Hougang Neighbourhood Guide Singapore 2026: Property Prices, Schools, MRT and Investment Outlook

Quick Answer: Hougang Singapore 2026 — Property Snapshot

- Location: District 19, North East Region (OCR). Mature HDB town with an established residential community.

- MRT access: North East Line (NEL) — Hougang (NE14) and Kovan (NE13). Cross Island Line (CRL) Phase 2 at Hougang, expected approximately 2032.

- Property types: Predominantly HDB flats (3-room to Executive Apartment); limited private condo supply; some landed properties in the Kovan enclave.

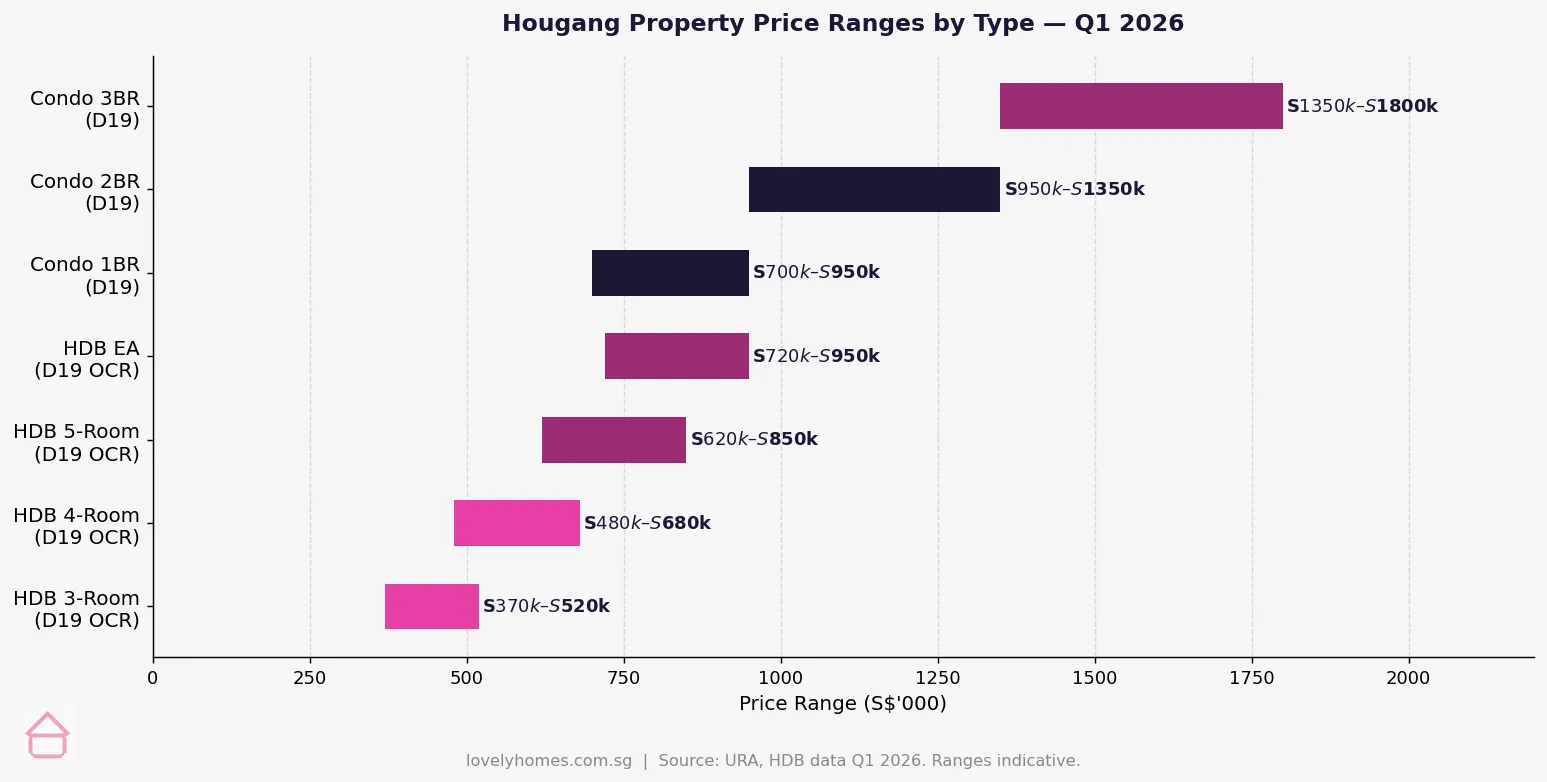

- HDB prices (Q1 2026): 3-room S$370k–S$520k; 4-room S$480k–S$680k; 5-room S$620k–S$850k; Executive Apartment S$720k–S$950k.

