Singapore Property Agent Guide 2026: CEA Rules, Commissions and Your Rights Explained

- All estate agents and salespersons in Singapore must be registered with the Council for Estate Agencies (CEA), established under the Estate Agents Act 2010.

- There are no statutory commission rates in Singapore — fees are market-driven and fully negotiable between client and agent.

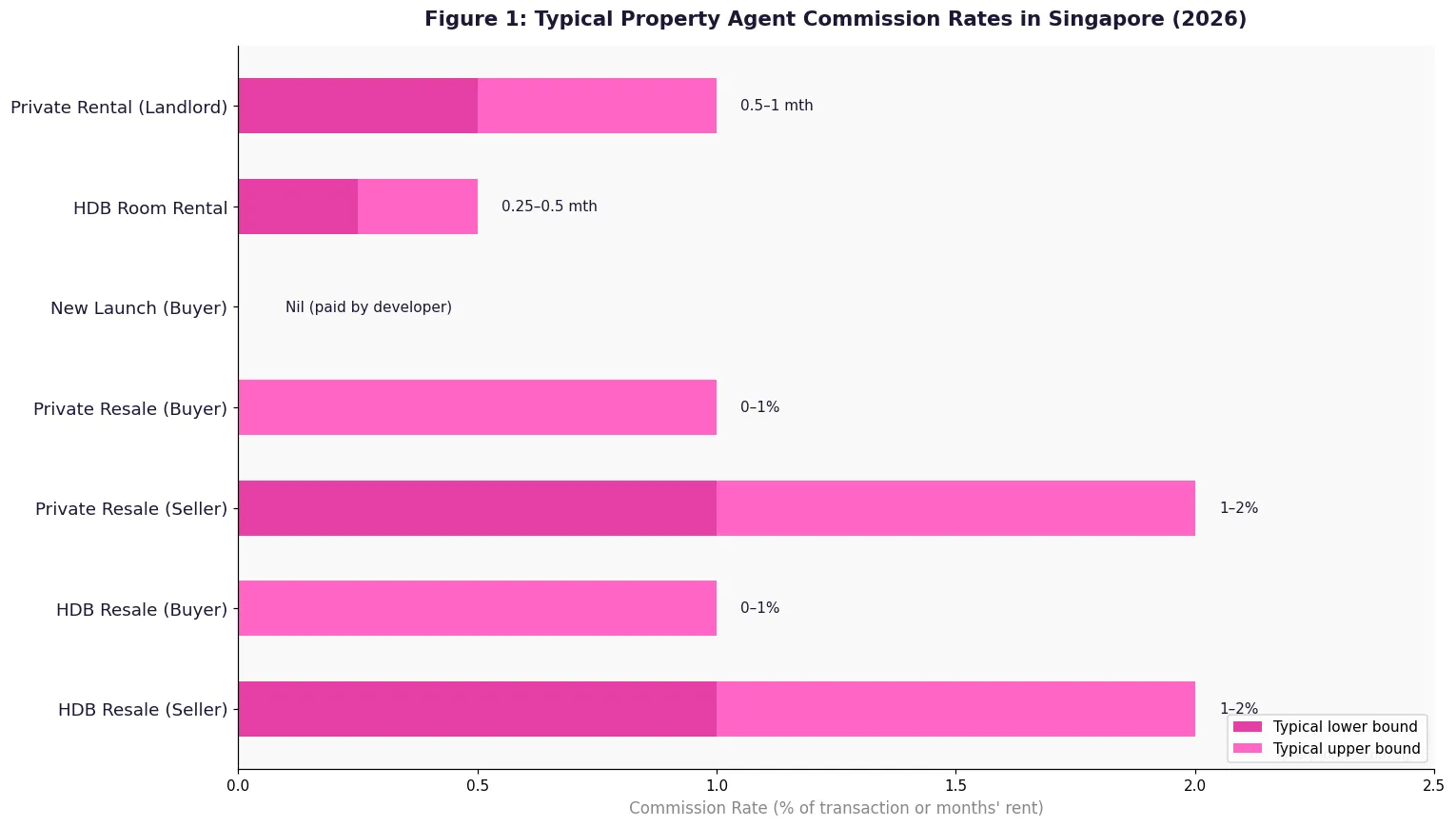

- Typical seller-side commissions run 1–2% of the transaction price; buyer-side commissions are typically 0–1%; rental landlord fees are 0.5–1 month’s rent.

