River Valley & Robertson Quay Neighbourhood Guide Singapore 2026: Property Prices, MRT and Investment Outlook

River Valley and Robertson Quay sit at the heart of Singapore’s most coveted residential precinct — District 9 (D09), Core Central Region (CCR). Sandwiched between the Singapore River to the south and the Orchard Road belt to the north, these two sub-precincts offer a rare combination: walkable waterfront lifestyle, genuine city-fringe connectivity (three MRT lines within 600 metres since the Thomson–East Coast Line opened in June 2023), internationally acclaimed schools, and a concentration of freehold and long-tenure leasehold condominiums that rarely appear in the Outside Central Region. This River Valley Robertson Quay neighbourhood guide Singapore 2026 covers property prices, MRT access, top schools, rental yields, capital growth trends, and everything a buyer or investor needs to know before committing to D09.

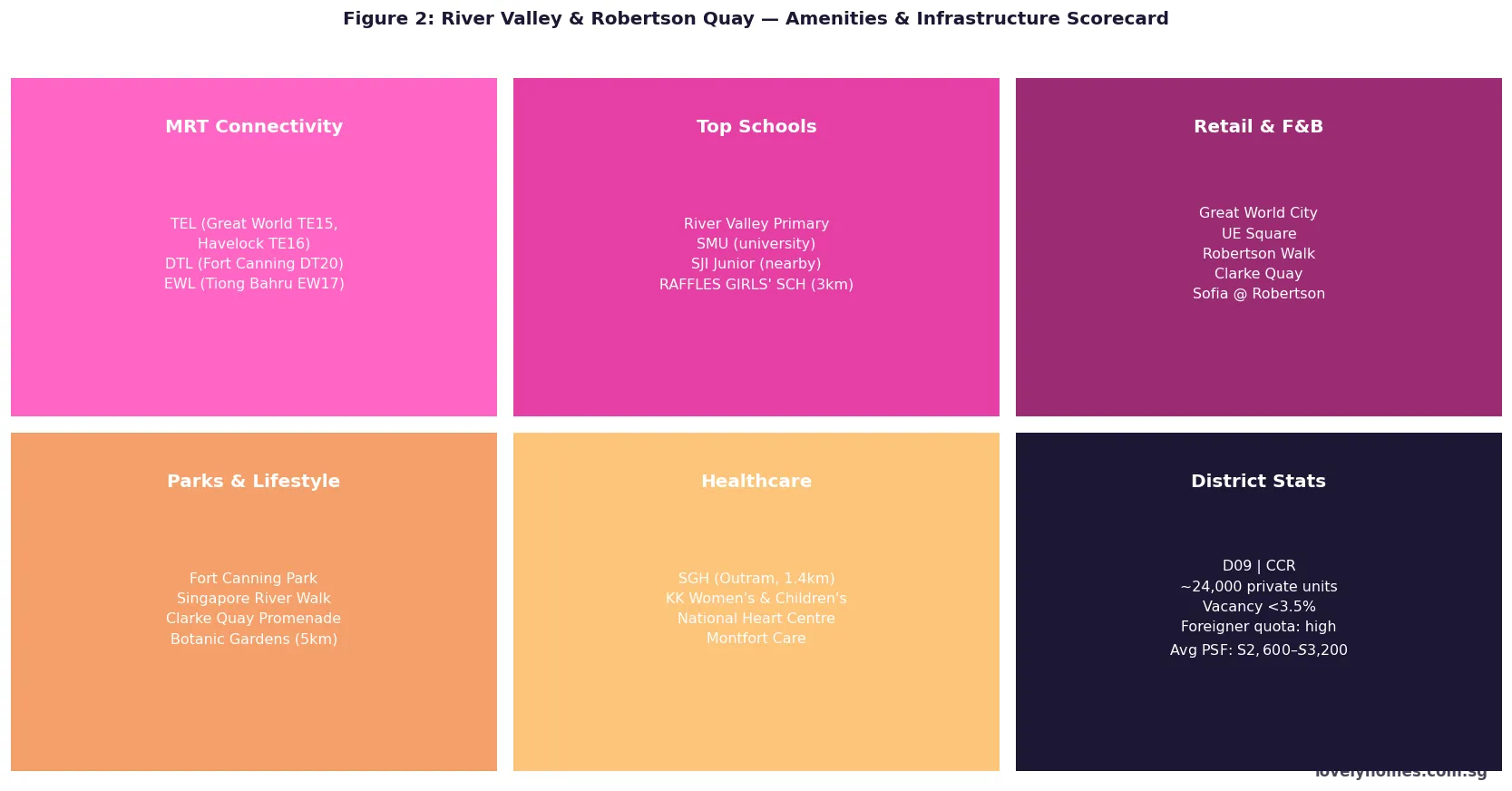

- District 9, CCR — one of Singapore’s three Core Central Region districts alongside D10 and D11.

- New TEL stations (Great World TE15 and Havelock TE16) opened June 2023, fundamentally improving connectivity without new launches disrupting the area’s streetscape.

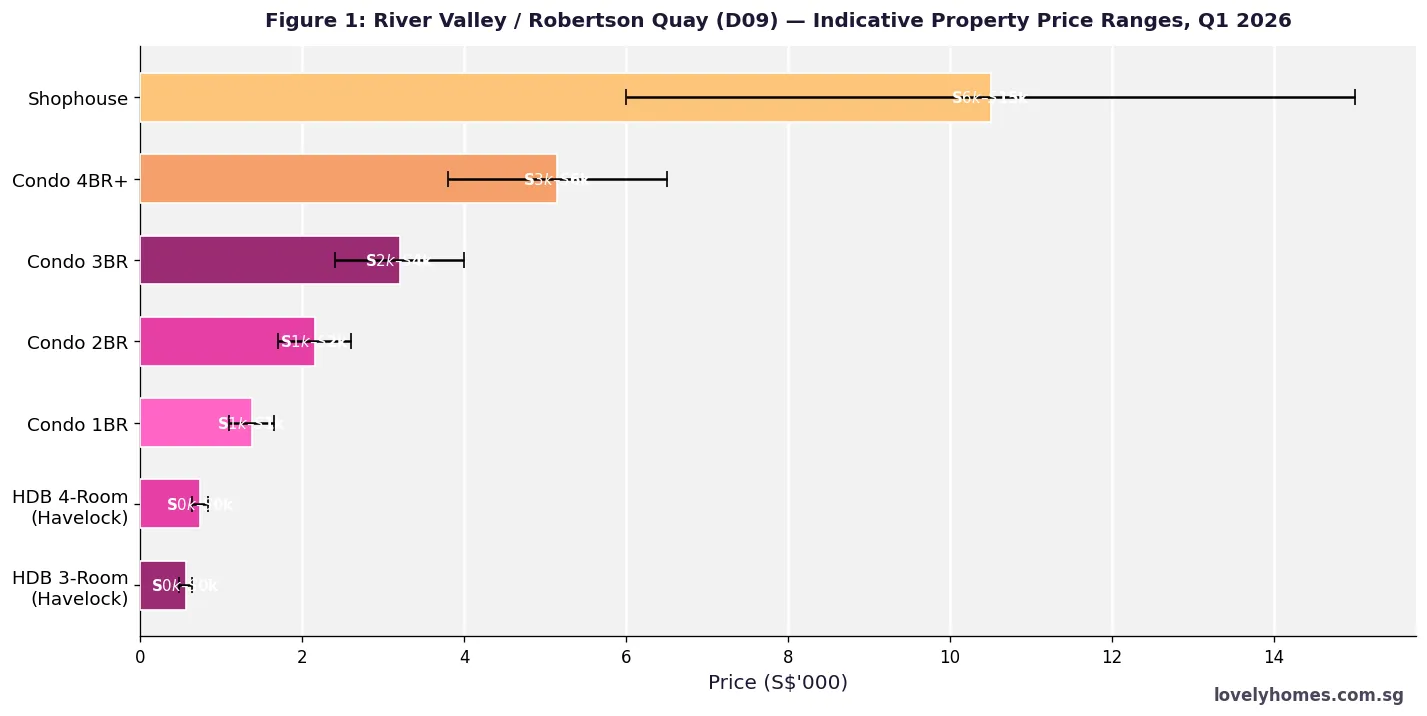

- Private condo prices range from S$1,100,000 for a 1-bedroom to S$6,500,000+ for a 4-bedroom; average PSF runs S$2,600–S$3,200 for freehold stock.

