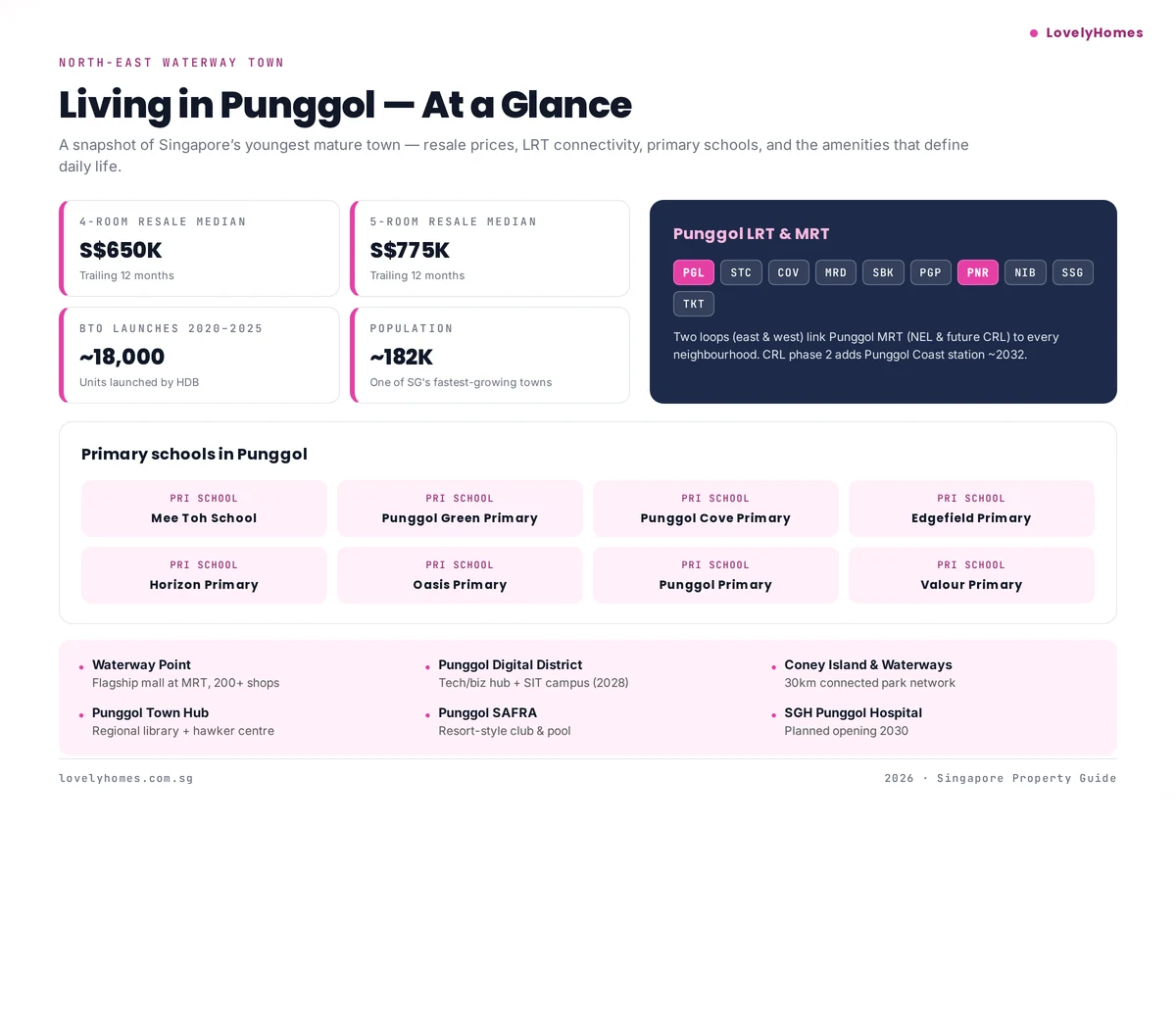

Punggol is a north-east waterway town of ~182,000 residents anchored by Punggol MRT (NEL), two LRT loops, and Waterway Point. A 4-room resale flat there now transacts at a S$650,000 median (trailing 12 months), and the upcoming Cross Island Line phase 2, SGH Punggol Hospital (~2030), and Punggol Digital District continue to lift its attractiveness.

Punggol was launched as Singapore’s first waterfront town in the early 2000s and has grown into one of the country’s busiest BTO neighbourhoods. With the Digital District turning on in 2028 and the new Cross Island Line station coming in the early 2030s, it has moved from “young estate” to fully mature in under two decades.

This guide walks you through Punggol’s transport, schools, amenities, and property numbers, and helps you decide whether it’s the right estate for your family. If you’re weighing it against other family estates, see our best HDB estates for young families ranking.

Punggol at a glance: resale prices, LRT stations, primary schools, and key amenities

Where is Punggol?

Punggol sits at Singapore’s north-eastern tip, bordered by the Tampines Expressway and the Strait of Johor. It is accessed via the North East Line (Punggol MRT) and, in future, the Cross Island Line’s Punggol Coast station. The Tampines Expressway, KPE, and SLE put the Central Business District within a 25-minute drive off-peak.

Transport — two LRT loops plus MRT

Punggol has Singapore’s densest LRT network. Two loops — East (via Cove, Meridian, Coral Edge, Riviera, Kadaloor, Oasis, Damai) and West (via Sam Kee, Teck Lee, Punggol Point, Samudera, Nibong, Sumang, Soo Teck) — fan out from Punggol MRT interchange.

North East Line: Punggol to Dhoby Ghaut in 26 minutes, HarbourFront 32 minutes.

Cross Island Line (Phase 2, from ~2032): Punggol Coast station linking to Jurong in ~30 minutes.

Expressways: TPE, KPE, SLE — 25 minutes to CBD, 22 minutes to Changi Airport.

Schools — 8 primaries, multiple secondaries

Punggol has 8 primary schools within the estate: Mee Toh, Punggol Green, Punggol Cove, Edgefield, Horizon, Oasis, Punggol Primary, and Valour. Secondaries include Edgefield, Compassvale, Greendale, and Punggol Secondary. Singapore Institute of Technology’s new campus at Punggol Digital District adds tertiary access from 2028.

