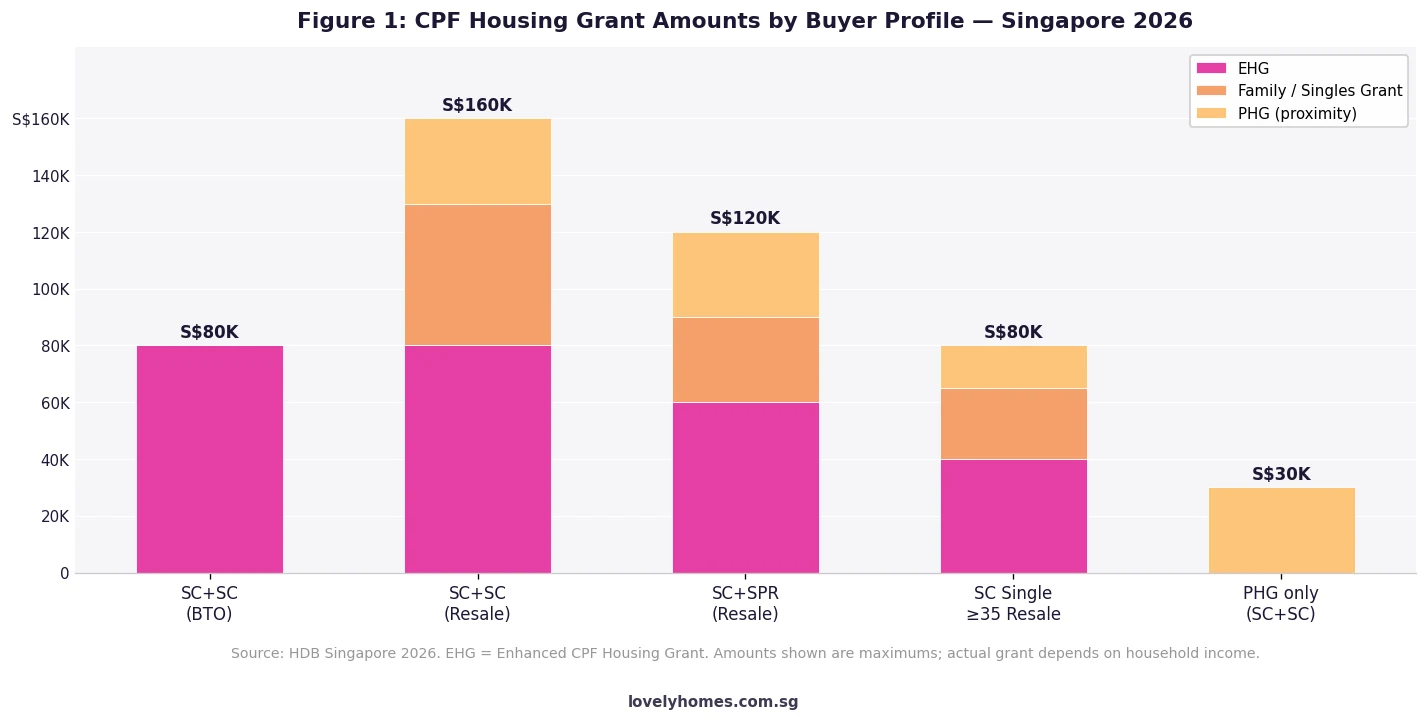

Largest grant available: Up to S$160,000 for eligible Singapore Citizen couples buying an HDB resale flat (EHG S$80K + Family Grant S$50K + PHG S$30K).

EHG (Enhanced CPF Housing Grant): Up to S$80,000; income ceiling S$9,000/mth for couples; covers BTO and resale; granted by HDB, paid from CPF.

Family Grant: Up to S$50,000 for SC+SC couples buying resale; S$30,000 for SC+SPR couples.

Singles Grant: Up to S$25,000 for unmarried/divorced Singapore Citizens aged 35 and above buying resale.

Proximity Housing Grant (PHG): S$30,000 if you buy within 4 km of your parents or children; S$10,000 if you buy to co-reside.

CPF Housing Grant for ECs: S$30,000 Family Grant available for eligible SC couples buying an Executive Condominium (EC); income ceiling S$16,000/mth.

You cannot double-count: EHG and Family Grant are added together, but you must meet both eligibility criteria separately. Grants are disbursed into your CPF Ordinary Account and reduce your outstanding loan accordingly.

Effective date: All figures reflect the grant amounts in force as at 15 July 2026; check HDB’s website before committing.

What Are CPF Housing Grants, and Who Administers Them?

CPF Housing Grants are cash-equivalent subsidies administered by the Housing & Development Board (HDB) on behalf of the Singapore government. Unlike rebates that appear on your invoice, these grants are credited directly into your CPF Ordinary Account (OA) and applied to reduce the amount you need to borrow or pay out of pocket. They represent one of the most significant levers in Singapore’s housing affordability framework, enabling first-timer households to reduce the effective purchase price of an HDB flat by tens of thousands of dollars.

Since their introduction alongside the BTO scheme, CPF Housing Grants have been restructured multiple times. The landmark 2019 reform merged the Additional CPF Housing Grant (AHG) and Special CPF Housing Grant (SHG) into the single Enhanced CPF Housing Grant (EHG), covering incomes up to S$9,000 per month. A further expansion in 2023 raised the Family Grant cap for resale flats and extended PHG coverage. As of 2026, the framework comprises four distinct grants — EHG, Family Grant, Singles Grant, and PHG — which can be combined subject to eligibility.

Figure 1: Maximum CPF Housing Grant amounts by buyer profile. SC = Singapore Citizen; SPR = Singapore Permanent Resident. Source: HDB.gov.sg 2026.

The Enhanced CPF Housing Grant (EHG): Singapore’s Core Affordability Tool

The EHG is the primary income-tested grant for first-timer households. It replaced the AHG and SHG from September 2019 and applies to both BTO and resale flats, removing the prior restriction that pegged larger grants exclusively to BTO purchases. The key parameters in 2026 are:

Maximum grant: S$80,000 for eligible SC couples.

Income ceiling: Average gross monthly household income of S$9,000 or below for couples; S$4,500 for singles.

Citizenship requirement: At least one Singapore Citizen among the buyers; the other applicant may be an SC or SPR.

Flat type: All HDB flat types from 2-Room Flexi upwards; also available for EC purchases under certain conditions.

Property bar: Neither applicant may own any private residential property, locally or overseas, at the time of application.

First-timer status: Both applicants must be first-timers (no prior HDB grant received, no prior subsidised flat sold without resale levy).

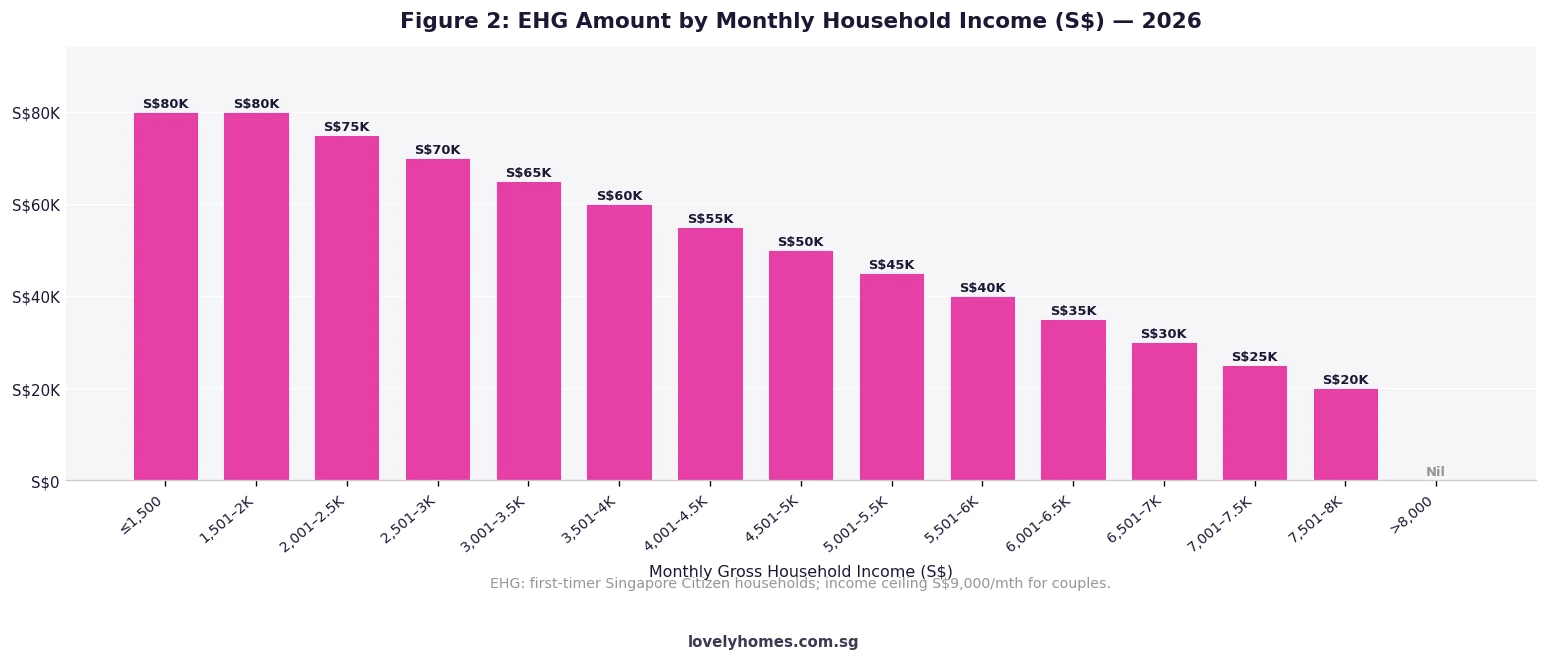

The EHG is structured in income bands: households earning S$1,500 per month or below receive the full S$80,000; those earning just under the S$9,000 ceiling receive S$5,000. Each band steps down by S$5,000 for every S$500 increase in income. Households earning S$9,001 or above receive nothing. Critically, EHG is computed on the average monthly income over the past 12 months — a point that catches some buyers off-guard when a recent pay rise pushes them over the ceiling retroactively.

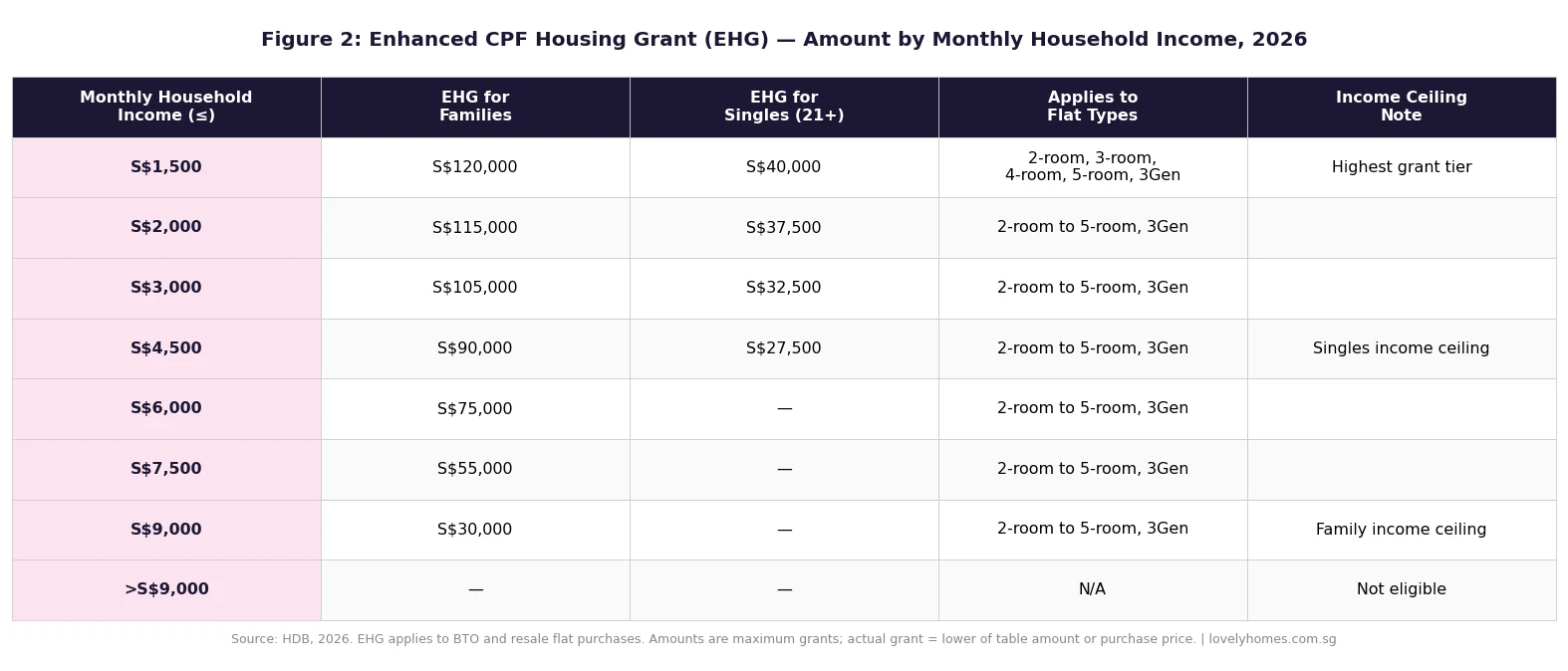

Figure 2: EHG grant amount by monthly gross household income bracket. The grant steps down by S$5,000 for each S$500 income band above S$1,500/mth, reaching zero for incomes above S$9,000/mth. Source: HDB.gov.sg 2026.

