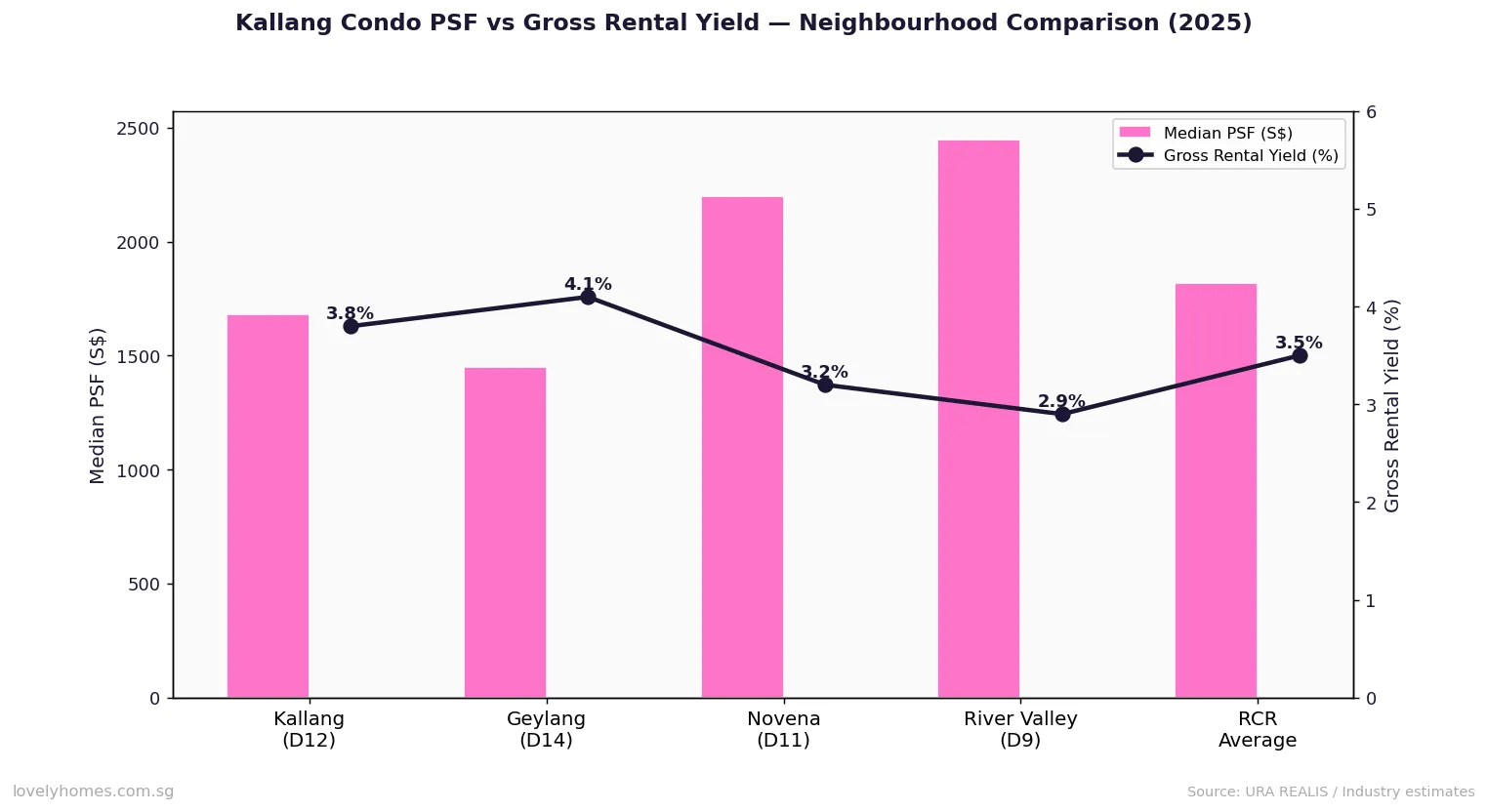

The private condo market in D12 is characterised by a mix of older developments and more recent launches. Key projects include Kallang Riverside (2017), One Kallang Avenue developments, and resale stock along Tanjong Rhu Road. In 2025, median transacted PSF in D12 landed around S$1,680, compared with an RCR average of approximately S$1,820 — positioning Kallang as a value play within the Central Region.

Gross rental yields in D12 average around 3.8%, supported by strong demand from expatriate sports professionals, government employees at the nearby Health Sciences Authority and civil service agencies, and young professionals attracted by the precinct’s lifestyle credentials. The rental demand story is structural: the Singapore Sports Hub hosts more than 60 major events per year, and the upcoming Kampong Bugis precinct — when built — will add a substantial resident population within walking distance of Kallang MRT.