Amenities — Waterway Point and beyond

Waterway Point — 200+ shops, supermarkets, cinemas, F&B over 3 levels, right at Punggol MRT.

Punggol Digital District — Singapore’s first enterprise district, ~28 ha, ~28,000 jobs by 2030.

Punggol Coney Island — 50 ha nature park at the north-east coast.

Punggol Waterway Park — 4.2 km of waterway-side greenery connecting the whole town.

Punggol Town Hub — regional library, community club, food centre, sports complex.

SGH Punggol Hospital — planned opening around 2030.

Property pricing — what Punggol costs in 2026

Flat type

Resale median (12M)

BTO median (after grants)

3-room

~S$465K

~S$315K

4-room

S$650K

~S$470K

5-room

S$775K

~S$565K

Executive

S$880K

n/a (not typically launched)

Who Punggol suits

Punggol fits young families, dual-income couples, and first-time buyers who value newer-build flats with amenities in easy reach. If you’re working in the north-east (Seletar Aerospace, Changi Business Park, future PDD) or can work hybrid from home, commute is manageable. Retirees also find the waterway-park lifestyle attractive.

Trade-offs: CBD commute is longer than mature central estates; some LRT services are stretched at peak; supermarket density in the outer pockets is still light. Also, because Punggol is newer, resale queue is deeper and grants like EHG plus PHG make a big price difference.

Frequently asked questions

Is Punggol a good area to buy for investment?

It depends on whether you’re buying private or public housing. For HDB resale, Punggol has strong rental demand driven by SIT students, PDD employees, and young families. For private condos near Punggol MRT, rental yields are moderate (3.0–3.5%) but capital appreciation from the CRL and PDD is expected to be meaningful.

How crowded is Punggol MRT?

Punggol MRT is the NEL terminus, so you get a seat boarding there in the morning. Returning home, peak crowding is heavy 6:30–8:00pm. Once CRL phase 2 opens, commuting patterns will rebalance significantly.

Are there good secondary schools in Punggol?

Edgefield Secondary, Compassvale Secondary, Greendale Secondary, and Punggol Secondary serve the estate. For Integrated Programme routes, students usually look toward Cedar Girls’, ACS(I), or RI outside the estate.

Is there a downside to Punggol?

Estate is still young, so some commercial and medical nodes are still being built out. Longer commute to town than central estates, and the LRT loops can be slow — allow an extra 10 minutes if you need to transit.

Disclaimer

This guide is for general information only. Estate pricing, upcoming launches, MRT opening dates, and masterplan details change over time. Always verify the latest HDB, URA, LTA and MND announcements before making property decisions. LovelyHomes is not a licensed property agent. For personalised advice, please engage a registered CEA agent.

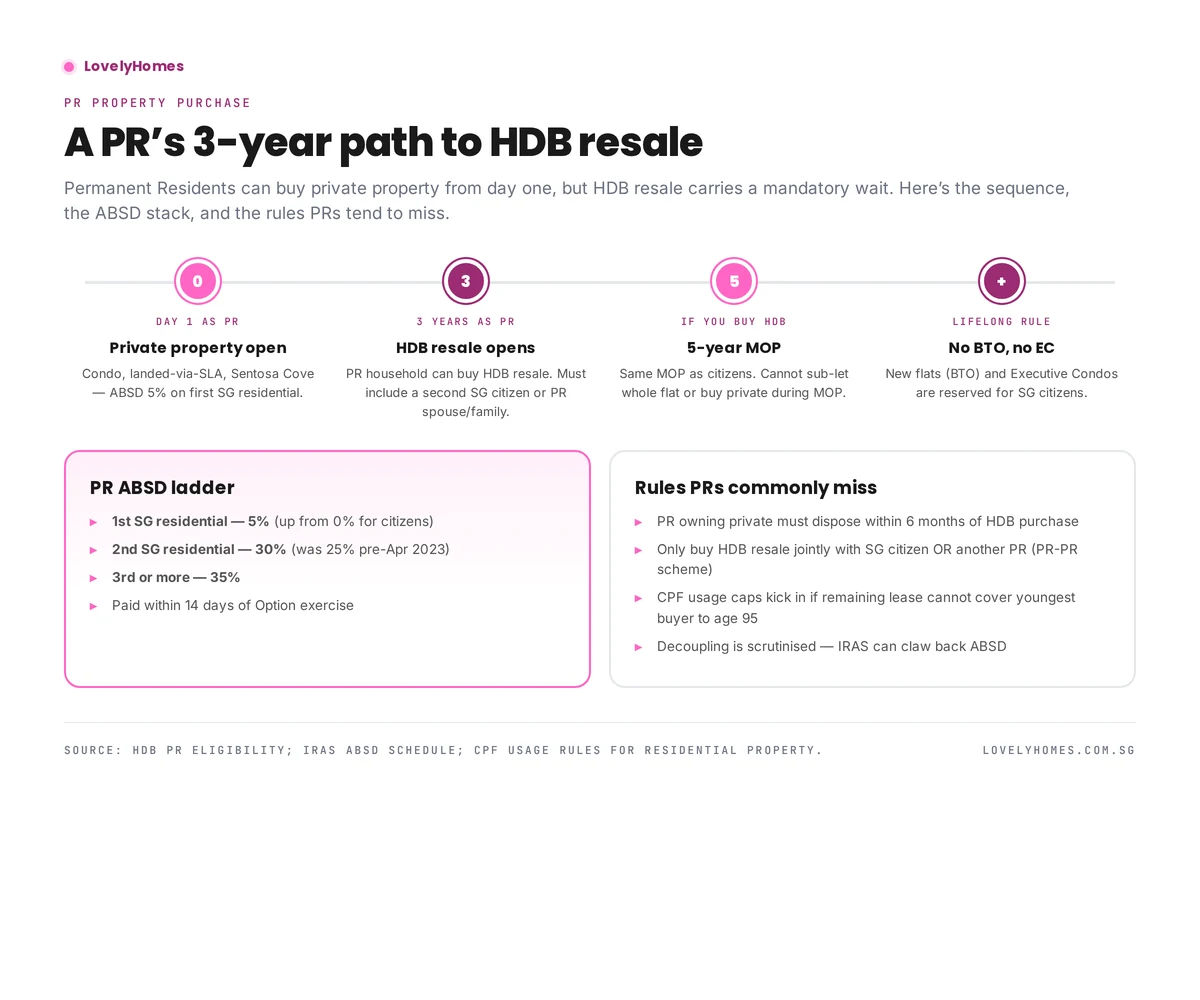

A Singapore Permanent Resident can buy private condos from day one of PR status, paying 5% ABSD on the first residential purchase (30% on second, 35% on third+). HDB resale flats open to PRs only after 3 years of PR status, and require a qualifying family nucleus. PRs cannot buy new BTO, Plus, Prime or EC flats. Landed property on the mainland needs LDAU approval. If you buy an HDB flat as a PR, MOP and subletting rules mirror citizens.

