River Valley Green Parcel C GLS 2026: Top Bid S$1,730 psf ppr Sets New River Valley Benchmark

Quick Answer: River Valley Green Parcel C GLS 2026

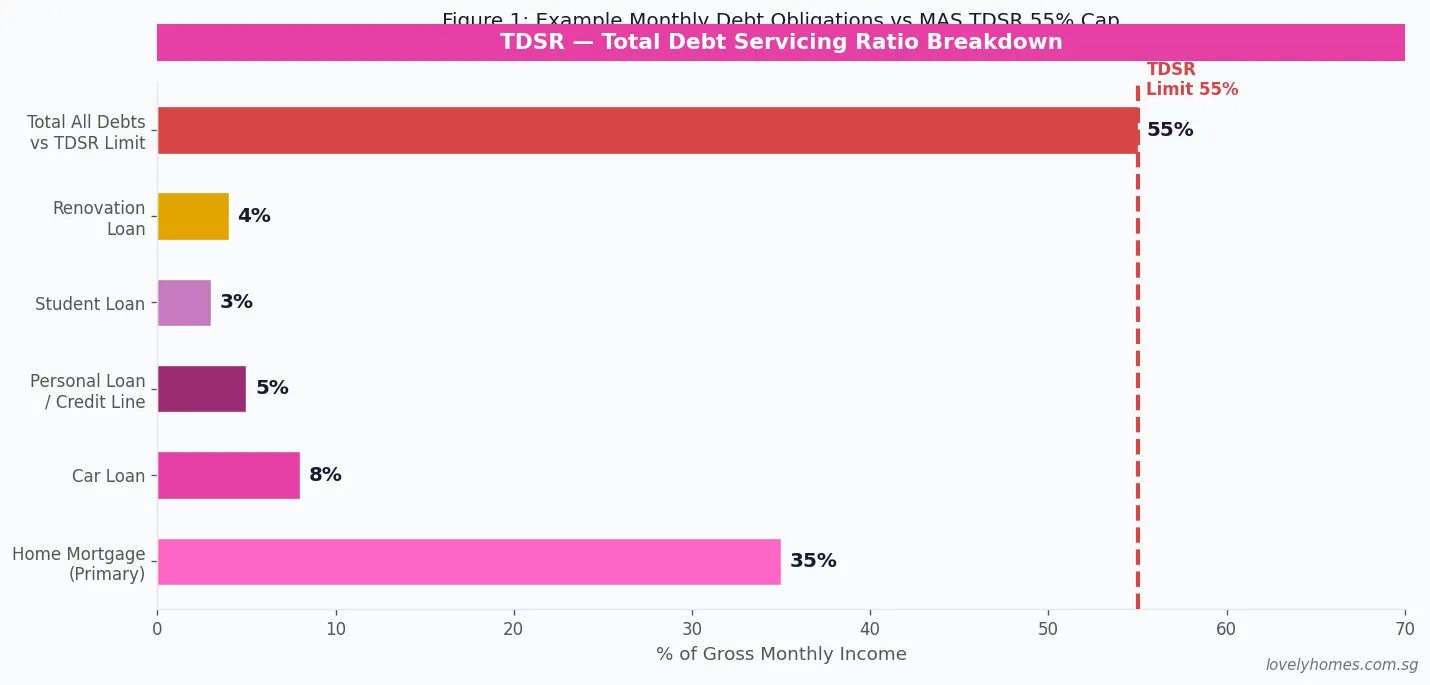

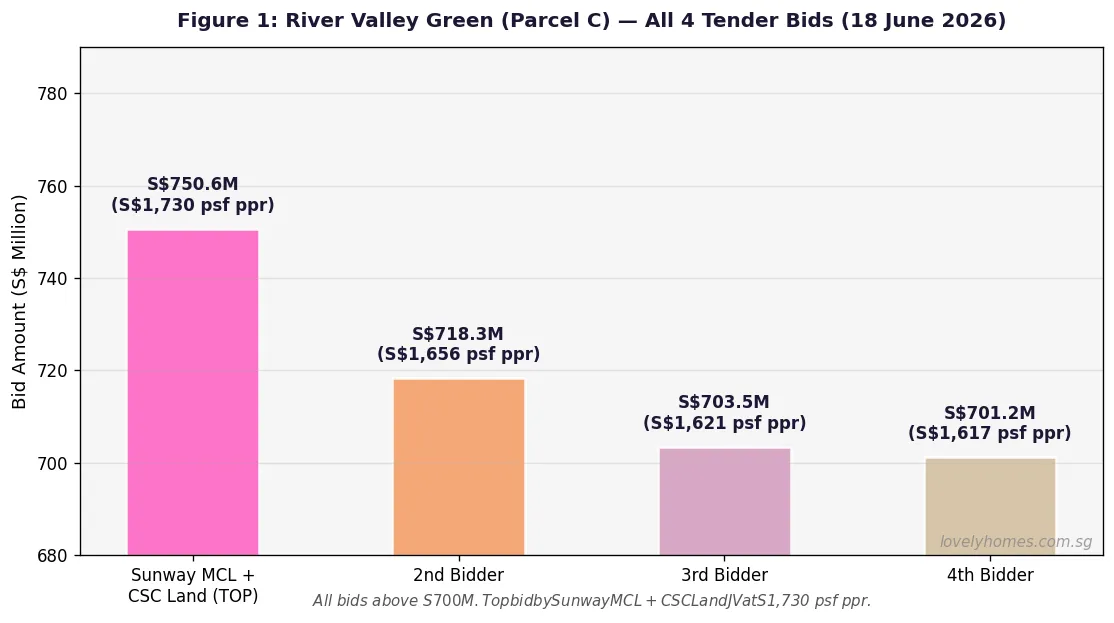

- Tender closed: 18 June 2026. The site received 4 bids, all above S$700 million — exceptional confidence from developers in the River Valley / District 9 market.

- Top bid: A joint venture between Sunway MCL and CSC Land Group submitted the highest bid of S$750.6 million at S$1,730 psf per plot ratio (ppr) — a new land rate record for the River Valley and Zion precinct.

- The site: 123,958 sq ft, Gross Plot Ratio 3.5, maximum GFA 433,854 sq ft, located steps from Great World MRT (Thomson-East Coast Line). Estimated yield: approximately 500 units.

- Expected development: Sunway MCL and CSC Land plan twin 36-storey residential towers. Formal URA award is pending; launch expected 2027–2028.

- Buyer implications: Higher land cost translates to higher new launch prices in the precinct — industry analysts project future launch prices of S$3,200–S$3,800 psf for this site.

River Valley Green Parcel C: The Last GLS Site in the Great World Precinct

The River Valley Green (Parcel C) Government Land Sales tender closed on 18 June 2026 at 12:00 noon, drawing four bids from established developers — all above S$700 million. The site is the final residential plot to be carved out of the River Valley Green precinct along River Valley Road, bookending a sequence of GLS sales that has transformed the stretch between Great World City and Zion Road.

URA launched the site in April 2026 as part of the 1H2026 GLS programme. At 123,958 sq ft with a GPR of 3.5, it can yield approximately 470–500 residential units. The site occupies a prime position within District 9 (CCR — Core Central Region), within a five-minute walk of Great World MRT Station on the Thomson-East Coast Line, and is flanked by the already-launched River Valley Green developments.

