Singapore EC Resale Guide 2026: Complete Guide to Buying an Executive Condominium Resale

Quick Answer: Singapore EC Resale 2026

- ECs are a hybrid housing class — built by private developers but subject to HDB eligibility rules for the first 10 years. After 10 years from completion, they are fully privatised and open to all buyers including foreigners.

- 5-year MOP before you can sell in the open market (to Singapore Citizens and PRs only). 10 years before foreigners may buy.

- No HDB loan for EC resale — bank loan only, regardless of citizenship. CPF OA funds are available for SC and SPR buyers.

- EC resale prices averaged S$1,200–S$1,240 per square foot (PSF) in Q1 2026, up from S$760 PSF in 2019 — a 63% increase over 7 years.

- ABSD applies to EC resale purchases for 2nd-and-above properties; SC first-property buyers pay 0% ABSD even within the 5-to-10-year window.

- No income ceiling for resale EC buyers — income limits only apply to new EC applications.

- The Ethnic Integration Policy (EIP) applies to EC resale within the 5-to-10-year window (before full privatisation).

- CPF withdrawal limits and the Withdrawal Limit (WL) / Valuation Limit (VL) framework apply to EC resale purchases the same way they do for private condos.

What Is an Executive Condominium and Who Administers EC Resale?

The Executive Condominium (EC) is a uniquely Singaporean housing class — sometimes called a “sandwich-class” product — built by private developers on land sold by the Housing and Development Board (HDB) at subsidised prices. ECs look identical to private condominiums from the outside, with full condo facilities (swimming pool, gymnasium, BBQ pits, guard house), but they carry a set of HDB-derived restrictions during the first decade of their existence.

HDB administers EC eligibility rules under the Housing and Development (Executive Condominium Housing Scheme) Act 1996 (Cap 129A). The Urban Redevelopment Authority (URA) tracks EC transaction data and publishes quarterly resale price statistics. The Inland Revenue Authority of Singapore (IRAS) administers stamp duties on EC resale transactions — Buyer’s Stamp Duty (BSD), Additional Buyer’s Stamp Duty (ABSD), and Seller’s Stamp Duty (SSD where applicable). This guide reflects rules as at June 2026.

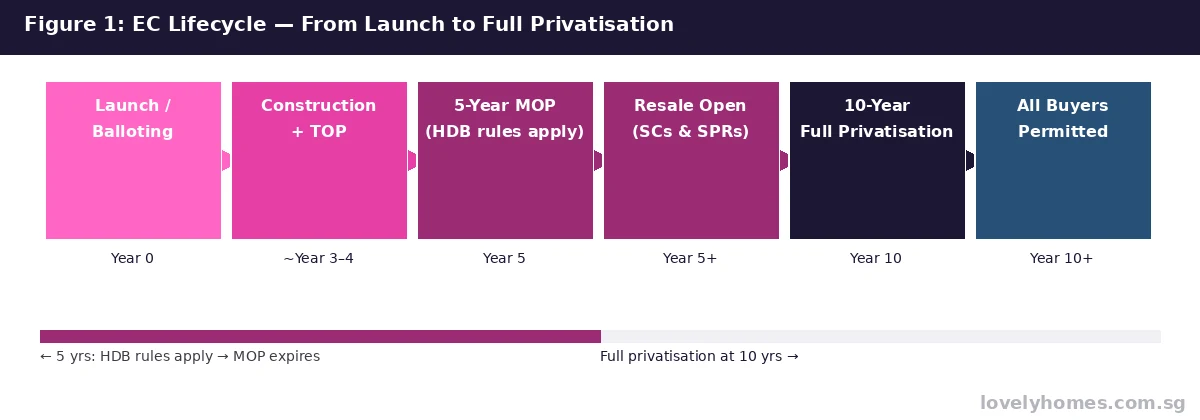

EC Resale: The Two Distinct Windows

Understanding the timeline is essential because EC resale operates under fundamentally different rules depending on when you buy:

Window 1 — After 5-Year MOP, Before 10-Year Full Privatisation

Once the EC’s 5-year MOP has been served (calculated from the date of the Temporary Occupation Permit, not key collection), the original HDB-scheme owner may sell to Singapore Citizens or Singapore Permanent Residents in the open market. During this window, HDB eligibility restrictions still apply:

- Eligible buyers: Singapore Citizens and Singapore PRs only (foreigners cannot buy).