The Kallang Alive Masterplan: A Decade of Transformation

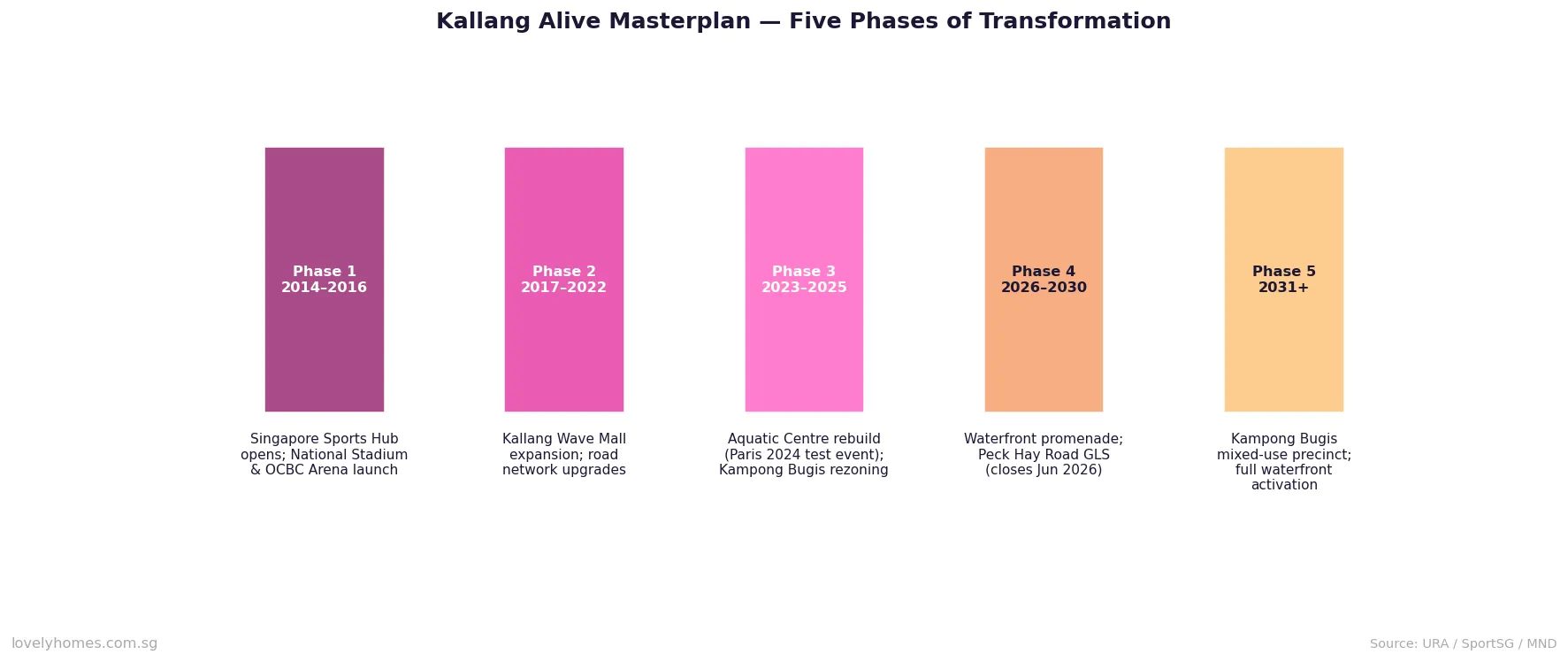

The Kallang Alive masterplan is a joint programme by the Ministry of National Development (MND), URA, and Sport Singapore (SportSG) to transform the 24-hectare Kallang precinct into Singapore’s premier live-work-play sports and lifestyle hub. It is one of the most consequential urban regeneration programmes in Singapore’s recent planning history, with a five-phase execution arc spanning 2014 to 2031 and beyond.

Phase 3 (2023–2025) saw the completion of the new Aquatic Centre, which hosted international test events ahead of the 2024 Paris Olympics qualifying circuit. Phase 4 (2026–2030) is now underway, with the waterfront promenade extension and the Peck Hay Road GLS tender (closing June 2026) expected to bring new private residential supply to the Farrer Park/Kallang fringe. Phase 5 looks ahead to the full buildout of Kampong Bugis — a 9-hectare waterfront site rezoned for mixed-use development under URA’s Master Plan 2025.