Permanent Residency fundamentally changes a buyer’s property menu in Singapore — but not overnight. From day one, private property opens. HDB resale still waits three years. New HDB (BTO/Plus/Prime) and new ECs remain closed to PRs regardless of wait time.

This guide maps the PR property timeline, the full 2026 ABSD ladder for PR buyers, the most common mistakes PRs make when disposing of existing property, and the rules PRs should know before taking out a CPF loan. For the foreigner-side equivalent, see our foreigner property guide.

A PR’s 3-year path to HDB resale.

The PR property timeline

Day 1 as PR

Private condo, landed-via-LDAU, and Sentosa Cove landed open immediately. CPF usage opens once the PR has active OA/SA balances. LTV, TDSR and MSR frameworks are identical to citizens.

3 years as PR

HDB resale opens. A PR household must form a qualifying family nucleus — typically a PR applicant with a spouse (PR or SG citizen), or the PR-PR Scheme (both applicants PRs for at least 3 years).

5 years after HDB purchase (if you buy HDB)

Minimum Occupation Period. Same 5-year MOP as citizens. Cannot sub-let the entire flat, cannot buy private residential, cannot sell on the open market. See our MOP rules guide.

Lifetime rule

PRs cannot buy new BTO, new Plus, new Prime or new EC flats. These are reserved for SG citizens with a citizen spouse or fiancé(e). The only HDB route for PRs remains the resale market.

ABSD for PRs — the 2026 ladder

Residential count

ABSD (PR)

Notes

1st SG residential

5%

Up from 0% that citizens pay

2nd SG residential

30%

Raised from 25% in Apr 2023

3rd or more

35%

Raised from 30% in Apr 2023

ABSD is payable within 14 days of Option exercise, on top of BSD. If two PRs buy jointly, the ABSD is calculated on the highest-count profile among the buyers.

The HDB-specific rules PRs must follow

Dispose of private within 6 months

A PR who owns private residential (in Singapore or overseas) must dispose of it within 6 months of the HDB resale completion. This is usually the biggest surprise for incoming PR buyers — overseas apartments count.

CPF usage and the lease rule

CPF can fund the purchase only if remaining lease covers the youngest buyer to age 95. For older HDB stock this is a real constraint — see our CPF for property guide.

No grants (mostly)

Most HDB grants (EHG, Family Grant, Proximity Housing Grant) are reserved for SG-citizen first-timer households. A PR-PR couple does not qualify for EHG. However, a PR with an SG-citizen spouse may qualify under the standard first-timer framework — see our grants guide.

Landed and Sentosa Cove

PRs need LDAU approval under the Residential Property Act to buy landed on the mainland — rarely granted except for long-tenured PRs with strong local ties. Sentosa Cove landed is much more accessible: SLA approval is routinely granted for owner-occupation.

Common PR mistakes

Forgetting the 3-year HDB wait. Newly-minted PRs cannot buy HDB until year 3.

Holding overseas property while buying HDB. HDB will compel disposal within 6 months.

Attempting decoupling to reset ABSD. IRAS actively scrutinises PR decoupling post-2022 and may claw back ABSD. See our decoupling guide.

Using CPF on a lease-short flat. Always check the lease-to-95 calculator first.

Frequently asked questions

Can a PR buy an EC?

Not a brand new EC — that’s citizen-only. A PR can buy a privatised EC (post-10-year MOP + privatisation), because by then it is effectively private property.

Can two PRs buy HDB resale together?

Yes — under the PR-PR Scheme, both must have been PR for at least 3 years. Grants are not available.

What if I become a citizen after buying HDB as a PR?

The flat becomes a citizen-owned flat. Any remaining rules (MOP, subletting) still apply from the purchase date.

Does a PR pay the 60% foreigner ABSD?

No. PR status attracts the PR ladder (5% / 30% / 35%) — not the foreigner flat rate.

This guide is for general information only and is accurate as of April 2026. Singapore property rules, taxes and cooling measures change frequently — always verify current figures with URA, IRAS, HDB or a licensed professional before committing. LovelyHomes is not a financial, legal or tax advisor.

Selling your HDB flat in Singapore is a four-stage process — Intent to Sell, marketing and negotiation, OTP, and completion. Each stage has its own legal document, its own timing constraints, and its own price-breaking pitfalls. This 2026 guide walks through the full sequence from the seller’s side.

See HDB’s official selling page for the regulatory details. This guide explains the practical mechanics.