Family Grant and Singles Grant: Boosting Resale Affordability

The Family Grant is available to first-timer families buying a resale HDB flat. Unlike the EHG, it is a flat sum that does not taper with income, though the household must still fall below the S$9,000 monthly income ceiling. For 2026:

Buyer Profile

3-Room or Smaller

4-Room or Larger

SC + SC couple (first-timer)

S$50,000

S$40,000

SC + SPR couple (first-timer)

S$30,000

S$25,000

SC single (35+, first-timer)

S$25,000 (Singles Grant)

S$20,000 (Singles Grant)

The Singles Grant operates on identical mechanics to the Family Grant but is specifically for unmarried Singapore Citizens aged 35 years and above, or widowed/divorced Singapore Citizens with no prior grant history. Singles may receive up to S$25,000 for a resale flat of 3-rooms or smaller and S$20,000 for a 4-room or larger unit. Note that singles buying a BTO flat are generally limited to 2-Room Flexi units at non-mature estates — a structural restriction that has been progressively relaxed since the 2023 housing reforms.

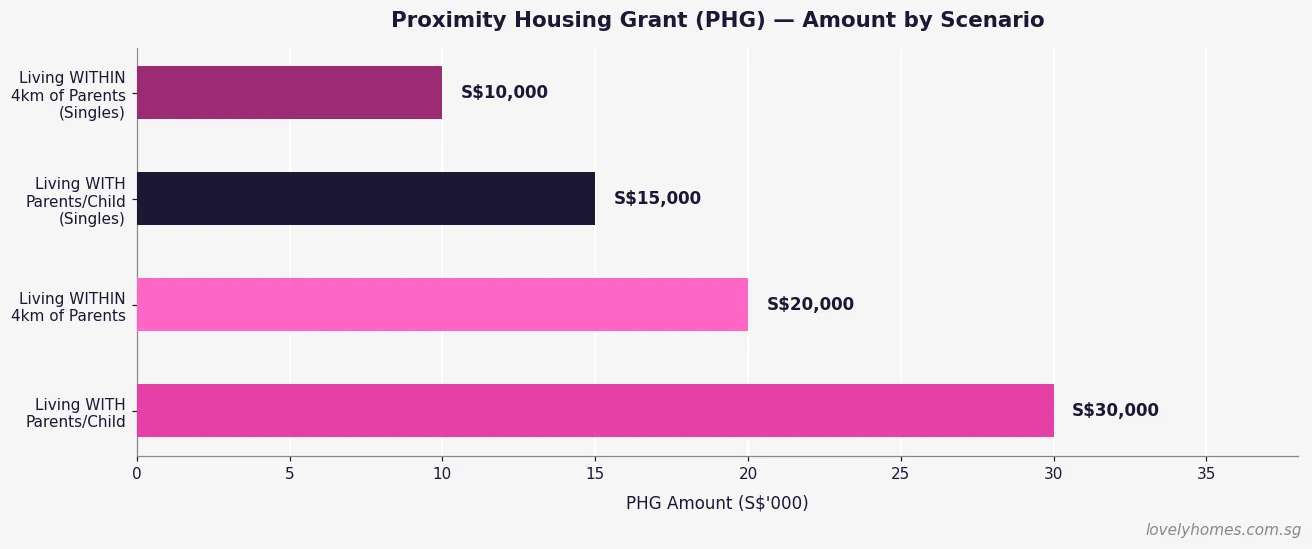

Proximity Housing Grant (PHG): Living Closer to Family

The Proximity Housing Grant was introduced in August 2015 to incentivise multi-generational proximity in public housing. In 2026, its parameters are:

S$30,000: For SC households buying a resale flat within 4 km of parents’ or married child’s current HDB flat or private residential property.

S$20,000: For SC households buying to co-reside in the same resale flat as parents or married child.

Income ceiling: S$14,000 per month for the buying household (higher than EHG/Family Grant).

Citizenship: At least one Singapore Citizen in the buying family nucleus.

No BTO eligibility: PHG applies exclusively to resale transactions. BTO applicants who wish to live near family should note this distinction when weighing BTO versus resale.

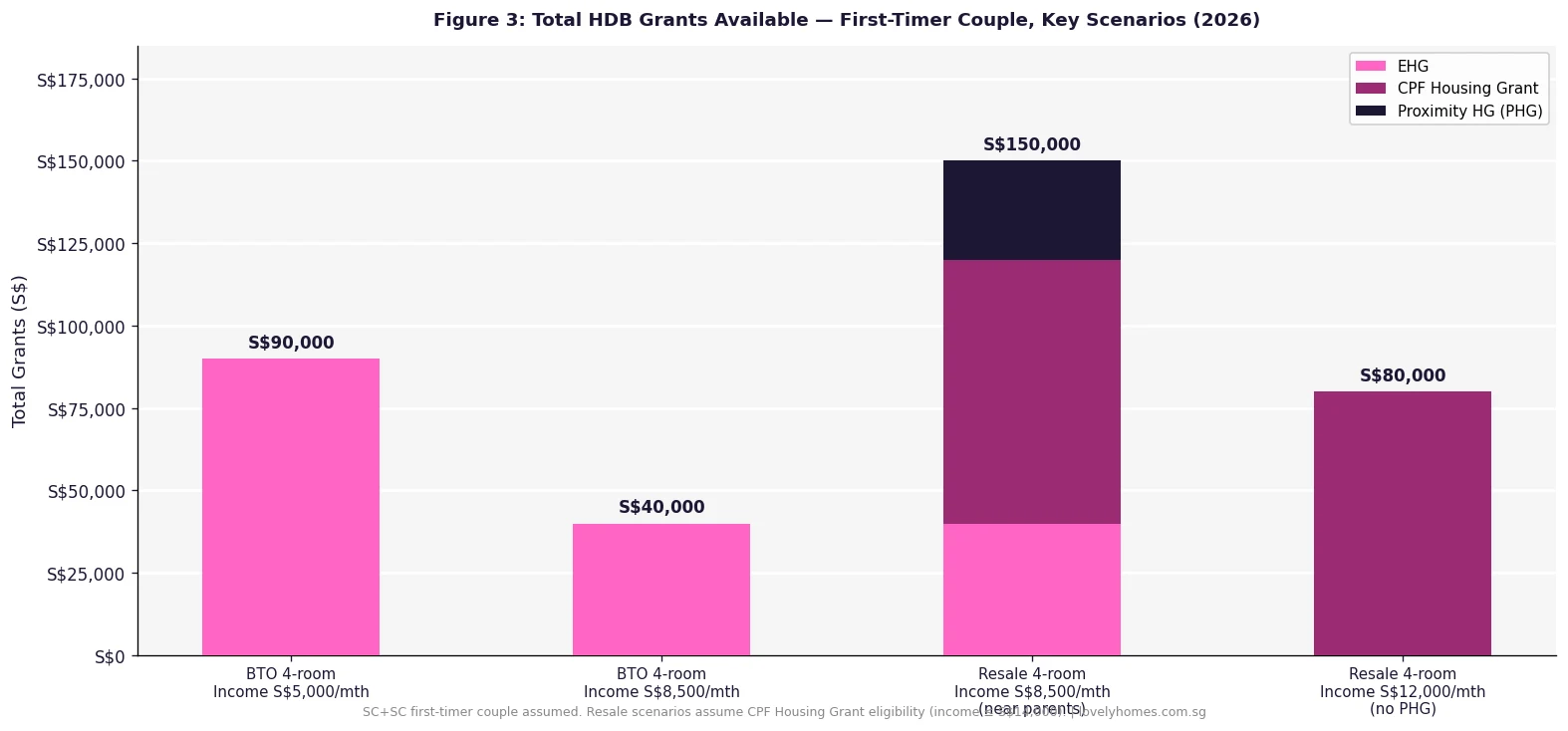

The PHG is stackable with the EHG and Family Grant, meaning an eligible SC couple buying a resale flat near their parents could potentially accumulate EHG (up to S$80K) + Family Grant (up to S$50K) + PHG (S$30K) = S$160,000 total. This scenario requires the household income to be S$9,000 or below (for the EHG and Family Grant components) and within 4 km of qualifying family (for PHG).

CPF Housing Grants for Executive Condominiums

Executive Condominiums (ECs) are a hybrid public-private housing type, and they carry their own grant structure. As of 2026:

CPF Housing Grant (Family Grant, EC tranche): Up to S$30,000 for SC+SC first-timer families; S$20,000 for SC+SPR first-timer families.

Income ceiling for EC grants: S$16,000 per month (higher than HDB flat grants).

EHG does not apply to new EC purchases from developers; EHG is only available for HDB flats.

Resale EC: Once an EC has been privatised (10 years from TOP), it is treated as a private property. No CPF Housing Grants apply to privatised EC resale transactions.

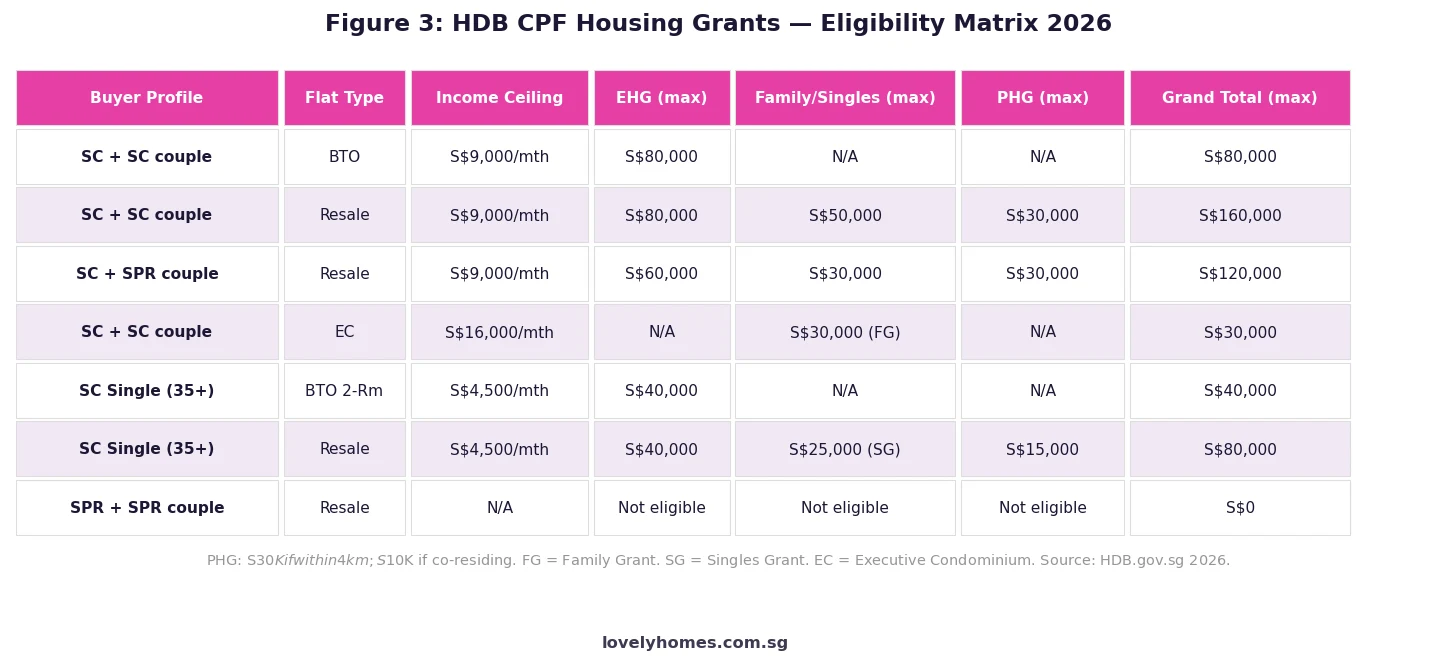

Figure 3: HDB CPF Housing Grants eligibility matrix by buyer profile, flat type, and income ceiling. Source: HDB.gov.sg 2026.