- The Ethnic Integration Policy (EIP) applies — buyers must comply with the ethnic quota for the block and neighbourhood.

- No income ceiling applies to resale buyers (income limits are only for new EC applicants).

- Bank loan only — HDB loans are not available for any EC purchase, new or resale.

Window 2 — After 10-Year Full Privatisation

After 10 years from the EC’s completion (TOP date), the development is fully privatised and HDB restrictions are lifted entirely. From this point, the EC is treated identically to any private condominium for all purposes:

- Eligible buyers: Singapore Citizens, Singapore PRs, foreigners, and companies.

- No EIP applies.

- ABSD at full private condo rates applies to foreigners (60% from February 2023).

- Seller’s Stamp Duty (SSD) obligations for original buyers were served under private-condo rules.

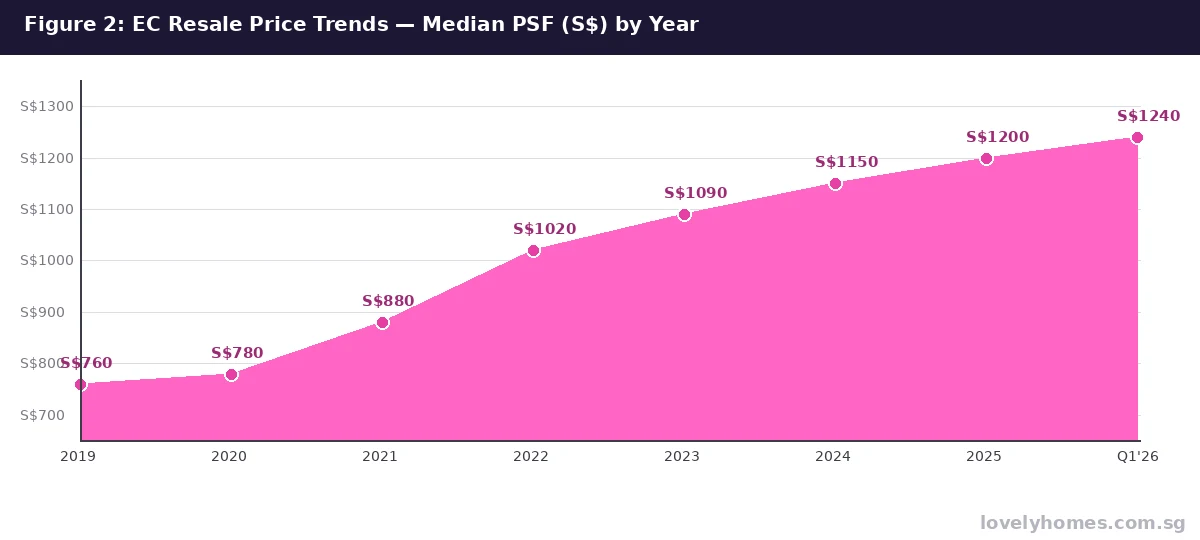

EC Resale Price Trends 2019–2026

EC resale prices have outperformed many market segments over the post-COVID recovery and tightening cycle. The key drivers of EC resale price appreciation include:

- Supply scarcity: EC launches are far fewer in number than HDB BTO launches, and the total stock of ECs is limited. With only a handful of projects entering the resale window each year, demand consistently outpaces supply.

- Upgrader demand: ECs appeal primarily to HDB upgraders — households who have served their HDB MOP and are looking to move into condo-style living at a price point below new private launches. This demand is structural and persistent.

- Location quality: Most ECs are sited in mature or established towns (Tampines, Sengkang, Jurong, Woodlands) with good MRT and bus connectivity, making them attractive as primary residences rather than pure investment plays.

- No income ceiling at resale: Resale buyers face no income ceiling, unlike new EC applicants who are capped at S$16,000/month household income. This broadens the resale buyer pool considerably.

As at Q1 2026, industry figures show median EC resale prices at approximately S$1,200–S$1,240 PSF, with some mature-estate ECs transacting above S$1,400 PSF. This compares to typical new EC launch prices of S$1,350–S$1,500 PSF — meaning a well-located resale EC is often priced comparably to a new launch, but with the benefit of knowing the actual unit and finished state.