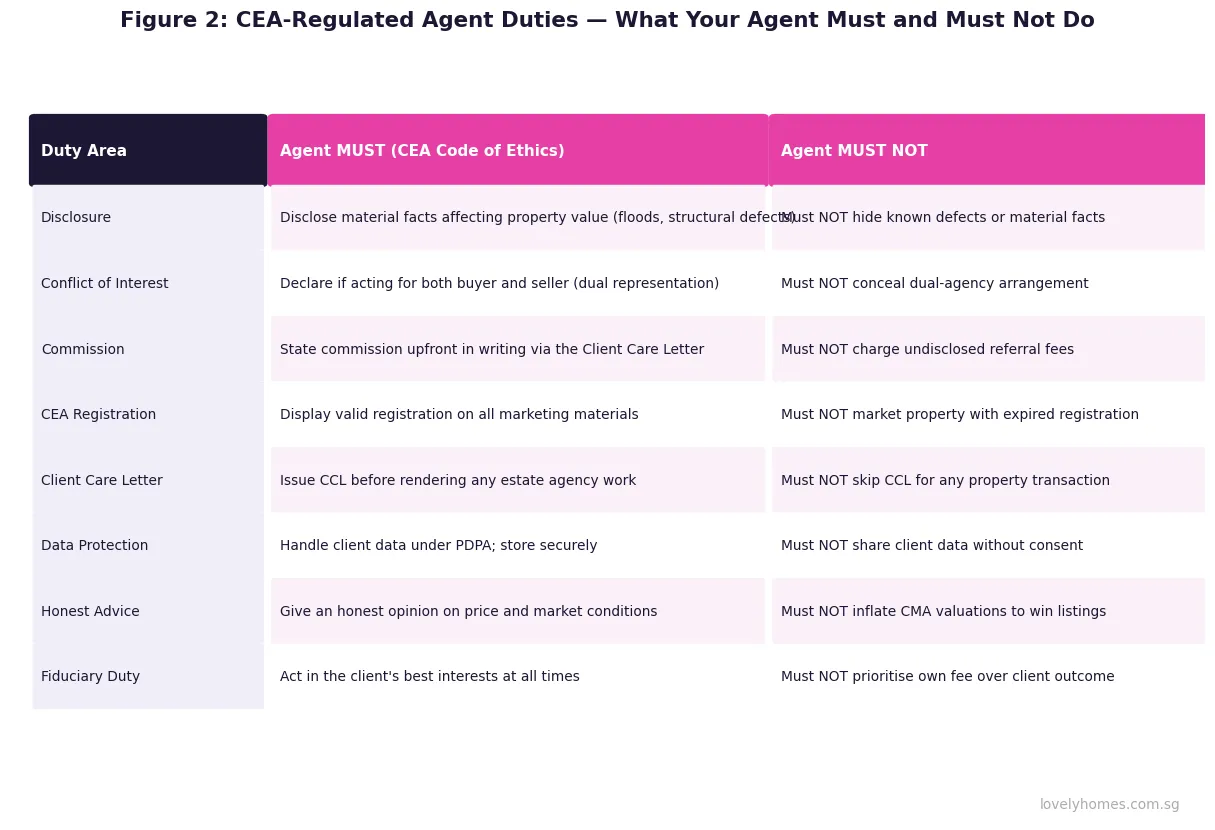

- Your agent must issue you a Client Care Letter (CCL) before performing any estate agency work — this is a CEA regulatory requirement.

