Seller’s Stamp Duty (SSD) Singapore 2026: When You Pay, How Much, and How to Avoid It Legally

Seller’s Stamp Duty (SSD) is the Singapore Government’s anti-flipping tax. If you sell a residential property within three years of buying it, you pay a percentage of the sale price — up to 12% — on top of every other selling cost. Get the holding period wrong by even a single day, and a profitable sale can flip into a six-figure loss.

This guide walks you through SSD in 2026: who pays it, how the rate ladder works, when the holding clock starts and stops, who is exempt, and the strategies sellers actually use to manage it. All rates reflect the framework in force since 11 March 2017, which remains current. For the authoritative figures, always check the IRAS Seller’s Stamp Duty page.

Quick Answer — SSD at a glance

- SSD applies only to residential property sold within 3 years of acquisition.

- Rate ladder: 12% (year 1) · 8% (year 2) · 4% (year 3) · 0% thereafter.

- The clock starts on the date you signed the OTP or accepted the S&P — not the day you collected the keys.

- Payable within 14 days of contract for sale, on the higher of price or market value.

- Most short-term sales are caught: divorce sales, job relocations, second properties — SSD applies to nearly all of them.

- Industrial property has a separate (shorter) ladder; commercial property is exempt.

What Is SSD and Why Does It Exist?

SSD is a transaction tax levied on the seller of a residential property in Singapore when the property is sold within a defined holding period. It is administered by the Inland Revenue Authority of Singapore (IRAS), calculated on the higher of the sale price or the market value, and payable within 14 days of the contract for sale.

The tax was first introduced in February 2010 and progressively widened in 2011 and 2013 as part of the Government’s suite of property cooling measures. The most recent recalibration was in March 2017, which shortened the SSD holding period from four years to three and lowered the headline rate from 16% to the present 12% — a deliberate easing aimed at supporting genuine homeowners rather than speculators. The 2017 framework is still the live rule book in 2026.

The policy goal is simple: discourage speculative flipping while leaving genuine end-users untouched. By the time you have held a private condo or HDB flat for three full years, the cooling-measure case for taxing your sale is gone, and SSD falls to zero.

