Sengkang Neighbourhood Guide Singapore 2026: Property Prices, Schools, MRT and Investment Outlook

Quick Answer — Sengkang 2026 at a Glance

- HDB 4-Room median resale price: S$652,000 (2026); entry-level from ~S$520,000 in non-mature precincts

- Private condo & EC: EC resale ~S$1.15M–S$1.35M; private condo ~S$1.1M–S$1.5M

- Connectivity: North East Line (NEL) + Sengkang LRT East & West loops — 10 LRT stops; ~25 minutes to City Hall

- Schools: Nan Chiau Primary & High, Compassvale Primary, Anchor Green Primary, CHIJ Our Lady of Good Counsel, Holy Innocent’s High School

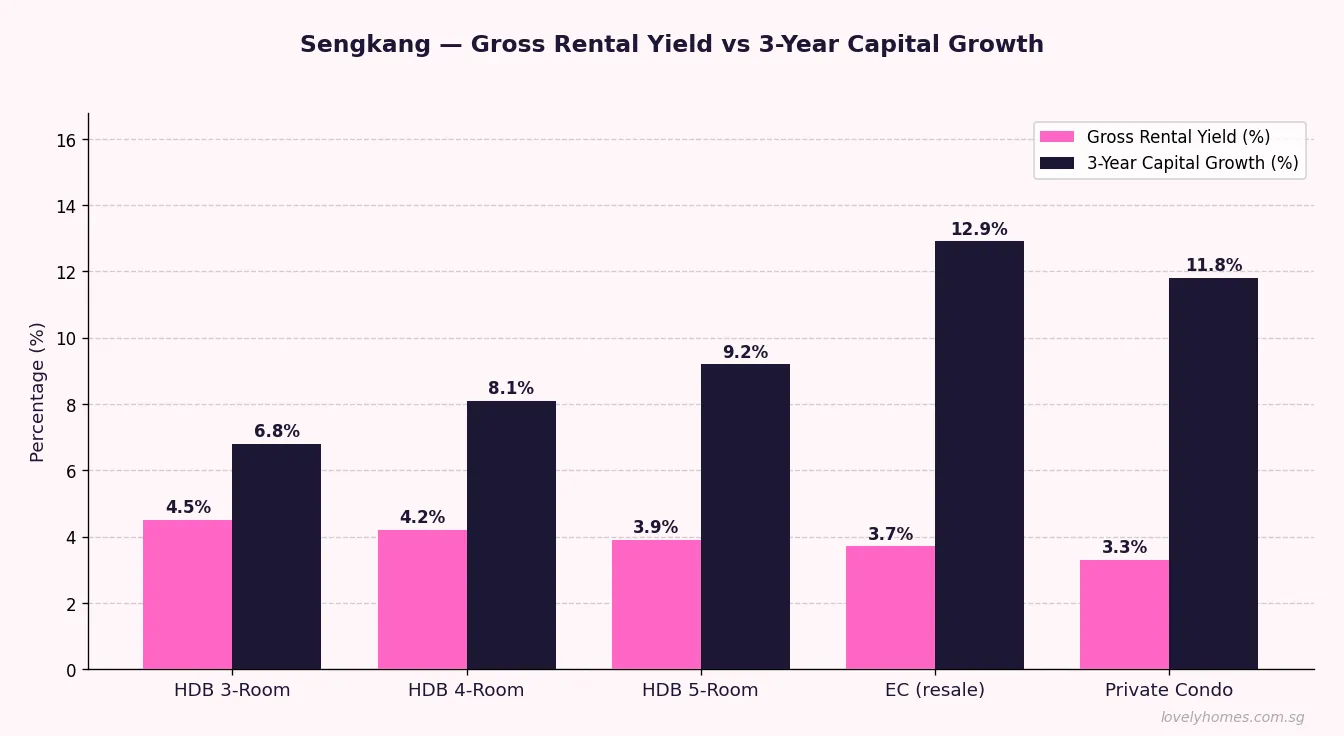

- Investment appeal: Gross rental yield ~3.3–4.5%; HDB 3-year capital growth ~8.1%; EC 3-year growth ~12.9%

- Key anchor: Sengkang General Hospital — a 1,400-bed SingHealth teaching hospital opened 2018

- MOP note: Sengkang BTOs from 2018–2020 hitting 5-year MOP in 2023–2025, adding resale inventory and buyer choice

What and Where Is Sengkang?

