Quick Answer: URA 2H2026 GLS Programme — Key Headlines

Announced: 3 June 2026 by the Urban Redevelopment Authority (URA) and Ministry of National Development.

Total supply (2H2026): 9,200 private residential units, 188,100 sqm GFA of commercial space, and 970 hotel rooms across all Confirmed and Reserve List sites.

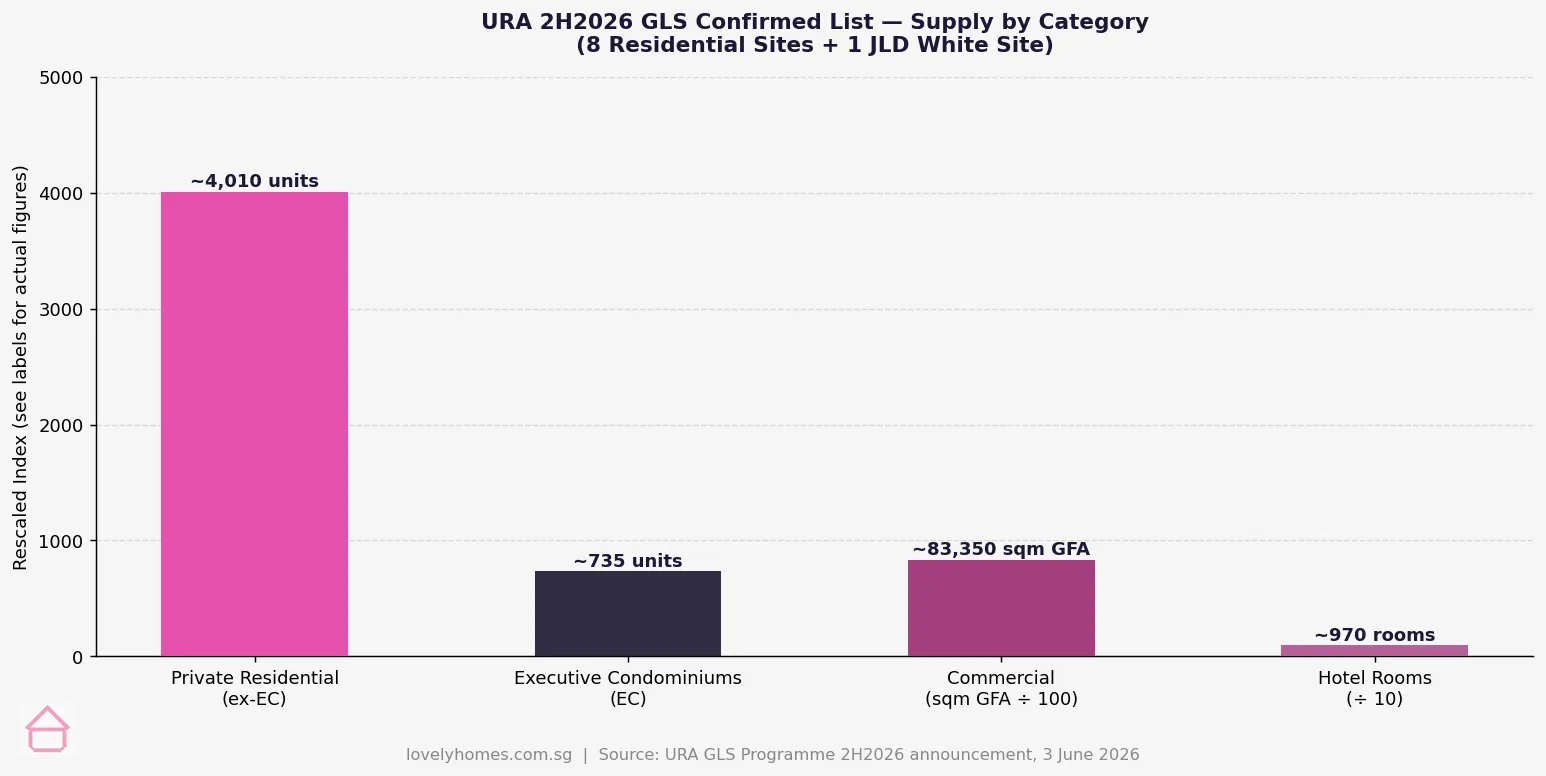

Confirmed List: 9 sites — 8 private residential (including 1 EC site) and 1 white site — yielding approximately 4,745 residential units and 83,350 sqm GFA of commercial space.

Jurong Lake District white site: To be launched for tender in July 2026; up to 1,200 private residential units, minimum 40,000 sqm office space, and 44,000 sqm complementary uses.

Pipeline total: With the 2H2026 injection, the overall private residential (including EC) supply pipeline rises to approximately 61,000 units from approximately 57,000 units.

Market signal: The Government signals continued commitment to sustaining adequate private housing supply and accelerating the development of Jurong Lake District as Singapore’s second CBD.

URA Releases 2H2026 GLS Programme: What It Means for Singapore Property

The Urban Redevelopment Authority (URA) announced Singapore’s Government Land Sales (GLS) programme for the second half of 2026 on 3 June 2026, releasing nine sites on the Confirmed List and thirteen sites on the Reserve List. The announcement is a significant policy signal, sustaining a high level of private housing supply while accelerating one of Singapore’s most ambitious urban development projects — the Jurong Lake District (JLD) transformation.

GLS programmes are released twice yearly (for 1H and 2H) and represent the Government’s primary tool for regulating private housing land supply. Sites on the Confirmed List are released for tender regardless of market conditions; those on the Reserve List are launched only when a developer submits an acceptable bid, providing a buffer of supply that can be activated when demand warrants.

2H2026 Confirmed List: Nine Sites, 4,745 Units

Figure 1: URA 2H2026 GLS Confirmed List supply breakdown — 8 residential sites (including 1 EC site) plus the Jurong Lake District white site, yielding approximately 4,745 private residential units and 83,350 sqm of commercial GFA. Source: URA, 3 June 2026.

The nine Confirmed List sites announced for 2H2026 can collectively yield approximately 4,745 private residential units (including 735 executive condominium units) and 83,350 sqm GFA of commercial space. The eight private residential sites include a mix of Outside Central Region (OCR), Rest of Central Region (RCR), and Core Central Region (CCR) locations, sustaining the supply diversity that has characterised recent GLS programmes. A single executive condominium (EC) site is included — responding to persistent demand for the EC tenure from HDB upgraders priced out of the full private market.

Taken together with the thirteen Reserve List sites — which can yield an additional approximately 4,455 residential units, 104,750 sqm of commercial GFA, and 970 hotel rooms if triggered by developer demand — the 2H2026 programme adds meaningful supply headroom to Singapore’s already robust private housing pipeline.

The Jurong Lake District White Site: Singapore’s Second CBD Moves Forward

The centrepiece of the 2H2026 programme is the Jurong Lake District (JLD) white site, scheduled for tender launch in July 2026. The JLD white site is a large, mixed-use parcel with a total development potential of approximately 186,000 sqm GFA, comprising:

A minimum of 40,000 sqm of office space (Grade A commercial)

Up to 1,200 private residential units

Approximately 44,000 sqm GFA of complementary uses (retail, hospitality, or civic)

The Government has invested heavily in JLD infrastructure ahead of this white site release — the revitalised 90-hectare Jurong Lake Gardens, the new Science Centre at Jurong Lake, the Jurong Gateway Hub, and two new MRT lines: the Jurong Region Line (JRL), opening in stages from approximately mid-2028, and the Cross Island Line (CRL) Phase 2, expected approximately 2032. These infrastructure investments significantly enhance the district’s attractiveness to both commercial occupiers and residential buyers, and represent the Government’s long-term commitment to decentralising Singapore’s economic activity away from the Raffles Place/Marina Bay corridor.

For property investors, the JLD white site is a landmark tender — likely to attract significant interest from Singapore’s major listed developers and potentially joint ventures with international capital partners. The development, once built, is expected to set a new benchmark for integrated mixed-use development outside the CCR and will meaningfully reshape the Jurong Lake corridor pricing landscape.

What This Means for Property Buyers and Investors

Stakeholder

Key Implication

Timing

Private property buyers

Confirmed List sites will produce new launches over 2027–2028. Buyers should monitor tender awards and expected launch timelines for preferred locations.

Tender launches from July 2026

HDB upgraders (EC buyers)

One EC site on the Confirmed List suggests a new EC project for 2027 application. Income ceiling remains S$16,000/month.

EC launch approximately 2027

Jurong/JLD investors

JLD white site signals the next phase of JLD development. Properties in Jurong (D22) may see re-rating as the master plan becomes reality.

JLD white site tender July 2026

Commercial space occupiers

83,350 sqm of new commercial GFA in confirmed sites (plus JLD 40,000 sqm office minimum). Grade A office supply will expand from approximately 2028.

Construction 2026–2028

Developers

High confirmed supply indicates Government policy intent to keep private housing prices in check. Competitive land pricing likely to remain disciplined.

Ongoing

Context: Overall Supply Pipeline Reaches 61,000 Units

With the 2H2026 programme confirmed, the total supply of private residential units (including ECs) in Singapore’s overall development pipeline rises to approximately 61,000 units — up from approximately 57,000 units before the announcement. This pipeline encompasses units under construction, those with planning approvals, and those with awarded GLS or en bloc land but not yet commenced. The Government considers a pipeline of approximately 60,000–65,000 units to be consistent with market balance given Singapore’s typical absorption rate of 8,000–12,000 units per year in private completions and sales.

The sustained high supply — following similarly large GLS programmes in 1H2026, 2H2025, and 1H2025 — reflects the Government’s ongoing commitment to ensuring that private housing price growth remains moderate and accessible. Property analysts note that the 2H2026 programme, while substantial, is not materially larger than recent halves — suggesting a deliberate policy of continuity rather than a supply shock or withdrawal.

Frequently Asked Questions

What is a GLS Confirmed List site and how is it different from a Reserve List site?

A Confirmed List site is released for public tender by the Government at a predetermined date, regardless of prevailing market conditions. This ensures a baseline level of private housing land supply even during market downturns. A Reserve List site, by contrast, is only placed on the market if a developer submits an application to tender the site at a price that meets the Government’s minimum threshold — effectively providing an on-demand supply buffer that is activated by real developer appetite. Reserve List sites give the Government flexibility to release additional supply quickly when demand is strong without committing to an inflexible fixed programme.

When will the Jurong Lake District white site tender close and who will likely bid?

The JLD white site is scheduled to be launched for tender in July 2026. Tender close dates for major white sites are typically set 10–14 weeks after launch, suggesting a likely close in September or October 2026. Given the scale and complexity of the site — mixed-use with mandatory minimum office space — bidders are likely to be Singapore’s largest listed developers (CapitaLand Development, City Developments, UOL Group, GuocoLand) potentially in joint venture with institutional capital partners. International consortia have bid on previous JLD sites. The winning bid will set a new benchmark land rate for the JLD corridor and signal developer confidence in Singapore’s Grade A office and premium residential demand.

How does the 2H2026 GLS programme affect private property prices?

The release of a large GLS Confirmed List — 4,745 units in addition to the existing pipeline — is generally a moderating influence on private property price growth, as it ensures developers have sufficient access to land without excessive competition for a scarce resource. However, the near-term effect on prices is limited: GLS land requires 2–4 years from tender award to new-launch sales, so 2H2026 sites will contribute to supply primarily in 2028–2030. More immediately, the JLD white site signals long-term confidence in Singapore’s property market fundamentals and the Jurong corridor specifically, which is likely to be read positively by investors already holding or considering D22 assets.

This article is for general informational and editorial purposes only. GLS programme details, site specifications, tender timelines, and supply figures are based on URA announcements as at 3 June 2026 and are subject to revision. Property buyers and investors should conduct independent due diligence and consult licensed property advisers and financial professionals before making property decisions. For official GLS information, refer to the Urban Redevelopment Authority at ura.gov.sg.

Award date: 30 March 2026 by the Urban Redevelopment Authority (URA) under the 1H 2026 Confirmed List.

Location: District 5 (D05), Queenstown Planning Area — RCR (Rest of Central Region), near Commonwealth MRT (EWL) and one-north MRT (CCL).

Site: Approximately 15,700 sqm, GPR 3.5, yielding an estimated 285–320 residential units on a 99-year leasehold tenure.