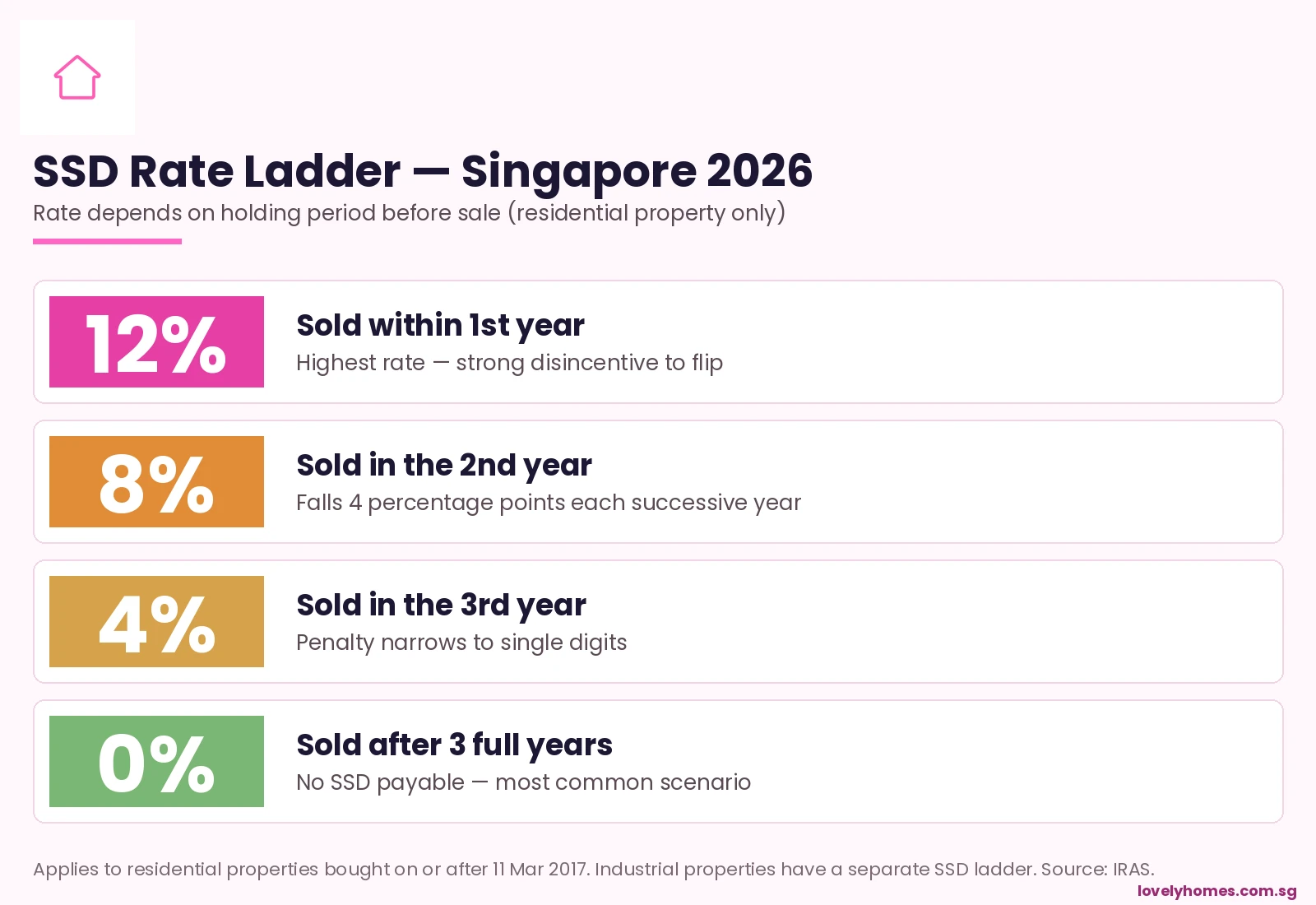

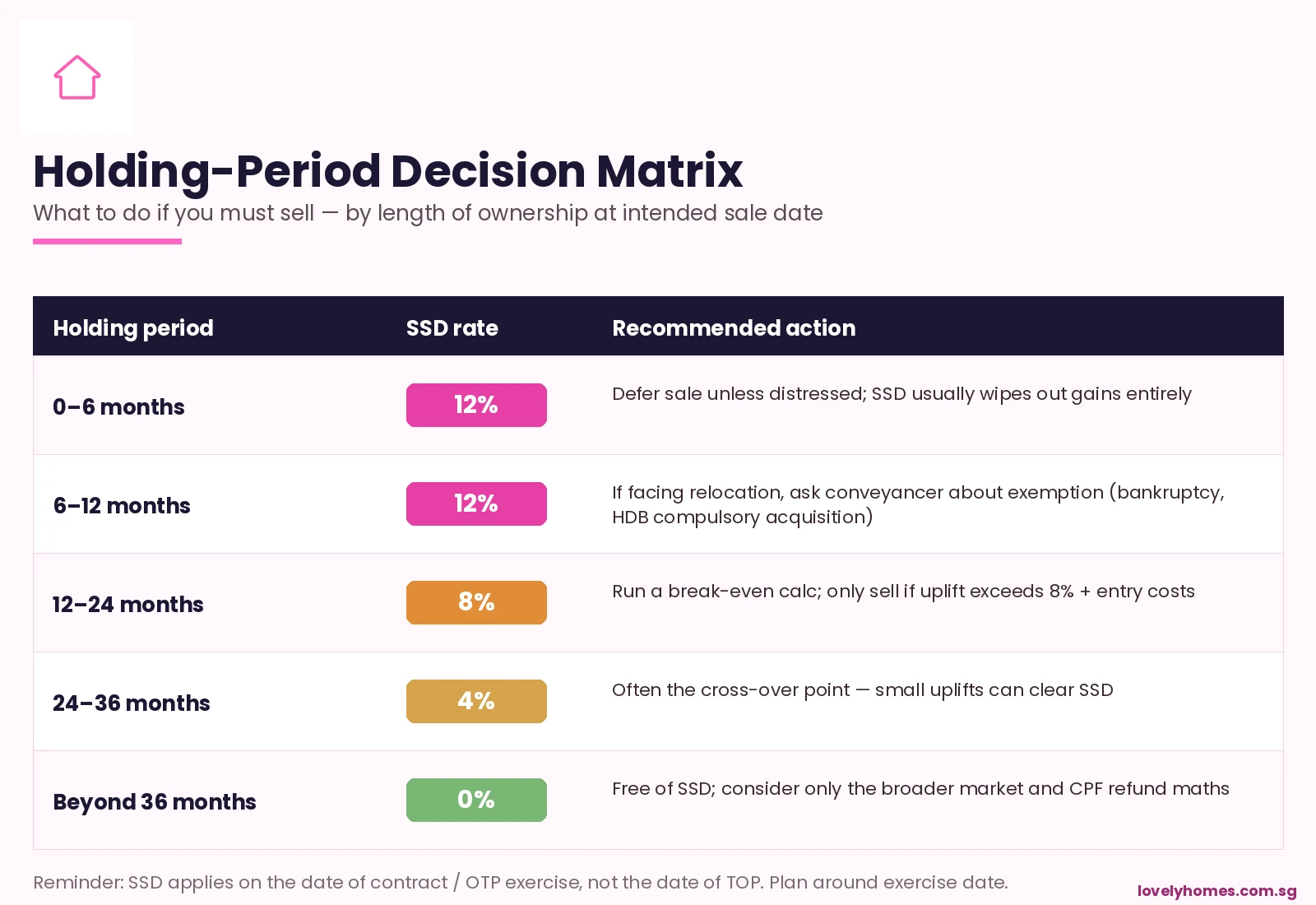

The 2026 SSD Rate Ladder

The rate you pay depends entirely on how long you held the property before signing the contract for sale. The ladder is steep at the top and falls four percentage points each subsequent year:

| Holding period at sale | SSD rate | Apparent on a S$1.5M sale |

|---|---|---|

| Up to 1 year (within 1st year) | 12% | S$180,000 |

| More than 1 to 2 years | 8% | S$120,000 |

| More than 2 to 3 years | 4% | S$60,000 |

| More than 3 years | 0% | Nil |

The rate is applied to the higher of the contracted sale price or IRAS’s assessed market value — sellers cannot lower their SSD bill by deliberately under-pricing a transaction.

When Does the Holding Clock Start — and Stop?

This is where most disputes arise, because the holding period is calculated to the day. The general rule is:

- Start: the date the buyer signs the Option to Purchase (OTP) or, if there is no OTP, the date of the Sale & Purchase Agreement (S&P).

- End: the date the buyer signs the next OTP or S&P when reselling.

Note carefully — the keys handover (TOP for new condos, vacant possession for resale) is irrelevant to SSD. A buyer who signs an OTP on 1 March 2024 and signs the next OTP on 28 February 2027 has held for one day under three years — SSD at 4% applies. Sign on 2 March 2027 and SSD drops to zero. Conveyancers routinely time exercise dates around this calendar boundary.

For new launches under construction, the start date is the OTP exercise date, not the TOP date. This means a buyer who signed an OTP in early 2023 for a project that only TOP’d in 2026 is already past the SSD window when they collect the keys.

Who Is Exempt or Remitted?

The exemptions list is narrow. SSD remission is granted only in specific situations, including:

- HDB flats — not subject to SSD because HDB has its own Minimum Occupation Period (MOP) regime, which generally bars resale within five years.

- Compulsory acquisition by the State (for example, road or MRT line widening).

- Bankruptcy of the owner, with proof of insolvency proceedings.

- Owners required by HDB to sell on grounds of policy violation.

- Inherited property — the holding period is reckoned from the original purchase by the deceased, not the date of inheritance.

- Property transferred between spouses as part of a court-ordered division on divorce, in some cases.

Standard life events — relocation overseas for work, family expansion, or financial difficulty — are not grounds for SSD remission. The tax applies even if the seller is selling at a loss.