How Grants Are Disbursed: The CPF Mechanics

A common point of confusion is that CPF Housing Grants are not cash you receive at completion. Instead, they are credited to your CPF Ordinary Account before or at the point of purchase and immediately applied to reduce your housing outlay. In practice:

HDB confirms your grant eligibility after your application is approved.

The grant amount is credited into the primary applicant’s CPF OA.

At the point of HDB loan drawdown or mortgage completion, the grant reduces the amount you must borrow.

If you later sell the flat, the grant principal (without accrued interest) is returned to your CPF OA. Unlike regular CPF OA usage, no accrued interest is charged on the grant portion returned to CPF — only the original grant quantum is repaid to CPF upon sale.

This CPF-return mechanic is an important consideration when computing net cash proceeds on a future sale. While the grant reduces your upfront cost, it creates a future CPF refund obligation that reduces the cash you pocket when you eventually sell.

Summary: Grant Combinations at a Glance

Buyer Profile

Flat Type

EHG (max)

Family/Singles (max)

PHG (max)

Grand Total (max)

SC + SC (1st-timer couple)

BTO

S$80,000

N/A

N/A

S$80,000

SC + SC (1st-timer couple)

Resale

S$80,000

S$50,000

S$30,000

S$160,000

SC + SPR (1st-timer couple)

Resale

S$60,000

S$30,000

S$30,000

S$120,000

SC + SC (1st-timer couple)

EC (new)

N/A

S$30,000

N/A

S$30,000

SC Single (35+, 1st-timer)

BTO 2-Rm

S$40,000

N/A

N/A

S$40,000

SC Single (35+, 1st-timer)

Resale

S$40,000

S$25,000

S$15,000

S$80,000

SPR + SPR couple

Any HDB

Nil

Nil

Nil

S$0

Worked Example: How the Grants Stack for a Real Buyer

📝 Case Study: The Wong Family, SC + SC, Monthly Income S$6,800

Profile: Mr and Mrs Wong, both Singapore Citizens, both first-timers. Monthly gross household income S$6,800. They are buying a 4-room resale HDB flat in Tampines near Mrs Wong’s parents (within 2.5 km).

Purchase price: S$580,000

EHG: S$6,800 gross income → grant table gives S$45,000 (income band S$6,501–S$7,000).

Family Grant (4-room resale, SC+SC):S$40,000.

PHG (within 4 km of parents):S$30,000.

Total grants: S$45,000 + S$40,000 + S$30,000 = S$115,000, credited to CPF OA before completion.

Effective purchase calculation:

Purchase price: S$580,000

Less grants applied: −S$115,000

Effective cost to fund: S$465,000

HDB loan (80% LTV on S$465,000): S$372,000 @2.60% p.a., 25 years → monthly instalment S$1,683

Cash upfront (5% option fee not covered by CPF): S$29,000

Net effect: The S$115,000 in grants effectively reduces the monthly instalment from S$2,235 (without grants, full loan on S$580K) to S$1,683 — a saving of S$552 per month, or S$165,600 over a 25-year loan at comparable rates.

Why CPF Housing Grants Matter for Singapore’s Housing Equation

Singapore’s public housing system is internationally praised as one of the few in which the majority of residents own their own homes. As of 2026, roughly 80% of Singapore citizens live in HDB flats, and about 90% of those residents own their unit. CPF Housing Grants are a central reason why homeownership remains attainable despite property prices that would otherwise appear formidable for median-income households.

For context: a 4-room BTO flat in a non-mature estate now launches at roughly S$380,000–S$500,000. A comparable unit in the private market in the same region would cost S$1.2M–S$1.6M. The combination of subsidised land cost (via HDB pricing below market), income-tested grants (EHG), and the availability of 30-year HDB loans at preferential rates (the CPF OA interest rate of 2.6%) means that a couple earning the median household income can service a BTO mortgage for a fraction of what private homeownership would cost.

The grants also serve as a redistributive mechanism: the EHG is explicitly income-tested and skewed towards lower-income households. A couple earning S$2,500/mth gets S$75,000 more than a couple earning S$8,500/mth for the same flat. This income-sensitive structure is a deliberate policy choice by the Ministry of National Development (MND) and HDB to ensure that public housing subsidies accrue proportionately to those who need them most.

What Might Come Next: Policy Watch 2026–2027

Note: the following reflects informed analysis, not confirmed policy. Several developments in the pipeline could affect CPF Housing Grants:

October 2026 BTO launch: HDB is expected to release close to 8,000 units in the October 2026 exercise, including the first BTO flats under the expanded Prime, Plus and Standard classification framework. Grant eligibility under the new classification — especially for Plus flats, which carry tighter resale conditions — will be clarified in the launch materials.

EHG income ceiling review: With median household income rising and the cost of living increasing, there is industry speculation that the EHG income ceiling of S$9,000 per month (unchanged since the 2019 restructuring) may be reviewed in the 2026 or 2027 Budget. An upward revision to S$10,000 or S$11,000 would extend subsidy access to a wider band of middle-income households.

Grant portability for right-sizers: As Singapore’s population ages, there is increasing pressure to extend targeted subsidies to seniors downsizing from larger flats to 2-Room Flexi units. The Senior Priority Scheme and Move-In Priority Scheme already offer indirect advantages; a specific grant for right-sizing seniors has been discussed but not yet formalised as of mid-2026.

Can I receive CPF Housing Grants if my spouse is a Singapore Permanent Resident (SPR)?

Yes, but with reduced grant amounts. A Singapore Citizen buying a resale flat with an SPR spouse can receive an EHG of up to S$60,000 (vs S$80,000 for SC+SC couples) and a Family Grant of up to S$30,000 (vs S$50,000). Both applicants must be first-timers and the household income must not exceed S$9,000 per month. The PHG is also available at the same quantum (S$30,000) as for SC+SC couples, provided the proximity requirement is met.

I received a CPF Housing Grant for a previous flat. Can I get another grant for my next purchase?

Generally, no — CPF Housing Grants (EHG, Family Grant, Singles Grant, PHG) are available to first-timers only. If you previously received a grant and sold the flat, you are classified as a second-timer. Second-timers are not eligible for EHG, Family Grant, or Singles Grant when buying their next flat. The PHG is an exception: it may be available to second-timer SC households buying a resale flat near their parents or children, subject to a lower ceiling (S$15,000 within 4 km, S$5,000 for co-residing). Additionally, if a resale levy applies to your next purchase, the levy amount is in most cases higher than any grant you might receive, effectively making grants moot for most second-timer resale purchases.

Can I use CPF Housing Grants towards the option fee or stamp duty?

CPF Housing Grants are credited to your CPF Ordinary Account and are not available as cash. They cannot be used for the Option to Purchase (OTP) exercise fee, which must be paid in cash. However, once the grant is in your CPF OA, it can be used to pay the Buyer’s Stamp Duty (BSD) and the mortgage downpayment (subject to the Valuation Limit and Withdrawal Limit). In practice, the grant effectively reduces the CPF OA portion of your overall transaction cost, increasing the residual balance available for other CPF-eligible expenses.

Does my overseas property disqualify me from receiving HDB grants?

Yes. HDB’s eligibility criteria for CPF Housing Grants require that neither the applicant nor any co-applicant owns or has disposed of any private residential property (including overseas properties) within 30 months before the flat application date. If you owned an overseas property and sold it, you must wait at least 30 months before applying. Undisclosed overseas property ownership is a statutory breach and can result in grant clawback plus penalties under the Housing & Development Act.

When I sell the flat, do I repay the grant to HDB or to CPF?

The grant is returned to CPF, not to HDB. Specifically, the original grant quantum (without accrued interest) is refunded to your CPF OA upon sale. This is different from regular CPF OA usage, where you must refund the principal plus accrued interest at 2.5% per annum. The no-interest feature of grant repayment is favourable: for a S$50,000 grant held for 20 years, you repay exactly S$50,000 to CPF rather than S$83,000 (which would apply if ordinary CPF interest accrual rules applied). Any cash proceeds above CPF refunds and outstanding loans are yours to keep.

Can a divorced or widowed Singapore Citizen get any HDB grants?

Yes. A divorced or widowed SC who has not previously received a CPF Housing Grant is treated as a first-timer for grant purposes (though not always for flat-type eligibility). Depending on age and circumstances: if aged 35 and above, the SC can apply for a 2-Room Flexi BTO (with EHG up to S$40,000) or a resale flat (with EHG + Singles Grant + PHG, up to S$80,000 in total). If the individual has a child and thus forms a family nucleus, they may be eligible for family-size flats and the full suite of family-tier grants, subject to income criteria.

Do EHG and Family Grant count towards my CPF Withdrawal Limit?

No. CPF Housing Grants do not count towards the Valuation Limit (VL) or Withdrawal Limit (WL) applicable to CPF usage for housing. The VL is capped at the property’s value, and the WL is capped at 120% of the VL for private properties. Grants are credited to your OA and can be applied without reference to these limits, which means the grant effectively gives you additional CPF headroom beyond the standard withdrawal cap. This is a meaningful benefit when buying an older or lower-valued resale flat where the WL might otherwise restrict CPF usage.

Disclaimer: This article is for general informational and educational purposes only. Grant amounts, income ceilings, eligibility criteria and application procedures are set by the Housing & Development Board (HDB) and may be revised without notice. Before committing to any property purchase, verify current grant parameters directly with HDB at hdb.gov.sg, consult a licensed conveyancing solicitor, and seek independent financial advice from a licensed financial adviser. LovelyHomes is not a licensed property agent or financial adviser and nothing in this article constitutes financial, legal or property advice.

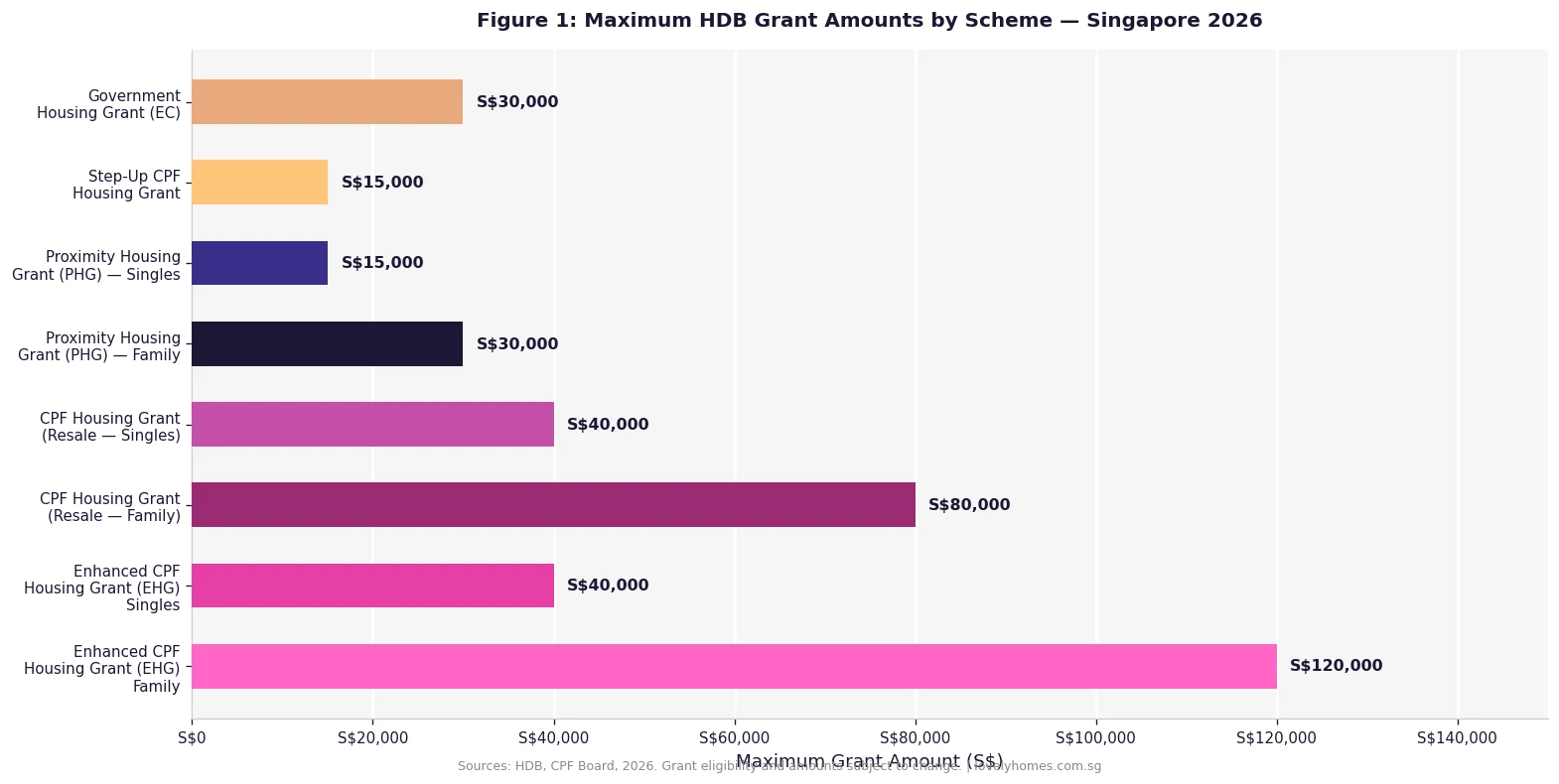

Enhanced CPF Housing Grant (EHG): Up to S$120,000 for eligible first-timer families; up to S$40,000 for eligible singles. Applies to both BTO and resale flats.

