Singapore Stamp Duty Complete Guide 2026: BSD, ABSD, SSD and ACD Explained

Singapore stamp duty is not a single tax — it is a suite of four distinct levies that can collectively add hundreds of thousands of dollars to the cost of a property transaction. Understanding each one, when it applies, and how to calculate it is essential before you sign any Option to Purchase. This guide covers all four: Buyer’s Stamp Duty (BSD), Additional Buyer’s Stamp Duty (ABSD), Seller’s Stamp Duty (SSD), and Additional Conveyance Duty (ACD).

All figures are current as at 31 May 2026. For the authoritative position, always refer to the IRAS Stamp Duty page and consult a licensed conveyancing lawyer before transacting.

- BSD — payable by EVERY buyer on every property purchase. Progressive rates 1%–6%.

- ABSD — additional levy on top of BSD. Singapore Citizens pay 0% on their first property, 20% on their second, 30% on their third+. PRs pay 5%/30%/35%. Foreigners pay 60% on any residential property.

- SSD — payable by the SELLER if the property is sold within 3 years of purchase. Rates: 12% (Year 1), 8% (Year 2), 4% (Year 3), nil thereafter.

- ACD — applies when residential property is transferred indirectly through corporate equity. Flat 33% on the residential property value component.

- BSD and ABSD are payable within 14 days of the Option to Purchase (OTP) or Sale & Purchase Agreement.

- SSD is payable within 14 days of the sale contract.

- CPF cannot be used to pay stamp duty at the point of purchase — you must pay in cash first, then apply for CPF reimbursement.

- ABSD remission is available to Singapore Citizen couples replacing their matrimonial home — subject to conditions and strict timelines.

What Is Stamp Duty and Why Does Singapore Use It?

Stamp duty is a transaction tax levied on documents that effect the transfer of a property or shares in a property-holding entity. In Singapore, the Inland Revenue Authority of Singapore (IRAS) administers all stamp duties under the Stamp Duties Act (Cap. 312). The modern stamp duty regime serves two purposes: raising revenue, and acting as a macro-prudential tool to moderate speculative demand in the residential property market.

When you buy a residential property, you will encounter BSD and possibly ABSD. When you sell, SSD may apply if you sell too quickly. If a property changes hands through an equity transfer in a company, ACD enters the picture. Each levy has its own trigger, its own rate schedule, and its own payment deadline.

Buyer’s Stamp Duty (BSD) — the Baseline Tax Every Buyer Pays

BSD is the foundational property transaction tax. Every buyer — regardless of citizenship, residency status, or how many properties they already own — pays BSD on every property purchase. It is computed on the higher of the purchase price or the market value of the property at the time of acquisition.

The rates are progressive for residential property:

| Purchase Price / Market Value | BSD Rate | Max BSD from This Tier |

|---|---|---|

| First S$180,000 | 1% | S$1,800 |

| Next S$180,000 | 2% | S$3,600 |

| Next S$640,000 | 3% | S$19,200 |

| Next S$500,000 | 4% | S$20,000 |

| Next S$1,500,000 | 5% | S$75,000 |

| Above S$3,000,000 | 6% | No cap |

A separate, flat-rate BSD schedule applies to non-residential property (commercial, industrial): 1% on the first S$180,000, 2% on the next S$180,000, and 3% on the remainder — capped at 3%. The progressive residential schedule shown above took effect for instruments executed on or after 15 February 2023, when the 5% and 6% tiers were introduced for high-value transactions.

Worked example (BSD only, S$1.5M residential condo):

First S$180,000 × 1% = S$1,800

Next S$180,000 × 2% = S$3,600

Next S$640,000 × 3% = S$19,200

Next S$500,000 × 4% = S$20,000

Total BSD = S$44,600

BSD is a fixed cost — there is no way to reduce it lawfully short of negotiating a lower purchase price. It is also not remissible (there are no BSD remission schemes for residential buyers equivalent to the ABSD remission).

