Singapore Property Investment Guide 2026: How to Buy, Rent and Build Wealth Through Property

Quick Answer: Singapore Property Investment 2026 — Key Takeaways

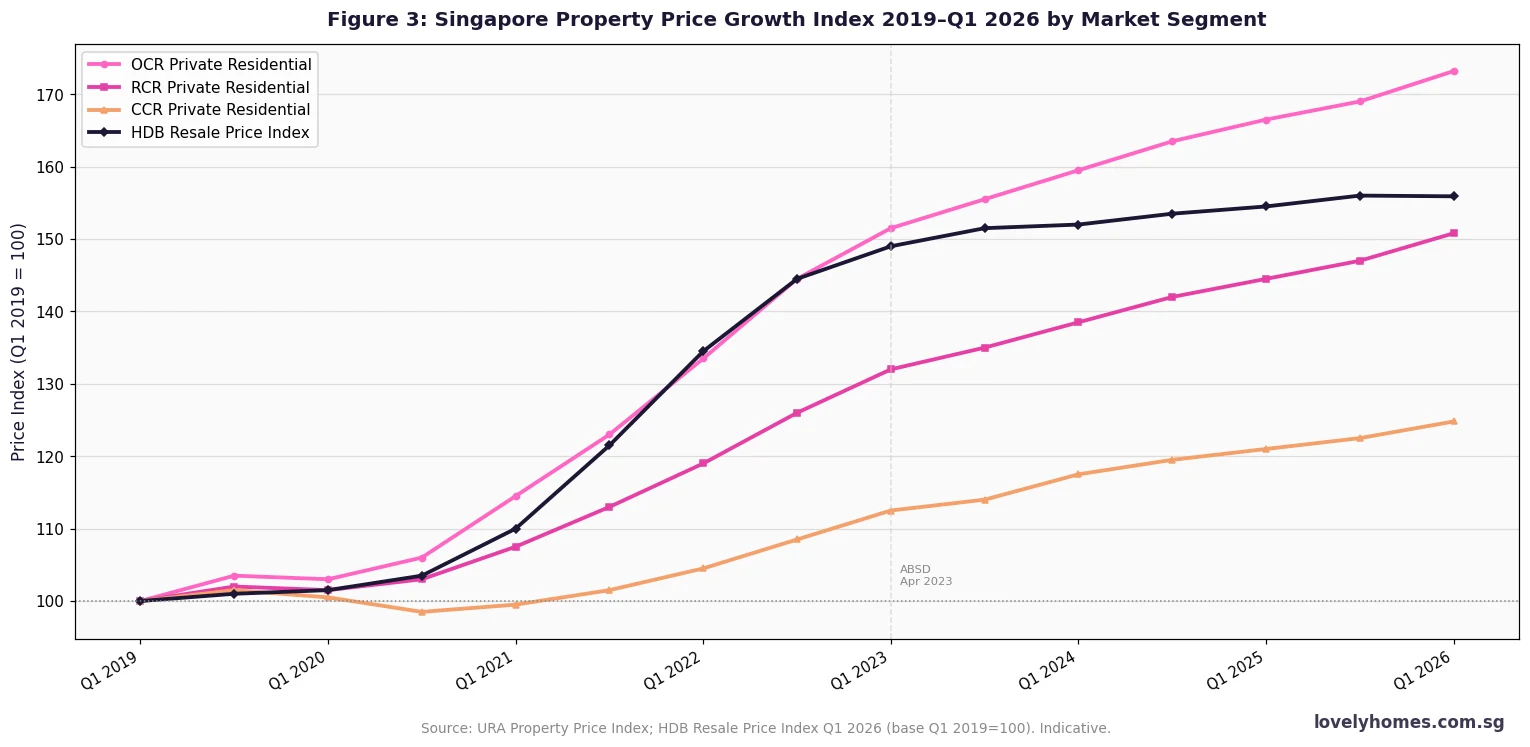

- Price growth: OCR private residential prices rose +2.2% in Q1 2026; RCR +1.6%; CCR -0.3%; HDB resale -0.1% — a stabilising market post-2023 cooling measures.

