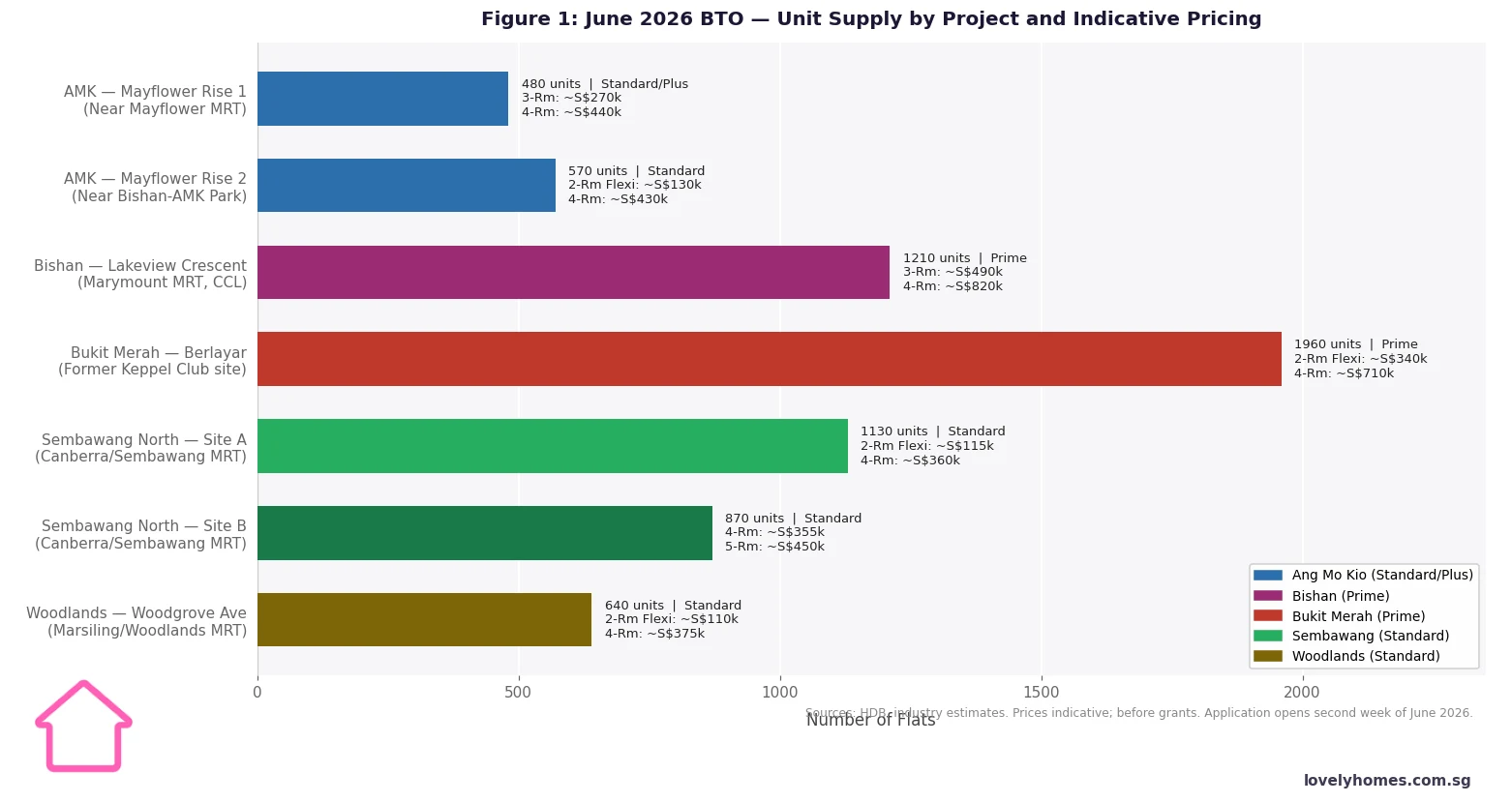

The June 2026 BTO exercise will offer approximately 6,900 flats across 7 projects in 5 towns: Ang Mo Kio, Bishan, Bukit Merah, Sembawang, and Woodlands. The application window opens in the second week of June 2026.

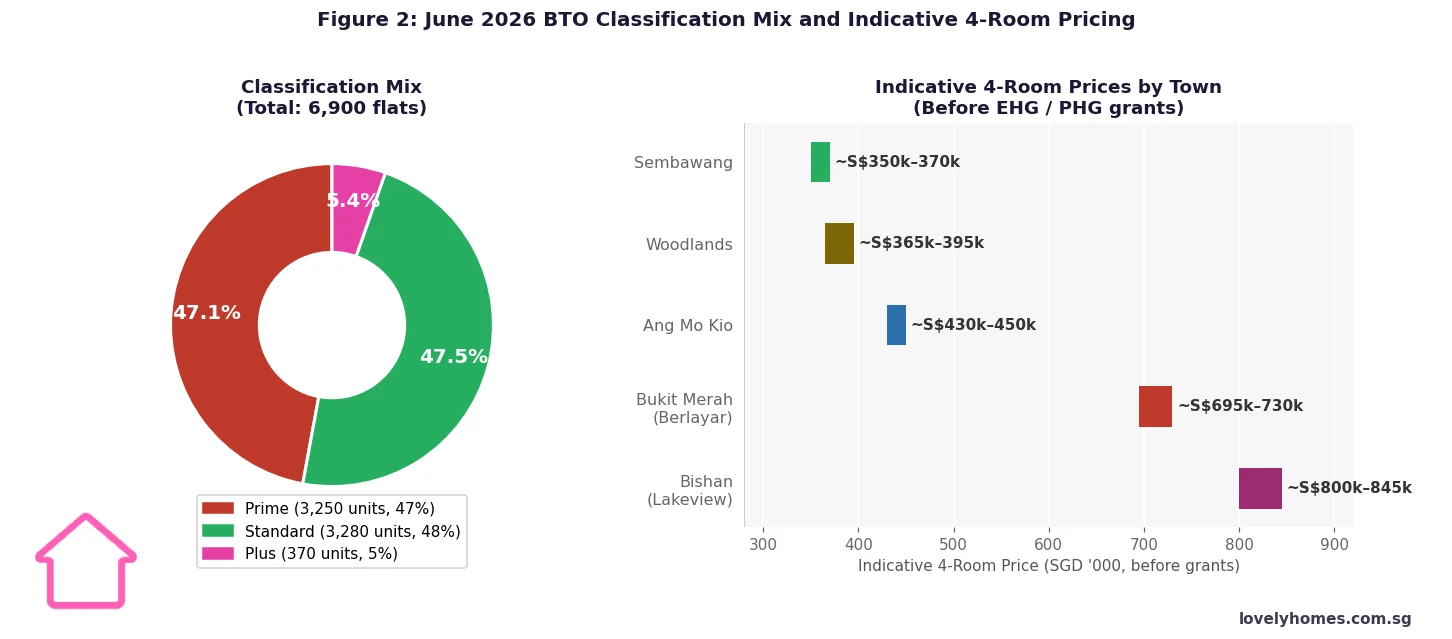

Nearly half the supply (approximately 3,250 units, or 47%) is classified as Prime — concentrated in Bishan (Lakeview Crescent) and Bukit Merah (Berlayar). Prime flats carry a 10-year MOP, SC-only resale, and a subsidy clawback on first resale.

Bishan — Lakeview Crescent is the headline project: the first new HDB development in Bishan in over 40 years, near Marymount MRT. Indicative 4-room prices are approximately S$820k before grants. Classified as Prime.

Berlayar (Bukit Merah) offers 1,960 units on the former Keppel Club site. Indicative 4-room: approximately S$710k. Classified as Prime.

Sembawang North offers the largest Standard supply (~2,000 units) at the most affordable prices — indicative 4-room from approximately S$350k before grants, with full EHG eligibility.

First-timer SC households earning up to S$9,000/month qualify for the Enhanced Housing Grant (EHG) of up to S$120,000 on Standard and Plus flats.

Ballot results are expected approximately 3 weeks after the application window closes, with flat selection appointments typically following 1–2 months later.

Overview: What Is on Offer in June 2026

The June 2026 BTO exercise is the second of three sales exercises HDB has planned for 2026, following the February 2026 exercise (4,692 flats) and ahead of the October 2026 exercise. At approximately 6,900 flats, it is the largest of the three 2026 tranches and includes some of the most sought-after locations in years — particularly the Bishan and Bukit Merah (Berlayar) projects.

HDB will launch the exercise on its HDB Flat Portal in the second week of June 2026. Potential buyers should prepare eligibility documents — including income declaration and citizenship verification — in advance, as these must be on file before a successful application can proceed to booking.

Figure 1: June 2026 BTO — Unit Supply by Project and Indicative Pricing | Source: HDB, industry estimates. Before grants.

Project-by-Project Analysis

Bishan — Lakeview Crescent (~1,210 units, Prime): This is the standout project of the exercise and arguably the most significant HDB launch in years. Bishan last received new BTO flats in 1984 — a gap of over 40 years. Lakeview Crescent sits near Marymount MRT (Circle Line) adjacent to the vast Bishan-Ang Mo Kio Park. CCL connectivity is excellent: Marymount to Dhoby Ghaut interchange in three stops, to Marina Bay in approximately seven. Blue-chip schools in the catchment include Catholic High School and St Gabriel’s Primary. Being classified Prime, it carries a 10-year MOP, income ceiling on resale, SC-only resale pool, and a subsidy clawback. Indicative 4-room: approximately S$820k before grants (EHG not available for Prime).

Bukit Merah — Berlayar (~1,960 units, Prime): Located on the former Keppel Club site off Telok Blangah Road, adjacent to the Southern Ridges nature corridor. Nearest MRT: Labrador Park or Telok Blangah (CCL). Unit mix is heavy on 4-room (~980) and 2-room Flexi (~810). Classified Prime: 10-year MOP, SC-only resale. Indicative 4-room: S$695k–S$730k. Strong lifestyle appeal for those who value the Southern Ridges and Harbourfront precinct.

Ang Mo Kio — Mayflower Rise (~1,050 units, Standard/Plus): Two projects near Mayflower MRT (Thomson-East Coast Line). Project 1 (480 units, Plus) near CHIJ St Nicholas Girls’: 3-room and 4-room at ~S$440k. Project 2 (570 units, Standard) near Bishan-AMK Park: 2-room Flexi and 4-room at ~S$430k. TEL provides direct access to Orchard Road and Marina Bay without interchange. EHG eligible for Standard project.

Sembawang North (~2,000 units, Standard): Largest town supply, most affordable pricing. Two projects near Canberra and Sembawang MRT (NSL). Indicative 4-room: S$350k–S$370k before EHG. Full EHG eligibility for qualifying households. Site A includes eating house, minimart, preschool, Residents’ Network Centre.

Woodlands — Woodgrove Avenue (~640 units, Standard): Moderate supply near Marsiling/Woodlands MRT (NSL). Indicative 4-room: ~S$375k before grants. Woodlands Regional Centre is undergoing long-term transformation as a northern business hub.