Additional Buyer’s Stamp Duty (ABSD) — the Policy Lever

ABSD was introduced in December 2011 and has been raised five times since, most recently in April 2023. It is the single largest upfront cost for most second-property buyers and foreigners. ABSD is levied on top of BSD, at a flat rate on the entire purchase price.

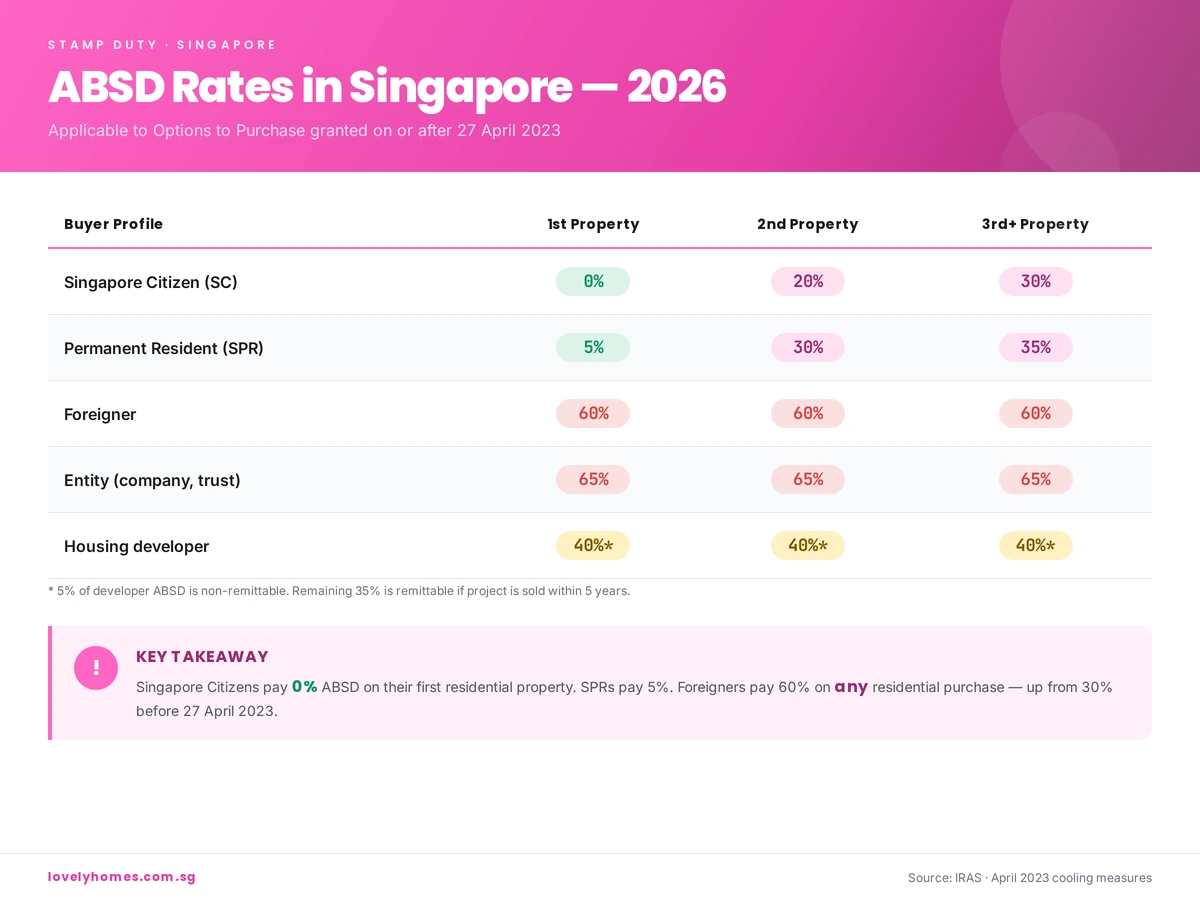

The current ABSD rate schedule (applicable to instruments executed on or after 27 April 2023) is:

