HDB BTO vs Resale Flat 2026: Complete Comparison — Prices, Grants, Waiting Time and New Classification Rules

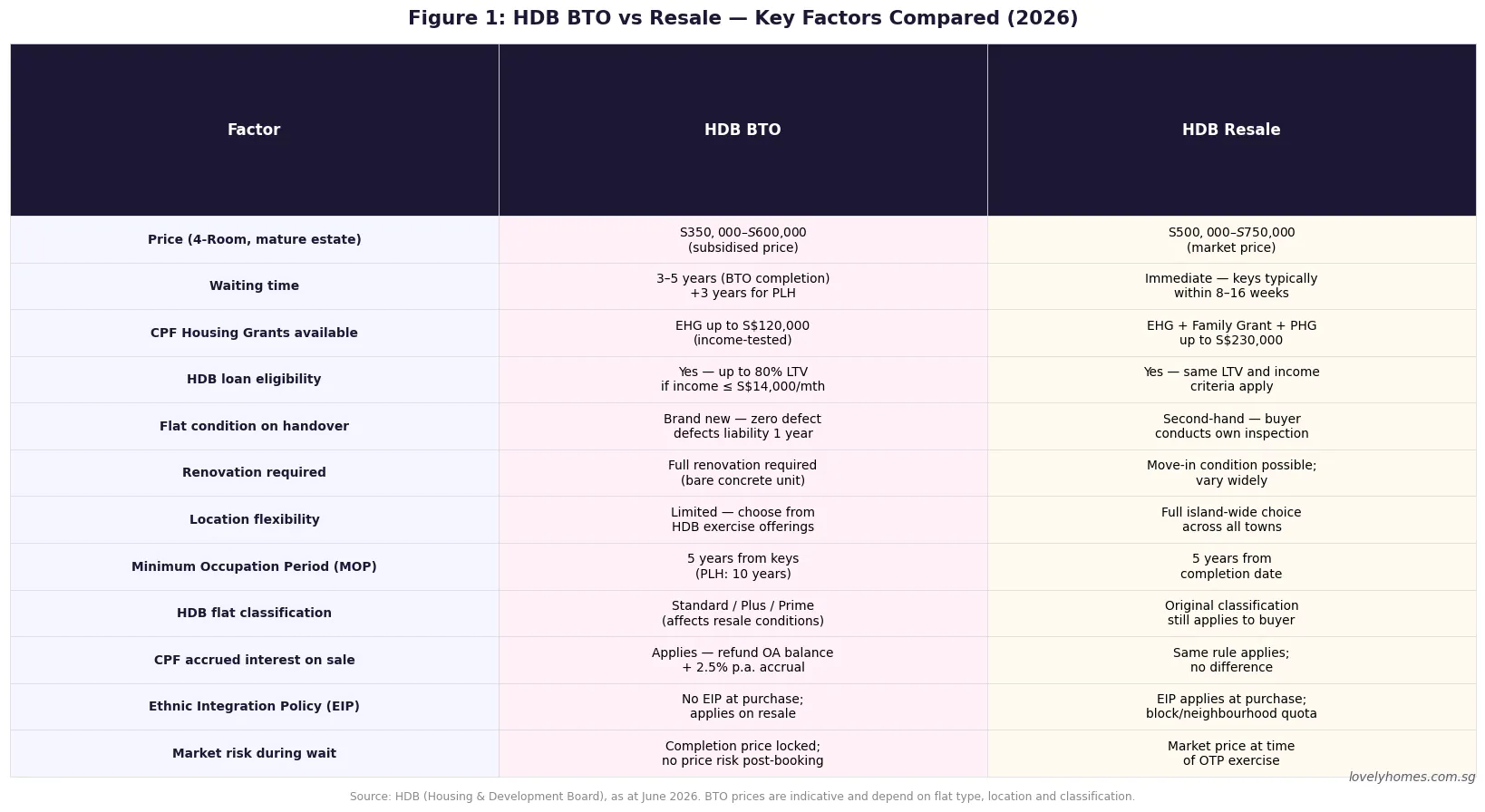

Quick Answer: HDB BTO vs Resale — Key Differences in 2026

- BTO flats are sold directly by HDB at subsidised prices; resale flats are bought from existing HDB owners at market prices.

