HDB Housing Grants Singapore 2026: Complete Guide to EHG, Family Grant and PHG

ℹ Quick Answer: Singapore HDB Housing Grants 2026

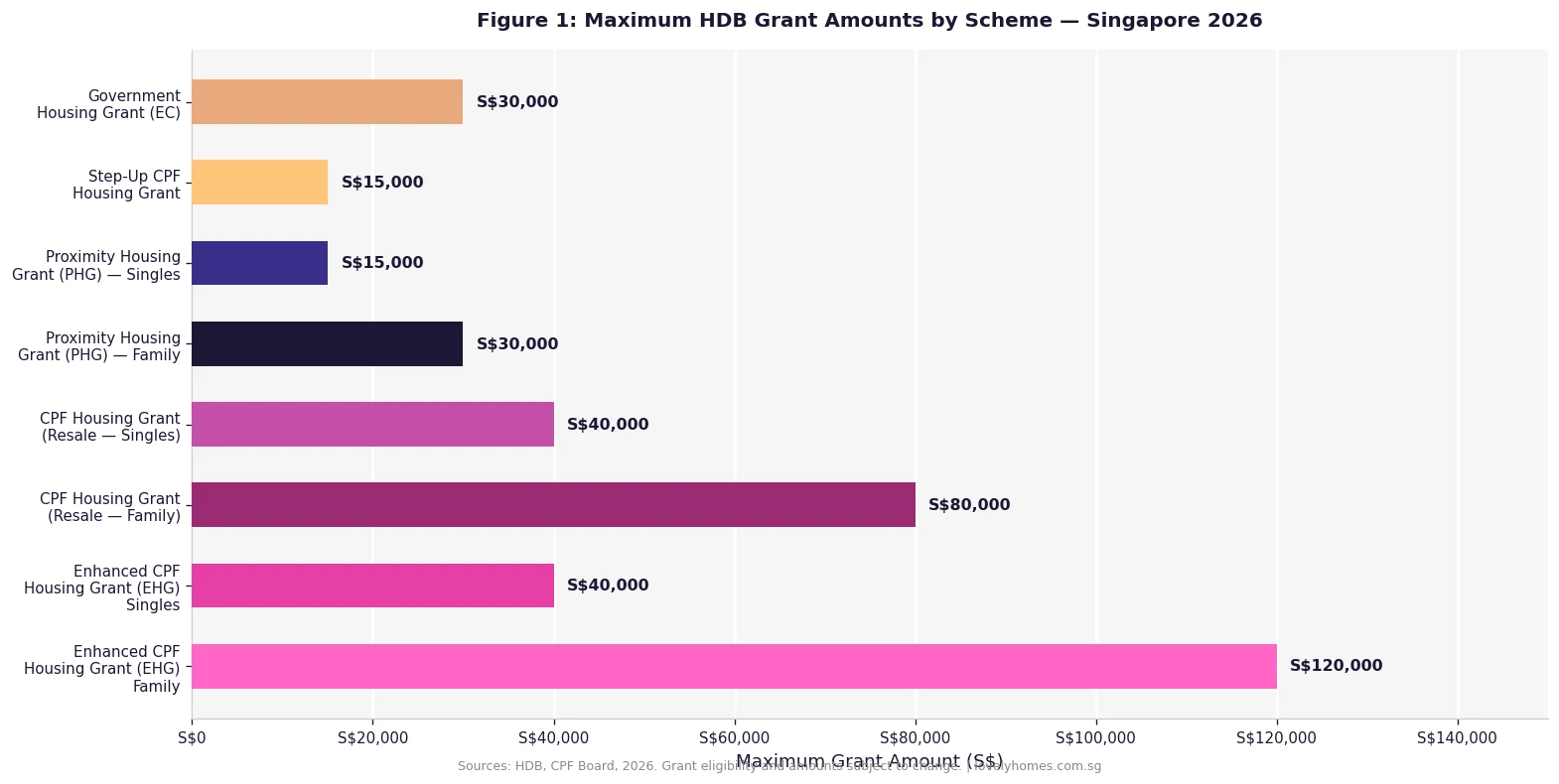

- Largest grant available: Up to S$160,000 for eligible Singapore Citizen couples buying an HDB resale flat (EHG S$80K + Family Grant S$50K + PHG S$30K).

