HDB BTO October 2026 Guide: All 7 Projects, Prices, Grants and Application Tips for Bedok Bayshore, Toa Payoh Caldecott, Yishun, Tengah and More

Quick Answer: HDB BTO October 2026 Key Facts

- Total supply: approximately 7,970 flats across 7 projects in 6 towns.

- Towns: Bedok (Bayshore ×2), Toa Payoh (Caldecott), Geylang (Mattar), Yishun (Chencharu), Tengah (Garden Avenue), Sembawang North.

- Classification: Bedok Bayshore (Prime), Toa Payoh Caldecott (Prime), Geylang Mattar (Plus), Yishun/Tengah/Sembawang (Standard).

- HFE letter deadline: Submit all supporting documents to HDB by 15 September 2026 to ensure your HDB Flat Eligibility (HFE) letter is ready for the October sales exercise.

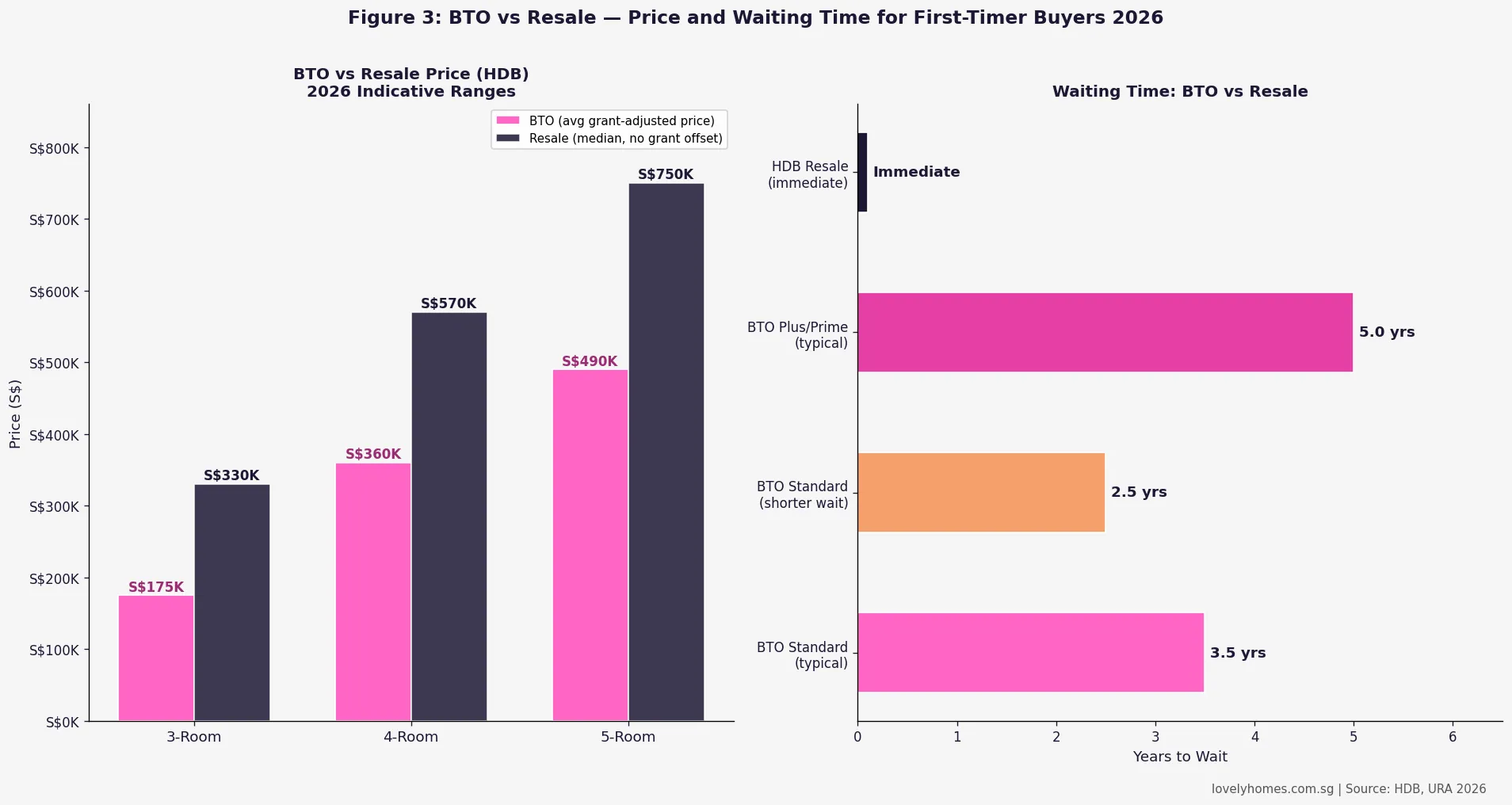

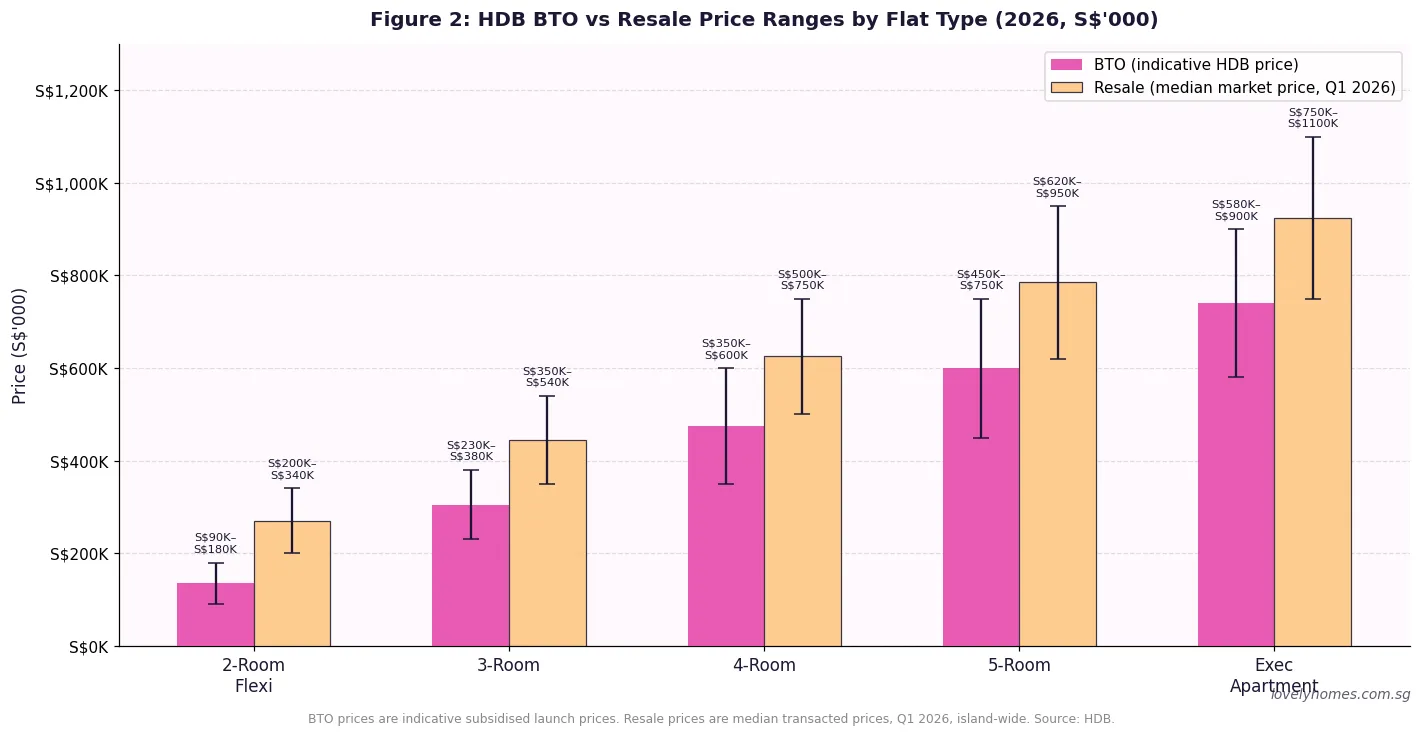

- Estimated 4-room prices: Standard (Yishun/Tengah) ~S$360K–S$400K; Plus (Geylang) ~S$500K–S$540K; Prime (Bedok/Toa Payoh) ~S$500K–S$555K.

- MOP: 5 years for Standard; 10 years for Plus and Prime classifications.

- Subsidy clawback: Plus and Prime flats are subject to a subsidy clawback on resale, calculated as a percentage of the resale price or value.

- Hottest picks: Toa Payoh Caldecott (only Prime project; next to Caldecott MRT interchange); Bedok Bayshore (waterfront precinct; near East Coast Park).

Overview: Singapore’s Final BTO Launch of 2026

