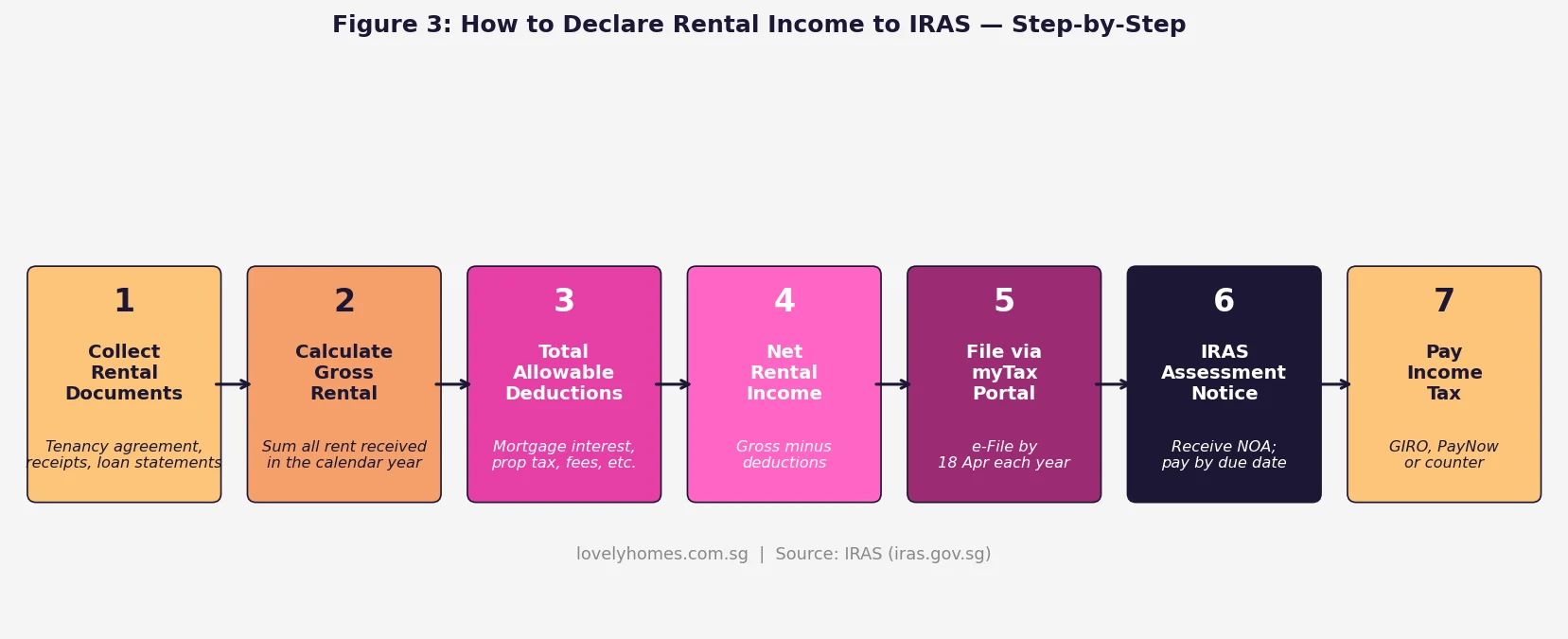

Singapore TDSR Guide 2026: Total Debt Servicing Ratio Explained

Click anywhere to close

⚡ Quick Answer: TDSR Singapore 2026

- TDSR stands for Total Debt Servicing Ratio — a MAS rule capping all monthly debt repayments at 55% of gross monthly income.

- All debts count: mortgage, car loan, personal loan, student loan, credit line, renovation loan — every obligation.

- HDB and EC buyers face two limits: TDSR 55% (all debts) and MSR 30% (the HDB/EC mortgage alone).

- Gross income is used, including CPF. Variable income (commission, bonuses) is typically haircut by 30%.

- TDSR was reduced from 60% to 55% on 30 September 2022 — the tightening that cooled the 2022 market.

- Banks stress-test at a slightly higher rate than your actual rate to ensure you can cope with rate rises.

- Exceeding 55% = loan declined — no exceptions under MAS Notice 645 for residential property loans.

What Is TDSR and Why Did MAS Introduce It?