| Buyer Profile | 1st Property | 2nd Property | 3rd & Subsequent |

|---|---|---|---|

| Singapore Citizen (SC) | 0% | 20% | 30% |

| Singapore Permanent Resident (SPR) | 5% | 30% | 35% |

| Foreigner (individual) | 60% | 60% | 60% |

| Entity (company, trustee) | 65% | 65% | 65% |

| Housing developer | 40%* | 40%* | 40%* |

* 5% of the developer ABSD is non-remittable. The remaining 35% is remittable upon completing the project and selling all units within 5 years.

FTA nationals — citizens of Iceland, Liechtenstein, Norway, Switzerland, and the United States — are accorded Singapore Citizen ABSD treatment under the respective Free Trade Agreements.

For a detailed breakdown of ABSD remission schemes (including the Married Couple Remission for upgraders), see our ABSD Complete Guide 2026.

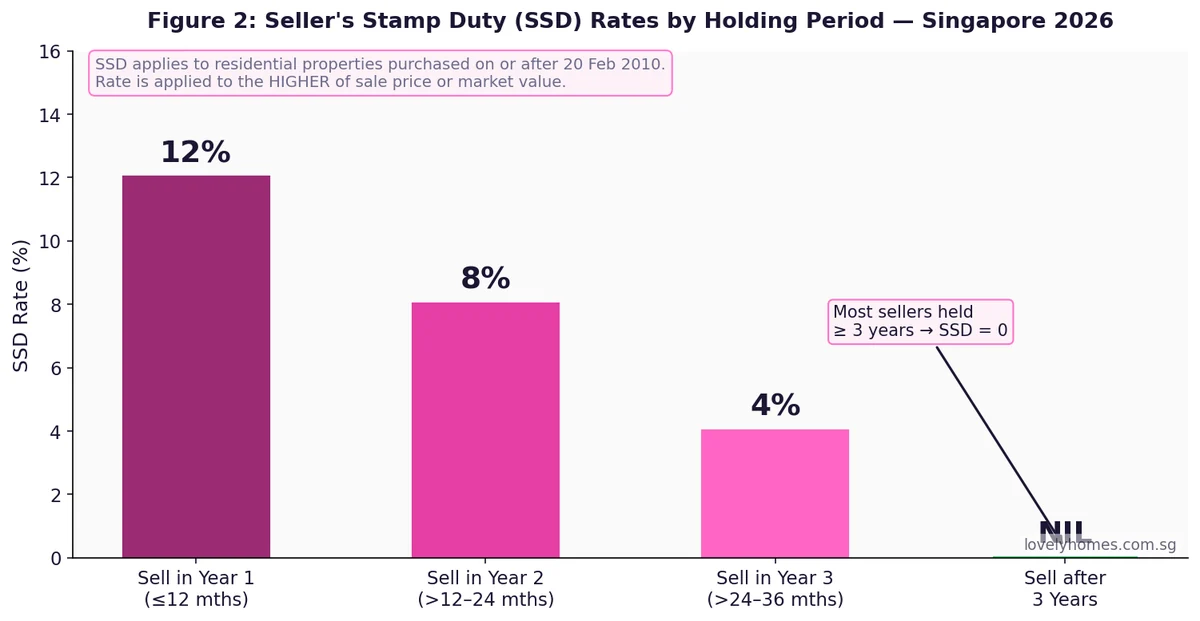

Seller’s Stamp Duty (SSD) — the Anti-Flipping Tax

SSD was introduced in February 2010 to discourage short-term residential property speculation. It is paid by the seller (not the buyer) when a residential property is disposed of within three years of its acquisition. The rate depends on how quickly the seller flips the property:

SSD is calculated on the higher of the sale price or the market value at the time of disposal. The holding period is measured from the date of purchase (execution of the Sale & Purchase Agreement) to the date of sale (execution of the disposal S&P). SSD does not apply to properties acquired before 20 February 2010, nor does it apply to commercial or industrial property.