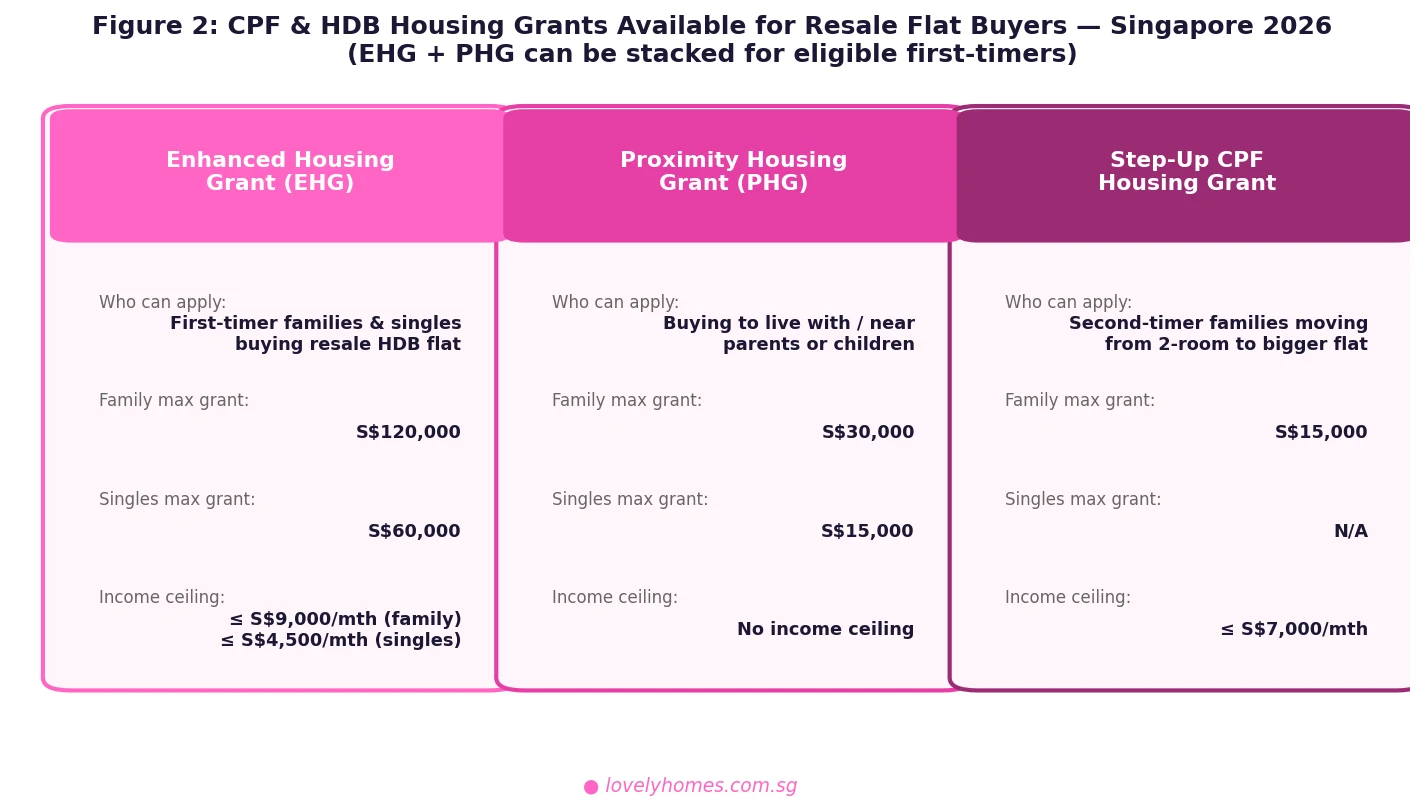

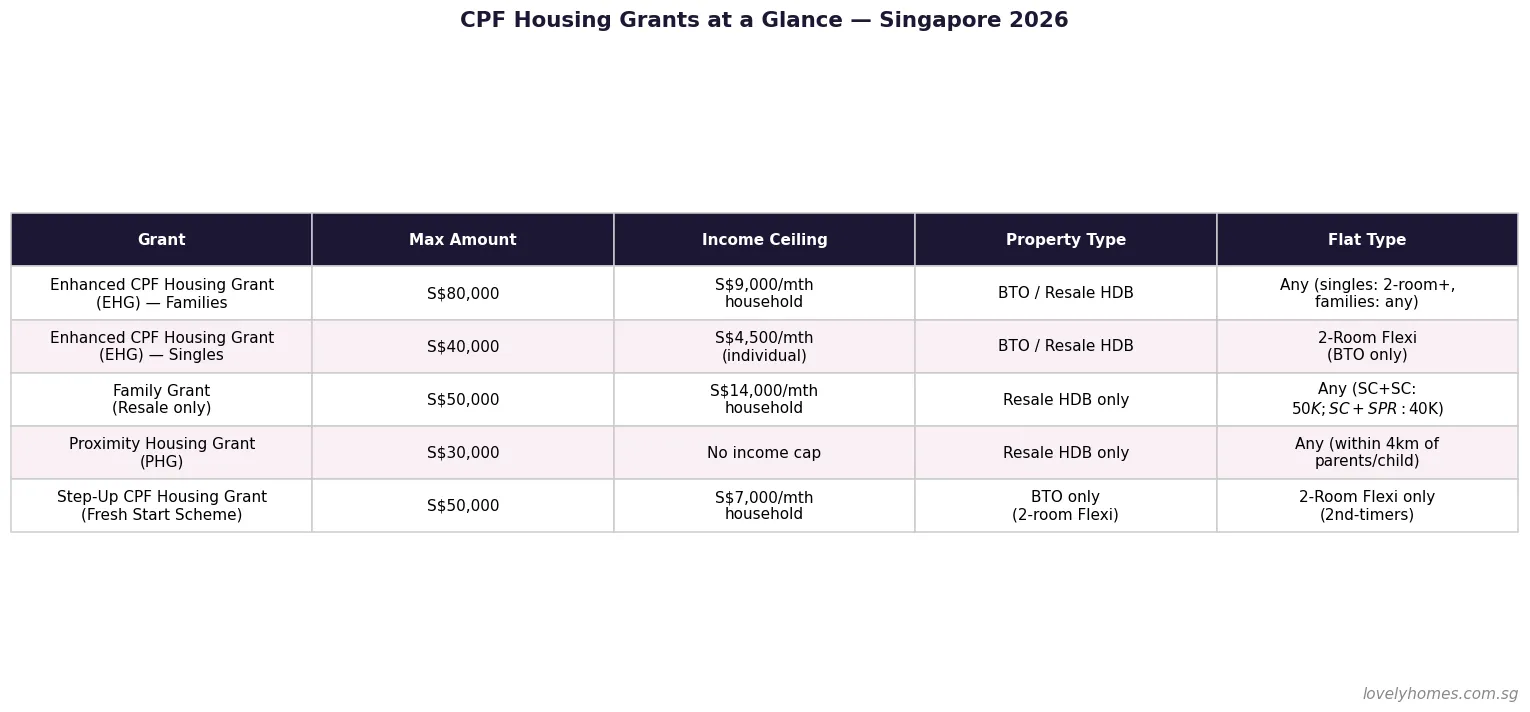

- EHG (Enhanced CPF Housing Grant): Up to S$80,000; income ceiling S$9,000/mth for couples; covers BTO and resale; granted by HDB, paid from CPF.

- Family Grant: Up to S$50,000 for SC+SC couples buying resale; S$30,000 for SC+SPR couples.

- Singles Grant: Up to S$25,000 for unmarried/divorced Singapore Citizens aged 35 and above buying resale.

- Proximity Housing Grant (PHG): S$30,000 if you buy within 4 km of your parents or children; S$10,000 if you buy to co-reside.

- CPF Housing Grant for ECs: S$30,000 Family Grant available for eligible SC couples buying an Executive Condominium (EC); income ceiling S$16,000/mth.

- You cannot double-count: EHG and Family Grant are added together, but you must meet both eligibility criteria separately. Grants are disbursed into your CPF Ordinary Account and reduce your outstanding loan accordingly.

- Effective date: All figures reflect the grant amounts in force as at 15 July 2026; check HDB’s website before committing.

What Are CPF Housing Grants, and Who Administers Them?

CPF Housing Grants are cash-equivalent subsidies administered by the Housing & Development Board (HDB) on behalf of the Singapore government. Unlike rebates that appear on your invoice, these grants are credited directly into your CPF Ordinary Account (OA) and applied to reduce the amount you need to borrow or pay out of pocket. They represent one of the most significant levers in Singapore’s housing affordability framework, enabling first-timer households to reduce the effective purchase price of an HDB flat by tens of thousands of dollars.

Since their introduction alongside the BTO scheme, CPF Housing Grants have been restructured multiple times. The landmark 2019 reform merged the Additional CPF Housing Grant (AHG) and Special CPF Housing Grant (SHG) into the single Enhanced CPF Housing Grant (EHG), covering incomes up to S$9,000 per month. A further expansion in 2023 raised the Family Grant cap for resale flats and extended PHG coverage. As of 2026, the framework comprises four distinct grants — EHG, Family Grant, Singles Grant, and PHG — which can be combined subject to eligibility.

