HDB Minimum Occupation Period (MOP) Singapore 2026: Complete Guide

📌 Quick Answer: HDB Minimum Occupation Period (MOP) 2026

- The MOP is the mandatory period you must live in your HDB flat before you are allowed to sell it on the open market or buy a private residential property.

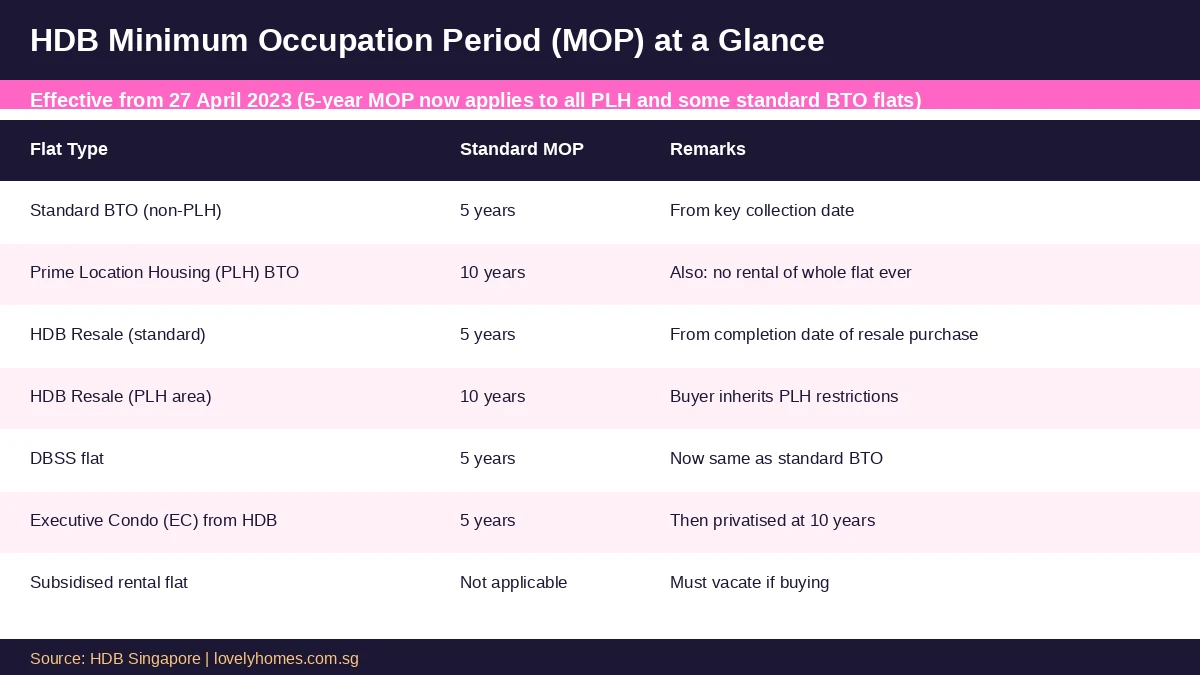

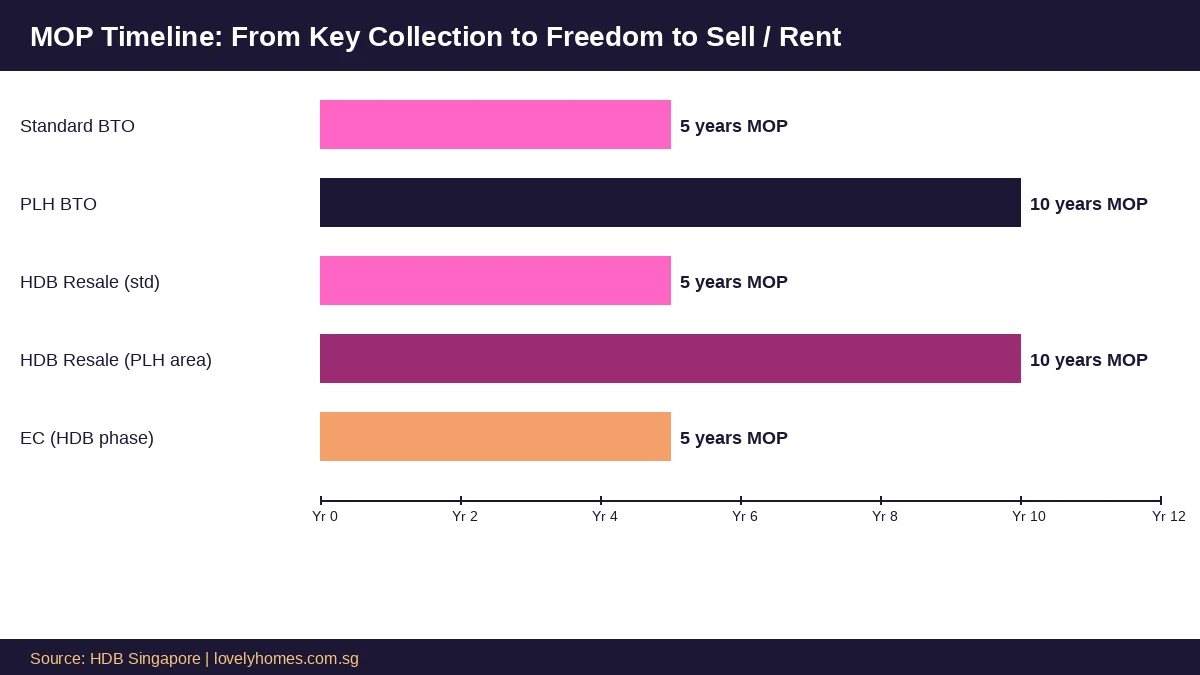

- Standard BTO and resale flats carry a 5-year MOP, counted from the date you collect your keys (for BTO) or the date the resale transaction is completed.

- Prime Location Housing (PLH) flats — introduced in October 2021 — carry a 10-year MOP and come with a permanent ban on renting out the whole flat.

- During MOP you cannot sell the flat on the open market, rent out the entire flat, or purchase a private residential property without first disposing of the HDB flat.

- Renting out individual rooms is permitted during MOP with HDB’s approval, provided occupancy caps are met.

- Executive Condominiums (ECs) have a 5-year MOP under HDB rules; they become fully privatised at the 10-year mark.

- Violation consequences include compulsory acquisition at below-market value, grant clawback, and debarment from future HDB applications.

- The MOP applies to the flat, not the owner: any attempt to sell before expiry is void and attracts penalties.

What Is the HDB Minimum Occupation Period (MOP)?

The Minimum Occupation Period — universally known as MOP in Singapore property circles — is a Housing & Development Board (HDB) policy requiring flat owners to physically occupy their flat for a stipulated number of years before they are permitted to sell, rent the entire unit, or purchase a private residential property. The MOP is administered under the Housing and Development Act and is one of the most consequential rules shaping the Singapore HDB resale market.

HDB introduced the MOP to prevent speculative “flipping” of subsidised public housing. Because the government provides substantial grants and subsidies when selling BTO flats, it wants genuine owner-occupiers to benefit from those subsidies rather than investors who might resell immediately for a quick profit. The MOP therefore acts as a temporal lock-in that aligns the interests of flat buyers with the public-housing mission of HDB.

The standard MOP has stood at five years since 2010. However, the introduction of the Prime Location Housing (PLH) model in October 2021 created a new, more restrictive 10-year MOP for BTO projects in central and highly sought-after locations. Understanding which MOP category applies to your flat — and what you are and are not permitted to do during that period — is critical before making any property decision.

How Is the MOP Counted?