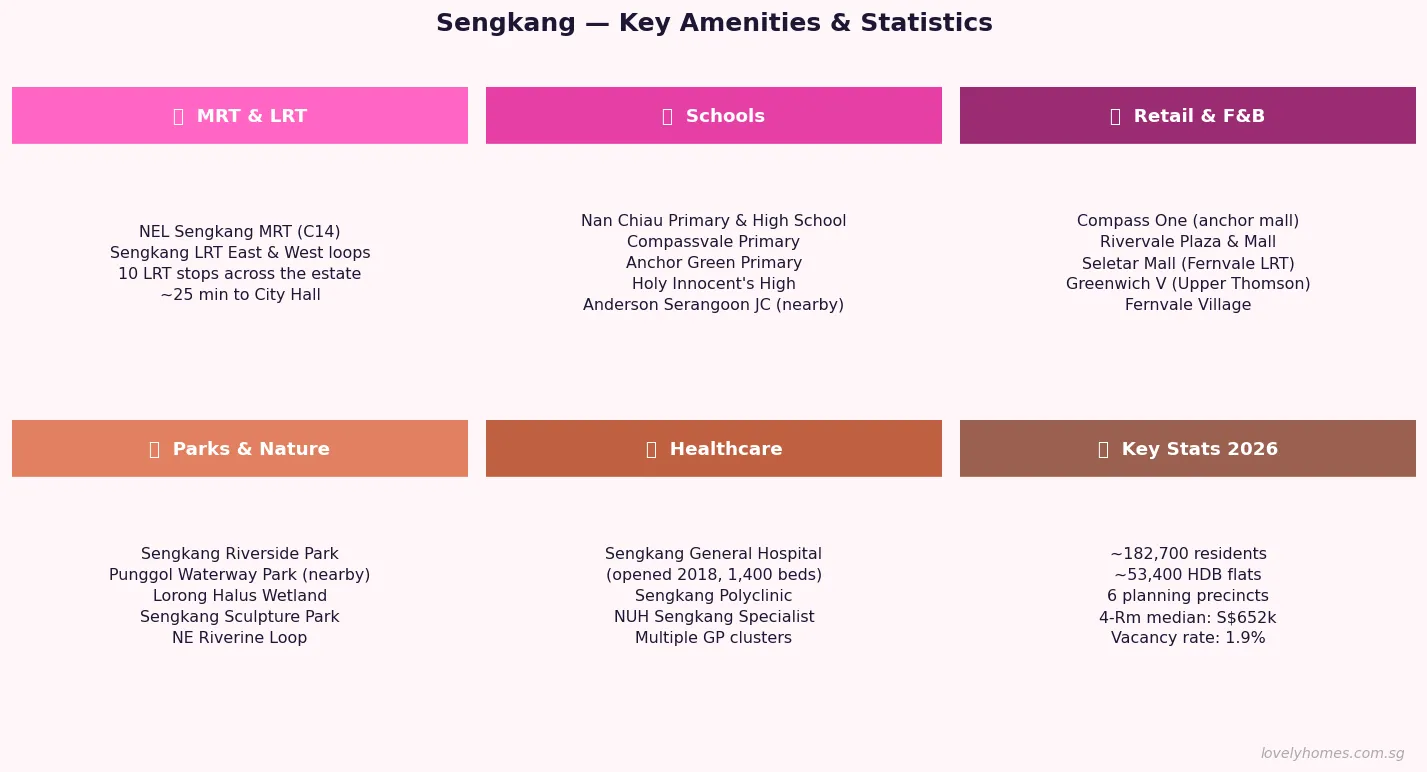

Sengkang is a maturing HDB town in the northeastern region of Singapore, located in Planning Area 23 under the Urban Redevelopment Authority’s (URA) Master Plan. Developed from the late 1990s onwards by the Housing & Development Board (HDB), the estate has grown into one of Singapore’s largest HDB towns, with approximately 182,700 residents and more than 53,400 flats across six planning precincts — Anchorvale, Compassvale, Fernvale, Lorong Halus North, Rivervale, and Sengkang Town Centre.