The October 2026 Build-To-Order (BTO) exercise is the final sales launch of the year and one of the largest in recent memory, with the Housing and Development Board (HDB) offering approximately 7,970 flats across seven projects in six towns. The October exercise completes the government’s 2026 BTO calendar, which has collectively offered around 19,600 new flats — matching HDB’s earlier public commitment to sustain high supply to moderate resale prices and address first-timer demand.

The exercise is notable for the geographic spread of its projects: it spans the sought-after east (Bedok’s new Bayshore waterfront precinct), the central region (Toa Payoh’s Caldecott precinct), an inner-city mixed area (Geylang’s Mattar neighbourhood near the Downtown Line), and the established growth corridors of Yishun and Tengah. For first-timer applicants who missed earlier launches, this is a high-stakes application exercise with a meaningful mix of price points and location quality.

Project-by-Project Analysis

Bedok — Bayshore I & II Prime

The two Bedok Bayshore projects together supply 2,500 flats (1,640 and 860 units respectively) in the new Bayshore housing estate along Bayshore Drive, adjacent to East Coast Park. Both are served by Bayshore MRT station on the Thomson-East Coast Line (TEL), which provides direct access to the CBD via Marina Bay. The Bayshore precinct is a purpose-built waterfront residential neighbourhood — the first HDB estate developed in this part of Singapore — and the BTO flats sit alongside private condominiums and commercial amenities in a mixed-use environment.