CPF Housing Grant (CHG): Up to S$80,000 for first-timer families buying a resale HDB flat; S$40,000 for singles.

Proximity Housing Grant (PHG): Up to S$30,000 for families who buy a resale flat to live with or near parents; S$15,000 for singles.

Step-Up CPF Housing Grant: S$15,000 for second-timer families upgrading from a 2-room to a 3-room or larger flat in a non-mature estate.

Government Housing Grant (EC): S$30,000 for eligible first-timer families buying a new Executive Condominium.

Grants are CPF-credited: All grants go into your CPF Ordinary Account and offset the purchase price — you do not receive cash.

No double-counting: You can stack compatible grants (e.g., EHG + PHG for resale) but each grant type can only be used once per application.

What Are HDB Grants and Who Administers Them?

HDB housing grants are government subsidies administered jointly by the Housing & Development Board (HDB) and the Central Provident Fund (CPF) Board. They are designed to make homeownership accessible to Singapore Citizens and, in some cases, Permanent Residents, by directly reducing the effective purchase price of an HDB flat.

Grants are credited into your CPF Ordinary Account (OA) — not paid as cash — and can be applied towards the purchase price of your flat or used to reduce your outstanding home loan. This is an important distinction: you cannot withdraw grant amounts in cash, and they are subject to the CPF accrued interest rules when you eventually sell your property.

The grant framework in Singapore is tiered by household income, citizenship status, flat type, and whether you are a first-timer or second-timer applicant. First-timers consistently receive significantly higher grants than second-timers, reflecting the government’s policy of prioritising owner-occupancy and discouraging property speculation within the public housing segment.

Figure 1: Maximum grant amounts across all HDB and EC grant schemes as at 2026. Subject to individual eligibility — verify with HDB/CPF Board before purchase.

Enhanced CPF Housing Grant (EHG) — The Largest Grant Available

The Enhanced CPF Housing Grant, introduced in September 2019, replaced the Additional CPF Housing Grant (AHG) and Special CPF Housing Grant (SHG). It is the most substantial grant available to first-timer Singapore Citizen households and is specifically calibrated to assist lower- and middle-income buyers.

The EHG is means-tested: the amount decreases as household income rises, and the eligibility ceiling is S$9,000 per month for families and S$4,500 per month for singles (as at 2026). To qualify, at least one applicant must have worked continuously for at least twelve months before the flat application date, and must continue working at the time of application.

One critical requirement that catches many applicants off-guard: the EHG is only available for flats purchased with a remaining lease of at least 20 years at the time of application, and whose remaining lease can cover the youngest buyer to at least age 95. This lease requirement affects certain older resale flats, which may otherwise be eligible by income but fail the lease longevity test.

Figure 2: EHG grant amounts by monthly household income bracket, 2026. Grants are maximum amounts; actual award = lower of EHG table amount or flat purchase price.

CPF Housing Grant (CHG) — For Resale Flat Buyers

The CPF Housing Grant (sometimes called the Family Grant or Singles Grant in older HDB materials) is specifically available to first-timer buyers purchasing a resale HDB flat on the open market. Unlike the EHG, which applies to both BTO and resale purchases, the CHG is resale-only — BTO buyers receive the EHG instead.

As at 2026, the maximum CHG is S$80,000 for first-timer Singapore Citizen families (where both applicants are Singapore Citizens) and S$40,000 for first-timer Singles aged 35 or above. For households where one applicant is a Singapore Citizen and the other is a Permanent Resident, the grant reduces to S$50,000. The income ceiling for the CHG is S$14,000 per month — notably higher than the EHG ceiling, meaning more households are eligible.

Proximity Housing Grant (PHG) — For Families Buying Near Parents

The Proximity Housing Grant incentivises multigenerational living by rewarding families who buy a resale HDB flat to live with or within 4 kilometres of their parents’ or children’s existing HDB flat. It is a resale-only grant and is available regardless of whether the buyer is a first-timer or second-timer, making it one of the few grants accessible to second-timers on a meaningful scale.

To live with parents or married children (same address), the PHG is S$30,000 for families and S$15,000 for singles. To live within 4 km of parents’ or children’s existing flat, the PHG is S$20,000 for families and S$10,000 for singles. There is no income ceiling for the PHG — any household, regardless of income, may apply as long as the proximity and family relationship conditions are met.

The PHG can be stacked with the EHG and CPF Housing Grant for resale buyers. A first-timer SC+SC couple earning S$8,500 per month buying a resale flat to live near parents could, in theory, receive EHG of S$40,000 + CHG of S$80,000 + PHG of S$30,000 = a total of S$150,000 in grants — making a resale flat in a mature estate substantially more affordable than it appears at headline price.

Step-Up CPF Housing Grant — Second-Timers Upgrading Within HDB

The Step-Up CPF Housing Grant of S$15,000 is specifically for second-timer Singapore Citizen families who currently live in a 2-room HDB flat (Flexi or standard) and wish to upgrade to a larger 3-room or bigger flat in a non-mature housing estate, sourced directly from HDB (i.e., a BTO flat in the relevant sales exercise). It is not available for resale flat purchases.

The income ceiling for the Step-Up Grant is S$7,000 per month, and at least one applicant must have been a Singapore Citizen for at least five years. This grant is deliberately narrow in scope — it targets a specific population of residents in smaller flats who need a capacity upgrade but remain in the lower-to-middle income band.

Government Housing Grant (GHG) for Executive Condominiums

First-timer Singapore Citizen families purchasing a new Executive Condominium (EC) directly from a developer are eligible for the Government Housing Grant of S$30,000, credited into the purchaser’s CPF OA. The income ceiling for the EC grant is the same as the EC purchase income ceiling — S$16,000 per month as at 2026. This grant cannot be combined with the EHG or CHG, as those apply only to HDB flat purchases; the GHG is the equivalent grant mechanism for the EC segment.

Figure 3: Total grants available across key first-timer scenarios, 2026. Scenario 3 (resale near parents) shows maximum stacking of EHG + CHG + PHG = S$150,000.

Summary: Grant Comparison Table

Grant

Max (Family)

Max (Singles)

Income Ceiling

BTO?

Resale?

First-Timer?

EHG

S$120,000

S$40,000

S$9,000 / S$4,500

✅

✅

Required

CPF Housing Grant

S$80,000

S$40,000

S$14,000

❌

✅

Required

PHG (live with)

S$30,000

S$15,000

None

❌

✅

Not required

PHG (within 4km)

S$20,000

S$10,000

None

❌

✅

Not required

Step-Up Grant

S$15,000

—

S$7,000

✅

❌

Not required

Govt HG (EC)

S$30,000

—

S$16,000

EC only

❌

Required

Worked Example: The Lim Family — Maximising HDB Grants on a Resale Flat

Mr and Mrs Lim are a Singapore Citizen married couple, both aged 29. Their combined gross monthly household income is S$6,500. They are first-timers. Mrs Lim’s parents own an HDB flat in Queenstown, and the couple would like to buy a resale 4-room flat in Buona Vista to live together with the parents.

Step 1 — EHG eligibility: Income S$6,500 → EHG for families at this income bracket = S$75,000. (From the EHG tier table: ≤S$7,500/mth = S$55,000. Correcting: S$6,000–S$7,500 range → S$55,000 EHG.)

Step 2 — CPF Housing Grant (resale): Income S$6,500 ≤ S$14,000 → CHG = S$80,000 (both SCs, first-timers, resale flat).

Step 3 — PHG (living with parents): Living with parents at same address → PHG = S$30,000. No income ceiling.

Step 4 — Total grants:

Grant

Amount

Enhanced CPF Housing Grant (EHG)

S$55,000

CPF Housing Grant (CHG)

S$80,000

Proximity Housing Grant (PHG — live with parents)

S$30,000

Total Grants (CPF OA credited)

S$165,000

Indicative resale flat price (Buona Vista 4-room)

S$780,000

Effective price after grants

S$615,000

HDB Concessionary Loan (80% of S$780k − grants offset)

~S$459,000

Cash + CPF down payment (20%)

~S$156,000

The Lims’ S$165,000 in grants reduces a S$780,000 resale flat to an effective out-of-pocket position requiring approximately S$156,000 in down payment (cash + CPF, with grants credited to OA first). Their HDB Concessionary Loan at 2.6% p.a. on approximately S$459,000 produces a monthly repayment of roughly S$2,060 — a MSR-compliant 31.7% of their S$6,500 combined income, below the 30% MSR cap when rounded down on the concessionary loan basis (HDB concessionary loan MSR = 30% of gross monthly income).

Note: CPF accrued interest will apply to the grants and CPF OA amounts used, payable upon eventual sale of the flat. The Lims should factor this into their long-term financial planning.

Why HDB Grants Matter in Singapore’s Property Market

Singapore’s HDB grant system is one of the most comprehensive public housing subsidy frameworks in the world. Unlike many countries where housing subsidies take the form of direct cash payments or tax credits, Singapore’s approach links grants directly to the CPF system and the property purchase process — ensuring subsidies are deployed towards asset acquisition rather than consumption spending.

For first-timer households earning S$6,000–S$8,000 per month — the Singapore median household income bracket — the combined effect of EHG, CHG, and PHG can reduce the effective purchase price of a resale flat by S$100,000 to S$165,000. On a S$600,000–S$800,000 resale flat, this represents a 15–25% effective discount, which is transformative for affordability.

The grant structure also reveals HDB’s policy priorities clearly: it heavily favours first-timers over second-timers, rewards proximity to elderly parents, and calibrates generosity inversely to income. Buyers who understand this structure can make significantly better purchase decisions — for example, choosing a resale flat with PHG eligibility over a BTO flat, purely because the grant stacking arithmetic makes the resale option more affordable net of grants.

What Might Come Next

The Singapore government reviews HDB grant parameters periodically, typically in line with National Day Rally announcements or budget statements. The most recent significant change was the introduction of the EHG in 2019 and the progressive upward revision of resale grant amounts in 2023. Given the ongoing focus on housing affordability — and the political salience of the HDB resale market — further adjustments to grant ceilings or income thresholds cannot be ruled out ahead of the next general election cycle. Buyers currently in the planning phase should check for the most current figures on the official HDB website before committing to a purchase.

Frequently Asked Questions

Can I receive grants as cash instead of CPF?

No. All HDB housing grants — EHG, CPF Housing Grant, PHG, Step-Up, and the Government Housing Grant for ECs — are credited directly into your CPF Ordinary Account. You cannot receive them as cash and you cannot use them for renovation or any purpose other than the property purchase. When you eventually sell the flat, the grant amounts (plus CPF accrued interest at 2.5% per annum) must be refunded to your CPF OA.

Do Singapore Permanent Residents qualify for HDB grants?

PRs have limited access to HDB grants. A PR who is part of an SC-PR couple applying for a resale flat may be eligible for a reduced CPF Housing Grant (S$50,000 for SC+PR families versus S$80,000 for SC+SC families). The EHG is only available where at least one applicant is a Singapore Citizen. The PHG and Step-Up Grant require at least one Singapore Citizen applicant. PRs applying as singles (single-nucleus PR household) are generally not eligible for HDB grants.

What is the difference between a first-timer and a second-timer?

A first-timer is a Singapore Citizen who has not previously received any HDB housing subsidy — meaning they have never owned an HDB flat bought directly from HDB, received a CPF Housing Grant, or been listed as an occupier of a subsidised flat that subsequently received a grant. A second-timer is anyone who has previously received an HDB housing subsidy. First-timers receive substantially higher grants and priority balloting across BTO exercises.

Can I use grants for the down payment?

Grants are credited to your CPF OA, which can then be used for the CPF-eligible portion of the down payment. For an HDB Concessionary Loan, the minimum cash down payment is 10% of the purchase price; the remaining 10% can be funded from CPF (including grants credited to CPF OA). For a bank loan, the cash down payment is 5% and the next 20% can be from CPF. So yes — grants effectively reduce the CPF component you need to contribute from your own savings, improving cash affordability.

