HDB Resale Levy Singapore 2026: Who Pays It, How Much, and How to Avoid It

Quick answer — the resale levy in 30 seconds

- The HDB resale levy is a one-off charge on second-timer households who take a second housing subsidy from HDB (BTO, Sale of Balance Flats, or a new Executive Condominium).

- It does not apply if you sell your subsidised flat and buy on the open resale market without claiming any fresh HDB grant.

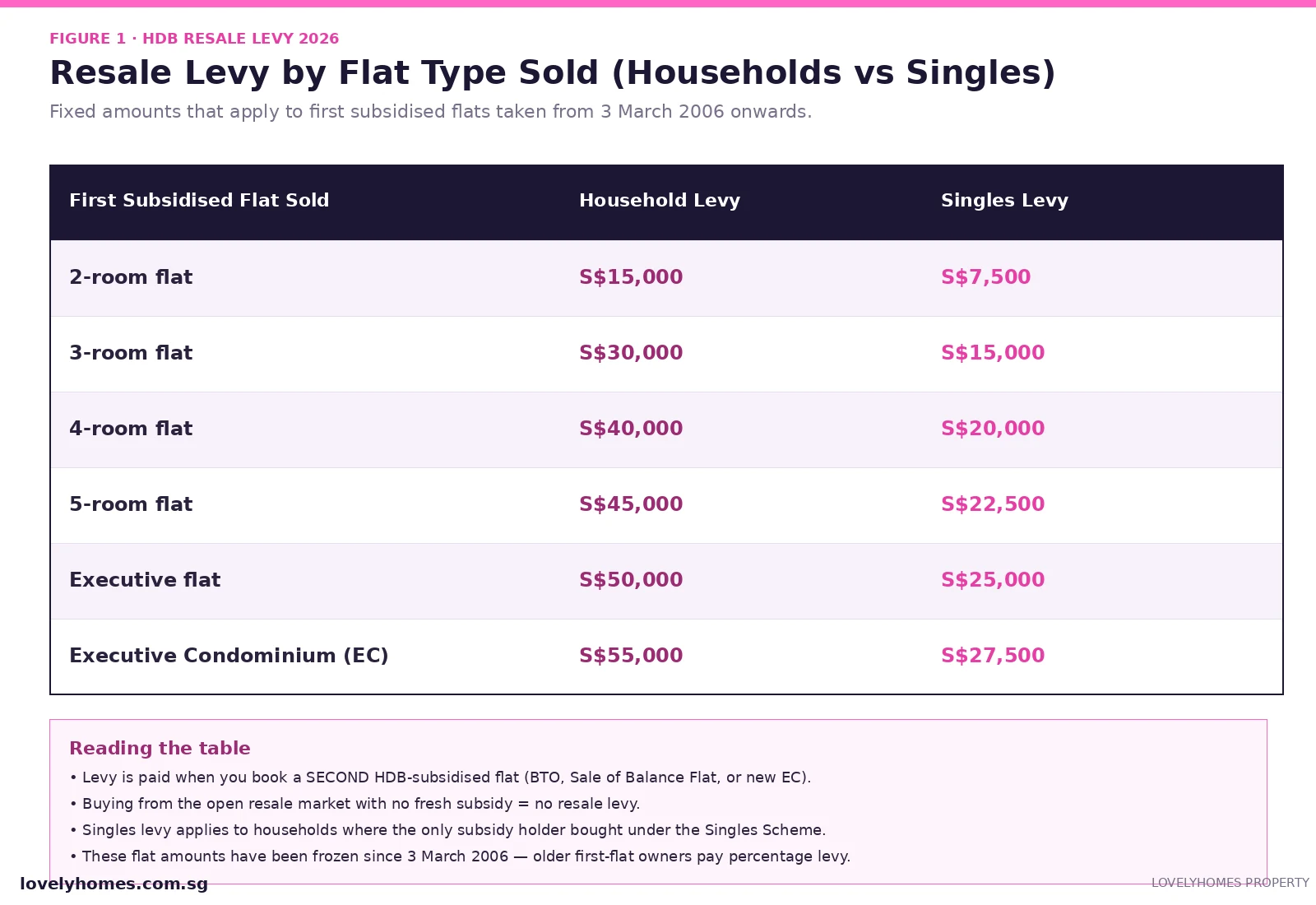

- For first subsidised flats taken from 3 March 2006, the levy is a fixed amount — S$15,000 for a 2-room sold up to S$55,000 for an EC.