- Condo prices (Q1 2026): 1BR S$700k–S$950k; 2BR S$950k–S$1.35M; 3BR S$1.35M–S$1.8M.

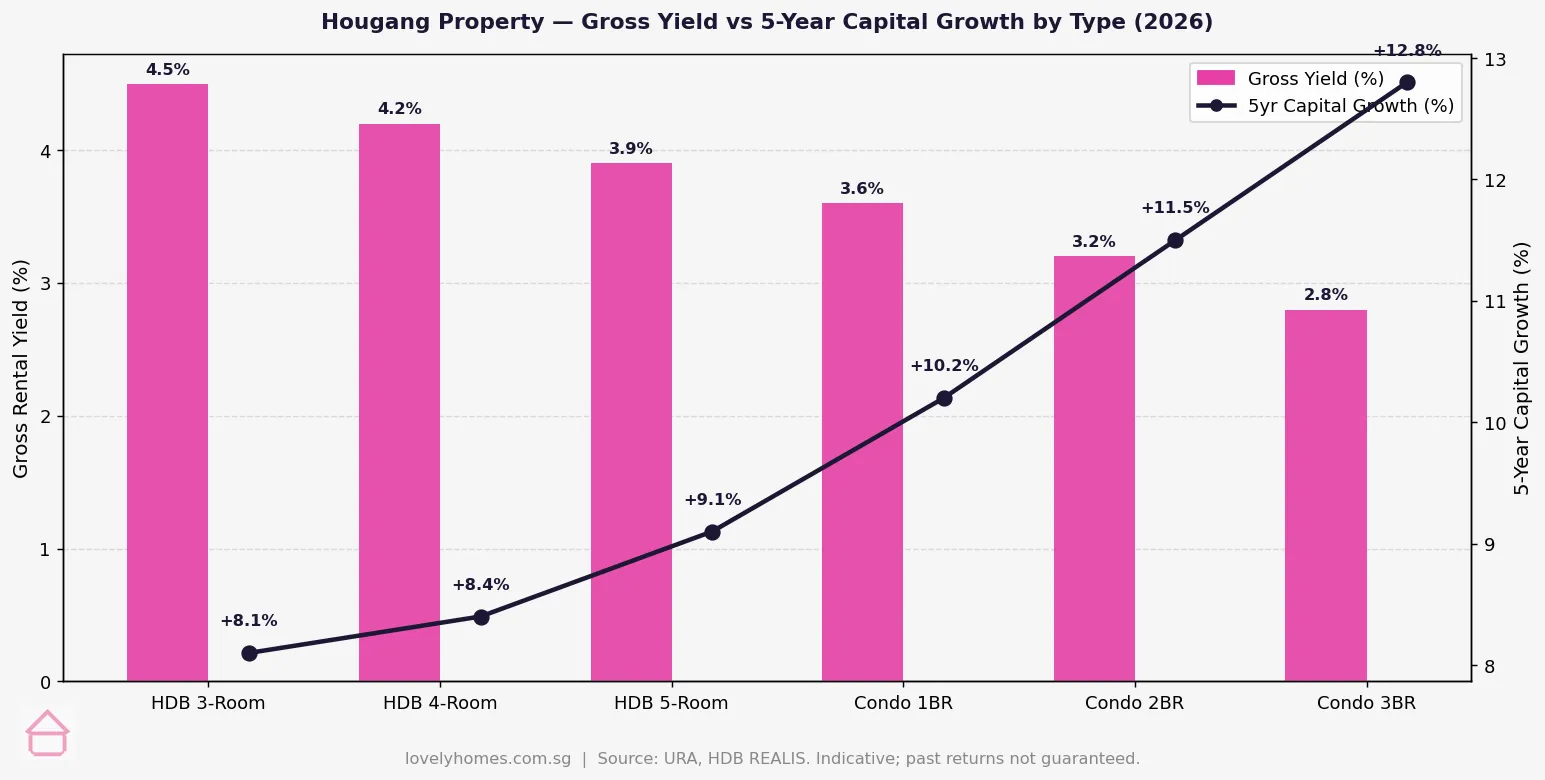

- Gross rental yield: HDB 3-room approximately 4.5%; condo 2BR approximately 3.2%.