The estate is bounded by Buangkok to the west, Punggol to the northeast, and the Punggol and Serangoon rivers on its fringes. Its proximity to Punggol Digital District and the planned Cross Island Line (CRL) Phase 2 terminus gives Sengkang an economic gravity that distinguishes it from comparable Outside Central Region (OCR) towns further west.

Under HDB’s classification framework introduced in 2024, Sengkang BTO flats are classified as Standard — preserving the 5-year Minimum Occupation Period (MOP) and allowing unrestricted resale thereafter. This is an important distinction for buyers assessing long-term liquidity, as Standard flats carry no income ceiling at resale and are not subject to the enhanced 10-year MOP that applies to Plus and Prime classifications.

Sengkang Property Market Overview 2026

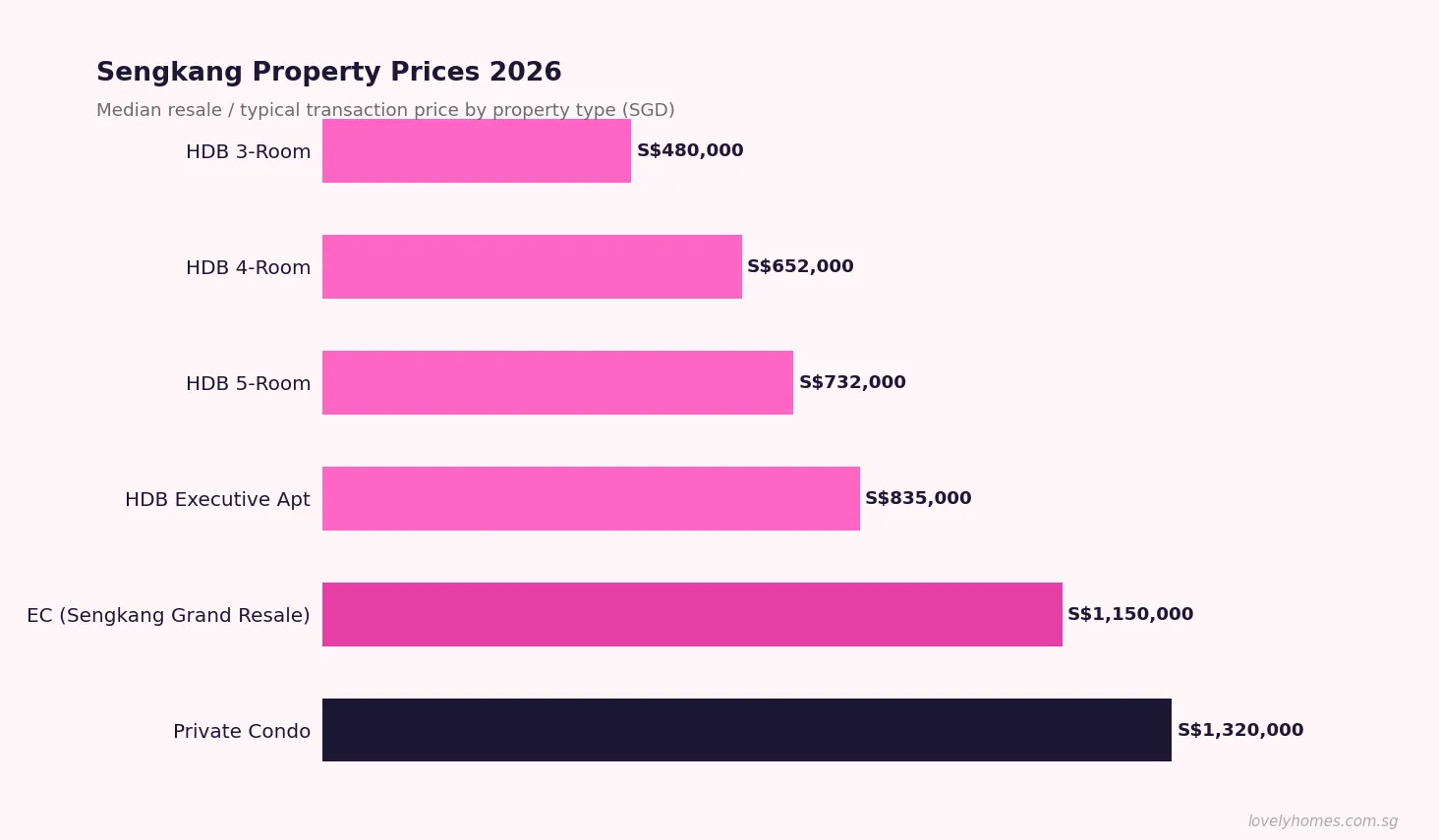

The Sengkang resale market recorded approximately 1,000 HDB transactions in 2025, with the median 4-Room flat transacting at S$652,000 and the median 5-Room at S$732,000 in 2026. While these figures sit at the lower end of the OCR resale spectrum compared with Tampines or Bishan, the estate’s relative affordability — combined with its strong transport network and growing amenities base — underpins steady buyer demand.

HDB resale highlights 2026: Sengkang 5-room resale flats have breached S$900,000 in standout locations with waterway views or high floors. A Rivervale Crescent 5-room flat transacted at S$895,000 in early 2026, reflecting the premium buyers place on units within walking distance of Sengkang MRT interchange. Flats in Fernvale and Anchorvale generally transact at a 10–15% discount to similarly sized Rivervale and Compassvale units, as the LRT adds a transfer hop from the North East Line.

Executive Condominium (EC) resale: Sengkang Grand Residences — the integrated mixed-use EC at Sengkang Central — stands out as Sengkang’s premium EC offering. Resale units transact at S$1,100–S$1,320 per square foot (psf), reflecting the mall podium and direct LRT access. Earlier ECs such as Riverparc Residence and Rivervale Crest trade at S$900–S$1,050 psf.

Private condo: Riverfront Residences (the former Rio Casa en-bloc redevelopment) commands S$1,150–S$1,350 psf. The estate’s limited private condo stock — relative to its HDB scale — creates a thin secondary market, which can amplify both upside and downside price movements. Buyers seeking private housing in this corridor sometimes compare against the neighbouring Hougang or Punggol supply pipelines.