What happens to grants when I sell my HDB flat?

When you sell your HDB flat, the total grant amount received — plus CPF accrued interest at 2.5% per annum compounded from the date of purchase — must be returned to your CPF OA. This is not a penalty; the accrued interest compensates for the fact that the grant money was in your CPF OA earning interest that was “diverted” to your flat purchase. The refunded amount forms part of your CPF savings and can be used for your next property purchase, subject to the applicable rules.

Do HDB grants affect how much I can borrow?

Not directly — grants do not increase your borrowing capacity, as loan quantum is determined by your income, credit profile, TDSR, and MSR (for HDB loans). However, grants reduce the effective purchase price, which means the loan quantum required to complete the purchase is lower. A lower loan quantum means lower monthly repayments, which in turn may make a higher-priced flat MSR/TDSR-compliant that would otherwise breach the borrowing limit.

Can grants be used to buy private property?

No. HDB housing grants — EHG, CHG, PHG, and Step-Up Grant — can only be used to purchase HDB flats (for BTO or resale). The Government Housing Grant can be used for EC purchases. None of these grants may be applied to the purchase of a fully private condominium, landed property, or commercial property. If you use grants to purchase an HDB flat and subsequently sell it to buy private property, the grant amounts plus accrued interest must first be refunded to your CPF OA.

Disclaimer: This article is for general informational purposes only and does not constitute financial or legal advice. HDB grant amounts, eligibility criteria, and income ceilings are subject to change by HDB and CPF Board at any time. Readers are strongly advised to verify current grant parameters directly with HDB at www.hdb.gov.sg, the CPF Board at www.cpf.gov.sg, and to consult a licensed financial adviser before making any property purchase decision.

First-timer families can receive up to S$80,000 in Enhanced CPF Housing Grant (EHG) for BTO or resale flats (household income ≤ S$9,000/month).

Singles buying a 2-Room Flexi BTO qualify for up to S$40,000 EHG (individual income ≤ S$4,500/month).

Resale buyers can stack the Family Grant (up to S$50,000) with the EHG and the Proximity Housing Grant (PHG, up to S$30,000) — potentially S$160,000 in total grants.

The PHG has no income ceiling and rewards buyers who live near or with parents or children.

All CPF grants go into your CPF Ordinary Account (OA) and are used against the purchase price — but they accrue interest that must be refunded upon sale.

Grants do not eliminate your cash component of the downpayment — at least 5% cash is still required for bank loans.

Applications are via the HDB flat portal and must be completed before exercising the Option to Purchase (OTP).

What Are CPF Housing Grants and Who Administers Them?

CPF Housing Grants are direct subsidies paid by the Singapore Government into the buyer’s CPF Ordinary Account (OA) to help Singaporeans afford their first — and in some cases, second — HDB flat. They are administered jointly by the Housing & Development Board (HDB) and the Central Provident Fund Board (CPF Board), with eligibility rules updated periodically to reflect prevailing market conditions and government housing policy.

Unlike an ABSD remission or a bank subsidy, a CPF Housing Grant is a genuine cash transfer from the public purse into your CPF OA. It immediately reduces the amount you need to borrow or fund from savings, which lowers your monthly mortgage instalment. However, grants are not free in the accounting sense: when you eventually sell the flat, the grant amount — plus accrued interest at the CPF OA rate of 2.5% per annum — must be refunded back into your CPF OA. The net effect is deferred rather than eliminated cost.

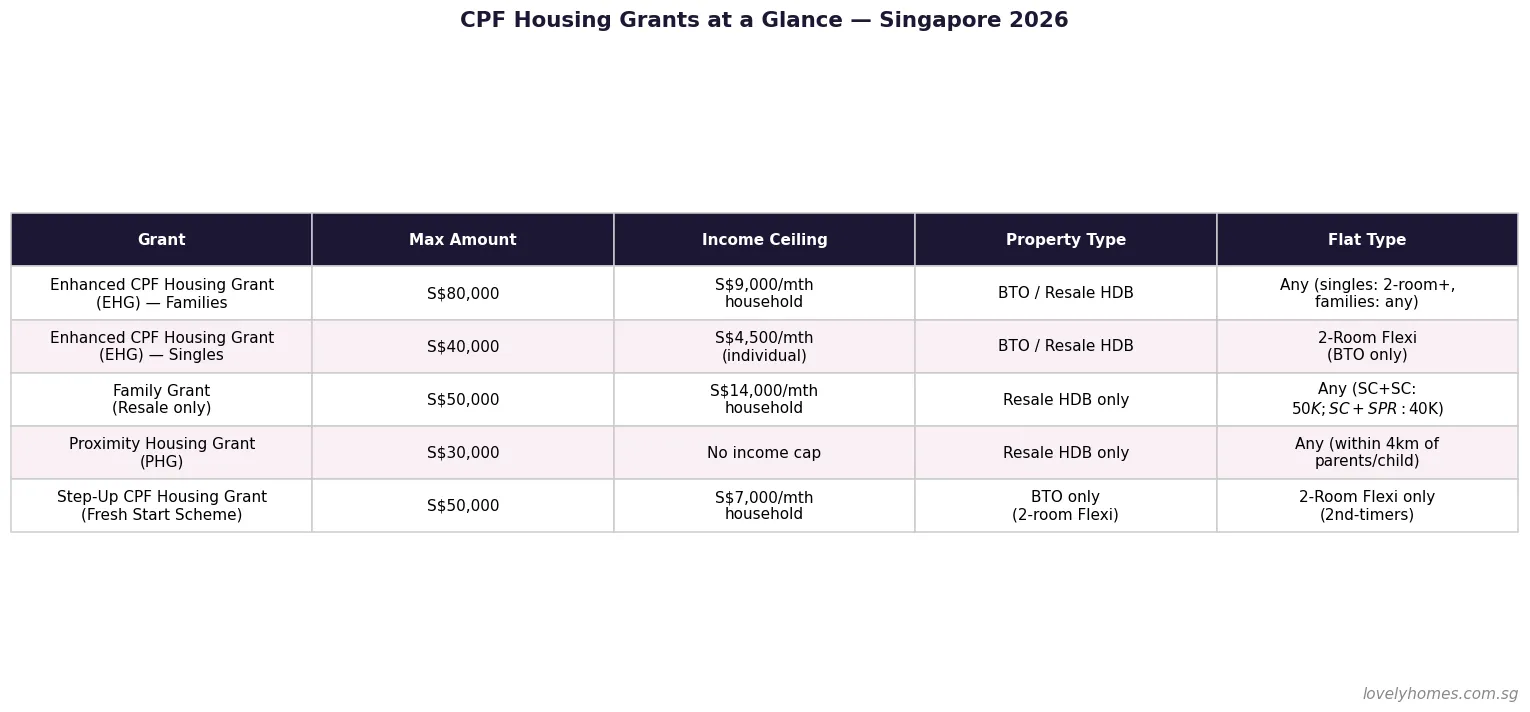

As of 26 April 2026, the key grant types in force are the Enhanced CPF Housing Grant (EHG), the Family Grant, the Proximity Housing Grant (PHG), and the Step-Up CPF Housing Grant for eligible second-timers under the Fresh Start Housing Scheme.

Enhanced CPF Housing Grant (EHG) — Rates and Eligibility

The Enhanced CPF Housing Grant, introduced in September 2019 to replace the Additional CPF Housing Grant (AHG) and Special CPF Housing Grant (SHG), is the flagship subsidy for first-timer buyers. It is progressive — the lower the household income, the higher the grant — and applies to both new BTO flats and resale HDB flats, making it more flexible than its predecessors.

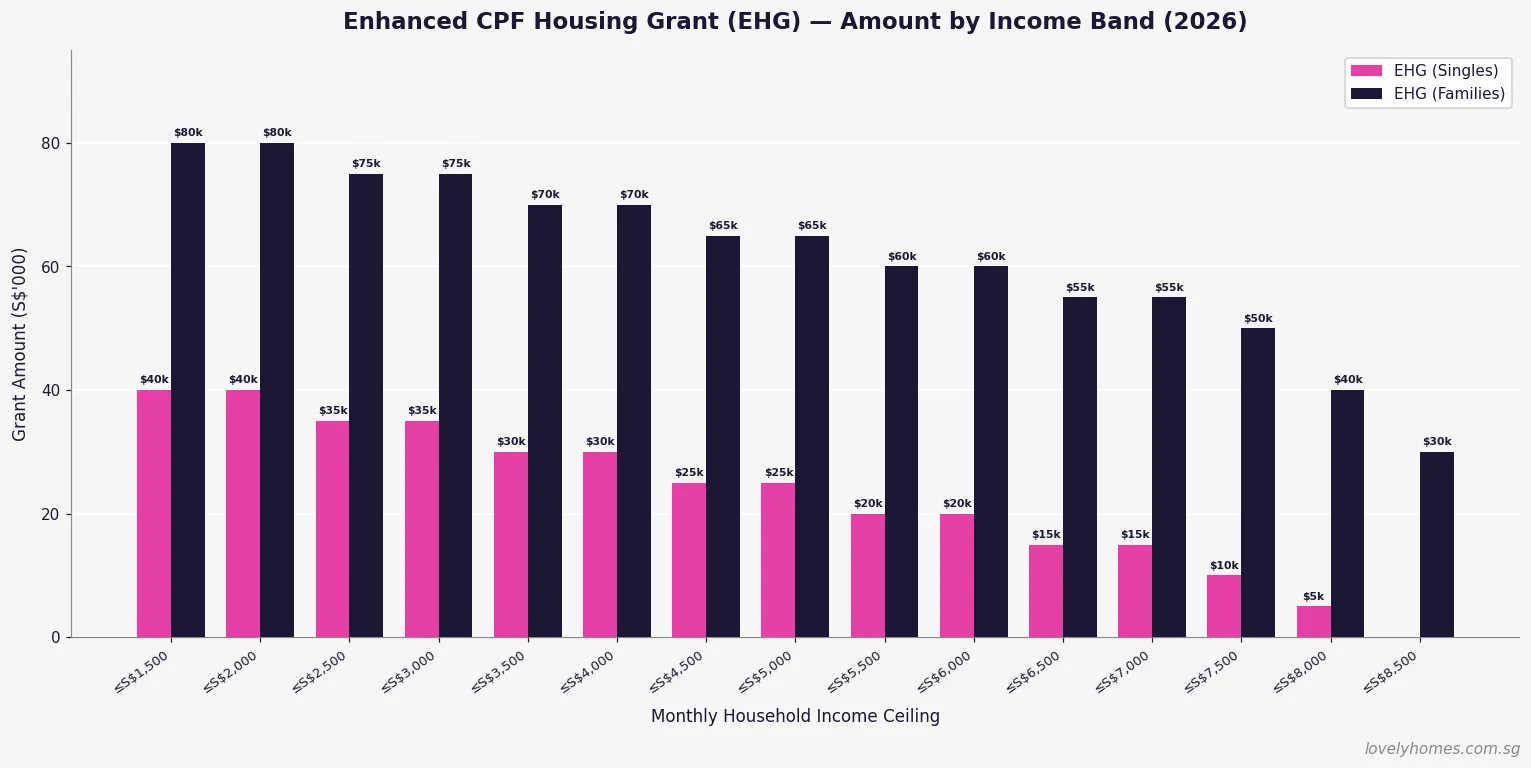

Figure 1: EHG amounts (S$’000) for singles vs families, by monthly household income band. Source: HDB (2026).

EHG for Families

For married or engaged couples — including those applying under the Fiancé/Fiancée Scheme — the EHG ranges from S$5,000 (household income ≤ S$8,000/month) to S$80,000 (household income ≤ S$1,500/month). The income assessed is the average gross monthly income of both applicants over the 12 months preceding the application. If the combined household income exceeds S$9,000/month, no EHG is payable.

EHG for Singles

First-timer singles aged 35 and above buying a 2-Room Flexi BTO flat in a non-mature estate qualify for EHG on a scaled basis, up to S$40,000 (individual income ≤ S$1,500/month). A single with income ≤ S$4,500/month qualifies for a minimum S$5,000 grant. Singles buying resale flats under the Single Singapore Citizen (SSC) scheme are also eligible, provided they purchase a 5-room flat or smaller.

Monthly Gross Income (Household)

EHG — Families

EHG — Singles

≤ S$1,500

S$80,000

S$40,000

≤ S$2,500

S$75,000

S$35,000

≤ S$3,500

S$70,000

S$30,000

≤ S$4,500

S$65,000

S$25,000

≤ S$5,500

S$60,000

S$20,000

≤ S$6,500

S$55,000

S$15,000

≤ S$7,500

S$50,000

S$10,000

≤ S$9,000

S$30,000–S$40,000

Not eligible

Family Grant — For Resale HDB Buyers

The Family Grant is available exclusively to buyers of resale HDB flats and is stackable on top of the EHG. It acknowledges that resale flat prices in many estates carry a premium over BTO prices, and provides an additional buffer for buyers who prefer a specific location or immediate occupancy over the BTO ballot process.

