Singapore Private Property Rental Guide 2026: How to Rent Out Your Condo

No Minimum Occupation Period, no HDB approval to wait for, no Non-Citizen Quota headaches — private property landlords in Singapore enjoy a straightforward path to rental income. This guide walks you through every step, from setting an asking rent to declaring income with IRAS, with figures drawn from URA transaction data for Q1 2026.

Quick Answer: Key Facts About Renting Out a Private Property in Singapore (2026)

- No MOP applies to private condominiums, apartments, or landed houses — you may rent your property out immediately after purchase, regardless of nationality.

- Minimum rental period: 3 consecutive months. Short-term lets under 3 months (including Airbnb-style arrangements) are not permitted without URA approval and carry fines up to S$200,000.

- Occupancy cap: up to 6 unrelated persons for units <90 sqm; up to 8 for units ≥90 sqm (extended to 31 December 2026 by URA).

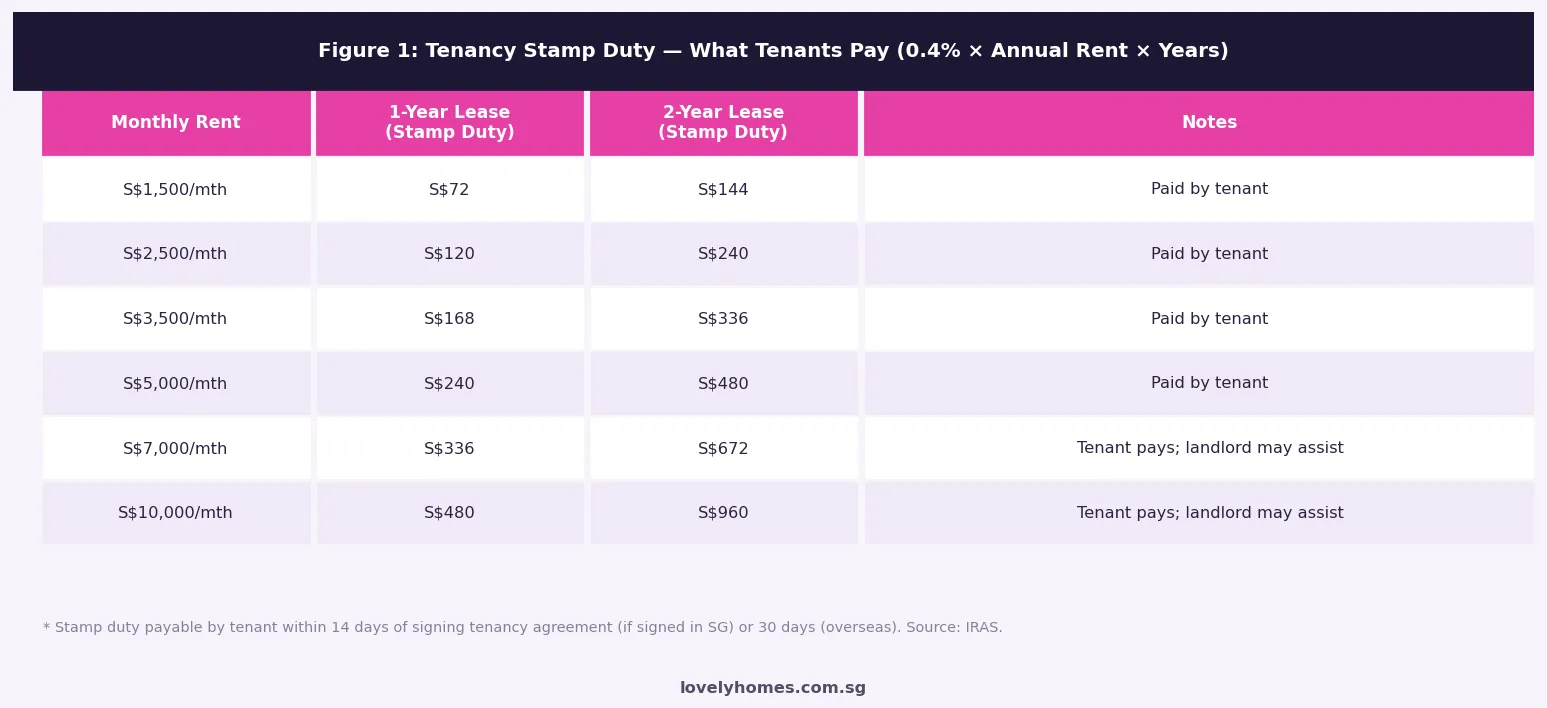

- Stamp duty on tenancy is paid by the tenant, not the landlord: 0.4% × annual rent × lease years, payable within 14 days of signing.