- BTO typically takes 3–5 years from application to keys; resale flats can complete within 8–16 weeks.

- Resale buyers qualify for more grants in total (up to S$230,000 for an SC couple) versus BTO (up to S$120,000 EHG only), but resale prices are generally higher.

- BTO flats are brand new; resale flats are second-hand and vary significantly in age, condition, and remaining lease.

- The new HDB classification — Standard, Plus, Prime — applies to BTO flats from August 2024 onwards, introducing longer resale restrictions for Plus and Prime flats.

- Resale buyers must comply with the Ethnic Integration Policy (EIP) quota at point of purchase; BTO buyers face EIP only when they later sell.

- Both BTO and resale flats are subject to a 5-year MOP (10 years for PLH flats), HDB loan eligibility rules, and the same TDSR/MSR framework.

- For most first-time buyers with flexible timelines, BTO offers better value; for those with urgent housing needs or preferring mature-estate locations, resale may be more practical.

The decision between buying an HDB Build-To-Order (BTO) flat and a resale flat is one of the most consequential financial choices a Singapore household will make. Both routes lead to the same product — a Housing and Development Board flat — but the economics, timelines, and trade-offs are fundamentally different. BTO flats come at a subsidised price set by HDB, with a waiting period of three to five years; resale flats trade at market value with immediate occupancy. The introduction of the new Standard, Plus, and Prime flat classification from August 2024, combined with an increase in BTO supply and a moderation in resale prices following the 2023–2024 cooling cycle, has shifted the calculus for buyers in 2026. This guide walks through every key dimension of the comparison so you can make an informed decision.

