Singapore CPF for Property Guide 2026: How to Use Your OA, Valuation Limits and Accrued Interest Explained

CPF for property Singapore — your Central Provident Fund Ordinary Account (CPF OA) is almost certainly your largest source of savings, and the rules governing how you can use it to buy a home are among the most misunderstood in Singapore’s property landscape. Buyers regularly assume they can use CPF for everything from their Additional Buyer’s Stamp Duty (ABSD) to their renovation bills — and are caught short at completion. Others sell a flat and are alarmed to see how much accrued interest has accumulated in their CPF ledger. This guide explains every rule, limit, and quirk in plain English.

Quick Answer — CPF for property at a glance

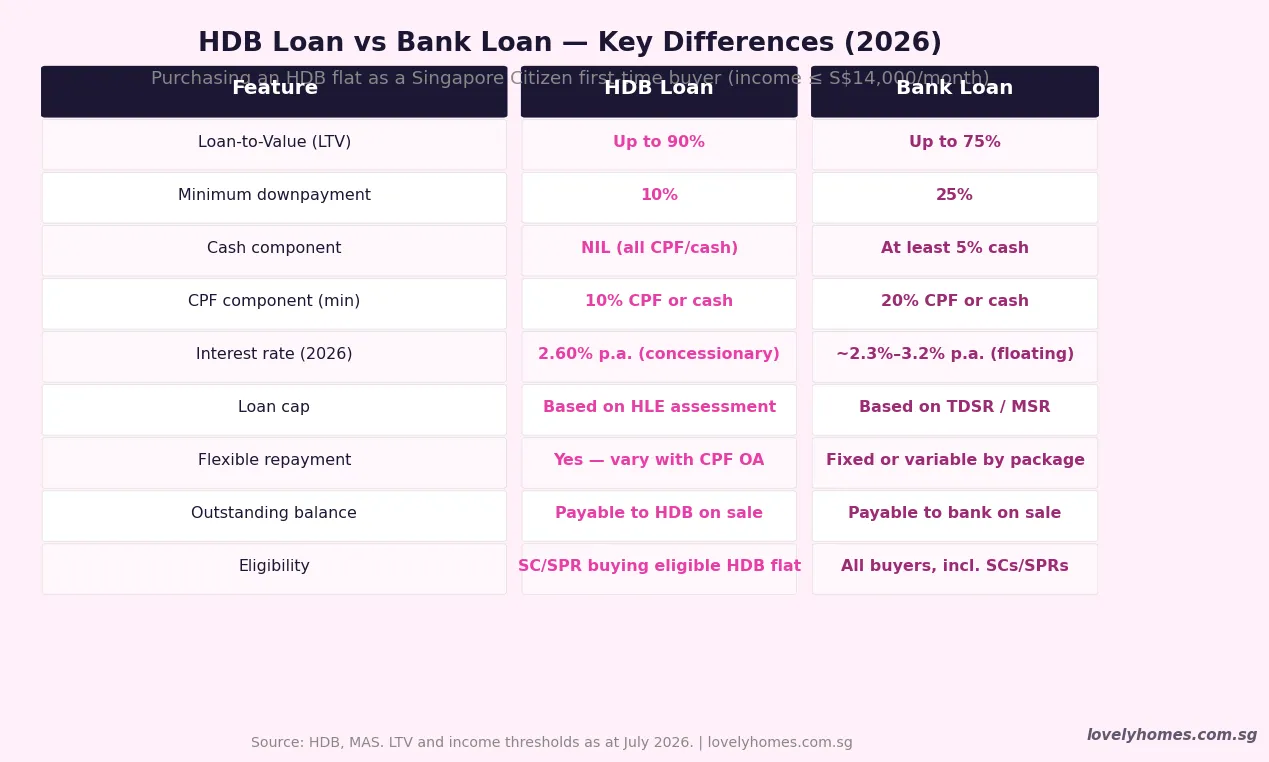

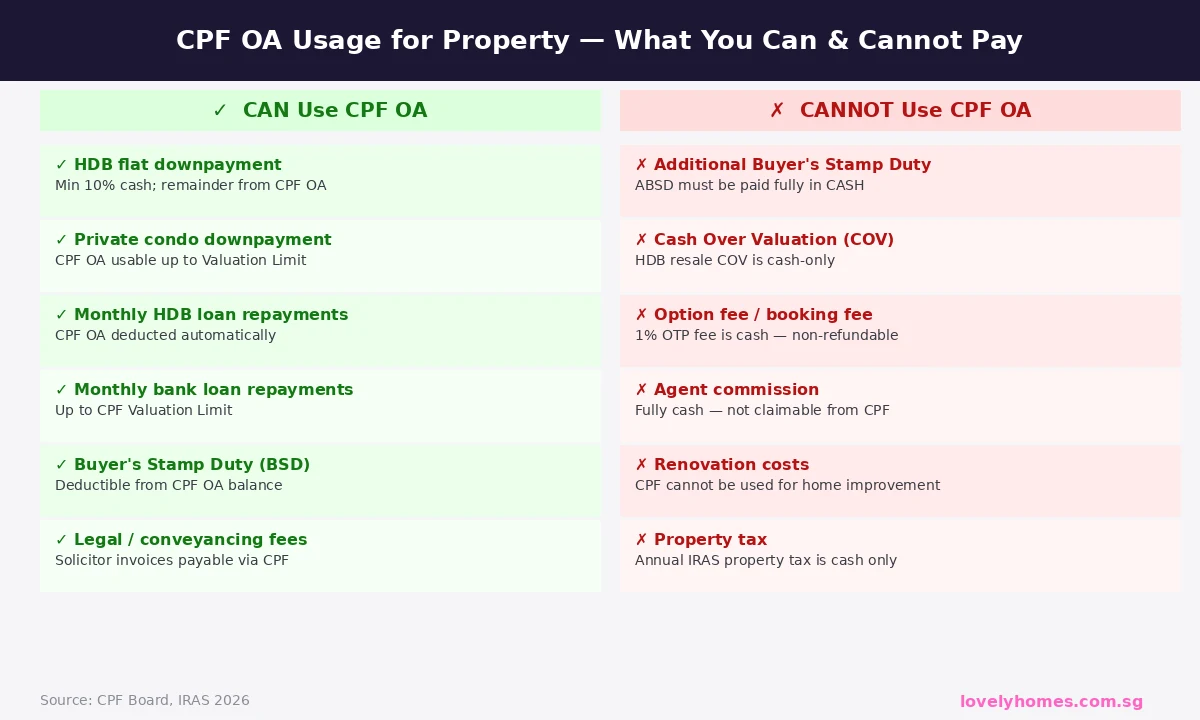

- CPF OA can be used for downpayment, monthly loan instalments, Buyer’s Stamp Duty, and legal fees.