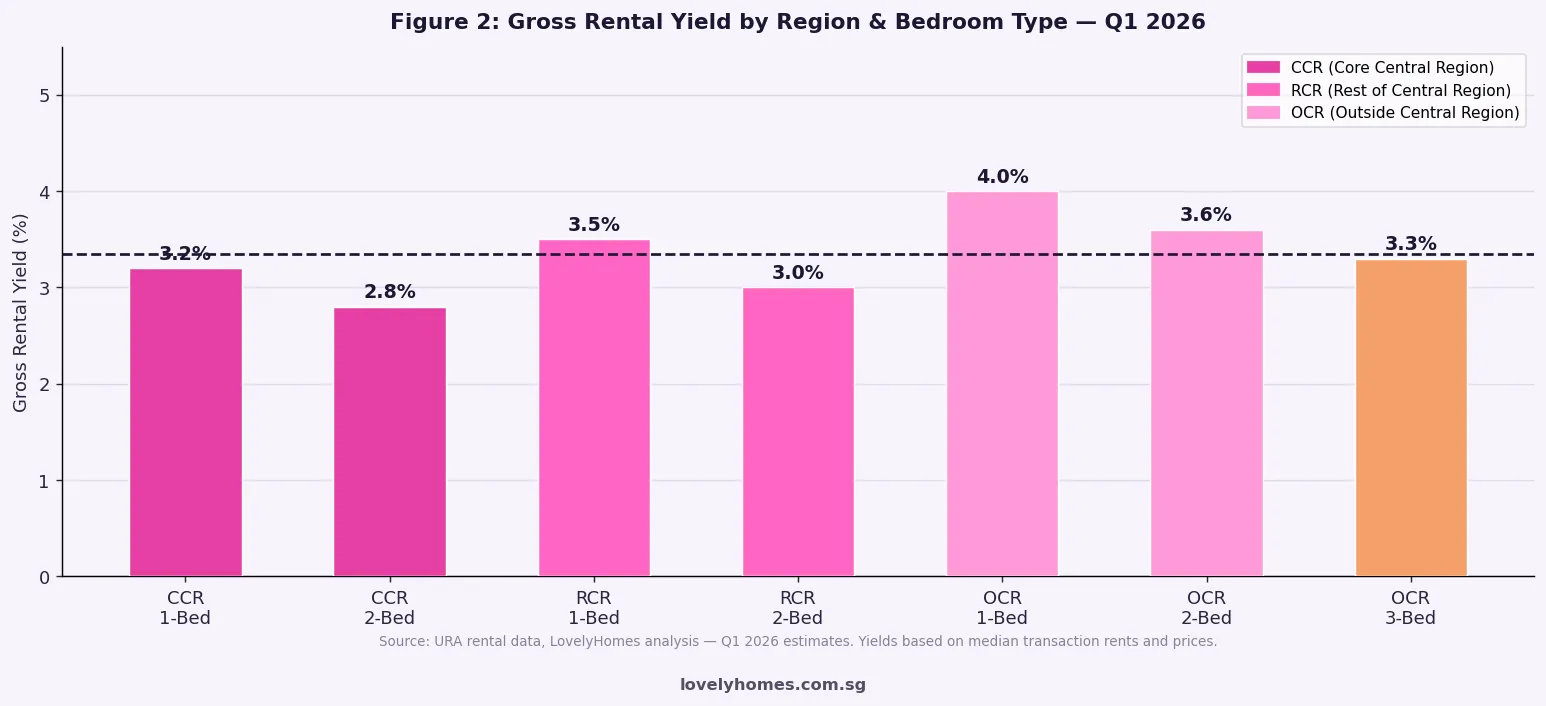

- Gross rental yields range from 3.0% (CCR 2-bed) to 4.0% (OCR 1-bed) as at Q1 2026, based on URA median rent and price data.

- Security deposit: 1 month for a 1-year lease; 2 months for a 2-year lease — held in trust by the landlord throughout tenancy.

- IRAS taxable income: rental proceeds are assessable; allowable deductions include mortgage interest, property tax, agent commission, and qualifying repairs.

Who Can Rent Out a Private Property in Singapore?