Quick Answer — Selling an HDB Flat

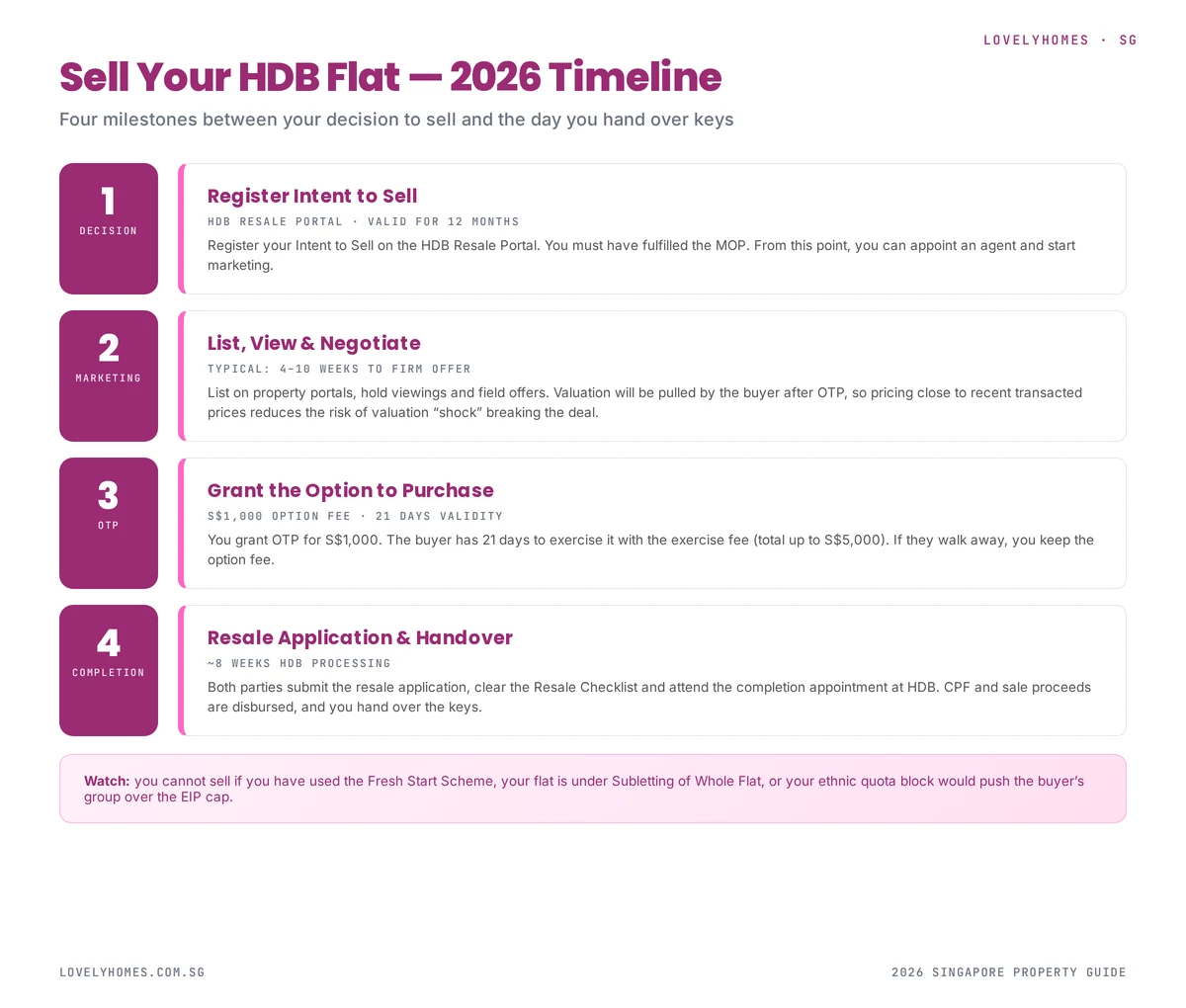

Check your MOP — 5 years from key collection for most flats.

Register Intent to Sell on the HDB Resale Portal.

List, view, negotiate — typically 4–10 weeks.

Grant the Option to Purchase (OTP) — S$1,000 option fee, 21-day validity.

Both parties submit the resale application — ~8 weeks HDB processing.

Completion appointment at HDB Hub — hand over keys.

Total: 3–4 months from listing to completion.

Four milestones between listing decision and handing over keys.

Step 1: Check Your MOP

You cannot sell an HDB flat until the Minimum Occupation Period (MOP) has been fulfilled. For most modern flats this is 5 years from key collection; for Plus and Prime flats it is 10 years. See our MOP guide for the exceptions and consequences of breach.

Time spent overseas for more than 6 months at a stretch does not count. If you have been posted abroad, verify with HDB that your effective MOP is what you think it is.

Step 2: Register Intent to Sell

Log into the HDB Resale Portal with Singpass and submit Intent to Sell. This is valid for 12 months. It:

Confirms your eligibility to sell (MOP, ethnic quota impact)

Allows you to appoint a licensed property agent

Triggers HDB’s valuation pipeline when an OTP is later granted

Gives buyers assurance that the flat is legitimately for sale

Step 3: Price, List and Negotiate

HDB resale is now in a tight market with COV back on the table. Price correctly:

Pricing benchmarks

Recent transacted prices on the HDB Resale Portal for the same block, type, and floor

Recent COV spread — has the estate been transacting above or below valuation?

Remaining lease — a shorter lease narrows the buyer pool considerably

Block-level ethnic quota — a block that is “closed” to major ethnic groups has a reduced buyer pool and attracts weaker offers

Agent vs no-agent

The HDB Resale Portal is designed to let sellers transact without an agent. However, a good agent will:

Run marketing on PropertyGuru, 99.co, and Facebook/IG for 2–4 weeks

Coordinate viewings (typically evenings and weekends)

Shepherd both parties through resale application submission

Typical seller-side commission in 2026 is 2% of the transacted price. See our agent commission guide.

Step 4: Grant the OTP

Once you and the buyer agree on a price, you grant the OTP. The option fee is fixed at S$1,000. The buyer then has 21 calendar days to exercise by paying the exercise fee (up to S$4,000 more, so total S$5,000 maximum). Key points:

If the buyer fails to exercise, you retain the S$1,000 option fee.

If the buyer does exercise, the sale becomes unconditional. You cannot then grant an OTP to another buyer.

Valuation is requested at this point — if it comes in below the agreed price, the buyer must pay the shortfall in cash (COV).

Step 5: Resale Application

Within 7 days of OTP exercise, both seller and buyer log into the HDB Resale Portal and jointly submit the resale application. You will:

Confirm the agreed price and terms

Select your conveyancing solicitor (HDB Legal or private)

Complete the Resale Checklist — a set of confirmations from both parties

Pay the administrative fee (S$80 for 1-2 room, S$120 for 3-room and above)

HDB then processes the application, targeted at 8 weeks. During this time, HDB will audit your ownership, verify the buyer’s eligibility, compute CPF refunds, and arrange the completion appointment.

Step 6: Completion Appointment

Typically 8–12 weeks after the resale application, you attend the completion appointment at HDB Hub. Both parties sign the transfer documents, CPF refund is credited to your Ordinary Account, the buyer’s loan is disbursed, and you hand over the keys.