Figure 2: June 2026 BTO Classification Mix and Indicative 4-Room Pricing (Before Grants) | Source: HDB, industry estimates

Classification Mix and Ballot Strategy

The June 2026 exercise is polarised: 47% Prime (Bishan + Berlayar), 48% Standard (Sembawang + Woodlands + AMK Project 2), and just 5% Plus (AMK Project 1). Buyers who need to sell or upgrade within five to eight years should avoid Prime flats — the 10-year MOP is a genuine life commitment and the subsidy clawback at resale partially offsets the apparent price advantage.

For Standard and Plus flats, first-timer SC applicants receive 95% of ballot queue allocations. Demand for Standard flats in Sembawang and Woodlands is historically more moderate than for central locations, improving odds for applicants who are flexible on location.

Summary Table: June 2026 BTO at a Glance

Town / Project

Units

Class

MOP

Indicative 4-Rm

Nearest MRT

AMK Mayflower Rise 1

480

Plus

10 yr

~S$440k

Mayflower (TEL)

AMK Mayflower Rise 2

570

Standard

5 yr

~S$430k

Mayflower (TEL)

Bishan Lakeview Crescent

1,210

Prime

10 yr

~S$820k

Marymount (CCL)

Bukit Merah Berlayar

1,960

Prime

10 yr

~S$710k

Labrador Pk (CCL)

Sembawang North A

1,130

Standard

5 yr

~S$360k

Canberra (NSL)

Sembawang North B

870

Standard

5 yr

~S$360k

Canberra (NSL)

Woodlands Woodgrove Ave

640

Standard

5 yr

~S$375k

Marsiling (NSL)

Total

~6,860

47% Prime · 48% Standard · 5% Plus

Worked Example: The Lim Couple Comparing Sembawang vs Bishan

Mr and Mrs Lim are both Singapore Citizens aged 30, applying as first-timers for the June 2026 BTO. Combined household income: S$7,000/month. They are comparing a Sembawang North Standard 4-room at S$360,000 versus a Bishan Lakeview Prime 4-room at S$820,000.

Item

Sembawang Standard

Bishan Prime

Selling price (indicative)

S$360,000

S$820,000

EHG (income S$7,000/mth)

– S$20,000

Not eligible (Prime)

Net price after EHG

S$340,000

S$820,000

CPF OA downpayment (20%)

S$68,000

S$164,000

HDB loan (80%, 25-yr, 2.60%)

S$272,000

S$656,000

Monthly instalment (HDB loan)

~S$1,230

~S$2,966

MSR check (30% of S$7,000)

PASS (S$2,100 limit)

FAIL (exceeds S$2,100)

MOP duration

5 years

10 years

Earliest eligible to sell

~2031

~2036

Resale eligibility after MOP

SC/SPR buyers

SC only (income ceiling)

The MSR check reveals an important constraint: the Lim couple on S$7,000/month can borrow at most 30% × S$7,000 = S$2,100/month via an HDB loan. On the Bishan Prime flat, the required monthly instalment of ~S$2,966 exceeds this limit — meaning an HDB loan is insufficient and a bank loan would be required (subject to TDSR and prevailing rates). On the Sembawang Standard flat, the monthly instalment of ~S$1,230 easily clears the MSR, leaving S$870/month in MSR headroom for other debts. For a first-timer couple with moderate income, the Sembawang Standard flat is clearly the financially sound choice.

What Happens After You Apply

The BTO application process follows HDB’s standard sequence: applicants submit via the HDB Flat Portal within the application window (second week of June 2026, approximately one week long) and pay a S$10 application fee. Ballot results are typically released 3 weeks after the window closes. First-timers receive 95% of ballot queue allocation. Applicants with a queue number are called for flat selection in order — upon selecting a unit, a booking fee of approximately S$2,000 is payable. Key collection for June 2026 flats is estimated in the 2029–2030 range, depending on project and contractor progress.

When does the June 2026 BTO application window open?

The application window is expected to open in the second week of June 2026 for approximately one week. HDB will announce the exact dates on the HDB Flat Portal (homes.hdb.gov.sg). There is no advantage to applying on the first day — all applications within the window are treated equally in the computer ballot. Prepare eligibility documents (income declaration, citizenship, prior HDB ownership history) before the window opens to avoid delays.

Is the Bishan Lakeview Prime flat worth the premium?

For a SC couple in their late 20s to early 30s with stable employment and no plans to move for at least 10 years, Bishan Lakeview at approximately S$820k is excellent value relative to nearby private condo prices of S$1.8M–S$2.5M. The Circle Line connectivity and park access are genuine quality-of-life advantages. The 10-year MOP is the key constraint — if there is any chance of needing to upgrade, downsize, or relocate internationally within a decade, a Standard flat is the more prudent choice. Buyers should also confirm they can satisfy the Mortgage Servicing Ratio (30% of income cap) at the Bishan price point before applying.

Can SC-SPR couples apply for the June 2026 BTO?

Yes. An SC-SPR household is eligible to apply for HDB BTO flats as a family nucleus. For Plus and Prime flats, the SC member’s status governs the resale conditions — the SPR spouse co-owns but the SC-only resale restriction (Prime) or income ceiling (Plus/Prime) applies when the flat is later sold. Both spouses’ incomes are counted for grant eligibility and MSR purposes.

Can I apply for two June 2026 BTO projects?

No. Each household may submit only one BTO application per exercise. If unsuccessful or if no suitable unit remains in the ballot, you receive enhanced priority (deferred applicant status) in the next exercise.

Are Prime flats eligible for the EHG grant?

No. Enhanced Housing Grant (EHG) is not available for Prime BTO flats. The EHG is designed to make Standard and Plus housing affordable for middle-income first-timers; Prime flats already carry a significant built-in subsidy through their pricing. The Proximity Housing Grant (PHG) — which gives S$20k–S$30k for buying near parents — is available for Prime flats. Verify the latest grant conditions directly with HDB at the time of application.

Disclaimer: This article is for general information only. All pricing is indicative and based on publicly available industry estimates as at 16 May 2026; actual selling prices will be released by HDB at the time of launch. Grant eligibility and amounts are subject to HDB review and may change. Always verify the latest requirements at hdb.gov.sg before making housing decisions. Monthly instalment figures are illustrative only.

The Build-To-Order (BTO) flat is the default starting point for most Singaporean households — subsidised, brand-new, and built on land released by the Housing & Development Board (HDB) only when there are enough committed buyers. In 2026, every BTO launch in a mature estate sees a 4-7x oversubscription rate; popular projects in Queenstown or Kallang/Whampoa cross 10x. That ballot pressure is why understanding the eligibility schemes, income ceilings, grant stack, and Ethnic Integration Policy quota is the single most leveraged hour you will spend before keying in your application.

This 2026 guide walks you through every gate — from the four eligibility schemes and the S$14,000 income ceiling, through the ballot mechanics and queue numbers, into the grants stack that can knock S$80,000 off your purchase price, and the EIP/SPR quota that decides which racial profiles can bid for which units. Figures reflect HDB’s policy stack as at April 2026.

Quick Answer — BTO at a glance

Income ceiling: S$14,000 (combined, family scheme); S$21,000 (extended-family or joint singles); S$7,000 (single SC, 2-room Flexi only).

Citizenship: at least one Singapore Citizen for any scheme except Joint Singles (which requires all SC).

Minimum age: 21 for couples; 35 for singles applying alone.

Ballot: queue number is randomly drawn within priority groups; first-timers get up to 3 queue numbers (vs 1 for second-timers).

Top grant stack (first-timer SC+SC): EHG S$120k + Family Grant S$80k + Proximity Grant S$30k = up to S$230k for resale; up to S$80k for BTO.

EIP/SPR quotas: apply at both block and neighbourhood level; a unit may show as “quota reached” for your race even if available physically.

Application fee: S$10 non-refundable; ballot results in 4–6 weeks.

What is BTO and Why Does the Scheme Exist?

The Build-To-Order scheme is HDB’s primary public-housing supply channel: instead of speculatively building flats and trying to sell them, HDB collects applications first and only proceeds to construction when at least 65–70% of units in a project have committed buyers. The buyer commits early (signing the lease and paying the 5% downpayment) and waits 3.5–4.5 years for completion, in exchange for a steeply subsidised price relative to comparable resale stock.

The scheme replaced an earlier system called Registration for Flats (RFS) in April 2002 and has since become the dominant route for first-time HDB buyers. Roughly 20,000–25,000 BTO flats are launched per year across four launches (typically February, May, August, November). The 2026 supply target announced by the Ministry of National Development is 22,000 units.

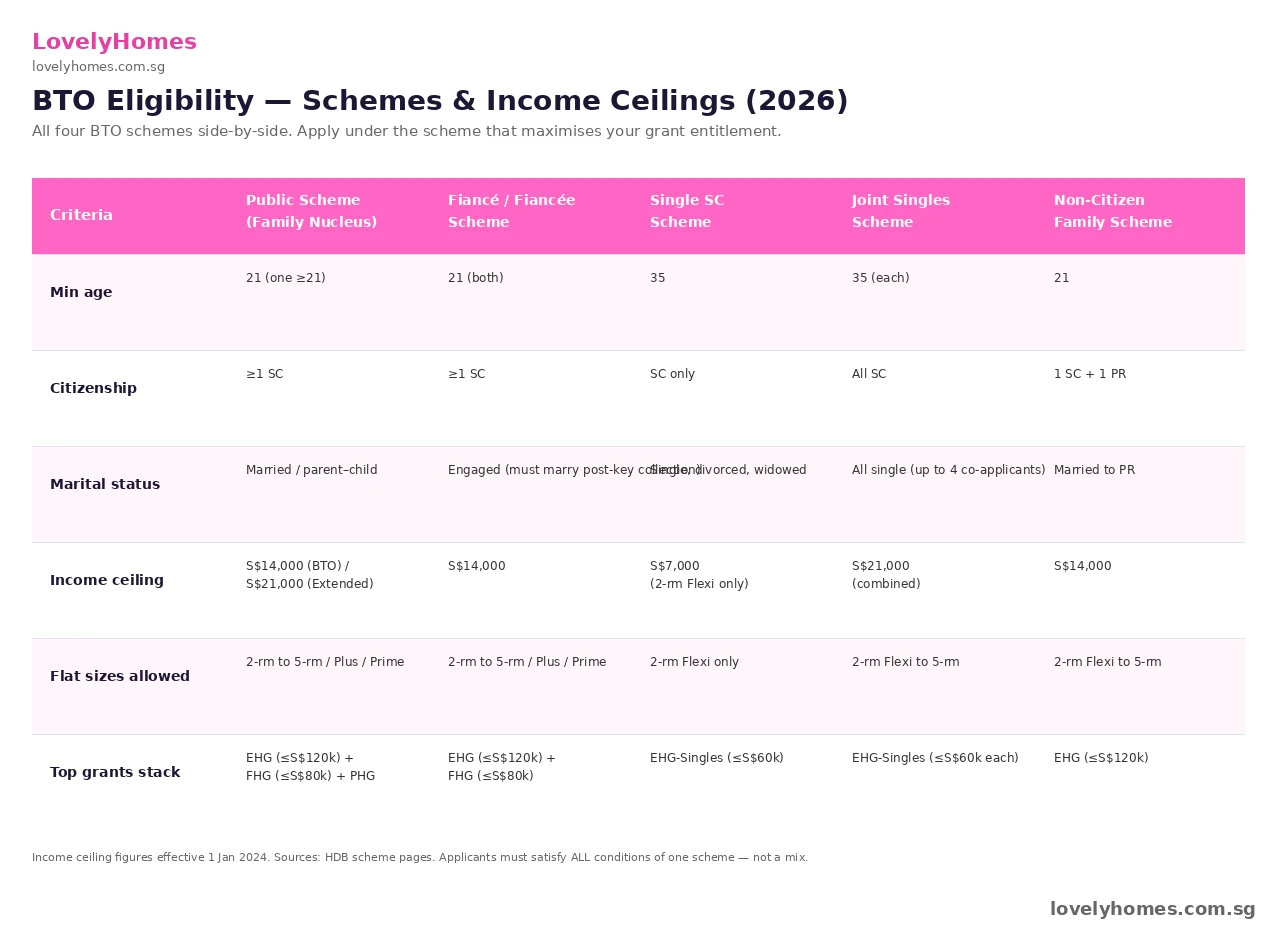

The Five Eligibility Schemes — Pick One

HDB classifies every applicant into exactly one of five schemes. Your scheme determines the income ceiling, age limits, allowed flat sizes, and the grant stack you qualify for. Choosing the right scheme is not optional — HDB will reject the application if you fit one scheme but apply under another.