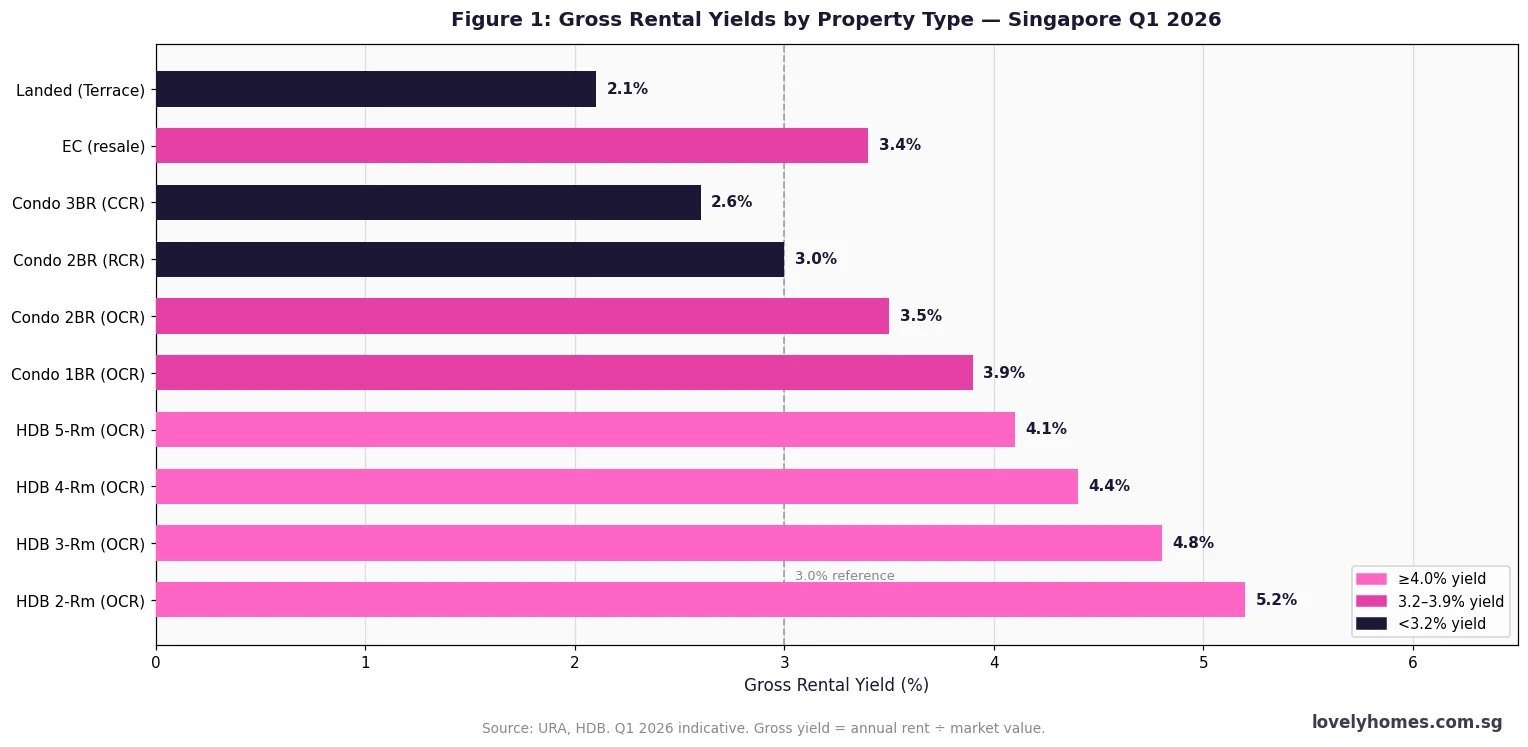

- Rental yields: HDB flats generate the highest gross yields at 4.1–5.2%; OCR condos 3.5–3.9%; CCR condos 2.5–2.8%.