- Households who got their first subsidy before 3 March 2006 pay a percentage levy of 10–25% of the resale price instead.

- Singles Scheme buyers pay half the household amount.

- The levy is paid in cash (or net cash proceeds from selling the first flat) — CPF cannot be used.

- Payment is collected at the point of booking the second subsidised flat, before key collection.

- Buying on the open market means no levy, but you still face BSD, ABSD (where applicable) and SSD if you sell within three years.

What is the HDB resale levy?

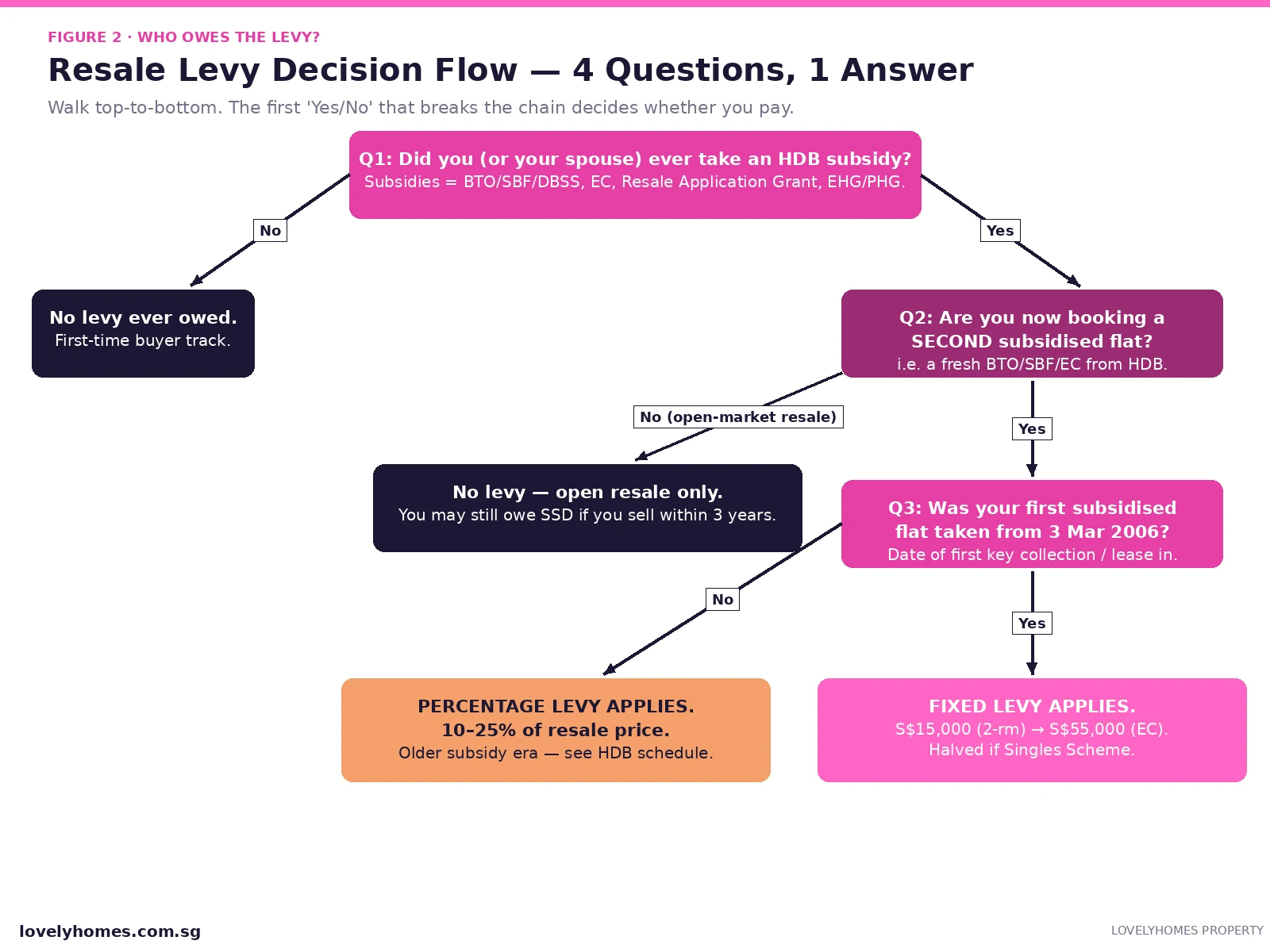

The resale levy is a charge that the Housing & Development Board (HDB) imposes on a household which has already enjoyed a housing subsidy and now wants a second bite at one. The Government’s logic is straightforward: public housing subsidies are taxpayer-funded, and a household should not collect them twice without contributing back. Selling the first subsidised flat is fine; what triggers the levy is the act of booking another subsidised flat — a fresh BTO, a Sale of Balance Flat, an open booking unit, or a brand-new Executive Condominium directly from the developer.

Crucially, the levy is administered by HDB, not IRAS. It is separate from Buyer’s Stamp Duty, ABSD, and Seller’s Stamp Duty. You can owe stamp duties and a resale levy in different scenarios, and they are calculated, paid, and tracked independently.

Who actually pays the levy?

The resale levy travels with the household, not the property. If at any point in your housing history you (or your spouse, or your essential occupier) have already enjoyed an HDB subsidy, you are a second-timer in HDB’s eyes the next time you approach them for a fresh subsidy. The subsidies that count include:

- A new flat purchased directly from HDB (BTO, Sale of Balance Flats, Re-Offer of Balance Flats, open-booking flats).

- A Design, Build and Sell Scheme (DBSS) flat bought from a private developer.

- An Executive Condominium bought directly from the developer (first hand).

- A resale flat bought with one of the older Resale Application Grants — CPF Housing Grant for Family, Singles Grant, or Half-Housing Grant — taken before changes to the levy rules.