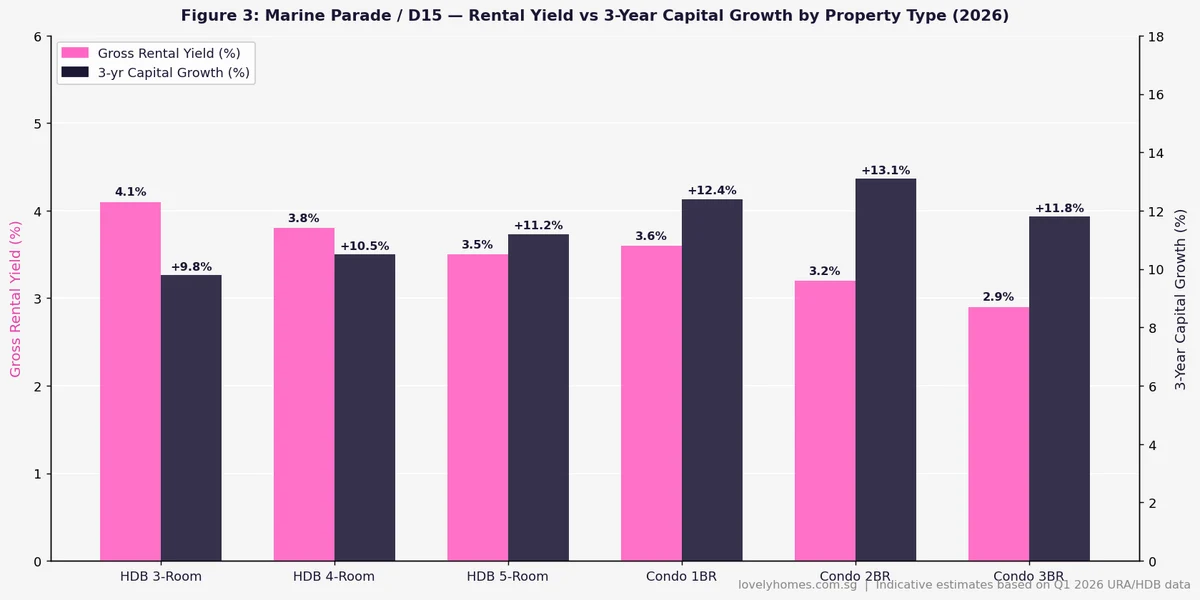

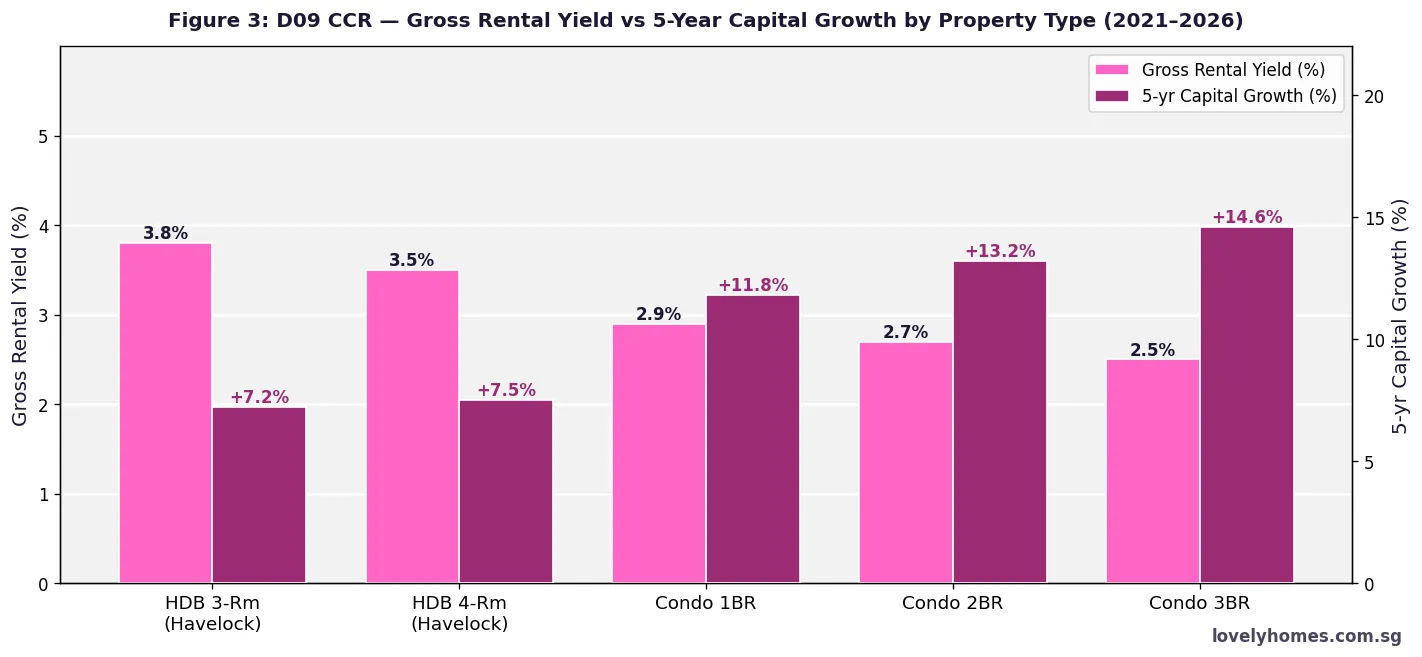

- Gross rental yields: 2.5%–2.9% for larger units, 3.4%–3.8% for 1-bedrooms — lower than OCR, but sustained by high-income expat tenants in finance, law, and tech.

- Five-year capital growth (2021–2026): +11.8% to +14.6% across private condos, tracking the broader CCR PPI.

- No new GLS site has been awarded in the River Valley / Robertson Quay sub-precinct since 2018 — supply scarcity is a structural investment thesis.

- Singapore Citizens buying their first private property pay 0% ABSD; foreigners pay 60%. ABSD 20% applies for SC second-property purchases.

River Valley Robertson Quay — Where Is It and What Makes It Distinctive?

River Valley and Robertson Quay are planning sub-zones within the Museum Planning Area and River Valley Planning Area of URA’s Master Plan. Geographically, the area stretches from River Valley Road (the main artery) south to the Singapore River, and from Mohamed Sultan Road / Clemenceau Avenue in the west to the Orchard/Somerset boundary in the east.

What makes this precinct genuinely different from Singapore’s other CCR sub-markets (Orchard, Cairnhill, Ardmore) is its character. Where Orchard feels commercial and Ardmore is quiet enclave-landed, River Valley and Robertson Quay have a lived-in, convivial quality — dozens of independent restaurants, riverside bars, weekend arts markets at Clarke Quay, Fort Canning Park’s concert lawn, and a density of international schools and nurseries that reflects the long-established expat tenant community. Many of Singapore’s largest private banks, law firms, and regional headquarters cluster within a 2-kilometre radius, feeding consistent demand for high-specification rental accommodation.