Figure 1: All five BTO eligibility schemes side-by-side — pick the one that maximises your grant entitlement.

Public Scheme (Family Nucleus)

The default scheme for married SC couples or parent-child households. At least one applicant must be a Singapore Citizen and at least one must be 21 or older. Combined gross household income is capped at S$14,000 for a standard application, or S$21,000 for an Extended-Family application (applicant + parents). The full range of flat types is available — 2-room Flexi to 5-room and 3Gen, including Plus and Prime locations.

Fiancé/Fiancée Scheme

For couples not yet married. Both applicants must be 21 or older and at least one a Singapore Citizen. The S$14,000 ceiling applies. The catch: you must produce a marriage certificate within 3 months of key collection, otherwise HDB has the right to repossess the unit. Couples who break off the engagement before key collection can withdraw without forfeiting the option fee.

Single Singapore Citizen Scheme

For singles aged 35 or older holding Singapore Citizenship. Only 2-room Flexi flats are available, and only in selected non-mature estates. Income ceiling is S$7,000. Couples who do not qualify under the Family or Fiancé schemes (e.g. one party is a foreigner) cannot use this route — it is genuinely a singles-only scheme.

Joint Singles Scheme

Two to four singles aged 35+ may co-apply. All must be Singapore Citizens. The combined income ceiling rises to S$21,000. Flat types extend up to 5-room. Joint singles must all hold equal shares; ownership cannot be reorganised after key collection. This scheme is increasingly used by adult siblings and long-term unmarried partners.

Non-Citizen Family Scheme

Where a Singapore Citizen is married to a Singapore Permanent Resident. The SC applicant must be 21 or older, the income ceiling sits at S$14,000, and only 2-room Flexi to 5-room flats are available (Plus and Prime are off-limits). Note: a Singapore Citizen married to a foreigner who is not a PR cannot apply under any HDB scheme — the household must wait for the foreigner to obtain PR status.

Income Ceilings — What Counts and How They Calculate

HDB’s income ceiling is based on average gross monthly household income. “Gross” means before CPF and tax. “Average” means the trailing 12-month average for salaried income; for variable income (commissions, bonuses, self-employment), HDB uses the most recent 24 months, divides by 24, then adds a 30% buffer to be conservative.

Applicants must submit Notice of Assessment (NOA) tax statements, the latest 3 months of payslips, and an Income Declaration (IRAS-issued for self-employed). HDB cross-checks against IRAS records. Inflated declarations to qualify for higher grants will be caught at the HFE (HDB Flat Eligibility) letter stage and the application rescinded; the ban from re-applying is 5 years.

For couples planning a BTO purchase but expecting one party to receive a windfall bonus or commission, timing matters: buy now while the trailing-12-month average is still under the ceiling, or wait until the 12 months have rolled past the bonus event.

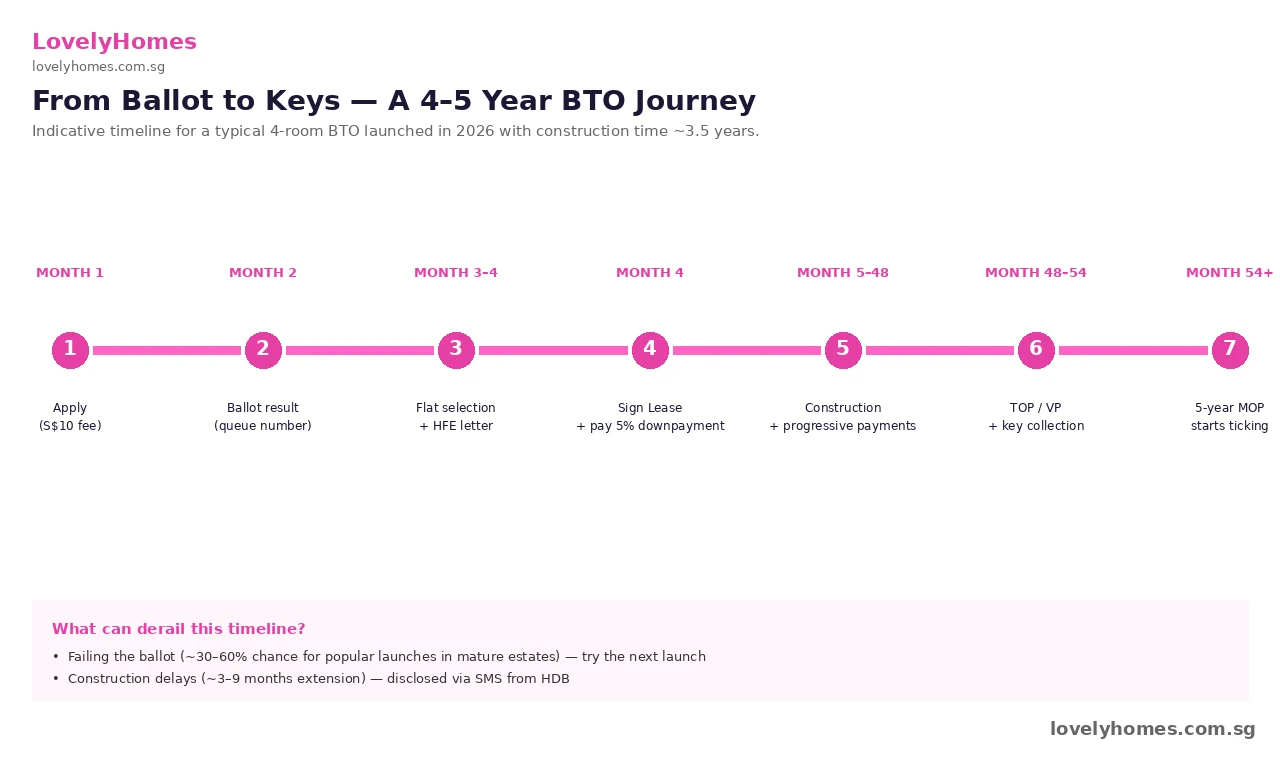

The Application Process — What to Do, In Order

Figure 2: Indicative 4–5 year BTO journey from ballot to key collection.

The mechanics of a BTO application have not changed materially since 2018, but the digital tooling has. Today every step bar key collection happens through the HDB Flat Portal and CPF/MyInfo integration:

Obtain HFE Letter — the HDB Flat Eligibility letter (introduced 9 May 2023) bundles eligibility assessment, grant assessment, and loan eligibility into one document valid for 6 months. You need it before you can apply for any BTO. Generated through the HDB Flat Portal in 21 working days; lenders use it to issue an in-principle approval.

Application window — each launch opens for 7 days. Apply via the HDB Flat Portal; the application fee is S$10 non-refundable. Applicants choose up to two flat types in their preferred town.

Ballot — 3–5 weeks after close. Each application is randomly drawn within its priority group (First-Timer Family, First-Timer Single, Second-Timer, etc.) and assigned a queue number. First-timers receive up to 3 queue-number chances (the “3 queue numbers” rule introduced in 2022); second-timers receive 1.

Flat selection appointment — you are booked into a 4-hour slot starting from queue number 1 onward. Lower queue numbers see the full selection; later applicants see only what is left. Bring your spouse, your HFE letter, and the option fee (S$500–2,000 by flat type, paid by NETS).

Sign Agreement for Lease — about 4 months after selection. You pay 5% downpayment, less the option fee already paid. Funds may come from CPF OA + cash; if you are taking an HDB concessionary loan, no cash is required.

Construction — typically 3.5–4 years. HDB releases progress updates by SMS and the Flat Portal.

Notice of Vacant Possession + Key Collection — the final 5% of the price is paid; you collect keys and the 5-year Minimum Occupation Period (MOP) clock starts ticking.

The Ballot — How Queue Numbers Are Decided

The single biggest source of confusion among first-time applicants is the difference between “ballot” and “flat selection”. The ballot determines your queue number; flat selection is when you actually pick a unit. The queue is sequenced by:

Priority groups (in order): Married Couples Priority Scheme (MCPS); Parenthood Priority Scheme (PPS); Multi-Generation Priority Scheme (MGPS); Tenants Priority Scheme; First-Timer Family; First-Timer Single; Second-Timer; Joint Singles.

Within a priority group: a random ballot.

Tiebreakers: later launches have started using the SC1 (sole-citizen 1-applicant) tiebreaker first.

Practical implication: a first-timer SC+SC couple with one child applying under PPS gets a meaningfully better queue position than the same couple without the priority application. Each launch reserves 30% of supply for first-timers, with the balance for second-timers and singles — so even a poor queue number does not necessarily mean exclusion if you are a first-timer.

The EIP and SPR Quotas — Why “Available” Doesn’t Mean “Available to You”

The Ethnic Integration Policy (EIP) was introduced in 1989 to prevent the formation of mono-ethnic enclaves. Every HDB block and every neighbourhood has a maximum proportion of flats that may be sold to each ethnic group:

Chinese: 84% of a neighbourhood, 87% of a block.

Malay: 22% of a neighbourhood, 25% of a block.

Indian / Other: 10% of a neighbourhood, 13% of a block.

The Singapore Permanent Resident (SPR) Quota sits on top of EIP and limits the proportion of non-Malaysian SPR households per neighbourhood (5%) and per block (8%). Malaysian SPRs are exempt because they are considered demographically and culturally close to Singaporean groups.

Each unit at flat selection shows the live EIP/SPR status. A unit may be physically vacant but unavailable to your ethnic group because the quota is full. You see this most acutely in popular projects in Bishan, Queenstown, or Bukit Merah, where Chinese-quota units sell out first while Indian-quota units may still be open at queue number 200+. Plan your back-up unit choices accordingly.

Grants — The Stack That Can Pay for Your Furniture

For BTO applicants, grants are awarded in fewer types than for resale buyers, but the absolute amounts are still material. As of 1 February 2024 the BTO-side grants are:

Enhanced CPF Housing Grant (EHG): S$5,000 to S$120,000 sliding scale by household income. The full S$120k is available for households earning up to S$1,500/month; the grant tapers to S$5,000 at the S$9,000–9,500 income band.