- HUDC flats and SERS replacement flats taken under HDB schemes count similarly.

If your only subsidy was the Enhanced CPF Housing Grant (EHG) or the Family Grant on a resale flat purchased after 3 March 2006, you are not automatically deemed a levy-paying second-timer for the purpose of a future resale flat purchase — but you do pay the levy if you next buy a new flat or new EC.

How the levy is calculated

Two regimes apply, and the dividing line is the date of your first subsidised flat’s key collection (or in the case of an EC, the date you signed the Sale & Purchase Agreement).

Fixed-dollar levy (first flat from 3 March 2006)

This is the regime almost every modern buyer falls under. The amount is locked to the type of flat you sold:

| First subsidised flat sold | Household levy | Singles Scheme levy |

|---|---|---|

| 2-room flat | S$15,000 | S$7,500 |

| 3-room flat | S$30,000 | S$15,000 |

| 4-room flat | S$40,000 | S$20,000 |

| 5-room flat | S$45,000 | S$22,500 |

| Executive flat / HUDC | S$50,000 | S$25,000 |

| Executive Condominium | S$55,000 | S$27,500 |

The fixed amount does not move with property prices, which is good news for households whose first flat appreciated heavily in resale. A 4-room sold today for S$700,000 still owes only S$40,000 in levy — about 5.7% of the resale price.

Percentage levy (first flat before 3 March 2006)

Older second-timers face the legacy regime. Levy is set as a percentage of the higher of the resale price or 90% of the market valuation:

| First subsidised flat sold | Household levy % | Singles Scheme levy % |

|---|---|---|

| 2-room flat | 10% | 5% |

| 3-room flat | 20% | 10% |

| 4-room flat | 22.5% | 11.25% |

| 5-room flat | 25% | 12.5% |

| Executive flat / HUDC | 25% | 12.5% |

For a household that sold a 4-room legacy flat for S$650,000, the percentage levy lands at S$146,250 — markedly higher than the modern fixed levy. This is one reason long-time HDB owners often choose to remain in the resale market rather than ballot for a fresh BTO.

When and how the levy is paid

HDB collects the resale levy at the point of booking the second subsidised flat. In practice this means:

- You sell your first subsidised flat. CPF is refunded with accrued interest; the cash balance is yours.