- CPF OA cannot be used for ABSD (cash only), Cash Over Valuation, option fee, agent commission, or renovation.

- Valuation Limit (VL): You may use CPF up to the purchase price or market value, whichever is lower.

- Beyond VL: CPF can be used up to 120% of VL — but only if you have set aside the Full Retirement Sum (FRS).

- Accrued interest rate: 2.5% p.a. compounded on all CPF withdrawn for property. On sale, principal + accrued interest is refunded to your CPF OA — it does not vanish.

- Lease rule: Property must have at least 30 years’ remaining lease for CPF to be used; graduated limits apply between 30 and 60 years.

- For the latest rules, check CPF Board’s official housing page.

What Is the CPF Ordinary Account and Why Is It Used for Property?

The CPF is Singapore’s mandatory social security savings scheme. Every employed Singapore Citizen and Permanent Resident contributes a percentage of their monthly wages into three accounts: the Ordinary Account (OA), Special Account (SA), and MediSave Account (MA). For most working-age Singaporeans, the OA accumulates the largest balance over time — and it earns a minimum guaranteed interest of 2.5% per annum, with an additional 1% on the first S$60,000 of combined CPF balances (with a cap of S$20,000 for OA).

The Government allows the OA to be used for housing because property ownership is a central pillar of Singapore’s social compact. By permitting CPF OA usage, the scheme effectively unlocks decades of compulsory savings for the single largest purchase most households will ever make. The trade-off is that money withdrawn from CPF for property must eventually be returned — with interest — to the account so it remains available for retirement.

What Can You Use CPF OA For?

Your CPF OA balance can be applied to the following property-related expenses in 2026:

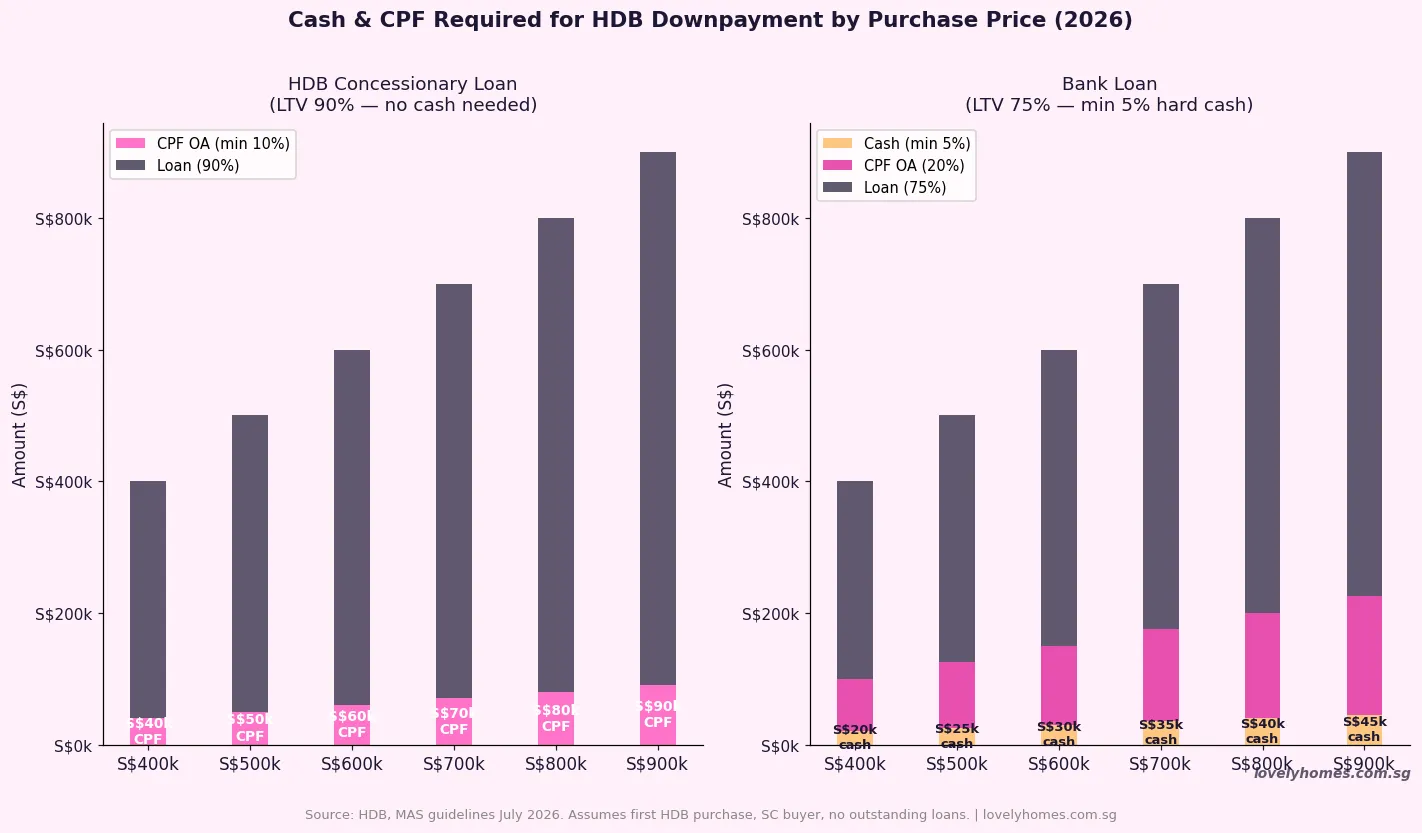

Downpayment: For an HDB flat purchased using an HDB loan, the minimum cash downpayment is 10% of the purchase price; the remaining 10% of the required 20% downpayment can come from CPF OA. For bank-financed purchases (HDB or private), the minimum cash downpayment is 5% of the purchase price (for loans up to 75% LTV), with the remaining 20% payable from CPF OA or cash.

Monthly loan repayments: Both HDB housing loan instalments and bank mortgage instalments can be paid from your CPF OA. HDB loans deduct directly via GIRO from your CPF OA. For bank loans, you must submit a CPF housing withdrawal application.