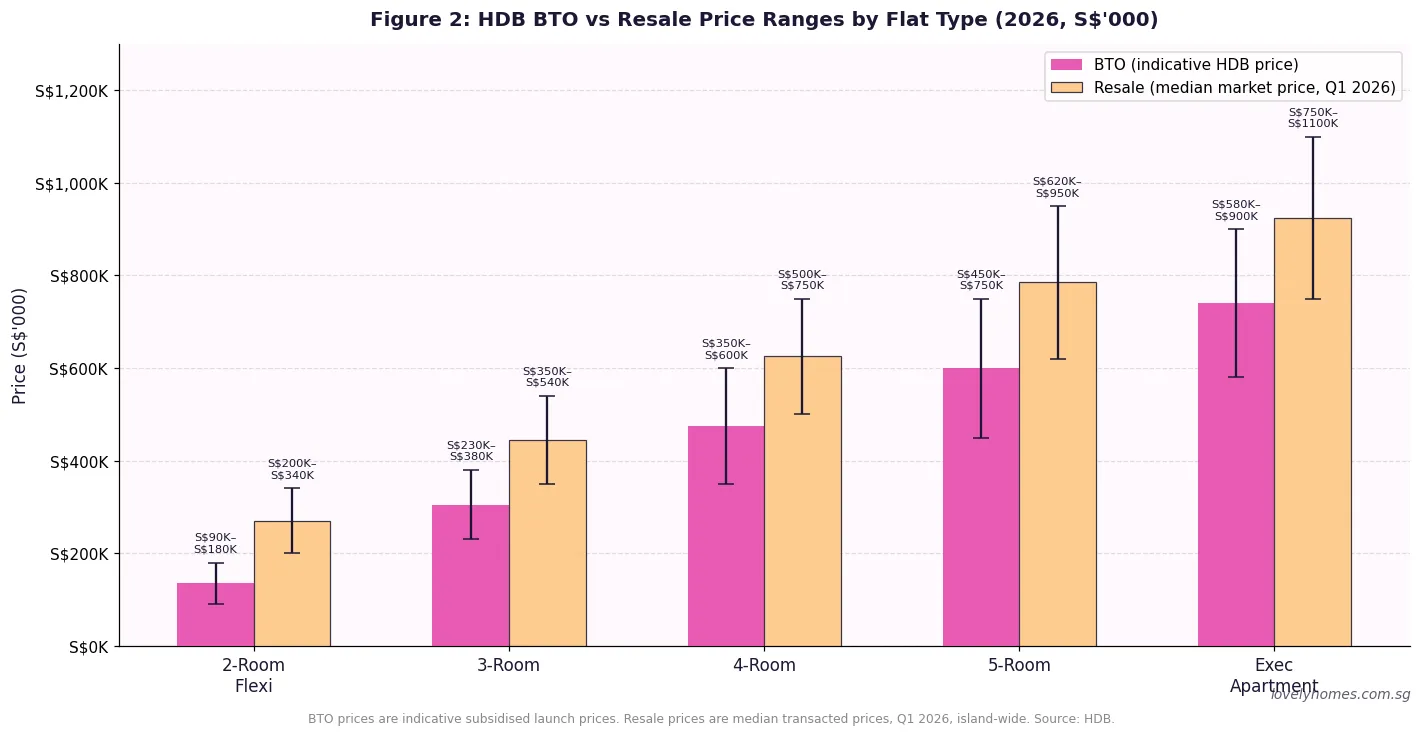

Price: BTO Subsidy vs Resale Market Value

The most obvious difference between BTO and resale is price. HDB sells BTO flats at a price that reflects a deliberate subsidy relative to market value. For a typical 4-room flat in a non-mature estate, a BTO price might be S$350,000–S$550,000 at launch, while a resale flat of similar size in the same town might transact at S$500,000–S$700,000. The gap narrows in mature estates, where BTO launches are rarer and resale supply is the only option for buyers who want to live in areas like Queenstown, Bishan, or Marine Parade.

It is important to note that BTO prices are not static: HDB adjusts BTO launch prices for each exercise based on prevailing market conditions, and the subsidy quantum (the gap between BTO price and estimated market value) has been explicitly referenced by HDB in its public communications as a policy instrument to keep public housing affordable. In 2025–2026, HDB increased BTO supply substantially — over 19,000 units are planned for 2026 across four exercises — as part of a concerted effort to reduce waiting times and moderate the resale price premium.

Waiting Time: BTO vs Resale Completion

BTO construction timelines have improved since the post-pandemic supply chain delays of 2021–2022, but the typical wait remains three to five years from the launch exercise to key collection, and this excludes the time spent waiting for a ballot exercise in your preferred town. Popular towns with first-timer subscription rates of 2×–5× may require multiple attempts before a successful ballot. Add the construction period and many buyers face an effective six-to-seven-year wait from first application to occupancy.

Resale flats can complete within eight to sixteen weeks of exercising the Option to Purchase (OTP). Buyers who need housing immediately — couples with an imminent wedding, families moving out of parents’ flats, or those relocating for work — have only one viable HDB option: the resale market. The opportunity cost of the BTO waiting period also includes continued rental expenditure, which can total S$80,000–S$120,000 over a four-year wait at current market rates.