- You ballot for, queue, and book a second BTO/SBF/SBF or sign for an EC.

- HDB issues a payment notice for the levy, payable in cash only. CPF cannot be used.

- Levy is paid before signing the lease agreement / S&P. Failure to pay forfeits the booking.

If the second flat is booked before the first has been sold, HDB defers the levy to the resale completion date and may require an undertaking. Some buyers structure it this way to avoid being homeless between sale and BTO completion, especially in long-build projects.

Who is exempt or partially relieved?

HDB allows a small set of waivers and concessions, and these matter most for older households and downgraders:

- Buying a 2-room Flexi flat on a short lease (45 years or less) at age 55 and above. The resale levy is waived in full to encourage right-sizing.

- Buying a Studio Apartment / Community Care Apartment. No resale levy applies (these are senior-targeted typologies).

- Divorce settlements where one party retains the existing flat. No levy event; only one of the parties may face a levy if they later buy a fresh subsidised flat.

- Sub-letting income or rental of bedrooms does not trigger the levy. The levy only fires when the subsidised flat is sold and a new subsidised flat is booked.

- Open-market resale purchases without grants are not levy events. You can move from a 4-room HDB to another resale 5-room without grant, and no levy is triggered.

Resale levy vs CPF refund vs stamp duty — separating the bills

It is easy to confuse three different cash flows that all hit a second-timer household at roughly the same time. They are independent and add up:

| What you pay | Who collects | Triggers | Source of funds |

|---|---|---|---|

| Resale levy | HDB | Booking second subsidised flat | Cash only |

| CPF accrued interest | CPF Board (refund into your OA) | Sale of any flat | Auto-deducted from sale proceeds |

| Buyer’s Stamp Duty | IRAS | Any property purchase | Cash + CPF allowed |

| Additional Buyer’s Stamp Duty | IRAS | Second / third / foreign buyer purchase | Cash + CPF allowed |

| Seller’s Stamp Duty | IRAS | Sale within 3-year holding period | From sale proceeds |

The CPF accrued interest is not a fee — it is your own money being returned to your OA — but it shrinks the cash you can deploy on the next purchase. Plan around it the same way you plan around the resale levy.

Worked example — same family, two paths

Take a Singapore Citizen couple, married 12 years, who bought a 4-room BTO in Punggol for S$320,000 in 2014 with a Family Grant. In 2026 they have hit the 5-year MOP, the flat is valued at S$680,000, and they are deciding whether to upgrade through a fresh BTO or to buy a private resale condo.

Path A — buying a 5-room BTO — costs S$40,000 in levy plus the new flat price of S$580,000. Path B — buying an S$1.4M open-market resale condo — skips the levy entirely but adds S$45,400 in BSD and S$280,000 in ABSD at the 20% citizen-second-property rate, totalling S$325,400 in stamp duty. The headline conclusion: the resale levy is real money, but it is dwarfed by ABSD whenever the alternative is a private-market upgrade. Couples often see this comparison only after they put pen to paper, which is why it pays to model both routes early.

Why the levy exists at all

Singapore’s housing model rests on two policy pillars: keeping public housing affordable to first-timers, and rationing taxpayer subsidies. Without a levy, a household could ride the BTO market repeatedly — cashing in on resale price growth at each cycle and stepping up to bigger flats with full subsidies each time. The levy is the friction that makes a second BTO a deliberate choice rather than a default. It also keeps queues for new BTOs balanced — first-timers always get priority, but second-timers compete for the remaining quota and pay the levy if they win one.

Compared with peer markets, the Singapore approach is unusual. Hong Kong’s Home Ownership Scheme uses a price clawback rather than a flat levy. Australia’s First Home Owner Grant has no second-time levy because grants there are smaller and time-limited. The Singaporean fixed-dollar approach is a useful piece of housing-policy plumbing that most buyers only encounter once.

What this means for you

If you are a current HDB owner thinking about your next move, the levy reshapes the decision in three concrete ways. First, it makes the open resale route surprisingly competitive — for many flat types the levy is comparable to the lawyer-and-valuer fees on a private resale and is comfortably under the BSD on a S$1.5M condo. Second, because the levy is fixed, smaller flat owners (2-room, 3-room) face a friendlier upgrade path than larger flat owners; the household that sold a 5-room or EC pays the most. Third, the levy is cash-only — that imposes a real liquidity hit at exactly the moment you are also funding the down-payment, legal fees, and renovation on the next home.