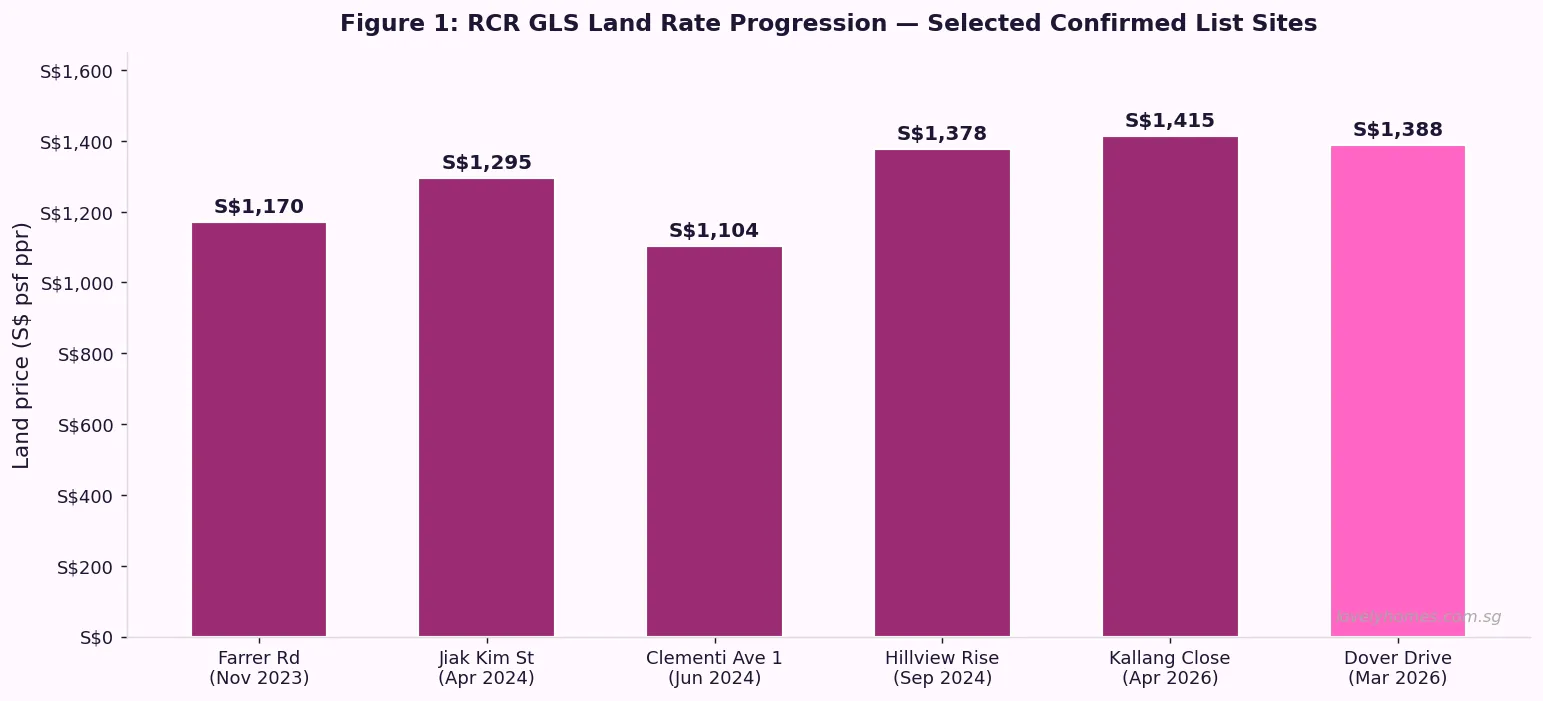

Land price benchmark: Industry reports indicate the site was awarded at approximately S$1,388 psf ppr — consistent with recent RCR confirmed-list benchmarks (Kallang Close: S$1,415 psf ppr, April 2026).

Estimated launch price: S$1,950–S$2,200 psf, translating to approximately S$1.6M–S$2.5M for a 1- to 3-bedroom unit.

Investment case: The one-north employment node (Biopolis, Fusionopolis, Mediapolis) anchors strong rental demand; gross yields of 3.2–3.8% are achievable for well-located 1- and 2-bedroom units.

ABSD note: Singapore Citizens purchasing their first property pay zero ABSD; second-property SC buyers face 20% ABSD on the full purchase price.

Timeline: Construction typically takes 3–4 years post-tender; an estimated launch window of Q3–Q4 2027 is plausible.

What Is the Dover Drive GLS Site?

The Dover Drive Government Land Sales (GLS) site is a residential 99-year leasehold parcel released by the URA under Singapore’s 1H 2026 Confirmed List — the government’s bi-annual programme of land tenders intended to calibrate private housing supply. Situated along Dover Road in the Queenstown Planning Area (District 5), the site occupies a prime RCR position with direct connectivity to the East-West Line (EWL) at Commonwealth MRT and the Circle Line (CCL) at one-north MRT, making it one of the more strategically located parcels in the 1H 2026 tranche.

The tender closed on 26 March 2026 and the award was announced by URA on 30 March 2026. The land parcel measures approximately 15,700 sqm with a plot ratio (GPR) of 3.5, giving a maximum gross floor area (GFA) of roughly 54,950 sqm. Assuming an average unit size of 65–70 sqm net sellable, the site is expected to yield between 285 and 320 residential units, with a likely mid-to-high-rise tower configuration of 20–30 storeys.

Dover Road itself is a quiet, tree-lined arterial that runs through one of Singapore’s most established educational and research corridors — home to Ngee Ann Polytechnic, National University of Singapore (NUS), Anglo-Chinese School (Independent), NUS High School of Mathematics and Science, and the sprawling one-north cluster comprising Biopolis, Fusionopolis, Mediapolis, and the JTC LaunchPad. This employer and educational density creates structural demand for rental accommodation that underpins the investment case for any new launch in the area.

Figure 1: RCR confirmed-list GLS land rates, selected sites 2023–2026. Dover Drive (March 2026) is consistent with the RCR land price trajectory. Source: URA GLS programme data; industry estimates.

Why the Dover Drive GLS Land Rate Matters for RCR Pricing

Land price benchmarks set by GLS tenders directly feed into developers’ breakeven calculations, which in turn set the floor for launch prices. Understanding this chain of cost-pass-through is essential for any buyer or investor evaluating a new launch project.

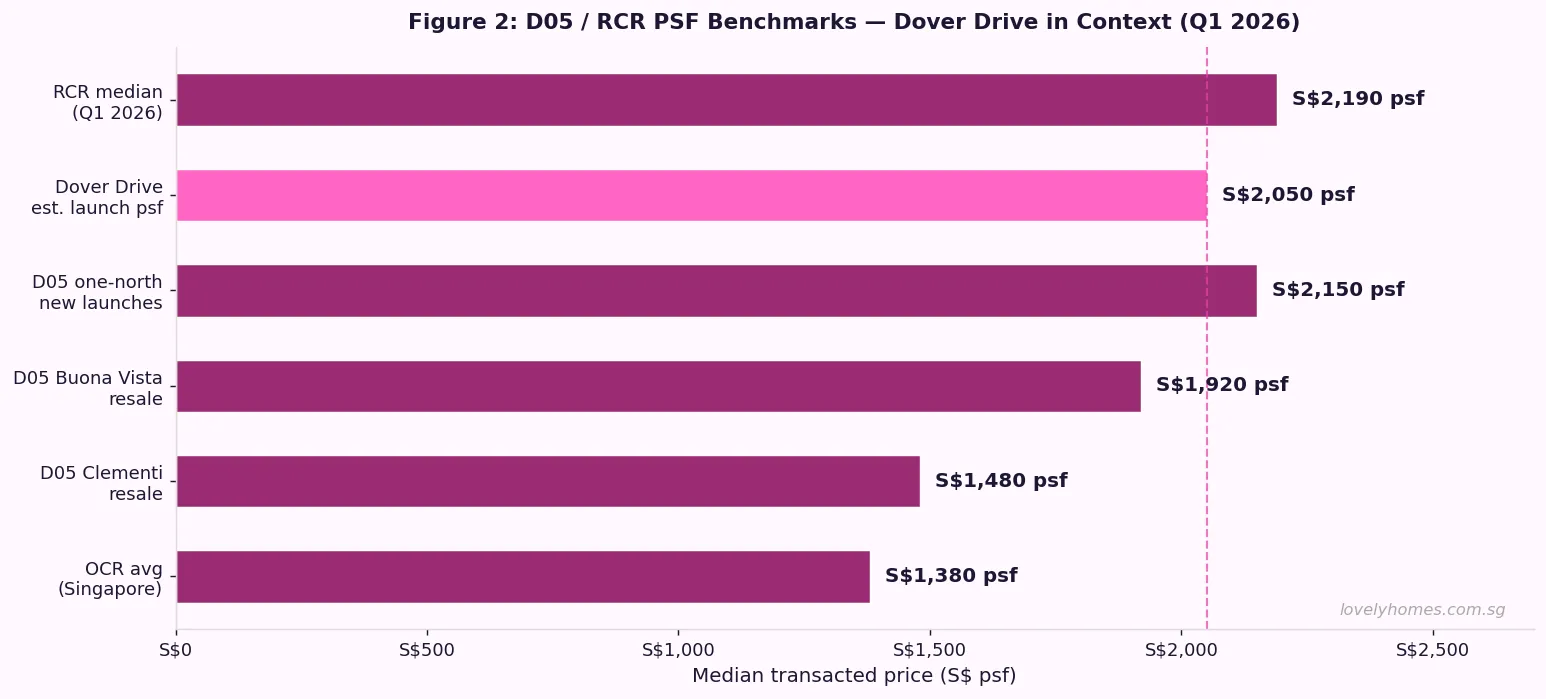

Industry analysts typically model a developer’s cost stack as follows: land acquisition + construction costs + professional fees + financing costs + developer’s margin (typically 12–18%). For a site awarded at approximately S$1,388 psf ppr, applying standard RCR assumptions yields an estimated breakeven of around S$1,800–S$1,950 psf. This directly informs the expected launch price range of S$1,950–S$2,200 psf, which would place Dover Drive’s future project solidly within the upper end of the RCR market — above Clementi resale averages (S$1,480 psf) but below CCR new launches at S$3,000+ psf.

Comparable RCR benchmarks further contextualise this data point:

Kallang Close GLS (awarded April 2026): S$1,415 psf ppr — Frasers-Mitsubishi consortium, RCR Kallang.

Hillview Rise GLS (awarded September 2024): S$1,378 psf ppr — OCR-adjacent, Bukit Timah fringe.

Clementi Avenue 1 GLS (awarded June 2024): S$1,104 psf ppr — pure OCR, lower land cost.

Dover Drive’s estimated rate of S$1,388 psf ppr is consistent with RCR pricing dynamics — meaningfully above Clementi’s OCR land cost but below the S$1,491 psf ppr that Sim Lian paid for the Holland Plain (CCR) site in May 2026. The distinction matters: buyers purchasing at Dover Drive’s expected launch price are paying for a genuine RCR location with CCR-adjacent amenities, at a price point below CCR launch levels.

Figure 2: D05/RCR PSF benchmarks, Q1 2026. The Dover Drive estimated launch price sits between Clementi resale and established one-north new-launch levels. Sources: URA Realis, industry estimates.

The one-north and Educational Corridor — Rental Demand Drivers

Any investment analysis of Dover Drive begins with an honest audit of who will actually rent the units. The answer, in this precinct, is unusually clear: the one-north employment cluster is one of Singapore’s highest-density concentrations of knowledge-economy jobs. Biopolis alone houses more than 50 biomedical research institutes; Fusionopolis is home to agencies including the Infocomm Media Development Authority (IMDA), A*STAR, and dozens of private-sector technology firms; Mediapolis anchors Singapore’s media and digital-content industry; and the JTC LaunchPad at one-north houses hundreds of startups. The combined workforce exceeds 50,000 employees — many of them well-paid professionals who prefer to rent within walking or short-MRT distance of the office.

Layered on top of this is the NUS student and postdoctoral research community. NUS enrolls approximately 40,000 students annually, with a significant proportion drawn from overseas or from Singapore households that prefer students to live near campus. The NUS High School of Mathematics and Science and ACS(I) add another demographic of parents willing to pay a premium for proximity to these schools.

This confluence of rental demand drivers — high-income working professionals at one-north and a large academic community at NUS — provides the structural basis for Dover Drive’s rental yield projections of 3.2–3.8% gross for 1- to 2-bedroom units. For a 1BR unit estimated at S$1.65M, an annual rental income of approximately S$58,000 (S$4,800/month) would represent a gross yield of 3.5%. By comparison, the broader RCR median gross yield for private condos in Q1 2026 sits at approximately 3.3%, suggesting Dover Drive’s micro-location may support a modest yield premium.