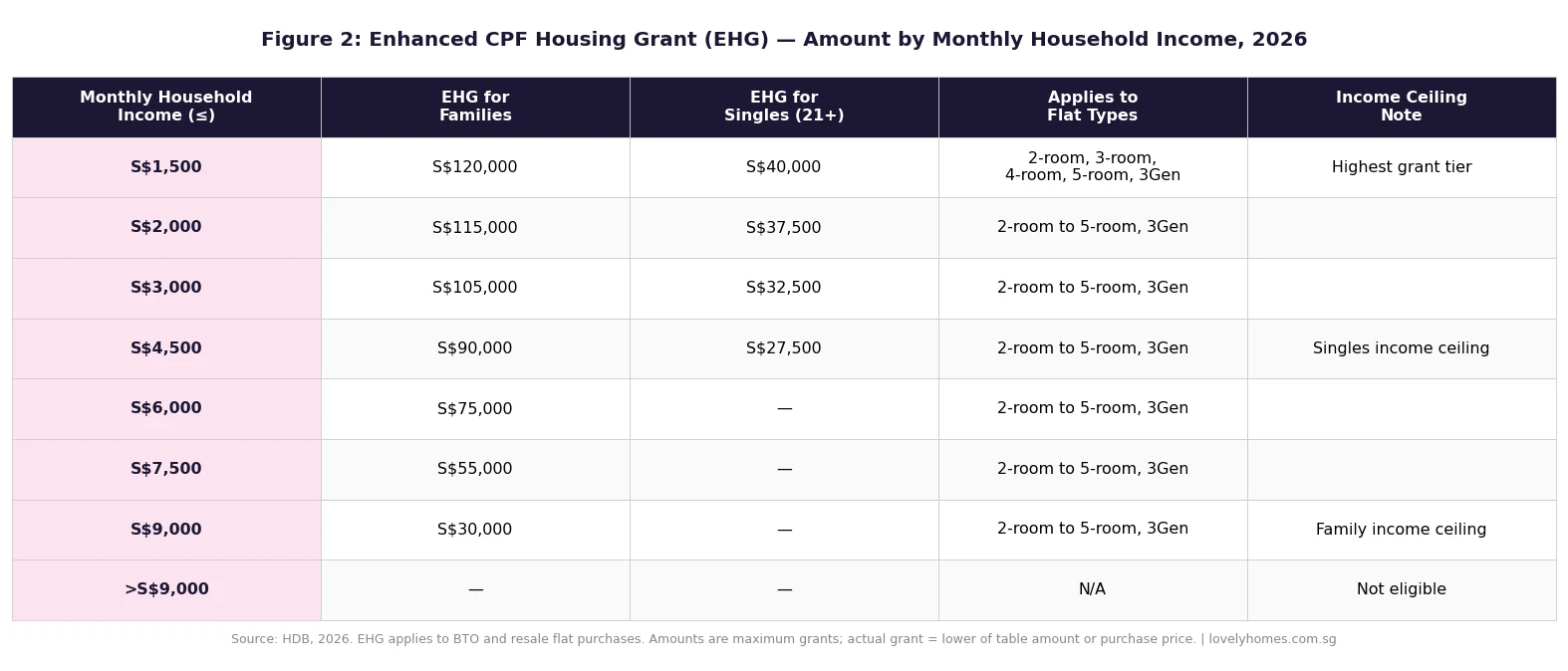

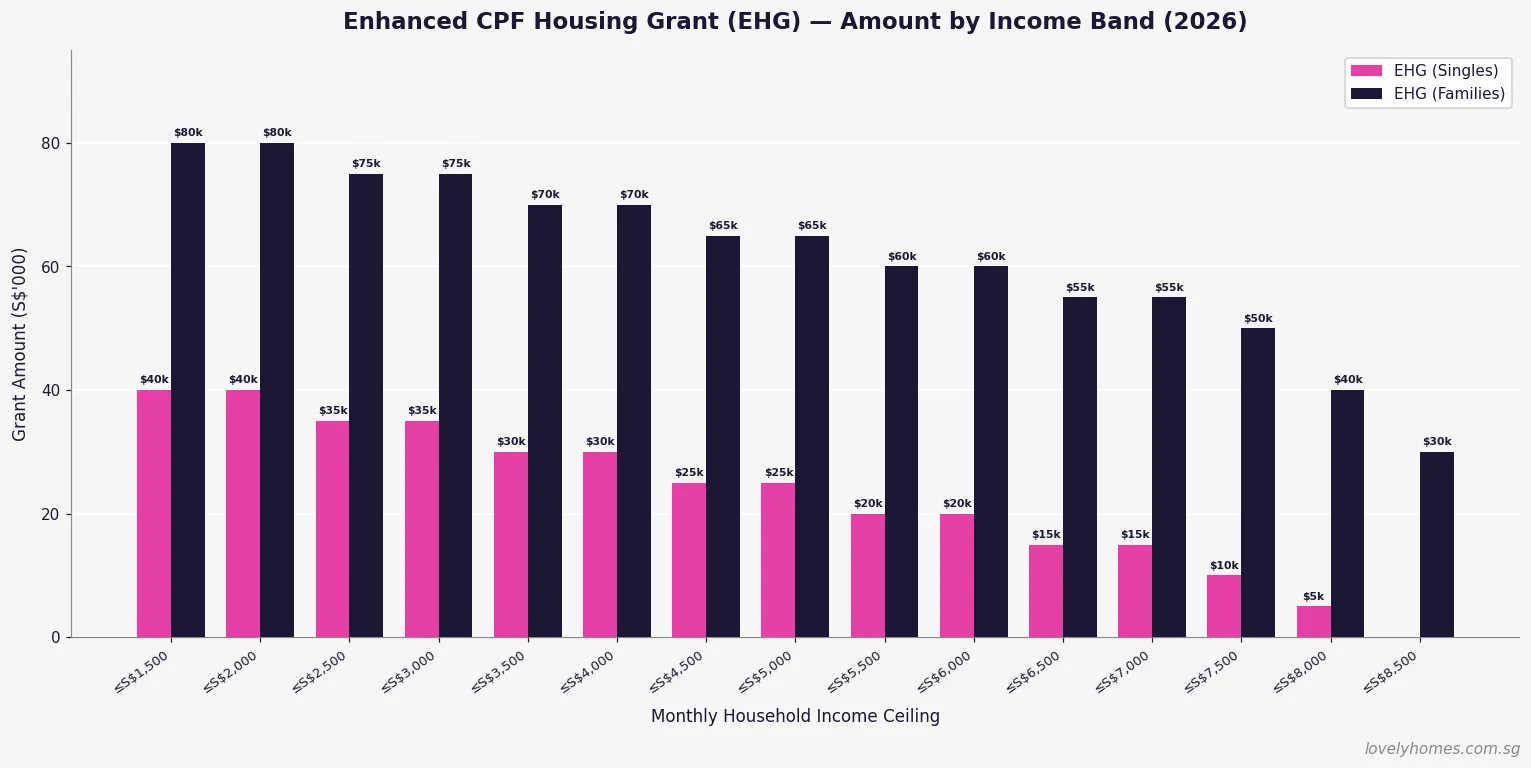

The Enhanced CPF Housing Grant (EHG): Singapore’s Core Affordability Tool

The EHG is the primary income-tested grant for first-timer households. It replaced the AHG and SHG from September 2019 and applies to both BTO and resale flats, removing the prior restriction that pegged larger grants exclusively to BTO purchases. The key parameters in 2026 are:

- Maximum grant: S$80,000 for eligible SC couples.