What Happens to Your CPF and Sale Proceeds

The sale proceeds flow in this sequence:

Outstanding HDB or bank loan is repaid in full from the proceeds.

CPF refund — the principal you used from CPF, plus accrued interest, is refunded back into your CPF Ordinary Account. This can be substantial on a flat you have lived in for 10+ years.

Balance — what remains is your cash-in-hand from the sale.

If the flat has appreciated slowly or you used a large CPF component, the CPF refund may consume most of the proceeds, leaving little cash. This is the “negative sale” scenario and a real risk for short-lease resale.

Worked Example: Selling a S$680k 4-Room Flat

You bought the flat 9 years ago for S$420k, paid using S$100k CPF (principal) and a S$300k HDB loan, and have S$150k outstanding on the loan:

Item

Amount

Sale price

S$680,000

Less: outstanding HDB loan

(S$150,000)

Less: CPF refund (principal + 9yr accrued @ 2.5%)

(S$125,000)

Less: agent commission (2%)

(S$13,600)

Less: legal fees

(S$500)

Net cash in hand

S$390,900

CPF Ordinary Account now holds

S$125,000 more

Common Pitfalls

Accepting an offer before verifying buyer HFE status — if the buyer cannot get HFE, the deal collapses.

Ethnic quota surprise — HDB rejects the application because the sale would push the block over its EIP cap for the buyer’s ethnic group.

Valuation shortfall — the buyer walks away if the valuation is too low and they cannot fund the cash COV.

Underestimating CPF accrued interest — many sellers find far less cash in hand than expected.

Overestimating the flat — overpricing leads to extended listing periods and ultimately a lower final transacted price.

FAQ — Selling an HDB Flat 2026

Can I sell my flat before MOP is fulfilled?

Only under exceptional circumstances (divorce, death, financial hardship) and with HDB’s explicit approval. Otherwise, sale before MOP is not permitted.

How much cash will I actually get from the sale?

Sale price minus outstanding loan minus CPF refund minus agent commission minus legal fees. For most owners 5–10 years in, cash in hand is 40–60% of sale price.

Do I pay Seller Stamp Duty on an HDB resale?

Only if you have owned the flat for less than 3 years (very rare because of MOP). See our SSD guide.

Can I reject a buyer after accepting their OTP offer?

No. Once the OTP is granted and the buyer has paid the option fee, you are legally bound to sell to them if they exercise within 21 days.

What if the buyer’s HDB loan gets denied?

The buyer can walk away from the OTP, forfeiting the option fee (and exercise fee if already paid). You are then free to re-list and sell to another buyer.

Disclaimer: HDB processes, fees and scheme rules change over time. Verify the current rules with HDB before committing to sale. Consult your conveyancing lawyer for advice on your specific situation.

Buying an HDB resale flat in Singapore in 2026 is a process with clear, legally-defined stages. Miss one, and the deal either stalls or collapses entirely. This guide walks you through every step in the exact order you will actually encounter it — from securing your HDB Flat Eligibility (HFE) letter to collecting the keys.

For the official rules, refer to the HDB Resale Buying page. This article explains what those rules mean in practice and how the numbers add up for a typical 2026 buyer.