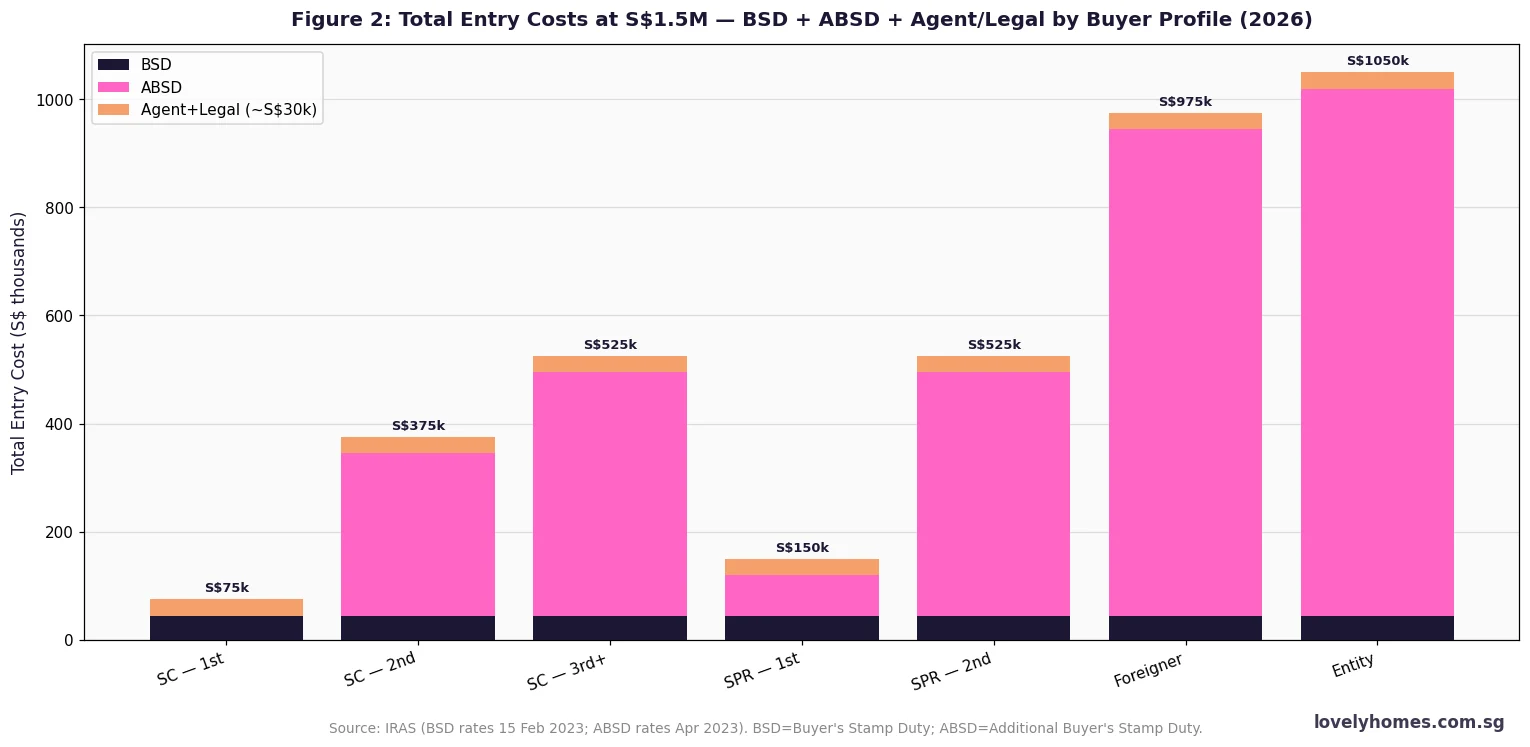

- ABSD is the single biggest cost variable: Singapore Citizens pay 0% on their first property and 20% on the second; foreigners pay 60%. ABSD must factor into every ROI calculation.

- BSD starts at 1% and rises progressively to 6% above S$3M. A S$1.5M condo incurs S$44,600 in BSD alone.

- Financing: TDSR is capped at 55% of gross income; MSR at 30% for HDB and EC purchases. CPF OA can fund downpayment and mortgage instalments but accrues 2.5% interest payable on sale.

- Capital appreciation: OCR private prices are up ~73% since Q1 2019; HDB resale up ~56%; CCR up ~25%.

- Pipeline risk: total private residential pipeline stands at ~61,000 units as at Q1 2026 — elevated supply is a medium-term moderating factor.

- Best entry strategies for most Singapore households: HDB resale (high yield, government grants available) → EC (medium yield, capital gains on privatisation) → OCR condo (growth play, TDSR-permitting).

What is Property Investment in Singapore?

Property investment in Singapore means acquiring residential or commercial real estate with the objective of generating rental income, capital appreciation, or both. Singapore’s property market is one of the most regulated in Asia — by design. The Urban Redevelopment Authority (URA) controls land supply through the Government Land Sales (GLS) programme; the Housing & Development Board (HDB) administers public housing policy; the Monetary Authority of Singapore (MAS) governs financing limits; and the Inland Revenue Authority of Singapore (IRAS) collects stamp duties.

This web of regulation is not accidental. Singapore uses property policy as a macro-prudential tool — adjusting ABSD rates, LTV caps, and supply releases to prevent asset-price bubbles and ensure housing remains accessible. For investors, understanding why each rule exists is as important as knowing the rates themselves, because policy changes (like the April 2023 ABSD hike to 60% for foreigners) can transform return profiles overnight.

This guide covers every dimension a Singapore property investor needs to understand in 2026: property types, buyer profiles, costs, financing, yields, price trends, and entry strategies — all benchmarked against current government data.

Understanding Singapore’s Property Market Structure

Singapore divides its residential market into three broad categories. The HDB market covers public housing flats, which house roughly 80% of Singapore’s resident population. HDB flats are sold by the government at subsidised prices via the Build-To-Order (BTO) scheme or on the open resale market. Singapore Citizens and Permanent Residents may own HDB flats under eligibility rules; foreigners may not. The executive condominium (EC) market is a hybrid tier — EC units are built by private developers on government land, initially subject to HDB eligibility rules, and progressively privatised after 5 years (partial privatisation) and 10 years (full privatisation), at which point foreigners may purchase them. The private property market includes condominiums, apartments, and landed houses, open to all buyer profiles subject to ABSD.

Geographically, URA divides Singapore into three market segments: the Core Central Region (CCR) — the prime districts 9, 10, 11 and Marina Bay — characterised by high absolute prices and lower yields but strong expat demand; the Rest of Central Region (RCR) — inner-ring districts like Queenstown, Toa Payoh, Bishan — offering a balance of capital upside and rental demand; and the Outside Central Region (OCR) — suburban estates like Tampines, Punggol, Jurong East, Woodlands — which offer the highest rental yields and the strongest capital growth over the past five years driven by HDB upgrader demand.

Singapore Property Prices in 2026 — What the Data Says

URA’s Q1 2026 private residential price index recorded an overall increase of +0.9% quarter-on-quarter — a steady but measured pace following the April 2023 ABSD hike that cooled the market materially. By segment, OCR led at +2.2%, reflecting robust HDB upgrader demand for suburban condos; RCR rose +1.6%; while CCR dipped -0.3% as the 60% foreign buyer ABSD continued to suppress transaction volumes in the prime market. The landed residential segment eased -0.4%. HDB resale prices slipped -0.1% — the first quarterly dip after an unbroken run of increases since 2021 — which analysts attribute to increased BTO supply and the dampening effect of PLH and Plus-category resale restrictions.