Both projects carry Prime classification under HDB’s 2023 flat classification framework, meaning buyers are subject to a ten-year Minimum Occupation Period (MOP) and a subsidy clawback on resale. Flat types span 2-room Flexi, 3-room, and 4-room, with no 5-room units offered — reflecting the Prime classification’s intent to maximise accessibility for first-timers rather than offer larger investment-grade units. Indicative 4-room pricing is estimated at approximately S$500,000–S$520,000.

Toa Payoh — Caldecott Prime

The Toa Payoh Caldecott project is expected to be the single most competitive project in October 2026. With 1,430 units — comprising around 590 two-room Flexi flats, 580 four-room flats, and a tranche of public rental units — it occupies land immediately adjacent to Caldecott MRT station, the interchange between the Circle Line (CCL) and the Downtown Line (DTL). This provides unparalleled MRT connectivity in a mature estate known for its proximity to Bishan, Ang Mo Kio, and Novena.

Caldecott is the only Pure Prime project in this exercise. Indicative 4-room prices are estimated to start from approximately S$550,000, reflecting the mature estate premium and the exceptional MRT interchange location. The ten-year MOP and subsidy clawback apply. Ballot competition is expected to be intense — the June 2026 Queenstown Prime project saw approximately 8× first-timer ballot rates for 4-room units, and Caldecott may approach similar demand.

Geylang — Mattar Plus

The Geylang Mattar project offers approximately 440 flats near Mattar MRT station on the Downtown Line (DTL3), within walking distance of MacPherson and the MacPherson estate. Geylang carries Plus classification — a ten-year MOP and subsidy clawback — reflecting its central location and good MRT connectivity without meeting the full Prime threshold. Flat types are expected to be 2-room Flexi and 4-room, with indicative 4-room pricing around S$500,000–S$540,000. The Geylang Mattar neighbourhood is undergoing gradual upgrading, and the BTO project sits in an area with established hawker centres, schools, and neighbourhood commercial facilities.

Yishun — Chencharu Standard

The Yishun Chencharu project is the largest single project in the October 2026 exercise at 1,580 units. Flat types run the full range — 390 two-room Flexi, 80 three-room, 460 four-room, and 650 five-room units — making it the most options-rich project for buyers seeking larger flat types at Standard pricing. Chencharu is the fifth BTO project launched in this new Yishun sub-precinct, which HDB is systematically building out on the former Chencharu estate lands near Khatib MRT station. Standard classification means a five-year MOP and no subsidy clawback. Indicative 4-room prices are estimated around S$360,000–S$400,000 — among the most affordable in this exercise.

Tengah — Garden Avenue Standard

Tengah Garden Avenue continues the ongoing build-out of Tengah New Town, the first car-lite eco-town in Singapore’s western corridor. The project is expected to offer approximately 620 units with 3-room, 4-room, and 5-room flat types. Tengah’s future MRT stations on the Jurong Regional Line (JRL) are under construction; the nearest current public transport option is bus connectivity to Bukit Gombak and Bukit Batok MRT stations. Standard classification applies; indicative 4-room prices are approximately S$360,000–S$380,000. Tengah’s car-free town centre design and green corridors are a lifestyle draw for buyers who prioritise environment over MRT proximity.

Sembawang — North Standard

The Sembawang North project adds approximately 400 units in the northern growth corridor, near Canberra MRT on the North-South Line. Flat types are expected to include 2-room Flexi, 3-room, 4-room, and 5-room options. Standard classification; indicative 4-room prices around S$320,000–S$360,000 — the most affordable in this exercise. Sembawang has seen a consistent stream of BTO launches in recent years as HDB continues to develop the Sembawang New Town precinct. The area is served by Canberra Plaza (opened 2020), Sembawang Shopping Centre, and a growing number of amenities. Bus connectivity is the primary mode of access to the town centre from the BTO site.