What the Masterplan Means for Property Values

Precinct-level masterplans in Singapore have a track record of delivering measurable PSF uplift. The Jurong Lake District (JLD) saw private condo PSF in Jurong East outperform the OCR average by 12–18 percentage points between 2013 and 2024. Analysts who track Kallang point to a similar dynamic: D12 PSF in 2019 was roughly 18% below the RCR average; by 2025 that gap had narrowed to approximately 8%. The narrowing reflects both masterplan progress and RCR-wide tightening, but the direction of travel is clear.

Transport Connectivity

Kallang benefits from two MRT lines: the East-West Line (EWL) at Kallang Station and the Circle Line (CCL) at Kallang, Bendemeer, and Geylang Bahru stations. The CCL connects directly to Marina Bay, Bishan, and Harbourfront without a transfer, while the EWL provides access to the CBD (City Hall: 5 stops) and Changi Airport (c.35 minutes). Bus connectivity is extensive, and the upcoming cycling/pedestrian infrastructure under Phase 4 of Kallang Alive will link the precinct to the Bishan–Ang Mo Kio Park network.

Schools Near Kallang

Within a 1–2 km radius of the Kallang/Whampoa precinct, buyers will find several well-regarded primary schools that are relevant for the Home Ownership Scheme Phase 1 (1km) and Phase 2 (2km) enrolment priority. St Andrew’s Junior School (1 km, SAP school) and Bendemeer Primary School sit within the core Kallang area. St Joseph’s Institution (secondary) and Raffles Institution (Bishan, 10 minutes by CCL) are nearby secondary options for families planning ahead.

Summary: Key Facts About Kallang in 2026

| Metric | Kallang D12 (2025/2026) |

|---|---|

| URA Planning Region | Central Region (RCR) |

| District | D12 |

| HDB 4-room resale median | S$650,000 |

| Private condo median PSF | ~S$1,680 |

| Gross rental yield (private) | ~3.8% |

| MRT lines | EWL (Kallang), CCL (Kallang / Bendemeer / Geylang Bahru) |

| Key masterplan | Kallang Alive (Phase 4 active) |

| Upcoming GLS | Peck Hay Road (closes June 2026, ~450 units) |

| ABSD (SC 1st property) | Nil (BSD only) |

| HDB loan rate | 2.60% p.a. (concessionary) |

Worked Example: Buying a Tanjong Rhu 2-Bedroom Condo

📊 Case Study: Ms Tan (SC, 35, First-Time Buyer) — S$1,580,000 2-Bedroom Condo, Tanjong Rhu Road

Purchase price: S$1,580,000

Buyer profile: Singapore Citizen, first property

Gross monthly income: S$9,500

Buyer’s Stamp Duty (BSD), administered by IRAS:

- First S$180,000 × 1% = S$1,800

- Next S$180,000 × 2% = S$3,600

- Next S$640,000 × 3% = S$19,200

- Next S$500,000 (balance to S$1.5m) × 4% = S$20,000… wait, S$1.58m – S$1.0m = S$580,000 at 4% = S$23,200

- Remaining: Balance of S$80,000 at 4% = S$3,200 (total above S$1.5M at 4%)

Total BSD = S$47,800

Additional Buyer’s Stamp Duty (ABSD): Nil — SC first property

Bank loan (75% LTV): S$1,185,000 @ 3.75% p.a., 25-year tenure = ~S$6,119/mth

TDSR check: S$6,119 ÷ S$9,500 = 64.4% — FAILS TDSR (ceiling 55%). Buyer would need to earn at least S$11,125/mth, or purchase jointly with a co-borrower.

With co-borrower at S$6,000/mth combined income S$15,500: TDSR = 39.5% — PASS.

Downpayment (25%): S$395,000

Total upfront: ~S$443,000 (downpayment + BSD + legal/conveyancing ~S$4,000)

This worked example illustrates why single-income buyers in Kallang’s private market may find the TDSR a binding constraint at prevailing prices. The HDB resale market — accessible with a HDB concessionary loan — remains the practical entry point for solo buyers earning below S$11k per month. Our Singapore home loan guide walks through TDSR and MSR in full detail.

What This Means for Buyers and Investors

Kallang’s investment case in 2026 rests on three pillars. First, the masterplan execution risk is substantially behind us — the Sports Hub is complete, the Aquatic Centre is open, and the precinct’s lifestyle infrastructure is no longer a promise but a reality. Second, the Kampong Bugis and Peck Hay Road pipeline will attract newer, higher-specification stock that tends to re-rate the area’s price ceiling rather than compress existing values (as seen in the Marina One / Marina Bay district effect on D1/D2 pricing). Third, rental demand from the sports and events corridor is sticky and growing as Singapore’s international events calendar expands.

