Singapore Foreign Buyer Property Guide 2026: ABSD 60%, Eligibility, Property Types and Stamp Duties Explained

Quick Answer: Buying Property in Singapore as a Foreigner

- ABSD rate: Foreigners (non-PR individuals) pay 60% Additional Buyer’s Stamp Duty on any residential property purchase — effective 27 April 2023.

- Entities (companies, trusts): Pay 65% ABSD on any residential purchase.

- FTA nationals (USA, Switzerland, Iceland, Liechtenstein, Norway): Treated as Singapore Citizens for ABSD purposes — 0% on first property, 20% on second.

- What foreigners can buy: Private condominiums, commercial shophouses, fully privatised Executive Condominiums (over 10 years old), and — with SLA approval — Sentosa Cove landed homes.

- What foreigners cannot buy: HDB flats (resale or BTO), Housing & Urban Development Company (HUDC) estates, or mainland landed property (bungalows, semi-Ds, terraces).

- BSD applies too: Buyer’s Stamp Duty at progressive rates from 1–6% is payable on top of ABSD.

- Bank financing: Foreign buyers can access Singapore bank loans; LTV cap is 75% on first property, repayment period up to 30 years, subject to TDSR 55%.

- Stamp duty deadline: Both BSD and ABSD must be paid within 14 days of signing the Option to Purchase (OTP) acceptance.

What Makes Singapore Property Law Distinct for Foreign Buyers?

Singapore occupies a rare position in global real estate: its private condominium market is freely accessible to foreign nationals, yet it surrounds that openness with some of the steepest entry costs in Asia. The centrepiece is the Additional Buyer’s Stamp Duty (ABSD), which since 27 April 2023 has stood at 60% for foreigners purchasing any residential property. On a S$2 million condominium, that translates to a stamp duty bill of more than S$1.2 million — before Buyer’s Stamp Duty (BSD) is even counted.

This guide explains, in plain terms, who qualifies as a foreigner under Singapore property law, what you can and cannot purchase, how ABSD and BSD are calculated, how bank financing works for non-residents, and what a realistic buying transaction looks like from OTP signing to key collection. All figures and rules reflect the position as at June 2026.

Governing legislation includes the Stamp Duties Act (Cap 312) administered by IRAS, the Residential Property Act (Cap 274) administered by the Singapore Land Authority (SLA), and the Housing and Development Act (Cap 129) administered by HDB.

