How to Choose a Property Agent in Singapore 2026: CEA Checks, Red Flags and Questions to Ask

Choosing how to select a property agent in Singapore 2026 is a decision that could save — or cost — tens of thousands of dollars. With approximately 35,000 licensed real estate salespersons registered with the Council for Estate Agencies (CEA) as at 2026, the quality and suitability of agents varies widely. This guide gives you a structured, step-by-step framework for finding, vetting, and working with the right agent for your specific transaction — whether you are buying, selling, or renting.

Quick Answer: How to Choose a Property Agent Singapore 2026 — Key Facts

- CEA registration is mandatory: Every property agent in Singapore must be registered with the Council for Estate Agencies. Unregistered agents cannot lawfully conduct property transactions. Verify at eservices.cea.gov.sg using the agent’s phone number — if it does not match, stop dealing immediately.

- Client’s Agreement is required by law: Under the Estate Agents Act, an agent must enter into a written Client’s Agreement with you before conducting any work on your behalf. Refuse any agent who asks you to proceed without one.

- Dual representation is restricted: An agent cannot represent both buyer and seller in the same transaction — unless both parties give informed written consent. This is a common cause of conflict-of-interest disputes.

- Commission rates are advisory, not fixed: CEA publishes advisory rates as a market benchmark; actual commission is negotiable. New launch buyer agents are paid by the developer, not the buyer.

- Check disciplinary record: CEA’s Public Register shows past sanctions, fines, and licence suspensions. This is a critical check many buyers skip.

- Specialisation matters: An agent who primarily transacts HDB resale may not have the market knowledge, network, or sub-sale experience for a D9 new launch.

- Red flags: WhatsApp-only contact, pressure to pay before viewing, no CEA registration match on phone number, reluctance to sign Client’s Agreement.

Why the Right Property Agent Matters More Than the Platform

Online property portals, valuation tools, and AI-assisted market data have made property information more accessible than ever. But the actual execution of a property transaction — negotiating on price, managing the OTP timeline, coordinating between buyer’s and seller’s solicitors, handling mortgage applications, navigating HDB procedures — still depends heavily on the agent’s competence, ethics, and market network. A well-chosen agent protects your interests actively; a poor choice, or worse, a fraudulent one, can expose you to misrepresentation, conflicts of interest, and financial loss.

Step 1: Verify CEA Registration Before Anything Else

This is the single most important step and takes under two minutes. Visit eservices.cea.gov.sg and search using the phone number the agent contacted you from. If the phone number does not return a matching, currently active salesperson licence, stop all engagement immediately — this is a classic fraud indicator.

Do not rely solely on the business card, name, or IC number that the agent provides. Scammers regularly impersonate real agents by using stolen photos and legitimate-sounding names while substituting a different phone number that you are meant to contact.

The Public Register also shows:

- The estate agency the agent is currently registered under.

- Whether the licence is active, lapsed, or suspended.

- The agent’s transaction history for the past 36 months (categories: HDB resale, HDB rental, private sale/resale, private rental).

- Any disciplinary actions taken by CEA, including fines, reprimands, and licence revocations.

Step 2: Match the Agent’s Specialisation to Your Transaction

Transaction history is your most objective indicator of an agent’s specialisation. An agent with 50 HDB resale transactions in the past 36 months and zero private property transactions is unlikely to be the best choice for a high-value CCR condominium purchase. Conversely, a specialist in D9–D11 luxury resales may be unfamiliar with HDB procedures and the nuances of the CPF Housing Grant application process.

Ask the agent directly: “How many transactions of this specific type — resale 4-room HDB in Tampines / new launch in OCR / commercial shophouse — have you done in the past 12 months?” A trustworthy agent will show you their track record rather than deflect the question.

Key specialisation signals to look for:

- HDB resale buyer: Look for 10+ HDB resale transactions in the past 36 months, familiarity with HFE letter procedures, and knowledge of the NCQ (Non-Citizen Quota) for rental scenarios.