Getting Around — MRT, LRT and Bus Connectivity

Sengkang’s transport backbone is the North East Line (NEL) Sengkang MRT interchange station (NE16), operated by SBS Transit under the Land Transport Authority’s (LTA) regulatory framework. From Sengkang MRT, commuters reach Serangoon (NEL/CCL interchange) in 5 minutes, Dhoby Ghaut (NEL terminus) in 22 minutes, and HarbourFront in 29 minutes. This places the central business district well within the 30-minute commute envelope that is consistently associated with residential price premiums in Singapore.

Unique to Sengkang is the Sengkang LRT system, which operates two loops from the MRT interchange — the East Loop and West Loop — serving 10 LRT stations across the estate. The LRT provides last-mile connectivity to precincts not immediately adjacent to the NEL, including Fernvale, Rivervale, and Lorong Halus North. The LRT runs at 5–10 minute frequency during peak hours and is seamlessly integrated with the MRT fare system.

Bus services connecting Sengkang to Punggol Digital District, Hougang, Ang Mo Kio, and the Woodlands Regional Centre further broaden the estate’s commuter catchment. The planned Cross Island Line (CRL) Phase 2 (~2031), which will serve Punggol at the town’s northeastern boundary, is expected to improve cross-island connectivity for residents in the Fernvale and Lorong Halus North precincts.

Schools and Education in Sengkang

Education infrastructure is a significant draw for families choosing Sengkang. The estate is home to a strong cluster of primary and secondary schools within the one-kilometre priority registration radius used by the Ministry of Education (MOE) for Phase 1 and Phase 2A registration balloting.

Primary schools: Nan Chiau Primary School and Nan Chiau High School (Secondary) sit in Compassvale, maintaining a direct feeder-school relationship valued by Chinese-stream families. Compassvale Primary and Anchor Green Primary serve the town-centre and Rivervale precincts respectively. CHIJ Our Lady of Good Counsel (Sengkang) is a popular all-girls primary that consistently draws strong demand in Phase 2B registration rounds.