- Income ceiling: Average gross monthly household income of S$9,000 or below for couples; S$4,500 for singles.

- Citizenship requirement: At least one Singapore Citizen among the buyers; the other applicant may be an SC or SPR.

- Flat type: All HDB flat types from 2-Room Flexi upwards; also available for EC purchases under certain conditions.

- Property bar: Neither applicant may own any private residential property, locally or overseas, at the time of application.

- First-timer status: Both applicants must be first-timers (no prior HDB grant received, no prior subsidised flat sold without resale levy).

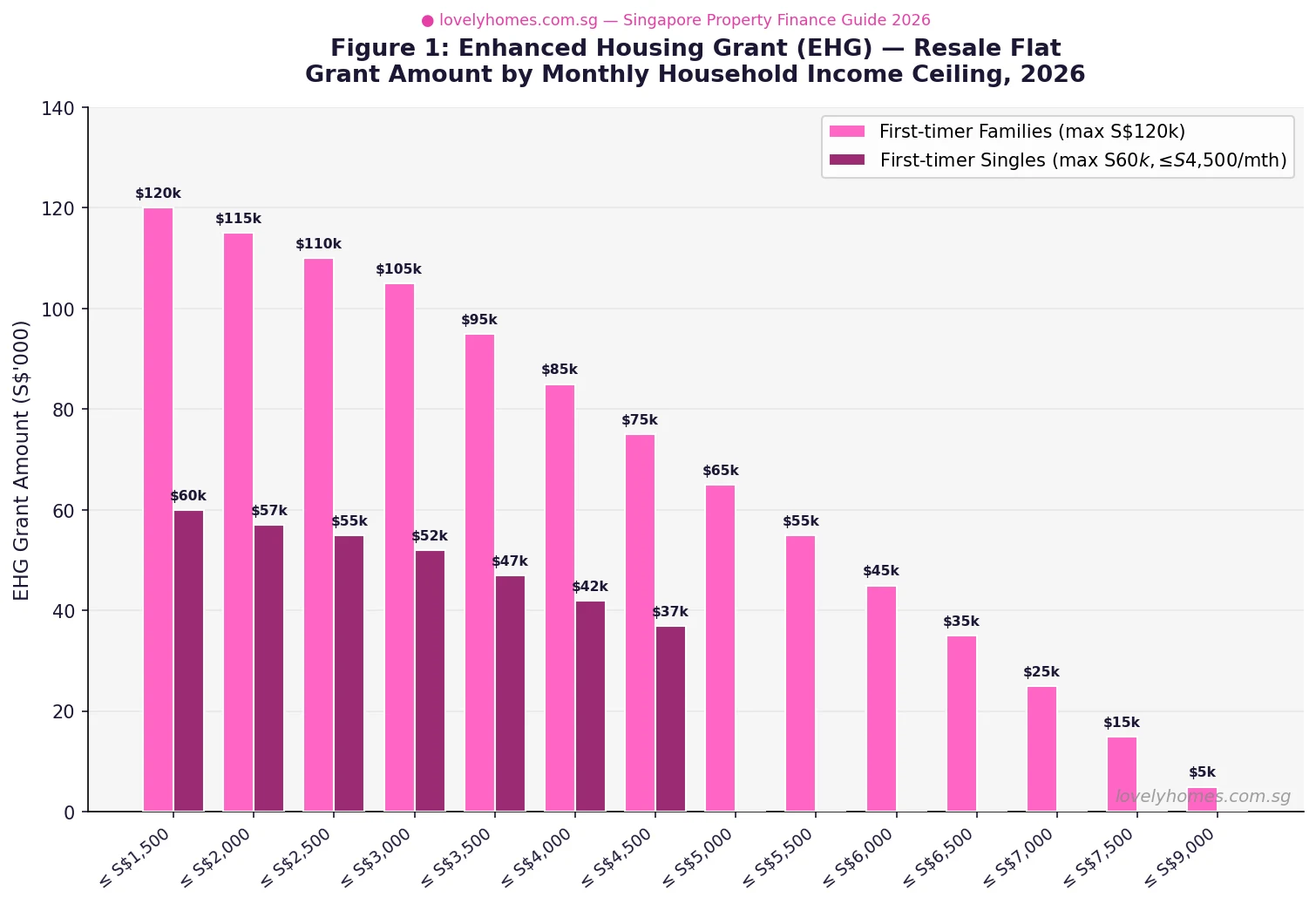

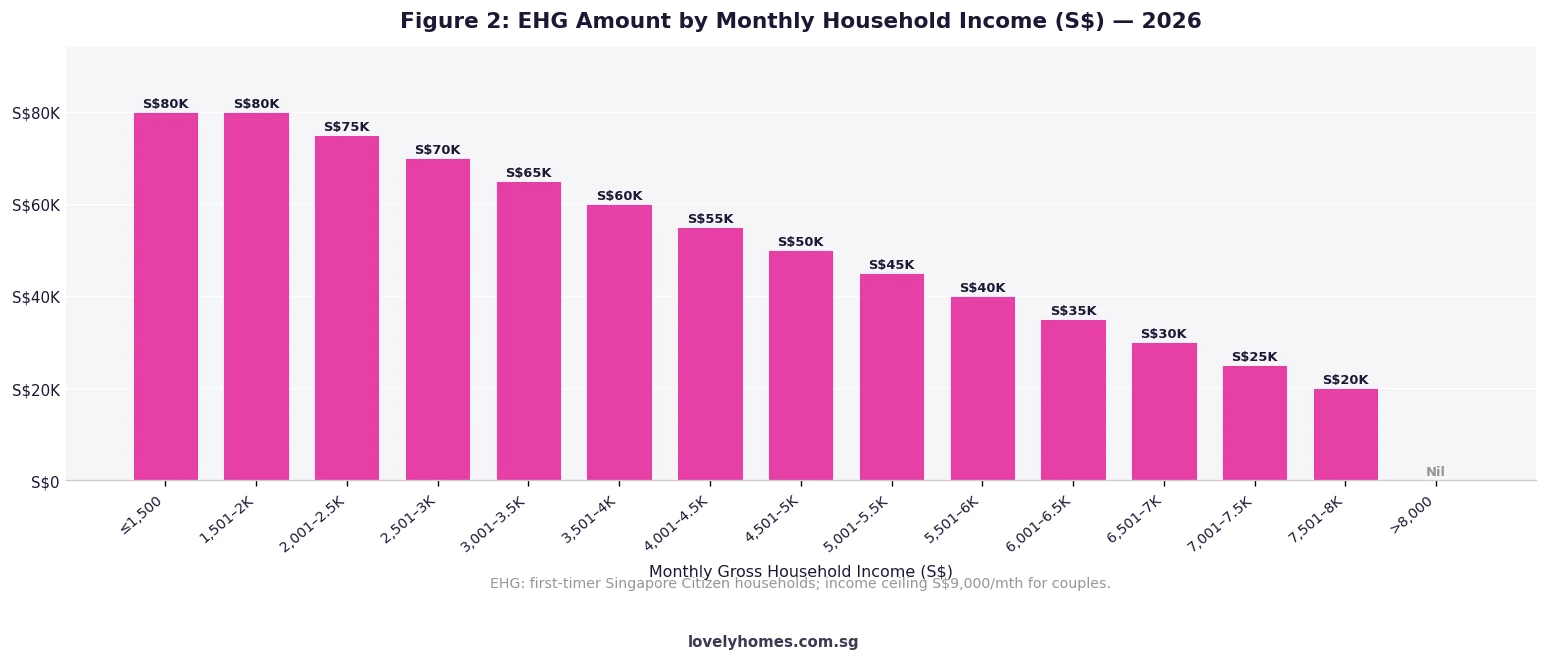

The EHG is structured in income bands: households earning S$1,500 per month or below receive the full S$80,000; those earning just under the S$9,000 ceiling receive S$5,000. Each band steps down by S$5,000 for every S$500 increase in income. Households earning S$9,001 or above receive nothing. Critically, EHG is computed on the average monthly income over the past 12 months — a point that catches some buyers off-guard when a recent pay rise pushes them over the ceiling retroactively.

Family Grant and Singles Grant: Boosting Resale Affordability

The Family Grant is available to first-timer families buying a resale HDB flat. Unlike the EHG, it is a flat sum that does not taper with income, though the household must still fall below the S$9,000 monthly income ceiling. For 2026:

| Buyer Profile | 3-Room or Smaller | 4-Room or Larger |

|---|---|---|