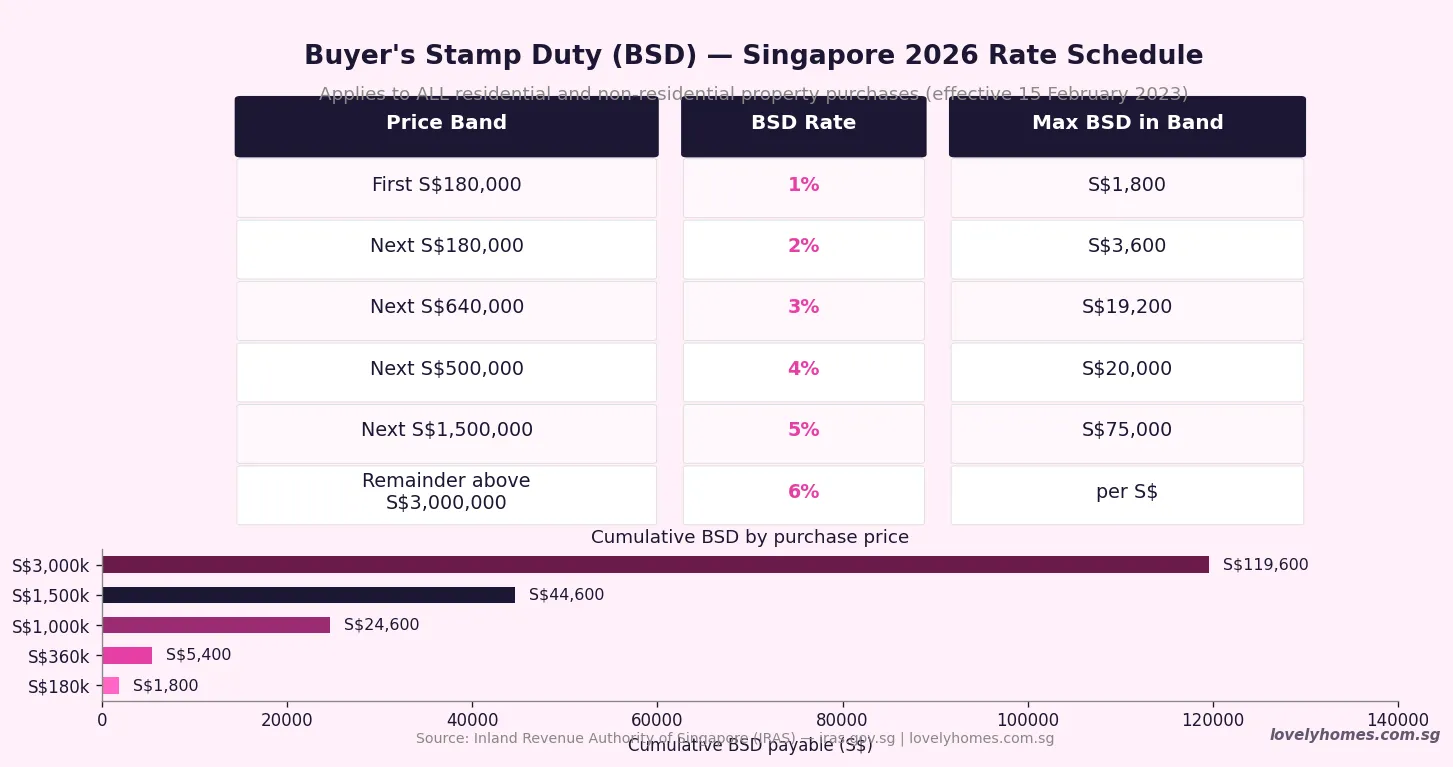

Buyer’s Stamp Duty (BSD): BSD can be paid from CPF OA — this is often overlooked by first-time buyers. At current rates, BSD on a S$600,000 HDB flat is approximately S$11,400, all of which can come from OA.

Legal and conveyancing fees: Solicitor fees for the purchase transaction are claimable from CPF OA, subject to the Valuation Limit rule.

What Cannot Be Paid with CPF OA?