Unlike HDB flats, private residential properties in Singapore carry no Minimum Occupation Period. A Singapore Citizen, Singapore Permanent Resident, or foreigner who legally owns a private condominium, apartment, or landed house may rent it out from the day of purchase. There is no HDB portal to seek approval through, and no requirement to occupy the property first.

The only eligibility constraint is that the property must have obtained its Temporary Occupation Permit (TOP) or Certificate of Statutory Completion (CSC) before a tenancy can commence. Properties still under construction cannot be occupied or rented, even if the Sale and Purchase Agreement has been executed.

Owners of Executive Condominiums (ECs) are subject to a different regime: during the first 5 years post-TOP, the EC is treated as a public housing flat and subletting is prohibited. After the 5-year Minimum Occupation Period but before the 10-year privatisation, ECs may be rented out subject to rules similar to HDB flats. Only after the 10-year mark do ECs become fully privatised and freely rentable.

URA Rules: Minimum Lease Period and Occupancy Limits

The Urban Redevelopment Authority (URA) is the primary regulator of private residential rentals. Two rules are non-negotiable:

Minimum 3-month tenancy. Every tenancy must cover at least 3 consecutive months. This rule was introduced to prevent the proliferation of short-term holiday lets that erode residential character. Violations attract fines of up to S$200,000 for the property owner. Platforms such as Airbnb and Agoda may not be used for listings below 3 months without a URA exemption, which is rarely granted for residential units.

Occupancy limits. URA caps the number of unrelated persons who may occupy a private residential unit simultaneously. For units smaller than 90 sqm, the limit is 6 unrelated persons. For units of 90 sqm or larger, URA raised the cap to 8 persons in 2024 and has extended this to 31 December 2026 to ease supply pressure in the rental market. Family members are not counted toward the unrelated persons cap.

Beyond the occupancy rule, URA also requires that any tenant who is a foreigner must hold a valid Long-Term Visit Pass, Employment Pass, S Pass, Work Permit, Dependent Pass, or Student Pass. Short-stay visitors on social visit passes may not be named tenants.

Setting Your Rental Price

Pricing a private property correctly is the single most important factor in minimising vacancy. A unit priced S$200–S$300 above market may sit empty for 4–6 weeks; at current yields of 3–4%, that vacancy erodes more income than a moderate price concession would.

The URA publishes median transacted rents quarterly, and the SRX portal aggregates live rental listings. As a starting point, research transactions in the same postal district for units of the same bedroom count, furnishing level, and floor range within the 6 months prior to your listing date. Use the URA Rental Transactions portal (freely accessible at ura.gov.sg) to pull the raw data, rather than relying on listing prices, which are asking prices and may sit above transacted levels.

Gross rental yield is a useful but incomplete metric. Net yield — after property tax, agent commission, mortgage interest, and maintenance — can be 0.8–1.2 percentage points lower than gross yield for a leveraged property. To calculate gross yield: divide the annual rental income by the purchase price and multiply by 100. A 3BR OCR condo purchased at S$1,550,000 and renting for S$4,200/mth yields approximately (S$50,400 / S$1,550,000) × 100 = 3.25% gross.

Finding Tenants: DIY vs Property Agent

Singapore landlords may list their units directly on rental portals (PropertyGuru, 99.co, SRX) or engage a licensed property agent. Each approach has trade-offs:

DIY listing: No commission payable. Listing fees range from S$0 (basic) to S$200–S$400 for featured placement. You conduct all viewings, screen tenants independently, and draft or adapt a standard tenancy agreement. Suitable for landlords with experience, flexible hours, and a well-priced unit in high demand.