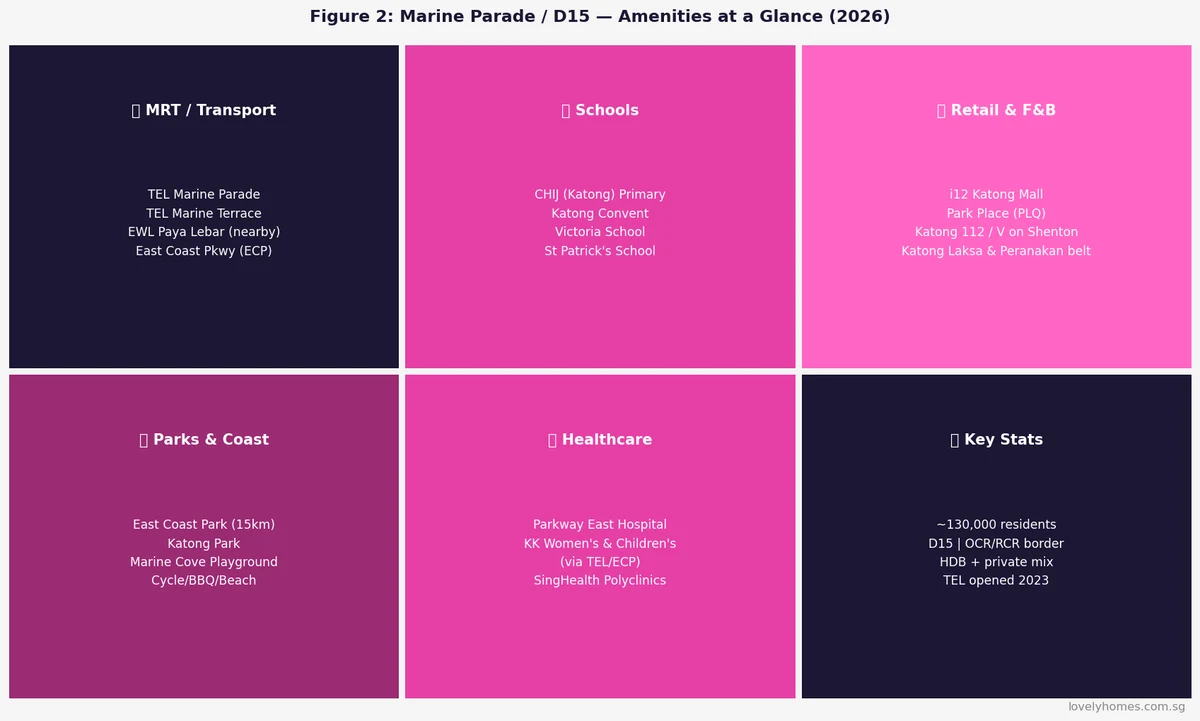

MRT Connectivity — Three Lines Within Walking Distance

Prior to June 2023, District 9’s connectivity was widely cited as its one weakness relative to D10 or D11 — the nearest MRT stations (Somerset NS23 and Clarke Quay NE5) required a 10–15 minute walk from many River Valley condominiums. The opening of the Thomson–East Coast Line’s Stage 3 changed the calculus materially:

- Great World (TE15 — TEL): Located on Kim Seng Road, a 5-minute walk from most River Valley condos along Kim Seng Road and Martin Road. Interchange planned with future Jurong Region Line extension in long-range planning; already connects to Orchard (TE14, 1 stop north) and the TEL’s eastern branches toward Marine Parade and Bayshore.

- Havelock (TE16 — TEL): Serves the Havelock Road and Robertson Quay western edge; useful for residents in River Gate, Aspen Heights, and Havelock View Towers. Connects south toward Outram Park (TE17 — interchange with EWL and NEL) and Cantonment (TE18).

- Fort Canning (DT20 — DTL): On the Downtown Line, this station is a 7–10 minute walk from Robertson Quay and links directly to Bugis (DT14/EW12), Downtown (DT17), and via interchange to Marina Bay, Buona Vista, and Expo.

For commuters to the CBD (Raffles Place, Shenton Way), the travel time from Great World TE15 to Marina Bay TE20 is approximately 8 minutes on the TEL — comparable to driving at peak hour and far more reliable. For residents working in the Orchard/Somerset belt, it is one stop. The TEL has repositioned River Valley from “slightly inconvenient” to “exceptionally well served”.

Schools in River Valley and Robertson Quay

River Valley Primary School (RVPS), located on River Valley Road, is the district’s anchor primary school and draws families from across Singapore willing to buy or rent in-zone to secure a Phase 2C ballot priority. The school is within the 1-kilometre priority zone for several major condominiums including The Avenir, Rivière, and Martin Modern.