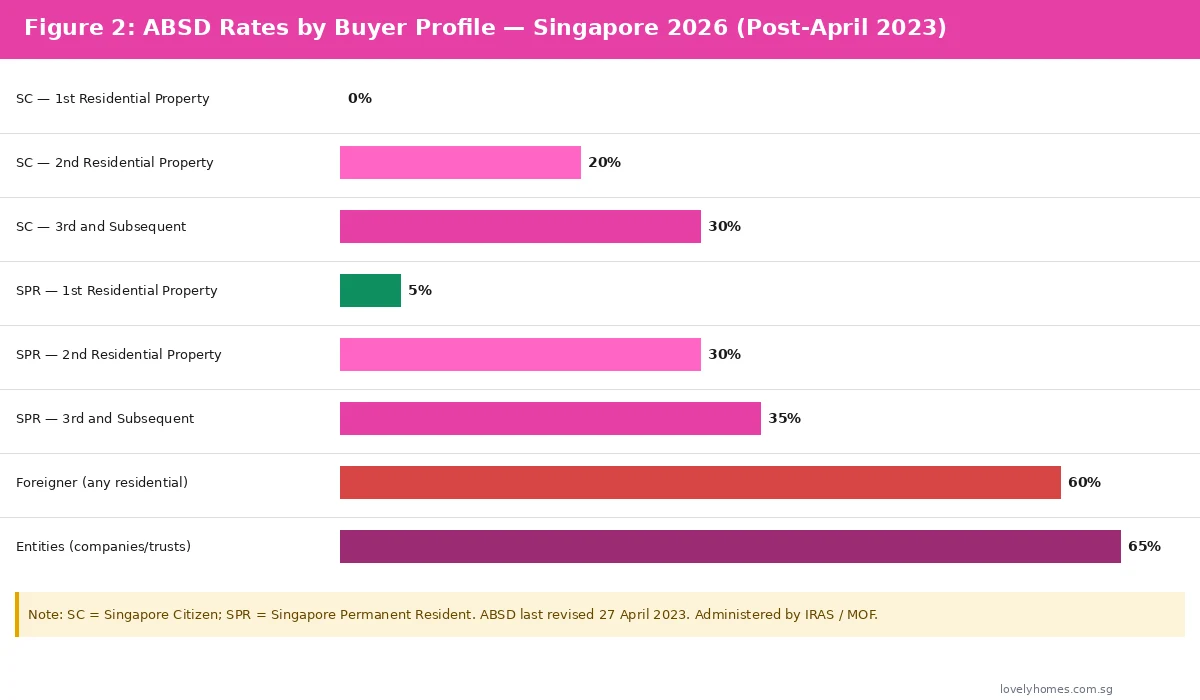

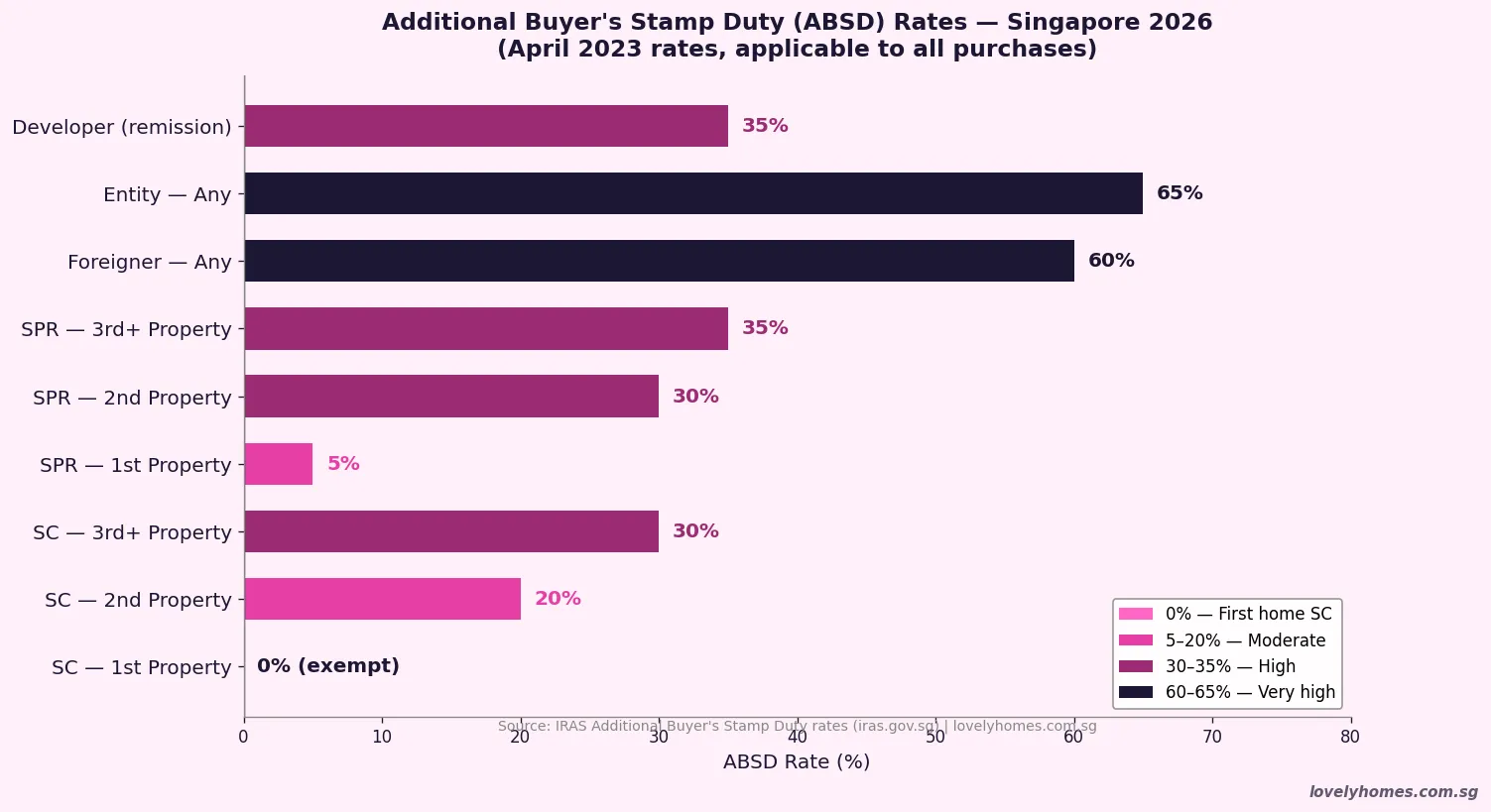

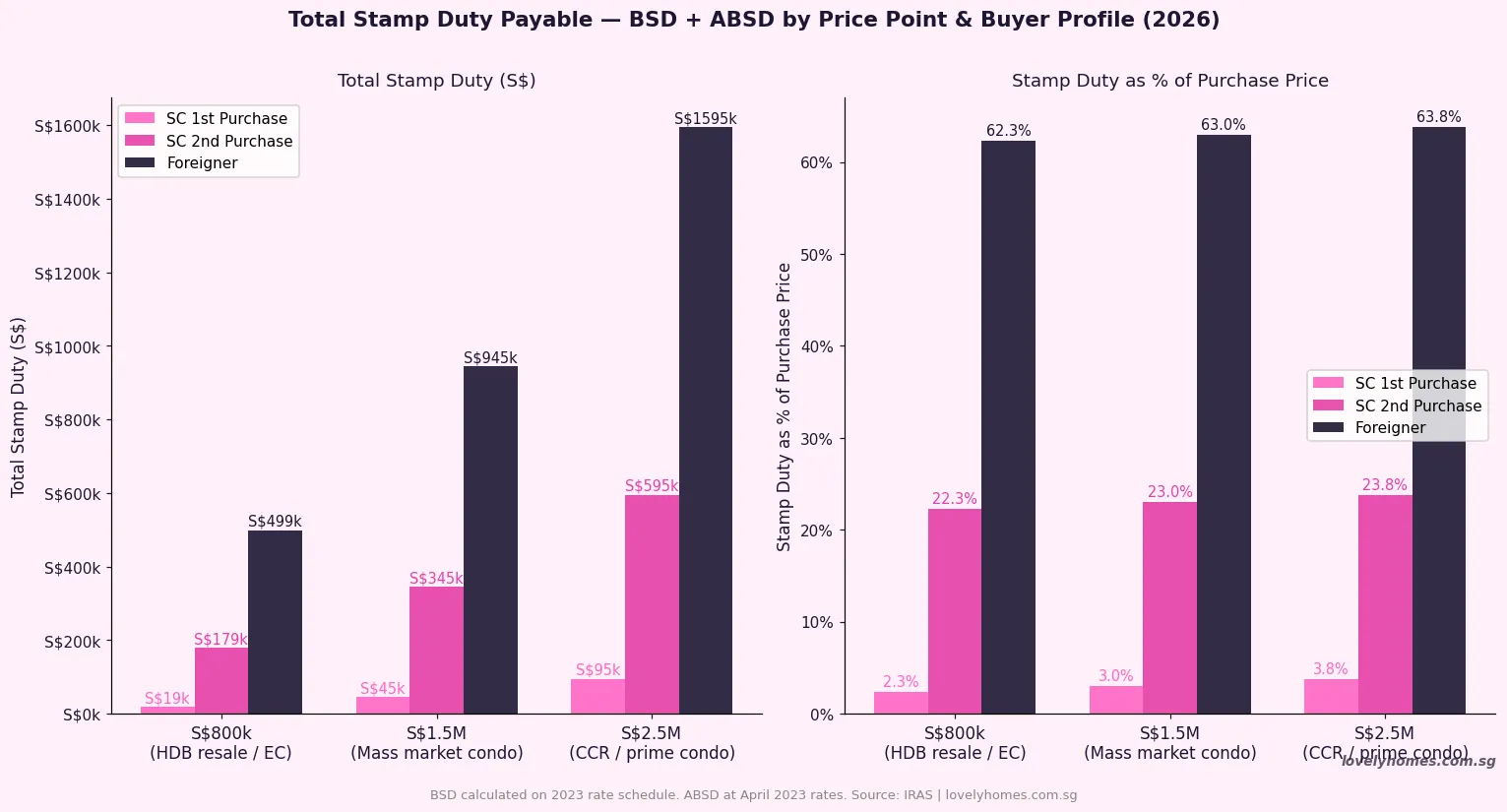

Additional Buyer’s Stamp Duty (ABSD) is the most significant item. Regardless of how large your CPF OA balance is, 100% of your ABSD liability must be paid in cash. At 20% for a Singapore Citizen purchasing a second residential property, this means a cash outlay of S$320,000 on a S$1.6M condo — before any other costs. Buyers who have not ring-fenced this amount routinely find themselves in difficulty at the 14-day ABSD payment deadline.

Cash Over Valuation (COV) in the HDB resale market is another cash-only item. Where a buyer agrees to pay above the HDB assessed value, the excess (COV) cannot be financed by either HDB loan or CPF.

Option fees, booking fees, good faith deposits — the initial 1% OTP fee and any booking deposit for new launches must be paid in cash. CPF cannot be applied until the formal sales process is completed.

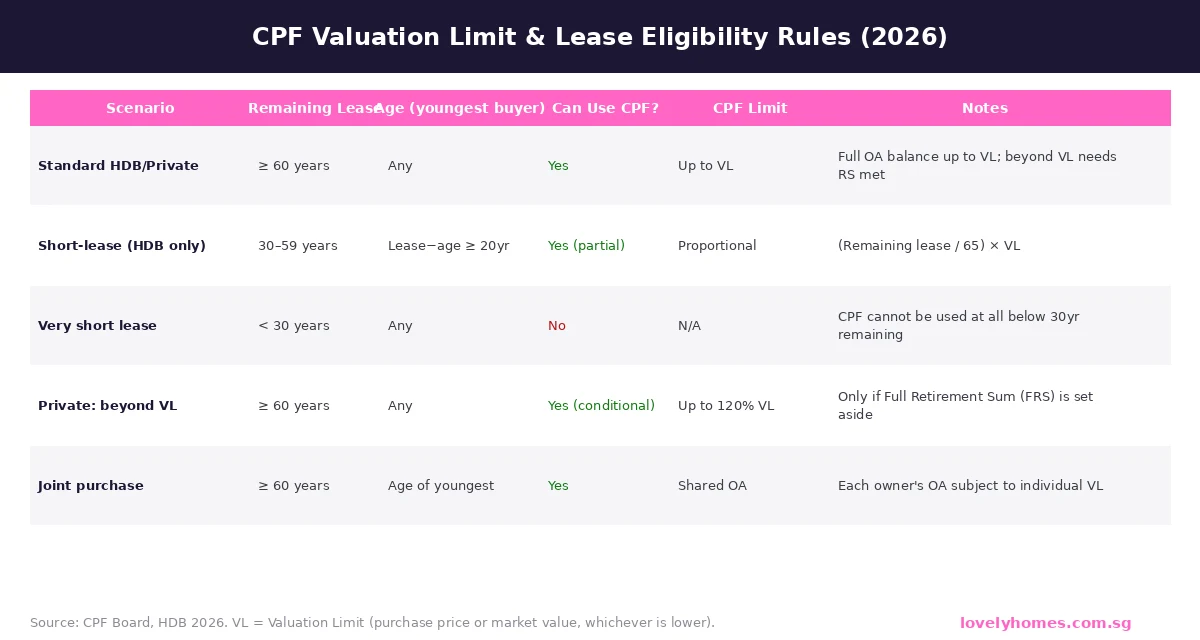

The Valuation Limit: How Much CPF Can You Use?

The Valuation Limit (VL) is the core rule governing total CPF usage on any single property. It is defined as the purchase price or the market value at the time of purchase, whichever is lower. You may use your CPF OA (and that of any co-owner or joint purchaser) to pay for the property purchase up to this limit.

Once cumulative CPF withdrawals (principal) reach the VL, no further CPF can be withdrawn for that property — unless you qualify for the 120% Valuation Limit extension.

To use CPF beyond the VL (up to 120% VL), the following conditions must be met:

- The property must have a remaining lease of at least 60 years.

- The property must have sufficient remaining lease to cover the youngest buyer to age 95.

- The buyer must have set aside or be setting aside the Full Retirement Sum (FRS) in their CPF SA and OA combined (S$213,000 as at 1 January 2026).

The Lease Rule: Remaining Lease and Age

CPF usage for property is not just limited by the VL — it is also constrained by the remaining lease of the property, particularly relevant for resale HDB flats with shorter tenures.

The general framework is: the property’s remaining lease, at the time of purchase, must be sufficient to cover the youngest buyer to age 95. Where the remaining lease falls short of 60 years, a pro-rated withdrawal limit applies. The formula used is: (Remaining Lease / 65 years) × Valuation Limit. Below 30 years of remaining lease, CPF cannot be used at all.