| SC + SC couple (first-timer) | S$50,000 | S$40,000 |

| SC + SPR couple (first-timer) | S$30,000 | S$25,000 |

| SC single (35+, first-timer) | S$25,000 (Singles Grant) | S$20,000 (Singles Grant) |

The Singles Grant operates on identical mechanics to the Family Grant but is specifically for unmarried Singapore Citizens aged 35 years and above, or widowed/divorced Singapore Citizens with no prior grant history. Singles may receive up to S$25,000 for a resale flat of 3-rooms or smaller and S$20,000 for a 4-room or larger unit. Note that singles buying a BTO flat are generally limited to 2-Room Flexi units at non-mature estates — a structural restriction that has been progressively relaxed since the 2023 housing reforms.

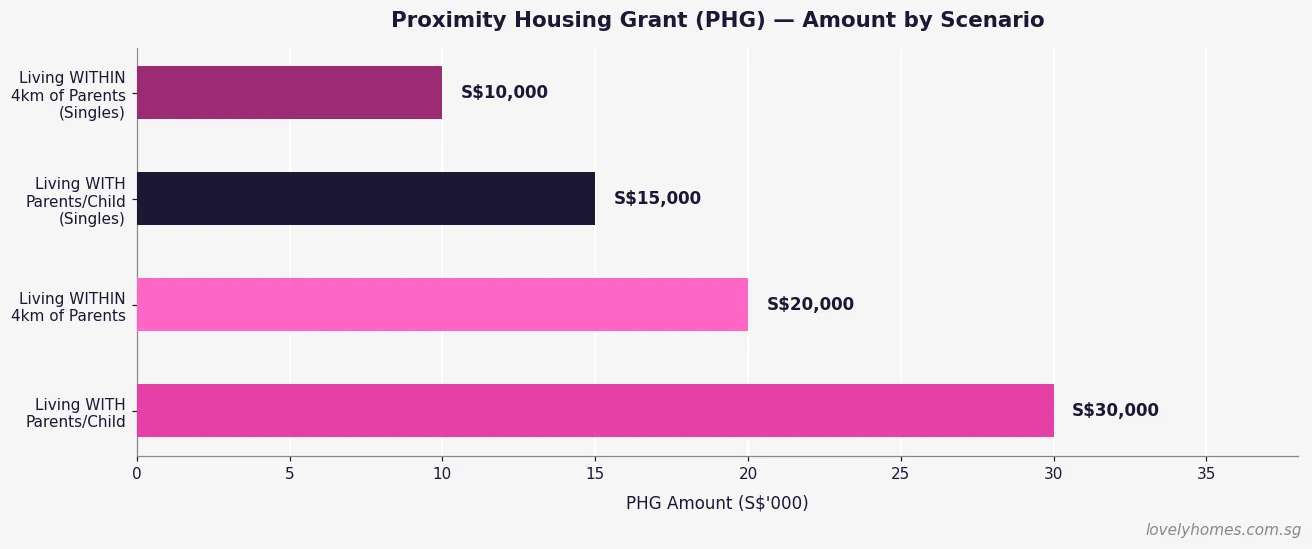

Proximity Housing Grant (PHG): Living Closer to Family

The Proximity Housing Grant was introduced in August 2015 to incentivise multi-generational proximity in public housing. In 2026, its parameters are:

- S$30,000: For SC households buying a resale flat within 4 km of parents’ or married child’s current HDB flat or private residential property.

- S$20,000: For SC households buying to co-reside in the same resale flat as parents or married child.

- Income ceiling: S$14,000 per month for the buying household (higher than EHG/Family Grant).

- Citizenship: At least one Singapore Citizen in the buying family nucleus.

- No BTO eligibility: PHG applies exclusively to resale transactions. BTO applicants who wish to live near family should note this distinction when weighing BTO versus resale.