Summary: Key Site Parameters and Investment Metrics

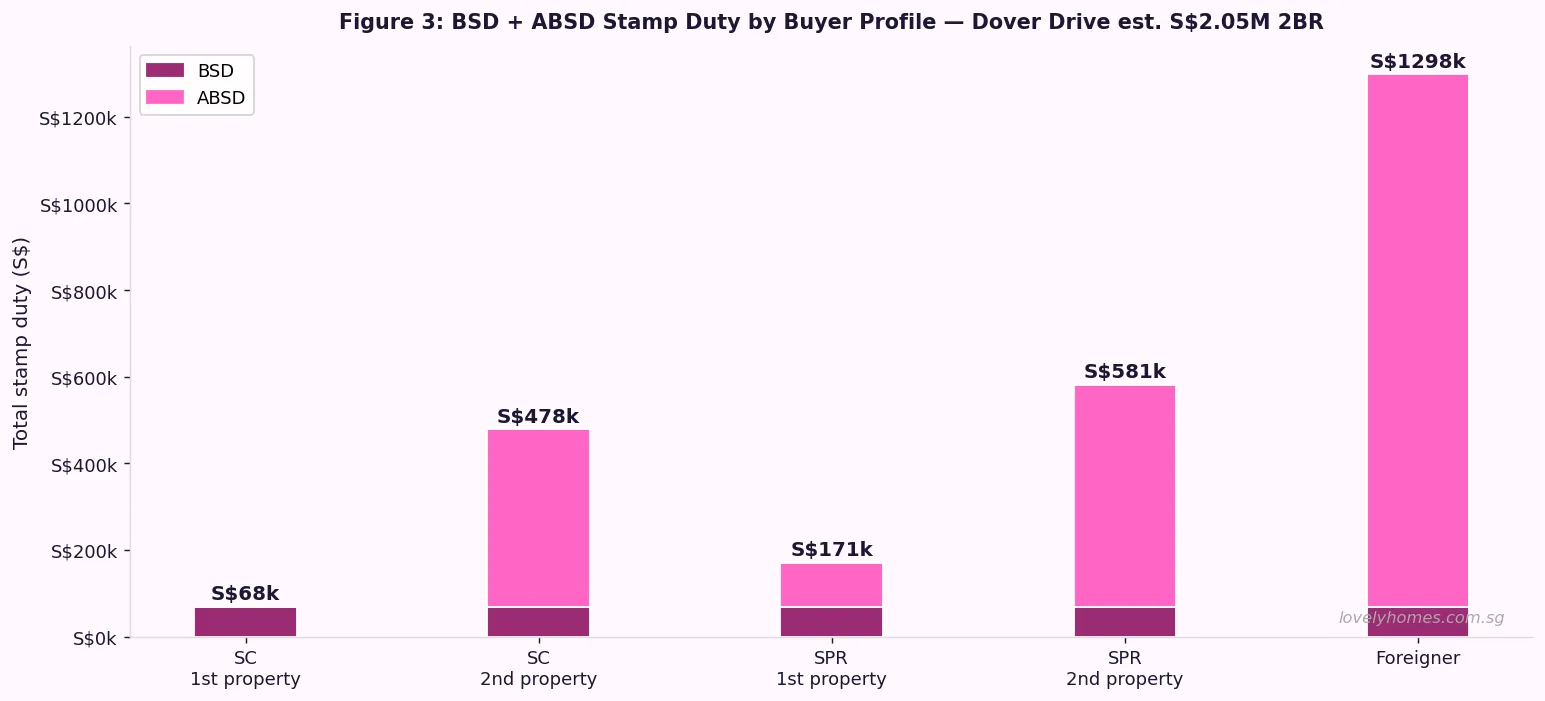

Stamp duty is a material cost element that varies significantly by buyer profile. For a Dover Drive 2-bedroom unit estimated at S$2.05M, the total stamp duty picture looks as follows:

Figure 3: Total stamp duty (BSD + ABSD) by buyer profile for an estimated S$2.05M 2-bedroom unit at Dover Drive. BSD on S$2.05M = S$68,400; ABSD rates per IRAS schedule effective 27 April 2023. Source: IRAS, LovelyHomes calculations.

The Buyer’s Stamp Duty (BSD) is payable by all buyers on a progressive scale administered by the Inland Revenue Authority of Singapore (IRAS). For a S$2.05M purchase, BSD is calculated as: 1% on the first S$180,000 + 2% on the next S$180,000 + 3% on the next S$640,000 + 4% on the next S$500,000 + 5% on the remaining S$550,000 = S$68,400 BSD.

Singapore Citizens (SC) purchasing their first residential property pay zero Additional Buyer’s Stamp Duty (ABSD) — making their total stamp duty S$68,400 (3.3% of purchase price). SC purchasing a second property face 20% ABSD (S$410,000) on top of BSD, bringing total stamp duty to S$478,400 — a 23.3% effective rate that significantly alters the investment calculus. Foreign purchasers face a 60% ABSD rate under the April 2023 cooling measures, amounting to S$1,230,000 on a S$2.05M unit — effectively making Dover Drive economically inaccessible to most foreigners absent exceptional circumstances.

Worked Example: Mr and Mrs Yeo — SC Couple, First Property

Worked Example — SC Couple, First Property, Dover Drive 2BR S$2.05M

Profile: Mr and Mrs Yeo, both Singapore Citizens, combined monthly income S$14,000. First residential property purchase. Both currently renting.

Purchase price: S$2,050,000

BSD: S$68,400 (IRAS progressive scale)

ABSD: S$0 (SC first property)

Total stamp duty: S$68,400

Bank loan (75% LTV): S$1,537,500

Cash / CPF downpayment (25%): S$512,500

→ Minimum cash (5% of purchase price): S$102,500

→ Balance via CPF OA: up to S$410,000

At 3.0% interest over 25 years, the Yeos’ monthly repayment of S$7,291 sits comfortably within the TDSR threshold of S$7,700 (55% of S$14,000 joint income). Their CPF Ordinary Account savings of approximately S$200,000 combined can fund part of the S$410,000 CPF portion of the downpayment, with the remainder drawn from cash savings or supplementary CPF contributions over time.

Estimated gross rental yield if rented out instead of owner-occupied: 3.5% p.a. (~S$5,979/month). Net yield after property tax and maintenance: approximately 2.8%.

What This Means for D05 Buyers and the Broader RCR Market

The Dover Drive GLS award is significant beyond the single site. As one of only a handful of RCR parcels released under the 1H 2026 Confirmed List, its land price sets a reference point that influences pricing expectations for the entire D05/RCR resale and new-launch market. Sellers of resale condos in the Commonwealth, Holland Road, and Queenstown sub-markets now have a credible data point to anchor asking prices — and buyers negotiating resale prices will find it harder to push below this implied new-launch floor.

For the broader Singapore property market, the moderate RCR land rate — lower than the CCR Holland Plain rate of S$1,491 psf ppr — signals that developers retain some pricing discipline even in sought-after corridors. The government’s continued steady release of GLS land is its primary mechanism for moderating price growth, and the 1H 2026 programme’s 3,940 confirmed-list private residential units (down from 5,030 in 2H 2025) suggests a deliberate calibration toward managing supply without flooding the market.

What Might Come Next — D05 Outlook

Looking ahead, several catalysts could further support property values in the Dover Drive / D05 corridor. The Greater Southern Waterfront (GSW) masterplan — which progressively redevelops the southern coastline from Pasir Panjang to Marina East — extends northward influence into the Queenstown and Buona Vista sub-markets. The planned relocation of Pasir Panjang Terminal operations would unlock significant waterfront land, adding long-term capital appreciation potential to nearby residential markets.

On the infrastructure side, the Cross Island Line (CRL), while primarily serving the north-eastern and eastern corridors in its Phase 1 (2030), has a future stage tentatively planned to connect through the one-north cluster — a development that, if confirmed, would add a third MRT line to the already well-served D05 corridor. Any CRL confirmation would likely catalyse a rerating of D05 property values.

However, buyers should also consider the risks. At an estimated S$1,950–S$2,200 psf, Dover Drive’s future project will be priced at a meaningful premium to current D05 resale condos (~S$1,480–S$1,920 psf), requiring a positive view on continued capital appreciation. Macroeconomic headwinds — including the possibility of higher-for-longer interest rates and global growth slowdowns — could dampen transaction volumes and delay capital appreciation timelines. As with all 99-year leasehold properties, buyers should factor in lease-decay risk on a 30–40 year holding horizon.

FAQ — Dover Drive GLS and D05 Property

When will the Dover Drive GLS development be launched for sale?

Following the tender award on 30 March 2026, the winning developer typically requires 12–18 months for design, planning approval, and showflat construction. A public launch in Q3–Q4 2027 is a plausible estimate, though this depends on the developer’s sales strategy and market conditions at the time. Watch URA’s Urban Redevelopment Authority website and the developer’s official project website for the official preview and balloting dates.

Is Dover Drive OCR or RCR, and does it matter?

Dover Drive falls within the Rest of Central Region (RCR) — a classification that sits between the Outside Central Region (OCR, predominantly HDB heartlands and suburban private estates) and the Core Central Region (CCR, the prime districts D9/D10/D11). RCR typically offers better connectivity and amenities than OCR at a price premium, but without the full CCR price point. For foreign buyers, ABSD applies equally across all regions at 60% (effective 27 April 2023), so the OCR/RCR/CCR distinction does not affect ABSD liability — only the underlying purchase price does.

Can a Singapore Permanent Resident (SPR) buy at Dover Drive?

Yes. Singapore Permanent Residents (SPR) may purchase private condominiums, including any new launch at the Dover Drive site, without SLA approval — unlike landed property. An SPR purchasing their first residential property pays 5% ABSD, while an SPR buying a second or subsequent property faces 25% ABSD. SPRs may use their CPF Ordinary Account savings for the downpayment and monthly instalments, subject to the CPF housing withdrawal limits and the property’s remaining lease (99-year leasehold from 2026 means the CPF Valuation Limit is unlikely to be a constraint for most SPRs of working age).

How does Dover Drive compare to the Holland Plain GLS (D10, CCR)?

The Holland Plain GLS site (awarded 12 May 2026 to Sim Lian, D10 CCR) is a meaningfully different proposition. At S$1,491 psf ppr land rate versus Dover Drive’s estimated S$1,388 psf ppr, Holland Plain commands a ~7% land cost premium — which flows through to an expected launch price range of S$3,100–S$3,800 psf versus Dover Drive’s S$1,950–S$2,200 psf. Holland Plain is freehold, a significant tenure advantage for long-term holders. Dover Drive offers a far more accessible absolute entry price (S$1.6M–S$2.5M for 1–2BR vs S$3M+ at Holland Plain) and a larger pool of qualifying buyers under TDSR constraints. The rental demand profiles also differ: Holland Plain targets expatriate families and CCR high-net-worth buyers, while Dover Drive targets the one-north professional and NUS academic community.

What schools are near Dover Drive?

The Dover Drive corridor is exceptionally well served by reputable schools. Within 1–2km: NUS High School of Mathematics and Science (gifted programme), Anglo-Chinese School (Independent) (ACS(I), IBDP and O-Level), and Ngee Ann Polytechnic (tertiary). Within 2–3km: New Town Primary School and Queenstown Primary School (both established neighbourhood schools). The broader D05 area also has access to Henry Park Primary School (within 1km of Holland Village, approximately 2.5km from Dover Drive) and National University of Singapore (walking distance). This educational density is a strong structural driver of rental demand from both families and the academic community.

What happens to existing D05 resale condo prices when Dover Drive launches?

Historically, a new GLS launch at a higher per-psf price than the surrounding resale market creates an upward anchoring effect on resale prices. Sellers and agents use the new launch’s pricing as a reference point to justify higher resale asking prices. In the near term (pre-launch), resale condos in the Commonwealth, Ghim Moh, and Holland Road area may see modest appreciation as market participants anticipate the new benchmark. However, any uplift is not guaranteed — if the new launch is poorly received or market conditions weaken, the anticipated anchor effect may not materialise. Buyers should evaluate each resale transaction on its own merits rather than assuming new-launch pricing always lifts the entire sub-market.

Can I use CPF to pay for Dover Drive?

Yes, subject to CPF Board rules on housing withdrawals. For a 99-year leasehold property where the remaining lease covers the buyer’s age to at least 95 years (i.e., at least 95 minus current age years remaining at the point of purchase), the full CPF housing withdrawal limit applies. For a 2026 purchase, the 99-year lease runs to 2125 — well beyond the 95-year threshold for all working-age buyers. CPF Ordinary Account (OA) savings may be used for the downpayment (above the minimum cash requirement of 5% of purchase price), monthly loan instalments (subject to the Valuation Limit and Withdrawal Limit), and stamp duty. Note that CPF accrued interest (currently 2.5% p.a. OA rate) must be returned to the CPF account on sale, which reduces net cash proceeds from any future disposal.

Disclaimer: This article is produced for general informational purposes only and does not constitute financial, legal, or property investment advice. All figures relating to the Dover Drive GLS bid price, estimated launch price, and investment returns are based on industry estimates and publicly available URA GLS programme data as at May 2026; actual figures will vary and should be verified with official sources including the URA (ura.gov.sg), IRAS (iras.gov.sg), and CPF Board (cpf.gov.sg). Readers are strongly encouraged to engage a licensed conveyancer, financial adviser, and HDB/CPF officer before making any property purchase decision.