The MOP clock starts differently depending on how you acquired the flat. For a BTO flat, the MOP begins on the date of key collection, which HDB formally records. If you collect your keys on 15 January 2022, your 5-year MOP expires on 15 January 2027. For a resale HDB flat, the MOP begins on the date the resale transaction is legally completed — that is, the date shown on the HDB resale completion letter, typically 8–12 weeks after HDB accepts the resale application. DBSS flats follow the same rule as resale. For an EC bought from an HDB-appointed developer, the MOP starts from the date of vacant possession (VP) and lasts five years, after which the EC becomes partially privatised and fully private at the 10-year mark.

Importantly, the MOP measures calendar time, not duration of active occupation. Even if you are posted overseas for work and your flat sits empty for part of the period, the clock does not pause. You must also maintain the flat as your sole registered address in Singapore during the MOP; abandoning the flat to stay elsewhere while the clock runs is a violation that HDB actively monitors through its inspection programme.

MOP by Flat Type — 2026 Reference Table

| Flat Type | MOP Duration | Whole-flat Rental After MOP? | Key Rule |

|---|---|---|---|

| Standard BTO (non-PLH) | 5 years from key collection | Yes, with HDB approval | Flat must be primary residence during MOP |

| Prime Location Housing (PLH) BTO | 10 years from key collection | No — permanently prohibited | Introduced Oct 2021; applies to centrally located BTO projects |

| HDB Resale (standard area) | 5 years from completion | Yes, with HDB approval | Buyer’s MOP starts from resale completion date |

| HDB Resale (PLH-designated area) | 10 years from completion | No — permanently prohibited | PLH restriction travels with the address, not the seller |

| DBSS flat | 5 years | Yes, with HDB approval | Treated the same as standard BTO for MOP purposes |

| Executive Condo (EC) | 5 years (HDB rules apply) | Yes, after MOP + HDB approval | Fully private at 10 years; no HDB restrictions thereafter |

What Can You Do During the MOP?

Many flat owners are surprised to discover that the MOP is not a blanket prohibition on all activity — it targets sale and whole-flat rental specifically. Renting out spare bedrooms is permitted: HDB allows flat owners to sublet individual rooms, subject to occupancy caps and prior HDB approval via the resale portal. The total number of occupants including owners must not exceed the flat’s authorised occupancy limit — six persons for a 3-room flat, eight for larger flats as of 2026. Running a small home-based business under HDB’s Home-Based Small Scale Business guidelines is also permitted and does not affect the MOP. Internal renovations are allowed subject to HDB’s renovation guidelines and town council rules.

What is prohibited is more significant. You cannot sell the flat on the open market — any purported contract of sale during MOP is void. You cannot rent out the entire flat for standard flats during MOP, and for PLH flats this prohibition is permanent. You cannot purchase a private residential property in Singapore while an HDB flat is under MOP; if you do, HDB will require you to dispose of the HDB flat within six months and may impose financial penalties. Voluntary ownership transfers to family members are generally not permitted during MOP without HDB’s prior approval, which is granted only in specific circumstances such as divorce, death, or financial hardship.

Worked Example: The Lim Family’s MOP Journey

👥 Scenario: Lim Family, 4-Room BTO in Tampines

Key collection date: 15 March 2021

MOP expiry date: 15 March 2026 (5-year standard MOP)

Goal in early 2026: Sell the flat and upgrade to a private condo.

- From 15 March 2026, the Lims are free to list the flat on the open market via the HDB resale portal.

- They may simultaneously exercise an OTP (Option to Purchase) on a private condo. If they buy the condo before completing the HDB sale, a 6-month disposal window applies.

- Had they bought the condo in January 2026 — before MOP expiry — HDB would have required them to sell the flat within 6 months and could have imposed a financial penalty.

- CPF Family Grant: Received at BTO purchase; not subject to clawback on MOP completion. A Resale Levy of S$50,000 applies if they later purchase another subsidised flat.

- They had also rented out two spare bedrooms since October 2022 (with HDB approval), earning approximately S$1,800 per month — a permitted activity during MOP.