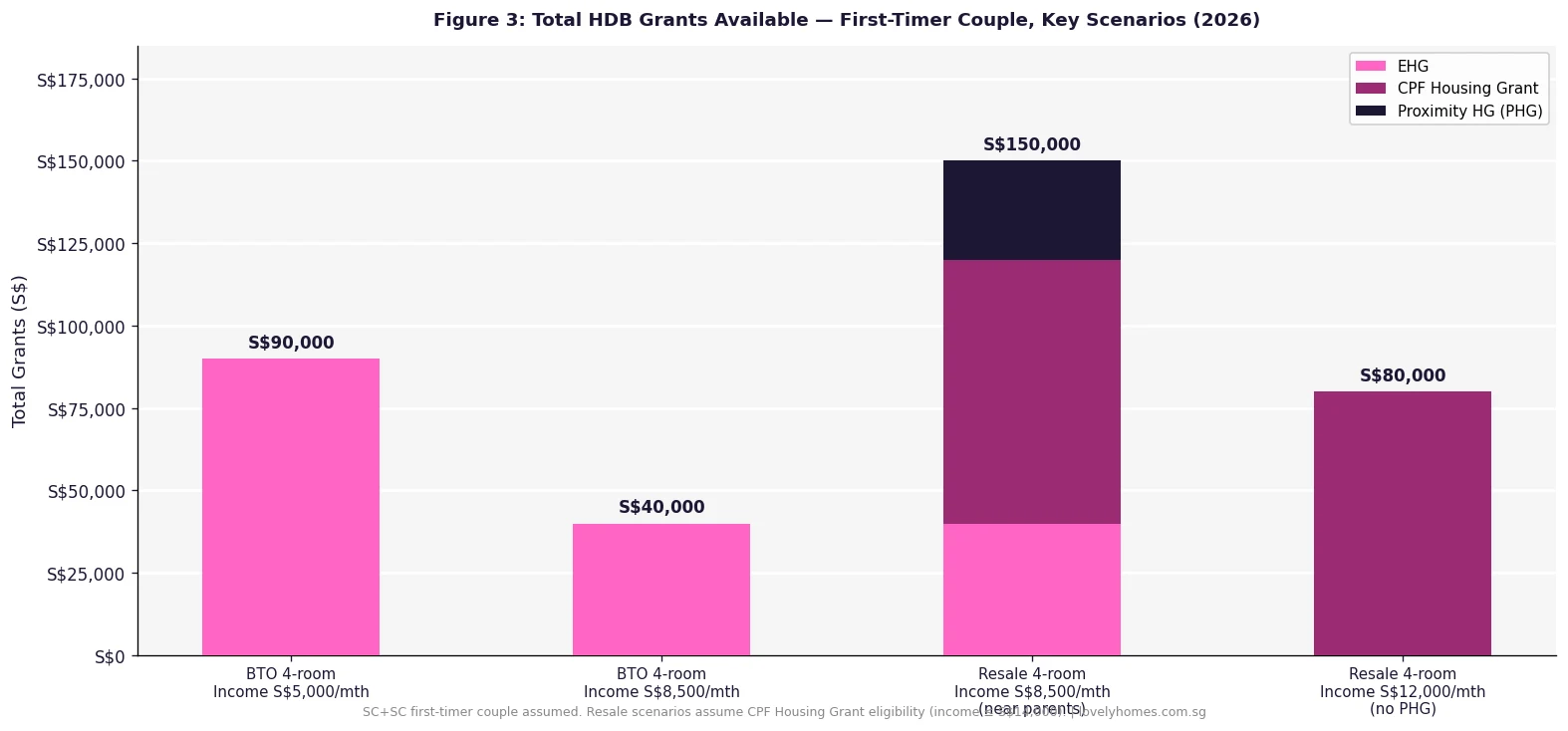

The PHG is stackable with the EHG and Family Grant, meaning an eligible SC couple buying a resale flat near their parents could potentially accumulate EHG (up to S$80K) + Family Grant (up to S$50K) + PHG (S$30K) = S$160,000 total. This scenario requires the household income to be S$9,000 or below (for the EHG and Family Grant components) and within 4 km of qualifying family (for PHG).

CPF Housing Grants for Executive Condominiums

Executive Condominiums (ECs) are a hybrid public-private housing type, and they carry their own grant structure. As of 2026:

- CPF Housing Grant (Family Grant, EC tranche): Up to S$30,000 for SC+SC first-timer families; S$20,000 for SC+SPR first-timer families.

- Income ceiling for EC grants: S$16,000 per month (higher than HDB flat grants).

- EHG does not apply to new EC purchases from developers; EHG is only available for HDB flats.

- Resale EC: Once an EC has been privatised (10 years from TOP), it is treated as a private property. No CPF Housing Grants apply to privatised EC resale transactions.

How Grants Are Disbursed: The CPF Mechanics

A common point of confusion is that CPF Housing Grants are not cash you receive at completion. Instead, they are credited to your CPF Ordinary Account before or at the point of purchase and immediately applied to reduce your housing outlay. In practice:

- HDB confirms your grant eligibility after your application is approved.

- The grant amount is credited into the primary applicant’s CPF OA.

- At the point of HDB loan drawdown or mortgage completion, the grant reduces the amount you must borrow.

- If you later sell the flat, the grant principal (without accrued interest) is returned to your CPF OA. Unlike regular CPF OA usage, no accrued interest is charged on the grant portion returned to CPF — only the original grant quantum is repaid to CPF upon sale.

This CPF-return mechanic is an important consideration when computing net cash proceeds on a future sale. While the grant reduces your upfront cost, it creates a future CPF refund obligation that reduces the cash you pocket when you eventually sell.