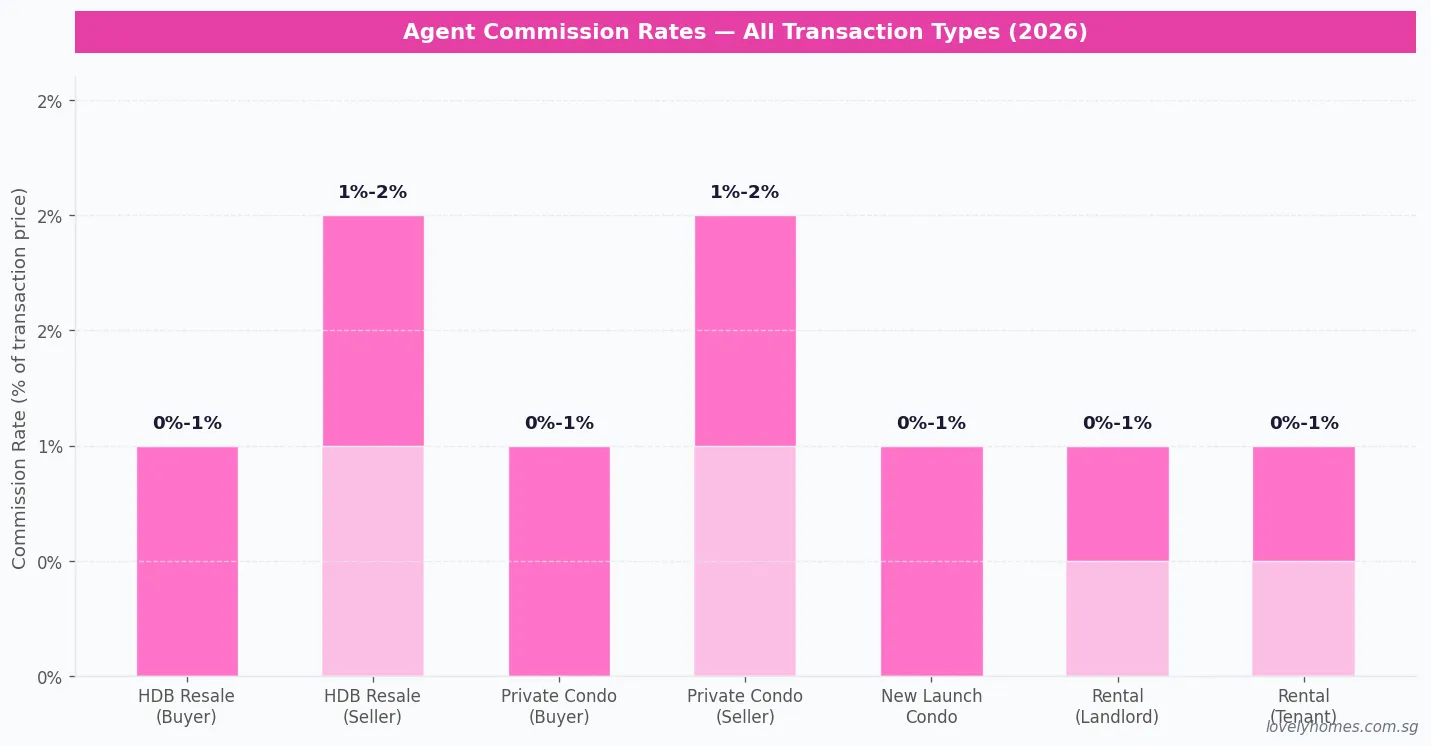

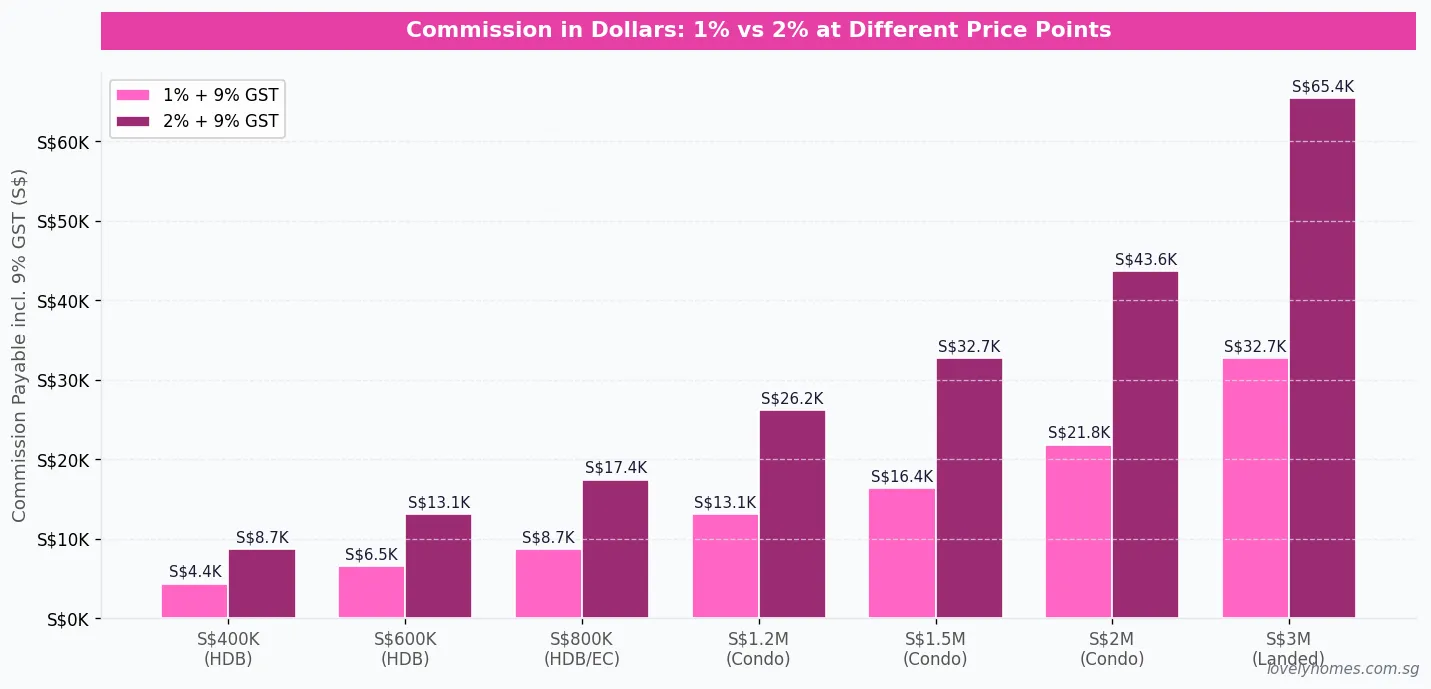

Engaging an agent: Typically, the landlord pays commission of approximately 1 month’s rent for a 2-year tenancy, plus GST (currently 9%). For a 1-year tenancy, some agents charge 0.5 month, and it is common for the tenant to contribute the other 0.5 month. Agent commission rates are not fixed by law, though the Council for Estate Agencies (CEA) publishes guidelines that set expected ranges. All real estate agents in Singapore must hold a valid CEA registration, which you can verify at the CEA Public Register at cea.gov.sg.

The Tenancy Agreement: Key Clauses Every Landlord Must Know

The Tenancy Agreement (TA) is the binding contract between landlord and tenant. Singapore follows English common law on tenancy matters, and courts have generally upheld clearly drafted TA clauses. Always use a written TA, executed before the tenant takes possession, and stamp it through IRAS e-Stamping within 14 days.

Several clauses deserve particular attention:

Diplomatic Clause (DC). This clause is standard in leases where the tenant is an expatriate professional. It allows the tenant to terminate a 2-year lease early after a minimum stay of 12 to 14 months, upon giving 2 months’ written notice. The rationale is that expatriates may be transferred abroad or have their employment pass cancelled at short notice. Landlords should consider whether to include the DC carefully: for high-demand units in areas popular with international tenants (Tanglin, Orchard, Holland Village, East Coast), including the DC broadens the tenant pool and reduces vacancy risk. For units in OCR estates with a predominantly local tenant profile, the DC may be unnecessary.

Minor repairs threshold. The TA should specify a dollar threshold below which minor repairs are the tenant’s responsibility. The standard range in Singapore is S$150 to S$250 per incident. Repairs above that threshold — including plumbing, electrical faults, structural defects, and major appliances — are the landlord’s obligation. Air-conditioning servicing is typically quarterly at the tenant’s cost, with the landlord responsible for major AC overhauls.

No-subletting clause. Unless you explicitly permit subletting, include a clause prohibiting the tenant from subletting to any third party, including family members not named in the TA, without the landlord’s written consent.

Inventory and condition report. A photographic inventory and condition report, signed by both parties at the point of handover, is not legally mandated but is highly advisable. It forms the evidentiary baseline if disputes arise at the end of the tenancy over the return of the security deposit.

Tenancy Stamp Duty and Security Deposit

Stamp duty on the tenancy agreement is a cost borne by the tenant (not the landlord), calculated at 0.4% of the annual rent multiplied by the number of years of the lease. For a 2-year lease at S$4,000/mth, the stamp duty is: 0.4% × S$48,000 × 2 = S$384. The tenant must pay through IRAS e-Stamping within 14 days of signing the TA if executed in Singapore, or within 30 days if signed overseas.