The risk to the thesis is D14 Geylang spillover, which some buyers perceive as a drag on D12 positioning. In practice, Tanjong Rhu and the Sports Hub precinct are well insulated by geography from Geylang’s entertainment belt, and the two micro-markets appeal to very different buyer profiles.

What Might Come Next for Kallang

Looking ahead, three developments bear watching. The Peck Hay Road GLS tender award (expected Q3 2026) will reveal what developers are willing to bid for land in the Farrer Park/Kallang fringe — a strong land rate would confirm upward pricing pressure. The Kampong Bugis planning brief is expected to be finalised by URA in 2027, at which point development applications should follow in short order. Finally, any revision to the Master Plan 2025 for the Kallang Sports Hub buffer zone — currently zoned Open Space — could unlock further mixed-use potential along the waterfront. These are speculative scenarios, but all point in the same direction.

❓ Frequently Asked Questions about Kallang Property

Is Kallang a good place to buy a condo in 2026?

Kallang offers a strong RCR value proposition in 2026, with private condo PSF running approximately 8% below the RCR average despite its central location and superior transport connectivity. The Kallang Alive masterplan is in active Phase 4 execution, and the Kampong Bugis precinct adds long-term upside. Buyers should factor in that D12 has fewer new launch options than D1–D5, so most purchases are resale. The TDSR constraint at prevailing prices means single buyers need an income of S$11,000+ per month to service a S$1.5M+ property without a co-borrower.

Which MRT stations serve Kallang?

The main stations are Kallang MRT (East-West Line, EW10) and Kallang MRT (Circle Line, CC10) — both at the same physical station, making it an interchange. Nearby CCL stations include Bendemeer (CC8) and Geylang Bahru (CC9), providing access to Bishan, Marymount, and Harbourfront without a line change. The EWL connects to Raffles Place and City Hall in under 10 minutes.

Can foreigners buy property in Kallang?

Foreigners may purchase private condominium units in Kallang, but are subject to a 60% Additional Buyer’s Stamp Duty (ABSD) on all residential property purchases (effective as at the 2023 cooling measures). HDB flats are not available to foreign nationals. Permanent Residents (PRs) buying a first private property pay 5% ABSD; a second property attracts 30% ABSD. Given the 60% ABSD, foreign demand for D12 is minimal, which means the market is almost entirely driven by Singapore Citizens and PRs — a structural positive for price stability.

What is the Kampong Bugis development plan?

Kampong Bugis is a 9-hectare waterfront site in Kallang/Tanjong Rhu that URA has identified for a car-lite, sustainable mixed-use precinct under the Master Plan 2025. The plan envisions residential, commercial, and community uses connected by a waterfront promenade extending to the Sports Hub. Development is expected to proceed in phases from the late 2020s onwards, pending URA finalisation of the planning brief. Once developed, Kampong Bugis is expected to add approximately 4,000–6,000 residential units to the Kallang corridor.

How does the Selective En-Bloc Redevelopment Scheme (SERS) affect Kallang HDB flats?

SERS is HDB’s programme to redevelop older housing estates, offering existing flat owners a replacement flat at a new site along with market-based compensation. Several Kallang and Whampoa HDB blocks have been selected for SERS over the years. If you are buying a resale flat in Kallang, check the HDB portal for any known SERS designations. A SERS selection effectively creates a de facto acquisition at compensation value — which may be favourable or unfavourable depending on the price paid and the replacement flat terms offered by HDB.

What are the best streets to buy in Kallang?

For lifestyle and masterplan upside, Tanjong Rhu Road and Stadium Boulevard / Stadium Crescent offer the best proximity to the Sports Hub waterfront and the anticipated Kampong Bugis uplift. For HDB buyers, Whampoa Drive and Boon Keng Road offer well-priced resale stock with strong CCL connectivity. The Bendemeer Road corridor suits buyers seeking new-ish private leasehold stock (e.g., Centro Residences) at a slight discount to the Tanjong Rhu premium.

What is the ABSD for a Singapore Citizen buying a first property in Kallang?

A Singapore Citizen purchasing their first residential property pays no ABSD — only Buyer’s Stamp Duty (BSD) applies. For a S$1,580,000 condo, BSD is approximately S$47,800 (calculated on the tiered rate schedule administered by IRAS: 1% on the first S$180k, 2% on the next S$180k, 3% on the next S$640k, and 4% on the remainder). Full ABSD rates for all buyer profiles are set out in our ABSD Singapore 2026 guide.

Click anywhere outside to close