Quick Answer — The HDB Resale Buying Process

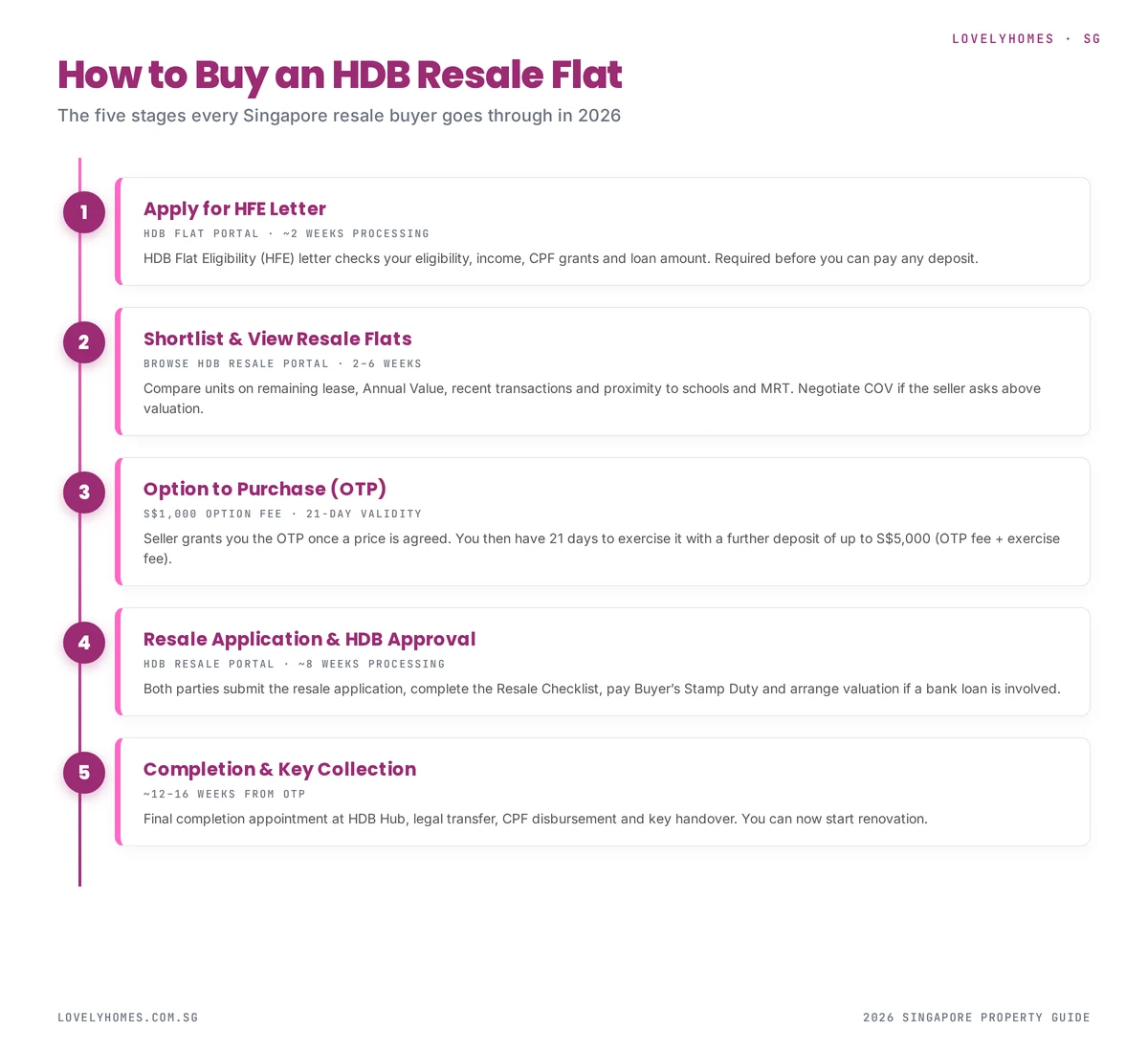

Apply for HFE letter on the HDB Flat Portal (~2 weeks processing).

Shortlist and view flats (typically 2–6 weeks).

Negotiate, then receive the OTP from the seller (S$1,000 option fee).

Exercise the OTP within 21 days with the exercise fee (up to S$4,000 more).

Submit the resale application on the HDB Resale Portal.

Complete the purchase at the HDB Hub appointment and collect keys.

Total elapsed time: typically 12–16 weeks from OTP to keys.

The five stages of buying an HDB resale flat, from HFE letter to keys.

Step 1: Apply for Your HFE Letter

The HDB Flat Eligibility (HFE) letter is the gating document for any HDB purchase. It confirms three things in a single statement: whether you are eligible to buy, how much CPF housing grant you qualify for, and the maximum HDB loan you can take.

You apply through the HDB Flat Portal using Singpass. The portal will check your household income, ages, citizenship, and existing property holdings. Processing usually takes around two weeks — but longer if HDB needs clarification on income or existing flat ownership.

The HFE letter is valid for six months, and you cannot exercise any OTP without one. Budget for your HFE to be ready before you start serious viewings — you will see sellers, and agents expect you to have it lined up.

What the HFE letter tells you

Whether your household meets the eligibility conditions (at least one SC, under the S$14,000 monthly household income ceiling, no overlapping private-property ownership).

The exact CPF Housing Grants you qualify for (CPF Housing Grant, Enhanced CPF Housing Grant, Proximity Housing Grant).

The maximum HDB Concessionary Loan you can take, based on TDSR and MSR.

The minimum cash required at OTP and exercise stages.

Step 2: Shortlist Flats and Conduct Viewings

Once you have your HFE letter in hand, you can begin serious viewings. The HDB Resale Portal and third-party sites (PropertyGuru, 99.co, ourselves at LovelyHomes) let you filter by town, flat type, remaining lease and recent transacted price.

What to actually evaluate at a viewing

Remaining lease: Directly affects your maximum loan tenure and CPF usage. Anything under 60 years of remaining lease starts restricting grants and CPF usage significantly.

Condition of the flat: Look past the paint. Check ceilings for water marks (upstairs leaks), windows for water ingress, and door frames for termite damage.

Ethnic quota status: Your ethnic group must be under the block-level EIP cap. Ask the agent if the block is “open” for your group.

Noise and dust: Traffic, MRT, and construction noise. Visit twice — once at peak hour, once in the evening.

Ownership history: The agent should be able to confirm the number of previous owners and whether any structural alterations were made without HDB approval.

Step 3: Negotiate the Price and Receive the OTP

Once you and the seller agree on a price, the seller grants you the Option to Purchase (OTP). The option fee is fixed by HDB at S$1,000, paid on the spot. This buys you the exclusive right to purchase that flat at the agreed price for 21 calendar days.

The OTP is a legally binding document for the seller during those 21 days — they cannot sell to anyone else. But you, the buyer, can walk away by simply not exercising the option. You forfeit the S$1,000 but have no further obligation.

Cash-Over-Valuation (COV) in 2026

If the agreed price exceeds HDB’s official valuation, the gap must be paid in cash — never from CPF or loan. This is Cash-Over-Valuation, and it is firmly back on the table in 2026’s tight resale market. Budget for it if you are bidding on a popular estate or a high-floor unit. See our full COV guide for negotiation tactics.

Step 4: Exercise the OTP

Within the 21-day window, you exercise the OTP by paying the exercise fee. The option fee plus exercise fee cannot exceed S$5,000 combined — typically structured as S$1,000 option + S$4,000 exercise. At this point the sale becomes unconditional.

In the same 21 days, you should:

Engage a conveyancing lawyer (HDB’s in-house Legal & Claims Registry is a low-cost option for straightforward cases).

If taking a bank loan, finalise your loan offer and submit it for valuation.

Prepare the Buyer’s Stamp Duty (BSD) — due within 14 days of OTP exercise.

Step 5: Submit the Resale Application

Once the OTP is exercised, both parties log into the HDB Resale Portal and submit the resale application jointly. The portal walks you through the Resale Checklist, financial plan, and any declarations.

You will pay stamp duty, agree on the completion timeline, and nominate your solicitor. Your CPF refund to the seller, the loan disbursement and the final cash shortfall are all calculated at this point. HDB aims to process the resale application within eight weeks.

Typical fees at application stage

Resale application fee: S$80 (1-room / 2-room flats) or S$120 (3-room and above).

Buyer Stamp Duty (BSD): Graduated — 1% on first S$180k, 2% on next S$180k, 3% on next S$640k, 4% thereafter. On a S$600k resale, BSD comes to S$12,600. See our BSD guide for the full maths.

Legal fees: S$350–S$600 via HDB Legal, S$1,800–S$3,000 via a private conveyancing firm.

Step 6: Completion and Key Collection

About twelve to sixteen weeks after you first exercised the OTP, you will attend the completion appointment at HDB Hub. Both parties sign the legal transfer documents, CPF disbursements are triggered, your bank or HDB loan is drawn down, and you receive the keys.

From this moment, the flat is legally yours. Your MOP clock starts ticking from this date — see our MOP guide for what that means going forward.

Worked Example: Buying a S$620,000 4-Room Resale Flat

Let’s walk through a realistic 2026 purchase. A young couple, both Singapore Citizens and first-time buyers, buy a 4-room resale flat in Sengkang at S$620,000 — S$30,000 above HDB’s valuation of S$590,000.