The security deposit is held by the landlord throughout the tenancy and is used to offset unpaid rent or damage beyond fair wear and tear. The standard quantum is:

- 1-year lease: 1 month’s rent as security deposit

- 2-year lease: 2 months’ rent as security deposit

The security deposit must be returned to the tenant within a reasonable timeframe after the end of tenancy — typically 14 to 30 days — less any properly documented deductions. Landlords who withhold deposits without justification may face claims in the Small Claims Tribunal.

Managing Your Tenancy: Obligations and Best Practices

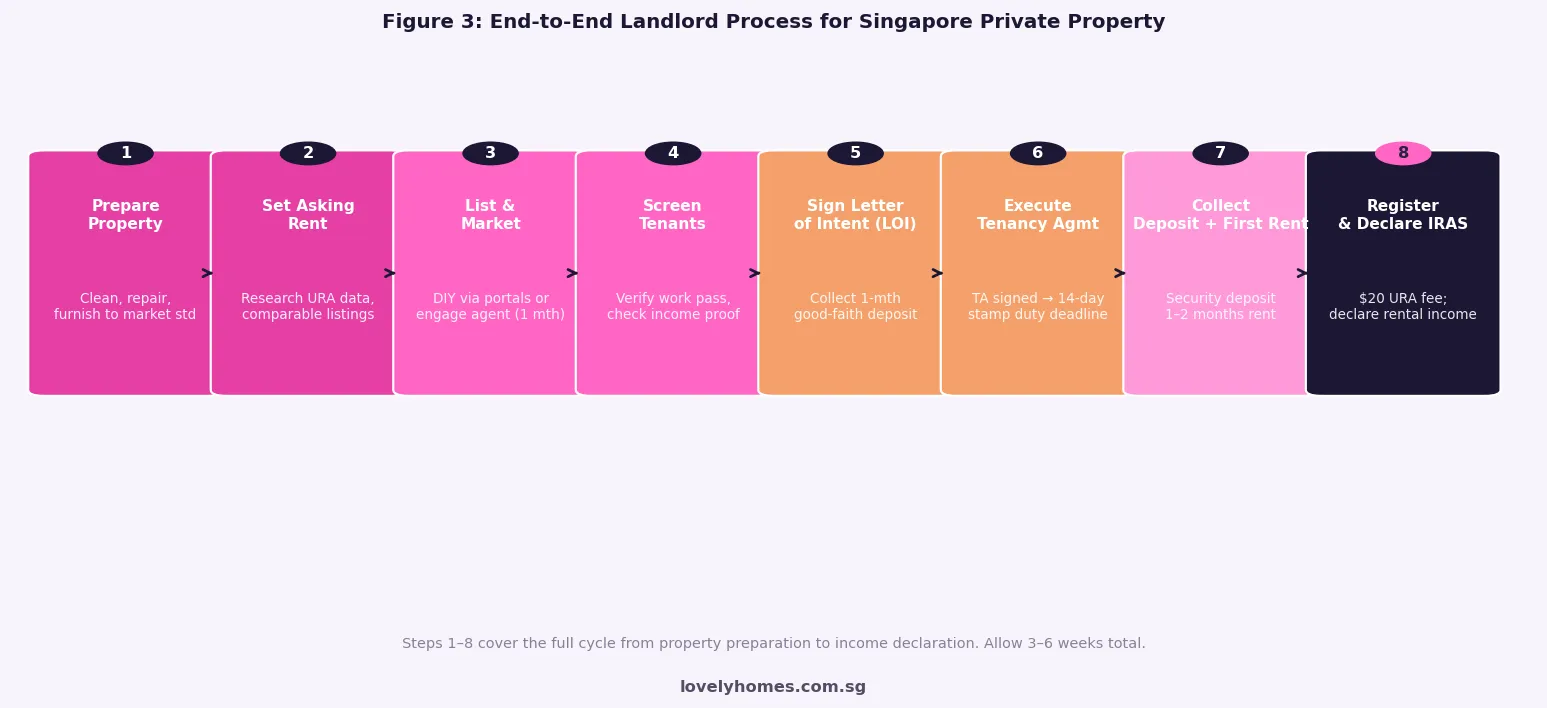

Once the tenancy commences, the landlord’s ongoing obligations include maintaining the property in a habitable condition, attending to major repairs promptly, ensuring the property tax and mortgage (if any) remain current, and registering the tenancy with URA at a one-time administrative fee of S$20 per tenancy through the URA e-Service portal.

Although Singapore law does not require landlords to register every tenancy, the S$20 registration creates a formal record that is useful if disputes arise about the lease period or the identity of authorised occupants. It is considered best practice.