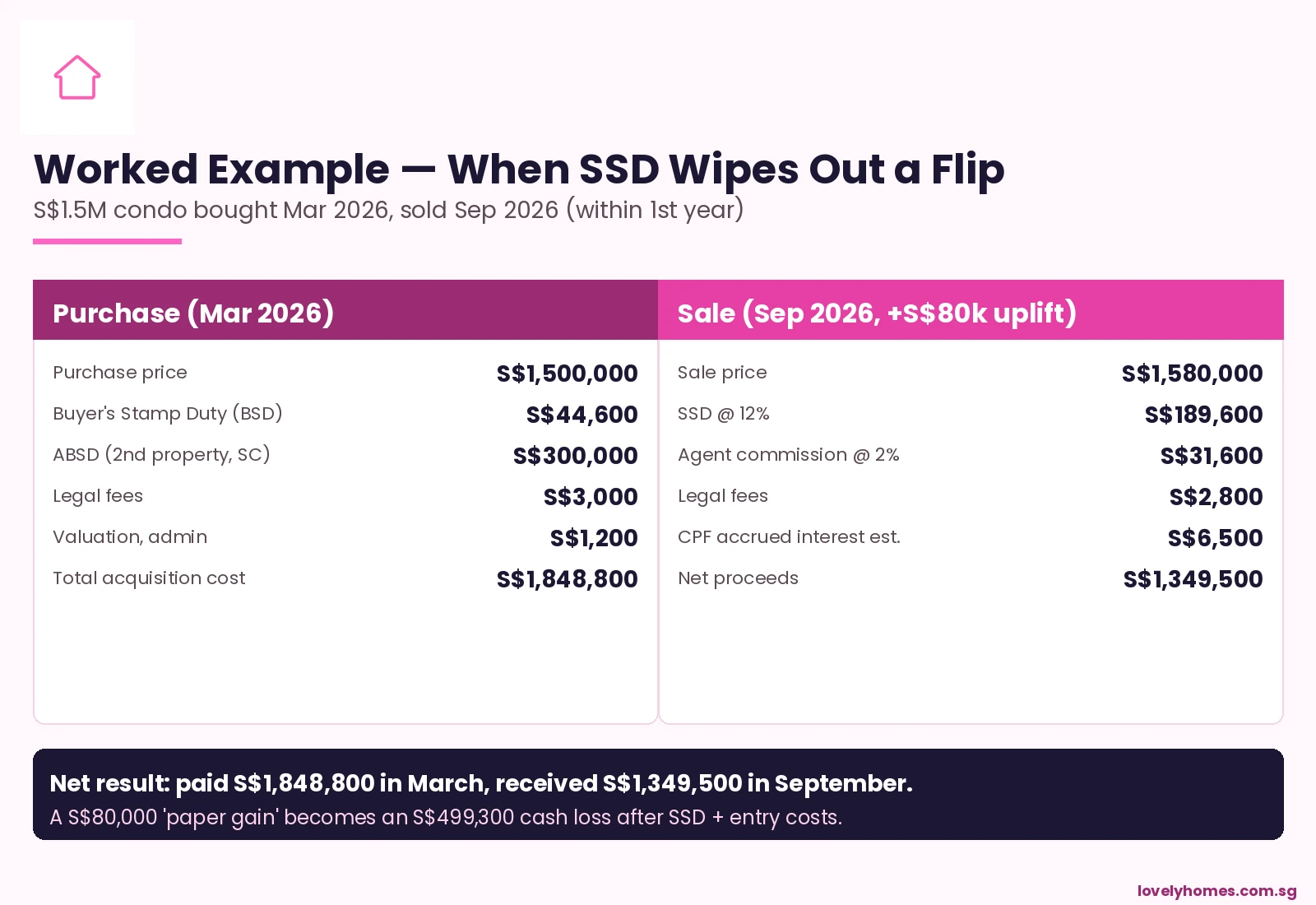

Worked Example — A S$1.5M Condo Flipped in 6 Months

Imagine a Singapore Citizen who buys a S$1.5M private condo as a second property in March 2026, then receives a job offer in Hong Kong six months later and decides to sell at S$1.58M (a S$80,000 paper gain). Here is what the maths actually looks like:

Acquisition costs (BSD, ABSD on the second property at 20%, legal fees) total S$348,800. The owner has paid S$1,848,800 to take possession. Six months later, the sale at S$1,580,000 attracts SSD at 12% (S$189,600), broker commission, legal fees, and CPF accrued interest. Net proceeds: S$1,349,500. Cash loss: S$499,300.

The lesson is brutal: SSD is designed to make short-term residential property sales economically unattractive even when the underlying market has moved up. For most second-property buyers, the only way to make the maths work is to stay invested for at least three years.

Strategies Sellers Actually Use

If you find yourself needing to sell within the SSD window, there are a small number of strategies practitioners commonly consider:

1. Run the holding-period calendar to the day

Conveyancers often time the OTP issue and exercise so that the sale falls just outside the next rate band. Selling on day 365 versus day 367 of the second year can mean a four-percentage-point swing on the sale price.

2. Rent out instead of selling

If holding-period maths do not work, leasing the unit until SSD falls to zero can preserve value. Singapore rental yields on private condos run 3.0–3.8% gross in 2026, which often covers the carrying cost of the mortgage during the wait.

3. Decoupling within marriage

Where one spouse needs to free up ABSD allowance for a future purchase, transferring a property between spouses (a Part-Disposal arrangement) may attract SSD on the transferred share. Practitioners check carefully whether the holding clock survives the transfer.

4. Swap residential for commercial

Commercial property (offices, shops) is not subject to SSD. Investors with a short horizon sometimes pivot from residential plays to commercial plays specifically to avoid the SSD window. Commercial does carry GST, however, so the trade-off is real.