On a five-year basis, the performance picture differs significantly by segment. OCR private prices are up approximately 73% since Q1 2019 (base year), driven by the work-from-home boom, pent-up upgrader demand, and the record-low supply of new OCR launches between 2020 and 2022. RCR has risen roughly 51%; CCR approximately 25%; and the HDB Resale Price Index approximately 56% over the same period — a remarkable run for public housing given its subsidised entry cost.

Buyer Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD)

Stamp duties are the single largest transaction cost in Singapore property and cannot be ignored in any investment analysis. Buyer’s Stamp Duty (BSD) applies to all property purchases regardless of buyer profile. It is progressive: 1% on the first S$180,000, 2% on the next S$180,000, 3% on the next S$640,000, 4% on the next S$500,000, 5% on the next S$1.5M, and 6% above S$3M (rates effective 15 February 2023). On a S$1.5M property, BSD amounts to S$44,600.

Additional Buyer’s Stamp Duty (ABSD) is the more consequential levy. Rates (effective April 2023) vary by buyer profile and property count: Singapore Citizens pay nil on their first property, 20% on their second, and 30% on their third or subsequent. Singapore Permanent Residents pay 5% on their first, 30% on the second. Foreigners pay a flat 60%; entities (companies) pay 65%. Certain FTA nationals (US, Swiss, and Icelandic/Liechtenstein/Norwegian nationals purchasing residential property) are treated the same as Singapore Citizens for ABSD on their first property under trade agreement provisions.