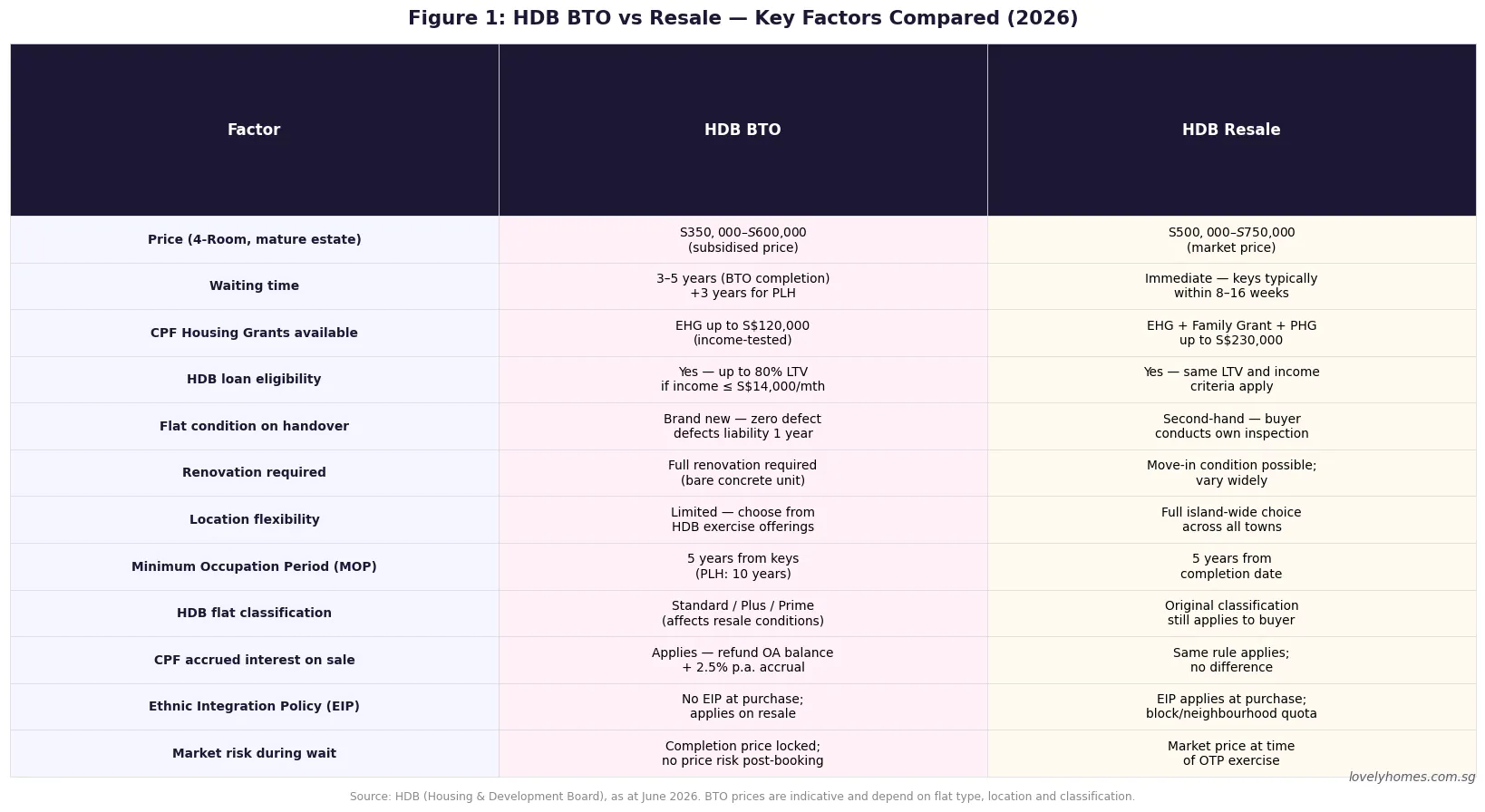

BTO Flat Classification — Standard, Plus and Prime in October 2026

The October 2026 exercise marks the third full year under HDB’s revised flat classification framework (Standard / Plus / Prime), which replaced the former Open Market / Prime Location Housing (PLH) and Mature / Non-Mature estate designations. The classification is determined by HDB based on locational advantage, transport connectivity, and proximity to the city centre:

| Feature | Standard | Plus | Prime |

|---|---|---|---|

| MOP | 5 years | 10 years | 10 years |

| Subsidy clawback on resale | None | Yes (% of resale price) | Yes (higher % of resale price) |

| Private property ownership during MOP | Not allowed | Not allowed | Not allowed |

| Eligible buyers | Usual HDB eligibility | Only first-timers (for 95% of units at launch) | Only first-timers (for 95% of units at launch) |

| Rental during MOP | With HDB approval after 3 yrs (rooms only) | Not allowed during MOP | Not allowed during MOP |

| October 2026 projects | Yishun, Tengah, Sembawang | Geylang Mattar | Bedok Bayshore, Toa Payoh Caldecott |

A critical implication of Plus and Prime classification is the subsidy clawback: when you resell a Plus or Prime flat after the ten-year MOP, HDB recovers a percentage of the gross resale price. This amount is not refunded to you — it is recovered by HDB as a repayment of the additional subsidy embedded in the below-market launch price. For buyers who plan to sell their flat after MOP to unlock equity, the subsidy clawback meaningfully reduces net sale proceeds.