SSD on HDB — Yes, Technically — But MOP Comes First

Strictly, SSD does not apply to HDB flats sold during the SSD window because the HDB Minimum Occupation Period (MOP) usually prevents resale within five years anyway. The rare exceptions — flats sold under HDB’s compulsory-sale rules, or flats where MOP has been waived by HDB — are also exempt from SSD.

For practical purposes, most HDB sellers should treat MOP as the binding constraint and ignore SSD entirely.

SSD on Industrial Property — A Different (Shorter) Ladder

SSD on industrial property uses a separate, shorter ladder introduced in January 2013: 15% within the first year, 10% in the second year, 5% in the third year, and 0% thereafter — harsher in headline terms but with the same three-year horizon. Commercial property (offices, shops, hotels) attracts no SSD at all.

What This Means for You as a Buyer in 2026

The 2026 environment makes the holding-period calculus even more important. With ABSD at 20% on the second property for Singapore Citizens and 60% for foreigners, entry costs are already punishing. Adding a 12% SSD on a quick exit means roughly one-third of an investment property’s purchase price is consumed by transaction taxes if the holding period is mismanaged.

For buyer-occupiers, the practical advice is unchanged: buy what you can hold through three full years and a typical Singapore property cycle (roughly 7 to 10 years). For investors, the calculus is whether the projected three-to-five-year capital appreciation comfortably exceeds the entry-cost stack — not just SSD but BSD, ABSD, conveyancing, agent commission, and CPF accrued interest combined.

Frequently Asked Questions

Does SSD apply if I bought before 11 March 2017?

Yes, but at the older rate ladder applicable on the date of acquisition. Properties bought between 14 January 2011 and 10 March 2017 use the four-year, 16% / 12% / 8% / 4% ladder. Properties bought between 20 February 2010 and 13 January 2011 use a three-year, 3% / 2% / 1% ladder. IRAS publishes the historical rate tables for cross-reference.

Is SSD payable on the sale of a property at a loss?

Yes. SSD is calculated on the higher of the contracted sale price or the assessed market value, regardless of whether the seller realised a profit or loss on the transaction. Loss-making short-term sales remain fully taxable.

How is SSD different from ABSD?

ABSD (Additional Buyer’s Stamp Duty) is paid by the buyer at purchase based on residency status and number of properties already owned. SSD (Seller’s Stamp Duty) is paid by the seller at sale based on how long the property was held. They are independent taxes and can both apply to the same transaction at different ends.

What if I co-own a property with my spouse and only my spouse’s share is sold (decoupling)?

SSD applies to the share being transferred, calculated on the value of that share. The holding period for the transferred share is reckoned from the original date of acquisition. Conveyancers will typically structure the transfer documentation so that SSD exposure is calculated correctly for the share at issue.

Can I deduct SSD against my income tax?

No. SSD is a transaction tax, not a deductible business expense for an individual seller. Property held by a corporate vehicle may treat SSD differently — consult a Singapore tax adviser for any company-held holding.

Does SSD apply to gifts or transfers within the family?

Generally yes, where the transfer is treated as a sale at market value. There are limited remissions for transfers between spouses incident to divorce or for inherited property where the holding period is reckoned from the deceased’s original acquisition. Always verify with IRAS directly for non-arm’s-length transfers.

When exactly is SSD due?

SSD must be paid within 14 days of the contract for sale — that is, the date the buyer exercises the OTP or signs the S&P. Late payment attracts penalty interest of 5% on the unpaid duty per annum, plus possible additional charges. The seller’s conveyancer typically pays SSD out of the sale proceeds at completion.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Decoupling for Married Couples Singapore 2026

- Foreign Buyer Guide Singapore 2026

- How to Sell Your Property in Singapore 2026

- Mortgage Refinancing in Singapore 2026

- Singapore Property Cooling Measures Timeline 2009–2026

Disclaimer

This article is intended as general information about Seller’s Stamp Duty in Singapore as at May 2026 and does not constitute tax, legal, or financial advice. Rates, exemptions, and procedures are set by the Inland Revenue Authority of Singapore and may be amended at any time without notice. For authoritative figures, refer to IRAS, the Housing & Development Board, the Monetary Authority of Singapore, the Urban Redevelopment Authority, and CPF Board for related procedures. For transactions of any size, engage a licensed Singapore conveyancing solicitor and, if relevant, a chartered accountant or tax practitioner before signing an OTP or S&P.