At the secondary level, Gan Eng Seng School and Queenstown Secondary are accessible via the TEL. Singapore Management University (SMU) — one of Singapore’s six autonomous universities — is a 15-minute walk from Robertson Quay via Fort Canning; its proximity contributes to the area’s intellectual and professional character. For international families, the international schools cluster in the broader CCR zone (Orchard, Tanglin, Stevens) is accessible in 10–15 minutes.

Property Market Overview — D09 CCR Prices and Supply

District 9 is a near-exclusively private residential market. HDB flat supply in the area is negligible — the Havelock HDB estate on the western fringe has a small number of older flats, most of which are past their lease peak, but they represent a tiny fraction of the district’s housing stock. The dominant product is the private condominium — ranging from boutique freehold projects of 30–50 units to larger 99-year leasehold developments of 300–600 units.

Key benchmark projects:

- The Avenir (freehold, D09, River Valley Close): 376 units across two 36-storey towers. Completed 2024. Benchmark PSF S$2,800–S$3,200. Developed by GuocoLand and Hong Leong Holdings.

- Rivière (99yr leasehold, Jiak Kim Street): 455 units. Former Zouk site. TEL Great World station at doorstep. Benchmark PSF S$2,400–S$2,900. Frasers Property development.

- Martin Modern (99yr leasehold, Martin Place): 450 units. GuocoLand. Benchmark PSF S$2,200–S$2,600.

- The Waterfall, RV Altitude, One Draycott (freehold older stock): PSF S$2,000–S$2,500.

Transaction volume in D09 is thin by Singapore standards — typically 250–400 resale caveats per year — which means individual transactions can move the median PSF meaningfully. Freehold premium over 99-year leasehold in this precinct runs approximately 8–15%, narrower than the national average because the 99-year stock (Rivière, Martin Modern) is of very high quality with TEL access.

| Property Type | Indicative Price Range | Indicative PSF | Gross Yield (Est.) | Tenure |

|---|---|---|---|---|

| HDB 3-Room (Havelock) | S$480k – S$640k | S$560–S$700 | 3.8% | Leasehold (ageing) |

| HDB 4-Room (Havelock) | S$640k – S$840k | S$580–S$720 | 3.5% | Leasehold (ageing) |

| Private Condo 1BR | S$1.1M – S$1.65M | S$2,400–S$3,000 | 3.4%–3.8% | Freehold / 99yr |

| Private Condo 2BR | S$1.7M – S$2.6M | S$2,500–S$3,100 | 2.9%–3.3% | Freehold / 99yr |

| Private Condo 3BR | S$2.4M – S$4.0M | S$2,600–S$3,200 | 2.5%–2.9% | Freehold / 99yr |

| Private Condo 4BR+ | S$3.8M – S$6.5M | S$2,700–S$3,300 | 2.3%–2.7% | Freehold / 99yr |

| Shophouse (Heritage) | S$6M – S$15M | S$5,500–S$9,000 | 1.8%–2.5% | Freehold |

Rental Market — Who Rents in River Valley and Robertson Quay?

The D09 rental market is structurally different from OCR precincts. Rather than young professionals on tight budgets seeking HDB rooms or studio apartments, the tenant pool in River Valley and Robertson Quay skews toward:

- Expatriate finance and legal professionals — private banks, hedge funds, and international law firms cluster in the Marina Bay Financial Centre and Raffles Place, both reachable from Great World TE15 in under 12 minutes. Housing allowances of S$6,000–S$12,000 per month are common.

- Senior corporate and tech executives — regional headquarters of multinational companies increasingly concentrate in the one-north/Tanjong Pagar corridor, accessible via the TEL.

- International families — the area’s proximity to the international school belt (Tanglin Trust, UWCSEA East, ISS) makes it attractive to families with school-age children.

Median monthly rents in D09 for a 2-bedroom condominium run approximately S$5,800–S$7,500 (Q1 2026), reflecting a modest correction from the 2022–2023 rental peak of S$7,000–S$9,000 but still well above pre-pandemic levels. Vacancy in the precinct is estimated below 3.5% — reflecting tight supply and durable expat demand.