The PLH Model and the 10-Year MOP

The Prime Location Housing (PLH) model was launched by HDB in October 2021 to address public concern that prime-location BTO flats — particularly in districts such as Rochor and the Central Area — were underpriced relative to private property. The two key additional restrictions of the PLH model are the 10-year MOP and the permanent ban on renting out the whole flat.

For buyers of PLH BTO flats, this means the flat cannot be sold until 10 full years from key collection. Even after those 10 years, the whole-flat rental prohibition is perpetual — it is address-based and permanent, running with the flat and not the owner. A resale buyer who purchases a PLH-designated flat on the open market inherits the same restriction; there is no way to clear it by buying second-hand. Individual rooms may still be sublet with HDB approval.

The Ministry of National Development (MND) has indicated that the PLH model will be applied selectively. Research from industry analysts suggests that PLH resale transactions — when they eventually enter the market after 2031 for the earliest PLH BTO projects — may be priced at a discount to non-PLH flats of equivalent size and location, precisely because of the rental prohibition narrowing the buyer pool.

Consequences of Violating the MOP

| Violation | HDB Action | Additional Consequence |

|---|---|---|

| Selling flat before MOP expires | Void transaction; possible compulsory acquisition at below-market value | Debarment from future HDB flat purchases for up to 5 years |

| Renting out whole flat during MOP | Fine of S$3,000–S$5,000; instruction to terminate tenancy immediately | Repeat offence may result in compulsory acquisition |

| Buying private property during MOP without disposing of HDB flat | 6-month disposal notice issued by HDB | Financial penalty; potential stamp duty complications |

| Giving false occupation declaration | Civil and/or criminal prosecution under the Housing and Development Act | Fines up to S$5,000 or imprisonment up to 6 months |

What Happens After the MOP?

Once your MOP expires, you gain substantially greater freedom. You may list the flat for sale via the HDB resale portal; the price is negotiated freely between buyer and seller with no government-set ceiling. Standard flat owners may apply to HDB for permission to sublet the entire unit, typically approved for 6–36 months under the Fair Tenancy Framework. You may also purchase a private property concurrently with your HDB flat — note that Additional Buyer’s Stamp Duty at 20% applies to Singapore Citizens buying a second residential property. Married couples may also explore decoupling one partner’s name off the HDB flat to facilitate a private property purchase by the other partner at a lower ABSD rate, subject to eligibility.

What the MOP Means for Singapore’s Property Market

The MOP is one of the most effective supply-management tools in Singapore’s housing policy toolkit. By locking new BTO supply out of the resale market for five years, HDB ensures that subsidised flat sales benefit genuine first-time owner-occupiers rather than investors arbitraging the gap between discounted BTO prices and open-market resale values. The MOP also creates a predictable “event horizon” in the resale market: estates where BTO keys were collected in large numbers five years ago tend to see a surge of resale supply as those MOP clocks expire. Estates where keys were collected in 2020 and 2021 — including Tengah, Tampines North, and Canberra — will see their 5-year MOPs rolling off through 2025 and 2026, contributing to resale supply in those towns. Buyers looking for competitively priced resale flats would do well to track upcoming MOP expiry clusters using HDB’s transaction data on the HDB website and URA transaction records.

🔮 Looking Ahead: Will the MOP Change?

The 5-year standard MOP has remained stable since 2010, and the government has consistently defended it as appropriately calibrated. The 10-year PLH MOP is newer (effective from 2021) and will only be stress-tested when the first PLH BTO projects complete their wait and owners begin to sell from 2031 onwards. Should PLH resale prices still show large profits despite the longer lock-in, policymakers may consider extending the PLH MOP further or broadening the PLH classification. Conversely, if PLH proves to dampen demand and leads to undersubscribed BTO launches in prime locations, the criteria may be moderated. These are speculative projections — official policy remains as described above.

Frequently Asked Questions

Can I buy a private property while my HDB flat is under MOP?