Family Grant: S$10,000 to S$80,000 depending on flat type and income, available only for resale BTO and for Plus/Prime BTO under the new classification. Standard BTOs do not qualify (the subsidy is built into the price).

Proximity Housing Grant (PHG): S$30,000 if buying with parents living in the same household; S$15,000 if buying within 4 km of parents’ existing flat.

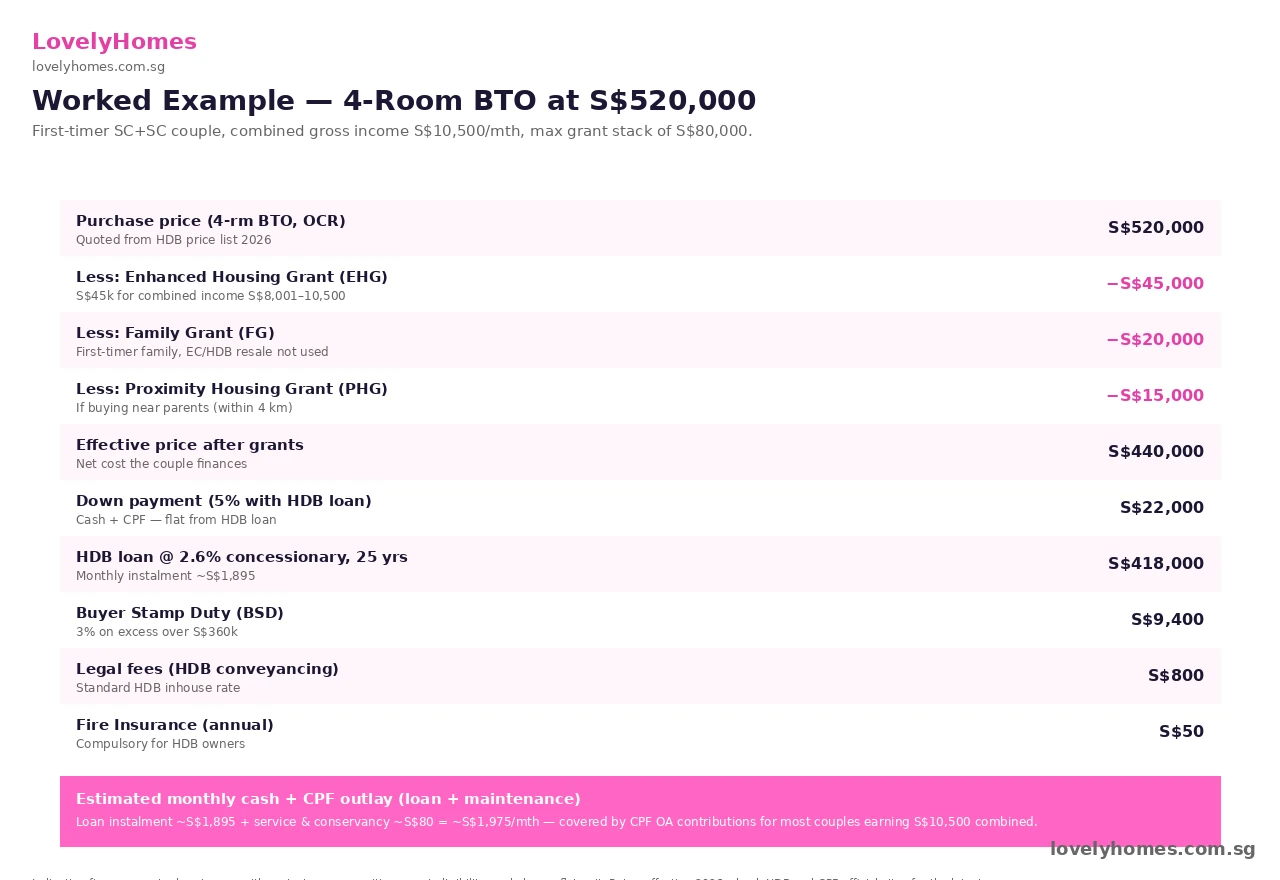

Figure 3: Worked example — SC+SC couple buying a S$520K 4-room BTO with a S$80K grant stack.

BTO Classification — Standard, Plus, Prime

From October 2024 onwards, every new BTO is classified as Standard, Plus, or Prime. This shifts the subsidy structure and the resale rules:

Standard: the legacy framework. 5-year MOP, no resale-price clawback, no income ceiling on the resale buyer. The default for non-mature estates.

Plus: 10-year MOP, income ceiling of S$14k applies even on resale, partial subsidy clawback at resale. Found in choicer locations within outer-mature estates.

Prime: 10-year MOP, S$14k income ceiling on resale, 6% subsidy clawback, no whole-flat rental ever (only room rental). Reserved for the most attractive locations like Queenstown and Kallang/Whampoa.

The classification affects your effective return on the flat 10 years out. A Plus flat in Hougang sold to a quota-restricted resale buyer will trade at a discount to the equivalent Standard flat in nearby Sengkang — that is the design intent, to keep the subsidy in the public-housing system.

Worked Example — SC+SC Couple, Combined S$10,500/Month

Take a 32-year-old + 30-year-old SC+SC couple, married, no children, combined gross income S$10,500/month. They are first-timers and applying under the Family Scheme. They target a 4-room BTO at S$520,000 in Punggol Coast (a Standard project).

Income ceiling check: S$10,500 < S$14,000. PASS.

Grants: EHG at the S$8,001–10,500 income band = S$45,000. Family Grant: not applicable for Standard BTOs. PHG: S$15,000 if their parents live within 4 km. Total: S$60,000.

BSD: 1% on first S$180k + 2% on next S$180k + 3% on next S$160k ≈ S$8,200, payable in cash or CPF OA.

Legal fees (HDB conveyancing): ~S$800.

Total upfront cash + CPF outlay: ~S$32,000 (downpayment + BSD + legal + option fee). Monthly outlay during construction: ~S$95/month service & conservancy charges only. Monthly outlay after key collection: ~S$2,070 (loan + S&C). Against a household income of S$10,500/month gross (~S$8,400 take-home), the loan is comfortably within the 30% MSR (Mortgage Servicing Ratio) limit for HDB loans.

Common Mistakes BTO Applicants Make

Skipping the HFE letter — without it, you cannot apply. Generate the HFE 6–8 weeks before the launch you want.

Choosing a project where your ethnic quota is already full — check the EIP status on the launch site before applying.

Underestimating the income ceiling buffer — HDB adds a 30% buffer for variable income. Sit just under the ceiling, not at it.

Applying as Family before marriage — if you are not yet married, you must use the Fiancé scheme. The Family scheme is for already-married couples.

Ignoring the 5-year MOP — or now 10-year for Plus/Prime. The MOP starts on key collection, not application; selling within MOP requires HDB’s express consent and is rarely granted.

What This Means for You

For most Singaporean first-timer households, BTO remains the single most subsidised real-estate transaction available. A successful 4-room BTO in 2026 typically delivers a paper gain of 60–100% by the end of the 5-year MOP — not because the project is special, but because the price gap between BTO and resale is structurally maintained. The key is winning the ballot. Increase your odds by applying under the right priority scheme (PPS for couples with children, MCPS for newlyweds), targeting non-mature estates where oversubscription is lower, and being flexible on flat type (4-room ballots have higher success rates than 5-room).

What Might Come Next

The Ministry of National Development has signalled three policy directions for the 2026–2028 horizon. First, BTO supply is forecast to remain at 22,000–25,000 per year through 2028, after which the pipeline tapers to 18,000 as the demographic bulge passes. Second, the Plus/Prime classification is expected to be applied to roughly 30% of new launches by 2028, up from ~15% in 2025. Third, the Joint Singles Scheme age threshold may be lowered from 35 to 30 if the Singapore Together Forward dialogue feedback gains policy traction. None of these is yet officially confirmed; watch the COS speech each March for the firm announcements.

Summary — Eligibility & Grant Stack by Scheme (Quick Reference)

Scheme

Min Age

Citizenship

Income Ceiling

Flat Sizes

Top Grant Stack

Public (Family Nucleus)

21 (one)

≥1 SC

S$14,000

2-rm to 5-rm + 3Gen

EHG up to S$120k + PHG S$30k

Fiancé/Fiancée

21 (both)

≥1 SC

S$14,000

2-rm to 5-rm

EHG up to S$120k + PHG

Single SC

35

SC only

S$7,000

2-rm Flexi only

EHG-Singles up to S$60k

Joint Singles

35 (each)

All SC

S$21,000 (combined)

2-rm Flexi to 5-rm

EHG-Singles up to S$60k each

Non-Citizen Family

21 (SC)

1 SC + 1 PR

S$14,000

2-rm Flexi to 5-rm

EHG up to S$120k

Frequently Asked Questions

Can I apply for a BTO if I already own a private property?

Yes, but you must dispose of your private property within 30 months of key collection of the BTO. If you fail to do so, HDB may compulsorily acquire the BTO at original cost. The 30-month window is intended to allow for sale logistics. You also forfeit any first-timer status — you will be treated as a second-timer for grant calculations. Most second-time HDB applicants in this position are downsizing from a private property after children leave home, or rebalancing portfolios after en-bloc proceeds.

How long does the entire process take, from application to keys?

Plan for 4 to 4.5 years from application close to key collection on a typical BTO project, with a further 5 years (Standard) or 10 years (Plus/Prime) of Minimum Occupation Period before you can sell. The construction stage is the longest phase — typically 36–48 months from breaking ground. Projects in Tengah and Punggol have generally tracked the lower end; mature-estate projects in Queenstown and Bishan have hit the upper end due to site constraints.

What happens if I fail the ballot?

You forfeit only the S$10 application fee and may apply again at the next launch. There is no penalty or queue-number penalty for non-selection — in fact, first-timers retain their first-timer status and the 3-queue-number allocation. Many couples cycle through 4–6 launches before securing a unit in their preferred town. To shorten the wait, broaden the geographies you are willing to apply in, or apply under a priority scheme like Parenthood Priority if you have children.

Can I use a private bank loan instead of an HDB concessionary loan?

Yes — bank financing is allowed for BTO buyers, and currently many do because SORA-pegged floating rates have hovered around 3.5–3.8% (vs the HDB concessionary rate at 2.6%, fixed at CPF OA + 0.1%). The trade-off: bank loans require a 25% downpayment (5% cash + 20% cash/CPF) instead of the 0% cash + 20% CPF on an HDB loan. Once you choose bank financing for your first BTO, you cannot switch back to an HDB concessionary loan for the same flat. Most first-timer BTO buyers stay on the HDB loan for the cash-flow flexibility.

If we are not yet married, can we still apply?

Yes — under the Fiancé/Fiancée Scheme. Both applicants must be 21+ and at least one a Singapore Citizen. You declare your intention to marry; HDB requires you to produce a marriage certificate within 3 months of key collection. If the relationship breaks down before key collection, you may withdraw from the application and forfeit only the option fee — HDB will not pursue you for damages.

How does the EIP affect resale value of my flat?