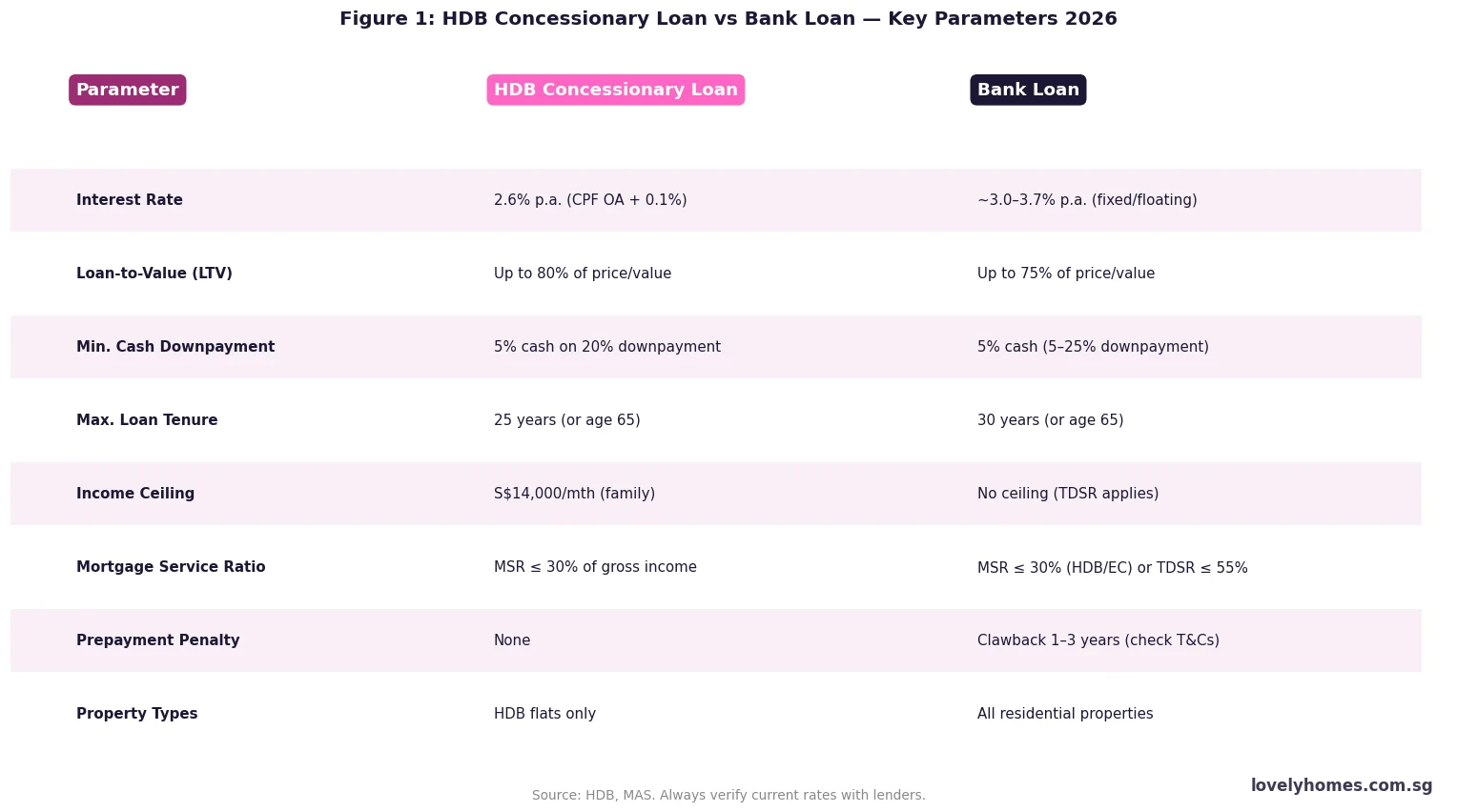

Financing: TDSR, MSR, LTV and CPF Rules

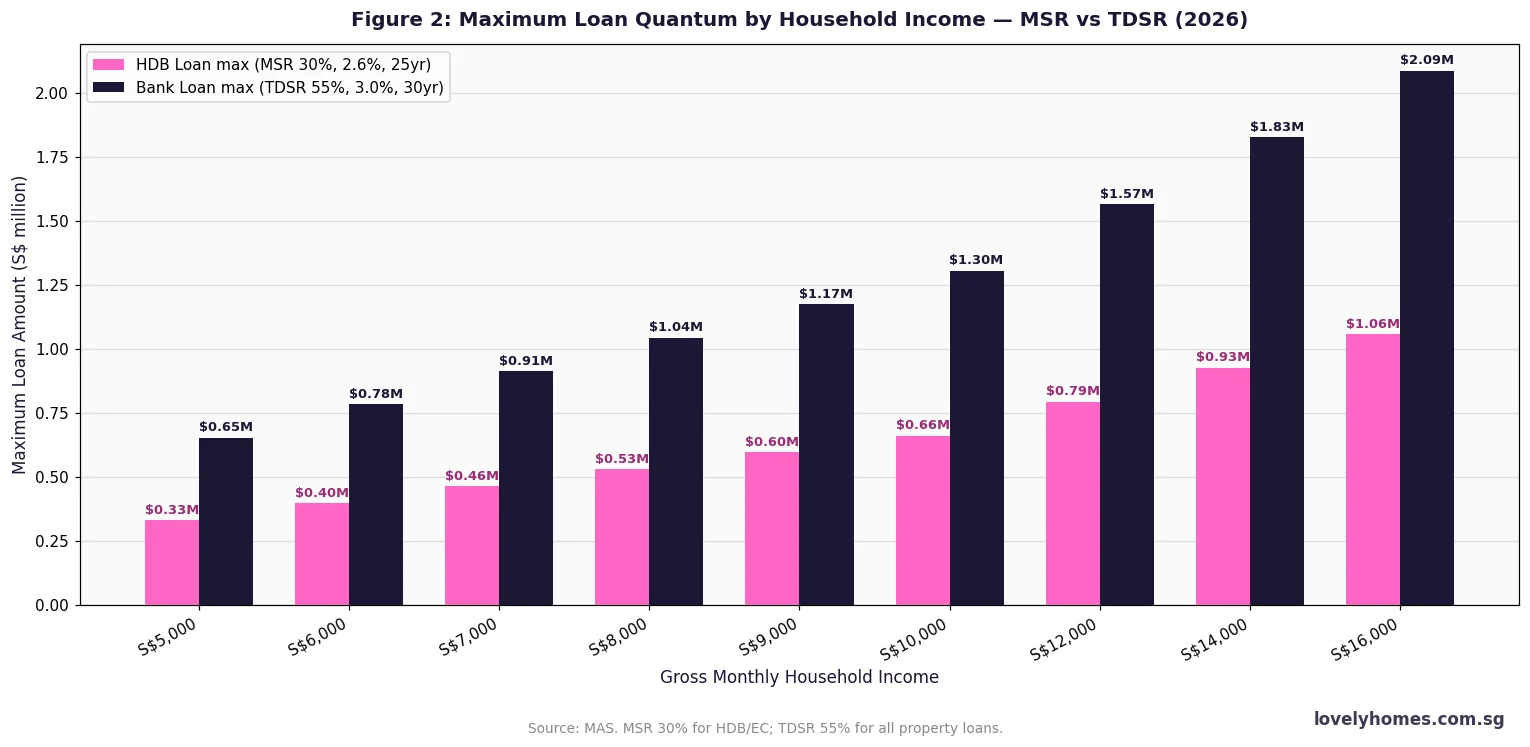

MAS introduced the Total Debt Servicing Ratio (TDSR) framework in June 2013 to prevent household over-leverage. Under TDSR, a borrower’s total monthly debt obligations — including the new property loan, car loans, personal loans, and credit card revolving debt — may not exceed 55% of gross monthly income. For married couples buying jointly, the household income can be combined but the same 55% cap applies to combined obligations. The Mortgage Servicing Ratio (MSR), which is more restrictive, limits monthly repayments on HDB flat loans and EC loans to 30% of gross monthly income.

Loan-to-Value (LTV) limits determine maximum loan quantum. For a first property with no outstanding housing loans, HDB concessionary loans allow up to 80% LTV (on purchase price or valuation, whichever is lower) with a minimum 5% cash downpayment. Bank loans for a first property are capped at 75% LTV, also with at least 5% in cash. For a second property, the LTV cap drops to 45% (with at least 25% cash for the downpayment). Third or subsequent properties: 35% LTV.