Note: If you inherit a property and subsequently sell it, the SSD holding period runs from the original purchase date (the date the deceased acquired the property), not from the date of inheritance. This is a common source of confusion. If a parent bought a condo in 2024 and passed away in 2025, and the heir sells in early 2026, SSD at 8% could still apply.

The SSD is the reason most investor-buyers hold Singapore residential property for at least three years before selling. In practice, the combination of SSD and the time needed to recover transaction costs (BSD + ABSD + legal fees + agent commissions) means the effective minimum hold for a profitable flip is typically four to five years.

Additional Conveyance Duty (ACD) — the Entity Transfer Tax

ACD was introduced in May 2017 to close a loophole that allowed buyers to acquire residential property held in companies without paying ABSD — by buying shares in the company rather than the property directly. Under the ACD regime, a transfer of equity interests in a residential-property-holding entity is taxed as if it were a direct property acquisition.

ACD applies when:

- The acquirer obtains a significant ownership interest (≥50%) in an entity (company, trust, or partnership);

- That entity holds Singapore residential property as its primary asset; and

- The residential property component exceeds a de minimis threshold.

The ACD rate is 33% on the residential property value component, levied on top of the existing stamp duty on the share transfer (which is normally 0.2%). For a $10 million residential property held in a company, an ACD transaction could trigger an additional $3.3 million in duty — making it broadly equivalent in cost to a direct ABSD transaction.

ACD is highly specialised and typically arises in commercial real estate transactions, family wealth restructuring, or en-bloc-related scenarios. Most individual residential buyers will never encounter it. If you are structuring a transaction that involves acquiring shares in a company that holds Singapore residential property, engage a tax adviser with stamp-duty expertise before proceeding.

Summary: All Four Singapore Stamp Duties at a Glance

| Duty | Who Pays | When It Applies | Rate (Residential) | Deadline |

|---|---|---|---|---|

| BSD | Buyer | All property purchases | 1%–6% progressive | 14 days from OTP/S&P |

| ABSD | Buyer | 2nd+ property / foreigner / entity | 0%–65% flat on full price | 14 days from OTP/S&P |

| SSD | Seller | Sold within 3 years of purchase | 4%–12% flat on full price | 14 days from disposal S&P |

| ACD | Acquirer of equity | ≥50% stake in residential-property entity | 33% on resi property value | 14 days from share transfer |

Comprehensive Worked Example: SC Couple Upgrading from HDB to Private Condo

Mr & Mrs Pang are Singapore Citizens. They own a Bishan 5-room HDB flat (purchased 2018, fully paid under CPF). They want to buy a S$2,000,000 2-bedroom freehold condo in District 10 and sell the HDB afterwards. Here is the full stamp duty picture:

Scenario A: Buy the condo BEFORE selling the HDB

Because they still own the HDB, the condo is their second residential property. ABSD at 20% is triggered.