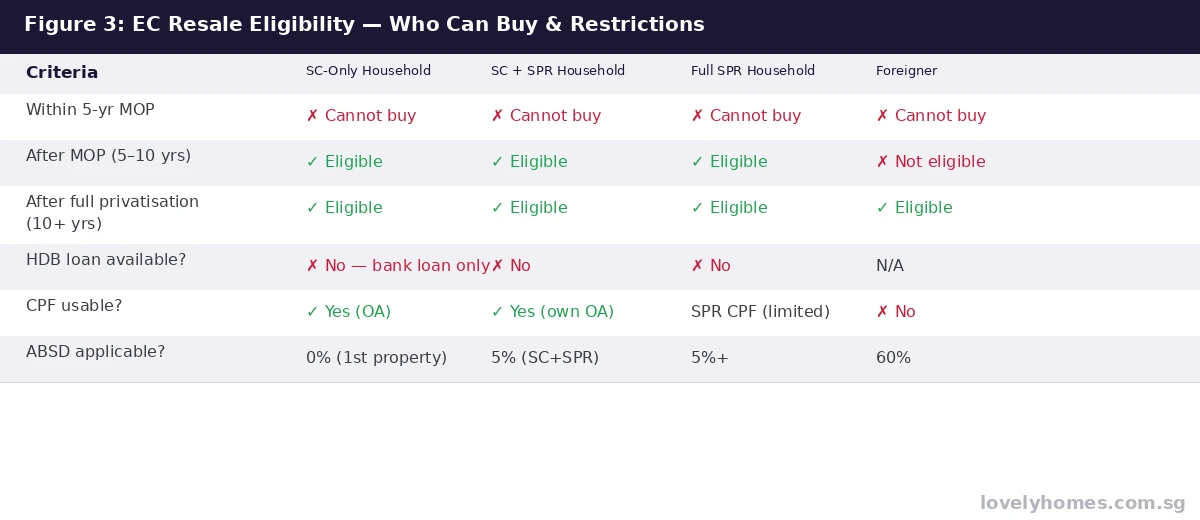

Eligibility, Restrictions and Stamp Duties

| Buyer Profile | 5–10 Yr Window | After 10 Yrs | ABSD (1st Property SC) | ABSD (2nd Property SC) |

|---|---|---|---|---|

| SC only household | Eligible | Eligible | 0% | 20% |

| SC + SPR household | Eligible | Eligible | 5% (on full purchase price) | 20%+ (SC rate applies) |

| Full SPR household | Eligible | Eligible | 5% | 30% |

| Foreigner | Not eligible | Eligible | 60% | 60% |

| Singapore company | Not eligible | Eligible | 35% | 35% |

Buyer’s Stamp Duty (BSD)

BSD applies to all EC resale purchases at the standard residential rates: 1% on the first S$180,000, 2% on the next S$180,000, 3% on the next S$640,000, 4% on the next S$500,000, 5% on the next S$1,500,000, and 6% on the remainder above S$3,000,000. BSD is administered by IRAS and must be paid within 14 days of the date of acceptance of the Option to Purchase (OTP).

CPF and Loan Rules

Bank loan only — HDB loans are not available for any EC purchase, including resale. The maximum Loan-to-Value (LTV) ratio is 75% of the property value (or purchase price, whichever is lower) for a first housing loan from a bank, subject to the Mortgage Servicing Ratio (MSR) of 30% of gross monthly income and the Total Debt Servicing Ratio (TDSR) of 55%, both administered by the Monetary Authority of Singapore (MAS).

CPF Ordinary Account (OA) funds may be used to service the loan and pay the downpayment for SC and SPR buyers, subject to the CPF Withdrawal Limit (WL) and Valuation Limit (VL) rules. Once CPF withdrawals hit the VL (equal to the lower of the purchase price or valuation), further withdrawal requires the property’s remaining lease to cover the youngest buyer to age 95.