⚡ Quick Answer — URA Berlayar Drive & New Upper Changi Road GLS Launch

The Urban Redevelopment Authority (URA) launched two new residential Government Land Sales (GLS) sites in May 2026 — at Berlayar Drive (District 3, Bukit Merah) and New Upper Changi Road (District 16, Bedok).

Berlayar Drive is a 271,929 sqft site with GPR 1.4, expected to yield ~415 homes; tender closes 4 August 2026.

New Upper Changi Road is a larger 331,194 sqft site with GPR 2.8, potentially yielding ~1,010 homes — a future mega-development; tender closes 1 September 2026.

Both sites are 99-year leasehold; no land price benchmark yet — developers submit sealed bids by the respective tender close dates.

Berlayar Drive sits within the Greater Southern Waterfront (GSW) transformation corridor — one of Singapore’s most significant long-term urban rejuvenation projects.

New Upper Changi Road is the first large OCR residential GLS site in Bedok since the Bayshore Drive parcel (Vela Bay, awarded 2025), bringing much-needed OCR supply to the eastern region.

Together, both sites add 1,425 estimated units to the 1H 2026 GLS pipeline, contributing to MAS and URA’s stated goal of maintaining adequate private housing supply.

URA Launches Two New Residential GLS Sites in May 2026

The Urban Redevelopment Authority (URA) released two residential sites for sale by public tender in May 2026 under the 1H 2026 Government Land Sales (GLS) programme — at Berlayar Drive in Bukit Merah and New Upper Changi Road in Bedok. The launch adds approximately 1,425 private homes to the confirmed list supply pipeline, reinforcing the government’s commitment to ensuring adequate housing supply as private residential prices continue to be closely monitored by both URA and the Monetary Authority of Singapore (MAS).

The two sites are markedly different in character. Berlayar Drive is a smaller, low-density waterfront parcel within the emerging Berlayar estate — part of the broader Greater Southern Waterfront transformation masterplan. New Upper Changi Road is a high-density OCR site that could become one of Singapore’s largest single condominium developments, with analysts projecting 1,000 or more units. Both sites will be sold by closed tender, with bids evaluated on the highest price basis subject to the technical conditions of tender.

Figure 1: Site-by-site comparison — Berlayar Drive (D3 RCR, ~415 units, tender 4 Aug 2026) vs New Upper Changi Road (D16 OCR, ~1,010 units, tender 1 Sep 2026). Source: URA GLS Programme 1H 2026.

Berlayar Drive — Waterfront Living at the Edge of the Greater Southern Waterfront

The Berlayar Drive site is located in the Bukit Merah planning area (District 3), adjacent to Telok Blangah MRT station on the Circle Line (CC29). The site forms part of the nascent Berlayar estate, a new residential precinct being carved out from the southern edges of Bukit Merah and Telok Blangah, with proximity to the Southern Ridges park connector system, Henderson Waves, and the Labrador Nature Reserve.

At 271,929 sqft with a gross plot ratio of 1.4, the Berlayar Drive site is notably low-density for a Singapore residential GLS parcel — reflecting URA’s planning intent to create a mid-rise, waterfront-adjacent neighbourhood rather than another high-rise tower cluster. The estimated 415 units would make this a boutique-to-mid-sized development, and the lower density is expected to attract premium pricing from developers given the site’s proximity to the Southern Waterfront and the overall scarcity of new residential supply in D3.

The Greater Southern Waterfront (GSW) masterplan — one of Singapore’s most ambitious urban transformation programmes — encompasses a 30km waterfront stretch from Pasir Panjang to Marina East, including the relocation of Tanjong Pagar Terminal (to Tuas by 2027), the repurposing of Pulau Brani, and the creation of new waterfront precincts at Keppel, Mount Faber, Berlayar, Labrador and Pasir Panjang. Berlayar Drive sits directly within this transformation zone. Industry analysts expect the developer to price land at S$1,300–1,600 psf ppr, reflecting the GSW premium, the D3 RCR location and the low-density advantage — which typically supports higher per-unit ASP.

New Upper Changi Road — Bedok’s Potential Mega-Development

The New Upper Changi Road site occupies a 331,194 sqft parcel in the Bedok planning area (District 16), a mature residential neighbourhood in Singapore’s eastern region. With a gross plot ratio of 2.8, the site could yield approximately 1,010 residential units — making it one of the largest GLS residential parcels on the 1H 2026 confirmed list. The nearest MRT station is Bedok (East-West Line), a major interchange point in D16 with established amenities including Bedok Mall, Bedok Interchange Hawker Centre, and bus interchange connectivity.

Bedok is a well-established mature estate, home to a large HDB population and a smaller but growing private condominium market. Notable recent transactions in D16 include units at Grandeur Park Residences (TOP 2019, ~S$1,600–2,000 psf) and Coco Palms (~S$1,400–1,700 psf). The New Upper Changi Road site’s OCR location means it will attract primarily HDB-upgrader buyers and Singapore Citizen first-time private buyers, for whom 0% ABSD applies on a first private property purchase. For these buyers, an OCR mass-market entry point (estimated launch price S$1,600–2,000 psf) represents an accessible entry into private property ownership in a mature, well-connected eastern district.

The mega-development scale — if fully realised at 1,010 units — carries both supply and marketing risk. Mega-developments require phased launches over 12–18 months to absorb market demand without undercutting their own prices. Developers who tender for this site will need deep marketing resources and a willingness to sustain a long selling campaign. The 2-year deadline from award to launch (under ABSD developer rules) adds urgency to the tender and project development timeline.

Figure 2: 1H 2026 GLS confirmed list supply by site (left) and recent land price benchmarks for comparison (right). New Upper Changi Road at ~1,010 units is the largest single site. Holland Plain (S$1,491 psf ppr) and Dover Drive (S$1,281 psf ppr) are the latest comparable land price benchmarks. Source: URA.

What the Two Sites Mean for the 1H 2026 Supply Programme

The URA’s 1H 2026 GLS confirmed list includes nine sites in total, with a combined estimated supply of approximately 5,050 private residential units. The two new sites — Berlayar Drive and New Upper Changi Road — account for 1,425 of these units, or roughly 28% of the confirmed list supply for the first half of 2026. Other sites on the confirmed list include Peck Hay Road (D9, ~350 units, tender closing 11 June 2026), River Valley Green Parcel C (D9, ~420 units, closing 18 June 2026), Dunearn Road (D11, ~325 units, already awarded), Holland Plain (D10, ~280 units, awarded to Sim Lian May 2026) and Kallang Close (D12, ~520 units, awarded to Frasers+Mitsubishi April 2026).

The geographic spread of the 1H 2026 sites — D3, D9, D10, D11, D12, D16 — reflects the URA’s deliberate intention to distribute supply across CCR, RCR and OCR markets. Including New Upper Changi Road (D16 OCR) ensures that affordable mass-market units are entering the pipeline, while the concentration of CCR sites (D9, D10, D11) addresses sustained high-end demand from upgraders and investors.

Site

District

Region

Est. Units

Tender/Award Status

Land Price (psf ppr)

Holland Plain

D10

CCR

~280

Awarded (May 2026, Sim Lian)

S$1,491

Dunearn Road

D11

CCR

~325

Awarded (Apr 2026)

S$1,250 (est.)

Kallang Close

D12

RCR

~520

Awarded (Apr 2026, Frasers)

S$1,415

Peck Hay Road

D9

CCR

~350

Tender closes 11 Jun 2026

TBD

River Valley Green C

D9

CCR

~420

Tender closes 18 Jun 2026

TBD

Berlayar Drive

D3

RCR

~415

Tender closes 4 Aug 2026

TBD

New Upper Changi Road

D16

OCR

~1,010

Tender closes 1 Sep 2026

TBD

Buyer and Investor Implications

For prospective buyers, the Berlayar Drive and New Upper Changi Road sites represent future pipeline supply that is unlikely to launch before 2028 in both cases — developers typically require 18–24 months from award to project launch, with construction-to-TOP timelines of an additional 3–4 years. A buyer registering interest in a Berlayar Drive development today would likely see a launch preview in mid-to-late 2027, with TOP potentially in 2031–2032. New Upper Changi Road, being larger and more complex, may launch in late 2027 or 2028 depending on the developer’s phasing strategy.

For investors tracking the pipeline, these two sites confirm that RCR (Berlayar, Kallang) and OCR (New Upper Changi Road) supply is building — which may moderate price growth in those segments beyond 2028 as completions arrive. The CCR, by contrast, has lighter confirmed list supply (Holland Plain and Dunearn Road are relatively small), which may support continued CCR price resilience through 2026–2027 even as OCR and RCR stock accumulates.

The worked example below illustrates what a buyer of a future Berlayar Drive unit might expect in acquisition costs, assuming an indicative launch price of S$2,200 psf for a 850 sqft 2-bedroom unit.

Worked example — Future Berlayar Drive 2-bedroom, est. S$1,870,000:

SC buyer (first private property, after selling HDB). BSD: 1%×S$180k (S$1,800) + 2%×S$180k (S$3,600) + 3%×S$640k (S$19,200) + 4%×S$500k (S$20,000) + 5%×S$370k (S$18,500) = S$63,100 BSD. ABSD: S$0. Bank loan 75% = S$1,402,500 @ 3.0% 25yr = S$6,649/month. TDSR: minimum income S$12,089/month required. Total upfront: S$467,500 downpayment + S$63,100 BSD + S$10,000 legal = est. S$540,600.

What Might Come Next

The immediate pipeline of tender closings is busy through Q3 2026: Peck Hay Road closes 11 June, River Valley Green Parcel C closes 18 June, Berlayar Drive closes 4 August, and New Upper Changi Road closes 1 September. Award announcements typically follow within 2–4 weeks of the tender close, at which point land price benchmarks will be set. If Peck Hay Road and River Valley Green (both D9 CCR) attract strong bids above S$1,500 psf ppr, it would signal continued developer appetite for CCR land despite the 60% foreigner ABSD headwind. If bids are soft (below S$1,200 psf ppr), it may indicate developer caution about CCR demand sustainability at current price levels. LovelyHomes will report on each tender award as results are released by URA.

Frequently Asked Questions

When will the Berlayar Drive and New Upper Changi Road projects launch for sale?

Developer launches are typically 18–24 months after GLS award and subject to planning approvals. Given the Berlayar Drive tender closes 4 August 2026 and award follows approximately 3–4 weeks later, the earliest a developer could realistically launch a Berlayar Drive project would be Q1–Q2 2028, with New Upper Changi Road slightly later given its larger scale. Buyers should register interest directly with developers (via project marketing teams) once the tender is awarded and the developer is publicly known, typically in Q4 2026 for Berlayar Drive.

How does the Greater Southern Waterfront affect Berlayar Drive’s investment case?

The Greater Southern Waterfront (GSW) transformation is one of Singapore’s most significant long-term urban projects — it will eventually create new residential, commercial and recreational precincts across a 30km southern coastal corridor. In the near term (2026–2028), the primary catalyst for Berlayar Drive is proximity to the Southern Ridges, Telok Blangah MRT (CC29) and the nascent Berlayar estate identity rather than operational GSW amenities, which remain years away. Longer term (2030+), as Keppel Terminal land is repurposed and waterfront promenades connect Sentosa to Marina East, Berlayar Drive’s capital appreciation could benefit significantly. Buyers should view GSW as a long-horizon catalyst, not a near-term price driver.

Is the New Upper Changi Road site a good investment given its mega-development scale?

Mega-developments (1,000+ units) in Singapore carry specific risks and benefits. On the risk side: a large supply of similar units in one development creates internal price competition during resale, especially when multiple sellers list simultaneously post-MOP. On the benefit side: mega-developments attract developer marketing resources, typically feature comprehensive facilities, and benefit from economies of scale in management fees. For owner-occupiers in Bedok seeking a large community and established facilities, the New Upper Changi Road project may be highly attractive. For investors focused on rental or capital gain, smaller boutique developments in the same area may offer tighter supply dynamics post-TOP.

Who can buy these properties once they launch — are there foreign buyer restrictions?

Both sites are non-landed residential developments and may be purchased by Singapore Citizens, Permanent Residents and foreigners subject to the applicable stamp duties. Singapore Citizens buying their first private property pay BSD only (0% ABSD). PRs pay 5% ABSD on a first property. Foreigners pay 60% ABSD on all residential property. There are no additional restrictions specific to the Berlayar Drive or New Upper Changi Road locations beyond these standard rules. GCB areas and landed housing restrictions do not apply to apartment/condominium developments.

How do I track when developers register interest for Berlayar Drive and New Upper Changi Road?

Once a developer is awarded a GLS site, they typically announce a sales gallery opening and register-interest campaign within 6–12 months of award. LovelyHomes will publish updates as each tender is awarded. You can also monitor URA’s website (ura.gov.sg), the respective developer’s official website (once known), and property portals such as PropertyGuru and 99.co, which aggregate new launch previews. Alternatively, a CEA-registered property agent can notify you directly when the developer’s marketing team begins collecting expressions of interest.