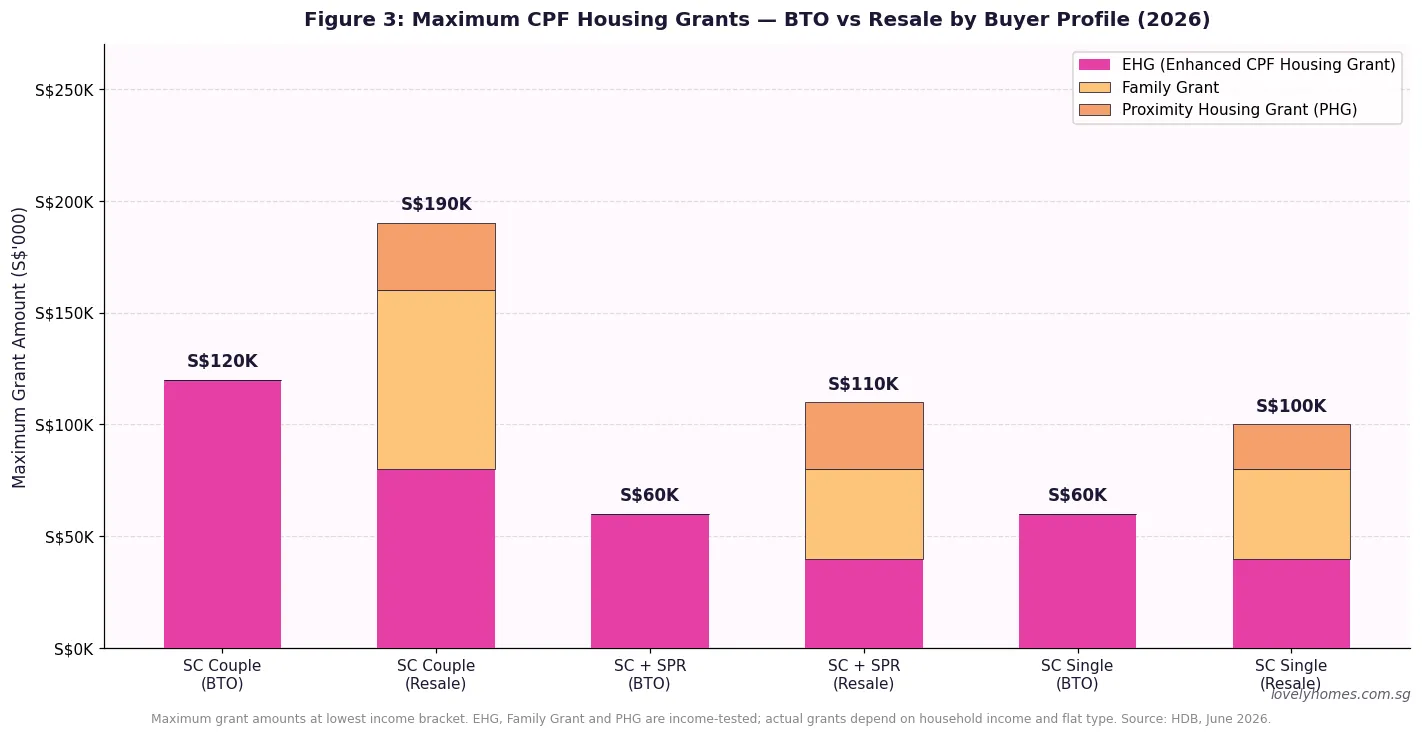

CPF Housing Grants: Where Resale Has the Edge

CPF housing grants are means-tested subsidies administered by HDB and disbursed from the Central Provident Fund (CPF) to help buyers finance their flat purchase. The grant landscape differs meaningfully between BTO and resale:

For BTO buyers, the primary grant is the Enhanced CPF Housing Grant (EHG), which provides up to S$120,000 for an SC couple earning a combined monthly income of S$1,500 or below, tapering to S$0 at income above S$9,000 per month. No additional grants apply for BTO purchases.

For resale buyers, three grants can stack: the EHG (up to S$80,000 for resale), the Family Grant (up to S$80,000 for SC couples buying a 4-room or smaller resale), and the Proximity Housing Grant (PHG) of up to S$30,000 for buyers choosing to live near parents or children. An SC couple at the lowest income bracket can receive up to S$230,000 in grants for a resale flat — nearly double the BTO maximum.

The higher grant quantum for resale partially offsets the higher purchase price. At mid-range incomes (combined S$7,000–S$8,000 per month), the effective all-in cost difference between BTO and resale may be narrower than headline prices suggest, once grants and the value of time saved (by avoiding the BTO waiting period) are factored in.

Flat Condition, Age, and Remaining Lease

BTO flats are handed over as bare concrete units — no flooring, no kitchen fittings, no bathroom tiles beyond the developer’s basic provision. A full renovation budget of S$40,000–S$80,000 is typical for a 4-room BTO flat. This is a significant additional cost that is sometimes overlooked in simple price comparisons.

Resale flats may require less renovation (in some cases none) if the existing fittings are in good condition. However, older flats — particularly those with 50 years or fewer remaining on their 99-year leases — carry meaningful risks. CPF withdrawal for older flats is restricted under the CPF property rules, and bank valuations may not fully support the asking price. HDB resale flats built in the 1980s and 1990s are now approaching the age at which lease decay begins to have a material effect on financing options and eventual resale value.