Summary Table: Private Property Rental at a Glance

| Item | Rule / Typical Rate | Who Pays | Authority |

|---|---|---|---|

| Minimum Occupation Period | None for private property | N/A | URA |

| Minimum lease duration | 3 consecutive months | N/A | URA |

| Occupancy cap (<90 sqm) | Max 6 unrelated persons | N/A | URA |

| Occupancy cap (≥90 sqm) | Max 8 persons (until 31 Dec 2026) | N/A | URA |

| Tenancy stamp duty | 0.4% × annual rent × years | Tenant (within 14 days) | IRAS |

| Security deposit (1-yr lease) | 1 month’s rent | Tenant (to landlord) | Market practice |

| Security deposit (2-yr lease) | 2 months’ rent | Tenant (to landlord) | Market practice |

| Agent commission (2-yr lease) | ~1 month’s rent + 9% GST | Landlord | CEA guidelines |

| URA tenancy registration | S$20 one-time | Landlord | URA |

| IRAS rental income declaration | Annual (with personal income tax return) | Landlord | IRAS |

Worked Example: The Chen Family Rent Out Their D15 Investment Condo

Scenario: SC couple renting out a 2BR freehold condo in Marine Parade (D15)

Property: 2BR, 780 sqft (72 sqm), purchased in 2021 at S$1,050,000. Monthly mortgage: S$3,300 (bank loan at current SORA package ~1.65%).

Asking rent: S$3,800/mth (based on URA Q1 2026 comparables in D15 for 2BR 700–900 sqft, median S$3,700–S$4,000/mth).

Lease: 2-year lease, with Diplomatic Clause, to an Employment Pass holder. Agent engaged at S$3,800 + 9% GST = S$4,142 commission (one-time).

Stamp duty (tenant pays): 0.4% × S$45,600 × 2 = S$365.

Security deposit collected: S$7,600 (2 months).

Gross annual rental income: S$45,600.

IRAS allowable deductions (Year 1):

- Mortgage interest component: ~S$10,200 (estimated; not principal repayment)

- Property tax (non-owner-occupied AV ~S$13,200, non-OO rate ~4%): S$528

- Agent commission: S$4,142

- AC servicing (quarterly, tenant-borne under TA): S$0 to landlord

- Minor repairs allowance: S$350

- Total deductions: ~S$15,220

Net taxable rental income: S$45,600 − S$15,220 = S$30,380.

Gross yield: S$45,600 / S$1,050,000 = 4.34% (D15 slightly above RCR average due to freehold, sea view).

Net cash flow after mortgage: S$45,600 − S$39,600 (mortgage) − S$528 (property tax) = +S$5,472/yr surplus. Property is largely self-funding, with tax on net income approximately S$2,280/yr (at 15% marginal rate), leaving ~S$3,190/yr net after all costs.

Why Renting Out Makes Financial Sense — and the Risks

Renting out a private property is one of the few ways Singapore resident-owners can generate a recurring, inflation-linked cash stream from an asset that also appreciates over time. Unlike REITs or equities, direct property rental gives landlords full control over the asset, no management fee layer, and the ability to claim mortgage interest as a tax deduction — a benefit not available for investment portfolio interest in Singapore.

For HDB upgraders who purchase a private property and place their HDB flat on the market within 6 months (to claim the ABSD remission), renting out the private property during the transitional period can offset the carrying cost of two mortgages. For pure investors holding an investment property outright or with modest leverage, the rental stream provides a yield that — at current SORA rates — compares favourably with Singapore Government Securities yields.

The primary risks are vacancy (particularly acute during lease renewals in a softer rental market) and tenant quality. Singapore’s Small Claims Tribunal offers a relatively efficient remedy for rental disputes up to S$30,000, but eviction for non-payment requires court proceedings under the Distress Act — a process that can take 2–4 months during which the landlord typically cannot recover rent. Thorough tenant screening at outset is the most cost-effective risk mitigation.

What Might Come Next in Singapore’s Rental Market

Rental volumes in Q1 2026 remained broadly stable at approximately 22,000 condo leases transacted, roughly in line with Q4 2025. Median rents in the OCR, however, edged down by 1.2% from the cyclical peaks recorded in H2 2023, as the supply pipeline from 2022–2024 en-bloc redevelopments and new launches progressively delivered completions. Analysts anticipate moderate rental softening of 3–6% in the OCR through 2026, particularly for older suburban condos competing with newer Integrated Developments near MRT stations.