In practical terms, most buyers of resale HDB flats in mature estates should verify remaining lease carefully. A 50-year-old flat with 49 years remaining means the youngest buyer must be under 46 to receive full CPF access. This has become increasingly relevant as older HDB estates approach their tipping points.

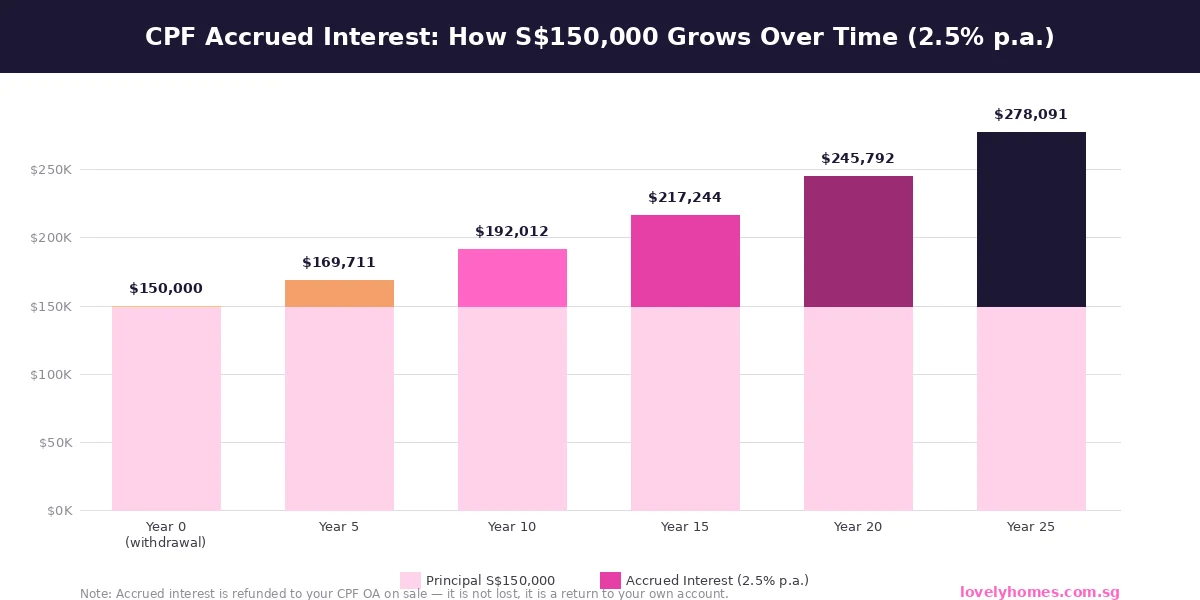

CPF Accrued Interest: The Most Misunderstood Rule

When you use CPF OA to buy a property, CPF Board tracks how much you have withdrawn. It then charges accrued interest on that amount at 2.5% per annum, compounded annually — the same rate your OA would have earned had the money remained in your account. The accrued interest accumulates throughout your period of ownership.

When you sell the property, the net sale proceeds must first be used to refund CPF the principal withdrawn plus all accrued interest. This refund goes back into your CPF OA — it is not a tax, fine, or fee. You are simply returning money to your own retirement savings with the interest it would have earned. The cash you receive after CPF refund, outstanding loan repayment, and transaction costs is your actual cash profit.

Many sellers are surprised by how large the CPF accrued interest sum is after 10–15 years of ownership. A S$150,000 CPF withdrawal grows to approximately S$191,000 after 10 years and S$244,000 after 20 years at 2.5% p.a. — meaning S$94,000 in accrued interest over 20 years returns to your CPF OA on sale.

Summary: CPF Rules at a Glance

| Rule / Limit | What It Means | Key Number (2026) | Source |

|---|---|---|---|

| Minimum Cash Downpayment (HDB Loan) | 10% of purchase price must be in cash; balance of 10% from CPF OA | 10% cash | HDB |

| Minimum Cash Downpayment (Bank Loan) | 5% cash; next 20% from CPF OA or cash | 5% cash | MAS / CPF Board |

| Valuation Limit (VL) | Total CPF withdrawable capped at lower of purchase price or market value | 100% VL | CPF Board |

| Beyond VL (120% cap) | Additional CPF use if FRS met and lease ≥ 60 years | 120% VL | CPF Board |

| Minimum Remaining Lease | Below 30 years: no CPF use; 30–59 years: pro-rated | 30 years | CPF Board |

| Accrued Interest Rate | 2.5% p.a. compounded on all OA withdrawals for housing | 2.5% p.a. | CPF Board |

| ABSD | Not payable via CPF — 100% cash | Cash only | IRAS |

| CPF Refund on Sale | Principal + accrued interest refunded to CPF OA from sale proceeds | Mandatory | CPF Board |

Worked Example: CPF in Action for a Resale HDB Purchase

The Tans — SC couple, combined income S$8,500/month, buying a 4-room resale flat in Tampines

Purchase price: S$640,000 | HDB valuation: S$625,000 | COV: S$15,000

Financing: HDB housing loan (LTV 80%) = S$500,000 loan; 20% downpayment = S$128,000