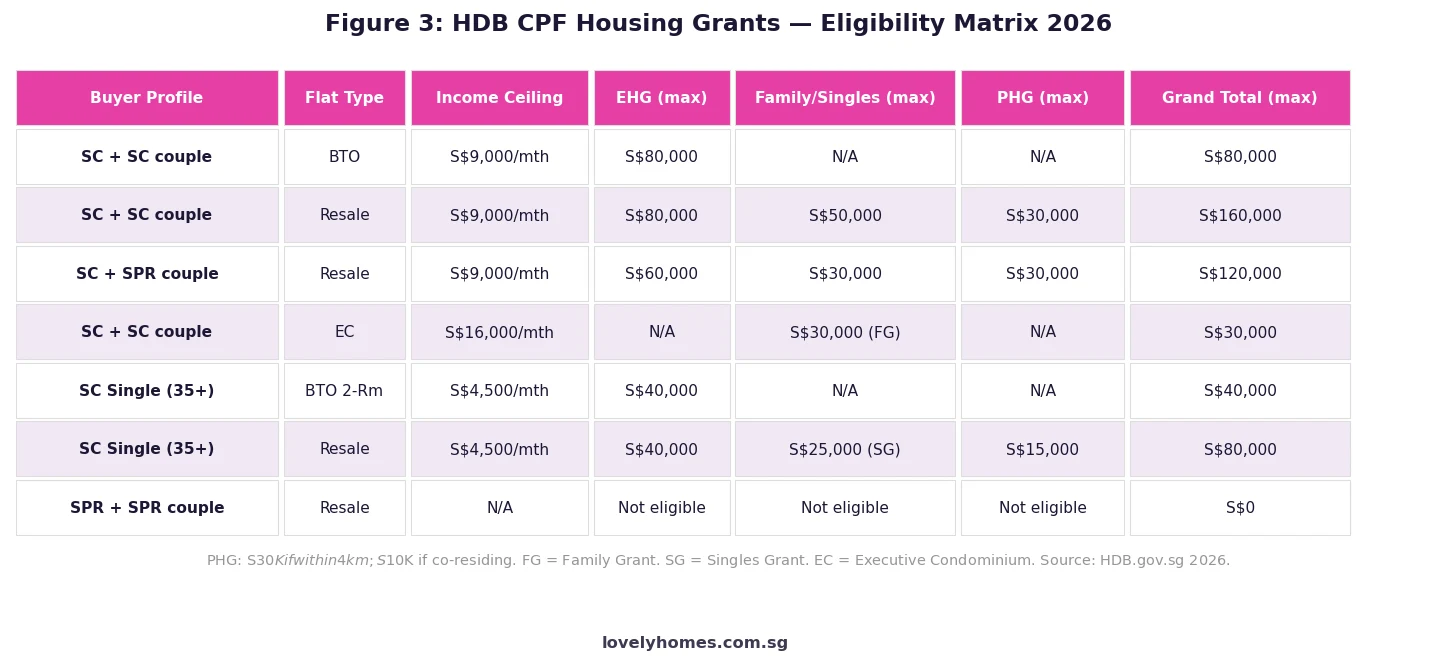

Summary: Grant Combinations at a Glance

| Buyer Profile | Flat Type | EHG (max) | Family/Singles (max) | PHG (max) | Grand Total (max) |

|---|---|---|---|---|---|

| SC + SC (1st-timer couple) | BTO | S$80,000 | N/A | N/A | S$80,000 |

| SC + SC (1st-timer couple) | Resale | S$80,000 | S$50,000 | S$30,000 | S$160,000 |

| SC + SPR (1st-timer couple) | Resale | S$60,000 | S$30,000 | S$30,000 | S$120,000 |

| SC + SC (1st-timer couple) | EC (new) | N/A | S$30,000 | N/A | S$30,000 |

| SC Single (35+, 1st-timer) | BTO 2-Rm | S$40,000 | N/A | N/A | S$40,000 |

| SC Single (35+, 1st-timer) | Resale | S$40,000 | S$25,000 | S$15,000 | S$80,000 |

| SPR + SPR couple | Any HDB | Nil | Nil | Nil | S$0 |

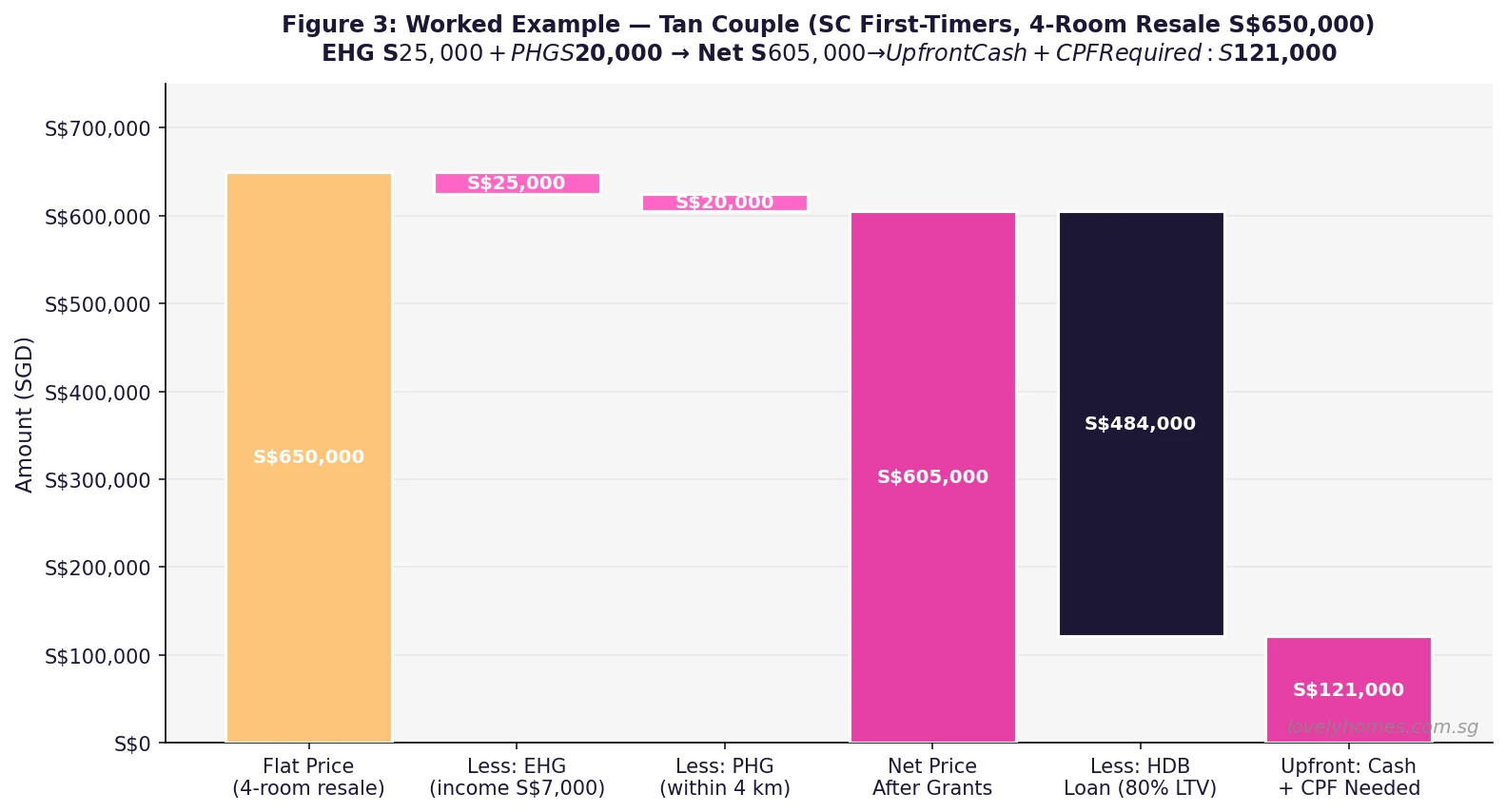

Worked Example: How the Grants Stack for a Real Buyer

📝 Case Study: The Wong Family, SC + SC, Monthly Income S$6,800

Profile: Mr and Mrs Wong, both Singapore Citizens, both first-timers. Monthly gross household income S$6,800. They are buying a 4-room resale HDB flat in Tampines near Mrs Wong’s parents (within 2.5 km).

Purchase price: S$580,000

- EHG: S$6,800 gross income → grant table gives S$45,000 (income band S$6,501–S$7,000).

- Family Grant (4-room resale, SC+SC): S$40,000.

- PHG (within 4 km of parents): S$30,000.

- Total grants: S$45,000 + S$40,000 + S$30,000 = S$115,000, credited to CPF OA before completion.