The Family Grant is administered by HDB and paid into the CPF OA of eligible applicants. Key parameters as of 2026:

SC + SC couple or family: S$50,000

SC + SPR couple or family: S$40,000

Singles (SSC scheme, resale 5-room or smaller): S$25,000

Income ceiling: S$14,000/month combined household income

Flat type restriction: any resale flat type; no restriction by town or estate

The S$14,000/month income ceiling makes the Family Grant accessible to many dual-income professional couples who earn too much for the EHG but still value the additional subsidy when purchasing resale.

Proximity Housing Grant (PHG) — Rewarding Family Ties

Introduced in August 2015, the Proximity Housing Grant is one of the most distinctive features of Singapore’s housing policy. It uses a direct cash subsidy to incentivise multi-generational proximity — encouraging adult children to live near, or with, their elderly parents. It applies only to resale HDB flats and has no income ceiling, meaning higher-earning buyers can benefit too.

Figure 3: PHG amounts by proximity scenario, for families and singles. Source: HDB (2026).

The PHG has four tiers based on whether you are buying as a family or single, and whether you are moving with parents or children (same household) or within 4 km of them:

Buyer Type

Living With Parents/Child

Living Within 4 km

Families (married/engaged couples)

S$30,000

S$20,000

Singles (SSC scheme)

S$15,000

S$10,000

The “living with” criterion requires the parent or child to be registered on the same flat as an occupier. The “within 4 km” criterion uses the straight-line distance between postal codes, verified at the point of application. The PHG is a one-time benefit — once received, it cannot be claimed again on a subsequent flat purchase.

Step-Up CPF Housing Grant — Fresh Start Scheme

The Step-Up CPF Housing Grant is a targeted measure for a specific group: second-timer applicants who previously owned a subsidised flat and now qualify for a second chance at affordable owner-occupied housing under HDB’s Fresh Start Housing Scheme, which was introduced in October 2016 and expanded over subsequent years.

Eligibility is tightly defined: second-timer families with at least one child aged under 16; monthly household income ≤ S$7,000; must apply for a 2-Room Flexi BTO flat; must not currently own a flat or private residential property; and must fulfil a 5-year Fresh Start Housing Scheme Minimum Occupation Period on the new flat. The grant amount is up to S$50,000. It is not stackable with the EHG.

CPF Housing Grants at a Glance — Summary Table

Figure 2: Summary of all CPF Housing Grant types — amounts, income ceilings, and eligible property types. Source: HDB / CPF Board (2026).

Worked Example — Maximum Grant Stack for a Resale Buyer

Scenario: SC + SC First-Timer Couple, Resale Flat Near Parents

Buyer profile: Mr and Mrs Tan — married, both Singapore Citizens, first-timer applicants. Combined monthly gross income: S$6,800. Mrs Tan’s parents reside in the same block as the resale flat they are purchasing in Ang Mo Kio.

EHG (family, income band S$6,500–S$7,500): S$50,000

Family Grant (SC + SC, resale): S$50,000

PHG (same block as parents = “living with”): S$30,000

Total grants: S$130,000

Purchase price: S$600,000 (4-Room resale, Ang Mo Kio) Effective net cost after grants: S$470,000 (before stamp duties and legal fees). BSD on S$600,000: approximately S$12,600. ABSD: Nil (first residential property, Singapore Citizen buyers). Legal / conveyancing fees: approximately S$2,500–S$4,000.

Taking an HDB concessionary loan at 90% LTV: loan = S$540,000 less S$130,000 grants = S$410,000 loan needed, reducing the monthly instalment significantly versus purchasing without grants.

The CPF Accrued Interest Rule — The Hidden Cost of Grants

Every dollar drawn from your CPF OA — including grant monies — accrues interest at the CPF OA rate (currently 2.5% per annum). When you sell the flat, the CPF Board requires you to refund the principal amount used (including grants) plus the hypothetical interest that amount would have earned in the OA. This refund is returned to your CPF OA — not the government — and is available for future use in retirement or a subsequent property purchase.

Practical implication: a S$80,000 EHG held for 10 years accrues approximately S$22,000–S$25,000 in interest (compounded at 2.5% p.a.), bringing the total CPF refund for the grant alone to roughly S$102,000–S$105,000. Plan for this when modelling net sale proceeds on exit. If the sale price is insufficient to cover the full CPF refund, you keep the shortfall — you are not personally liable to top up the difference.

Why CPF Housing Grants Matter for Singapore’s Property Market

CPF Housing Grants fulfil a dual function in Singapore’s property ecosystem. At the individual level, they represent one of the most powerful demand-side subsidies in the world — transferring significant public funds directly to low- and middle-income buyers to help them achieve owner-occupation without over-relying on private financing. At the market level, they compress effective pricing for first-timers in the HDB resale segment, sustaining affordability across economic cycles.

The 2019 introduction of the EHG deliberately raised the income ceiling to S$9,000/month (from S$6,000/month under the legacy AHG/SHG regime), reflecting the Government’s recognition that median household incomes had risen and the historical ceilings were excluding a growing segment of first-timers who genuinely needed assistance.

Compared with equivalent policies in Hong Kong — where the Home Ownership Scheme provides a flat discount on market price rather than a direct grant — or Australia, where the First Home Owner Grant is a modest flat sum, Singapore’s progressive, stackable grant framework is both more generous and more targeted to income need.

What Might Come Next — Grant Policy Outlook for 2026–2028

The CPF Housing Grant framework is reviewed periodically in tandem with BTO flat pricing and HDB resale indices. Three plausible near-term developments:

EHG income ceiling revision: With household income growth continuing, HDB may raise the S$9,000/month family ceiling to extend coverage to the lower-professional bracket — especially as Prime Location Public Housing (PLH) flat prices edge towards S$700,000–S$800,000 in central estates.

PHG extension to BTO buyers: Currently restricted to resale buyers, extending the PHG to BTO buyers in family-friendly towns like Tengah and Bidadari has been discussed in policy circles, though not confirmed as of this date.

Grant indexing to flat type or BTO pricing band: A flat S$80,000 EHG ceiling becomes proportionally less meaningful as PLH BTO prices climb. Grant amounts indexed to flat type could better reflect affordability gaps across different segments.

These are speculative. Always verify current grant levels at the HDB Grant Eligibility page before exercising any OTP.

Frequently Asked Questions

Can I use CPF Housing Grants towards the downpayment?

Grants are credited into your CPF OA and can be applied in the same way as your own CPF savings — towards the downpayment, the purchase price, and stamp duties (BSD). However, if you are taking a bank loan, the minimum 5% cash downpayment must be paid in cash; CPF (including grants) cannot cover this component. If you are taking an HDB concessionary loan, there is no mandatory cash component, so grants can fully offset the downpayment requirement alongside your other CPF OA balance.

Can both the EHG and Family Grant be claimed for the same resale flat purchase?

Yes. For resale flat purchases, a first-timer SC couple can claim both the EHG and the Family Grant simultaneously, provided they meet the eligibility criteria for each. If the couple also qualifies for the PHG — for example, buying near parents — that can be added on top. The theoretical maximum for an SC + SC couple buying resale is S$80,000 (EHG) + S$50,000 (Family) + S$30,000 (PHG living-with) = S$160,000, though achieving the maximum EHG requires a household income ≤ S$1,500/month, which is uncommon for buyers at today’s resale prices.

Does receiving a CPF Housing Grant affect my HDB Loan Eligibility (HLE)?

Grants and HLE are assessed separately. Your HDB Loan Eligibility letter determines the maximum HDB concessionary loan you can borrow, based on income, credit history, outstanding debts, and MSR/TDSR compliance. Grants reduce the net amount you need to borrow, but the HLE loan quantum is not directly inflated by the grant. You apply for both the HLE and the grant through the HDB flat portal before exercising the OTP.

I am a Singapore Permanent Resident married to a Singapore Citizen. What grants are we eligible for?

An SC + SPR couple counts as a mixed-citizenship household for CPF grant purposes. You are eligible for the EHG at the family rate (since one applicant is SC), the Family Grant at the reduced SC + SPR amount of S$40,000, and the PHG if applicable. You are not eligible for the full SC + SC Family Grant of S$50,000. The SPR spouse’s income is included in the combined household income calculation for EHG and Family Grant means-testing.

What happens to my grant if I divorce after purchasing the flat?

Divorce does not trigger a grant clawback. The grant remains in the CPF OA of the respective owner(s) and normal CPF refund-on-sale rules apply. However, if the divorce results in one party retaining the flat and the other being bought out, the outgoing party’s CPF contributions — including grant amounts attributed to them — must be refunded at that point, with accrued interest. This is handled through the matrimonial asset division process, usually with the assistance of a family law solicitor.

Can I appeal for a higher grant if my income is irregular or I am self-employed?

Yes. HDB uses average gross monthly income over the 12 months preceding the application for means-testing. If your income is irregular — for example, you are a freelancer, commission-based worker, or recently returned to employment — HDB has a declared income process for the self-employed and an appeal mechanism for unusual circumstances. Supporting documents such as Notice of Assessment from IRAS, payslips, or CPF contribution history are typically required. Speak to an HDB branch officer early in the process if your income situation is non-standard.

Do the grants expire if I do not use them within a certain period?

CPF Housing Grants are credited into your CPF OA at the point of flat purchase — they are not a time-limited voucher. However, your eligibility to receive grants can change: if your income rises above the ceiling before application, or if you purchase a private property before your HDB flat, you may lose eligibility. The grant application must be submitted before you exercise the Option to Purchase, and the grant is disbursed only upon completion of the purchase.

Disclaimer: This article is intended for general information only and does not constitute financial, legal, or tax advice. CPF Housing Grant amounts, income ceilings, and eligibility conditions are subject to change. Always verify current grant details on the official HDB Grant Eligibility page and the CPF Board Home Ownership page. Consult a licensed property agent (CEA-registered) or HDB branch officer before making any purchase decision.

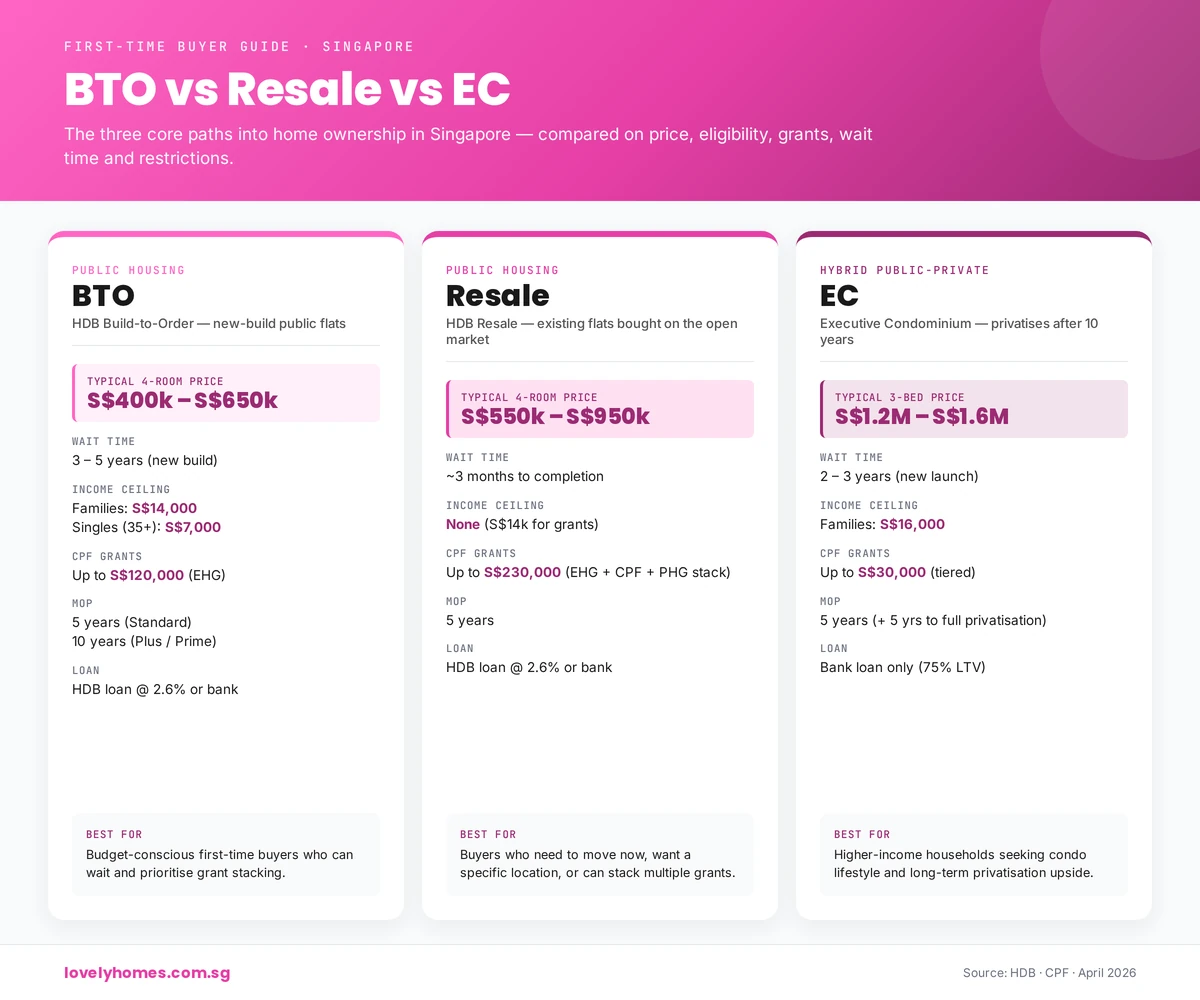

For most Singapore citizens, the decision between a Build-To-Order (BTO) flat, an HDB resale flat, or an Executive Condominium (EC) represents the single largest financial commitment of their lives. Yet the answer is far from straightforward: each option offers distinct advantages and trade-offs in price, location, waiting time, and long-term wealth building.