CPF Ordinary Account (OA) savings, earning a guaranteed 2.5% p.a., can be used for the property downpayment, monthly mortgage instalments, and stamp duties. However, the Valuation Limit (VL) caps total CPF use at the property’s lower of purchase price or market value, while the Withdrawal Limit (WL) — set at 120% of VL — represents the absolute ceiling if the property has at least 60 years of remaining lease. Any CPF drawn must be refunded with 2.5% accrued interest on eventual sale, which can meaningfully reduce net cash proceeds.

Summary: Key Investment Parameters at a Glance

| Parameter | HDB Flat | Executive Condo (EC) | OCR Condo | CCR Condo |

|---|---|---|---|---|

| Typical price range | S$300k–S$900k | S$850k–S$1.4M | S$900k–S$2.5M | S$1.8M–S$6M+ |

| Gross rental yield | 4.1–5.2% | 3.2–3.6% | 3.4–3.9% | 2.3–2.8% |

| 5-year price growth | +8–12% (resale) | +12–18% (resale) | +15–25% | +8–14% |

| Foreign buyer eligible? | No | Only after 10 yrs | Yes (60% ABSD) | Yes (60% ABSD) |

| Max LTV (first property) | 80% (HDB loan) | 75% (bank loan) | 75% (bank loan) | 75% (bank loan) |

| Minimum occupation period | 5 yrs (PLH/Plus: 10 yrs) | 5 yrs before sale | No MOP | No MOP |

| Income ceiling | S$14,000/mth | S$16,000/mth | None (TDSR applies) | None (TDSR applies) |

| Capital gains tax | Nil | Nil | Nil (SSD may apply) | Nil (SSD may apply) |

Worked Example: SC Household Upgrading from HDB to OCR Condo

Case Study — Mr & Mrs Ong, Singapore Citizens upgrading to a first private property

Household profile: Mr & Mrs Ong, both Singapore Citizens, joint gross income S$14,000/month. They own a 5-room HDB flat in Jurong East which has completed its 5-year MOP, currently valued at S$780,000 (outstanding HDB loan S$220,000; CPF used S$320,000 + S$43,000 accrued interest = S$363,000 total CPF refund on sale). Target: buy an OCR 2BR condo at S$1,350,000.

Step 1 — Sell HDB first: Sale proceeds S$780,000 − HDB loan redemption S$220,000 − CPF refund S$363,000 − agent commission 2% S$15,600 − legal S$2,500 = net cash ~S$178,900. After selling, their ABSD on the new private purchase is nil (first private property, SC). If they buy before selling and hold both simultaneously, the condo purchase would attract 20% ABSD = S$270,000 — avoidable by selling first (or using the SC married couple remission: buy first, sell HDB within 6 months).

Step 2 — Buy OCR condo S$1,350,000: BSD = S$37,400. Minimum cash downpayment = 5% × S$1,350,000 = S$67,500. Balance downpayment 20% total = S$270,000 (S$67,500 cash + S$202,500 CPF). Bank loan: 75% LTV = S$1,012,500 @ 3.0% p.a. 30 years → monthly instalment S$4,268. TDSR check: S$4,268 ÷ S$14,000 = 30.5% — well within 55% PASS. Total upfront cost: S$67,500 (5% cash down) + S$37,400 (BSD) + S$2,800 (legal) = S$107,700 cash. CPF deployed: S$202,500 (balance of 20% down). Net cash from HDB sale S$178,900 covers the full S$107,700 requirement with S$71,200 remaining.

Capital Appreciation: Singapore Property vs Other Asset Classes

Singapore residential property has compounded at an effective annualised rate of roughly 8–10% in OCR markets over the 2019–2026 period — broadly comparable to the Straits Times Index total return of around 6–8% annually, and notably lower than the Nasdaq’s run but with far lower volatility. The critical advantage of property is leverage: a S$270,000 equity stake (20% downpayment on a S$1.35M property) growing at 8% per annum generates capital on the full S$1.35M base, dramatically amplifying the equity return relative to unleveraged assets.