The Resale Process: From OTP to Keys

The EC resale process is broadly similar to a private condominium resale and is governed by the Conveyancing and Law of Property Act (Cap 61) and standard Law Society of Singapore conditions of sale. Key milestones include:

| Step | Timeline | Key Actions |

|---|---|---|

| 1. Option to Purchase (OTP) | Day 0 | Seller grants OTP; buyer pays 1% option fee (typically). OTP is valid 14 days. |

| 2. Exercise OTP | Day 7–14 | Buyer exercises OTP, pays 4% exercise fee (cash); BSD due within 14 days of exercise. |

| 3. HDB resale checklist (if applicable) | Day 7–14 | Required if seller is an original HDB-scheme EC owner within the 5–10 year window. |

| 4. Engage solicitors | Day 7–21 | Both parties engage conveyancing solicitors (same firm only with conflict-of-interest waiver). |

| 5. Secure bank loan & CPF approval | Week 2–6 | Letter of Offer from bank; CPF OA withdrawal letter of authority. |

| 6. Completion | Week 8–12 | Balance purchase price paid; keys handed over; SLA caveat registered. |

Worked Example: The Lim Family, EC Resale in Sengkang

Mr and Mrs Lim are Singapore Citizens with a combined gross income of S$14,000/month. They are currently in HDB MOP (completed in March 2026) and are looking to upgrade to a 4-bedroom EC resale unit in Sengkang priced at S$1,480,000. The EC obtained its TOP in 2019 and has been in its resale window since 2024.

Stamp duties:

- BSD: 1% x S$180,000 = S$1,800 + 2% x S$180,000 = S$3,600 + 3% x S$640,000 = S$19,200 + 4% x S$480,000 = S$19,200 = S$43,800

- ABSD: 0% — SC household, first property (HDB sold simultaneously with EC purchase, remission applied)

- Total stamp duties: S$43,800

Financing:

- Bank loan: 75% LTV = S$1,110,000 (bank offers S$1,110,000 at 3.1% for 25 years)

- Monthly instalment: approximately S$5,324/month; MSR = 38.0% — EXCEEDS 30% MSR cap

- MSR adjustment: Maximum loan at 30% MSR = S$4,200/month. Reverse-engineer loan: approximately S$878,500 at 3.1% for 25 years.

- Revised LTV: S$878,500 / S$1,480,000 = 59.4%. Downpayment: S$601,500 (5% cash S$74,000 + 20% CPF/cash S$226,000 + additional S$301,500).

Note: The Lims should explore a 30-year tenure — at 3.1% for 30 years, S$1,110,000 = approximately S$4,740/month (MSR 33.9%, still above cap). Even at 30 years, the MSR constraint limits their borrowing. The EC at S$1,480,000 may be at the upper end of their budget. A S$1,300,000 unit would produce MSR of ~30.0% (just within cap) at 30 years, making it the comfortable maximum.

Why ECs Represent a Compelling Upgrader Proposition

From a financial-planning perspective, ECs offer something private condominiums typically do not: the ability to tap CPF housing grants at the new-launch stage (up to S$30,000 for first-timer families), combined with private condo facilities and a historically strong resale trajectory. The “wait and see” option that many HDB upgraders exercise — waiting for EC resale after MOP rather than committing to new private — reflects the consensus that EC resale offers better value-for-money than a new private launch of comparable size and location.

For investors buying a fully privatised EC (post-10-year window), the product trades essentially as a private condominium with a slightly lower absolute price. Rental yields on mature ECs have ranged from 3.0% to 4.5% gross as at early 2026, broadly comparable to the OCR private condominium market.

What Might Come Next: EC Policy and Supply Outlook

This section is editorial speculation and does not constitute confirmed government policy.

The government has signalled its intent to calibrate EC supply to demand, with the 2H2026 Government Land Sales (GLS) programme including two EC sites. With approximately 5,000–6,000 new EC units expected to enter the market annually over 2026–2029 from recent launches, supply in the resale window should gradually increase. This may exert some moderation on the near-term price trajectory, though structural upgrader demand is expected to remain supportive. Any change to the income ceiling for new EC applicants (currently S$16,000/month) could affect the buyer pool for new launches without directly impacting resale eligibility.

Frequently Asked Questions

Can I use my CPF to buy an EC resale unit?