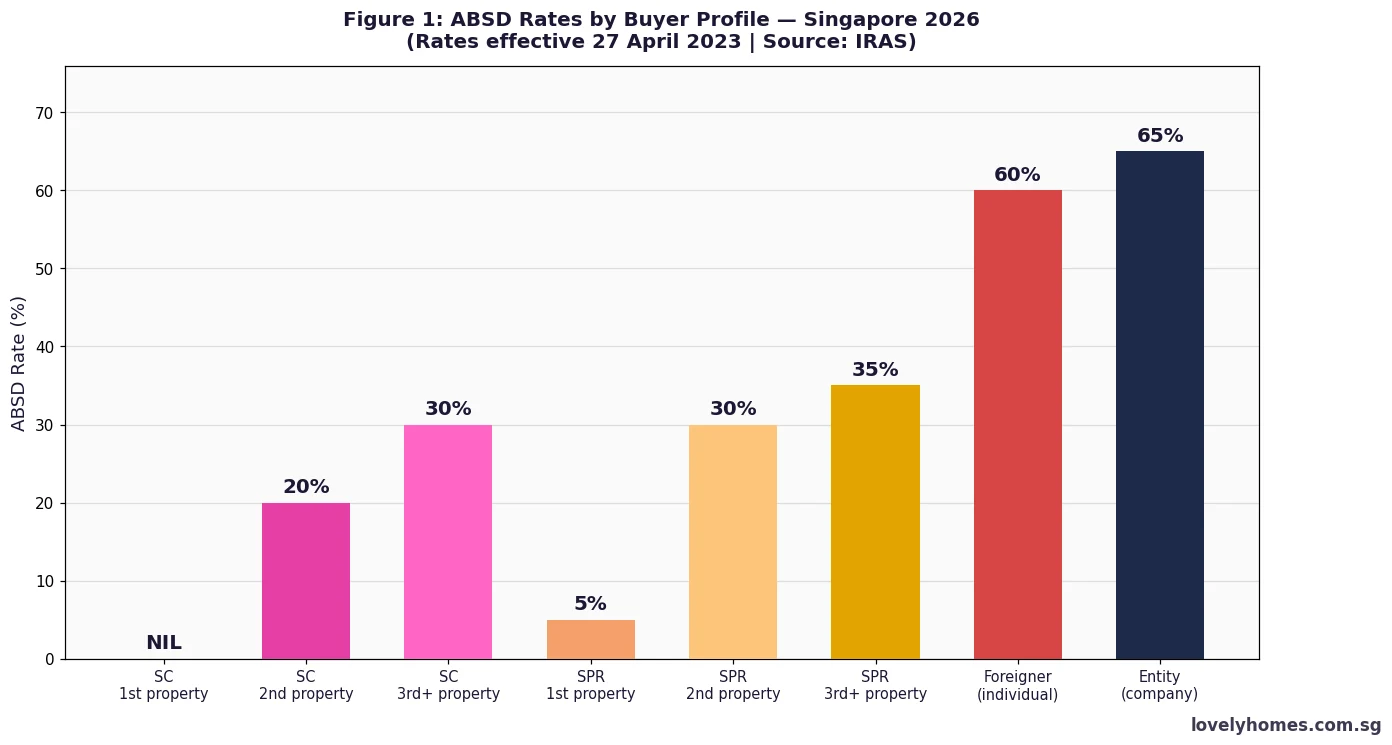

ABSD Rates for Foreign Buyers: 60% Since 27 April 2023

The ABSD is a tax layered on top of BSD whenever a residential property in Singapore is purchased. Rates are set by IRAS under the Stamp Duties Act and are tiered by the buyer’s residency status and how many residential properties they already own (globally, not just in Singapore).

Since the Government’s 27 April 2023 cooling-measure announcement, foreigners purchasing any Singapore residential property — regardless of whether it is their first or fifth — pay a flat 60% ABSD. Entities (companies, trusts) pay 65%.

Free Trade Agreement (FTA) Nationals: A Critical Exception

Citizens of a small number of countries are treated as Singapore Citizens for ABSD calculation purposes, by virtue of bilateral Free Trade Agreements. This means they pay 0% ABSD on their first residential property, 20% on the second, and 30% on the third and above — the same schedule as a Singapore Citizen. The qualifying nationalities are:

- United States nationals (US-Singapore FTA)

- Swiss nationals (Trans-Pacific Partnership / bilateral treaty)

- Nationals of Iceland, Liechtenstein, and Norway (Singapore-EFTA FTA)

Citizens of all other countries — including the United Kingdom, France, Germany, Australia, China, India, Japan, and Malaysia — pay the full 60% ABSD on any purchase. The Singapore-EU FTA does not extend to ABSD relief for EU nationals.

The FTA concession applies to the individual’s citizenship, not their work pass or residency status. A French national on an Employment Pass is not eligible; a Norwegian national on a Student’s Pass is.