In 2026, first-time buyers face more choices than ever before. HDB’s new Standard, Plus and Prime classification (introduced October 2024) has reshaped BTO pricing and subsidy structures. The Enhanced CPF Housing Grant (EHG) has been raised to S$120,000 for families and S$60,000 for singles. Executive Condos remain a viable middle ground for those earning S$10,000–S$16,000 monthly. Meanwhile, resale flats offer immediate occupancy but at a premium price.

This comprehensive guide walks you through all three options, compares the financial reality with worked examples, and helps you choose the path that fits your circumstances, timeline and budget.

Quick Answer — Which one is right for you?

Choose BTO if: You can wait 3–5 years, want the cheapest entry price, and prioritise subsidised flats in newer estates. Best for budget-conscious buyers and families.

Choose Resale if: You need to move in within 12 months, want an established neighbourhood with proven amenities, and have sufficient CPF savings. Best for upgraders and those near MOP.

Choose EC if: Your household income is S$10,000–S$16,000, you value hybrid public–private living, and you’re willing to pay a premium for potential capital appreciation after the 10-year privatisation period.

Figure 1: Household income is the biggest filter — it determines which paths are open to you.

HDB BTO Explained

What Is BTO?

Build-To-Order (BTO) flats are new HDB units built to demand. HDB launches BTOs in batches (typically every four months), offers them at subsidised prices below market rates, and constructs them over 3–5 years. Once completed and handed over, you own the flat outright and must occupy it for a minimum occupation period (MOP) before you can sell or rent it out.

Eligibility for BTO in 2026

Citizenship: At least one applicant must be a Singapore Citizen. For families, both applicants can be Singapore Citizens or one can be a Permanent Resident (SPR).

Age: You must be at least 21 years old. Singles aged 35 and above can now buy 2-room Flexi BTOs in any location (expanded from 12 non-mature estates in October 2024).

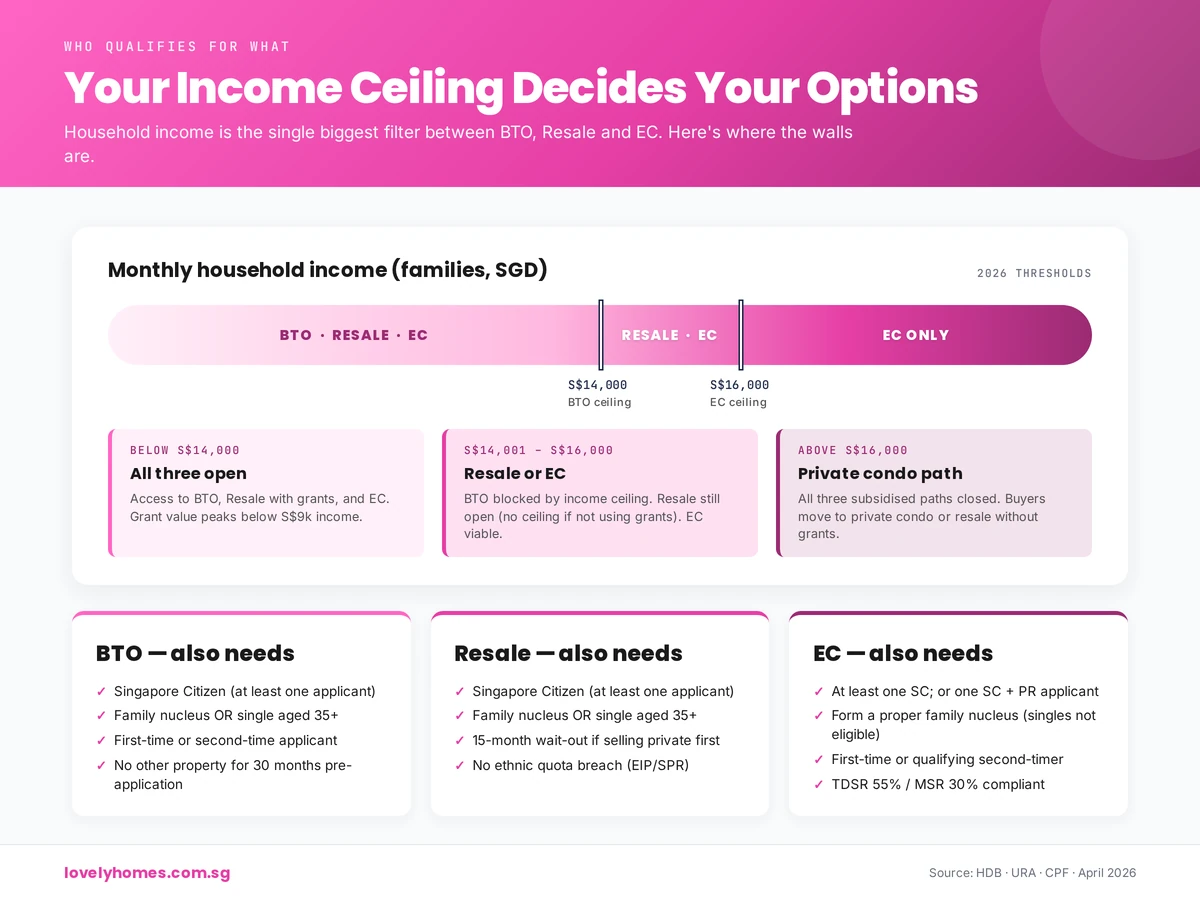

Income Ceiling (2026):

Families and couples: S$14,000 monthly

Singles (for all flat types and 2-room Flexi): S$7,000 monthly

Ownership: You and your spouse (if applicable) must not own any other property. Inheritance and co-ownership with parents do not disqualify you, provided the flat is not mortgaged.

BTO Pricing Framework: Standard, Plus & Prime (October 2024)

HDB replaced its old classification with three tiers based on location and amenities:

Classification

Features

MOP Period

Subsidy Clawback on Resale

Standard

Good connectivity, suburban, new estates

5 years

None (keep full subsidy)

Plus

Choicer locations, mature estates, proximity to city

10 years

6–8% of resale price

Prime

Choicest locations, central, excellent transport

10 years

9% of resale price

Example Prices (October 2024 Launch): A 4-room Standard BTO in Woodlands or Sengkang starts around S$400,000–S$450,000. A 4-room Plus BTO in a mature estate (e.g. Punggol, Hougang) costs S$550,000–S$650,000. Prime flats (rare) command prices above S$750,000.

Waiting Time & Build Cycle

From the launch month to handover typically takes 3–5 years. HDB now offers a “Shorter Waiting Time” (SWT) option for selected projects, reducing the wait to approximately 3 years. Check each BTO exercise’s buyer’s guide for your project’s expected handover date.

CPF Grants for BTO

Enhanced CPF Housing Grant (EHG) for BTO:

Families (SC+SC or SC+SPR): up to S$120,000 (income ceiling S$9,000/month)

Singles (aged 35+): up to S$60,000 (income ceiling S$4,500/month)

CPF Housing Grant (for those above EHG income ceiling): Families earning S$9,001–S$14,000 receive a grant tapering from S$120,000 to S$0.

All grants are paid into your CPF Ordinary Account and applied automatically at flat handover.

Minimum Occupation Period (MOP)

Standard flats: 5-year MOP. After 5 years, you can sell without restriction and keep the entire subsidy.

Plus & Prime flats: 10-year MOP. When you sell after 10 years, HDB claws back 6–9% of the resale price to recover a portion of the subsidy you received.

During MOP, you cannot rent out the entire flat (though private let of rooms is allowed for some schemes). You must occupy it as your main residence.

Advantages of BTO

Lowest entry price, especially for Standard flats

Large CPF grants (up to S$120,000 for families)

New flat – minimal repairs for first 5–10 years

Predictable pricing and transparent framework

New neighbourhoods with fresh amenities

Disadvantages of BTO

Long wait (3–5 years) – cannot move in immediately

Location not guaranteed (you choose from allocated projects)

Longer MOP for Plus/Prime (10 years vs. 5 for Standard)

Subsidy clawback on Plus/Prime resales reduces gains

Less mature neighbourhoods compared to older estates

HDB Resale Explained

What Is HDB Resale?

HDB resale flats are existing units on the open market, sold by current owners who have completed their MOP. You can view, negotiate and purchase immediately – no waiting for construction. The buyer’s 5-year MOP obligation begins on the date of transfer, even though the previous owner already completed theirs.

Eligibility for HDB Resale in 2026

Citizenship: You must be a Singapore Citizen or a Singapore Permanent Resident. For SC+SPR couples buying in non-mature estates, there is a quota limit (typically 10%) on SPR purchases.

Age: Minimum 21 years old (single or couple).

Income Ceiling: An income ceiling (S$14,000 for families, S$7,000 for singles) applies only if you are claiming CPF grants. If you have sufficient cash and CPF savings, you can buy a resale flat with any income level.

Ownership: You must not own any other property. First-timer status unlocks priority for certain grants.

Resale Flat Pricing

Resale prices are set by market forces and vary widely by location, flat type, floor level, condition and remaining lease:

4-room flats in mature estates (Tampines, Bedok, Punggol): S$550,000–S$750,000

4-room flats in central estates (Bukit Merah, Tanjong Pagar): S$700,000–S$950,000

3-room flats in non-mature estates: S$350,000–S$500,000

Prices fluctuate with economic cycles, interest rates and supply.

CPF Grants for HDB Resale

Enhanced CPF Housing Grant (EHG) – Families:

Up to S$120,000 (income ceiling S$9,000/month)

CPF Housing Grant (Family) – Standard:

SC+SC or SC+SPR couple: S$80,000

Proximity Housing Grant (PHG):

Living with parents (same flat): S$30,000

Living within 4 km of parents: S$20,000

For Singles (EHG – Resale): Up to S$60,000 (income ceiling S$4,500/month).

Total grant stack (families): EHG (S$120,000) + CPF Housing Grant (S$80,000) + Proximity Grant (S$30,000) = up to S$230,000 if all criteria met.

Minimum Occupation Period for Resale

Once you purchase a resale flat, you must occupy it as your main residence for 5 years before you can sell or rent it out. The previous owner’s MOP is already satisfied; yours begins afresh.

Multiple grants available (EHG, CPF, PHG) can stack to S$230,000+

Disadvantages of HDB Resale

Significantly higher purchase price than BTO

Older flats (20–40 years common) – higher repair/renovation costs

Lease decay – remaining lease affects resale value and loan eligibility

Must negotiate price, condition and terms yourself

Requires more cash upfront (HDB resale loans capped at 80% LTV, BTO can be 90%)

Executive Condominium (EC) Explained

What Is an EC?

An Executive Condominium is a hybrid public–private residential scheme. HDB sells the land to private developers, who build and sell the units directly to buyers. For the first 10 years (the “HDB control period”), ECs are subject to HDB-like rules: you must occupy it, cannot rent the whole unit, and are subject to an income ceiling. After 10 years, the building is privatised, and it becomes a full private condominium with no income restrictions, rental caps, or ownership limits.

Eligibility for EC in 2026

Citizenship: At least one applicant must be a Singapore Citizen.

Family Nucleus: You must be in a family nucleus – married couple, divorced/widowed with child, or parents with adult child (25+). Singles cannot buy ECs directly.

Income Ceiling (2026): Household monthly income must not exceed S$16,000. This applies to all new EC purchases from developers.

Ownership: You must not own any other property. First-timer priority applies to ballot allocation.