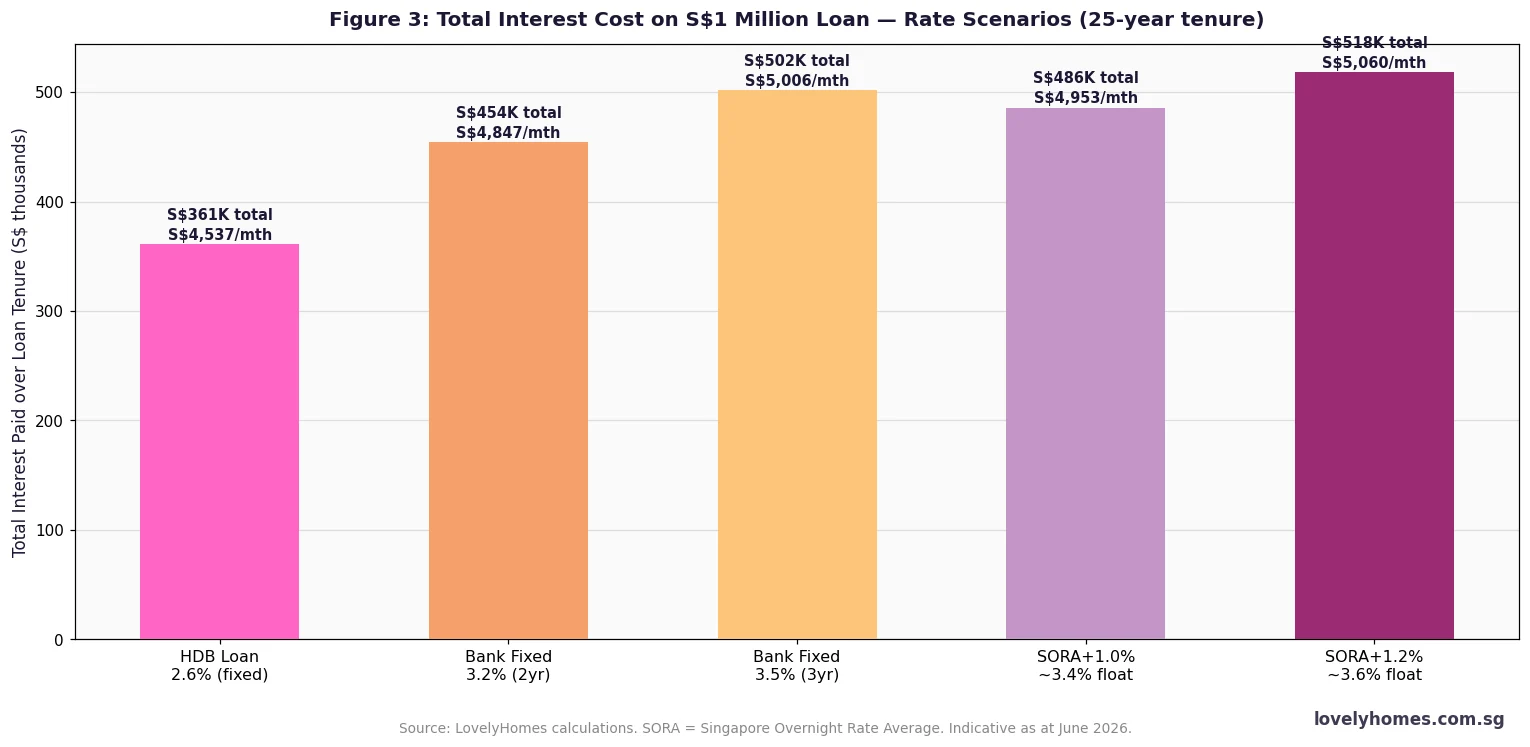

However, leverage cuts both ways. A 15–20% property price correction — comparable to the 2013–2017 period when prices fell roughly 12% following TDSR and cooling measures — would erode a 20% equity buffer significantly. Investors should stress-test their holdings against an interest rate spike (3M SORA remains at approximately 2.4% as at June 2026 but has ranged from 0.05% to 4.0% in the past five years) and against a 12–18 month vacancy period.

Why Singapore Property Remains a Core Investment Asset

Three structural factors continue to underpin Singapore’s residential market. First, land scarcity: Singapore covers 733 km² and cannot expand its land mass materially beyond ongoing reclamation. The total stock of private residential units stands at roughly 365,000, with a pipeline of ~61,000 units as at Q1 2026. Government control of the GLS programme means supply is managed, not market-driven. Second, strong legal framework: Singapore’s property rights are among the most secure globally — clear title, transparent transactions, an independent judiciary, and efficient land registration through the Singapore Land Authority (SLA). Third, no capital gains tax: Singapore does not levy capital gains tax on property. The Seller’s Stamp Duty (SSD), which applies at 12%, 8%, or 4% for properties sold within 1, 2, or 3 years of purchase respectively, effectively discourages speculative flipping but leaves medium-to-long-term investors entirely unaffected.

Compared to peers in the region, Singapore’s regulatory environment is more transparent than Hong Kong or mainland China, and its legal protections are stronger than most ASEAN markets. For high-net-worth individuals and regional corporates, Singapore residential property serves as both a wealth store and a hedge against currency risk in Southeast Asia’s most stable monetary environment.

What Might Come Next: Outlook for H2 2026 and Beyond

Speculation follows, not government guidance. The 2H2026 Government Land Sales programme announced by URA in June 2026 includes nine Confirmed List sites capable of yielding approximately 4,745 residential units and 735 EC units, alongside the landmark Jurong Lake District white site. The sustained supply pipeline is expected to moderate price growth in the OCR to a 1–2% quarterly range through 2026. The Jurong Region Line opening in phases from approximately 2028 will likely catalyse a re-rating of Jurong, Tengah, and Choa Chu Kang OCR pricing, potentially delivering a 8–15% uplift to proximate properties based on historical MRT-opening precedents.