The Bids: A New Land Rate Benchmark for River Valley

| Bidder | Bid (S$ Million) | Land Rate (S$ psf ppr) | Premium vs 2nd Bid |

|---|---|---|---|

| Sunway MCL + CSC Land JV (Top Bidder) | S$750.6M | S$1,730 | +4.5% above 2nd |

| 2nd Bidder | ~S$718.3M | ~S$1,656 | — |

| 3rd Bidder | ~S$703.5M | ~S$1,621 | — |

| 4th Bidder | ~S$701.2M | ~S$1,617 | — |

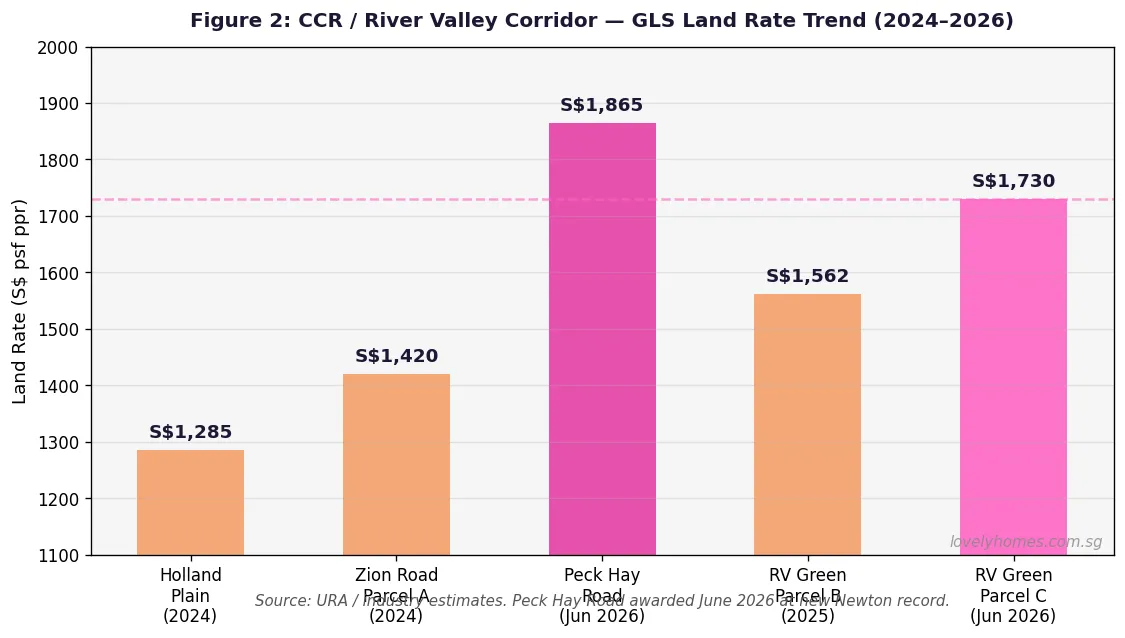

The tight clustering of bids — with only S$49.4M separating the top from the bottom bid, and all four above S$700M — reflects strong consensus among developers on the site’s land value. The top bid of S$1,730 psf ppr is approximately 22% higher than the land rate achieved at the most recent comparable River Valley Green tender, and sets a new benchmark for the Zion / River Valley precinct.

How This Compares to Recent CCR Land Sales

The S$1,730 psf ppr land rate also trails Peck Hay Road (awarded June 2026 at S$1,865 psf ppr — a new Newton precinct record), placing River Valley Green Parcel C firmly within the upper tier of Singapore’s CCR land market but not at the absolute frontier. The Peck Hay Road site, also in CCR District 11, attracted stronger bids due to its Newton / Cairnhill adjacency and higher-value catchment. The River Valley site, while slightly less premium in location, benefits from the Thomson-East Coast Line connectivity and the established Great World City mixed-use ecosystem.

In comparison, Zion Road Parcel A cleared at approximately S$1,420 psf ppr in 2024, meaning the Parcel C award represents land value appreciation of roughly 22% over that two-year period — consistent with the overall premium property price appreciation of 10–15% across the same period.

What Sunway MCL and CSC Land Plan for the Site

In a joint press release issued on 18 June 2026, Sunway MCL and CSC Land confirmed that if awarded the site, they intend to develop a 500-unit premium residential project comprising twin 36-storey towers. This is the second joint venture between the two developers following their collaboration on ELTA along Clementi Avenue 1 (501 units, launched February 2025). The developers did not disclose pricing but noted their commitment to delivering a premium product reflecting the site’s strategic location and land cost. Formal URA award is expected within weeks of the tender close; launch is anticipated in 2027 or early 2028 subject to planning approvals and construction commencement.