Component

Amount

Purchase price

S$620,000

HDB valuation

S$590,000

COV (cash)

S$30,000

HDB loan @ 75% of valuation

S$442,500

Cash + CPF downpayment (25% of valuation)

S$147,500

Buyer Stamp Duty

S$13,200

Legal fees (HDB route)

~S$500

Minimum cash needed upfront

~S$60,000

The couple might qualify for an Enhanced CPF Housing Grant of up to S$80,000 depending on their combined income, which offsets a large chunk of the downpayment. See our CPF for property guide for how the grants flow into the purchase.

Common Mistakes That Delay or Kill the Deal

No HFE letter in hand: You cannot exercise an OTP without one. Plan at least three weeks of buffer before you start offering.

Underestimating COV: It has to come from cash savings, not CPF. Many deals collapse at OTP because buyers find their cash short.

Ignoring the ethnic quota: Your offer can be accepted, only to have HDB reject the resale application because the block is full for your group.

Not checking structural alterations: Unauthorised renovations (load-bearing wall removal, unpermitted window grilles) are the buyer’s problem after completion.

Valuation shock: If the valuation comes in below the purchase price, the cash shortfall must be covered by you — not CPF.

FAQ — HDB Resale Buying 2026

How long does the entire HDB resale process take?

Typically 12–16 weeks from OTP exercise to keys. Add another 2–6 weeks for your flat search, and 2 weeks for the HFE letter.

Can I use CPF to pay the option fee?

No. The S$1,000 option fee and the up-to-S$4,000 exercise fee both come from cash. CPF Ordinary Account funds only flow in at the resale-application stage.

What happens if I cannot exercise the OTP in time?

You forfeit the S$1,000 option fee. The seller is then free to grant the OTP to someone else.

Do I need a property agent to buy HDB resale?

No. HDB’s Resale Portal is designed to let buyers and sellers complete the process without an agent, though you are welcome to use one. Total agent commission on the buyer side is typically 1% of the purchase price.

Can I back out after I exercise the OTP?

Only with the seller’s agreement, and you would likely forfeit both the option and exercise fees (up to S$5,000). HDB does not have a “cooling-off” period for resale buyers once OTP is exercised.

Disclaimer: This is general guidance, not legal advice. Rules, fees and grant amounts change periodically — always verify with HDB directly before committing. Consult a qualified conveyancing lawyer for your specific purchase.

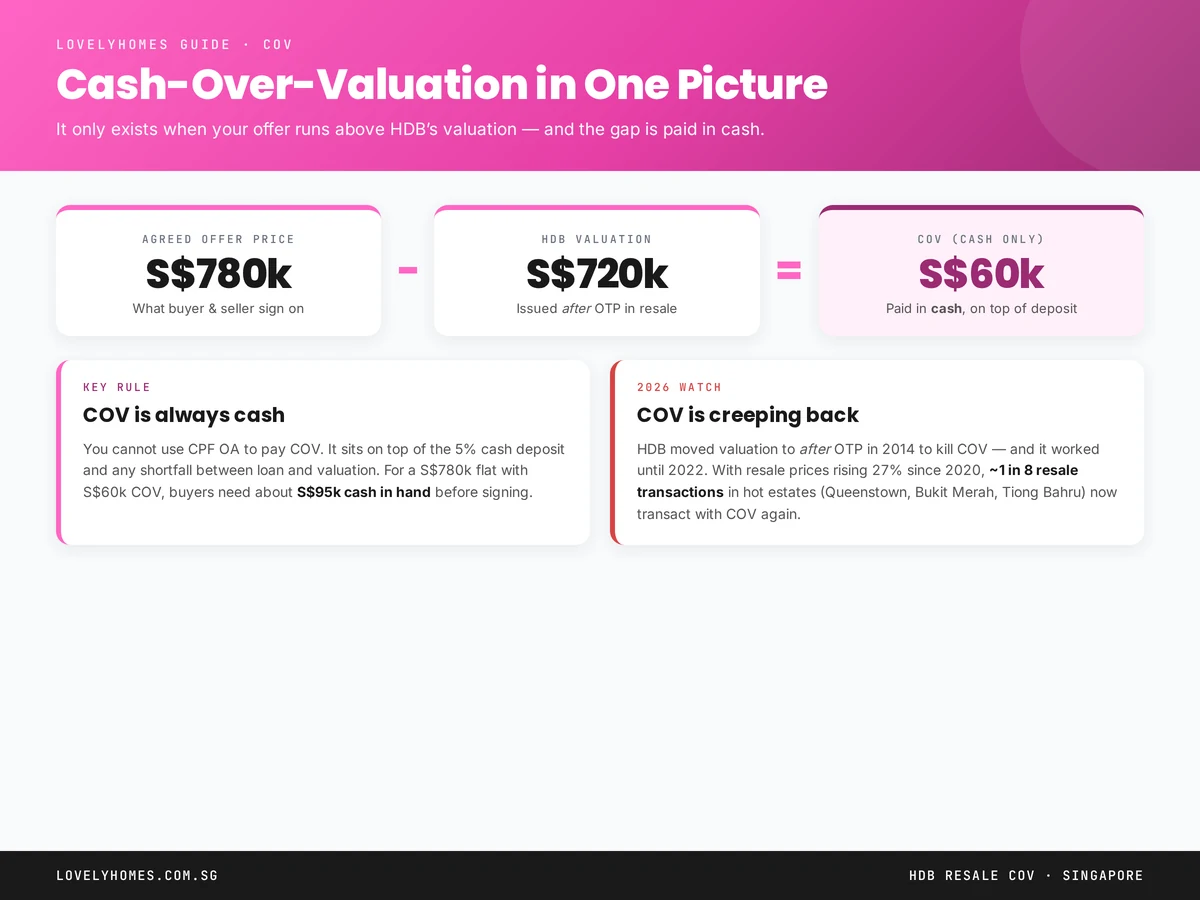

Cash-Over-Valuation — COV — is the gap between the price a Singapore HDB resale buyer agrees to pay and the official valuation HDB assigns to the flat. That gap is paid entirely in cash, on top of the 5% deposit and any loan shortfall. For the first time since 2014, COV is measurably back in Singapore’s hotter resale estates — and most buyers have no mental model for it.