For landlords, this signals a need to maintain unit presentation to retain good tenants, and to build in realistic vacancy buffers of 3–4 weeks per year when modelling rental returns. CCR and RCR units in established expatriate catchments (Orchard, Novena, Marine Parade, East Coast, Buona Vista) remain structurally supported by continued inflows of professionals, and URA data suggests that sub-1,000 sqft condo rentals in these areas held their rents more firmly than larger units through H1 2026.

URA’s temporary increase of the occupancy cap for units above 90 sqm (to 8 persons) expires on 31 December 2026. Whether this is extended will depend on rental market conditions in H2 2026. Landlords of larger units benefit from the current flexibility; if the cap reverts to 6 persons, it may marginally reduce demand from coliving arrangements in larger apartments.

FAQ: Renting Out a Private Property in Singapore

Can I rent out my condo if I have an outstanding HDB loan or CPF housing refund?

Yes. The HDB loan and CPF usage relate to your HDB flat (if you own one), not your private property. Owning a private property and having an outstanding HDB loan simultaneously is not permitted under HDB rules — HDB flat owners who purchase private property must sell the HDB within 6 months or repay the HDB loan first. But if your private condo is your only or primary property and you hold a bank loan (not an HDB loan), there is no restriction on renting it out. The CPF refund obligation on your CPF-funded purchase only crystallises when you sell, not when you rent out.

Do I need to be in Singapore to manage a tenancy?

No. Many Singapore landlords manage their rental properties remotely from overseas. You can appoint a property manager or a licensed agent to handle viewings, inspections, maintenance coordination, and rent collection. A Power of Attorney may be executed to authorise a person in Singapore to sign the tenancy agreement on your behalf. Overseas landlords are subject to the same IRAS obligations and must declare Singapore-sourced rental income in their annual tax returns, which can be filed online.

What happens if my tenant refuses to leave at the end of the lease?

If a tenant holds over (remains in possession after the tenancy expiry) without your agreement, they become a statutory monthly tenant, and you are entitled to raise the rent to market rate or seek vacant possession through court proceedings. Singapore courts generally move relatively expeditiously on uncomplicated holdover matters. To minimise risk, issue a formal written notice to yield up possession at least 2 months before the lease expiry, and document all correspondence.

Can I rent out individual rooms rather than the whole unit?

Yes. Unlike HDB flats (which require approval to sublet a room), private property owners may rent individual rooms without URA approval, provided the overall occupancy cap is not exceeded (6 unrelated persons for <90 sqm; 8 for ≥90 sqm). Each room rental is still subject to the 3-month minimum lease rule. Landlords who live in the property and rent one or two rooms should note that they are still required to declare the room rental income to IRAS, though they may deduct a proportionate share of allowable expenses.

Is rental income from a furnished condo taxed differently from an unfurnished one?

No. IRAS does not distinguish between furnished and unfurnished rentals for income tax purposes. Rental income is assessed on the full rental amount received. If you charge a separate furniture rental fee in addition to the base rent, IRAS will aggregate both components as taxable income. You may, however, claim depreciation on furniture through the Renovation and Refurbishment (R&R) deduction, which IRAS generally caps at 1/3 of the qualifying expenditure per year over 3 years, subject to conditions.

What is the difference between the Diplomatic Clause and a break clause?

The Diplomatic Clause is specific to expatriate tenants whose residency in Singapore is contingent on their employment or immigration status. It allows early termination of the lease if the tenant’s employment in Singapore is terminated or they are transferred overseas, after a minimum occupancy period (usually 12–14 months) and upon 2 months’ written notice. A break clause is a more general early-termination mechanism available to either party (or both) at defined intervals during the lease, regardless of the reason. Landlords in Singapore rarely grant general break clauses; the Diplomatic Clause is the most common form of landlord-accepted early exit provision.

What CEA rules apply to me as a landlord?

If you are the direct property owner transacting as a principal (not as a licensed agent), CEA regulations do not restrict you from advertising your own property or signing your own tenancy agreement without an agent. You are not required to be CEA-registered to rent out your own property. However, any person you engage to facilitate the rental (conduct viewings, negotiate terms, execute documentation) must hold a valid CEA registration. Engaging an unlicensed intermediary exposes you to potential complications if disputes arise.

Click anywhere outside to close • Scroll to zoom