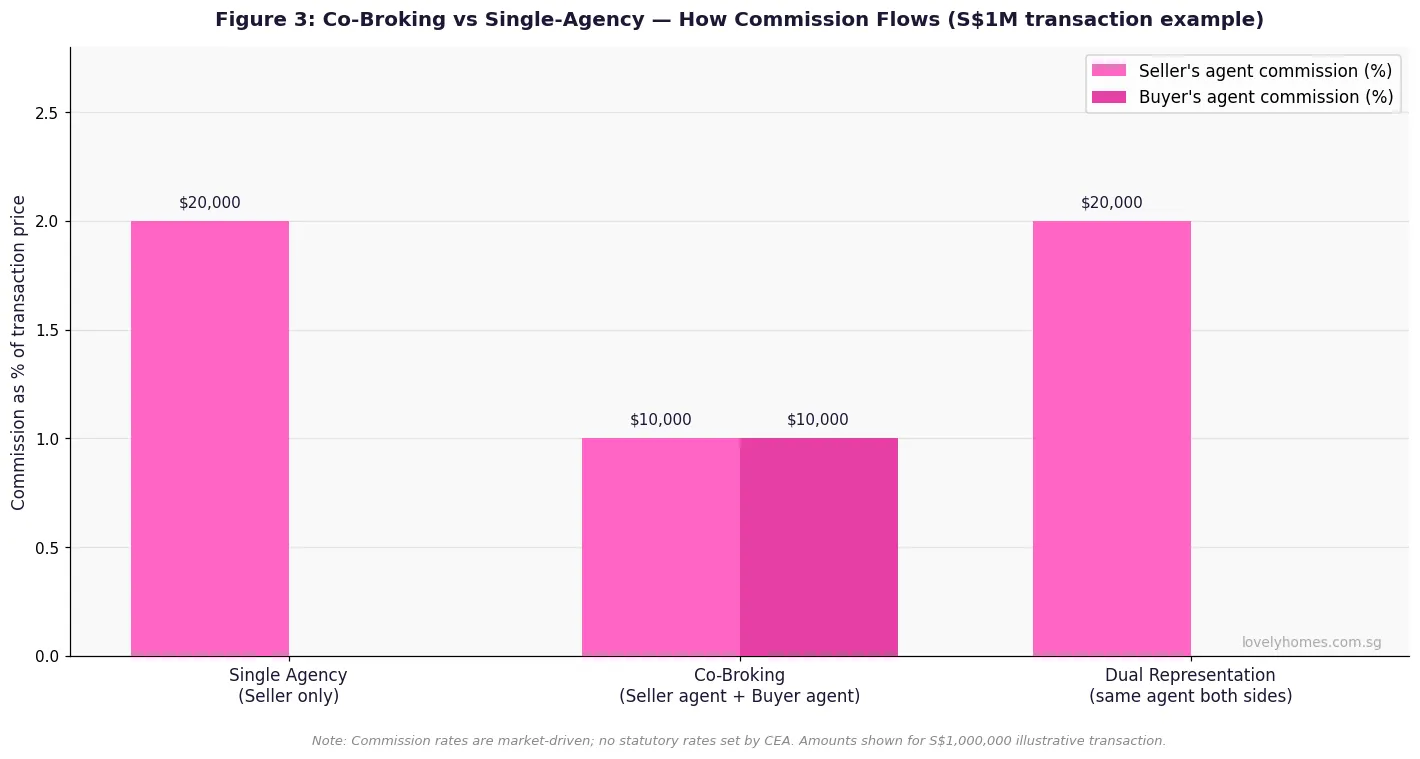

- In a co-broking arrangement, your agent and the other party’s agent each represent their own client; a dual-representation arrangement (one agent acting for both) is permitted but must be disclosed in writing.

- You can verify any agent’s registration, track record, and disciplinary history on the CEA Public Register at cea.gov.sg/public-register.

- Agents must declare all material facts affecting value, disclose any conflict of interest, and may not receive undisclosed referral fees or kick-backs.

- A complaint against an agent can be lodged with the CEA; sanctions range from financial penalties to suspension or revocation of registration.

What Is a Property Agent in Singapore — and Who Regulates Them?

A property agent in Singapore is a licensed professional who facilitates the sale, purchase, or rental of residential and commercial real estate on behalf of clients. The industry is regulated by the Council for Estate Agencies (CEA), a statutory board under the Ministry of National Development, established by the Estate Agents Act 2010.

Before the CEA’s formation, the property agency industry operated with minimal oversight, leading to consumer complaints about misleading advice, undisclosed commissions, and conflicts of interest. The CEA fundamentally restructured the profession: today, every estate agency must hold a valid estate agent licence, and every individual salesperson must hold a real estate salesperson (RES) registration. Operating without these credentials is a criminal offence.

Understanding how the CEA framework works — and what your agent is legally required to do and prohibited from doing — puts you in a far stronger position when buying, selling, or renting property in Singapore.