- Private resale buyer: Look for private property transaction history, knowledge of current sub-sale volumes in your target district, and relationships with mortgage brokers.

- New launch buyer: Developer accreditation and attendance at developer previews; knowledge of ballot priority systems; familiarity with the Progressive Payment Scheme.

- Seller (HDB or private): Track record of actual listings sold, average days on market for recent listings, familiarity with comparative market analysis.

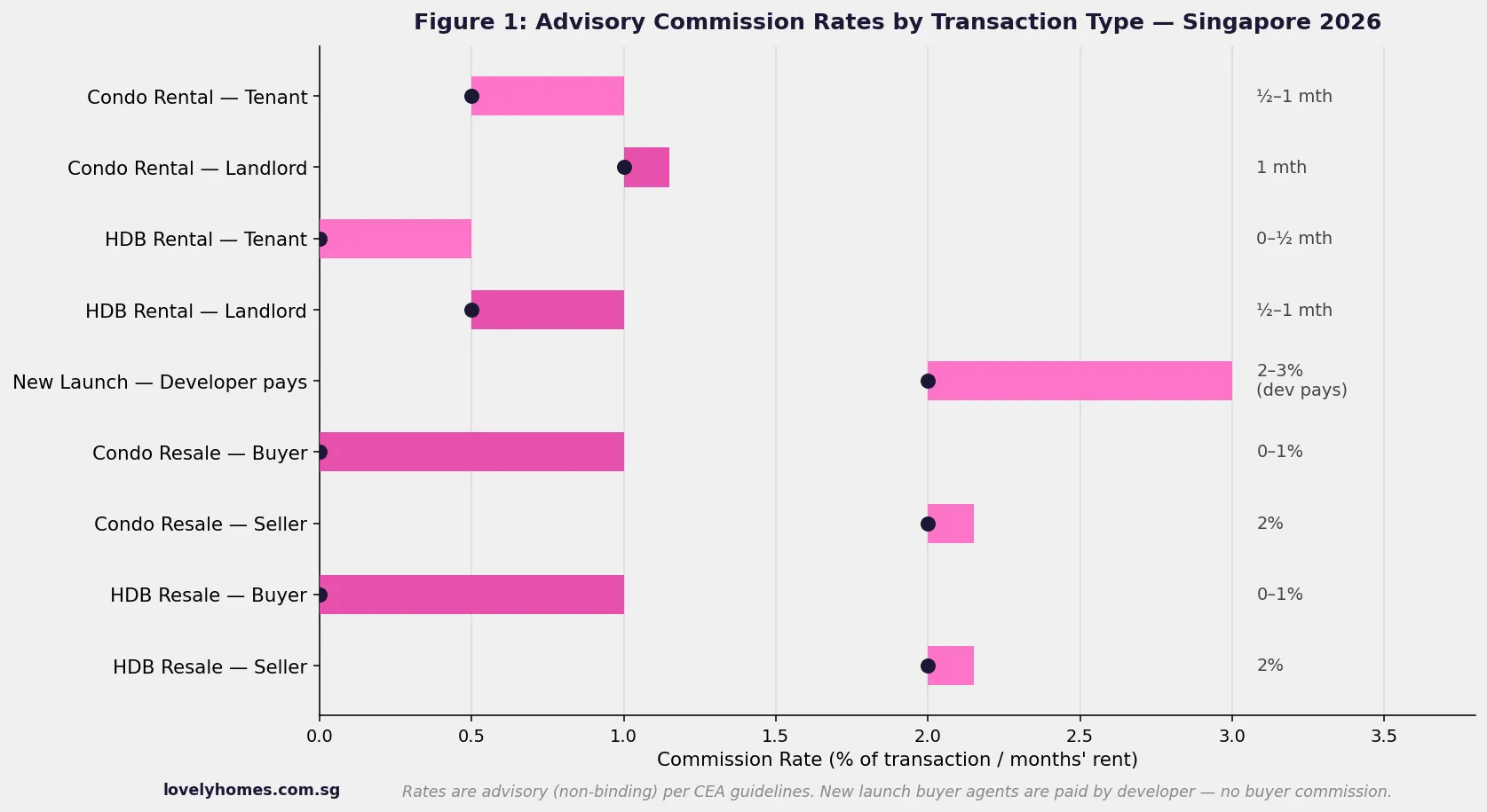

Step 3: Understand Commission and Negotiate Clearly

Commission rates in Singapore are not regulated by law — the figures published by CEA are advisory rates that serve as market benchmarks. They are not binding on either party. In practice, most HDB seller agents charge around 2% of the transaction price; HDB buyer agents typically charge 0–1%. For private property, seller agents charge approximately 2% and buyer agents 0–1% on resale transactions.

For new launch private condominiums, the developer pays the buyer’s agent directly — the buyer pays no commission. Developer commissions for buyer’s agents typically range from 2% to 3% of the purchase price, sometimes higher for international buyers or premium units. This creates a structural incentive that is worth understanding: the buyer’s agent in a new launch transaction is economically the developer’s agent. Ask whether the agent has compared alternative units in different projects at the same price point before endorsing a specific development.

Always agree on commission in writing as part of the Client’s Agreement before any work begins. Verbal agreements on commission are difficult to enforce and frequently the source of disputes lodged with CEA.

Step 4: Insist on a Client’s Agreement

Under section 64 of the Estate Agents Act (Cap 95A), an estate agent and a registered salesperson must sign a Client’s Agreement with any client before performing any estate agency work. The Client’s Agreement must specify: the scope of services, the commission rate (or formula), the duration of the exclusive arrangement (if any), and the salesperson’s and agency’s registration details.

An agent who is reluctant to sign a Client’s Agreement is operating outside the legal framework — and likely has good reason to avoid a paper trail. Refuse to proceed without a signed Client’s Agreement in every circumstance. The Client’s Agreement also gives you a formal dispute mechanism: if an agent breaches its terms, you have grounds to file a complaint with CEA and seek compensation.

Dual Representation: Know Your Rights

Dual representation occurs when a single agent acts for both the buyer and the seller (or both landlord and tenant) in the same transaction. CEA rules permit dual representation only if both parties provide informed written consent — and only if the agent discloses the arrangement and both clients agree they understand the conflict of interest involved.

If an agent introduces you to a property and then reveals they are also representing the seller, you have every right to refuse and engage a separate buyer’s agent. In practice, the seller’s agent who shows you a property is acting for the seller; you should either negotiate directly or engage your own buyer’s agent to represent your interests.