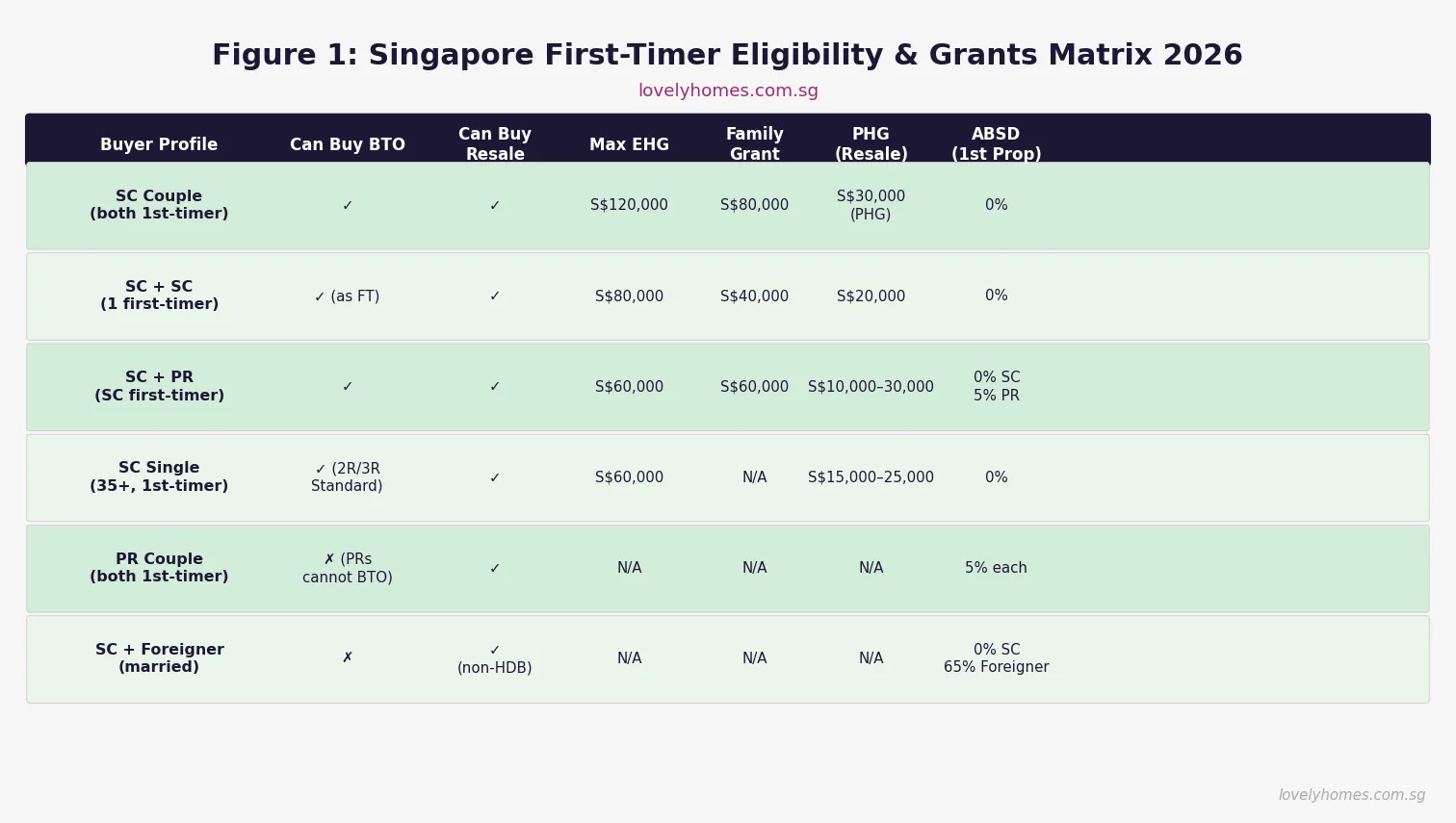

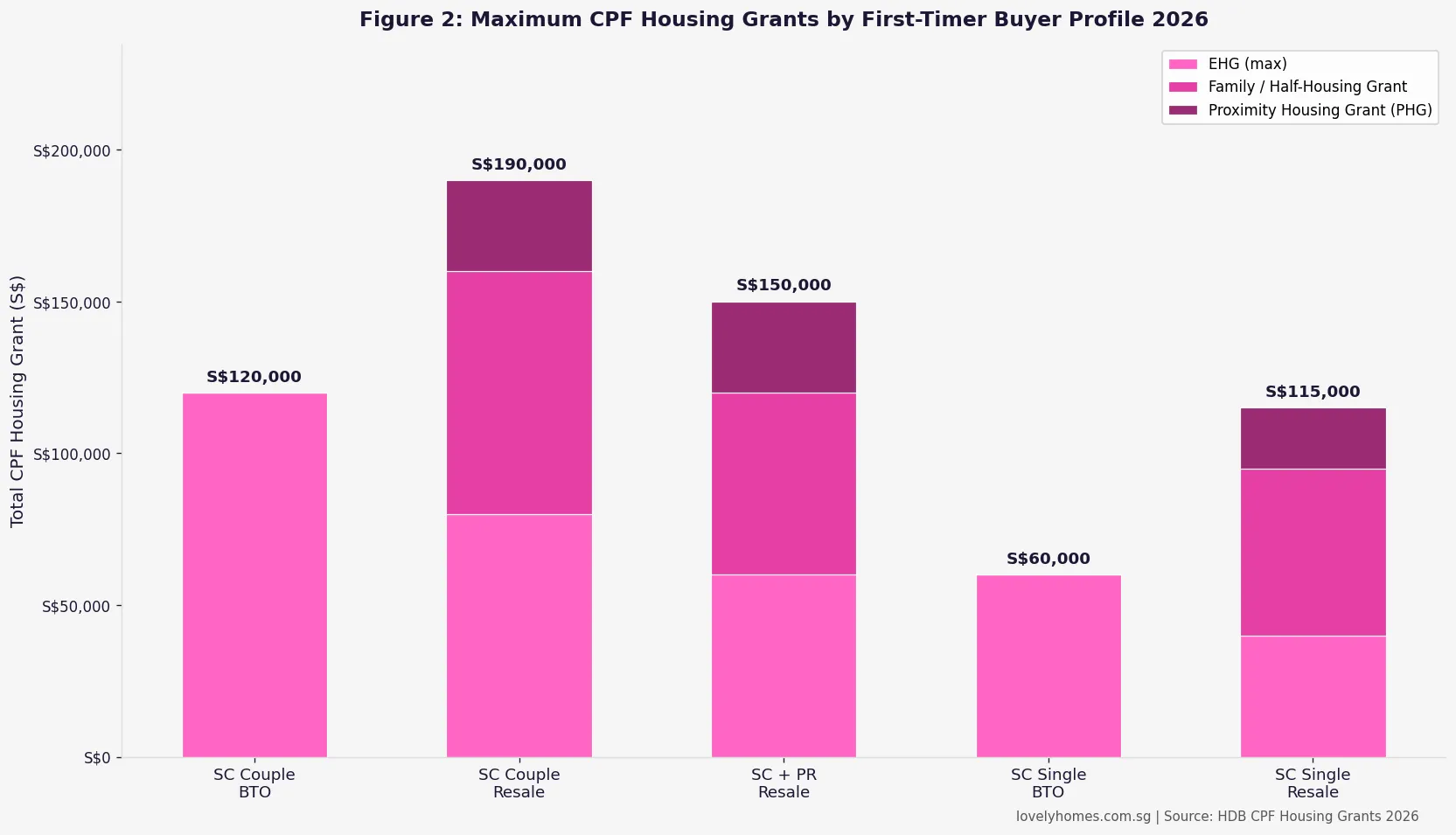

Grants — What First-Timers Can Receive in October 2026

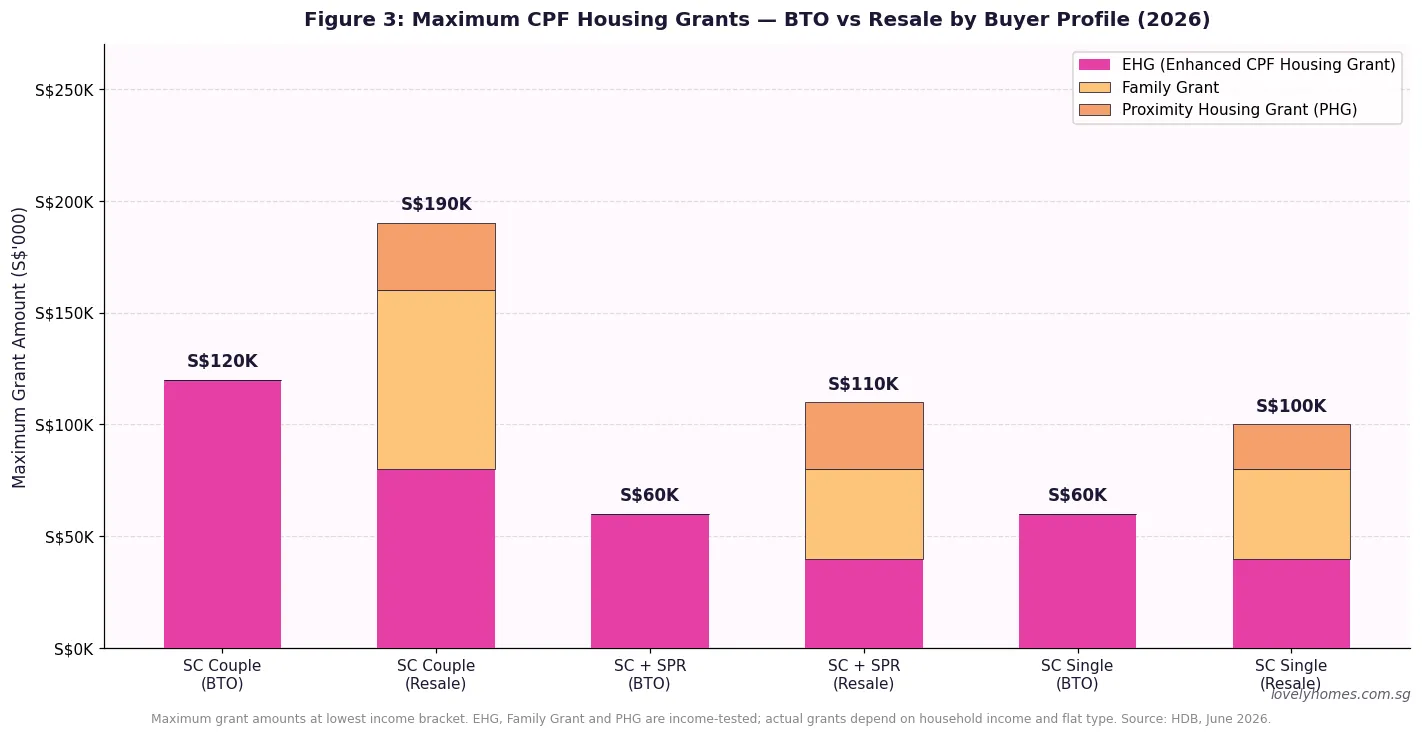

First-timer Singapore Citizen households applying for BTO flats may be eligible for the following CPF housing grants:

| Grant | Maximum Amount | Eligibility | Income Ceiling |

|---|---|---|---|

| Enhanced CPF Housing Grant (EHG) | S$80,000 (couple); S$40,000 (single) | First-timer SC couple or single; buying new or resale HDB | S$9,000/mth (couple); S$4,500/mth (single) |

| CPF Housing Grant — BTO | S$40,000 (SC couple); S$20,000 (single) | First-timer buying directly from HDB (BTO, SBF) | S$14,000/mth |

| Step-Up CPF Housing Grant | S$25,000 | Second-timer moving from 2-room to larger BTO in non-mature/Standard estate | S$7,000/mth |

| Proximity Housing Grant (Resale only) | S$30,000 (couple); S$20,000 (single) | Buying resale HDB within 4km of parents; does not apply to BTO | Not applicable for BTO |

For a qualifying SC first-timer couple with household income below S$9,000 per month, the maximum combined BTO grant (EHG + CPF Housing Grant) is S$120,000. This means a Yishun Standard 4-room BTO estimated at S$380,000 could effectively cost as little as S$260,000 after grants — making it among the most subsidised home-ownership options available in 2026.