This article is for general informational purposes only. All unit yield estimates are projections based on site area and GPR and actual development plans will be determined by the awarded developer subject to URA’s planning approval. Land price forecasts are market speculation and may differ materially from actual tender results. Nothing in this article constitutes investment or financial advice. Readers should conduct independent due diligence and consult licensed advisers before making any property decisions. Official information about these GLS sites is available at ura.gov.sg.

Quick Answer — Holland Plain GLS 2026: What You Need to Know

Sim Lian Group won the Holland Plain GLS tender on 12 May 2026 as the sole bidder at S$454 million — translating to S$1,491 psf ppr.

The 99-year leasehold site in District 10 (CCR) spans 15,717 sq m with a max GFA of 28,291 sq m and an estimated yield of ~280 residential units.

Building height is capped at 6 to 8 storeys, pointing to a low-rise boutique development — a rare product type in the Holland Road / Farrer Road corridor.

Estimated launch price: S$3,100–S$3,800 psf, based on the S$1,491 psf ppr land cost plus construction, financing, and a market premium over One Holland Village Residences resale benchmarks.

Preview is likely in Q3–Q4 2027 at the earliest, given the 18–24 month planning and construction mobilisation window typical of CCR boutique sites.

The sole-bid outcome reflects cautious developer sentiment in the CCR at current interest rates, but Sim Lian’s calculated entry represents a significant up-market pivot for the group.

For SC buyers, no ABSD on a first property purchase. Foreigners face a 65% ABSD surcharge — materially reducing demand from the international pool that traditionally drives CCR volumes.

Holland Plain GLS Awarded to Sim Lian — The Deal Breakdown

On 12 May 2026, the Urban Redevelopment Authority (URA) announced the award of the Government Land Sales (GLS) site at Holland Plain, District 10, to Sim Lian Group — Singapore’s only bidder. The developer tendered S$454,110,000 for the 99-year leasehold parcel, equivalent to approximately S$1,491 per square foot per plot ratio (psf ppr).

The sole-bid outcome drew immediate attention from industry observers. In previous cycles, prime CCR confirmed-list sites in District 10 attracted three to six bidders. The absence of competing bids from large listed developers such as City Developments, CapitaLand Development, UOL Group, or Frasers Property points to a recalibration of risk appetite in the Core Central Region, where the 65% Additional Buyer’s Stamp Duty on foreigners has significantly dampened the international buyer pool that historically underpinned CCR price discovery.

That Sim Lian Group — better known for large-scale Outside Central Region projects such as Treasure at Tampines (2,203 units) and Parc Clematis (1,468 units) — stepped into this site alone is a notable strategic shift for the developer. It signals confidence in the long-term premium of the District 10 address book and suggests Sim Lian has modelled a profitable outcome at launch prices that may be more measured than the aspirational pricing sometimes associated with CCR boutique developers.

Site Specifications — A Boutique Low-Rise in the Heart of D10

Parameter

Details

Location

Holland Plain, District 10 (CCR), Singapore

Tenure

99-year leasehold from 12 May 2026

Site Area

15,716.9 sq m (approximately 169,148 sq ft)

Max Gross Floor Area

28,291 sq m (approx. 304,590 sq ft)

Gross Plot Ratio

1.8

Permitted Building Height

6 to 8 storeys

Estimated Residential Units

~280 units

Land Use

Residential (private condominium)

Developer

Sim Lian Group

Award Price

S$454,110,000 (S$1,491 psf ppr)

Tender Closed

7 May 2026

Award Date

12 May 2026

The six-to-eight storey height cap is significant. In the Holland Plain and Farrer Road precinct, most condominium developments are low-to-mid-rise, and the Master Plan’s height guidance for this parcel maintains the neighbourhood’s established residential character. Sim Lian is unlikely to build a high-density tower; buyers can expect a product more akin to Cluny Park Residences or Gallop Green — intimate, well-appointed, and positioned for owner-occupier and high-net-worth tenant demand from the nearby international schools.

D10 Comparable PSF — Where Holland Plain Fits

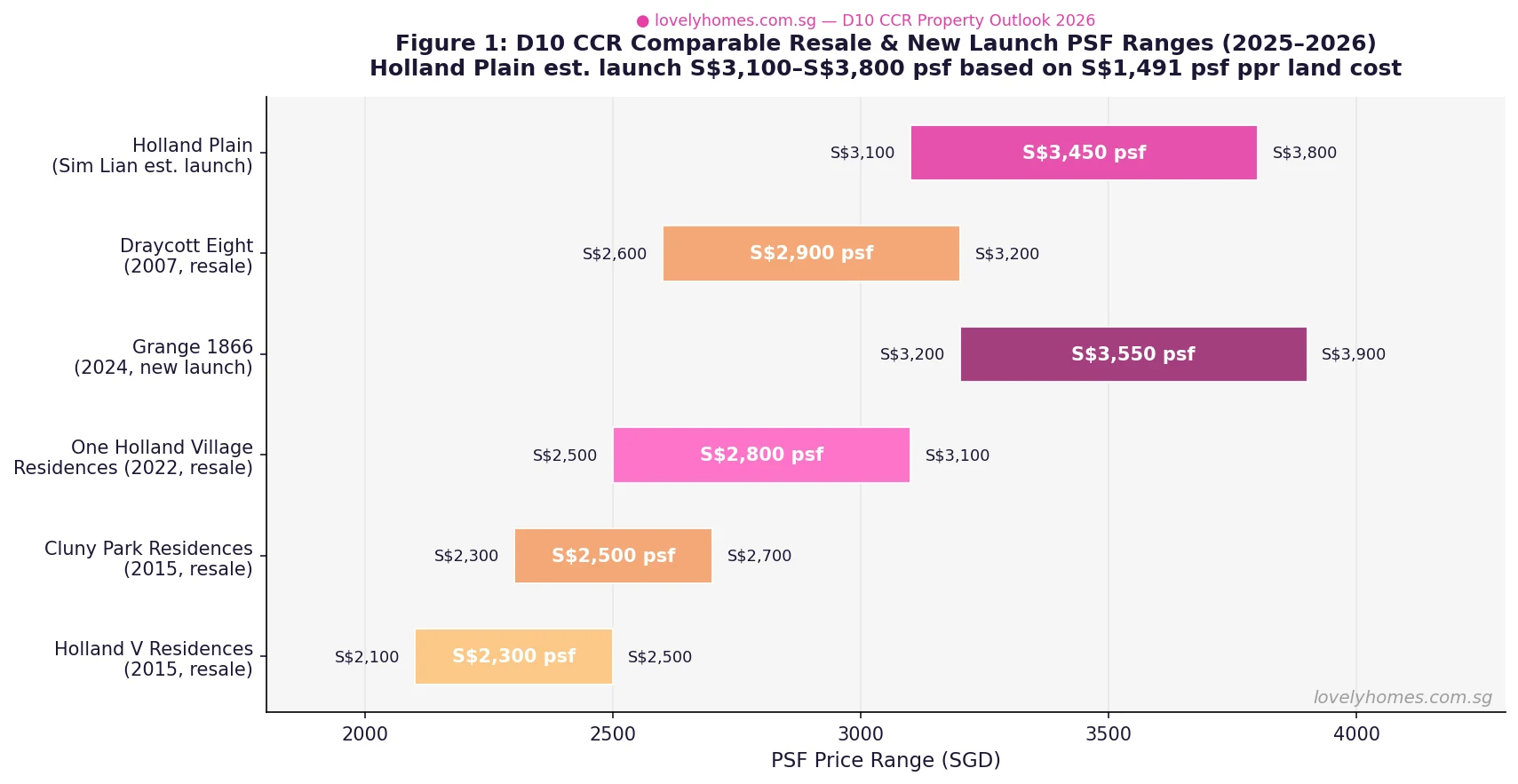

Figure 1: D10 CCR comparable resale and new-launch PSF ranges for selected condominiums (2025–2026). Holland Plain’s estimated launch range of S$3,100–S$3,800 psf reflects the S$1,491 psf ppr land cost plus construction and a market premium. Source: URA REALIS, EdgeProp, LovelyHomes analysis.

The chart above places Holland Plain’s estimated launch price alongside established D10 benchmarks. One Holland Village Residences — the most proximate recent comparable, launched in 2022 and developed by Far East Organization — traded at roughly S$2,800–S$3,000 psf on launch and currently resells at S$2,500–S$3,100 psf depending on floor level and facing. Grange 1866 in D9 launched in 2024 at S$3,200–S$3,900 psf. Draycott Eight — an older freehold project in D10 — commands S$2,600–S$3,200 psf on resale despite its 2007 completion date, underlining the sustained value of CCR addresses.

Holland Plain’s 99-year leasehold tenure will attract a discount versus freehold and 999-year leasehold projects in the same district. Buyers accustomed to Cluny Park Residences or Good Class Bungalow (GCB) adjacency-premium projects will note that freehold equivalents in the Farrer Road–Grange Road belt command a 10–15% premium over comparable 99-year leasehold product. This suggests the achievable PSF at Holland Plain may cluster towards S$3,100–S$3,500 psf for the majority of units, with penthouses and premium stacks potentially touching S$3,800 psf.

Estimated Launch Pricing and Unit Mix

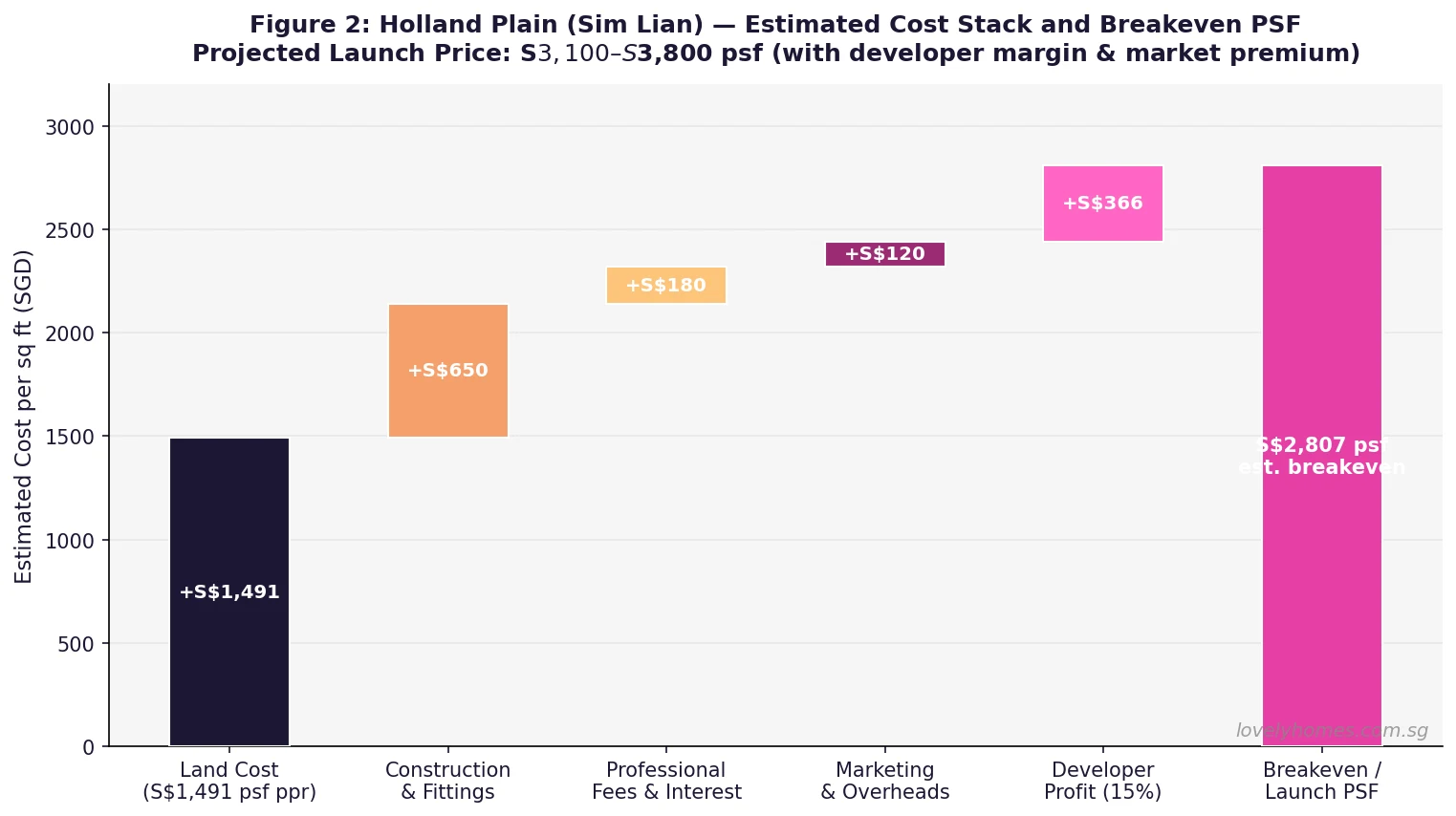

Figure 2: Holland Plain (Sim Lian) estimated cost-stack and breakeven PSF analysis. Land at S$1,491 psf ppr plus construction, professional fees, interest carry, and a 15% developer margin points to a breakeven of approximately S$2,800 psf, with the likely launch range of S$3,100–S$3,800 psf allowing for market positioning and a D10 CCR brand premium. Source: LovelyHomes analysis based on industry cost benchmarks.