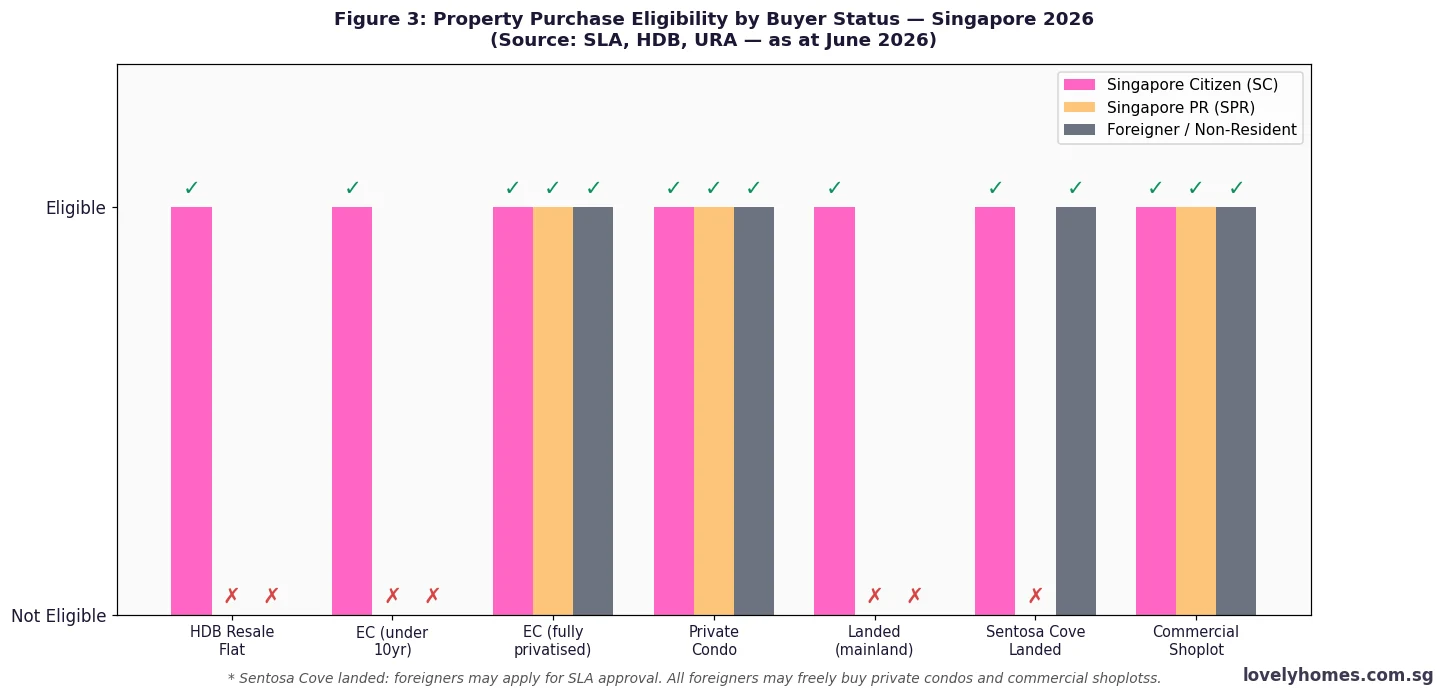

What Property Can Foreigners Buy in Singapore?

The Residential Property Act (Cap 274) is the key statute governing foreign purchases. Its restrictions apply to “restricted residential property” — essentially, low-rise residential land and housing. Strata-titled properties (condominiums, apartments) are generally unrestricted for foreign purchase. The practical breakdown is as follows:

Permitted: Private Condominiums and Apartments

Any private condominium or apartment (strata-titled, not landed) may be purchased freely by foreign nationals. This includes new launch units sold directly by developers, resale market units, and units in mixed-use developments with a residential component. There is no cap on the number of units a foreigner may own, no minimum value requirement, and no minimum holding period before resale — though the Seller’s Stamp Duty (SSD) regime imposes a financial penalty for sales within three years of purchase (12% in year one, 8% in year two, 4% in year three).

Permitted: Executive Condominiums (ECs) After Full Privatisation

ECs are a hybrid housing type built by private developers on government land with HDB subsidy. They are subject to a staged ownership opening: only eligible Singapore Citizens and PRs may purchase during the first five years; PRs may also purchase in the resale market from the sixth year. Foreign nationals may purchase an EC in the open resale market only after the full 10-year privatisation period, at which point the development is treated as a fully private condominium.

Permitted: Commercial Shophouses and Non-Residential Properties

Commercial and industrial properties — shophouses zoned for commercial or mixed commercial/residential use, office units, retail space, factory space — are generally purchasable by foreign nationals without the ABSD applicable to residential property. However, if the shophouse contains a residential component (for example, a “mixed” shophouse with living quarters on the upper floor), ABSD at the foreigner rate applies to the entire purchase price. Buyers should obtain a URA written permission confirmation before assuming a mixed-use property is exempt from ABSD.