- 5-year capital growth: HDB 4-room +8.4%; condo 2BR +11.5% (URA/HDB data Q1 2026).

- Best for: HDB upgraders, value-seeking first-timers, and investors targeting the CRL uplift thesis.

- Key catalysts: CRL Phase 2 at Hougang station, Hougang Town Centre rejuvenation, proximity to Serangoon and NEX mall.

Why Hougang? An Overview of District 19

Hougang (pronounce: “Haw-kang”) is one of Singapore’s most established and self-sufficient HDB towns, situated in the North East Region of Singapore in District 19 (D19). The area encompasses the Hougang Planning Area under the URA Master Plan and extends into parts of the Serangoon and Punggol planning areas. It is bounded by the Kallang-Padan River to the south, Sengkang to the north, and Serangoon to the west.

Hougang is primarily an Outside Central Region (OCR) market — which means property prices are significantly more accessible than in the Core Central Region (CCR) districts like Orchard or River Valley, while still offering strong connectivity and a mature estate with comprehensive amenities. The town’s character is deeply residential: wide tree-lined boulevards, multiple hawker centres, well-maintained void decks, and a close-knit community that has made Hougang one of Singapore’s most liveable mature towns for decades.

For property buyers, Hougang’s appeal in 2026 centres on three themes: affordability relative to central districts, the CRL Phase 2 uplift catalyst (the Cross Island Line will add a station in Hougang with interchange potential, expected approximately 2032), and strong HDB rental yields sustained by proximity to Serangoon’s commercial hub and the Ngee Ann Polytechnic student population.

Hougang Property Market: Prices and Supply

HDB Resale Market

Hougang’s HDB resale market is well-established, with approximately 34,000 HDB units across the Hougang and Kovan precincts. The stock is predominantly 3-room to 5-room flats and Executive Apartments (EAs), with a smaller supply of studio/2-room units. Prices have risen consistently over the past five years — 5-room flats that transacted at approximately S$510–580k in 2021 now regularly achieve S$650–850k in 2026, driven by the broader Singapore OCR HDB resale price uplift and improving MRT connectivity expectations from the CRL announcement.

Million-dollar HDB transactions in Hougang remain rare relative to more central OCR estates such as Queenstown, Toa Payoh, or Bishan — making it an attractive option for buyers priced out of those areas. The 5-room and EA segment in Hougang commands premiums for units facing Punggol Park or within 500 metres of Hougang MRT (NE14).

Private Condominium Market

Private condominium supply in Hougang is limited relative to the HDB stock, contributing to relatively stable pricing and lower vacancy. Key developments include Kingsford Waterbay (near Hougang Avenue 4, 1,165 units, 99-year leasehold, launched 2015), The Minton (Lorong Ah Soo, 1,145 units, 99yr), and the more recent Parc Botannia (Fernvale Road, 735 units, 99yr). Freehold options are available in the Kovan enclave — Kovan Residences (1BR from S$720k, 2BR from S$1.0M) and various smaller boutique freehold developments along Upper Serangoon Road command a freehold premium of approximately 15–20% over comparable 99-year leasehold developments.

Landed Property

Hougang and the adjacent Kovan area have a cluster of landed properties — terraces, semi-detached houses, and a small number of detached bungalows — primarily along Upper Serangoon Road and the private enclaves off How Sun Drive and Upper Paya Lebar Road. Terraces typically transact at S$2.8–4.5M; semi-detached houses at S$4.0–7.0M. These landed options attract buyers seeking the peace and space of a landed home while remaining close to the NEL and Hougang’s established amenities.

Connectivity and MRT: NEL Today, CRL Tomorrow

Hougang is served by two North East Line (NEL) stations: Hougang (NE14) and Kovan (NE13), providing direct connections to Serangoon interchange (NE12/CCL13) in approximately 6 minutes, and onward to Dhoby Ghaut (NE6) — the heart of the Orchard/City Hall corridor — in approximately 28 minutes total. The NEL is one of Singapore’s most reliable and frequent lines, operating at approximately 2-minute headways during peak hours.