The EIP can constrain the buyer pool when you eventually sell. If your block’s Chinese quota is full and you are Chinese, you can only sell to a non-Chinese buyer — which is a smaller market and typically yields a 1–3% price discount. The reverse is also true: minority-quota sellers in mature estates often see a small premium. Most owners do not feel this until they list; consult your conveyancing lawyer for an EIP-aware listing strategy.

Can I rent out my BTO flat after MOP?

For Standard BTOs: yes, after the 5-year MOP, you may rent out the entire flat under HDB’s Whole Flat Rental scheme (subject to a 6-monthly registration). For Plus and Prime BTOs: only room rental is permitted, never whole-flat rental. The whole-flat rental rule is a permanent restriction designed to keep the subsidy in the owner-occupier pool. Non-citizen sub-tenant quotas also apply: the Non-Citizen Quota caps non-Malaysian PRs at 5% of a neighbourhood and 8% of a block.

This guide is for general information only and does not constitute legal, financial, or housing advice. Eligibility schemes, income ceilings, grant amounts, EIP/SPR quotas, and BTO classification rules are illustrative as at April 2026 and are subject to change at the discretion of the Housing & Development Board, the Ministry of National Development, and the Central Provident Fund Board. Always verify the latest figures with primary sources — the Housing & Development Board, the CPF Board, the Inland Revenue Authority of Singapore, and consult a qualified housing consultant or conveyancing lawyer before signing any agreement.

First-timer families can receive up to S$80,000 in Enhanced CPF Housing Grant (EHG) for BTO or resale flats (household income ≤ S$9,000/month).

Singles buying a 2-Room Flexi BTO qualify for up to S$40,000 EHG (individual income ≤ S$4,500/month).

Resale buyers can stack the Family Grant (up to S$50,000) with the EHG and the Proximity Housing Grant (PHG, up to S$30,000) — potentially S$160,000 in total grants.

The PHG has no income ceiling and rewards buyers who live near or with parents or children.

All CPF grants go into your CPF Ordinary Account (OA) and are used against the purchase price — but they accrue interest that must be refunded upon sale.

Grants do not eliminate your cash component of the downpayment — at least 5% cash is still required for bank loans.

Applications are via the HDB flat portal and must be completed before exercising the Option to Purchase (OTP).

What Are CPF Housing Grants and Who Administers Them?

CPF Housing Grants are direct subsidies paid by the Singapore Government into the buyer’s CPF Ordinary Account (OA) to help Singaporeans afford their first — and in some cases, second — HDB flat. They are administered jointly by the Housing & Development Board (HDB) and the Central Provident Fund Board (CPF Board), with eligibility rules updated periodically to reflect prevailing market conditions and government housing policy.

Unlike an ABSD remission or a bank subsidy, a CPF Housing Grant is a genuine cash transfer from the public purse into your CPF OA. It immediately reduces the amount you need to borrow or fund from savings, which lowers your monthly mortgage instalment. However, grants are not free in the accounting sense: when you eventually sell the flat, the grant amount — plus accrued interest at the CPF OA rate of 2.5% per annum — must be refunded back into your CPF OA. The net effect is deferred rather than eliminated cost.

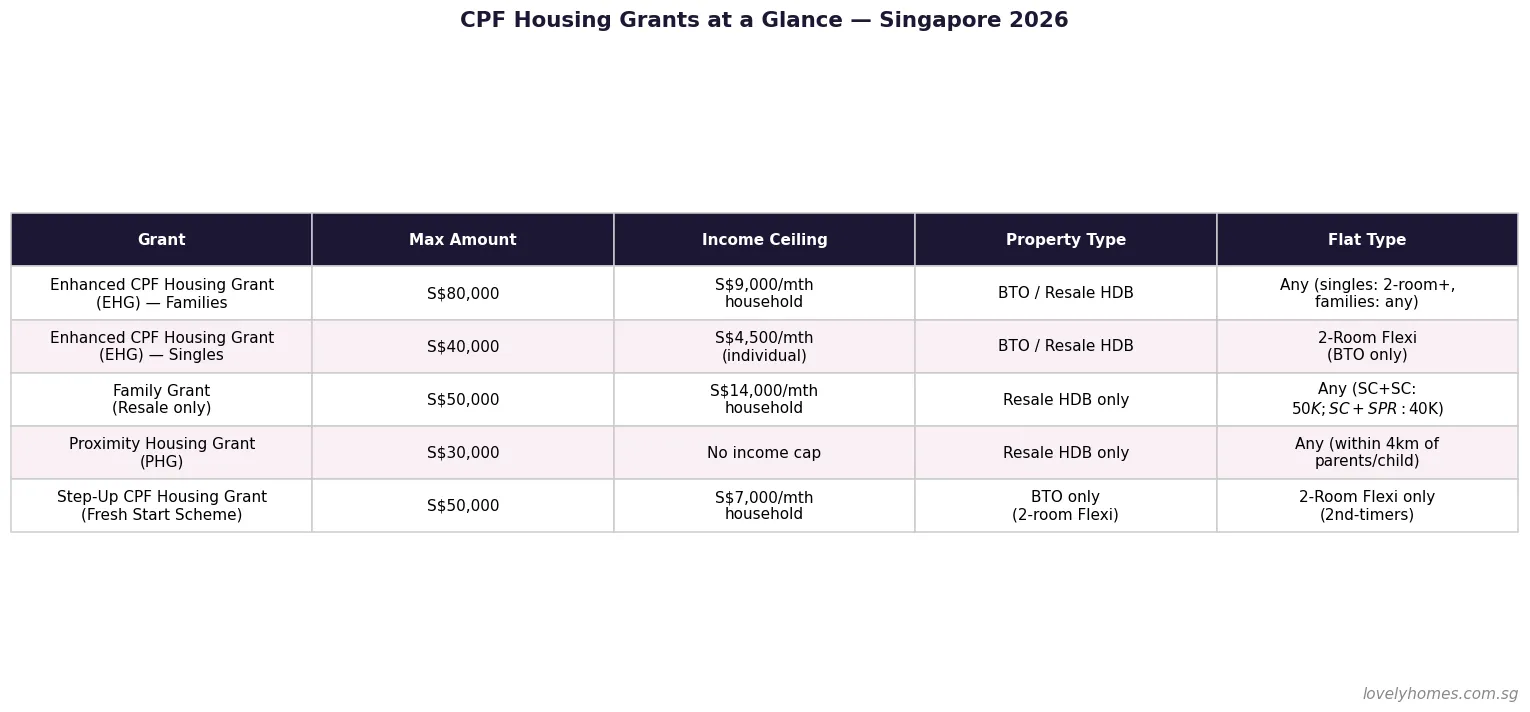

As of 26 April 2026, the key grant types in force are the Enhanced CPF Housing Grant (EHG), the Family Grant, the Proximity Housing Grant (PHG), and the Step-Up CPF Housing Grant for eligible second-timers under the Fresh Start Housing Scheme.

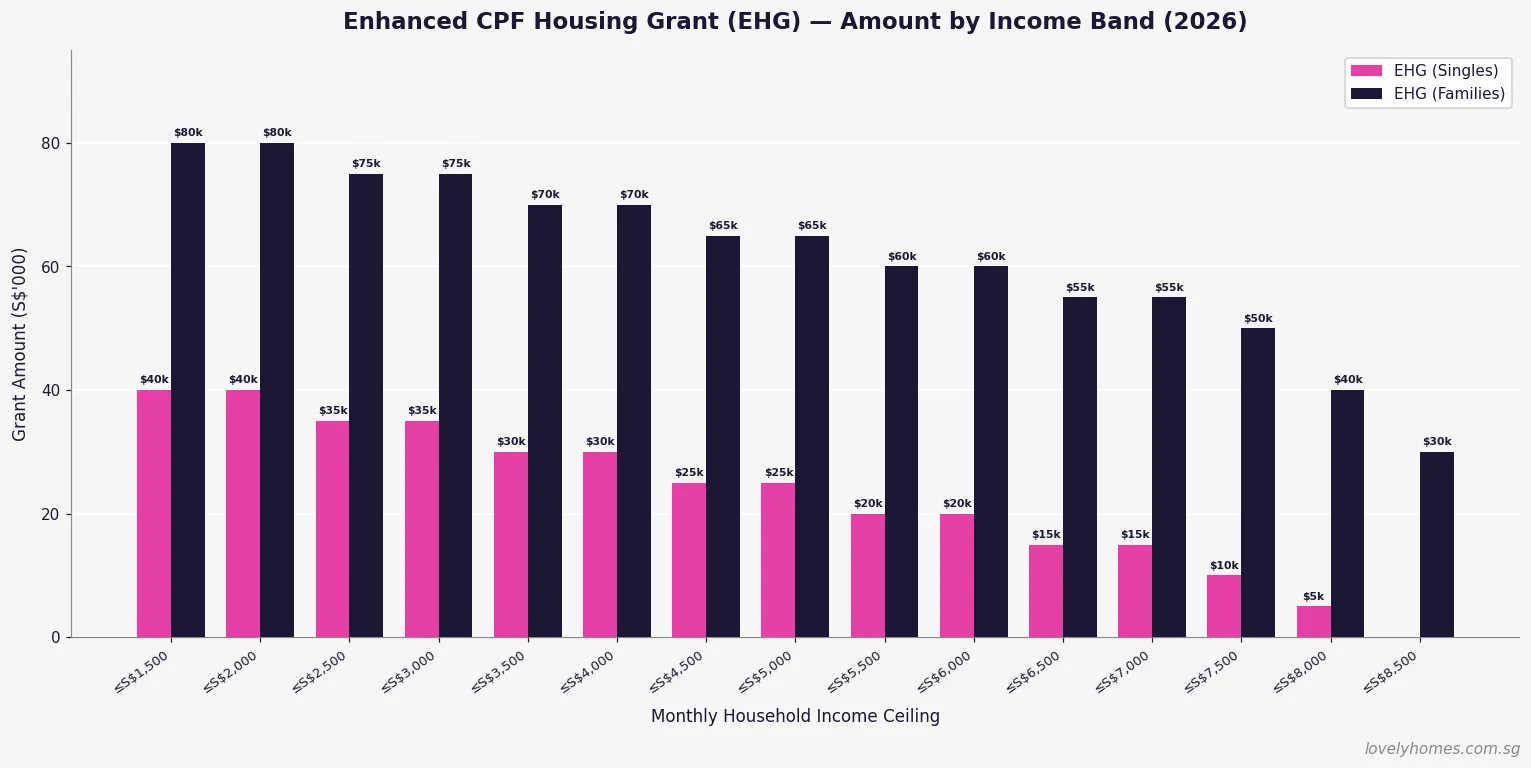

Enhanced CPF Housing Grant (EHG) — Rates and Eligibility

The Enhanced CPF Housing Grant, introduced in September 2019 to replace the Additional CPF Housing Grant (AHG) and Special CPF Housing Grant (SHG), is the flagship subsidy for first-timer buyers. It is progressive — the lower the household income, the higher the grant — and applies to both new BTO flats and resale HDB flats, making it more flexible than its predecessors.

Figure 1: EHG amounts (S$’000) for singles vs families, by monthly household income band. Source: HDB (2026).