Permitted (with SLA Approval): Sentosa Cove Landed Homes

Sentosa Cove is the only precinct in Singapore where foreigners may apply to purchase landed property. Applications go through the SLA’s Land Dealings Approval Unit (LDAU). Approval is not guaranteed, and conditions may be imposed. Even with SLA approval, the 60% ABSD still applies to the purchase. Sentosa Cove landed homes — primarily bungalows and strata-landed cluster housing — are among the most internationally traded properties in Singapore, with prices typically ranging from S$5 million to S$30 million and above.

Not Permitted: HDB Flats

HDB flats — both the Build-To-Order (BTO) primary market and the open resale market — are reserved exclusively for Singapore Citizens (and, in the resale market, for Singapore Permanent Residents and mixed-nationality couples involving at least one SC or SPR). Foreign nationals on any visa type cannot purchase an HDB flat, regardless of how long they have lived and worked in Singapore.

Not Permitted: Mainland Landed Residential Property

Bungalows (detached houses), semi-detached houses, terrace houses, and strata-landed housing on the Singapore mainland are restricted residential property under the Residential Property Act. Foreign nationals may not purchase these without special approval from the Minister for Law — approval that is rarely granted and typically limited to cases of exceptional economic contribution. This restriction applies irrespective of the buyer’s wealth, tenure in Singapore, or investment intentions.

Buyer’s Stamp Duty (BSD): Rates and Calculation

BSD is payable by every purchaser of Singapore property — residents and foreigners alike — and is calculated on the purchase price or market value, whichever is higher. The progressive BSD tiers as at June 2026 (revised 15 February 2023) are:

| Purchase Price Band | BSD Rate | Maximum Duty in Band |

|---|---|---|

| First S$180,000 | 1% | S$1,800 |

| Next S$180,000 (S$180k–S$360k) | 2% | S$3,600 |

| Next S$640,000 (S$360k–S$1.0M) | 3% | S$19,200 |

| Next S$500,000 (S$1.0M–S$1.5M) | 4% | S$20,000 |

| Next S$1,500,000 (S$1.5M–S$3.0M) | 5% | S$75,000 |

| Amount above S$3,000,000 | 6% | Uncapped |

BSD is administered by IRAS and must be paid within 14 days of signing the acceptance of the OTP (for private residential property) or the S&P Agreement. Payment is made via IRAS e-Stamping. Failure to pay on time attracts penalties of up to four times the stamp duty amount.

Bank Financing for Foreign Buyers: LTV, TDSR and Practical Limits

Foreign nationals may borrow from Singapore-licensed banks to finance a property purchase here. The key regulatory parameters are set by MAS (Monetary Authority of Singapore):

- LTV cap: 75% of purchase price or valuation (whichever is lower) for the first property loan. This falls to 45% for the second and 35% for the third and subsequent loans. Loan amounts above S$1.5 million may attract more conservative lender assessments.

- TDSR (Total Debt Servicing Ratio): Introduced by MAS in June 2013, TDSR limits total monthly debt obligations (including the proposed new loan) to 55% of gross monthly income. Lenders apply a stressed rate — typically 4.0% p.a. or the contractual rate, whichever is higher — when computing TDSR for variable-rate loans.

- CPF: Foreign nationals who are not Singapore PRs or citizens do not have CPF accounts and therefore cannot use CPF Ordinary Account funds for the down payment or monthly instalments. All costs must be funded from personal savings or foreign income.

- Minimum cash down payment: At least 5% of the purchase price must be paid in cash (not CPF). The remaining 20% of the 25% down payment (i.e., the amount not covered by the bank loan) may also be paid in cash.

In practice, a foreign buyer of a S$2 million condominium needs approximately S$500,000 in cash for the down payment alone — before accounting for stamp duties. This effectively means most foreigner purchasers in Singapore are self-funding the ABSD component entirely from liquid savings or overseas wealth.