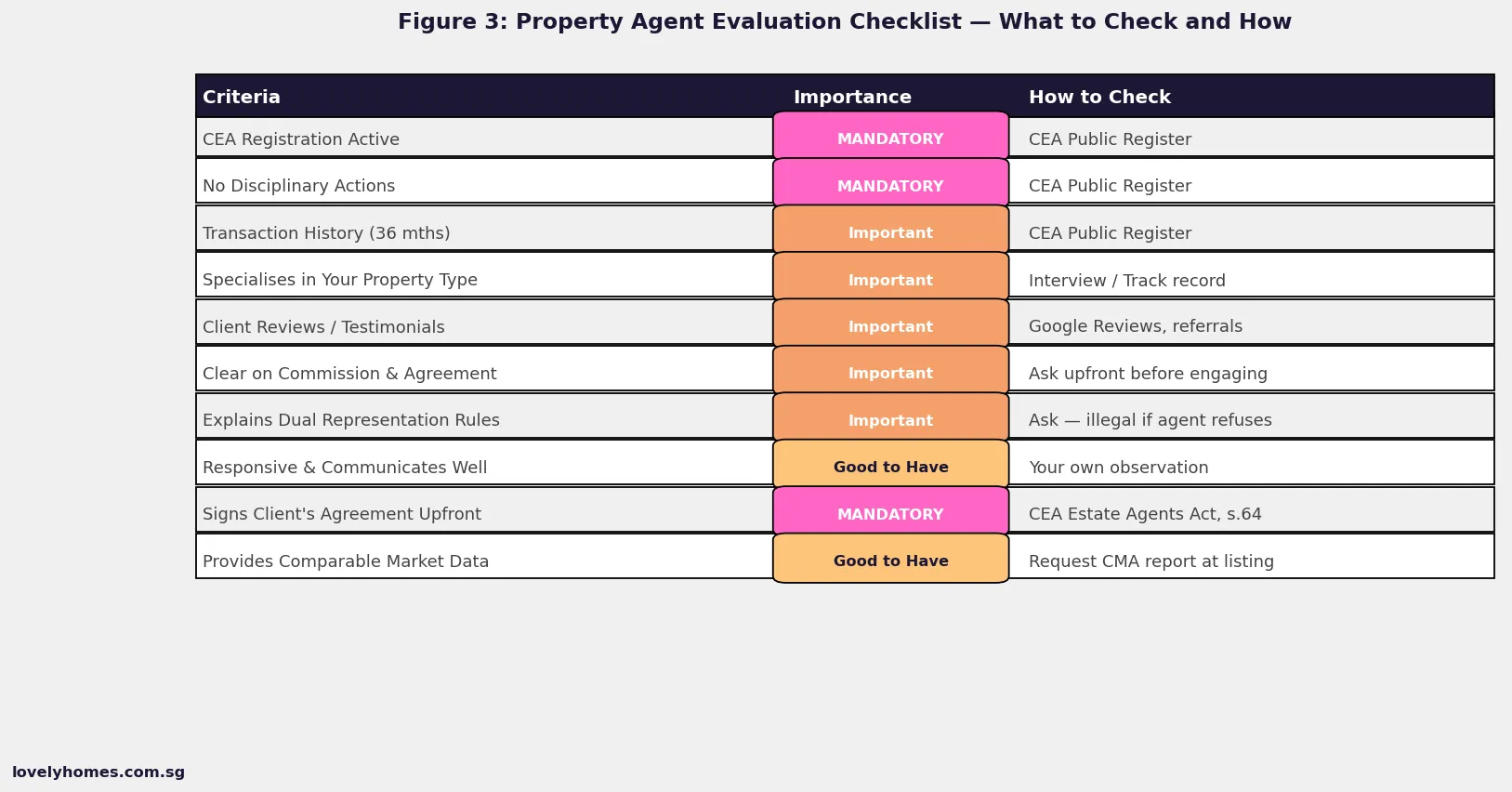

Summary Table: What to Check When Choosing a Property Agent

| Check | How to Do It | Importance |

|---|---|---|

| CEA licence is active | Search phone number at eservices.cea.gov.sg | Mandatory — do not proceed without this |

| No disciplinary record | CEA Public Register → check actions tab | Mandatory |

| Transaction history matches your property type | CEA Public Register → transaction history tab | High |

| Client’s Agreement signed before any work | Request before first viewing or listing appointment | Mandatory by law |

| Commission agreed in writing | Included in Client’s Agreement | High |

| Dual representation disclosed and consented to (if applicable) | Ask directly; get written confirmation | High |

| Reviews from past clients for same property type | Google Business profile, referrals, developer feedback | Moderate |

| Comparative market data provided | Request a CMA report before pricing your listing or making an offer | Moderate |

Worked Example: Mr Tan — Selling an HDB Flat in Tampines

Mr Tan holds a 5-room HDB resale flat in Tampines (MOP completed). He shortlists three agents by asking each the same set of questions:

- Agent A: CEA-registered, 22 HDB resale transactions in past 36 months including 8 in Tampines, no disciplinary record, quoted 2% commission, offered to sign Client’s Agreement immediately. Provided a Comparative Market Analysis showing recent 5-room transacted prices in Tampines (S$680K–S$760K range). Explained the SSD regime for his acquisition year (no SSD applicable — MOP completed, held more than 4 years).