Effective purchase calculation:

- Purchase price: S$580,000

- Less grants applied: −S$115,000

- Effective cost to fund: S$465,000

- HDB loan (80% LTV on S$465,000): S$372,000 @2.60% p.a., 25 years → monthly instalment S$1,683

- MSR check: S$1,683 / S$6,800 = 24.7% ✓ (below 30% cap)

- Buyer’s Stamp Duty (BSD): S$580,000 → S$11,400 (paid via CPF OA)

- Cash upfront (5% option fee not covered by CPF): S$29,000

Net effect: The S$115,000 in grants effectively reduces the monthly instalment from S$2,235 (without grants, full loan on S$580K) to S$1,683 — a saving of S$552 per month, or S$165,600 over a 25-year loan at comparable rates.

Why CPF Housing Grants Matter for Singapore’s Housing Equation

Singapore’s public housing system is internationally praised as one of the few in which the majority of residents own their own homes. As of 2026, roughly 80% of Singapore citizens live in HDB flats, and about 90% of those residents own their unit. CPF Housing Grants are a central reason why homeownership remains attainable despite property prices that would otherwise appear formidable for median-income households.

For context: a 4-room BTO flat in a non-mature estate now launches at roughly S$380,000–S$500,000. A comparable unit in the private market in the same region would cost S$1.2M–S$1.6M. The combination of subsidised land cost (via HDB pricing below market), income-tested grants (EHG), and the availability of 30-year HDB loans at preferential rates (the CPF OA interest rate of 2.6%) means that a couple earning the median household income can service a BTO mortgage for a fraction of what private homeownership would cost.

The grants also serve as a redistributive mechanism: the EHG is explicitly income-tested and skewed towards lower-income households. A couple earning S$2,500/mth gets S$75,000 more than a couple earning S$8,500/mth for the same flat. This income-sensitive structure is a deliberate policy choice by the Ministry of National Development (MND) and HDB to ensure that public housing subsidies accrue proportionately to those who need them most.

What Might Come Next: Policy Watch 2026–2027

Note: the following reflects informed analysis, not confirmed policy. Several developments in the pipeline could affect CPF Housing Grants:

- October 2026 BTO launch: HDB is expected to release close to 8,000 units in the October 2026 exercise, including the first BTO flats under the expanded Prime, Plus and Standard classification framework. Grant eligibility under the new classification — especially for Plus flats, which carry tighter resale conditions — will be clarified in the launch materials.

- EHG income ceiling review: With median household income rising and the cost of living increasing, there is industry speculation that the EHG income ceiling of S$9,000 per month (unchanged since the 2019 restructuring) may be reviewed in the 2026 or 2027 Budget. An upward revision to S$10,000 or S$11,000 would extend subsidy access to a wider band of middle-income households.

- Grant portability for right-sizers: As Singapore’s population ages, there is increasing pressure to extend targeted subsidies to seniors downsizing from larger flats to 2-Room Flexi units. The Senior Priority Scheme and Move-In Priority Scheme already offer indirect advantages; a specific grant for right-sizing seniors has been discussed but not yet formalised as of mid-2026.

Frequently Asked Questions: HDB Housing Grants 2026

Can I receive CPF Housing Grants if my spouse is a Singapore Permanent Resident (SPR)?

Yes, but with reduced grant amounts. A Singapore Citizen buying a resale flat with an SPR spouse can receive an EHG of up to S$60,000 (vs S$80,000 for SC+SC couples) and a Family Grant of up to S$30,000 (vs S$50,000). Both applicants must be first-timers and the household income must not exceed S$9,000 per month. The PHG is also available at the same quantum (S$30,000) as for SC+SC couples, provided the proximity requirement is met.

I received a CPF Housing Grant for a previous flat. Can I get another grant for my next purchase?

Generally, no — CPF Housing Grants (EHG, Family Grant, Singles Grant, PHG) are available to first-timers only. If you previously received a grant and sold the flat, you are classified as a second-timer. Second-timers are not eligible for EHG, Family Grant, or Singles Grant when buying their next flat. The PHG is an exception: it may be available to second-timer SC households buying a resale flat near their parents or children, subject to a lower ceiling (S$15,000 within 4 km, S$5,000 for co-residing). Additionally, if a resale levy applies to your next purchase, the levy amount is in most cases higher than any grant you might receive, effectively making grants moot for most second-timer resale purchases.

Can I use CPF Housing Grants towards the option fee or stamp duty?

CPF Housing Grants are credited to your CPF Ordinary Account and are not available as cash. They cannot be used for the Option to Purchase (OTP) exercise fee, which must be paid in cash. However, once the grant is in your CPF OA, it can be used to pay the Buyer’s Stamp Duty (BSD) and the mortgage downpayment (subject to the Valuation Limit and Withdrawal Limit). In practice, the grant effectively reduces the CPF OA portion of your overall transaction cost, increasing the residual balance available for other CPF-eligible expenses.

Does my overseas property disqualify me from receiving HDB grants?

Yes. HDB’s eligibility criteria for CPF Housing Grants require that neither the applicant nor any co-applicant owns or has disposed of any private residential property (including overseas properties) within 30 months before the flat application date. If you owned an overseas property and sold it, you must wait at least 30 months before applying. Undisclosed overseas property ownership is a statutory breach and can result in grant clawback plus penalties under the Housing & Development Act.

When I sell the flat, do I repay the grant to HDB or to CPF?

The grant is returned to CPF, not to HDB. Specifically, the original grant quantum (without accrued interest) is refunded to your CPF OA upon sale. This is different from regular CPF OA usage, where you must refund the principal plus accrued interest at 2.5% per annum. The no-interest feature of grant repayment is favourable: for a S$50,000 grant held for 20 years, you repay exactly S$50,000 to CPF rather than S$83,000 (which would apply if ordinary CPF interest accrual rules applied). Any cash proceeds above CPF refunds and outstanding loans are yours to keep.

Can a divorced or widowed Singapore Citizen get any HDB grants?

Yes. A divorced or widowed SC who has not previously received a CPF Housing Grant is treated as a first-timer for grant purposes (though not always for flat-type eligibility). Depending on age and circumstances: if aged 35 and above, the SC can apply for a 2-Room Flexi BTO (with EHG up to S$40,000) or a resale flat (with EHG + Singles Grant + PHG, up to S$80,000 in total). If the individual has a child and thus forms a family nucleus, they may be eligible for family-size flats and the full suite of family-tier grants, subject to income criteria.

Do EHG and Family Grant count towards my CPF Withdrawal Limit?

No. CPF Housing Grants do not count towards the Valuation Limit (VL) or Withdrawal Limit (WL) applicable to CPF usage for housing. The VL is capped at the property’s value, and the WL is capped at 120% of the VL for private properties. Grants are credited to your OA and can be applied without reference to these limits, which means the grant effectively gives you additional CPF headroom beyond the standard withdrawal cap. This is a meaningful benefit when buying an older or lower-valued resale flat where the WL might otherwise restrict CPF usage.

Click anywhere to close