A common mistake is to treat the levy as one of many transaction costs and bake it into the budget late. Run the numbers up front, ideally on the same spreadsheet you use for down payment and LTV planning. If you are upgrading to a private property, the right comparison is the levy versus the ABSD and BSD on the alternative — almost always a smaller bill, in absolute terms, than the stamp duties on a S$1.5M+ condo.

What might come next

The fixed-dollar regime has been frozen since March 2006. Construction costs and median flat prices have roughly tripled since then, which has progressively eroded the real value of the levy. There has been periodic public commentary that the Government may reconsider the schedule — either by indexing it to a property price benchmark or by raising the EC and 5-room amounts. In the same vein, the percentage-based legacy regime continues to age out as pre-2006 first-flat owners exit the market.

Two policy directions are plausible from here. One is a recalibration that pushes the larger-flat levies upward to keep relative ratios stable as flat prices move. The other is a structural rethink that ties the levy to the resale price like the legacy regime, but capped to avoid punishing strong resale gains. Either direction would arrive with notice and a generous grace period for booked transactions; speculation is not a reason to rush a BTO ballot. The forward-looking view here is that some upward adjustment is likely over the next several years, but transparency and lead time are part of HDB’s playbook.

Frequently asked questions

Does the resale levy apply if I sell my HDB and buy a private condo?

No. The levy only triggers when you book another subsidised flat from HDB (BTO, SBF, fresh EC). Buying a private resale condo or a new condo from a developer does not engage the levy at all — although you will face full BSD plus ABSD where applicable.

Does the resale levy apply when I buy a resale flat with a CPF grant?

For first subsidised flats taken from 3 March 2006 onwards, second-timer households who buy a resale flat with grants are subject to a smaller adjustment rather than a full resale levy. Historically (pre-March 2006) a percentage levy did apply. Always check HDB’s resale flat eligibility letter for your specific case before you make an offer.

Can I pay the resale levy from my CPF Ordinary Account?

No. The levy is payable in cash. The cash you have on hand from the sale of your first flat — after CPF is refunded with accrued interest — is the typical source of funds. Some households top up with a small bridging loan to cover the gap between flat sale completion and second-flat booking.

What if my spouse and I both owned subsidised flats before marriage?

HDB looks at the household, not the individual. If either of you previously took an HDB subsidy, the next subsidised flat the new household books is treated as a second purchase. Only one resale levy is owed per household per flat sold.

Will the levy be waived if I am buying a smaller flat to right-size?

Only in tightly defined cases — chiefly the 2-room Flexi short-lease flat at 55+, and Studio Apartment / Community Care Apartment purchases. Right-sizing into a longer-lease 2-room or 3-room generally still triggers the levy if it is a fresh subsidised flat.

Does the resale levy apply to Executive Condominium buyers?

Yes — and it is the largest category, S$55,000 for households who previously sold an EC. Crucially, the levy fires on the first hand EC purchase only. After the EC’s 5-year MOP and 10-year privatisation, subsequent buyers are private-market buyers and never face the levy.

If I divorce and one of us keeps the flat, does the other party still owe the levy?

The party who retains the flat keeps the subsidy attribution; if they later remarry and book another subsidised flat, the levy applies. The other party’s eligibility is reviewed against their new household status — the levy is only assessed at the point of booking a fresh subsidised purchase.

Disclaimer: This article summarises the resale levy regime as administered by the Housing & Development Board (HDB) of Singapore. Levy amounts, eligibility rules and waivers may be updated by HDB from time to time. Always verify the current schedule against the HDB resale levy page on hdb.gov.sg, your eligibility letter, and where relevant the Inland Revenue Authority of Singapore (IRAS), the Central Provident Fund (CPF) Board, the Monetary Authority of Singapore (MAS), and SingStat for housing market data. This article does not constitute legal, financial or tax advice — speak to a licensed conveyancing lawyer, a HDB-listed mortgage advisor, or a registered financial adviser before transacting.