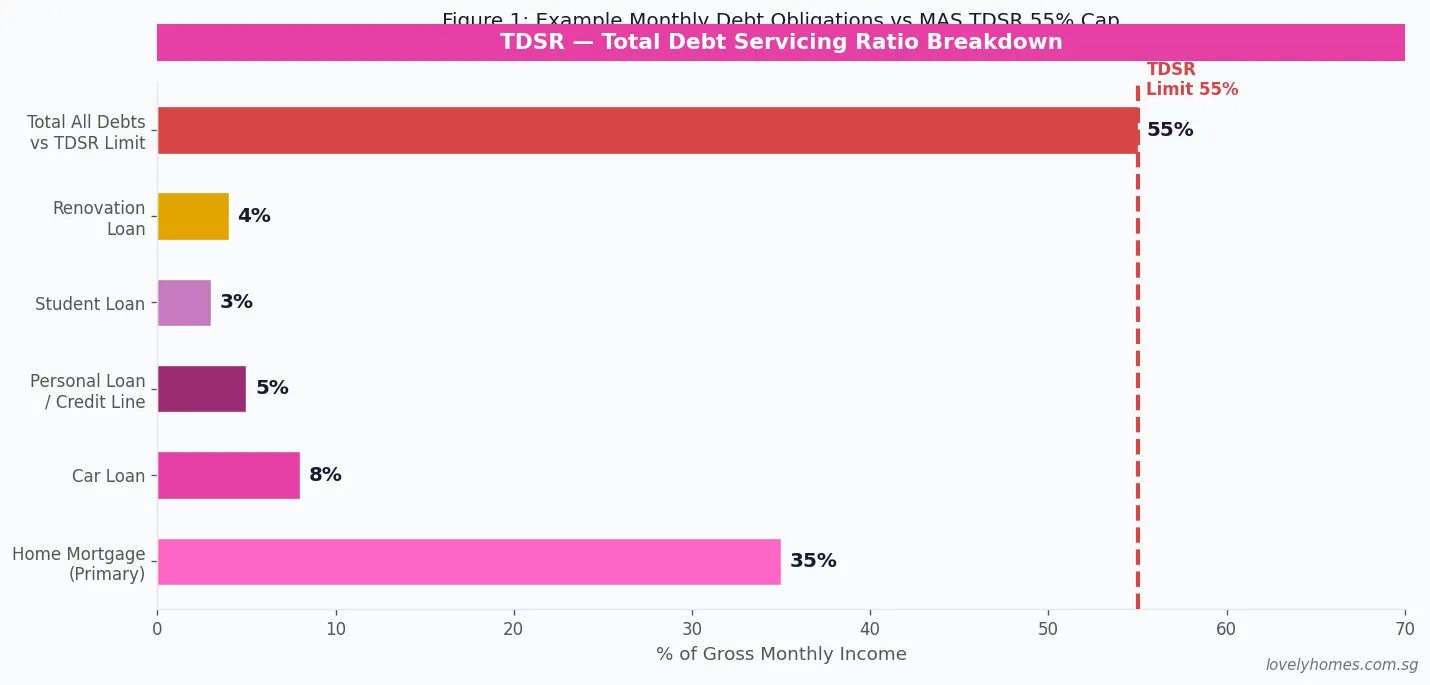

The Total Debt Servicing Ratio (TDSR) is a financial prudential measure introduced by the Monetary Authority of Singapore (MAS) on 29 June 2013 under MAS Notice 645. It requires every MAS-regulated financial institution in Singapore to verify that a borrower’s aggregate monthly debt obligations — across all loans, not just the new mortgage — do not exceed 55% of gross monthly income before extending a property loan.

The policy was created in response to a prolonged low-interest-rate environment that was encouraging households to borrow heavily for property. Without TDSR, a borrower could theoretically obtain a mortgage even if their total monthly repayments consumed 80% or more of their income. TDSR closed that gap by introducing a single universal ceiling enforced across all lenders simultaneously.

On 30 September 2022, MAS tightened the TDSR from 60% to its current 55%, as part of a package of property cooling measures. This 5-percentage-point reduction effectively cut maximum loan sizes by approximately 8-10% and is credited with contributing to the slower price growth seen in 2023 through 2025.