How to Apply — Key Steps and Dates

The October 2026 BTO application process follows the standard HDB BTO application procedure:

1. Obtain a valid HDB Flat Eligibility (HFE) Letter. An HFE letter confirms your eligibility to buy an HDB flat, the loan amount you qualify for, and the grants you may receive. HFE letters are valid for six months. HDB recommends applying for the HFE letter early — submit all required documents by 15 September 2026 to ensure your letter is processed before the October application window opens. Apply via the HDB Flat Portal at homes.hdb.gov.sg.

2. Select your project and flat type. When the October 2026 sales exercise opens (HDB will announce the exact application window), log into the HDB Flat Portal, browse available projects, and submit your application for one project and flat type.

3. Ballot and queue number. HDB conducts a computer ballot. First-timer SC applicants receive priority balloting status (two ballot chances before being deemed a second-timer). Your queue number determines the order in which you book a flat. A lower queue number (closer to 1) means you have first pick of available units within your shortlisted flat type.

4. Flat selection and signing of Agreement for Lease (AFL). When called for flat selection, you choose a specific unit, pay the option fee (typically S$2,000), and subsequently sign the Agreement for Lease and pay the down payment (5% of flat price from cash/CPF, plus stamp duty).

5. Keys collection. BTO construction timelines typically run 3–5 years. For most projects in non-mature towns (Yishun, Tengah, Sembawang), expected completion is 2029–2031. For Prime projects in mature areas, timelines may be shorter given higher development priority, though HDB has not yet released official completion estimates for the October 2026 projects.

Worked Example: The Wong Family Apply for Yishun Chencharu 4-Room

Scenario

Mr and Mrs Wong, both Singapore Citizens aged 28, are first-time home buyers. Combined gross monthly income: S$7,500/mth. Both are applying for the Yishun Chencharu 4-room BTO in October 2026.

Grant eligibility:

- EHG (S$7,500/mth income → proportionate to income): approximately S$50,000

- CPF Housing Grant (BTO, SC couple): S$40,000

- Total grants: S$90,000

Estimated 4-room flat price: S$380,000

Effective price after grants: S$380,000 − S$90,000 = S$290,000

HDB Loan (90% LTV on post-grant price, subject to MSR):

- Maximum HDB loan: 80% of flat price = S$304,000 (before grants reduce the price quantum; HDB loan is on flat price, grants reduce initial outlay)

- Monthly instalment at HDB loan rate 2.6% p.a., 25 years on ~S$290,000: approximately S$1,320/mth

- MSR check: S$1,320 / S$7,500 = 17.6% — well within the 30% MSR cap — PASS

Cash outlay at sign of AFL: approximately S$3,200 (option fee S$2,000 + legal S$1,200)

BSD payable: S$290,000 × 1% = S$2,900 (paid from CPF OA)

Estimated waiting time: approximately 3.5–4 years; expected keys collection 2030–2031.

For this couple, the Yishun BTO is an exceptionally affordable path to home ownership — the effective post-grant cost of S$290,000 for a new 4-room flat in a growth precinct compares favourably to current HDB resale 4-room prices in Yishun (~S$420,000–S$490,000).

What Might Come Next — BTO Supply and Policy Outlook

The October 2026 exercise completes the government’s publicly stated 19,600-flat target for 2026. For 2027, HDB is expected to announce the BTO supply target in January — industry observers anticipate a maintained high supply of 18,000–22,000 units given continued strong first-timer demand. The government has signalled that BTO supply will remain elevated until the HFE application-to-first-timer-receipt wait time is consistently below four years for most non-Prime projects.

The longer-term supply story for October 2026 buyers is positive: Bedok Bayshore (TEL fully operational 2025), Toa Payoh Caldecott (Caldecott interchange operational), and Yishun Chencharu (fifth project in a maturing precinct) will all benefit from continued infrastructure investment and precinct maturation during the waiting period. Tengah buyers face a longer MRT wait — the Jurong Regional Line stations serving Tengah are not expected to open until 2028–2029 — but the car-free town centre design and cycling-focused layout are increasingly valued by younger buyers.