Step-by-Step Buying Process for Foreign Purchasers

The transactional mechanics are the same as for any private property purchase in Singapore, with the additional stamp duty burden being the primary difference:

- Engage a Singapore-licensed solicitor: Choose a law firm experienced in foreign purchaser transactions. Confirm your ABSD status (FTA eligibility check).

- Obtain an In-Principle Approval (IPA) from a bank: Singapore banks lend to foreign nationals on Employment Passes or other long-term visas; some will lend to non-residents. IPA confirms your loan quantum and helps set your budget before you negotiate on price.

- Issue or accept the OTP: For new launches, developers issue the OTP automatically. For resale, the seller’s agent issues the OTP. You pay the option fee (typically 1% of purchase price) to secure the property.

- Exercise the OTP within 21 days: Pay the exercise price (typically 4% further deposit, making 5% total). At this stage the sale is legally binding.

- Pay BSD and ABSD within 14 days of OTP exercise: This is the single largest cash outflow for foreign buyers. Payment is through IRAS e-Stamping, and your solicitor handles the process.

- Complete the sale: Typically 8–12 weeks after OTP exercise for resale; or on the developer’s progressive payment schedule for new launches. For new launches, BSD and ABSD are typically stamped on the Sales & Purchase Agreement rather than the OTP.

- Register the transfer with SLA: Your solicitor lodges the instrument of transfer at the Singapore Land Authority. The Certificate of Title is issued upon completion.

Summary: Key Facts for Foreign Buyers at a Glance

| Parameter | Detail |

|---|---|

| ABSD rate (non-FTA foreigner) | 60% flat on all residential properties (effective 27 April 2023) |

| ABSD rate (entity/company) | 65% flat on all residential properties |

| FTA nationals (US, Swiss, EEA-3) | Same ABSD schedule as SC: 0% first, 20% second, 30% third+ |

| BSD | Progressive 1–6% on purchase price; applies to all buyers |

| ABSD + BSD deadline | 14 days from OTP acceptance or S&P Agreement date |

| LTV cap (first property) | 75% bank loan; no HDB loan available to foreigners |

| TDSR | 55% of gross monthly income (MAS, Jun 2013) |

| Minimum cash down payment | 5% cash + up to 20% cash/CPF; foreigners must fund all from cash |

| Properties foreigners may freely buy | Private condominiums, privatised ECs (10yr+), commercial property |

| Properties foreigners may NOT buy | HDB flats, ECs under 10 years, mainland landed property |

| Sentosa Cove landed | Purchasable with SLA/LDAU approval; ABSD still applies |

| SSD on resale within 3 years | 12% (yr 1), 8% (yr 2), 4% (yr 3) — applies to all buyers |