🏠 Worked Example: Mr & Mrs Chua — SC Upgraders Buying Martin Modern 2BR

Profile: Mr & Mrs Chua, Singapore Citizens, joint income S$16,000/month. Currently own a Bishan 4-room HDB flat (MOP cleared, sold on 30 April 2026 for S$840,000). Buying a Martin Modern 2BR (99yr leasehold) at S$2,200,000. This is their first private property.

Stamp duty:

- BSD on S$2,200,000: 1% × S$180k + 2% × S$180k + 3% × S$640k + 4% × S$500k + 5% × S$700k = S$1,800 + S$3,600 + S$19,200 + S$20,000 + S$35,000 = S$79,600

- ABSD: Nil — SC couple, first private property (HDB sold before OTP granted)

Financing:

- Purchase price: S$2,200,000 | LTV 75% → Bank loan: S$1,650,000

- Monthly repayment at 3.0% p.a. 25yr: approximately S$7,832/month

- TDSR: S$7,832 ÷ S$16,000 = 48.9% — PASS (within 55% limit)

Upfront cash/CPF required:

- 25% down payment: S$550,000

- BSD: S$79,600

- Conveyancing fees: ~S$5,000

- Total upfront: approximately S$634,600 (can partly draw from CPF OA after HDB CPF refund)

Investment projection: At +13.2% 5-year CCR growth (historical trend), the S$2.2M unit appreciates to approximately S$2.49M by 2031. Combined with net rental income (~S$5,800/month at 2.9% gross, less property tax and maintenance), the total return scenario is approximately S$290k capital + S$174k net rental = ~S$464k over 5 years. Past performance does not guarantee future results — see Disclaimer.

Investment Case — Why River Valley and Robertson Quay in 2026

The structural case for D09 rests on three pillars that are unique to this precinct. First, supply scarcity: unlike OCR planning areas such as Tampines or Sengkang where GLS sites are regularly released, the River Valley and Robertson Quay sub-zones are essentially built-out. URA has not awarded a GLS site in this immediate precinct since the Jiak Kim Street site (Rivière, awarded 2018). Future supply, if any, would likely come from en-bloc redevelopment — a slow, expensive process that takes 5–8 years from acquisition to launch.

Second, the TEL re-rating is still working through property values. Research from URA transaction data suggests that properties within 500 metres of new TEL stations in previously underserved areas have outperformed the broader CCR average by 2–4 percentage points per annum in the two to three years post-opening. The Great World and Havelock stations opened in June 2023, meaning the full impact may not yet be fully priced in.

Third, Singapore’s attraction as a global wealth hub continues to drive demand for the CCR’s top-end rental pool. Despite the 60% ABSD on foreigners (which has effectively removed foreign owner-occupier buyers from the market), Singapore’s population of ultra-high-net-worth individuals — many of whom now hold Permanent Residency or citizenship — continues to grow. Wealthy PRs buying a first or second property in D09 pay 5% or 30% ABSD respectively — meaningful but manageable given the capital quantum. Many still prefer D09 over offshore alternatives for personal use.

What Might Come Next for River Valley and Robertson Quay

This section is editorial opinion and forward-looking speculation, clearly labelled as such.

The URA Draft Master Plan 2025 identified the Greater Southern Waterfront (GSW) — a 2,000-hectare stretch from Pasir Panjang to Marina East — as a long-term transformation zone. River Valley and Robertson Quay sit at the northern edge of this precinct, and the eventual reconfiguration of the Tanjong Pagar port lands (expected 2027–2030 for the first phases) could draw more F&B, cultural, and lifestyle development southward along the Singapore River, extending the Robertson Quay “lifestyle zone” further toward the coast.

On the regulatory side, some market analysts have speculated that ABSD rates for foreigners (currently 60%) could be moderated if the US–Singapore bilateral economic relationship strengthens and if Singapore’s primary residential market cools further following the 60% ABSD introduction. However, there are no signals from the Ministry of National Development or the Ministry of Finance that any such change is imminent.

Frequently Asked Questions

Is River Valley a good place to buy property in Singapore?