Summary: October 2026 BTO At-a-Glance

| Town | Project | Class | Units | MOP | Est. 4-Room | MRT |

|---|---|---|---|---|---|---|

| Bedok | Bayshore I | Prime | 1,640 | 10 yrs | ~S$510K | Bayshore (TEL) |

| Bedok | Bayshore II | Prime | 860 | 10 yrs | ~S$510K | Bayshore (TEL) |

| Toa Payoh | Caldecott | Prime | 1,430 | 10 yrs | ~S$555K | Caldecott (CCL+DTL) |

| Geylang | Mattar | Plus | ~440 | 10 yrs | ~S$520K | Mattar (DTL) |

| Yishun | Chencharu | Standard | 1,580 | 5 yrs | ~S$380K | Near Khatib (NSL) |

| Tengah | Garden Avenue | Standard | ~620 | 5 yrs | ~S$370K | Future JRL |

| Sembawang | North | Standard | ~400 | 5 yrs | ~S$340K | Canberra (NSL) |

| Total | ~7,970 | HFE deadline: 15 September 2026 | ||||

Frequently Asked Questions

What is the difference between Prime, Plus and Standard BTO flats in October 2026?

The classification reflects the locational advantage of each project and determines the restrictions placed on the flat. Prime flats (Bedok Bayshore, Toa Payoh Caldecott) carry a ten-year MOP, a subsidy clawback on resale, and a restriction on renting out the whole flat or any room during the MOP period. Plus flats (Geylang Mattar) have the same ten-year MOP and clawback, but the subsidy is calibrated as less than Prime. Standard flats (Yishun, Tengah, Sembawang) have a five-year MOP and no subsidy clawback — they behave like traditional BTO flats and can be resold on the open market at prevailing prices after the MOP. If you are buying primarily as a home rather than as an investment, the classification matters mainly for your lifestyle flexibility during MOP. If you intend to sell after five to seven years, Standard is strongly preferable.

Can I apply if I currently own a private property?

No. HDB BTO eligibility requires that you do not own a private residential property (in Singapore or overseas) at the time of application, and that you have not disposed of any private property within 30 months before the HDB flat application date. If you or your co-applicant own or recently sold a private property, you are ineligible to apply for a BTO flat. This 30-month wait-out period also applies if your private property is held through a company or other entities where you hold a significant interest. Check your eligibility carefully via the HDB Flat Eligibility portal before submitting an application.

What happens if my ballot number is beyond the available units — can I try again for free?

Yes. If you applied as a first-timer and your ballot number is beyond the available units (or you did not receive any ballot chance), you are considered to have made an unsuccessful attempt. Your first-timer priority status is not used up by simply not receiving a queue number low enough to select a flat. You retain your first-timer priority ballot chips for future exercises. However, if you receive a queue number and are called for flat selection but decline to select a flat, you lose one ballot chip and may be deemed a non-first-timer for subsequent exercises. HDB provides two priority ballot attempts for first-timer SC households before reclassifying them as second-timers.

Can Singapore Permanent Residents (SPRs) apply for October 2026 BTO flats?

SPRs cannot apply for BTO flats as the sole applicant or as two SPR co-applicants. However, a SPR can co-apply as a joint applicant with a Singapore Citizen spouse or family member under the Public Scheme or Fiance/Fiancee Scheme. In that case, the SC-SPR household is eligible to apply for Standard and Plus classification BTO flats but may not apply for Prime classification flats (which are restricted to SC households only at launch). The SC-SPR household also qualifies for a reduced set of CPF grants — for example, the CPF Housing Grant for BTO is capped at S$20,000 (rather than S$40,000 for SC-SC couples), and EHG applies at the SC first-timer level for the SC co-applicant only.

How is the EHG (Enhanced CPF Housing Grant) calculated — is it always S$80,000?

The EHG is means-tested. The maximum of S$80,000 (for SC couples) is only available to households with an average gross monthly income of S$1,500 or less. As income rises, the EHG tapers down in steps. At S$4,500/mth the EHG for a couple is approximately S$50,000; at S$6,000/mth it is approximately S$30,000; at S$9,000/mth (the income ceiling) it is S$5,000. Income is assessed as the average gross monthly household income over the 12 months preceding the flat application, including variable components such as overtime, commissions, and bonuses. Check the official HDB EHG calculator at hdb.gov.sg for your specific income band.

Can I buy a BTO flat on a single income if I am not applying as a single?

Yes, but your borrowing capacity and grant eligibility are assessed on the household’s combined income. If you are applying as a couple (Public Scheme or Fiance/Fiancee Scheme) but only one person is currently working, HDB assesses your income ceiling based on the working person’s income alone for grant purposes, but the MSR (Mortgage Servicing Ratio) of 30% is applied to the working person’s gross monthly income for loan affordability. At an income of S$4,000/mth, MSR 30% allows a monthly HDB loan repayment of up to S$1,200, which at 2.6% over 25 years supports a loan of approximately S$268,000. Combined with grants, this can comfortably support a 4-room BTO in a Standard estate like Yishun or Tengah.

Is there a priority ballot for applicants near the project location?

Yes, under certain conditions. HDB provides a Married Child Priority Scheme (MCPS) for applicants whose parents live in the same town or within 4km of the BTO project. MCPS allocates a portion of units (typically 30% for those in the same town, 15% for within 4km) to eligible applicants before the general ballot. This priority scheme is separate from the EHG and does not require an income ceiling. To qualify, both the applicant household and the parents’ household must be Singapore Citizens, and the parents must be registered at an HDB address in the applicable town or within 4km of the BTO site. There is no corresponding scheme for applicants working near the project — only family proximity qualifies.