The transformational infrastructure catalyst is the Cross Island Line (CRL) Phase 2, announced by the Land Transport Authority (LTA). CRL Phase 2 will include a station at Hougang, expected to open approximately 2032 and providing a direct cross-island connection linking Hougang to Pasir Ris in the east and to the future Aviation Park station serving Changi Airport Terminal 5. The CRL will significantly improve Hougang’s connectivity for residents who currently rely on the NEL for cross-town travel. Historically in Singapore, MRT line announcements and openings have been associated with 10–20% price uplifts in the surrounding catchment — though this is location- and timing-specific and not guaranteed.

Schools, Amenities and Lifestyle

Hougang has a comprehensive education ecosystem serving families across all levels. At primary level, schools within 1–2km include Yuhua Primary, Hougang Primary, Pei Chun Public School, and Punggol Primary. For secondary education, Bowen Secondary, Montfort Secondary, and Serangoon Garden Secondary are established options. At the pre-university and tertiary level, Nanyang Junior College is located nearby in Serangoon, and Ngee Ann Polytechnic (approximately 3km, accessible by bus) generates consistent student rental demand for smaller HDB and condo units.

Hougang Mall (Hougang Central) is the primary retail anchor — a mid-sized suburban mall with a supermarket, cinema, and food and beverage offerings. Hougang 1 (Upper Serangoon Road) provides additional retail options. For a larger shopping experience, NEX at Serangoon — one of Singapore’s largest suburban malls — is just two NEL stops away at Serangoon NE12 and accessible within 10 minutes door to door.

Residents cite Hougang’s hawker food culture as one of its strongest lifestyle drawcards. The Hougang Central Food Centre, Teck Ghee Food Centre, and the informal coffee shops along Hougang Avenue 8 are local institutions well-regarded for affordability and variety. Punggol Park (approximately 32 hectares) provides green space and jogging tracks east of the town centre, while the North East Park Connector links Hougang to the broader Kallang-Bishan park network.

Summary: Hougang Property at a Glance

| Property Type | Price Range (S$) | Approx PSF | Gross Yield | 5-Yr Growth |

|---|---|---|---|---|

| HDB 3-Room (OCR) | S$370k – S$520k | S$540–760 | ~4.5% | +8.1% |

| HDB 4-Room (OCR) | S$480k – S$680k | S$490–700 | ~4.2% | +8.4% |

| HDB 5-Room (OCR) | S$620k – S$850k | S$480–660 | ~3.9% | +9.1% |

| HDB EA (OCR) | S$720k – S$950k | S$460–610 | ~3.7% | +9.5% |

| Condo 1BR (D19) | S$700k – S$950k | S$1,100–1,500 | ~3.6% | +10.2% |

| Condo 2BR (D19) | S$950k – S$1.35M | S$1,050–1,380 | ~3.2% | +11.5% |

| Condo 3BR (D19) | S$1.35M – S$1.80M | S$980–1,280 | ~2.8% | +12.8% |

Investment Outlook: Gross Yield and Capital Growth

Hougang offers a compelling yield-versus-growth profile in Singapore’s OCR landscape. For investors, HDB 3-room flats remain the highest-yielding proposition at approximately 4.5% gross, reflecting consistent rental demand from young couples, singles, and the student population near Ngee Ann Poly. Capital growth for HDB flats has been solid — approximately 8–9% over the past 5 years — tracking the broader OCR HDB resale price appreciation.

Private condominiums in Hougang offer lower yields (2.8–3.6%) but stronger capital growth (10–13% over 5 years), reflecting the market’s re-rating of D19 as the CRL uplift thesis gains traction. Investors targeting total return — combining rental yield with capital appreciation — will find the OCR condo market in Hougang competitive relative to CCR and RCR alternatives, particularly given the lower entry quantum (2BR from approximately S$950k versus S$1.8–2.4M for comparable CCR units).

Worked Example: Buying in Hougang 2026

Case Study: Mr and Mrs Rajan — HDB Resale, Hougang 2026

Mr and Mrs Rajan are Singapore Citizens, first-timers, joint income S$8,500 per month. They are buying a 4-room HDB resale flat in Hougang Central at S$580,000.