- Minimum cash downpayment (10%): S$64,000 in cash

- Remaining downpayment (10%): S$64,000 from CPF OA ✓

- COV S$15,000: Cash only (cannot use CPF) ✓

- BSD on S$640,000: S$12,600 — payable from CPF OA ✓

- Legal fees (est.): S$2,800 — payable from CPF OA ✓

- Total CPF used at purchase: S$64,000 + S$12,600 + S$2,800 = S$79,400

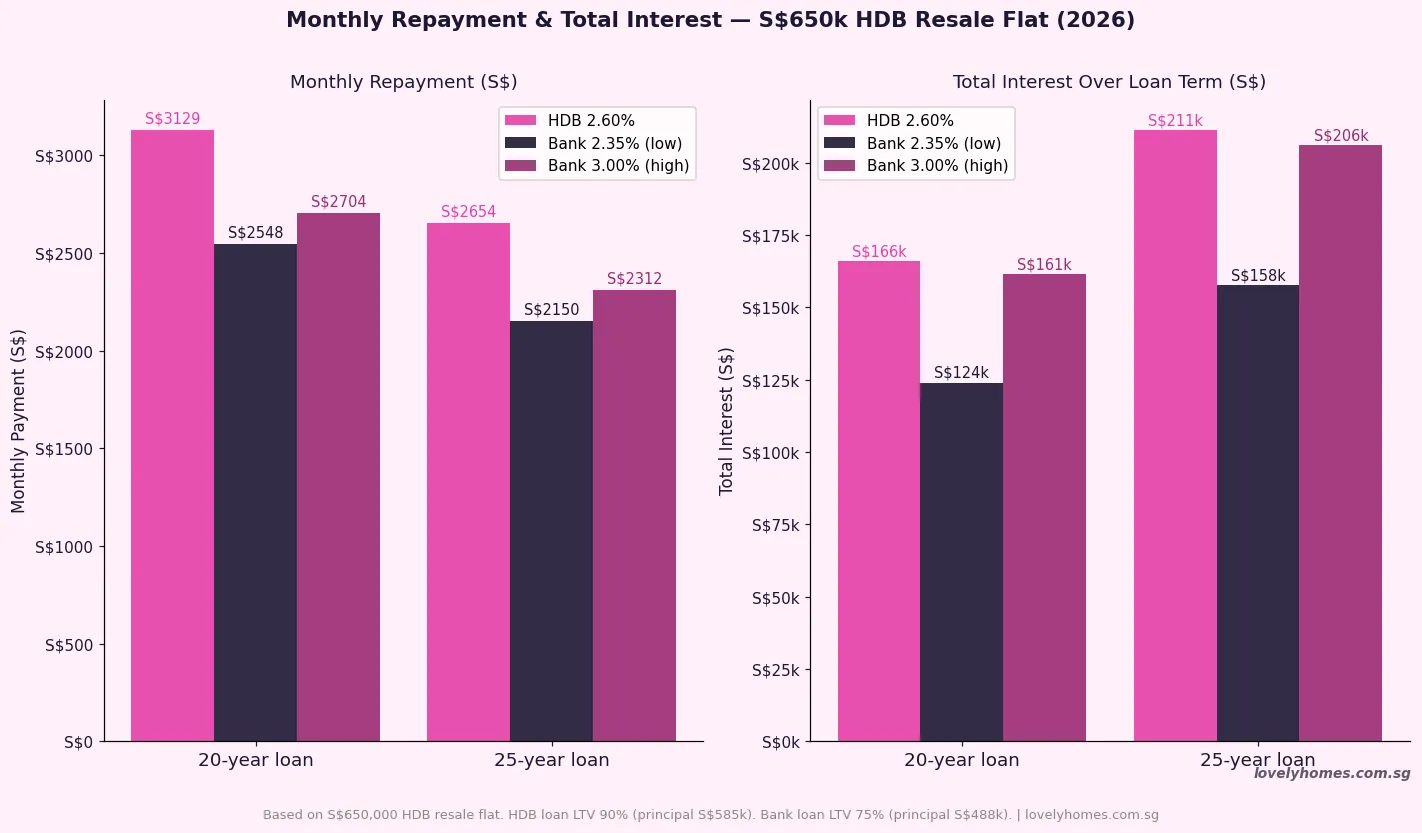

- Monthly instalment at HDB loan 2.60% over 25 years: S$2,275/month (MSR 26.8% ✓ under 30%)

After 8 years (selling):

- CPF principal withdrawn (downpayment + instalment contributions): S$218,000 (estimated)

- Accrued interest at 2.5% p.a. over 8 years: approx. S$24,500

- CPF refund required: S$242,500 (back into CPF OA — not a loss)

- Outstanding HDB loan at sale: ~S$384,000

- If sale price = S$780,000: Net cash after CPF refund + loan repayment: ~S$153,500

Why CPF Accrued Interest Is Not a Penalty

A common misconception is that CPF accrued interest represents a hidden cost of home ownership. It does not. The 2.5% p.a. accrued interest is precisely the return your OA would have earned had you not withdrawn the funds. When you sell and refund CPF, the money returns to your retirement account — meaning you have effectively used the property as an alternative vehicle for your CPF savings during the period of ownership.

The practical implication is that sellers should model their net cash position including the CPF refund, rather than treating the refund as pure cost. In a rising market, property appreciation typically far outstrips the accrued interest — the effective “cost” of using CPF is simply the opportunity cost of not having that money in your OA earning 2.5%. For most Singaporeans buying in a rising market, this is an excellent trade.

Where accrued interest does matter more acutely is for sellers in a flat or declining market, or for sellers who have held for a very long time at low appreciation. A 20-year hold with heavy CPF usage and modest appreciation can result in a smaller-than-expected cash payout — with the “profit” largely returned to CPF. This is not a loss, but it shapes the seller’s immediate liquidity position.

What Might Come Next for CPF and Property

CPF housing rules have been periodically tightened since the 2016 Enhanced Retirement Sum (ERS) framework was introduced. The Government’s stated trajectory is to gradually raise the retirement sums (BRS, FRS, ERS) each year by approximately 3.5%, which in turn raises the bar for the 120% VL extension. By 2030, the FRS is projected to exceed S$250,000, meaning buyers relying on the 120% rule will need substantially more CPF savings set aside.

There is ongoing policy discussion about the tension between property as a retirement asset and CPF as a retirement savings vehicle. The Retirement and Re-employment Act framework and the silver housing bonus schemes suggest the Government is nudging older Singaporeans to unlock property equity for retirement rather than relying on CPF alone. Buyers today should factor in that CPF usage rules may tighten further for properties with shorter remaining leases as the HDB lease decay issue becomes more pronounced in the 2030s and 2040s.

Frequently Asked Questions About CPF and Property

Can I use CPF to pay my ABSD?

No. The Additional Buyer’s Stamp Duty (ABSD) must be paid entirely in cash, regardless of how large your CPF OA balance is. IRAS has never permitted CPF to be used for ABSD since the duty was introduced in 2011. This is one of the most commonly misunderstood rules in Singapore property finance. If you are a Singapore Citizen buying a second property, you must have the full ABSD amount (currently 20% of purchase price) available in cash at the 14-day payment deadline after signing the Option to Purchase.

What happens to my CPF if I sell at a loss?

Even if you sell at a loss, you are still required to refund your CPF the principal withdrawn plus accrued interest — up to the available sale proceeds. If the net sale proceeds after repaying the outstanding loan are insufficient to cover the full CPF refund, you refund whatever is available. Any shortfall in the CPF refund does not need to be made up from your other savings — it is simply not refunded. However, this scenario (selling for less than you owe CPF + loan) is a genuine financial risk that buyers should model before purchasing.

Can I use my spouse’s CPF OA to buy property if they are not a co-owner?