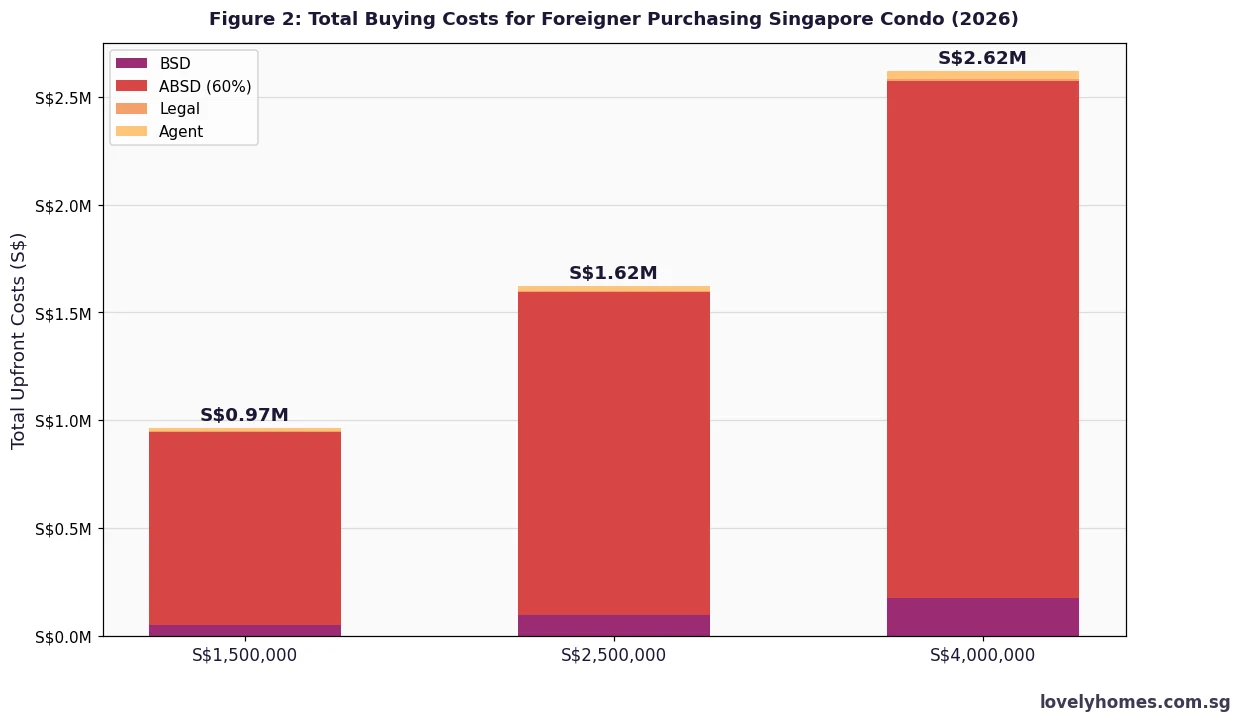

Worked Example: Mr & Mrs Laurent (French Nationals) — Purchasing a 2BR Condo at S$1,800,000

Profile: Mr Laurent (37) and Mrs Laurent (34), both French citizens on Employment Passes, joint gross income S$16,000/month. This is their first Singapore property purchase. They have S$1.8 million in savings and a S$350,000 CPF OA balance between them — however, as foreign nationals, CPF funds are not available for property purchase. All costs must be cash-funded.

Step 1 — BSD calculation on S$1,800,000:

- 1% × S$180,000 = S$1,800

- 2% × S$180,000 = S$3,600

- 3% × S$640,000 = S$19,200

- 4% × S$500,000 = S$20,000

- 5% × S$300,000 (S$1.5M–S$1.8M) = S$15,000

- Total BSD = S$59,600

Step 2 — ABSD calculation:

- French nationals are not FTA-eligible → 60% ABSD applies

- 60% × S$1,800,000 = S$1,080,000

Step 3 — Total stamp duties: S$59,600 + S$1,080,000 = S$1,139,600 (payable within 14 days of OTP exercise)

Step 4 — Bank loan and TDSR check:

- LTV 75%: loan = S$1,800,000 × 75% = S$1,350,000

- At 3.0% p.a. over 30 years: monthly instalment ≈ S$5,691

- TDSR = S$5,691 ÷ S$16,000 = 35.6% — PASS (below 55% threshold)

- Lender will stress-test at 4.0%: S$6,444/mth ÷ S$16,000 = 40.3% — PASS

Step 5 — Cash outlay summary:

| Item | Amount (S$) |

|---|---|

| 25% down payment (cash — no CPF) | S$450,000 |

| BSD | S$59,600 |

| ABSD (60%) | S$1,080,000 |

| Legal fees (est.) | S$4,000 |

| Agent commission (buyer side, 1%) | S$18,000 |

| Total cash required upfront | S$1,611,600 |

Note: The Laurents’ S$1.8M savings just covers the total cash outlay, leaving minimal liquidity. Most foreigner buyers at this price point fund the ABSD from offshore savings or liquidity events (asset sales, equity release elsewhere). A US national purchasing the same property would pay 0% ABSD (first property) — total stamp duty just S$59,600, cash upfront S$531,600: a S$1.08M difference.