What This Means for Buyers in the River Valley / District 9 Market

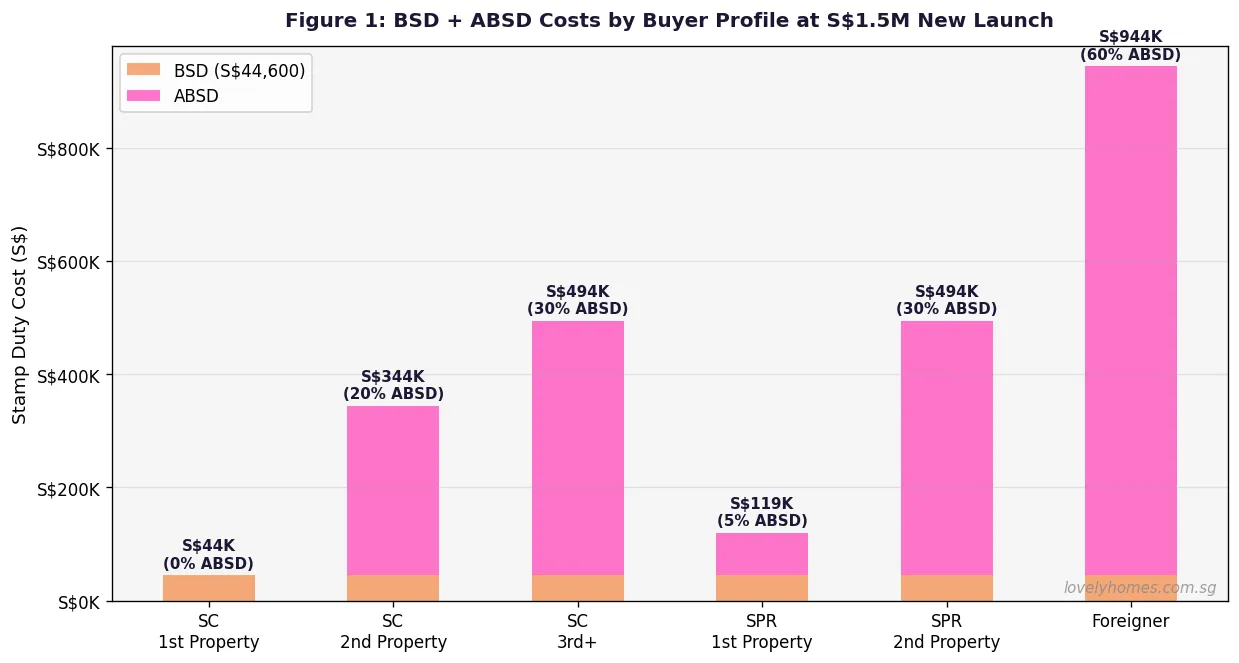

Higher land cost at GLS almost always translates into higher launch prices — developers need to recover land, construction, and holding costs, and build in a profit margin. With land at S$1,730 psf ppr and construction costs running at approximately S$600–S$800 psf, industry analysts project break-even prices around S$2,800–S$3,000 psf. A typical developer margin of 15–20% on a prime CCR product would place launch prices in the range of S$3,200–S$3,800 psf. For a 1,000 sq ft unit, that translates to S$3.2M–S$3.8M — firmly above the average SC first-property buyer’s budget, and targeted primarily at SC second-property buyers (20% ABSD), SPR buyers (5% ABSD for 1st property), and overseas purchasers who already pay 60% ABSD on any Singapore condo.

For existing owners in the River Valley, Zion Road, and Great World precinct, the strong GLS result is broadly positive — it reinforces the ceiling for comparable units in the secondary market and supports resale prices in the precinct.

Frequently Asked Questions: River Valley Green Parcel C GLS

What is a GLS tender and what happens next?

A Government Land Sales (GLS) tender is the process by which Singapore’s government — via the Urban Redevelopment Authority (URA) or HDB — sells public land to private developers for residential or mixed-use development. After the tender closes, URA evaluates all bids and formally awards the site, typically within two to four weeks. The developer then pays the accepted bid price, commences planning and design, applies for planning permission, and eventually launches the development for sale — a process that typically takes 18–36 months from GLS award to sales launch.

What does “psf ppr” mean and how does it relate to end prices?

“Per square foot per plot ratio” (psf ppr) is the standard unit for land pricing in Singapore GLS. It normalises land cost across sites of different sizes and densities. To estimate the impact on end unit prices: multiply the land rate (S$1,730) by the GPR (3.5) to get the land cost per square foot of gross floor area — approximately S$4,955 psf GFA. Add construction (S$600–S$800 psf), financing, and marketing costs, plus developer margin, to arrive at approximate launch prices of S$3,200–S$3,800 psf net sellable area.

When will this development launch for sale?

Based on the typical timeline from GLS award to sales launch, the development is expected to launch in 2027 or early 2028. The developers will need to obtain planning approval, finalise design, set up the showflat, and receive the Controller of Housing’s Sale Licence before selling any units. Singapore buyers who are interested should monitor URA’s new sales data and property portals for VIP preview announcements, which typically occur one to three months before the official launch.

Can foreigners buy units in this development?

Yes. Condominiums are open to all buyers including foreigners, subject to ABSD. Foreigners pay ABSD of 60% as at 2026, in addition to Buyer’s Stamp Duty. On a S$3.5M unit, a foreigner would pay BSD of approximately S$184,600 plus ABSD of S$2,100,000 — total stamp duty of S$2,284,600. The high ABSD rate introduced in April 2023 has substantially dampened foreign demand for Singapore condominiums, making CCR new launches now more dependent on Singapore Citizen and SPR buyers than in prior cycles.

Are there any upcoming GLS sites in the River Valley area?

Parcel C is the final GLS residential site in the River Valley Green precinct. The broader 2H2026 GLS programme includes sites in other growth corridors — Jurong Lake District, Tengah, and Bayshore — but no further River Valley or Zion Road residential plots have been announced. Any future supply in this precinct would be from redevelopment of private sites or collective sales (en bloc), which are individually negotiated and not part of the GLS programme. The next significant CCR GLS event to watch is the formal award of River Valley Green Parcel C by URA, expected in late June or early July 2026.