No. Only registered co-owners of the property may use their CPF OA for that property. However, you can add a family member as a co-owner to allow their CPF to be used, subject to HDB and MAS eligibility rules. For private property, there is no prohibition on adding a spouse or family member as a co-owner, though stamp duty and legal implications should be reviewed with a solicitor. You cannot use someone else’s CPF even with their written consent unless they are a co-owner on the title.

Does buying a property with CPF affect my CPF LIFE annuity payout?

Indirectly, yes. Because CPF OA withdrawn for property (plus accrued interest) is refunded to CPF on sale, the funds that return to your account can then be transferred to the Retirement Account (RA) when you turn 55, boosting your CPF LIFE payout. However, if your property has not been sold by retirement age and you have drawn down heavily from OA, your CPF LIFE baseline payout may be lower if you have not independently met the Full Retirement Sum. The key planning point is to not assume that housing CPF withdrawals have no retirement impact — model your retirement savings position including expected CPF refund on eventual sale.

I bought an HDB flat and later upgraded to a private condo. Can I transfer remaining CPF usage from the HDB to the condo?

No. Your CPF housing withdrawals are tracked per property. When you sell the HDB flat, the CPF principal and accrued interest are refunded to your OA. Those funds are then available as fresh OA balance to be applied to the purchase of your next property. However, you do not “carry over” any unused CPF limit from the HDB flat — you start fresh with the new property’s own Valuation Limit. The refunded CPF balance effectively becomes available capital you can redeploy toward the condo’s downpayment and loan repayments.

Is there a limit on how much CPF I can use each month for loan repayments?

There is no separate monthly CPF withdrawal cap beyond the overall Valuation Limit rule. As long as your cumulative withdrawals (downpayment + BSD + legal fees + cumulative monthly instalments) have not reached the VL (or 120% VL if applicable), you may continue to pay monthly instalments from CPF OA. Once you hit the VL, all subsequent instalments must be paid in cash. For most buyers with moderate remaining OA balances or mid-priced properties, VL exhaustion typically occurs somewhere between 10 and 20 years of ownership — and only then does the monthly cash commitment escalate.

Can foreigners or PRs use CPF for property in Singapore?

Singapore Permanent Residents (PRs) contribute to CPF and may use their CPF OA to purchase HDB resale flats and private property, subject to the same VL, lease, and ABSD rules as Singapore Citizens. PRs face a 5% ABSD on their first residential property purchase (versus 0% for SC first property), which must be paid in cash. Foreigners are not CPF contributors and therefore have no CPF OA to access. All property acquisition costs for foreigners — downpayment, BSD, ABSD at 60%, legal fees — must be funded from cash or offshore financing.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Stamp Duty Calculator 2026: BSD and ABSD Explained

- HDB Downpayment Guide 2026: How Much Cash Do You Need?

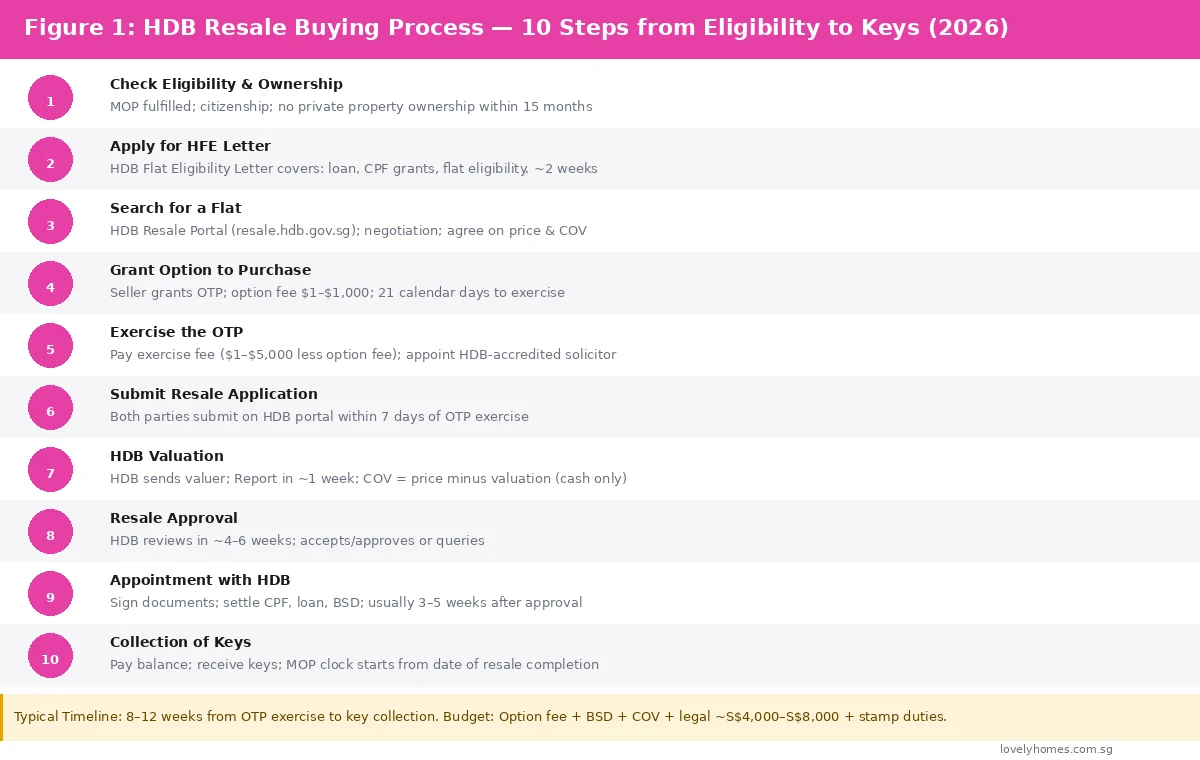

- Singapore HDB Resale Buying Process Guide 2026: Step-by-Step

- Singapore Home Mortgage Guide 2026: Fixed vs Floating, SORA Rates

- Singapore Property Cooling Measures 2026: Complete Guide

Disclaimer: This article is for general informational purposes only. CPF housing rules, valuation limits, and retirement sum thresholds are updated periodically by the CPF Board and may change after the publication date of this article. All figures reflect the framework as at 3 July 2026. Readers should verify current rules at cpf.gov.sg and consult a licensed financial adviser or HDB-appointed solicitor before making any property purchase or CPF withdrawal decision. LovelyHomes does not provide financial or legal advice.