No. Purchasing a private residential property in Singapore while your HDB flat is under MOP is prohibited. If you exercise an OTP on a private property before your MOP expires, HDB will issue a notice requiring you to dispose of the HDB flat within six months. Failure to comply can result in financial penalties and debarment from future HDB applications. The practical approach is to wait for the MOP to expire, then purchase the private property. You may co-own both thereafter, though the second-property ABSD of 20% (for Singapore Citizens) will apply to the private purchase.

Does the MOP restart if I add a family member to my flat?

No. Adding an authorised occupier or essential occupier to your flat does not reset the MOP clock. The MOP runs from your original key collection date (for BTO) or resale completion date and continues uninterrupted regardless of changes in the list of occupants. If you are seeking to transfer ownership — for example, adding a spouse as co-owner — HDB’s approval is required and may be subject to conditions, but an approved ownership change does not affect the MOP count.

Can I rent out my whole flat after MOP if it is a PLH flat?

No. The prohibition on renting out the entire flat is a permanent condition attached to all Prime Location Housing designated flats. It applies regardless of whether the flat has completed the 10-year MOP. Once a flat is designated PLH — determined by the BTO project it belongs to or, for resale flats, by the address being in a PLH-designated estate — the whole-flat rental ban is perpetual. You may still rent out individual rooms with HDB’s prior approval, subject to occupancy cap rules. If rental income is important to your long-term plan, verify whether any flat you are considering carries PLH status before committing.

What happens to my CPF housing grant if I sell before MOP?

Selling your HDB flat before the MOP expires is prohibited and any purported sale is void. Were HDB to compulsorily acquire the flat due to a MOP violation, CPF housing grants received would be subject to clawback — amounts deducted from the proceeds, returned to your CPF Ordinary Account, and you would face an additional financial penalty. Beyond the clawback, you would be debarred from purchasing an HDB flat or EC for up to five years. Attempting to circumvent the MOP is both illegal and financially destructive.

Can I sell my flat on the very day my MOP expires?

Yes. On the expiry date, you may submit a resale application via the HDB resale portal. In practice, most owners arrange a buyer in advance through private negotiation and grant the OTP a few days before the MOP date, with the actual HDB resale application submitted on or after the expiry date. Check with your conveyancing solicitor on precise timing — HDB’s position is that the resale application must be submitted after the MOP, though the OTP can be arranged a few days ahead.

How does the MOP interact with divorce proceedings?

If a couple holding an HDB flat divorces during the MOP, the Family Justice Courts of Singapore may make orders relating to the flat — including ordering a sale or transfer to one party — notwithstanding the MOP. HDB has an established process for court-ordered transfers that may occur before MOP expiry, handled case-by-case and requiring a court order before HDB will process the transfer. HDB does not automatically waive the MOP on divorce, but a court’s order can effectively override HDB’s normal MOP restriction for the purpose of the divorce settlement. Legal advice from a family law solicitor is strongly recommended.

What is the MOP for an EC bought on the resale market?

If you buy an EC on the resale market (i.e., after it has been privatised), there is no HDB MOP applicable to you as the buyer — the EC is already a private property. HDB rules only apply during the first 10 years of an EC’s life from the date of TOP (Temporary Occupation Permit). If you buy an EC that is, say, 12 years old on the resale market, you are buying a fully private condominium and the transaction is governed by standard private property rules, including ABSD if applicable.

Related Articles

- HDB BTO Application Guide 2026: How to Apply, Ballot and Select Your Flat

- Singapore HDB Resale Guide 2026: Buying a Resale Flat Step-by-Step

- Singapore Executive Condo (EC) Complete Guide 2026

- Singapore Property Decoupling Guide 2026: How to Decouple and Save ABSD

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- HDB Upgrading Guide 2026: From HDB to Condo — Everything You Need to Know

- CPF Property Withdrawal Limits Singapore 2026: How Much Can You Use?

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or professional advice. HDB rules and policies are subject to change; always verify current requirements directly with the Housing & Development Board, the Inland Revenue Authority of Singapore, or your legal and financial advisers before making any property decision. LovelyHomes does not accept responsibility for reliance on information in this article.