- Agent B: CEA-registered, 5 transactions in past 36 months (mix of HDB and private), quoted 1.5% but said “we can discuss after the listing”. Did not proactively offer the Client’s Agreement. Could not provide a CMA on the spot.

- Agent C: Could not be verified by phone number on CEA Public Register — immediately disqualified.

Decision: Mr Tan engaged Agent A. The higher commission (2% vs 1.5%) was justified by the stronger local track record and the immediate CMA. The listing was priced at S$720,000, received three offers within 10 days, and was sold at S$736,000 — S$16,000 above asking price.

Commission paid: 2% × S$736,000 = S$14,720 + 9% GST = S$16,044.80 — fully accounted for in Mr Tan’s net sale proceeds.

Questions to Ask a Property Agent Before Engaging

The following 10 questions help filter out unsuitable agents quickly and give you the information you need to make an informed choice. A competent, ethical agent will answer each question directly:

- Can I search for your CEA registration using your phone number right now?

- How many transactions have you completed in the past 12 months for my specific property type and area?

- Are you willing to sign a Client’s Agreement today before we proceed further?

- Are you representing the seller (or buyer) of any properties you will show me?

- What is your commission rate and is it inclusive of GST?

- Can you provide a Comparative Market Analysis for my target area or my listing price?

- What is your exclusive period, and what are the exit conditions if I am unhappy?

- How do you handle co-broking — will you share commission with a buyer’s agent?

- Have you been subject to any CEA disciplinary proceedings?

- How and how often will you update me on enquiries and market feedback?

Why This Matters: The Cost of Getting It Wrong

CEA received approximately 370 consumer complaints against property agents in FY2025, the majority relating to misrepresentation, failure to disclose material facts, and commission disputes. An agent who misrepresents the remaining lease, the NCQ position, or the property’s Minimum Occupation Period status can expose you to legal liability and significant financial loss. The consequences of working with an unverified or unregistered agent are even more severe — any contract entered into with an unregistered person is voidable, and the agent has no professional indemnity insurance.

The estate agency industry in Singapore is regulated under the Estate Agents Act (Cap 95A) and the CEA Code of Ethics and Professional Client Care. CEA has the power to fine agents, suspend or revoke licences, and impose a public reprimand. These enforcement tools exist precisely because the consequences of dishonest or incompetent agency work in a high-value property market are severe.

What Might Change: Digital Tools and AI in Property Agency

Several platforms now offer AI-assisted valuations and transaction matching that reduce the information asymmetry between buyers, sellers, and agents. Industry watchers expect the share of transactions involving “self-service” buyer portals to grow modestly, particularly for straightforward HDB resale transactions. However, for higher-value or more complex transactions (CCR condos, commercial properties, en-bloc proceedings, cross-border purchases), the regulatory, legal, and negotiation complexities mean the licensed agent remains the essential professional for the foreseeable future.

CEA is also exploring digital licence verification tools embedded in property portal listings, which would surface real-time CEA registration status alongside every listing. If implemented, this would make basic verification automatic — though the more nuanced checks (disciplinary history, specialisation fit, commission terms) will always require the buyer or seller to engage directly.

Frequently Asked Questions

Do I have to pay an agent as a buyer in Singapore?

For new launch private condominiums, no — the developer pays the buyer’s agent’s commission. For HDB resale and private resale transactions, the convention is that the seller pays the seller’s agent and the buyer may or may not engage their own buyer’s agent (typically at 0–1% of the purchase price). Some buyers choose to rely on the seller’s agent to facilitate the transaction, which is permitted only if dual representation is disclosed and consented to in writing. Engaging your own buyer’s agent provides independent representation for a relatively modest fee and is generally advisable for high-value or complex transactions.

What is a Co-Broking arrangement and should I be concerned?