Secondary and post-secondary: Holy Innocent’s High School (Hougang, within close proximity) and North Vista Secondary serve Sengkang’s secondary-school population. Anderson Serangoon Junior College — formed from the 2020 merger of Anderson JC and Serangoon JC — is located in Ang Mo Kio and within reasonable commuting distance.

The opening of Singapore Institute of Technology (SIT)’s Punggol Campus at the adjacent Punggol Digital District in 2024 has drawn a cohort of tertiary students and young professionals to the northeast corridor — a rental demand segment supporting yields for 2-room and 3-room HDB units in Sengkang.

Retail, Amenities and Lifestyle

Compass One, the anchor shopping mall directly above Sengkang MRT, serves as the town’s retail and F&B hub with a cinema, Cold Storage supermarket, and family-oriented tenants. Rivervale Mall and Rivervale Plaza serve the eastern precincts with neighbourhood-scale supermarkets and clinics. Seletar Mall at Fernvale LRT provides a significant retail node with NTUC FairPrice Finest and lifestyle tenants, drawing residents from the western precincts.

Sengkang Riverside Park, adjacent to the Punggol River, connects to the northeast riverine loop for cyclists and joggers. Lorong Halus Wetland — a former landfill converted into a bird-watching and recreational destination — sits at Sengkang’s northeastern edge and represents one of Singapore’s more unusual ecological assets close to a residential estate.

Healthcare: Sengkang General Hospital, a 1,400-bed acute hospital under the SingHealth cluster, opened in 2018 and is one of Singapore’s newer integrated teaching hospitals. It acts both as a healthcare resource for residents and as a significant employer anchoring the northeast. Sengkang Polyclinic, operated by the National Healthcare Group (NHG), provides primary-care services to residents.

Sengkang HDB Resale — Key Facts Summary

| Property Type | Typical Price Range (S$) | Median 2026 (S$) | Key Notes |

|---|---|---|---|

| HDB 3-Room | 410,000 – 570,000 | 480,000 | Good entry for investors; strong rental demand from singles and couples |

| HDB 4-Room | 520,000 – 790,000 | 652,000 | Highest transaction volume; premium for Rivervale/Compassvale facing units |

| HDB 5-Room | 620,000 – 920,000 | 732,000 | Records approaching S$900k in prime locations with water or park views |

| HDB Executive Apt | 700,000 – 980,000 | 835,000 | Limited supply; Rivervale Executive Apartments most sought-after |

| EC (resale, post-MOP) | 980,000 – 1,550,000 | 1,150,000 | Sengkang Grand Residences commands integrated-development premium |

| Private Condo | 950,000 – 1,700,000 | 1,320,000 | Thin market; Riverfront Residences dominates secondary supply |

Worked Example — SC Couple First Home in Sengkang 2026

Mr and Mrs Tan, Singapore Citizens, combined monthly income S$9,500. Buying a 4-Room HDB resale in Compassvale, Sengkang as their first property.

| Purchase price | S$670,000 |

| Buyer’s Stamp Duty (BSD, administered by IRAS) | S$12,200 |

| Additional BSD (ABSD) — SC buying 1st property | Nil (0%) |

| HDB Loan (80% LTV at 2.6% p.a.) | S$536,000 |

| Down payment (20%, CPF-eligible) | S$134,000 |

| Conveyancing and caveat fees (est.) | ~S$3,200 |

| Monthly instalment (30-year HDB loan) | S$2,436/month |

| Mortgage Servicing Ratio (MSR, MAS cap ≤ 30%) | 25.6% ✓ |

| Total Debt Servicing Ratio (TDSR, MAS cap ≤ 55%) | 25.6% ✓ |

BSD computed using IRAS progressive rates: 1% on first S$180,000 + 2% on next S$180,000 + 3% on balance. HDB loan rate of 2.6% p.a. = CPF OA rate (2.5%) + 0.1%. MSR and TDSR administered by MAS; MAS rules limit HDB resale loan tenure to 25 years (bank) or 30 years (HDB loan).