The New BTO Classification Framework

From August 2024, all new BTO flats are classified under HDB’s new Standard / Plus / Prime framework, replacing the previous Mature / Non-Mature categorisation for new launches. The key distinctions are:

| Classification | Locations | Subsidy Level | Resale Restriction | Income Ceiling |

|---|---|---|---|---|

| Standard | Heartland estates, non-central towns | Standard subsidy | Standard 5-yr MOP then open resale | S$14,000/mth |

| Plus | Near MRT interchange, town centre, amenity-rich sites | Deeper subsidy | 5-yr MOP + 10-yr restricted resale (SC/SPR only) + subsidy clawback | S$14,000/mth |

| Prime | City-fringe, central locations (Queenstown, Rochor) | Deepest subsidy | 10-yr MOP + restricted resale + subsidy clawback on sale | S$14,000/mth |

The subsidy clawback for Plus and Prime flats means that on eventual resale, a proportion of the subsidy received is returned to HDB. This reduces your net sale proceeds but is structured to prevent windfall gains from publicly subsidised flats. For buyers primarily motivated by investment upside, Standard flats or resale flats may offer better flexibility; for buyers prioritising lower entry cost and location quality, Plus or Prime BTO flats may still be the better long-term choice.

Worked Example: Lee Family — BTO vs Resale Decision

Scenario: Mr and Mrs Lee, SC Couple, Combined Income S$8,500/mth

The Lees are first-time buyers. They are considering two options: (A) a 4-room BTO flat in Tengah (Standard classification) at S$420,000, with an expected wait of 4 years from launch to keys; or (B) a 4-room resale flat in Bukit Batok at S$610,000, with completion expected in 12 weeks.

Option A: BTO — Tengah 4-Room Standard, S$420,000

Option B: Resale — Bukit Batok 4-Room, S$610,000

Comparison summary: Option A BTO total out-of-pocket over 4 years (before valuation appreciation): S$420K price + S$55K renovation + S$96K rental − S$35K grant = effective all-in entry cost ~S$536K. Option B resale: S$610K price + S$15K reno − S$105K grants = effective all-in ~S$520K. In this scenario, the Lees’ resale option is marginally cheaper in total outlay — driven by the larger grant stack and the elimination of four years of rental costs — though their monthly mortgage commitment is S$687/mth higher than the BTO.

What This Means for Buyers in 2026

The BTO versus resale decision in 2026 is more finely balanced than it was during the 2021–2022 resale price surge, when resale flats were trading at sharp premiums over BTO prices. The HDB resale price index recorded its first quarterly decline since Q2 2019 in Q1 2026 (down 0.1% quarter-on-quarter), while BTO supply has increased materially. Buyers who previously felt priced out of resale now have a more realistic comparison to make.

Several structural shifts make resale more attractive in 2026 than it has been in recent years. The new classification framework means that some BTO sites carry extended resale restrictions that limit eventual exit flexibility. Meanwhile, the grant system for resale has been left intact and continues to provide up to S$230,000 for qualifying first-timer couples. For buyers who prioritise a specific location — a mature town, proximity to ageing parents, or a well-established school cluster — resale remains the only viable route.

Conversely, buyers with flexible timelines and no urgent housing need continue to find BTO the better financial proposition in most non-mature towns. The government’s stated policy goal — ensuring that public housing remains within reach for first-timer households across a range of income levels — means BTO subsidies are unlikely to be withdrawn. The deeper subsidies attached to Plus and Prime flats, in particular, make BTO viable in locations that would otherwise be inaccessible to median-income households.

What Might Come Next

HDB has indicated that BTO waiting times should return to the pre-pandemic norm of three years or fewer for most projects by 2026–2027, as the construction backlog clears and new projects are designed from the outset with more efficient procurement. A shorter BTO waiting time would reduce one of the main deterrents to the BTO route. The October 2026 BTO exercise, expected to offer approximately 7,960 flats in six towns, will be the final exercise of the year and is likely to attract significant demand from buyers who held back during the 2025 exercises. On the resale side, the 2026 MOP cohort (13,480 flats) will continue to put new supply onto the resale market through the year, exerting some downward pressure on resale prices — a trend to watch for buyers on the fence between the two routes.