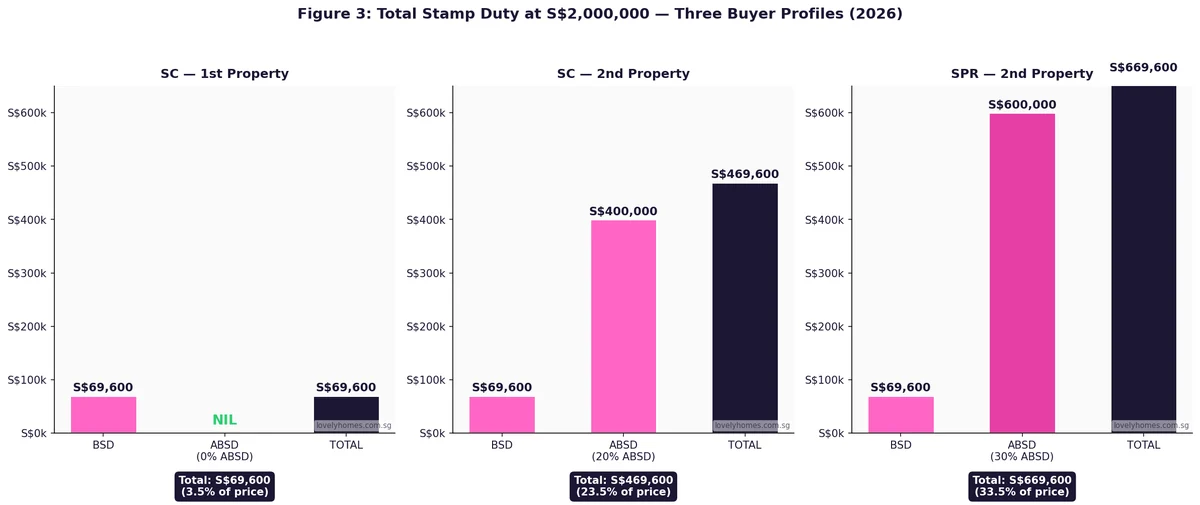

- BSD on S$2,000,000: S$64,600

- ABSD (20%): S$400,000

- Total stamp duty: S$464,600

- However, they can apply for the ABSD Married Couple Remission — they get the S$400,000 back if they sell the HDB within 6 months of the later of (a) the condo’s purchase date or (b) its TOP date.

- They must pay the ABSD upfront in cash and wait for the refund.

Scenario B: Sell the HDB FIRST, then buy the condo

After selling the HDB, they hold zero residential properties. The condo becomes their first residential property. Zero ABSD.

- BSD on S$2,000,000: S$64,600

- ABSD: S$0

- Total stamp duty: S$64,600

Scenario B saves the Pangs S$400,000 and avoids the need for the remission application. The trade-off is the risk of not finding a new home before the HDB sale completes — and potentially needing temporary accommodation in the interim. Many upgrading couples use a bridging loan to manage this gap.

When Does Stamp Duty Really Matter? — Why These Numbers Are So Significant

Stamp duty in Singapore is, by international standards, among the highest in the world for non-citizen buyers. A foreign individual purchasing a S$3 million residential property in 2026 faces: BSD of approximately S$119,600 plus ABSD of S$1,800,000 — a total of S$1,919,600, or 64% of the purchase price. This is intentional: the Government has consistently stated that Singapore’s residential property market is primarily for Singaporeans to live in, and the ABSD is the mechanism that enforces that policy goal.

For Singapore Citizens, the numbers are far more manageable — but still significant. A first-time buyer at S$2 million pays S$64,600 in BSD alone. For an upgrader buying their second property at the same price, adding S$400,000 in ABSD transforms what might otherwise be a healthy financial decision into a transaction that requires either substantial cash reserves or careful sequencing via the remission route.

Stamp duty also has a secondary effect on the property market as a whole: it creates a minimum holding period incentive. Investors who pay BSD and ABSD on entry need their property to appreciate by at least those amounts — plus legal costs, agent commissions, and financing costs — before they break even on a sale. This structurally discourages short-term speculation and was a deliberate part of the policy design when rates were raised in 2021 and 2023.

What Might Change in 2026 and Beyond?

This section is speculative analysis, not official policy.

As at May 2026, there has been no signal from the Ministry of Finance or MAS of imminent changes to the stamp duty regime. Private residential prices rose 0.9% in Q1 2026 — a moderate pace that does not, on its own, suggest further tightening is imminent. The Government has traditionally intervened when quarterly price growth exceeds 2–3% or when transaction volumes indicate re-entry of speculative buyers.