Is Sengkang a Good Property Investment in 2026?

Sengkang occupies a compelling mid-tier position in Singapore’s property investment landscape. For HDB investors and owner-occupiers who value yield, the estate delivers some of the strongest gross rental yields in the OCR — particularly for 3-Room flats, which gross approximately 4.5% at 2026 median prices versus median rents of roughly S$1,800/month for a furnished 3-Room unit near Sengkang MRT.

Capital growth has been moderate-to-solid for HDB but more pronounced for the EC segment. Sengkang EC resale prices have appreciated roughly 12–13% over the past three years, outperforming the island-wide private residential price index growth of approximately 8–9% over the same period. This reflects limited EC supply in the northeast following MOP completions at Riverparc Residence and Rivervale Crest, and the premium commanded by Sengkang Grand Residences’ integrated format.

Risk factors to weigh: The HDB resale supply pipeline is meaningful — Sengkang BTOs from 2018–2020 have been hitting their 5-year MOP, adding inventory. The LRT dependency for Fernvale and Lorong Halus North precincts means transport accessibility is inferior to Compassvale and Rivervale, and prices reflect this discount of 10–15%. Investors should also model the impact of Additional Buyer’s Stamp Duty (ABSD) — at 20% for Singapore Citizens buying a second residential property — on net investment returns before committing.

What Might Come Next for Sengkang Property?

The following section reflects editorial analysis and forward projections by LovelyHomes as at 19 May 2026. It is speculative and should not be construed as financial or investment advice.

Three catalysts are worth watching over the next 3–5 years. First, Punggol Digital District’s employment ramp-up: as the 28,000-job tech, media, and design cluster at the adjacent Punggol Coast matures, rental demand for 2-room and 3-room HDB units in Sengkang’s northeastern precincts is likely to strengthen, narrowing the discount these precincts carry versus Rivervale and Compassvale.

Second, CRL Phase 2 (~2031): the Cross Island Line’s Punggol terminus will offer direct cross-island access to Jurong Lake District via a single transfer. While Sengkang itself is not on the CRL alignment, the improved connectivity of neighbouring Punggol will raise the entire northeast corridor’s accessibility profile with positive price spillover for Sengkang.

Third, HDB’s evolving classification framework: Sengkang’s BTO flats currently classified as Standard carry no enhanced resale restrictions. This is a feature — not a constraint — for resale buyers. If housing policy shifts towards designating more northeast flats as Plus classification, the resale pool could contract, supporting secondary-market prices but reducing liquidity. Buyers who purchase Standard flats today avoid this classification risk entirely.

Frequently Asked Questions — Sengkang Property 2026

Is Sengkang a good place to buy property in 2026?

Sengkang offers a strong combination of affordability, transport connectivity, and amenity density for families and first-time buyers. The 4-Room HDB median price of S$652,000 is meaningfully below comparable sizes in Bishan, Toa Payoh, or Queenstown, yet the North East Line delivers competitive CBD commute times. For investors, gross rental yields of 3.3–4.5% are attractive by Singapore standards. Buyers should factor in Additional Buyer’s Stamp Duty (ABSD), administered by IRAS, when calculating returns if this is not their first property purchase.

Which MRT and LRT stations serve Sengkang?

The main interchange is Sengkang MRT (NE16) on the North East Line, connecting to Serangoon, Dhoby Ghaut, and HarbourFront. The Sengkang LRT system runs two loops from this interchange, operated by SBS Transit under LTA regulation. East Loop stops: Cheng Lim, Farmway, Renjong, and back to Sengkang. West Loop stops: Compassvale, Tongkang, Rumbia, Bakau, Kangkar, Ranggung, and back to Sengkang. Frequency is 5–10 minutes at peak hours.

How does Sengkang compare with Punggol for property buyers in 2026?

Sengkang and Punggol are neighbouring northeast towns with similar demographics and transport corridors, but they differ in maturity and price positioning. Sengkang’s 4-Room median (~S$652,000) currently sits below Punggol’s (~S$700,000), reflecting Punggol’s stronger forward-looking narrative around the Digital District and CRL Phase 2. Sengkang offers a denser current amenity base (Compass One, Sengkang General Hospital) and a more established school cluster. Punggol offers newer flats, waterway-facing units, and a longer-duration growth story. For families valuing schools and healthcare today, Sengkang is often preferred; for younger buyers with longer time horizons, Punggol’s infrastructure pipeline may justify its premium.