With 280 units across ~304,590 sq ft of GFA, the average unit will be approximately 1,088 sq ft — consistent with a mix weighted towards 2- and 3-bedroom configurations appropriate for the family-oriented D10 demographic. LovelyHomes estimates the following indicative pricing grid, based on a blended average launch PSF of S$3,300:

Unit Type

Est. Size (sq ft)

Indicative Price Range

1-Bedroom

450–550

S$1.40M – S$2.09M

2-Bedroom

700–900

S$2.17M – S$3.42M

3-Bedroom

1,000–1,300

S$3.10M – S$4.94M

4-Bedroom / Penthouse

1,500–2,000

S$4.65M – S$7.60M+

Indicative only. Actual pricing will depend on Sim Lian’s unit mix strategy, prevailing SORA rates at the time of launch, and market conditions in 2027–2028. Consult a licensed property professional before making any commitment.

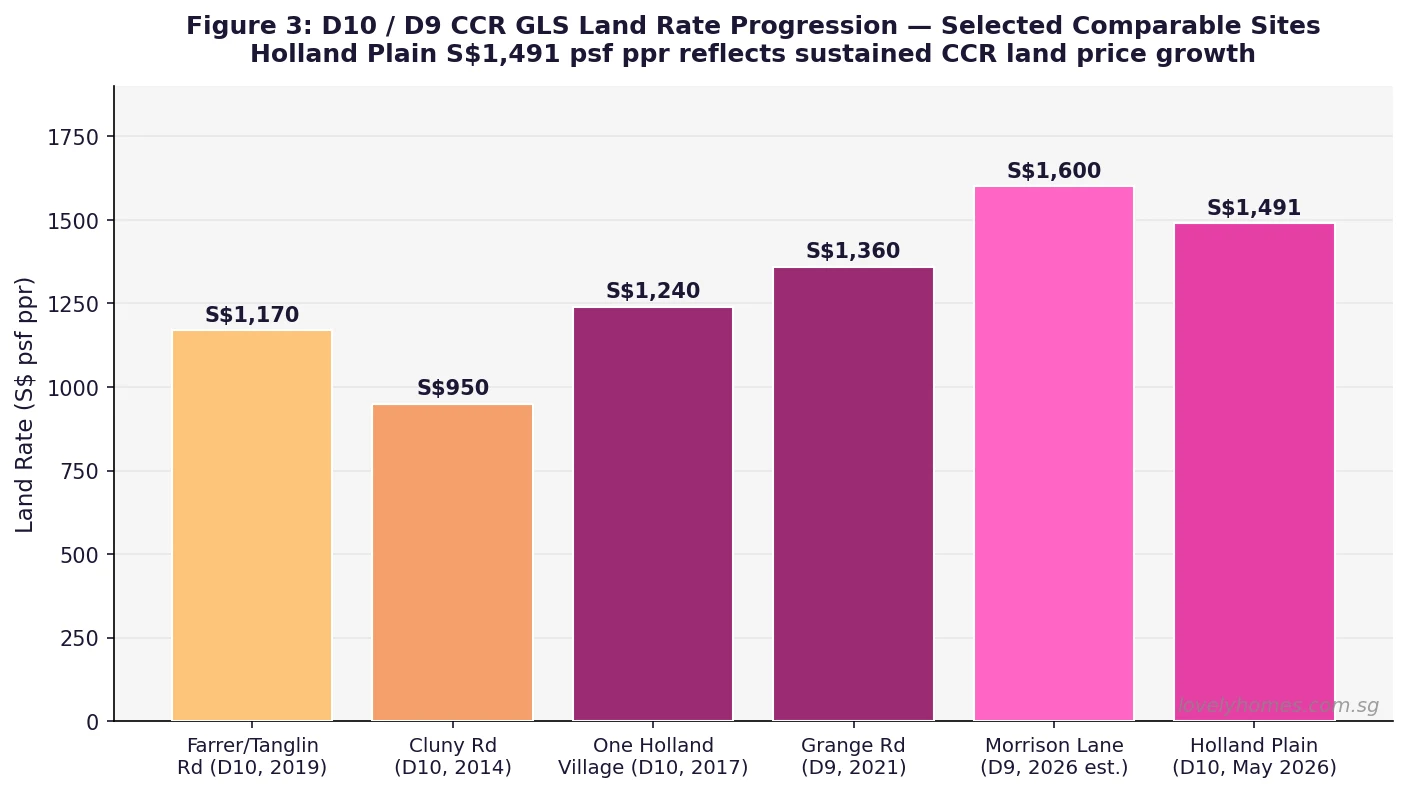

D10 GLS Land Rate Progression — Context

Figure 3: Historical D10 and D9 CCR GLS land rates for selected comparable sites, showing the broad upward trend in CCR land values since 2014. Holland Plain’s S$1,491 psf ppr reflects measured (not euphoric) CCR pricing, consistent with developers’ caution given the 65% foreigner ABSD. Source: URA GLS programme data, LovelyHomes analysis.

Holland Plain’s S$1,491 psf ppr land rate is notable for what it is not: a record. In the pre-cooling-measure era, CCR land bids regularly pushed past S$2,000 psf ppr. The 60% Additional Buyer’s Stamp Duty on foreigners (raised to 65% in April 2023) has structurally redirected international capital away from the new-launch CCR pipeline, removing the speculative demand layer that previously compressed developer margins and pushed bids skyward. What remains is the durable owner-occupier and long-term investment demand from Singapore Citizens and Permanent Residents, which is more price-sensitive and longer in decision horizon.

Sim Lian’s S$1,491 psf ppr bid is broadly consistent with a financially disciplined modelling exercise rather than a prestige land-banking move. The developer is betting on a specific thesis: that D10 boutique, low-rise product at 280 units will sell through comfortably to local families and returning expatriates, even at S$3,100–S$3,500 psf, given the paucity of new launch supply in the Holland Road–Farrer Road corridor since 2022.

Who Will Buy Holland Plain — The Target Buyer Profile

Several distinct buyer archetypes are likely to drive take-up at Holland Plain:

SC upgraders from the OCR. With OCR private condo prices rising 2.2% in Q1 2026 and MOP waves releasing large numbers of resale HDB flats into the market, a cohort of Singapore Citizens who purchased OCR condominiums or HDB flats in 2018–2021 are now sitting on significant capital gains. For couples with household incomes of S$20,000–S$30,000 per month, a 3-bedroom unit at Holland Plain at S$3.5M–S$4.5M represents an aspirational CCR upgrade with no ABSD on a first private property purchase.

D10 residents downsizing or lateral moving. Freehold condominium owners in the Farrer Road, Grange Road, and Tanglin Road precinct who seek newer infrastructure, modern facilities, and professional property management without leaving the district will look seriously at Holland Plain, even with the 99-year leasehold caveat.

Expat tenants’ employers and parents. The international schools immediately adjacent — United World College of South East Asia (Dover campus), the Australian International School, the German European School — generate sustained demand for family-sized rental units in D10. Investor-buyers who target the expat tenant pool will find Holland Plain’s 3-bedroom stock particularly compelling, especially given one-north and the Buona Vista biomedical employment cluster’s continued expansion driving corporate housing budgets.

High-net-worth Singaporeans for own stay. At six to eight storeys in a low-density neighbourhood, Holland Plain will offer a level of privacy and exclusivity rarely available in new launches. The limited unit count of ~280 means the development will feel intimate — a selling point for buyers accustomed to landed living who want managed-property convenience.

ABSD Implications — The Foreigner Market Is Largely Sidelined

The 65% Additional Buyer’s Stamp Duty on foreign buyers, in force since 27 April 2023, means that any foreigner purchasing a S$2M 2-bedroom unit at Holland Plain would face an ABSD bill of S$1.3 million — on top of BSD of approximately S$57,600. Total acquisition cost before loan: over S$3.35M. This is not a purchase case that works for most foreign nationals who do not have deep Singapore roots or a specific business reason to own in the CCR.

The practical implication: Holland Plain will be absorbed almost entirely by Singapore Citizens and Permanent Residents. SPR buyers pay 5% ABSD on a first property — manageable at S$100,000–S$180,000 on a typical unit — and a meaningful segment of the take-up will come from this pool. SC buyers on a first property pay zero ABSD. SC buyers on a second or subsequent property pay 20% ABSD — a S$640,000 bill on a S$3.2M unit — which remains a significant friction, though less prohibitive for high-net-worth upgraders than the foreigner rate.

Worked Example — Mr & Mrs Chua: SC Upgraders Buying a 3-Bedroom at Holland Plain

Mr & Mrs Chua are Singapore Citizens in their early 40s. They sold their OCR condominium in Tampines in late 2025 for S$1.55M (purchased in 2019 for S$1.1M), banking approximately S$350,000 in net cash after paying off the outstanding mortgage. They are now renting in D10 and plan to purchase a 3-bedroom unit at Holland Plain when it launches, estimated at approximately S$4.1M.

ABSD: As SC buyers on their second private residential property (they now own zero properties — the Tampines unit was sold), they are effectively first-time owners at point of purchase. Zero ABSD applies. ✓

BSD on S$4.1M: 1% × S$180k = S$1,800; 2% × S$180k = S$3,600; 3% × S$640k = S$19,200; 4% × S$500k = S$20,000; 5% × S$1.1M = S$55,000; 6% × S$1M = S$60,000. Wait — let me apply the correct BSD tiers. On S$4.1M: 1%×180k + 2%×180k + 3%×640k + 4%×500k + 5%×2.6M. Actually: First S$180k at 1% = S$1,800; next S$180k at 2% = S$3,600; next S$640k at 3% = S$19,200; next S$500k at 4% = S$20,000; above S$1.5M: next S$1.5M at 5% = S$75,000; above S$3M: remaining S$1.1M at 6% = S$66,000. Total BSD = S$185,600.

Financing: At a blended bank fixed rate of approximately 2.0% per annum (estimated for 2027), the Chua couple borrows 75% of the S$4.1M purchase price = S$3,075,000. Monthly instalment over 25 years ≈ S$13,020. TDSR check: assuming joint gross income S$35,000/mth — TDSR = 37.2% (below 55% cap). ✓

Down payment and cash needed: 25% down = S$1,025,000 (can be funded from CPF OA and cash); BSD S$185,600 in cash. Using S$350,000 cash from the Tampines sale and drawing S$675,000 from CPF OA, the couple meets both the down payment and stamp duty requirements with ~S$164,000 CPF OA remaining as a buffer.

Summary for Mr & Mrs Chua: S$4.1M Holland Plain 3-bedroom → ABSD nil → BSD S$185,600 → bank loan S$3.075M @ 2.0% for 25yr → monthly S$13,020 → TDSR 37.2% → cash outlay S$535,600 (cash from Tampines proceeds + stamp duty) + CPF drawdown S$675,000.

Development Timeline and What to Watch

Following the tender award on 12 May 2026, Sim Lian will enter the planning and approvals phase with URA. A provisional building plan is typically submitted within six months of award, with a building plan approval following three to six months later. Construction commencement generally occurs 18–24 months post-award for CCR boutique sites. Based on this trajectory, the likely public preview window is Q3–Q4 2027, with expected project completion (Temporary Occupation Permit) in 2030–2031.

Watch for: Sim Lian’s project name announcement (likely within six months), architectural rendering release, showflat construction in the Holland Plain vicinity, and any pre-indication of pricing through EdgeProp or Stacked Homes developer briefings approximately 60–90 days before the official launch date.

What This Means for D10 Buyers and the Broader CCR

The Holland Plain award is a data point in a larger story about CCR supply discipline. With the 65% foreigner ABSD in place and a generation of Singaporean private property owners sitting on significant unrealised equity from 2019–2024 price appreciation, the CCR market in 2026–2028 will be one where supply is lean, developer caution is visible (sole bids, measured land rates), and local buyers — particularly SC upgraders — will find themselves as the dominant demand driver for the first time in decades.