Co-broking occurs when a listing agent (representing the seller) works with another agent (representing the buyer), splitting the total commission between them. This is a standard and healthy market practice — it incentivises seller’s agents to accept viewings from co-brokers, widening the pool of buyers. The seller typically pays the full commission, which the two agents then divide. As a buyer, co-broking generally means you are properly represented. As a seller, you should ask whether your listing agent is willing to co-broke; an agent who refuses co-broking is limiting your buyer pool, which can reduce your final sale price.

What are the consequences if an agent misrepresents a property to me?

Misrepresentation by a licensed property agent is actionable under both the Estate Agents Act and the Misrepresentation Act (Cap 390). You may file a complaint with CEA for disciplinary action against the agent, claim damages from the agent’s estate agency (which carries professional indemnity insurance), and, in cases of fraudulent misrepresentation, pursue civil action or a police report. If the misrepresentation relates to material facts — remaining lease, whether the property is encumbered, rental tenancy status — and you can demonstrate reliance and loss, damages claims can be substantial. Always get material facts confirmed in writing during the offer process, and instruct your solicitor to conduct due diligence independently.

How do I check if a property agent has been disciplined by CEA?

The CEA Public Register at eservices.cea.gov.sg shows the disciplinary record for every registered salesperson, including the date, nature, and sanction of any disciplinary proceedings. You can search by the agent’s name, registration number, or phone number. Disciplinary actions range from advisory letters and fines (minor breaches) to licence suspension or revocation (serious breaches such as misrepresentation, unauthorised receipt of monies, or criminal convictions). An advisory letter for a minor procedural breach should not necessarily disqualify an otherwise strong candidate; a licence suspension for misrepresentation is a clear disqualifier.

Can I switch agents if I am unhappy after signing a Client’s Agreement?

The Client’s Agreement will specify its duration, typically 60–90 days for an exclusive listing or buyer-representation arrangement. Most agreements include early termination provisions with notice periods of 7–14 days. If the agent has materially breached the agreement — failed to meet agreed obligations, made misrepresentations, acted without authority — you may have grounds to terminate immediately without notice. If the agent has merely been unsatisfactory without a clear breach, you will typically need to wait out the notice period or negotiate a mutual early termination. Any dispute about termination rights can be escalated to CEA’s Dispute Resolution Scheme before going to the courts.

What if I want to buy or sell property without an agent?

Transacting without an agent is legally permissible for private property and HDB resale (the HDB also facilitates direct seller-to-buyer transactions through its Resale Portal). However, you take on the full responsibility for negotiating the OTP, conducting due diligence, managing the conveyancing timeline, coordinating with the other party’s solicitor, and ensuring all regulatory conditions are met. A licensed solicitor is still required for the legal transfer. For straightforward transactions in a familiar market, experienced buyers and sellers sometimes transact direct; for first-time buyers, those unfamiliar with Singapore property law, or those handling complex transactions, engaging a qualified agent is strongly advisable.

Related Articles

- Singapore Property Agent Commission Guide 2026: How Much Does an Agent Cost?

- Singapore Property Conveyancing Guide 2026: OTP, S&P Agreement, Legal Fees and Timelines Explained

- Singapore HDB Resale Guide 2026: Complete Guide to Buying and Selling HDB Resale Flats

- Singapore Property Downpayment Guide 2026: How Much Cash and CPF You Need

- Singapore Home Loan Complete Guide 2026: HDB Loans, Bank Loans, TDSR and MSR Explained

- Singapore Executive Condo Buying Guide 2026: Eligibility, Prices, MOP and the New 10-Year Rules Explained

Disclaimer: This article is for general information only and does not constitute financial, legal, or professional advice. Information on CEA registration requirements and the Estate Agents Act may be updated by the Council for Estate Agencies. Verify all agent details at eservices.cea.gov.sg and consult the CEA website for the current Code of Ethics and professional standards. Engage a licensed solicitor for all conveyancing matters.

Click or press Esc to close