Are there upcoming BTO launches in Sengkang in 2026?

HDB’s confirmed June 2026 BTO exercise covers Ang Mo Kio, Bishan, Bukit Merah, Sembawang, and Woodlands — Sengkang is not among the June 2026 sites. HDB typically rotates BTO supply across towns on a 12–18 month cycle; prospective BTO buyers should monitor HDB’s website (hdb.gov.sg) for August and October 2026 announcements. Sengkang BTOs, when launched, are Standard classification with a 5-year MOP and the standard income ceilings: S$14,000 for families, S$7,000 for singles buying 2-Room Flexi flats.

What rental income can I expect from a Sengkang HDB flat in 2026?

Rental income varies by flat type, location, and furnishing. As a guide: furnished 3-Room flats near Sengkang MRT let for approximately S$1,750–S$2,100/month; 4-Room furnished flats command S$2,200–S$2,700/month; 5-Room furnished units achieve S$2,600–S$3,200/month. HDB flat owners must have fulfilled MOP and obtained HDB’s subletting approval before letting. Rental income is subject to Inland Revenue Authority of Singapore (IRAS) taxation; landlords may deduct allowable expenses (mortgage interest, maintenance, agent fees) against gross rental income.

Can a Permanent Resident buy a Sengkang HDB resale flat?

Yes — Singapore Permanent Residents (SPRs) can purchase HDB resale flats in Sengkang subject to HDB’s eligibility criteria. SPRs must form a family nucleus (single SPRs generally cannot buy HDB resale alone), must have held PR status for at least three years, and must not own any other property at the time of purchase. SPRs must use bank financing — the HDB concessionary loan is available only to Singapore Citizens. ABSD of 5% applies to an SPR buying their first residential property in Singapore. HDB’s Ethnic Integration Policy (EIP) quotas also apply.

Which precinct in Sengkang offers the best value?

From a convenience standpoint, Rivervale and Compassvale are the most sought-after precincts, commanding the highest prices. Rivervale units near Sengkang Riverside Park attract waterway premiums; Compassvale benefits from the Nan Chiau school cluster and direct NEL connectivity. Fernvale and Anchorvale offer lower entry prices — attractive for yield-focused investors — with Seletar Mall compensating for the extra LRT transfer. Lorong Halus North offers the most affordable entry in Sengkang but is the most distant from the MRT interchange, making it best suited for buyers whose daily routines do not require CBD commutes.

Related Articles

- Punggol Neighbourhood Guide Singapore 2026 — Waterfront Living, Digital District & Property Outlook

- Ang Mo Kio Neighbourhood Guide Singapore 2026

- Tampines Neighbourhood Guide Singapore 2026

- Bedok Neighbourhood Guide Singapore 2026

- Pasir Ris Neighbourhood Guide Singapore 2026

- ABSD Singapore 2026 — Complete Guide to Additional Buyer’s Stamp Duty

- HDB Grants Singapore 2026 — EHG, CPF Housing Grant, Proximity Grant and Step-Up Grant

- Home Loan Comparison Singapore 2026 — HDB Loan, Fixed vs Floating and the SORA Explained

Disclaimer

This article is intended for general information and educational purposes only and does not constitute financial, investment, legal, or property advice. All property prices, rental yields, market data, and regulatory information are based on sources available as at 19 May 2026 and are subject to change. Buyers, sellers, and investors should verify current information directly with the Housing & Development Board (HDB) at hdb.gov.sg, the Urban Redevelopment Authority (URA) at ura.gov.sg, the Inland Revenue Authority of Singapore (IRAS) at iras.gov.sg for stamp duty matters, and the Monetary Authority of Singapore (MAS) at mas.gov.sg for loan regulations. Always consult a licensed financial adviser, mortgage specialist, and Law Society-accredited conveyancing solicitor before making any property transaction decision.

Click anywhere to close