Yes, Singapore Citizens may use their CPF Ordinary Account (OA) savings to pay for the downpayment and service the mortgage on an EC resale purchase, subject to the CPF Withdrawal Limit (WL) and Valuation Limit (VL). The VL is equal to the lower of the purchase price or the property’s valuation at the time of purchase. Once CPF withdrawals reach the VL, you may only continue withdrawing if the property’s remaining lease covers the youngest buyer to at least age 95. Singapore PRs may use their CPF OA too, but the rules on VL and lease coverage apply equally to them.

Is ABSD payable on an EC resale purchase?

It depends on your profile and property count. For a Singapore Citizen purchasing their first residential property (i.e., the HDB flat has been or will be sold), ABSD is 0%. For a Singapore Citizen purchasing a second property, ABSD is 20% on the full purchase price. SC + SPR joint buyers pay 5% ABSD on any purchase. PRs purchasing their first property pay 5%; second property 30%. Foreigners pay 60% regardless of property count. ABSD is administered by IRAS and must be paid within 14 days of the OTP exercise date.

What is the difference between the EC MOP and the HDB MOP?

Both are 5-year periods, but they are measured from different dates. The HDB MOP for BTO flats is measured from the date of flat possession (key collection). The EC MOP is measured from the date the Temporary Occupation Permit (TOP) is issued for the development — not from when individual buyers receive their keys, and not from the Sales & Purchase agreement date. This means that if you purchased an EC before TOP was issued (i.e. at launch), your MOP countdown does not start until the building physically completes and receives its TOP.

Can an EC resale buyer get an HDB loan?

No. HDB concessionary loans are not available for any EC purchase — new or resale, within or outside the MOP window. This is a hard rule under the EC scheme: all EC financing must be through a licensed financial institution (bank or finance company). The absence of the HDB loan option means EC buyers must have at least 5% of the purchase price in cash (the minimum bank downpayment) and must qualify under the bank’s credit assessment, MSR, and TDSR criteria.

Does the Ethnic Integration Policy apply to EC resale?

Yes, but only within the 5-to-10-year window (before full privatisation). During this period, EC resale transactions are subject to the EIP quotas administered by HDB — the buyer’s ethnicity must not cause the EC block or neighbourhood to exceed its allocated proportion for that ethnic group. After full privatisation (10 years from TOP), the EIP ceases to apply and the EC trades as a fully private development with no ethnic quota restrictions. You can check EIP quota availability for a specific EC on the HDB e-Service portal.

What is the Seller’s Stamp Duty situation for EC resale sellers?

Seller’s Stamp Duty (SSD) for residential properties, administered by IRAS, applies when you sell within 3 years of purchase: 12% if sold in year 1, 8% in year 2, and 4% in year 3. For EC original owners, SSD is assessed from the date the Sales & Purchase agreement was signed (i.e. the launch purchase date). Since ECs typically have a 5-year MOP, any sale after MOP will be at least 5 years after purchase, well past the 3-year SSD window. For resale buyers who subsequently re-sell, the SSD clock restarts from their own purchase date.

Is there any income ceiling for buying an EC in the resale market?

No. The S$16,000/month household income ceiling only applies to applicants for new EC launches (where the developer applies HDB eligibility criteria at point of sale). It does not apply to EC resale buyers at any stage. A household earning S$50,000/month could freely purchase an EC resale unit after MOP without any income-related restriction. This is one of the key attractions of EC resale compared to applying for a new EC launch.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Private Property Buying Costs 2026: All-In Cost Guide

- Singapore HDB Resale Levy Guide 2026: What Second-Timer Flat Buyers Pay

- Singapore Joint Property Ownership Guide 2026: JT, TiC, ABSD and CPF

- Singapore CPF Housing Grant Guide 2026: EHG, PHG, Family Grant

- HDB Minimum Occupation Period (MOP) Singapore 2026: Complete Guide

- Singapore Buyer’s Stamp Duty (BSD) 2026: Rates and Calculations

Disclaimer

This article is produced by the LovelyHomes Editorial Team for general information purposes only. It is not legal, tax, or financial advice. EC eligibility rules, stamp duty rates, and CPF withdrawal limits are subject to change; always verify current requirements with hdb.gov.sg, iras.gov.sg, and mas.gov.sg before committing to any property transaction. Consult a licensed financial adviser and conveyancing solicitor for advice tailored to your circumstances.