For buyers considering Holland Plain, the opportunity is clear: a boutique, low-rise D10 CCR address in a school belt with strong expat tenant demand, delivered by a developer with an established sales track record, at land rates that suggest a measured (rather than euphoric) launch PSF. The risk factors are the 99-year leasehold tenure, the reliance on local SC/SPR demand, and the long wait time (2027–2028 launch, 2030–2031 completion) during which market conditions may shift.

What Might Come Next — GLS Pipeline and CCR Outlook

This is speculative. The remaining 1H 2026 GLS confirmed list site — River Valley Green Parcel C — closes for tender on 18 June 2026 and is expected to attract two to four bidders given its smaller site area. If it also draws a sole bid at conservative land rates, it would confirm a broader pattern of developer restraint in the CCR. The URA may respond to this signal when compiling the 2H 2026 GLS programme (expected announcement December 2026) by adjusting the CCR mix on the confirmed list, potentially holding back sites to avoid depressing land values further or to allow existing pipeline to absorb before adding new confirmed-list supply.

Watch also for any policy review of the 65% foreigner ABSD. If global capital flows to Singapore property are assessed to have become too restricted and if housing prices stabilise, there is a non-trivial possibility of a partial relaxation (e.g., from 65% to 30–45% for longer-term PRs or certain FTA-holder nationalities) in the 2026–2027 National Day Rally or Budget cycle. Any such relaxation would immediately revive international demand at D10 project launches and push achievable PSF upwards — a significant upside scenario for early Holland Plain buyers.

FAQ: Holland Plain GLS 2026 — Sim Lian AwardWhy did only one developer bid for Holland Plain?

The sole-bid outcome reflects a combination of factors: the 65% Additional Buyer’s Stamp Duty on foreigners has substantially reduced the addressable buyer pool for CCR new launches, narrowing the demand basis that developers model when deciding how aggressively to bid. Many larger listed developers were also managing existing CCR inventory — including ongoing projects in D9 (Peck Hay Road, River Valley) — and may have chosen to preserve capital rather than pursue a concurrent D10 commitment. Sim Lian’s willingness to bid alone at S$1,491 psf ppr suggests the group has a specific product and pricing thesis that pencils out within that land cost, without requiring the foreign buyer premium that other developers may have deemed necessary to justify a higher bid.

Is Holland Plain’s 99-year leasehold a concern for long-term value?

Leasehold tenure is always a consideration in the CCR, where freehold and 999-year projects exist as alternatives. A 99-year leasehold in D10 will typically trade at a 10–15% discount to a freehold equivalent on a like-for-like basis. However, for buyers with a 10–20 year investment horizon, the leasehold discount at point of purchase can represent a compelling entry point, particularly if the area’s rental demand and capital growth story remain intact. The critical factor is the remaining lease at the point of future sale: a buyer who purchases a 99-year leasehold unit in 2028 and sells in 2043 will be transacting a unit with approximately 84 years remaining — still well above the HDB housing grant lease-coverage threshold and broadly financeable for the next generation of buyers.

When is the expected launch date for Sim Lian’s Holland Plain project?

Based on the typical CCR boutique development timeline — URA planning approvals (6–12 months), building plan submission and approval (3–6 months), showflat construction and marketing preparation (3–6 months) — the most likely preview window is Q3 to Q4 2027. Construction commencement would follow in late 2027 or early 2028, with a Temporary Occupation Permit (TOP) date of approximately 2030–2031. This is an estimate based on typical timelines; Sim Lian has not publicly confirmed any milestones.

What is the nearest MRT station to Holland Plain?

The Holland Plain site is located approximately 700 metres to 1 kilometre from Holland Village MRT station (Circle Line CC21 and Thomson-East Coast Line TE17). The dual-line interchange at Holland Village provides excellent connectivity to Botanic Gardens (CC19/DT9), Buona Vista (CC22/EWL), and Marina Bay (TE20/CC29/NS27/CE1). The Thomson-East Coast Line also connects northward to Caldecott (TE9/CC17) and southward through the city to Bayshore. For commuters working in the CBD or Orchard, Holland Village MRT offers a one- to two-interchange journey of approximately 20–30 minutes.

What schools are near Holland Plain?

The Holland Plain site benefits from proximity to some of Singapore’s most sought-after schools. Henry Park Primary School is located within approximately 1 kilometre, making the project eligible for Phase 2B HDB priority balloting for future owners with children. Nanyang Primary School in Buona Vista is another highly-regarded option within approximately 2 km. For international school demand — which drives a significant portion of D10 rental volumes — United World College of South East Asia (Dover campus), the Australian International School, and the German European School Singapore are all within a 3–4 km radius. This cluster is a major driver of family tenant demand at S$5,000–S$9,000 per month for 3- to 4-bedroom units.

Should I register interest now to buy Holland Plain?

Sim Lian has not opened any registration of interest (ROI) process as at 22 May 2026. The project has not been named, priced, or publicly marketed. It is premature to commit funds or make any financial arrangement based solely on this GLS award. LovelyHomes recommends monitoring Sim Lian’s official announcements, EdgeProp project launch alerts, and URA’s building plan approvals database for planning-permission milestones, which will give approximately 60–90 days’ advance notice before a formal marketing launch. Do not rely on unofficial registration lists maintained by individual marketing agents, as these carry no legal weight and may involve data privacy risks.

Disclaimer: This article contains LovelyHomes’ independent analysis and projections based on publicly available URA GLS data, industry cost benchmarks, and comparable transaction information. Projected launch prices, unit mixes, timelines, and investment outcomes are estimates only and do not constitute financial advice, a solicitation to purchase, or a guarantee of any outcome. The Singapore property market is subject to government policy changes, interest rate movements, and macroeconomic conditions that may materially alter outcomes. Always consult a licensed real estate agent, licensed financial adviser, and qualified conveyancing solicitor before making any property purchase decision. Source data: URA GLS programme 1H 2026, URA REALIS, MND, CPF Board.

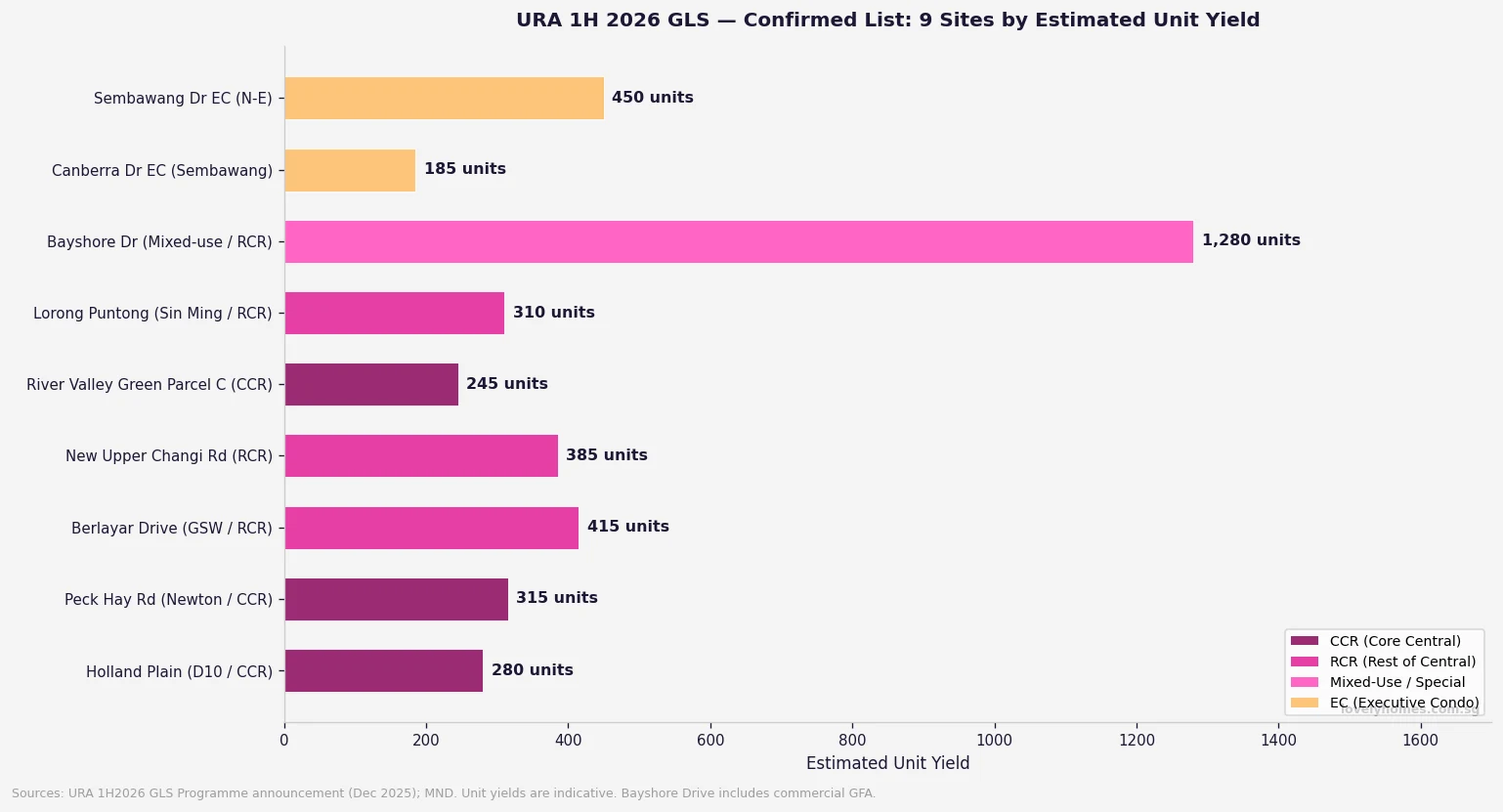

URA 1H 2026 GLS Programme: All 9 Confirmed List Sites Analysed — Supply, Locations and Price Outlook

Quick Answer — 1H 2026 GLS Confirmed List at a Glance

9 sites on the 1H 2026 Confirmed List: 6 private residential, 1 mixed-use, 2 EC plots

Total supply: 3,940 private residential units + 635 EC units = 4,575 units via confirmed list

Bayshore Drive mixed-use site is the headline parcel — 1,280 residential units + 22,500 sqm commercial

Holland Plain (2nd site) sole bid received: Sim Lian at S$1,491 psf ppr (tender closed 7 May 2026)

Peck Hay Road (Newton CCR) tender closes 11 June 2026; River Valley Green Parcel C closes 18 June 2026

1H 2026 confirmed list private supply is ~50% above the 10-year average — Government signalling adequate pipeline

Two EC sites at Canberra Drive (185 units) and Sembawang Drive (450 units) — now subject to 10-year MOP post-8 May reforms

The Urban Redevelopment Authority’s Government Land Sales (GLS) programme is the primary tool through which Singapore manages its private residential and executive condominium housing pipeline. Every new launch condo you see advertised — from Vela Bay to Tengah Garden Residences — originates with a developer winning a GLS tender years earlier. Understanding what is on the 1H 2026 confirmed list, where those sites sit, and what developers are likely to pay for them tells you a great deal about where new private supply will come from in 2028 and beyond.

This analysis covers all nine confirmed list sites from the 1H 2026 GLS programme, tracking tender timelines, indicative psf ppr ranges, expected launch pricing implications, and the macro supply picture. We cross-reference each site’s outcome against the most recent tender awards to give the clearest picture available as at 17 May 2026.

The 9 Confirmed List Sites — Overview and Unit Yield

Figure 1: URA 1H 2026 GLS Confirmed List — all 9 sites by estimated unit yield, colour-coded by market segment (CCR, RCR, Mixed-Use, EC). Sources: URA, MND, December 2025.