EHG for Families

For married or engaged couples — including those applying under the Fiancé/Fiancée Scheme — the EHG ranges from S$5,000 (household income ≤ S$8,000/month) to S$80,000 (household income ≤ S$1,500/month). The income assessed is the average gross monthly income of both applicants over the 12 months preceding the application. If the combined household income exceeds S$9,000/month, no EHG is payable.

EHG for Singles

First-timer singles aged 35 and above buying a 2-Room Flexi BTO flat in a non-mature estate qualify for EHG on a scaled basis, up to S$40,000 (individual income ≤ S$1,500/month). A single with income ≤ S$4,500/month qualifies for a minimum S$5,000 grant. Singles buying resale flats under the Single Singapore Citizen (SSC) scheme are also eligible, provided they purchase a 5-room flat or smaller.

Monthly Gross Income (Household)

EHG — Families

EHG — Singles

≤ S$1,500

S$80,000

S$40,000

≤ S$2,500

S$75,000

S$35,000

≤ S$3,500

S$70,000

S$30,000

≤ S$4,500

S$65,000

S$25,000

≤ S$5,500

S$60,000

S$20,000

≤ S$6,500

S$55,000

S$15,000

≤ S$7,500

S$50,000

S$10,000

≤ S$9,000

S$30,000–S$40,000

Not eligible

Family Grant — For Resale HDB Buyers

The Family Grant is available exclusively to buyers of resale HDB flats and is stackable on top of the EHG. It acknowledges that resale flat prices in many estates carry a premium over BTO prices, and provides an additional buffer for buyers who prefer a specific location or immediate occupancy over the BTO ballot process.

The Family Grant is administered by HDB and paid into the CPF OA of eligible applicants. Key parameters as of 2026:

SC + SC couple or family: S$50,000

SC + SPR couple or family: S$40,000

Singles (SSC scheme, resale 5-room or smaller): S$25,000

Income ceiling: S$14,000/month combined household income

Flat type restriction: any resale flat type; no restriction by town or estate

The S$14,000/month income ceiling makes the Family Grant accessible to many dual-income professional couples who earn too much for the EHG but still value the additional subsidy when purchasing resale.

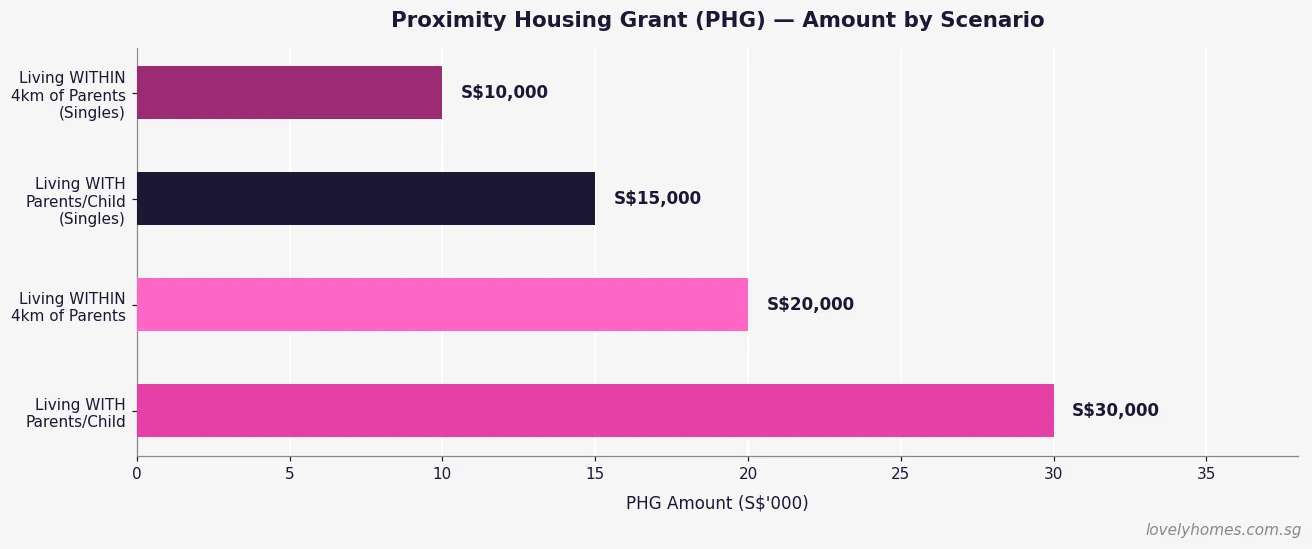

Proximity Housing Grant (PHG) — Rewarding Family Ties

Introduced in August 2015, the Proximity Housing Grant is one of the most distinctive features of Singapore’s housing policy. It uses a direct cash subsidy to incentivise multi-generational proximity — encouraging adult children to live near, or with, their elderly parents. It applies only to resale HDB flats and has no income ceiling, meaning higher-earning buyers can benefit too.

Figure 3: PHG amounts by proximity scenario, for families and singles. Source: HDB (2026).

The PHG has four tiers based on whether you are buying as a family or single, and whether you are moving with parents or children (same household) or within 4 km of them:

Buyer Type

Living With Parents/Child

Living Within 4 km

Families (married/engaged couples)

S$30,000

S$20,000

Singles (SSC scheme)

S$15,000

S$10,000

The “living with” criterion requires the parent or child to be registered on the same flat as an occupier. The “within 4 km” criterion uses the straight-line distance between postal codes, verified at the point of application. The PHG is a one-time benefit — once received, it cannot be claimed again on a subsequent flat purchase.

Step-Up CPF Housing Grant — Fresh Start Scheme

The Step-Up CPF Housing Grant is a targeted measure for a specific group: second-timer applicants who previously owned a subsidised flat and now qualify for a second chance at affordable owner-occupied housing under HDB’s Fresh Start Housing Scheme, which was introduced in October 2016 and expanded over subsequent years.

Eligibility is tightly defined: second-timer families with at least one child aged under 16; monthly household income ≤ S$7,000; must apply for a 2-Room Flexi BTO flat; must not currently own a flat or private residential property; and must fulfil a 5-year Fresh Start Housing Scheme Minimum Occupation Period on the new flat. The grant amount is up to S$50,000. It is not stackable with the EHG.

CPF Housing Grants at a Glance — Summary Table

Figure 2: Summary of all CPF Housing Grant types — amounts, income ceilings, and eligible property types. Source: HDB / CPF Board (2026).

Worked Example — Maximum Grant Stack for a Resale Buyer

Scenario: SC + SC First-Timer Couple, Resale Flat Near Parents

Buyer profile: Mr and Mrs Tan — married, both Singapore Citizens, first-timer applicants. Combined monthly gross income: S$6,800. Mrs Tan’s parents reside in the same block as the resale flat they are purchasing in Ang Mo Kio.

EHG (family, income band S$6,500–S$7,500): S$50,000

Family Grant (SC + SC, resale): S$50,000

PHG (same block as parents = “living with”): S$30,000

Total grants: S$130,000

Purchase price: S$600,000 (4-Room resale, Ang Mo Kio) Effective net cost after grants: S$470,000 (before stamp duties and legal fees). BSD on S$600,000: approximately S$12,600. ABSD: Nil (first residential property, Singapore Citizen buyers). Legal / conveyancing fees: approximately S$2,500–S$4,000.

Taking an HDB concessionary loan at 90% LTV: loan = S$540,000 less S$130,000 grants = S$410,000 loan needed, reducing the monthly instalment significantly versus purchasing without grants.

The CPF Accrued Interest Rule — The Hidden Cost of Grants

Every dollar drawn from your CPF OA — including grant monies — accrues interest at the CPF OA rate (currently 2.5% per annum). When you sell the flat, the CPF Board requires you to refund the principal amount used (including grants) plus the hypothetical interest that amount would have earned in the OA. This refund is returned to your CPF OA — not the government — and is available for future use in retirement or a subsequent property purchase.

Practical implication: a S$80,000 EHG held for 10 years accrues approximately S$22,000–S$25,000 in interest (compounded at 2.5% p.a.), bringing the total CPF refund for the grant alone to roughly S$102,000–S$105,000. Plan for this when modelling net sale proceeds on exit. If the sale price is insufficient to cover the full CPF refund, you keep the shortfall — you are not personally liable to top up the difference.

Why CPF Housing Grants Matter for Singapore’s Property Market

CPF Housing Grants fulfil a dual function in Singapore’s property ecosystem. At the individual level, they represent one of the most powerful demand-side subsidies in the world — transferring significant public funds directly to low- and middle-income buyers to help them achieve owner-occupation without over-relying on private financing. At the market level, they compress effective pricing for first-timers in the HDB resale segment, sustaining affordability across economic cycles.

The 2019 introduction of the EHG deliberately raised the income ceiling to S$9,000/month (from S$6,000/month under the legacy AHG/SHG regime), reflecting the Government’s recognition that median household incomes had risen and the historical ceilings were excluding a growing segment of first-timers who genuinely needed assistance.

Compared with equivalent policies in Hong Kong — where the Home Ownership Scheme provides a flat discount on market price rather than a direct grant — or Australia, where the First Home Owner Grant is a modest flat sum, Singapore’s progressive, stackable grant framework is both more generous and more targeted to income need.

What Might Come Next — Grant Policy Outlook for 2026–2028

The CPF Housing Grant framework is reviewed periodically in tandem with BTO flat pricing and HDB resale indices. Three plausible near-term developments:

EHG income ceiling revision: With household income growth continuing, HDB may raise the S$9,000/month family ceiling to extend coverage to the lower-professional bracket — especially as Prime Location Public Housing (PLH) flat prices edge towards S$700,000–S$800,000 in central estates.

PHG extension to BTO buyers: Currently restricted to resale buyers, extending the PHG to BTO buyers in family-friendly towns like Tengah and Bidadari has been discussed in policy circles, though not confirmed as of this date.

Grant indexing to flat type or BTO pricing band: A flat S$80,000 EHG ceiling becomes proportionally less meaningful as PLH BTO prices climb. Grant amounts indexed to flat type could better reflect affordability gaps across different segments.

These are speculative. Always verify current grant levels at the HDB Grant Eligibility page before exercising any OTP.

Frequently Asked Questions

Can I use CPF Housing Grants towards the downpayment?

Grants are credited into your CPF OA and can be applied in the same way as your own CPF savings — towards the downpayment, the purchase price, and stamp duties (BSD). However, if you are taking a bank loan, the minimum 5% cash downpayment must be paid in cash; CPF (including grants) cannot cover this component. If you are taking an HDB concessionary loan, there is no mandatory cash component, so grants can fully offset the downpayment requirement alongside your other CPF OA balance.

Can both the EHG and Family Grant be claimed for the same resale flat purchase?

Yes. For resale flat purchases, a first-timer SC couple can claim both the EHG and the Family Grant simultaneously, provided they meet the eligibility criteria for each. If the couple also qualifies for the PHG — for example, buying near parents — that can be added on top. The theoretical maximum for an SC + SC couple buying resale is S$80,000 (EHG) + S$50,000 (Family) + S$30,000 (PHG living-with) = S$160,000, though achieving the maximum EHG requires a household income ≤ S$1,500/month, which is uncommon for buyers at today’s resale prices.

Does receiving a CPF Housing Grant affect my HDB Loan Eligibility (HLE)?