CEA Registration: Licences, RES Certificates and the Public Register

The CEA maintains a two-tier registration system. At the agency level, an estate agency licence is required — this is the firm through which salespersons operate. At the individual level, every salesperson must hold a current RES registration, which requires passing the two-part RES examination administered by the Singapore Institute of Estate Agents (SREA) or the CEA-approved course providers, and completing continuing professional development (CPD) hours each year to renew.

The CEA Public Register is the most important tool for consumers. It is free, publicly accessible at cea.gov.sg/public-register, and allows any member of the public to:

- Confirm a salesperson’s registration status (active, suspended, or lapsed).

- View the agency the salesperson is affiliated with.

- Check whether any disciplinary actions or court orders have been taken against the individual.

- Verify the estate agency’s licence number and status.

Before engaging any property agent, run their name and the agency name through the Public Register. An agent who hesitates to provide their registration number is a red flag.

CEA Licence and Registration at a Glance

| Item | Estate Agency (Firm) | Salesperson (Individual) |

|---|---|---|

| Credential Required | Estate Agent Licence | RES Registration |

| Issued By | Council for Estate Agencies (CEA) | Council for Estate Agencies (CEA) |

| Prerequisite | Key Executive Officer (KEO) with RES + 3 yrs experience | RES examination (2 papers) + background check |

| Renewal | Annual | Annual (with CPD requirement) |

| Public Verification | CEA Public Register | CEA Public Register |

| Disciplinary Body | CEA Disciplinary Committee | CEA Disciplinary Committee |

| Offence (Unregistered) | Fine up to S$100,000 and/or imprisonment | Fine up to S$75,000 and/or imprisonment |

The Client Care Letter (CCL): Your Most Important Document

The Client Care Letter is a mandatory document that every CEA-registered salesperson must issue to a client before rendering any estate agency service. Think of it as the formal engagement agreement between you and your agent. The CCL must specify:

- The scope of estate agency work to be performed.

- The commission rate or fee, and who pays it.

- Whether the agent will be representing you only, the other party only, or both parties (dual representation).

- The duration of the exclusive or non-exclusive engagement (if applicable).

- The agent’s and agency’s CEA registration numbers.

The CCL exists to protect consumers. If you have signed a CCL, you have a documented record of the agreed terms — and the agent is legally bound by it. Never sign anything or pay any fee before receiving and reviewing the CCL. Any agent who asks you to pay a commission before issuing a CCL is in breach of the CEA Code of Ethics.

Agent Commission in Singapore: How It Works and What You Should Expect to Pay

Singapore has no statutory commission rates — the CEA does not set minimum or maximum fees. This means all commission is negotiable between the client and the agent. In practice, market norms have emerged that give buyers and sellers a clear benchmark.

For private residential resale transactions, the seller’s agent typically earns 1–2% of the sale price, paid by the seller. The buyer’s agent, if engaged, typically earns 0–1%, often paid by the seller as a co-broking fee or by the buyer directly. For HDB resale, the same broad range applies, though some agents charge a fixed fee for lower-priced flats.

For new launch condominiums, the developer pays all agent commissions — buyers typically pay nothing to their agent, though the cost is arguably baked into the launch price. Developers usually pay 2–4% of the purchase price to the selling agency.

For rental transactions, the landlord’s agent typically receives 0.5–1 month’s gross rent per year of tenancy; the tenant’s agent (if engaged separately) may charge the tenant 0.25–0.5 months as well. For room rentals, the commission is typically 0.25–0.5 months.

When negotiating commission, remember that a lower rate does not always mean better value. An experienced agent with a strong track record of achieving above-market prices may deliver a higher net outcome even after a 2% fee than a lower-cost option who settles at asking price.

Co-Broking vs Dual Representation: What Every Buyer and Seller Must Understand

Two structural arrangements govern how agents interact in a Singapore property transaction:

Co-broking is the standard arrangement in which the seller’s agent and the buyer’s agent each represent their own client and split the commission. The seller’s agent acts solely in the seller’s interest; the buyer’s agent acts solely in the buyer’s interest. This is generally the arrangement that offers the strongest protection to both parties, as each has an advocate.

Dual representation occurs when a single salesperson (or two salespersons from the same estate agency) acts for both buyer and seller in the same transaction. This creates an inherent conflict of interest — the same agent cannot truly maximise the price for the seller whilst simultaneously minimising it for the buyer. Under CEA rules, dual representation is permitted but comes with strict disclosure obligations: the agent must obtain written consent from both parties, issue a separate CCL to each, and make clear that they are not acting exclusively for either side.