Grant eligibility:

- Enhanced CPF Housing Grant (EHG): S$25,000 (household income S$8,500 qualifies under the S$9,000 ceiling for families)

- Proximity Housing Grant (PHG): S$10,000 (living within 4km of parents)

- Total grants: S$35,000

Buyer’s Stamp Duty (BSD): S$580,000 → BSD = (S$180,000 × 1%) + (S$180,000 × 2%) + (S$220,000 × 3%) = S$1,800 + S$3,600 + S$6,600 = S$12,000

ABSD: Nil (Singapore Citizens, first residential property)

HDB Concessionary Loan: LTV 80% → loan S$464,000 at 2.6% p.a. over 25 years. Monthly instalment approximately S$2,101/month. MSR check: S$2,101 ÷ S$8,500 = 24.7% — within the 30% MSR ceiling. PASS.

Cash upfront: 5% cash (S$29,000) + BSD S$12,000 + legal S$2,500 + valuation S$350 = approximately S$43,850

CPF OA usage: Remaining 15% downpayment S$87,000 from CPF OA, plus monthly instalments drawn from CPF OA thereafter.

Net grant-adjusted price: S$580,000 − S$35,000 = S$545,000 effective

Is Hougang a Good Place to Buy Property in 2026?

The case for Hougang rests on four pillars. First, it is one of the more affordable mature OCR towns in Singapore — buyers priced out of Serangoon (D19/D20 border) or Bishan (D20) often find equivalent-sized HDB units in Hougang at S$30–80k less. Second, the CRL Phase 2 catalyst is not yet priced in for most Hougang properties; comparable towns that received new MRT lines in the past decade saw 10–15% uplifts in property values in the 5 years surrounding opening. Third, HDB rental yields are strong by Singapore standards — 3.7–4.5% gross for HDB flats — supported by Ngee Ann Poly students, migrant workers, and young professionals who appreciate the town’s accessibility and affordability. Fourth, Hougang’s existing amenities are mature and comprehensive — no waiting for new malls or parks; everything from hawker centres to polyclinics and Punggol Park is already there.

The primary risk factors are the limited private condo pipeline (which constrains capital appreciation relative to developments in more active en bloc or GLS corridors) and the generally older HDB stock (some blocks built in the 1980s will face lease-decay considerations as they age towards the 40–50 year mark). Buyers of older HDB units should check remaining lease carefully, as CPF withdrawal rules restrict usage for flats with fewer than 30 years of lease remaining.

What Might Come Next: Hougang’s Property Outlook to 2030

The dominant medium-term story for Hougang is the Cross Island Line Phase 2. As the anticipated 2032 opening draws closer, we expect growing market attention from buyers seeking to position ahead of the connectivity uplift — a pattern well-established in Singapore from the opening of the Thomson-East Coast Line (TEL) stations in 2023, which re-rated Marine Parade and Bedok South pricing. Hougang’s current CRL discount relative to Serangoon and other NEL towns with more direct connectivity to the CBD is likely to narrow progressively through the late 2020s.

The HDB market in Hougang is also likely to benefit from the broader OCR HDB price trajectory. URA Q1 2026 data showed OCR HDB resale prices up approximately 2.2% quarter-on-quarter and 8.1% year-on-year — momentum that industry analysts expect to moderate but not reverse given the ongoing construction pipeline tightness for new BTO flats.

Frequently Asked Questions

Is Hougang a good area to buy property in Singapore?

Hougang is a well-regarded mature OCR town offering a strong balance of affordability, amenity, and community infrastructure. For HDB buyers, it provides access to the EHG and PHG grant ecosystem at entry prices significantly below central OCR estates like Queenstown, Toa Payoh, or Bishan. For private property investors, the limited condo supply creates a relatively stable pricing environment, and the forthcoming CRL Phase 2 station provides a medium-term capital growth catalyst. The estate is especially suited to families who value proximity to quality schools and hawker food, and to investors seeking sustainable HDB rental yields above 4%.

Which MRT stations serve Hougang?

Hougang is currently served by two North East Line (NEL) stations: Hougang (NE14) — the main town centre station — and Kovan (NE13) for the upper Kovan and Upper Serangoon Road area. From Hougang NE14, Serangoon interchange (NE12/CCL13) is one stop (approximately 4 minutes) and Dhoby Ghaut (NE6) at the City Hall/Orchard corridor is approximately 28 minutes. The forthcoming Cross Island Line (CRL) Phase 2, expected approximately 2032, will add a further station in Hougang, significantly enhancing connectivity east–west across Singapore without requiring a transfer.

Can PRs and foreigners buy HDB flats in Hougang?