Why Singapore Charges Foreigners 60% ABSD

Singapore’s property market is one of the most liquid and transparent in the world, and it serves as a preferred wealth-preservation vehicle for a globally mobile, high-net-worth demographic. The Government’s ABSD policy has three stated objectives: to maintain housing affordability for Singaporeans, to ensure a stable and sustainable property market, and to give priority to citizens in the accumulation of residential property assets. Deputy Prime Minister Lawrence Wong, speaking at the April 2023 cooling-measure announcement, described the 60% rate as necessary to prevent the market from being “driven by speculative demand from foreigners”.

The 2023 doubling (from 30% to 60%) had a tangible effect: foreign purchases as a share of total private residential transactions fell from approximately 4–5% in 2022 to around 1–2% in 2024–2025, according to URA caveats data. Despite this, transaction volumes in the luxury CCR (Core Central Region) segment — the typical market for foreign buyers — held firm, suggesting that high-net-worth foreign demand persists even at elevated ABSD levels, though the typical buyer profile has shifted towards those with the most compelling reasons to own Singapore property rather than those treating it as a convenient investment.

Peer-Country Comparison: How Singapore’s Foreign Buyer Policy Stacks Up

Singapore is not unique in restricting or taxing foreign property buyers, but its approach is among the most explicit globally. Australia charges foreign nationals an application fee plus a vacant residential land tax surcharge, and state-level duties in Victoria and New South Wales include foreign purchaser surcharges of 8% and 9% respectively — steep, but still well below Singapore’s 60%. New Zealand outright bans most foreigners from purchasing existing residential property. Canada introduced a two-year ban on foreign residential purchases in 2023. Hong Kong imposes a 15% New Residential Stamp Duty on foreign buyers. Against this backdrop, Singapore’s 60% rate stands out as a revenue-generating deterrent rather than a blanket prohibition, allowing the market to remain open in principle while pricing out all but the most committed foreign purchasers.

What Might Come Next for Foreign Buyer Policy?

This section represents editorial speculation and should not be relied upon for investment decisions. The 60% ABSD rate was set deliberately high, and the Government has indicated that any easing would be considered only if the market has “clearly stabilised”. As at June 2026, private residential prices continue to edge upward — URA’s Q1 2026 Private Residential Property Index rose 2.1% quarter-on-quarter — suggesting there is no near-term pressure on policymakers to reduce the foreign buyer burden.

Some market observers speculate that the Government might introduce a tiered ABSD regime that distinguishes between Singapore Permanent Residents who have been granted PR for over five years (and who contribute economically) and genuinely non-resident foreign investors. Others have suggested that the FTA concession framework could be extended to additional trading partners as Singapore negotiates further bilateral agreements. For now, however, the policy landscape appears settled: 60% ABSD for foreigners, 65% for entities, with FTA relief remaining narrowly targeted.

Frequently Asked Questions

Can a foreigner buy an HDB flat if they are married to a Singapore Citizen?

A foreign national married to a Singapore Citizen (SC) may purchase an HDB flat under the Public Scheme, provided the SC is the primary applicant and the couple meets HDB’s income ceiling (S$14,000/month for standard resale and BTO flats). The foreign national does not count as an SC or SPR, so the household eligibility depends entirely on the SC spouse’s status. The couple would not be eligible for the Enhanced CPF Housing Grant (EHG) if the foreign national has income, and must meet all other HDB eligibility criteria. Under the Citizen-Foreigner Public Scheme, the foreigner spouse is listed as a non-owner occupier, and the SC spouse must bear full ownership. Upon purchasing an HDB flat under this scheme, the SC spouse is treated as owning a first HDB — future HDB or private purchases will be subject to the usual MOP and ABSD implications for the SC owner.

Do Free Trade Agreement (FTA) nationals pay zero ABSD on their first Singapore property?

Yes — qualifying FTA nationals (US, Swiss, Icelandic, Liechtenstein, Norwegian citizens) are treated as Singapore Citizens for ABSD purposes. They pay 0% ABSD on their first residential property, 20% on the second, and 30% on the third and subsequent properties. This does not exempt them from Buyer’s Stamp Duty (BSD), which applies to all purchasers. The FTA concession is tied to citizenship, not to work-pass status, length of stay, or tax residency. A US citizen on an EP purchasing their first Singapore condo pays 0% ABSD; a UK citizen on an EP pays 60%. To claim the concession, the buyer’s solicitor submits proof of citizenship at the IRAS e-Stamping portal when paying stamp duty.