Grants and HLE are assessed separately. Your HDB Loan Eligibility letter determines the maximum HDB concessionary loan you can borrow, based on income, credit history, outstanding debts, and MSR/TDSR compliance. Grants reduce the net amount you need to borrow, but the HLE loan quantum is not directly inflated by the grant. You apply for both the HLE and the grant through the HDB flat portal before exercising the OTP.

I am a Singapore Permanent Resident married to a Singapore Citizen. What grants are we eligible for?

An SC + SPR couple counts as a mixed-citizenship household for CPF grant purposes. You are eligible for the EHG at the family rate (since one applicant is SC), the Family Grant at the reduced SC + SPR amount of S$40,000, and the PHG if applicable. You are not eligible for the full SC + SC Family Grant of S$50,000. The SPR spouse’s income is included in the combined household income calculation for EHG and Family Grant means-testing.

What happens to my grant if I divorce after purchasing the flat?

Divorce does not trigger a grant clawback. The grant remains in the CPF OA of the respective owner(s) and normal CPF refund-on-sale rules apply. However, if the divorce results in one party retaining the flat and the other being bought out, the outgoing party’s CPF contributions — including grant amounts attributed to them — must be refunded at that point, with accrued interest. This is handled through the matrimonial asset division process, usually with the assistance of a family law solicitor.

Can I appeal for a higher grant if my income is irregular or I am self-employed?

Yes. HDB uses average gross monthly income over the 12 months preceding the application for means-testing. If your income is irregular — for example, you are a freelancer, commission-based worker, or recently returned to employment — HDB has a declared income process for the self-employed and an appeal mechanism for unusual circumstances. Supporting documents such as Notice of Assessment from IRAS, payslips, or CPF contribution history are typically required. Speak to an HDB branch officer early in the process if your income situation is non-standard.

Do the grants expire if I do not use them within a certain period?

CPF Housing Grants are credited into your CPF OA at the point of flat purchase — they are not a time-limited voucher. However, your eligibility to receive grants can change: if your income rises above the ceiling before application, or if you purchase a private property before your HDB flat, you may lose eligibility. The grant application must be submitted before you exercise the Option to Purchase, and the grant is disbursed only upon completion of the purchase.

Disclaimer: This article is intended for general information only and does not constitute financial, legal, or tax advice. CPF Housing Grant amounts, income ceilings, and eligibility conditions are subject to change. Always verify current grant details on the official HDB Grant Eligibility page and the CPF Board Home Ownership page. Consult a licensed property agent (CEA-registered) or HDB branch officer before making any purchase decision.

HDB’s May 2026 Build-To-Order launch is expected to open for application in the first week of May, the second launch of the year after the February 2026 exercise. Based on the sites gazetted through URA Government Land Sales in late 2024 and 2025, and on pre-launch developer briefings released by HDB, we preview the likely site mix, expected application rates, and the first-timer vs second-timer allocation picture.

At a glance

May 2026 BTO is expected to launch approximately 6,800 flats across Standard, Plus and Prime categories.

Confirmed launch sites include Bukit Merah (Henderson), Tampines (Tampines North), Tengah (Garden District) and Woodlands (Woodlands North Coast).

Bukit Merah Henderson is the category headliner — Prime location classification; expect application rates above 10x for 4-room.

Family grant framework (Enhanced CPF Housing Grant, Family Grant, Proximity Housing Grant) applies; first-timer ballot weights unchanged.

Applications typically close 7 days after opening; ballot results announced 4–6 weeks later.

What a Plus / Prime BTO classification means for May buyers

The Plus and Prime classifications — introduced under the revised 2024 HDB framework — replace the legacy Mature / Non-Mature framework for new BTO launches. Standard flats follow the traditional BTO rules. Plus flats, typically in choice non-mature locations, carry a 10-year Minimum Occupation Period (up from 5) and subsidy clawback on resale. Prime flats, in the most central and amenity-rich locations, carry the same 10-year MOP plus a resale income ceiling that applies when the flat is eventually sold.

Buyers should model the full hold cycle before ballot. A Prime classification delivers an under-market purchase price and exceptional location, but the 10-year MOP plus resale-income-ceiling combination narrows the eventual buyer pool at exit. For households expecting to stay in the flat 15–20 years, the Prime route is straightforward. For households planning a shorter trade-up, the Standard category is typically the better fit.

Site-by-site expectations

Bukit Merah (Henderson) — Prime classification

Estimated launch: approximately 1,200 flats, 4-room and 5-room mix. The site sits on Henderson Road, about a 5-minute walk from Redhill MRT (East-West Line) and within walking distance of Dawson Estate and Bukit Merah Central. The Prime designation is expected to deliver a substantial price discount vs the adjacent resale market, where four-room flats are transacting in the S$850–S$1,050k band. Expect application rates for 4-room flats above 10x on the first-timer pool.

Tampines (Tampines North) — Plus classification

Estimated launch: approximately 1,600 flats, full mix from 2-room Flexi to 5-room. The site is adjacent to the Tampines North MRT (Cross Island Line Stage 1, opened late 2024) and sits in a growing mixed-use district bracketed by Tampines Regional Centre and Tampines North Park. The Plus classification carries a 10-year MOP but no resale-income ceiling. Expect application rates of 4–6x on 4-room flats.

Tengah (Garden District) — Standard classification

Estimated launch: approximately 2,400 flats, the largest single-site batch of the May 2026 launch. The Tengah Garden District is the western master-planned town pioneered as Singapore’s first car-free town centre. The Jurong Region Line MRT is under construction with stations expected to open progressively from 2027 through 2029. Expect application rates of 2–3x on 4-room flats given the larger supply and the longer MRT wait.

Woodlands (Woodlands North Coast) — Standard classification

Estimated launch: approximately 1,600 flats. The Woodlands North Coast site benefits from the recently opened Thomson-East Coast Line terminus at Woodlands North, cross-border connectivity via the under-construction Johor Bahru-Singapore Rapid Transit System, and the still-developing Woodlands Regional Centre. Expect application rates of 2–3x on 4-room flats.

First-timer, second-timer and quota mechanics

HDB ring-fences a majority of every launch for first-time applicant families — specifically, at least 85% of four-room and larger Standard flats are reserved for first-timer families. Two-timer applicants (families who already own or have previously owned an HDB flat, EC or private property) compete for the remaining quota and typically face ballot odds 2–4x longer than first-timers. Singles and first-timer families under the joint application framework are balloted separately under the 2-Room Flexi scheme.

Prime and Plus flats have the same general first-timer preference but with a further stratification: households with household income under the relevant bracket receive the CPF Housing Grant stack, which can add up to S$80,000 in grants depending on income-group position.

Application tactics for a strong ballot position

Three behavioural points the HDB system rewards. First, ballot entry across multiple launches does not compound — each launch is a fresh lottery. But second-timers who roll over their application to a next launch do receive a small priority-weighting uplift, capped at two rollovers. Second, the Proximity Housing Grant (S$30,000 for applying to live with or near parents) is a strong signal to the ballot system and materially improves odds at Bukit Merah Henderson and Tampines North. Third, the Enhanced CPF Housing Grant is income-tiered — the lowest income tier receives the largest grant, which influences eligibility for Standard categories.

Expected timeline

What May 2026 means for the resale market

A May launch of approximately 6,800 flats is a moderate supply pulse into the BTO pipeline, but the immediate effect on resale is indirect. In the short term, first-timer applicants who commit to a BTO ballot typically withdraw from active resale viewings while waiting for the result, which softens resale transaction volume for 4–6 weeks. If ballot rates are high (as expected for Bukit Merah Henderson), disappointed applicants often re-enter the resale market in late June, which typically produces a small transaction bounce in July. This pattern has been consistent across the last six BTO launch cycles.

Frequently asked questions

When exactly does the May 2026 BTO open for application?

HDB typically announces the exact launch window approximately two weeks before applications open. Based on past May launches, the window usually falls in the first 10 days of May, with applications closing roughly 7 days after opening.

Can I apply for both a BTO and a resale flat at the same time?

You can apply for a BTO while viewing resale flats, but you cannot hold a BTO booking and simultaneously enter a resale HDB agreement. Most applicants use the BTO ballot window to continue resale research; successful balloters decline at booking if they have already committed to a resale.

How much is the ABSD and BSD on a BTO flat?

BTO flats are sold directly by HDB under the Housing & Development Act. Buyers’ Stamp Duty applies on the purchase price at the standard schedule. Additional Buyer’s Stamp Duty does not apply to first-timer BTO applicants buying their first residential property.

What is the difference between Plus and Prime?

Both carry a 10-year MOP and subsidy clawback on sale. Prime adds a resale-income-ceiling constraint at exit — the eventual resale buyer must meet an income ceiling. Plus has no such eventual-buyer constraint.

Can PRs apply for BTO flats?

PR-only households cannot apply for a BTO. A Singapore Citizen applying with a PR spouse or family nucleus can apply under the HDB Fiancé/Fiancée, Family or Joint Singles scheme.

What happens if I decline the allocated BTO flat?

Declining a BTO selection appointment has consequences for future applications: after two non-selections in a 12-month period, HDB may debar the applicant from applying for BTO for a period of up to 12 months. Plan your ballot portfolio carefully.

Source

Source: HDB public information on the BTO launch framework and 2024 revised category system, URA GLS announcements, and public site-gazetting records. Full documentation: HDB BTO flat selection and URA GLS current sites.

Editorial note. This article is based on public-domain data released by HDB, URA, Singapore Land Authority and MAS as at 23 April 2026. All analysis is our own. No marketing-agency research is cited. Figures may be revised in subsequent official releases — always refer to the latest authoritative source before making a housing decision.

Quick Answer — the May 2026 BTO launch in five bullets

HDB’s quarterly Build-to-Order exercise is expected to open in mid-May 2026, the second of four regular 2026 launches after February’s exercise.

The May window will sit inside the new Standard / Plus / Prime flat-classification framework, meaning subsidy-recovery clawbacks and 10-year MOP apply to any Plus or Prime flat selected.

Applicants should have CPF Housing Grant eligibility, HDB Financial Information (HFE) letter, and preferred-town shortlist ready before the launch opens — the application window is short (one week).

First-timer families with young children benefit most from the First-Timer (Parents and Married Couples) priority scheme introduced in the August 2024 exercise.

Balance-ballot strategy: in oversubscribed towns, a second-timer or non-priority applicant’s realistic chance of selection is often under 1 in 8 — pick towns where the queue-to-unit ratio is lower.

BTO Framework — Standard · Plus · Prime — LovelyHomes editorial infographic, 22 April 2026.

Why the May 2026 launch matters

The May 2026 BTO exercise lands at a pivotal moment for HDB policy. The Standard / Plus / Prime classification — rolled out from the October 2024 launch — has now been applied across five full launches, and the August 2024 refinement of the First-Timer priority scheme has reshaped how families are slotted into the ballot queue. Applicants who last studied the BTO rulebook before 2024 will find materially different mechanics.

The May slot also traditionally carries heavier volume than February: the Ministry of National Development’s 2026 guidance is approximately 19,600 BTO units across the year, and historically the May and November exercises each release roughly a quarter of annual supply. That means a realistic expectation is 4,500–5,500 units across non-mature and mature-town estates, with a meaningful portion earmarked under the Plus or Prime bands.