If you are a buyer and your agent is also acting for the seller, you should understand that their advice on pricing, negotiation, and terms may not be in your exclusive interest. You have the right to engage a separate buyer’s agent, though you may then be responsible for their fee.

Worked Example: Buying a S$1.35M D15 Resale Condo — Agent Fees from Both Sides

Mr and Mrs Chen are Singaporean citizens buying a three-bedroom resale condominium in District 15 (East Coast/Katong) for S$1,350,000. The seller is represented by Agent A (from Agency X). The Chens engage Agent B (from Agency Y) as their dedicated buyer’s agent. This is a co-broking arrangement.

Seller’s side: The seller has agreed to pay Agent A a commission of 2% of the sale price = S$27,000. The seller also agrees to pay a co-broking fee to Agent B of 1% = S$13,500. Total commission borne by the seller: S$40,500 (3%).

Buyer’s side: The Chens pay Agent B nothing directly — their agent’s co-broking fee is borne by the seller. However, the Chens should note that had the seller not agreed to co-broke, they would have needed to either pay Agent B themselves or negotiate the seller’s agent into a lower price to compensate.

HDB sale scenario: If the Chens had been buying an HDB resale flat at S$680,000 instead, and engaged a buyer’s agent, the seller would typically pay the seller’s agent 2% (S$13,600) whilst the buyer’s agent may charge the Chens 1% (S$6,800) payable by the buyer. Total transaction cost differs significantly from the private market.

Key takeaway: Always clarify upfront, in writing via the CCL, who pays what before agreeing to engage any agent. Ask whether the seller is paying co-broking and at what rate, and whether your agent has any other financial relationships with the other party or agency.

How the CEA Handles Agent Misconduct: The Complaint and Disciplinary Process

The CEA takes a structured approach to consumer complaints. If you believe an agent has breached the Code of Ethics, the Estate Agents Act, or any CEA circular, you can file a complaint via the CEA’s online portal at cea.gov.sg. The CEA investigates and may refer the matter to its Disciplinary Committee (DC).

Sanctions available to the DC range from written warnings and financial penalties up to S$75,000 (individual) or S$100,000 (agency), through to suspension or permanent revocation of registration. In serious cases, criminal prosecution under the Estate Agents Act is possible. All disciplinary decisions are published in the CEA’s enforcement reports and reflected on the Public Register.

Common grounds for complaints include: failure to issue a CCL, misrepresentation of property condition or price, unauthorised receipt of referral fees, failure to disclose dual representation, and staging or fabricating viewings. The CEA’s Code of Ethics and Professional Client Care sets out in detail the full range of obligations.

Why Understanding CEA Rules Protects Your Largest Financial Transaction

Property transactions in Singapore typically represent the single largest financial commitment a household will ever make. A S$1.5M condo purchase involves not only the purchase price but Buyer’s Stamp Duty, possible ABSD, legal fees, mortgage costs, and ongoing maintenance — easily totalling S$1.8M in lifetime costs. In this context, the role of an agent who genuinely acts in your interest (rather than their own) is material.

The CEA framework, while broadly effective, cannot eliminate every conflict of interest or guarantee the quality of every agent. Singapore’s property market is large enough that the range of agent quality is wide. Understanding the rules — particularly dual representation, the CCL requirement, and the Public Register — gives consumers the tools to select wisely and hold agents accountable.

By comparison, markets like Hong Kong (RICS, EAAB) and Australia (state-based licensing) operate similar registration frameworks but typically have higher regulatory barriers to entry and stronger mandatory insurance requirements. Singapore’s framework is robust but continues to evolve: the CEA has periodically tightened CPD requirements and is exploring strengthened buyer-protection measures.

What Might Come Next for CEA Regulation in Singapore

The CEA has signalled ongoing interest in strengthening consumer protection in the estate agency industry. Areas that industry observers expect to be addressed in coming years include: mandatory professional indemnity insurance for individual salespersons (currently required at agency level only), further tightening of dual-representation rules in light of rising transaction complexity, and the potential introduction of a consumer redress fund analogous to those found in insurance and financial advisory sectors. The CEA has also moved toward digitising the CCL process, with a view to making client care documentation more standardised and harder to circumvent.