Singapore Permanent Residents (PRs) may purchase HDB resale flats (not BTO) in Hougang subject to HDB eligibility conditions — the PR must form a family nucleus with a Singapore Citizen or another SPR, and the flat must have been owned by the seller for at least 5 years (MOP fulfilled). PRs are not eligible for CPF Housing Grants (EHG, PHG) and must use their CPF OA balances or cash for the purchase. Foreign nationals (non-PRs) are not permitted to purchase HDB flats under any circumstances. Foreigners may purchase private condominiums in Hougang but are subject to the 60% ABSD on the purchase price as of April 2023.

What are the best condominiums in Hougang?

Among Hougang’s private condo developments, Kingsford Waterbay (Hougang Avenue 4, 1,165 units, 99-year leasehold, river-facing blocks) is the largest and most established, offering a range of 1–5 bedroom units. In the Kovan enclave, Kovan Residences (freehold, Upper Serangoon Road) commands a tenure premium and is popular with buyers seeking a freehold asset. The Minton (Lorong Ah Soo) is another large 99-year leasehold development with good facilities. Buyers seeking newer stock may look at Parc Botannia (Fernvale Road) or monitor future GLS sites in the broader D19/D28 OCR corridor for new launches.

How does Hougang compare to Serangoon for property investment?

Hougang and Serangoon are adjacent and share the NEL, but they serve somewhat different buyer profiles. Serangoon (D19/D20 border area) benefits from the NEL/CCL interchange at Serangoon station and the NEX mega-mall, making it marginally more accessible for CBD commuters and more attractive to premium rental tenants. As a result, Serangoon HDB and condo prices are typically 5–15% above comparable Hougang units. Hougang offers better affordability and the forthcoming CRL catalyst, while Serangoon is already a more fully-priced, established market. For investors with a longer horizon and sensitivity to entry price, Hougang’s CRL upside story is compelling; for investors prioritising immediate rental demand depth, Serangoon has a slight edge.

What is the minimum occupation period (MOP) for Hougang HDB flats?

Standard HDB BTO and resale flats in Hougang must be occupied by the owner for a minimum of 5 years from the date of key collection (for BTO) or from the resale completion date before the owner may sell on the open resale market or rent out the entire flat. Hougang does not currently have any HDB Plus or Prime classification flats — the 10-year MOP classification applies to specific new estates designated as Plus or Prime under the October 2024 classification framework. If any Hougang BTO launches in future receive a Plus or Prime designation, those flats would carry the longer MOP — check the HDB launch classification at launch time.

What income do I need to buy a condo in Hougang?

For a 2BR condo in Hougang at approximately S$1.1M (mid-range of the current market), a Singapore Citizen buying as a first private property (ABSD nil) would need to satisfy: BSD of approximately S$27,600; a minimum 25% downpayment (5% cash = S$55,000 + 20% CPF/cash = S$220,000); and a bank loan of up to S$825,000 at 75% LTV. At 3.0% p.a. over 25 years, the monthly instalment is approximately S$3,910. Under the TDSR of 55%, the minimum monthly gross income required is approximately S$7,109 (S$3,910 ÷ 55%). Joint applicants can combine income. Note that if buyers still own an HDB flat, they must factor ABSD (20% for SC buying a second property, unless the HDB is sold first within 6 months under the remission framework).

Related Articles

- Serangoon Neighbourhood Guide Singapore 2026: Property Prices, Schools and Investment

- Singapore HDB BTO Guide 2026: Eligibility, Grants and Step-by-Step Process

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore CPF Property Withdrawal Limits 2026: OA and Withdrawal Limits Explained

- First-Time Property Buyer Singapore 2026: HDB, EC and Condo — Every Step and Cost

- Bedok Neighbourhood Guide Singapore 2026: Property Prices, MRT and Investment

Disclaimer

This article is for general informational and educational purposes only and does not constitute financial, legal, or investment advice. Property prices, HDB eligibility conditions, CPF withdrawal rules, ABSD rates, and MRT construction timelines are subject to change by the Singapore Government. Figures cited are derived from URA REALIS and HDB REALIS data as at Q1 2026 and are indicative only — actual transaction prices vary by unit, floor, facing, and condition. Buyers should conduct their own due diligence, engage a licensed property agent registered with the Council for Estate Agencies (CEA), and consult a mortgage broker or financial adviser before committing to any property transaction. For official current HDB grant and eligibility information, refer to the Housing and Development Board (hdb.gov.sg). For private property data, refer to the Urban Redevelopment Authority (ura.gov.sg).