Standard, Plus, Prime — what the three bands actually mean

HDB reclassified BTO flats from “mature” / “non-mature” to a three-band framework in October 2024. The band is tied to the flat’s location attributes — proximity to the CBD, to MRT interchanges, to established amenities — rather than the age of the surrounding estate. Each band has its own pricing approach, subsidy profile, resale restrictions and income-ceiling rules.

BTO Classification Bands — May 2026 Framework

Source: HDB Standard/Plus/Prime guidelines · Effective from October 2024 BTO exercise

Band

Typical location

MOP

Resale conditions

Standard

Non-central towns with standard amenities

5 years

Standard resale rules; no subsidy clawback

Plus

Choicer locations, near amenities or transport

10 years

Subsidy clawback on resale; income ceiling on buyer

Prime

Most central or premium locations

10 years

Higher subsidy clawback; income ceiling; no renting out of whole flat

Key shift: under Plus and Prime, the subsidy recovery at resale is calculated as a percentage of resale price, not a fixed dollar figure — which protects HDB’s public investment when values appreciate meaningfully.

Which towns have featured in recent launches

Exact May 2026 town selection is announced by HDB approximately two weeks before the launch opens. Based on the pattern of recent launches, applicants can reasonably expect coverage spanning all three regions — typically two to three non-mature towns, two mature towns, and at least one site in a new or emerging estate such as Tengah or Bayshore.

In the February 2026 exercise, HDB launched units in Tampines, Woodlands, Queenstown, Toa Payoh, and Yishun, with a strong skew to Plus-classified units in the more central towns. The May launch is widely expected to include Punggol, Sengkang, Jurong West, Bukit Merah and Kallang/Whampoa — but this is projection, not confirmation.

Applicants who want the highest chance of selection should keep an open geographic mind: Bukit Batok, Choa Chu Kang, Bukit Panjang and Sembawang have historically carried queue-to-unit ratios below 2 for four-room Standard flats, versus ratios of 5–9 in choicer Plus or Prime locations.

The First-Timer priority reshuffle — who benefits most in May

From the August 2024 exercise onwards, HDB restructured the First-Timer priority scheme into three tiers:

First-Timer (Parents and Married Couples) — or FT (PMC) — married couples with at least one Singaporean child below 18, or engaged couples with a projected child, receive three ballot chances for any non-mature Standard, Plus or Prime flat.

First-Timer (Family) — or FT (F) — all other first-timer families without young children receive two ballot chances.

Non-First-Timers — one ballot chance for non-mature Standard flats only.

The practical impact: an FT (PMC) applicant’s effective probability of being invited to a selection appointment is approximately 1.5x that of an FT (F) applicant in the same queue — not a guarantee of selection, but a materially better ballot position. Couples expecting to apply in May 2026 and carrying a child below 18 should ensure their family nucleus is registered correctly on the HFE letter; a missed declaration loses the PMC priority.

The HFE letter — your pre-application gatekeeper

Since the May 2023 exercise, an HDB Financial Information (HFE) letter is required before submitting a BTO application. The HFE is an integrated eligibility assessment covering:

Flat and grant eligibility (CPF Housing Grants, EHG, Proximity Housing Grant)

HDB Housing Loan Eligibility Letter (where applicable)

Mortgage Servicing Ratio (MSR) and Total Debt Servicing Ratio (TDSR) assessment

Final affordability quantum based on income and CPF position

The HFE takes up to 21 working days to process. This means applicants who plan to bid in mid-May must apply for the HFE no later than the third week of April 2026 — right now is the realistic latest window. A late HFE is the single most common reason a motivated applicant misses the exercise window.

We have a full guide to the CPF Housing Grants stack for 2026 that explains how the EHG and Proximity Housing Grant combine with the HFE affordability figure — useful reading while waiting for the HFE result.

Income ceilings and grant quantum in 2026

The family-unit income ceiling for BTO flats remains S$14,000 per month (S$21,000 for extended families in 3Gen flats), unchanged since September 2019. For singles applying for a 2-room flexi flat in non-mature towns under the Single Singapore Citizen Scheme, the ceiling is S$7,000.

Grants available at the point of BTO application in May 2026 include:

Enhanced CPF Housing Grant (EHG) — up to S$80,000 for first-timer families, tiered by average household income.

EHG (Singles) — up to S$40,000 for first-timer singles buying a 2-room flexi.

Proximity Housing Grant (PHG) — applicable on resale only (not BTO), but worth noting that families planning a BTO now may still consider PHG-eligible resale as a backup.

At the top end, an FT (PMC) couple earning S$5,000 combined can receive up to S$80,000 EHG — which, combined with a 75% HDB concessionary loan and the 30-year repayment horizon, brings a four-room Plus flat at approximately S$550,000 valuation well within affordable-range for a dual-income Singaporean household.

Worked example — four-room Plus flat, May 2026

Worked scenario — FT (PMC) couple, combined S$8,500/month

Four-room Plus flat priced at S$620,000 (indicative)

EHG: S$45,000 (tiered on S$8,500 average)

Effective price after grant: S$575,000

Downpayment at 20% (HDB loan): S$115,000, of which up to 20% can be CPF Ordinary Account

HDB loan quantum: S$460,000 at 2.6% concessionary rate

Monthly instalment over 25 years: approximately S$2,090

This scenario assumes baseline HDB concessionary loan terms and does not include any bank-loan alternative; bank-loan applicants face a stricter TDSR ceiling of 55% and typically secure lower rates when the 3M SORA is running below 2.5%.

The seven-day window — what to do in each step

The application window is compressed. Planning each day in advance is what separates applicants who secure a booking from those who miss out:

T-14 days: HDB publishes town list, unit count by flat type, and indicative pricing. Shortlist two or three towns based on location and queue-to-unit ratio.

T-7 days: Application window opens. Submit within the first three days — no advantage to waiting.

T+7 days: Application closes. Ballot results are published approximately three weeks later.

Ballot notification: Selected applicants are invited for an HDB appointment within six weeks. Bring HFE letter, CPF statements, marriage certificate (or letter of intent for engaged couples), and photo ID.

Option fee: S$500 for 2-room flexi; S$1,000 for 3-room; S$2,000 for 4-room and above. Payable at flat selection.

Queue realities — setting a realistic expectation

Across the February 2026 exercise, application rates (applications per unit available) by broad category were approximately:

Four-room Prime — 8.2x oversubscribed

Four-room Plus — 5.6x oversubscribed

Four-room Standard (non-mature) — 1.9x oversubscribed

Three-room Standard (non-mature) — 1.4x oversubscribed

Five-room Standard — 3.1x oversubscribed

What this means: for a Plus or Prime four-room, even a PMC-priority applicant should expect multiple ballot attempts across launches before drawing a good queue number. For a Standard non-mature four-room, many first-time applicants secure a flat on their first or second attempt.

The resale alternative — when to switch tracks

For applicants facing short timelines — a planned wedding inside two years, a growing family, a parent needing close-proximity care — the BTO four-to-five-year wait from ballot to keys can be decisive. HDB resale offers an immediate-occupancy alternative, with the Proximity Housing Grant (PHG) of up to S$30,000 applicable for first-timer families buying near parents.

Resale volumes in Q1 2026 were stable, and median four-room resale prices across non-mature towns settled at approximately S$620,000 — roughly on par with a four-room Plus BTO selection price. That said, BTO remains the subsidised-entry path and is usually worth one or two rounds of attempt before switching.

Sale of Balance Flats — the May parallel track

Alongside the May BTO exercise, HDB will also conduct a Sale of Balance Flats (SBF) round covering unsold units from prior launches plus repurchased flats. SBF pricing is close to BTO pricing but waiting time is significantly shorter (often six to eighteen months to keys). Any applicant applying for BTO May 2026 should also apply for SBF simultaneously — there is no additional application cost and a separate ballot is run.

Market context — BTO versus the private market in 2026

Against the backdrop of Q1 2026’s private PPI flash estimate showing decelerating-but-firm growth, the BTO market is in a different rhythm. HDB Resale Price Index growth has slowed to sub-3% annualised through 2025, and the BTO subsidy profile ensures first-timer families still have a meaningfully cheaper path to homeownership than the private resale or new-launch private market.

The Plus and Prime classification is best thought of as HDB’s tool for capturing the value of public-land subsidy when the underlying land is in high-demand locations — the 10-year MOP and subsidy clawback are the price of access to the choicest catchments. For buyers with a longer-term horizon (10+ years to MOP and beyond), Plus and Prime remain attractive; for buyers who may need geographic flexibility within a decade, Standard flats offer cleaner resale mechanics.

FAQ — May 2026 BTO

Q1. When exactly will HDB open the May 2026 BTO launch? HDB has not announced the exact date at time of writing (22 April 2026). Based on the Feb / May / Aug / Nov cadence, the application window is expected mid-May. Monitor HDB press releases at hdb.gov.sg for the confirmed date.

Q2. Do I need an HFE letter before applying? Yes. The HFE is mandatory for all BTO applicants since the May 2023 exercise. It takes up to 21 working days — apply now if you plan to submit for May.

Q3. Can I apply for BTO and SBF at the same time? Yes, HDB typically runs the two exercises in parallel. Applying for both increases your chance of securing a flat within the same quarter.

Q4. What happens if I miss the application window? You wait for the August 2026 exercise. There is no mid-cycle application option outside the four annual launches.

Q5. My partner and I earn S$15,000 combined — can we still apply? No, the family income ceiling for a standard BTO flat is S$14,000. You may consider the Executive Condominium track (ceiling S$16,000) or resale-private routes.

Q6. What is the key difference between a Plus and a Prime flat? Both carry 10-year MOP and subsidy clawback on resale, and both impose an income ceiling on future resale buyers. Prime flats additionally prohibit renting out the whole flat; Plus flats allow whole-flat rental after MOP. Prime flats are also in the most central catchments.

Q7. Can a single Singaporean apply for a 4-room BTO? No. Singles under the Single Singapore Citizen Scheme are restricted to 2-room flexi flats in non-mature towns. For other room types, singles must apply jointly with an eligible occupier (e.g., parent or sibling) under a joint scheme.

Q8. If my ballot number is not called, do I keep a priority position for the next exercise? No — each exercise is an independent ballot. However, accumulating non-selection histories does boost the applicant’s queue position in certain priority schemes (e.g., the Married Child Priority Scheme retains its weighting across exercises).

Q9. Is there any advantage to submitting on day one versus day seven? No. The ballot is computer-randomised; submission time within the window has no effect on queue position.

Q10. When do I start paying for the flat? The option fee is paid at flat selection. Downpayment is payable in stages aligned to construction milestones (typically 15% at signing of Agreement for Lease, 5% at key collection for HDB loan). Monthly instalments begin only after key collection.

The May 2026 BTO exercise is an exercise in preparation: HFE letter in hand, town shortlist validated against queue-to-unit ratios, First-Timer priority correctly filed. Families applying as FT (PMC) for a Standard non-mature flat have realistic one-to-two-attempt odds; those targeting Plus or Prime in a choicer catchment should plan for several exercises of patience. The framework has changed since 2024 — re-read the rules even if you applied under the old mature/non-mature system.