EC Pricing & Affordability

ECs are built by private developers and priced above HDB but below private condos:

2-bedroom EC: S$800,000–S$1,200,000

3-bedroom EC: S$1,200,000–S$1,600,000

4-bedroom EC (rare): S$1,600,000+

Price varies by location, developer, and finishing standard.

CPF Grants for EC

Enhanced CPF Housing Grant (EHG) – Families:

Up to S$30,000 (income ceiling S$9,000/month for maximum grant)

Note: EC grants are significantly lower than HDB resale (S$30,000 vs. S$120,000) and are based on a lower income threshold.

EC Financing & Loan Requirements

No HDB Concessionary Loan: Unlike HDB flats, ECs cannot be financed with an HDB concessionary loan. You must use a bank mortgage.

Bank Loan Criteria:

Loan-to-Value (LTV): up to 75% (vs. 90% for HDB)

Mortgage Servicing Ratio (MSR): 30% maximum monthly income

Your down payment must be at least 25%

Effective Cost: With a higher down payment (25% vs. 10% for HDB) and a bank mortgage at ~3.5% interest (versus HDB concessionary rates at ~2.6%), monthly payments are significantly higher than a comparable HDB flat.

Minimum Occupation Period & Privatisation

5-year MOP: You must occupy the EC as your main residence for 5 years. You cannot rent it out (whole unit) or sell it.

After 5 years: You can sell on the resale market (still subject to income ceiling if you wish to re-buy an EC or HDB).

After 10 years: The EC block is privatised. Income restrictions are lifted, and it becomes a private condo. You can then rent it out freely, sell to foreigners, or use it as an investment without restriction.

Advantages of EC

Hybrid lifestyle – condominium amenities (gym, pool, concierge) with HDB affordability

Privatisation upside – potential capital appreciation and rental income from year 11 onwards

Better quality finishes than new HDB (private developer standards)

Often in prime locations with strong transport and amenities

Eligible for CPF grants (though smaller than HDB)

Disadvantages of EC

Much higher purchase price than HDB (25–100% more)

Require 25% down payment vs. 10% for HDB – significant cash outlay

Bank mortgage at market rates (~3.5%) vs. HDB concessionary rate (~2.6%)

Lower LTV (75% vs. 90%) – less leverage possible

Smaller CPF grants (S$30,000 vs. S$120,000 for HDB)

No rental income for first 10 years (occupation requirement)

10-year MOP for first unit – cannot upgrade as easily as HDB

Service charges, maintenance fees and sinking funds (not present in HDB)

Figure 2: Price, wait time, grants, MOP and loan type compared across the three options.

Side-by-Side Comparison Table

Factor

BTO (Standard)

HDB Resale

Executive Condo

Entry Price (4-room)

S$400–450k

S$600–750k

S$1.2–1.6m

Occupancy Timeline

3–5 years wait

Immediate

Immediate

Max CPF Grant (Family)

S$120,000

S$230,000 (stacked)

S$30,000

Down Payment

10–15%

10–20%

25%

Financing

HDB concessional (~2.6%)

HDB concessional (~2.6%)

Bank mortgage (~3.5%)

Max LTV

90%

80–90%

75%

MOP Period

5–10 years

5 years

5–10 years

Subsidy Clawback

None (Standard); 6–9% (Plus/Prime)

None

None (private)

Rental During MOP

Room rental allowed; no whole-unit rental

Room rental allowed; no whole-unit rental

No rental (whole unit or rooms) for 10 years

Income Ceiling

S$14,000 (families); S$7,000 (singles)

S$14,000 (families) for grants only

S$16,000

Facilities

Basic (void deck, lift lobby)

Basic (void deck, lift lobby)

Premium (gym, pool, concierge)

Ethnic Quota

25% Chinese, 13% Malay, 9% Indian

Estate-dependent; no restrictions on resale

No ethnic quota

Worked Example: Which Option Costs Less?

The Scenario

Meet Sarah and Michael — both 30 years old, both Singapore Citizens, combined monthly income S$10,000 (S$5,000 each). They are HDB first-timers looking to buy a 4-room flat and need to decide between BTO, resale and EC. Both have S$80,000 in combined CPF Ordinary Account savings (after set-asides). They plan to hold the flat for 10 years, then either sell or upgrade.

Option 1: BTO (Standard 4-room in Sengkang)

Component

Amount (S$)

Purchase Price

420,000

CPF Housing Grant

–80,000

Net Price After Grant

340,000

Loan Amount (80% LTV)

336,000

Cash Down Payment

4,000

Monthly Mortgage (25 years @ 2.6% HDB)

~1,440

Total Interest Paid (25 years)

94,000

Total All-In Cost After 10 Years

~514,000

Est. Flat Value at Year 10 (assume 2% p.a. appreciation)

512,000

Notional Equity Gain/(Loss)

–2,000

Insight: The BTO is the cheapest entry and has the lowest ongoing costs. However, at only 2% annual appreciation, you barely break even on interest costs after 10 years. The real value is housing affordability now and long-term capital preservation.

Option 2: HDB Resale (4-room in Punggol)

Component

Amount (S$)

Purchase Price

630,000

Enhanced CPF Housing Grant

–80,000

Proximity Housing Grant (living 4km from parents)

–20,000

Net Price After Grants

530,000

Loan Amount (80% LTV)

504,000

Cash Down Payment

26,000

Monthly Mortgage (25 years @ 2.6% HDB)

~2,160

Renovation/Repair Estimate (older flat)

30,000–50,000

Total Interest Paid (25 years)

140,000

Total All-In Cost After 10 Years (incl. renovations)

~810,000

Est. Flat Value at Year 10 (assume 3% p.a. appreciation)

846,000

Notional Equity Gain

+36,000

Insight: Resale flats cost significantly more upfront (S$630k vs. S$420k for BTO). However, established Punggol flats appreciate faster (~3% p.a. vs. 2% for new Sengkang BTO), and you capture a modest gain after 10 years. You also benefit from higher grants (S$100,000 vs. S$80,000 with PHG) and immediate occupancy, valuable if you need to move within 12 months.

Option 3: Executive Condo (3-bed in Tampines)

Component

Amount (S$)

Purchase Price

1,300,000

CPF Housing Grant (EHG, S$9k income threshold)

–30,000

Net Price After Grant

1,270,000

Down Payment Required (25%)

325,000

Loan Amount (75% LTV)

975,000

Monthly Mortgage (25 years @ 3.5% Bank Rate)

~4,580

Monthly Service Charges & Maintenance

~300–500

Total Interest Paid (25 years)

371,000

Total All-In Cost After 10 Years

~1,910,000

Est. Flat Value at Year 10 (assume 4% p.a. appreciation pre-privatisation)

1,920,000

Notional Equity Gain (After Privatisation)

+10,000 (conservative)

Insight: ECs are dramatically more expensive — S$1.3m vs. S$420k BTO, or S$630k resale. Monthly payments are triple a BTO (S$4,580 vs. S$1,440). However, ECs benefit from stronger appreciation (4% p.a. vs. 2–3%) due to privatisation upside and prime locations. After 10 years (and especially after privatisation at year 11), rental income and capital gains potential accelerate. An EC makes sense only if your timeline is 15+ years and you can afford the premium monthly cost.

Figure 3: Ten-year all-in cost of ownership for the same couple — BTO S$514k, Resale S$810k, EC S$1.91M.

Resale (Moderate): S$810,000 all-in cost; modest capital gains (S$36,000)

EC (Premium): S$1,910,000 all-in cost; conservative gains, but privatisation upside at year 11+

Key Takeaway: If you want to minimise housing costs and build equity steadily, BTO wins. If you need to move now and expect moderate appreciation, resale is rational. If you want premium lifestyle and long-term wealth (15+ year hold), EC can pay off after privatisation.

Which Should You Choose?

Choose BTO If:

You can wait 3–5 years for occupancy

You want the lowest entry price and monthly mortgage

You prioritise maximising CPF grants (up to S$120,000 for families)

You value a brand-new flat with minimal repairs for 15+ years

You are budget-conscious and wish to minimise lifetime housing costs

You are comfortable with newer, less-established neighbourhoods

You are open to the estate HDB assigns you (limited location choice)

Choose Resale If:

You need to move in within 12 months (or less)

You want to choose your exact location, estate and block

You value established neighbourhoods with proven amenities and connectivity

You have sufficient CPF savings and can afford the higher purchase price

You are a second-time buyer or upgrader (eligible for larger grants)

You live near parents and are eligible for Proximity Housing Grant

You expect faster capital appreciation (established estates appreciate 2.5–3.5% p.a.)

You plan to hold the flat for 10+ years

Choose Executive Condo If:

Your household income is S$10,000–S$16,000 (above HDB ceiling but below private condo buyers)

You value condominium lifestyle (pool, gym, concierge) but cannot afford pure private condo

You can afford a 25% down payment and monthly mortgage of S$4,000+

You plan to hold for 15+ years, targeting post-privatisation rental income and capital gains

You prefer prime or central locations (ECs are often well-positioned)

You are willing to pay a premium for privacy, space and amenities vs. HDB

You can accept no rental income for the first 10 years and an income ceiling restriction

Frequently Asked Questions

1. Can I apply for BTO and HDB resale simultaneously?

Yes, but strategically. You can submit a BTO application for one project and bid for a resale flat at the same time. However, if you win the resale first, you must withdraw your BTO application (as you cannot own two properties). Many buyers use this two-pronged approach: they apply for BTO as a backup while actively bidding on resale flats.

2. Can a single person buy an Executive Condo?

No, singles cannot buy ECs directly. You must be in a family nucleus (married couple, divorced/widowed with child, or parent with adult child 25+). If you are single and interested in hybrid housing, your only option is HDB (BTO or resale).

3. What happens if I miss the BTO ballot multiple times?

You can keep applying. There is no limit to the number of BTOs you can apply for. However, if you consistently miss (do not win the ballot), it may be a signal that you should pivot to resale or EC if you have the means and timeline allows.

4. Is an Executive Condo considered a private condo?

For the first 10 years: No. ECs are HDB-controlled and subject to HDB rules (income ceiling, occupancy requirement, no whole-unit rental). After 10 years, the block is privatised, and it becomes a full private condo with no restrictions. At that point, it is legally and practically identical to any other private condo.

5. Can I rent out my BTO flat during the MOP?

Not the whole flat. During MOP, you can rent out individual rooms to lodgers, but you cannot rent out the entire flat to a tenant. This occupancy rule is strict. After MOP (5 years for Standard BTO), you can sell or rent out the whole flat freely.

6. What grants am I eligible for?

It depends on your household structure, income and purchase type:

For BTO: Enhanced CPF Housing Grant (families up to S$120,000; singles up to S$60,000, both with income ceilings S$9,000 and S$4,500 respectively).

For HDB Resale: Enhanced CPF Housing Grant + CPF Housing Grant (family) + Proximity Housing Grant, totalling up to S$230,000 if you meet all criteria.

For EC: Enhanced CPF Housing Grant (families up to S$30,000, tiered between S$9,000 and S$16,000 income).

Apply for an HDB Flat Eligibility (HFE) letter to confirm your exact grant amount.

7. Should I wait for BTO or buy resale now?

This depends on three factors:

Timeline: If you need housing within 12 months, buy resale. If you can wait 4–5 years, BTO may save you S$150k–S$250k.

Location: If a specific neighbourhood is critical (e.g. near parents, near your workplace), resale gives you certainty. BTO assigns location at ballot.

Finances: If you have substantial CPF savings but limited cash, resale grants are larger (S$230k vs. S$80k for BTO). If cash is tight, BTO’s lower entry price wins.

Pragmatic approach: Apply for BTO while simultaneously bidding for resale flats. Whichever closes first is your home; the other falls away.

Upgrader’s Guide — Planning your second property? Learn about upgrading from 4-room to 5-room, EC to private condo, and tax implications.

Property Finance Hub — Understand CPF Housing Grants, HDB loans, bank mortgages, and financing strategies.

Home Loans & Mortgages — Deep-dive into HDB concessionary loans, bank mortgage rates, MSR and TDSR calculations.

ABSD Complete Guide 2026 — If upgrading to private property, understand Additional Buyer’s Stamp Duty and tax planning.

Disclaimer

This guide is for general information only and does not constitute legal, tax or financial advice. HDB policy, grants, income ceilings and pricing frameworks change periodically. The figures and eligibility rules cited reflect policy as of April 2026, but may be subject to change. Always verify current information on HDB’s official website (https://www.hdb.gov.sg), consult HDB’s Customer Service or engage a licensed mortgage advisor or housing consultant before committing to any property purchase. CPF withdrawal limits and grant eligibility are subject to CPF Board rules (https://www.cpf.gov.sg). For EC and resale purchases, seek independent legal and financial counsel.