Frequently Asked Questions

Do I need a buyer’s agent when buying a new launch condo in Singapore?

You do not need to engage your own agent for a new launch purchase — but it costs you nothing to do so, because the developer pays all salesperson commissions (typically 2–4%). Having your own agent means someone is documenting your interest, helping you compare units and price points, and flagging any unusual contractual terms in the Sale and Purchase Agreement. Since you bear no direct cost, the main question is simply whether you trust the developer’s show-suite agent to advise you impartially — they are paid by the developer, not you.

Can I negotiate agent commission on an HDB resale transaction?

Yes, absolutely. There are no statutory rates, and HDB commission is fully negotiable. It is perfectly reasonable to ask for a fixed fee rather than a percentage, particularly for lower-priced flats where a 2% rate results in a disproportionately small workload versus income. Some sellers offer 1.5% for exclusive listings; some buyers’ agents will work for 0.5% co-broking fees. What matters is that the agreed rate is documented in the CCL before any work begins.

What should I do if my agent is not issuing a CCL?

Decline to proceed until the CCL is issued. A salesperson who skips the CCL is in breach of CEA regulations, and you have no documented protection of your agreed terms. If an agent refuses to issue a CCL or insists it is unnecessary, report the matter to the CEA. You can also lodge a complaint after the fact if the agent collected a fee without issuing a CCL. Keep records of all communications, including WhatsApp messages, emails, and any invoices.

What is the difference between exclusive and non-exclusive agency?

An exclusive agency agreement means only the agent you engage can market and transact the property for the agreed period (typically one to three months). You cannot list with other agents during this time. An exclusive arrangement usually motivates the agent to invest more in marketing (professional photos, video walkthroughs, portal placement). A non-exclusive agreement allows you to list with multiple agents simultaneously. The risk is that agents may not invest heavily when competing for the same transaction. Whichever you choose, the exclusivity terms must be clearly stated in the CCL.

Can a Singapore property agent represent a buyer and seller in the same deal?

Yes, but with strict conditions. Under the CEA framework, dual representation is permitted if: (a) the agent discloses the dual representation to both parties in writing before proceeding; (b) both parties provide written consent; and (c) the agent issues a separate CCL to each party. Practically, this situation most commonly arises when a buyer contacts the seller’s listing agent directly without engaging their own agent. Whether to accept dual representation is your choice — you are entitled to insist on having your own agent even if that means bearing the buyer’s agent fee yourself.

How do I file a complaint against a property agent in Singapore?

Visit cea.gov.sg and navigate to the complaint submission portal. You will need the agent’s registration number (verifiable via the Public Register), a description of the alleged breach, and supporting documentation (CCL, email or chat logs, receipts). The CEA investigates and can issue warnings, fines, suspension, or revocation. There is no fee to file a complaint. For disputes over commission or contract terms where no CEA breach is alleged, the Small Claims Tribunal or civil courts are the appropriate avenue.

Does GST apply to agent commission in Singapore?

It depends on whether the estate agency is GST-registered. Large agencies with annual turnover exceeding S$1 million are required to be GST-registered, in which case their commission invoices will include 9% GST (the current rate as of 2026) on top of the agreed commission. Smaller agencies or individual salespersons below the S$1M threshold may not charge GST. Always check the CCL for whether quoted commission rates are inclusive or exclusive of GST, as this affects your total cost materially on high-value transactions.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Property Conveyancing Guide 2026: Step-by-Step from OTP to Keys

- Singapore Property Cooling Measures Guide 2026: ABSD, TDSR, LTV and SSD Explained

- Singapore Property Agent Commission Guide 2026: What You Actually Pay

- Singapore First-Time Buyer Guide 2026: HDB, Resale or New Launch?

- Singapore New Launch Condo Buying Guide 2026

Disclaimer

This article is intended for general information purposes only and does not constitute legal, financial, or professional advice. Property transactions in Singapore involve complex legal and financial considerations. Commission rates, CEA regulations, and other details described in this article are accurate to the best of our knowledge as at June 2026 but may change. Readers should consult a CEA-registered property agent, a licensed conveyancing solicitor, and where relevant a licensed financial adviser before making any property-related decisions. Official information on CEA registration and the Code of Ethics is available at cea.gov.sg. Stamp duty information is available at iras.gov.sg. HDB loan and eligibility information is available at hdb.gov.sg.