Site

Location / Region

Units

Tender Status (May 2026)

Indicative Launch PSF

Holland Plain (2nd site)

D10 / CCR, Bukit Timah

~280

Closed 7 May; Sim Lian sole bid S$1,491 psf ppr

S$2,800–S$3,200+

Peck Hay Road

Newton / CCR

~315

Tender closes 11 June 2026

S$3,200–S$3,800+

Berlayar Drive

Gr Southern Waterfront / RCR

~415

Tender open / result pending

S$2,400–S$2,900

New Upper Changi Road

Bedok / RCR-adjacent OCR

~385

Tender open / result pending

S$2,100–S$2,500

River Valley Green Parcel C

River Valley / CCR

~245

Tender closes 18 June 2026

S$3,500–S$4,000+

Lorong Puntong (Sin Ming)

Bishan–AMK / RCR

~310

Tender open / result pending

S$2,400–S$2,800

Bayshore Drive (Mixed-Use)

Bayshore / RCR-adjacent

~1,280

Tender just opened; est. closes Jul 2026

S$2,750–S$3,100

Canberra Drive EC

Sembawang / North

~185

Tender result pending

S$1,400–S$1,600 (EC)

Sembawang Drive EC

Sembawang / North-East

~450

Tender result pending

S$1,350–S$1,550 (EC)

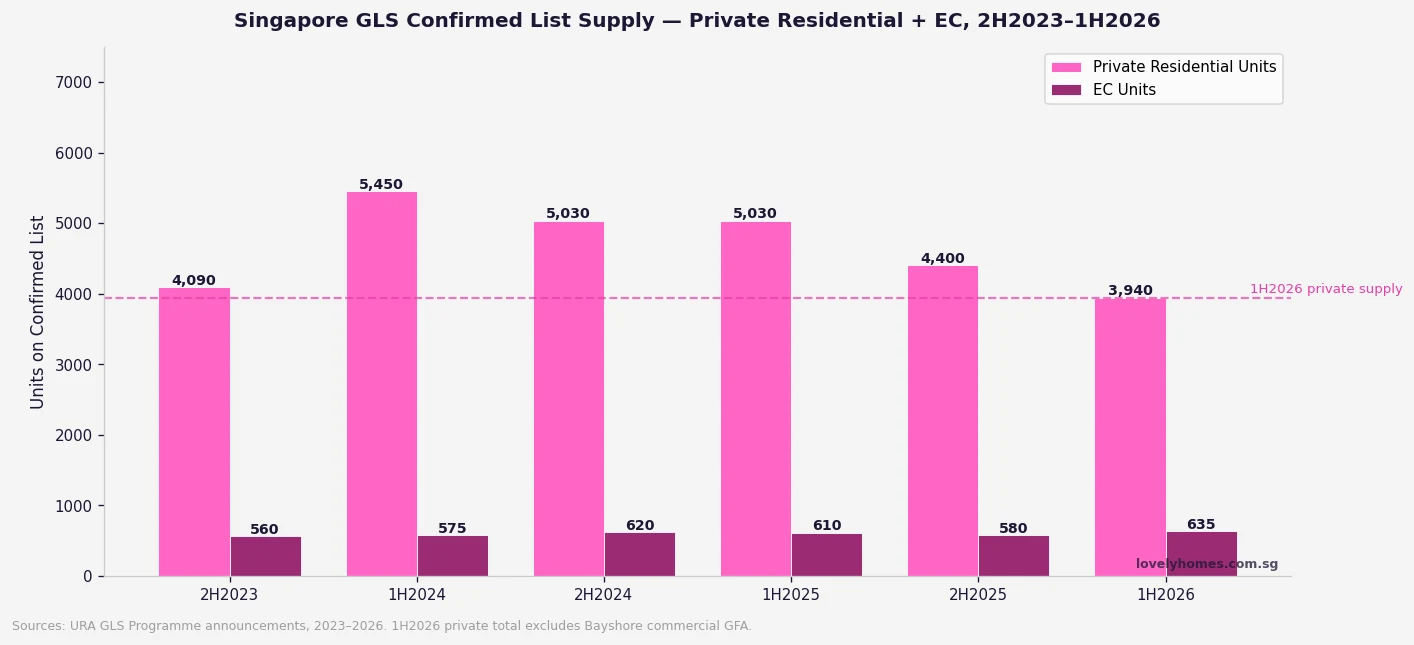

The Supply Context — Is 1H 2026 GLS Generous or Restrained?

Figure 2: Singapore GLS Confirmed List supply, 2H2023–1H2026 — private residential and EC units. Sources: URA GLS Programme announcements.

The 1H 2026 confirmed list private residential supply of 3,940 units is approximately 50% above the 10-year average for a half-year GLS confirmed list, according to URA’s own commentary on the programme at announcement in December 2025. The Government has explicitly stated that this elevated supply is intended to “provide adequate housing options to cater to housing demand” and to moderate price growth — particularly after private residential prices rose 0.9% in Q1 2026 (following 0.6% in Q4 2025), driven by outside central region (OCR) outperformance.

However, the 3,940 private units across six sites is still meaningfully below the 5,450 units offered in 1H 2024 (the cyclical peak). The pattern reflects the Government’s calibrated approach: high enough to signal commitment to supply, but not so aggressive as to flood the pipeline and depress developer sentiment. The Reserve List (which requires developer applications to activate) provides an additional buffer of approximately 5,200 private units that can be unlocked if demand signals warrant it.

Site-by-Site Analysis

Holland Plain (2nd Site) — A Sole Bid That Surprised Analysts

The second Holland Plain site drew a single bid from Sim Lian Group at S$1,491 psf ppr (S$454 million) when the tender closed on 7 May 2026. Analysts had expected three to five bidders; the sole bid reflects elevated construction cost pressure, the lingering premium already embedded in District 10 pricing, and the fact that Sim Lian already holds the adjacent first Holland Plain site. A sole bid does not automatically mean the site will be awarded — URA typically evaluates whether the bid meets the reserve price — but Sim Lian’s continued strategic interest in Holland Plain is clear.

If awarded at S$1,491 psf ppr, market observers indicate a launch PSF of approximately S$2,800–S$3,200 would be needed for the developer to achieve a reasonable margin. This would mark a modest premium to recent CCR resale comparables in the D10 corridor, but is not out of step with the broader trajectory of central region new launches.

Peck Hay Road — Newton’s Newest CCR Site (Closes 11 June 2026)

The Peck Hay Road site is arguably the most competitively positioned residential plot in the 1H 2026 programme. Located in the Newton MRT interchange area (North South and Downtown Lines), the 0.55-hectare former transitional office site is expected to yield approximately 315 units. Newton is one of Singapore’s most liquid and sought-after CCR sub-markets; recent comparable projects in the vicinity have transacted at S$3,000–S$3,800 psf for new launches.

The tender closes 11 June 2026. Given Newton’s track record with competing bids — the area consistently attracts four to six developers per tender — this is likely to be one of the more competitive tenders of the half. A top bid in the S$1,600–S$1,900 psf ppr range is plausible.

River Valley Green Parcel C — CCR Premium Pricing (Closes 18 June 2026)

River Valley Green Parcel C is the third plot in the River Valley Green precinct and sits within Singapore’s prime residential core. The previous two parcels in this precinct were awarded at S$1,246 psf ppr (Parcel A, 2023) and S$1,402 psf ppr (Parcel B, 2024). Parcel C is expected to follow this upward trajectory, with a likely bid range of S$1,450–S$1,700 psf ppr. At those land costs, launch pricing of S$3,500–S$4,000+ psf is feasible. The tender closes 18 June 2026.

Bayshore Drive Mixed-Use — The Billion-Dollar Site

Bayshore Drive is the marquee site of the 1H 2026 programme. As a mixed-use parcel combining 1,280 residential units with 22,500 sqm of commercial space and a direct underground link to Bayshore MRT station (Thomson-East Coast Line), it is the largest and most complex tender in the current cycle. URA and EdgeProp analysis suggests bids of S$1.2–S$2 billion are plausible — making it one of the largest single GLS transactions in Singapore’s history if realised at the upper end. The tender was recently opened and is expected to close around July 2026. We will report on the results as they emerge. See our full Bayshore Drive analysis published 17 May 2026 for detailed site-level commentary.

The Two EC Sites — First Launches Under the New Rules

Canberra Drive (185 units, Sembawang) and Sembawang Drive (450 units) are the first EC tender sites to be marketed entirely under the 8 May 2026 rule changes — specifically the 10-year MOP, 90% first-timer quota, Normal Payment Scheme only, and 15-year privatisation. Developers bidding for these sites must now price in a longer hold requirement and potentially reduced secondary-market liquidity for buyers, which may moderate land bids slightly relative to pre-May 2026 EC tenders. That said, the 90% first-timer quota actually increases base demand, partially offsetting the downward pricing pressure from the MOP extension.

Worked Example — How GLS Land Cost Translates to Launch Price

To understand why these GLS tender outcomes matter for buyers, consider a simple breakeven analysis. If Peck Hay Road is awarded at S$1,750 psf ppr (the psf per plot ratio applied to the maximum permissible gross floor area), a developer builds 315 units on a 0.55 ha site with a plot ratio of approximately 3.5 (hypothetical). Total land cost per unit: approximately S$960,000–S$1,100,000 per unit across a mix of 1-bedroom to 3-bedroom formats.

Adding construction costs (approximately S$450–S$550 psf of GFA in 2026), financing costs (~5–7% of total development cost over 4–5 years), professional fees, and developer margin (~15–18% on cost), the resulting launch price to achieve commercial viability is approximately S$3,200–S$3,600 psf for a typical Newton CCR new launch. This is the arithmetic that underpins the price forecasts in our summary table above.

For buyers, the practical implication is straightforward: land acquired in 1H 2026 tenders will yield projects launching in approximately 2028–2029. The prices you see in those launch brochures will reflect today’s land cost, construction cost inflation over the next two years, and developer expectations for market conditions at launch.

What to Watch in 2H 2026

The three immediate milestones for the GLS programme are: the Peck Hay Road tender result (11 June), River Valley Green Parcel C result (18 June), and the Bayshore Drive tender outcome (expected ~July 2026). Each will provide a live read on developer appetite, construction cost pressures, and land pricing at different market segments.

The 2H 2026 GLS programme (expected to be announced in June 2026) will also be watched closely for whether the Government adjusts the confirmed list size up or down — a signal of its read on both housing demand and developer capacity. Given Q1 2026’s 0.9% private price rise, any material reduction in the 2H confirmed list would likely be read as a market-positive signal by developers and investors alike.

Frequently Asked Questions

What is the GLS programme and how does it affect property prices?

The Government Land Sales (GLS) programme is the mechanism through which URA and HDB release state land for private and public housing development. Developers bid competitively for confirmed list sites, and the winning bid establishes the land cost that feeds through into eventual new-launch pricing approximately 3–5 years after the tender award. A higher volume of GLS sites — and more competitive bidding — generally anchors the supply pipeline and moderates price growth. Conversely, a lean GLS programme or weak bidding signals supply tightening and can anticipate future price pressure. For buyers of new launch condominiums, understanding the GLS pipeline helps set realistic expectations for the prices and supply timing of projects coming to market in 2027–2029.

Why did Holland Plain attract only one bid?

The sole bid for the Holland Plain second site reflects a combination of factors: (1) construction costs remain elevated in Singapore, squeezing developer margins on premium CCR land; (2) Sim Lian already holds the adjacent first Holland Plain site, giving them a strategic advantage that reduces other developers’ relative competitiveness; (3) rising interest rates globally (despite Singapore’s SORA decline) have increased the cost of development financing; and (4) the site’s expected launch PSF of S$2,800–S$3,200 sits in a segment where buyer depth (given ABSD and TDSR constraints) is more limited than in the OCR. A sole bid is unusual but not unprecedented in CCR tenders.

What is the Bayshore Drive mixed-use site and why is it significant?

The Bayshore Drive site is a 3.4-hectare mixed-use parcel that combines 1,280 residential units with 22,500 sqm of commercial gross floor area and a direct underground pedestrian connection to Bayshore MRT (Thomson-East Coast Line). Its significance lies in scale (it is among the largest single GLS parcels offered in several years), location (the emerging Bayshore precinct next to East Coast Park), and mixed-use zoning (which adds commercial value alongside residential). If awarded at estimated values of S$1.2–S$2 billion, it will be one of the highest-value individual land sales in Singapore’s GLS history. See our Bayshore Drive GLS Tender 2026 piece for full site analysis.

How does the 1H 2026 GLS supply compare to previous years?

The 3,940 private residential units on the 1H 2026 confirmed list is approximately 50% above the 10-year average for a half-year confirmed list, but below the 5,450-unit peak seen in 1H 2024. URA has explicitly framed the elevated supply as a measure to ensure adequate pipeline and moderate price growth. Combined with the 12-site reserve list providing a further ~5,200 private units that can be activated on demand, total potential supply from the 1H 2026 GLS programme is approximately 9,185 units — a robust buffer against near-term supply shortfalls.

Should I wait for GLS results before buying a new launch?

GLS results affect new launches that will be built and sold approximately 3–5 years from now — they do not directly affect the pricing of projects already in the market today (such as Bayshore Parcel A, Tengah Garden Residences, or projects under construction). If you are considering a new launch purchase in 2026, the relevant supply is what is already available and selling, not what developers will bid for land this year. That said, monitoring GLS demand (bid volumes, psf ppr paid) gives a useful forward signal: when developers bid aggressively, they believe in future demand and pricing — which is supportive for current buyers. When they bid conservatively or not at all (as with Holland Plain’s sole bid), it may suggest more caution about the premium segment’s near-term outlook.

Disclaimer: This analysis is for general informational and commentary purposes only and does not constitute financial, investment, or property advice. GLS tender outcomes, indicative unit yields, and launch price projections are estimates based on publicly available data from URA, MND, and industry commentary as at 17 May 2026, and are subject to change. Actual tender results, awarded prices, and developer launch strategies may differ materially from projections. Always conduct independent research and consult a licensed conveyancing lawyer, financial adviser, or property consultant before making any investment decision. For official data, refer to URA.gov.sg, MND.gov.sg, and HDB.gov.sg.