Can foreigners use a Singapore company to buy residential property and save ABSD?

No — and attempting this will result in a higher ABSD bill. Entities (including companies, trusts, and other legal persons) pay a flat 65% ABSD on any residential property purchase, five percentage points higher than the individual foreigner rate of 60%. Singapore’s ABSD framework was specifically designed to close corporate-vehicle loopholes. IRAS also has anti-avoidance provisions in the Stamp Duties Act that allow it to look through arrangements where the substance of the transaction is a residential property purchase, even if structured differently. There is no ABSD exemption for residential properties held through corporate vehicles, except for licensed housing developers who qualify for the conditional remission regime (which requires the developer to complete and sell all units within a prescribed period).

What is the Seller’s Stamp Duty (SSD) and does it apply to foreigners?

SSD is a tax on the seller of a residential property, payable if the property is sold within three years of purchase. The rates are 12% of the sale price or market value (year one), 8% (year two), and 4% (year three). SSD applies to all sellers in Singapore regardless of nationality — there is no foreigner exemption or additional rate. SSD is intended to deter short-term speculation. For a foreigner who buys a S$2 million condominium and sells it 18 months later, the SSD would be 8% × S$2 million = S$160,000, on top of the 60% ABSD they paid on entry. Given these dual costs, most foreigner buyers approach Singapore property as a medium-to-long-term holding rather than a short-term trade.

Can foreigners on a Tourist Pass or Short-Term Visit Pass buy Singapore property?

Yes — there is no requirement to hold a work pass or long-term visa in order to purchase Singapore private residential property. The transaction is governed by the Residential Property Act and the Stamp Duties Act, and the buyer’s immigration status does not affect eligibility to purchase a private condominium. However, practical considerations apply: Singapore banks will not extend a mortgage to someone with no Singapore income or no long-term visa, so cash purchasers are typically the only buyers in this category. Additionally, non-residents purchasing property may be subject to home-country tax reporting and capital controls depending on their jurisdiction of domicile.

Are there minimum income or minimum stay requirements to buy a Singapore condo as a foreigner?

There are no minimum income or minimum stay requirements to purchase a private condominium in Singapore as a foreign national. The Singapore property market does not operate an investors’ visa scheme that ties property purchase to immigration status. Foreign nationals do not receive any immigration benefit from purchasing property here. However, as noted above, if you wish to finance the purchase with a Singapore bank mortgage, you will need to demonstrate sufficient income and financial standing to satisfy the bank’s credit assessment and MAS’s TDSR requirements. Without a Singapore income, banks may require evidence of overseas income, asset statements, or a guarantor.

What happens to ABSD if a foreigner later becomes a Singapore Permanent Resident (SPR)?

ABSD is levied at the point of purchase and is assessed based on the buyer’s status at the time of signing the OTP or S&P Agreement. If a foreign national purchases a property paying 60% ABSD and subsequently becomes an SPR, there is no refund of the excess ABSD already paid. The change in residency status only affects future purchases: as an SPR, any subsequent residential property purchase would attract ABSD at SPR rates (5% on first property, 30% on second). There is also an ABSD refund mechanism for married couples involving a Singapore Citizen, where the couple initially pays ABSD on a second property and then sells the first within six months — but this remission scheme does not apply to foreigners paying the 60% rate on a first purchase.

Disclaimer: This article is intended for general informational purposes only and does not constitute legal, financial, or taxation advice. ABSD rates, BSD tiers, LTV ratios, and property ownership rules are subject to change by the Government at any time. The information in this article reflects the position as at June 2026. Before making any property transaction, readers should consult a Singapore-licensed solicitor, a Monetary Authority of Singapore (MAS)-licensed financial adviser, and the relevant government authorities including IRAS (iras.gov.sg), HDB (hdb.gov.sg), SLA (sla.gov.sg), and URA (ura.gov.sg). LovelyHomes does not accept liability for any loss arising from reliance on information in this article.