This 2026 guide explains exactly how COV arises, why HDB redesigned the valuation process to kill it in 2014, why it came back, and how to negotiate it down when you are sitting across the table from a seller’s agent. For the official valuation process, see the HDB resale valuation page.

Quick Answer — COV at a glance

COV = offer price − HDB valuation. If positive, the difference is payable in cash only.

No CPF allowed. You cannot draw CPF OA to pay COV.

No loan allowed. Banks and HDB cap their loans at LTV applied to valuation, not to price.

On top of: 5% cash deposit, any BSD and ABSD, and any shortfall between loan quantum and valuation.

Typical 2026 COV in hot estates: S$20,000–S$80,000 in Queenstown, Bukit Merah, Tiong Bahru.

How COV Arises

HDB resale purchases follow a fixed sequence: buyer and seller agree on a price; buyer pays a S$1,000 Option Fee; HDB conducts its valuation; buyer exercises the OTP within 21 days with a further 4% cash Option Exercise Fee. The valuation comes after the price agreement.

If the agreed price is higher than HDB’s valuation, the buyer has a choice: abandon the option (losing S$1,000) or proceed and pay the gap in cash. That gap is COV.

Figure 1: The COV formula. S$60k in cash, stacked on top of the S$39k cash deposit, is what a buyer really needs before signing.

A Worked Example

A couple agrees to buy a 4-room flat in Queenstown for S$780,000. HDB valuation comes back at S$720,000.

Loan ceiling: HDB loan at 75% LTV on valuation = 75% × S$720,000 = S$540,000.

Downpayment (25%) on valuation: 25% × S$720,000 = S$180,000 from CPF or cash.

Loan shortfall: loan only covers S$540,000; purchase price is S$780,000 — shortfall of S$240,000 covered by downpayment (S$180,000) + COV (S$60,000).

Total cash required (excluding stamp duty): 5% deposit + COV = S$39,000 + S$60,000 = S$99,000. BSD of about S$17,400 must also be paid (reimbursable from CPF OA).

Why COV Was “Killed” in 2014

From 1994 to 2014, HDB valuations were issued before buyers made offers. Agents advertised a flat with both the valuation and the asking COV — e.g. “valued at S$500k, asking S$550k (S$50k COV).” This framing normalised COV as a negotiated headline number and fed a runaway COV culture.

In March 2014, HDB reversed the sequence: buyers agree a price first, then HDB values the flat. With buyers no longer able to advertise or openly negotiate COV, the market default moved to “price at valuation” and COV collapsed to zero on most transactions for nearly a decade.

Why COV Is Back in 2026

Resale prices rose 27% between 2020 and 2025 on the HDB Resale Price Index. HDB’s own valuations are based on a 6-month trailing transaction window — which means when prices rise fast, valuations lag the market. In a hot estate, an agent can credibly point to last-week comparables at S$800k while HDB’s valuation, anchored to six-month-old evidence, comes in at S$740k.

Premium locations: mature estates near MRT and international schools see thinner supply and bigger price-to-valuation gaps.

Cash-heavy buyer pools: multi-generational households and HDB upgraders returning to buy smaller units have cash on hand to pay COV.

In Q4 2025, HDB data showed roughly 1 in 8 resale transactions with measurable COV, concentrated in Queenstown, Bukit Merah, Tiong Bahru, Toa Payoh, and Kallang/Whampoa. Two years earlier the number was closer to 1 in 30.

How to Negotiate COV Down

Sellers asking for COV have real competition. Use these levers:

Pull recent transaction comparables.HDB Resale Portal publishes all resale transactions with price, flat type, floor range and storey. If the asking price is above the 90th percentile for comparable flats in the same block, push back with evidence.

Request HDB valuation before exercise. The valuation is issued to you after the OTP is granted. If the gap is unacceptable, you have 21 days to walk away and lose only the S$1,000 Option Fee.

Time your viewing. Sellers under pressure (downgrading, emigrating, selling to fund a BTO completion) drop COV asks fastest. Ask the agent what the seller’s next move is.

Offer a smooth completion. Sellers often trade COV against completion certainty — pre-approved loan, short exercise window, willingness to extend for them to buy their next place.

Walk away. On 2 of every 3 COV asks in 2026, the next buyer in the pipeline pays less or at valuation. Patience is priced.

When COV Is Actually Worth Paying

COV is not always irrational. Sometimes it reflects real scarcity that will not reverse:

Rare floor plate. A high-floor corner unit with panoramic view and cross-ventilation in a mature estate.

Zero-renovation condition. Move-in-ready flats save S$40k–S$80k in renovation and 3–6 months of rent elsewhere.

Family proximity. Living near parents for childcare or caregiving has a legitimate non-market value.

The rule of thumb: if the COV is less than 2% of the purchase price and the trade-offs are non-replicable, paying is defensible. Above 5% COV is rarely justified.

Frequently Asked Questions

Is COV allowed for BTO or EC purchases?

No. COV only appears in HDB resale transactions where a valuation is issued separately from the price. BTO flats are priced directly by HDB; ECs are priced by developers. Both settle on price and never encounter a valuation gap.

Can the seller accept my offer at or below valuation?

Yes. Many transactions settle at valuation with zero COV. The seller’s agent may push back, but the buyer ultimately chooses whether to pay COV.

What happens if HDB undervalues the flat and I walk away?

You forfeit the S$1,000 Option Fee and the 21-day exercise window lapses. No other penalty.

Can I request a second valuation?

HDB valuations are final for the purpose of that transaction. You cannot appeal or request a second opinion — you must walk away and try a different flat.

Does the seller benefit from a higher COV?

Yes, directly. Every dollar of COV goes to the seller in cash at completion. This is why agents representing sellers push for higher COV asks in a tight market.

TDSR & MSR 2026 — because MSR, not LTV, is usually the binding loan limit for HDB buyers.

BSD Singapore 2026 — stamp duty on the purchase price, including any COV component.

Disclaimer: This guide is general information, not financial advice. HDB rules and valuation practice are subject to change. Verify current rules at hdb.gov.sg.