Interest rate trajectory remains the key macro variable. If 3M SORA retreats to the 1.5–2.0% range by late 2026 as some market observers anticipate, monthly servicing costs for SORA-pegged bank loans could fall materially, broadening the pool of TDSR-eligible buyers and supporting price momentum. Conversely, any renewed MAS tightening — whether via further ABSD increases or LTV reductions — could quickly dampen transaction volumes, as the April 2023 measures demonstrated.

Frequently Asked Questions: Singapore Property Investment 2026

Do Singapore Citizens pay any tax on capital gains from property?

No. Singapore does not levy a capital gains tax on residential property sales. However, the Seller’s Stamp Duty (SSD) applies if you sell within three years of purchase: 12% for sale within the first year, 8% within the second year, and 4% within the third year, calculated on the higher of the sale price or market value. Properties held for more than three years attract zero SSD. This means medium-to-long-term investors retain the full capital gain on sale, making Singapore’s tax environment highly favourable for property investment by global standards.

How does ABSD affect investment property returns?

ABSD fundamentally reshapes the return maths for all but first-time SC buyers. A Singapore Citizen purchasing a second property worth S$1.5M pays 20% ABSD = S$300,000 upfront. To break even on this cost alone — before financing and other expenses — the property must appreciate at least S$300,000 beyond the purchase price (roughly a 20% gross gain) before any net profit is realised. For SPR second-property buyers (30% ABSD) and foreigners (60% ABSD), the bar is even higher. This is precisely why many experienced property investors in Singapore prioritise holding their first property long-term and are extremely cautious about second purchases — the ABSD converts a 10% market gain into a near-breakeven outcome.

Can I use CPF to pay for investment property?

Yes, CPF Ordinary Account (OA) funds can be used for the downpayment and monthly mortgage instalments on a second or investment property. However, CPF usage for a second property is subject to the Valuation Limit (VL) and Withdrawal Limit (WL = 120% of VL), and critically — all CPF drawn must be refunded with 2.5% per annum accrued interest when the property is sold. This means long-holding-period investors will accumulate a substantial refund obligation that directly reduces net sale proceeds. If you have deployed S$400,000 in CPF over 15 years, your refund obligation at 2.5% compound could exceed S$590,000 — a significant deduction from the sale price.

What is the difference between OCR, RCR and CCR for investment purposes?

The three planning regions serve very different investor profiles. The CCR (Core Central Region — Districts 9, 10, 11, Downtown Core, Sentosa) offers prestige, expat rental demand, and freehold tenure, but yields are the lowest at 2.3–2.8% and price growth since 2019 has lagged at ~25%. The RCR (Rest of Central Region — inner suburbs like Queenstown, Toa Payoh, Bishan) offers a middle ground: yields of 3.0–3.5% and solid capital appreciation of ~51% since 2019. The OCR (Outside Central Region — Tampines, Jurong, Woodlands, Punggol) delivers the highest gross yields (3.4–3.9% for condos) and the strongest capital growth (~73% since 2019) driven by HDB upgrader demand. Most Singapore residents with a single investment property budget should look at OCR first.

Is it better to buy an HDB resale flat or a private condo as an investment?

For most Singapore Citizens and PRs within HDB eligibility criteria, HDB resale flats offer compelling investment characteristics: the highest gross rental yields in the market (4.1–5.2%), government grants for eligible buyers, an established tenant pool, and lower absolute entry costs that improve leverage efficiency. The key constraint is the 5-year Minimum Occupation Period (MOP) — 10 years for Plus and Prime flats — during which the flat cannot be rented out entirely and cannot be sold. Private condos offer no MOP, greater flexibility, and exposure to the private price index, but entry costs are significantly higher and yields are lower. For buyers who need immediate rental income and cannot lock up capital for five years, a private condo is the better choice. For patient investors willing to occupy first, HDB offers the most efficient risk-adjusted return in the Singapore market.

What is the Seller’s Stamp Duty (SSD) and when does it apply?

The Seller’s Stamp Duty (SSD) was introduced in February 2010 and last revised in January 2011 to its current three-tier structure. SSD applies to residential properties (and industrial properties, which have a separate regime) sold within three years of purchase. The rates are: 12% if sold within the 1st year of purchase, 8% within the 2nd year, and 4% within the 3rd year. SSD is computed on the higher of the sale price or market value at the date of sale. Inherited properties: SSD runs from the original purchase date of the deceased, not the date of inheritance. For most buy-and-hold investors, SSD is a non-issue, but it effectively eliminates profitable short-term flipping strategies for properties purchased at market rates.

Should I invest in residential property or Singapore REITs?

REITs (Real Estate Investment Trusts) listed on the Singapore Exchange (SGX) offer exposure to commercial, industrial, retail, and hospitality property without the ABSD, TDSR, MOP, and management burden of direct ownership. Singapore REIT distribution yields typically range from 5–7%, compared to 3–4% gross yields for direct residential investment. However, REITs are equity instruments subject to market sentiment volatility and do not carry the leverage benefit of direct property. For investors who cannot qualify for a second property loan under TDSR, or who have already exhausted CPF, REITs offer a capital-light alternative. Most sophisticated investors hold both: direct residential for leverage and capital gains, REITs for yield and liquidity.