River Valley and Robertson Quay offer a compelling combination of lifestyle, connectivity, and capital preservation that justifies the premium over OCR and RCR districts. The TEL opening in June 2023 resolved the precinct’s previous connectivity weakness. The absence of new GLS supply in the sub-zone for over seven years means that any further demand uplift — from population growth, wealth inflows, or the Greater Southern Waterfront transformation — would tighten an already scarce market. For buyers who can absorb the higher entry price (S$1.1M+ for a 1-bedroom) and do not need above-3% yield, D09 River Valley and Robertson Quay represents one of Singapore’s most defensible residential investments. It is not the right choice for buyers seeking high rental yield or affordable entry.

Which MRT stations serve River Valley and Robertson Quay?

Three MRT stations are within comfortable walking distance of the precinct. Great World (TE15, Thomson–East Coast Line) on Kim Seng Road serves the eastern River Valley portion; Havelock (TE16, TEL) serves Robertson Quay’s western side and the Havelock Road corridor. Fort Canning (DT20, Downtown Line) is a 7–10 minute walk from Robertson Quay via River Valley Road and is particularly useful for commuters heading toward Bugis, Promenade, or Buona Vista. Somerset (NS23, North–South Line) is a 12–15 minute walk from the northern edge of River Valley Road and provides access to Orchard and the NSL.

Can foreigners buy property in River Valley and Robertson Quay?

Foreigners can purchase private condominiums, apartments, and commercial shophouses in D09. However, since April 2023, foreigners pay 60% ABSD on any Singapore residential property purchase — a flat rate on the entire purchase price. On a S$2.5M condominium, that is S$1.5M in ABSD alone. Foreigners cannot purchase HDB flats, ECs (within MOP), or landed property (unless on Sentosa Cove or with specific SLA approval). Despite the 60% ABSD, a small number of ultra-high-net-worth foreign buyers continue to transact in CCR — particularly for trophy units above S$5M — typically sourced from family offices and private banking clients who view Singapore residential property as part of a broader wealth-preservation and residency strategy.

What are the best condominiums in River Valley and Robertson Quay?

The benchmark freehold projects in 2026 are The Avenir (River Valley Close, 376 units freehold, completed 2024, PSF S$2,800–S$3,200) and the established older-stock freehold buildings along River Valley Road including RV Altitude and The Grange. For 99-year leasehold, Rivière (Jiak Kim Street, 455 units, Frasers Property, adjacent to Great World TE15 station) and Martin Modern (Martin Place, 450 units, GuocoLand) are the contemporary benchmarks. Rivière in particular benefits from arguably the best direct TEL station access of any condominium in the precinct. Older boutique freehold projects (sub-100 units) can offer attractive value for buyers who prioritise freehold tenure and do not require a gymnasium or full facilities.

How does River Valley compare to Holland Village or Orchard?

All three sub-precincts sit within D09/D10 CCR, but each has a distinct character. River Valley and Robertson Quay offer the most vibrant street-level lifestyle — riverside F&B, Fort Canning Park, and the Singapore River waterfront — but at CCR prices and with smaller absolute retail mall footprints than Orchard. Holland Village (D10) has a village-in-the-city feel, lower density, and proximity to Buona Vista’s biomedical cluster. Orchard (D09/D10 border) offers the greatest retail density and brand-name condominium presence, but the immediate streetscape is less liveable. For families, Holland Village’s proximity to international schools (UWCSEA, AIS) is a draw that River Valley does not fully replicate. For young professionals and empty-nesters prioritising walkable lifestyle and CBD access, River Valley/Robertson Quay tends to win the comparison.

Is there any new HDB BTO supply in River Valley?

No. There is no HDB BTO supply in River Valley or Robertson Quay. The area is designated as a mature private residential precinct under the URA Master Plan. The only HDB stock in the broader D09 area is the existing Havelock Road HDB estate — older flats built in the 1970s and 1980s that transact at S$480,000–S$840,000 on the resale market. These Havelock flats are subject to lease decay risk given their age (remaining leases of 40–55 years as of 2026) and are generally not recommended for buyers seeking CPF-eligible long-tenure financing. For HDB BTO applicants interested in CCR-adjacent living at lower cost, the June 2026 BTO launch in Ang Mo Kio and Bukit Merah is the nearest available option.

Click anywhere outside the image to close