Watch for the following triggers that could lead to a review: (1) sustained quarter-on-quarter private price growth above 2% for two or more consecutive quarters; (2) a significant rise in foreign buyer transactions as a proportion of total; (3) a global interest rate environment that makes Singapore dollar assets more attractive to offshore capital. Conversely, a sharp economic slowdown could prompt targeted relief — as was done in 2020 with the COVID-19 stamp-duty deferral scheme.

Frequently Asked Questions

Can I use my CPF to pay stamp duty?

No, not at the point of payment. BSD and ABSD (and SSD for sellers) must be paid in cash by the statutory deadline. After the duty has been stamped and paid, you may apply to withdraw from your CPF Ordinary Account to reimburse the cash outlay, provided the property qualifies under CPF Board rules and you have sufficient OA balance. The CPF withdrawal is a reimbursement step, not a direct payment channel.

Does SSD apply if I sell because of financial hardship?

There are no hardship exemptions to SSD built into the Stamp Duties Act. SSD is triggered automatically on any disposal within 3 years of purchase, regardless of the reason for sale. IRAS has no general discretion to waive SSD except in the specific circumstances defined in the Act (e.g. compulsory acquisition by the state). If you are facing distress and need to sell within the SSD window, factor the SSD cost into your net sale proceeds before deciding.

My spouse is a foreigner. Do we pay 60% ABSD on our first home together?

For a jointly-owned first matrimonial home where one owner is a Singapore Citizen and the other is a foreigner, the couple can apply for ABSD remission to be taxed at the SC rate (0% on a first property). The remission is available for a property that will be used as the couple’s matrimonial home, and conditions must be met. The ABSD is still payable upfront at the foreigner rate; the remission is applied for thereafter. Engage a conveyancing lawyer well before the OTP is exercised to ensure the remission application is properly structured.

Is stamp duty payable on a property gift (transfer without payment)?

Yes. BSD (and ABSD where applicable) is computed on the market value of the property at the time of transfer, even if no money changes hands. A parent transferring a private condo to an adult child as a gift is treated as a purchase at market value for stamp duty purposes. The child is treated as the buyer and must pay BSD and ABSD based on their own buyer profile and existing property count.

How is stamp duty calculated for an uncompleted property (new launch)?

For an uncompleted unit bought directly from the developer, the stamp duty is computed on the purchase price stated in the Sale & Purchase Agreement (which is executed at the point of booking the unit). ABSD — where applicable — is payable within 14 days of the S&P execution, which means the full ABSD amount is due upfront even though the project may not complete for several years. The Married Couple Remission window (6 months to sell the existing property) runs from the later of the S&P date or the Temporary Occupation Permit (TOP) date.

Does stamp duty apply to HDB flat purchases?

Yes. BSD applies to all HDB flat purchases (new BTO and resale) at the same progressive rates as private residential property. For new BTO flats, BSD is computed on the selling price set by HDB; for resale, it is on the higher of the resale price or HDB’s valuation. ABSD also applies to HDB flat purchases under the same rules — although Singapore Citizen first-time buyers pay 0% ABSD, meaning only BSD is due. SPR first-time buyers face 5% ABSD even on an HDB flat purchase.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty (BSD) Singapore 2026: How It Is Calculated

- CPF Property Withdrawal Limits 2026: OA Valuation Limit and Accrued Interest Explained

- Singapore Bridging Loan Guide 2026: How to Bridge the Gap Between Selling and Buying

- Singapore Property Inheritance Guide 2026: Wills, CPF Nominations and Stamp Duty

- Singapore Property Cooling Measures Timeline 2009–2026

- Singapore Property Upgrader Guide: HDB to Condo Sequencing and ABSD Planning

Disclaimer: This article is for general informational purposes only and does not constitute legal, tax, or financial advice. Stamp duty rates and remission rules may change. Always verify the current position with the IRAS Stamp Duty page and the Ministry of Finance. Consult a licensed conveyancing lawyer or tax specialist before transacting.