How TDSR Is Calculated

The TDSR formula is:

Must be ≤ 55% for a residential property loan to be approved under MAS Notice 645.

Gross monthly income includes fixed salary (before CPF deduction), allowances, and discounted variable pay. Variable components — commissions, overtime, bonuses, rental income — are typically reduced by 30% (i.e., the bank counts only 70% of such income). Self-employed borrowers must provide at least two years of IRAS Notices of Assessment; the bank uses the lower of the two-year average or the latest year’s net trade income, often with a further haircut.

Total monthly debt obligations covers: the proposed new property mortgage (at the bank’s applicable stress-test rate, which may be 0.5%–1% above your actual rate), all existing property loans, car hire purchase instalments, personal loan repayments, student loan repayments, credit card minimum payments (typically 5% of outstanding balance per month), and renovation loans.

If you own another property with an outstanding mortgage, that entire monthly repayment is included in your TDSR calculation for any new loan application. This is the key reason why owning multiple properties progressively reduces your borrowable amount on each subsequent purchase.

TDSR for Different Property Types

The TDSR framework applies to all property loans extended by MAS-regulated financial institutions, but the practical constraints differ by property type:

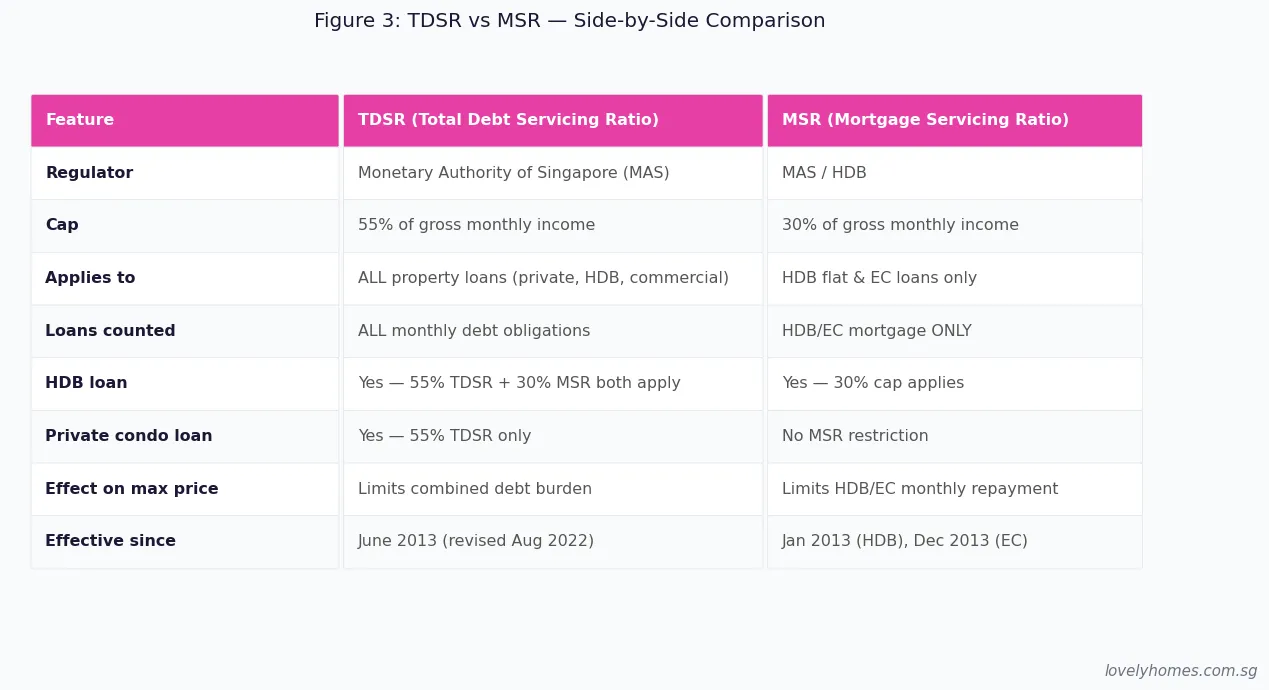

Private residential (condominiums, apartments, landed homes): TDSR 55% applies. There is no separate MSR restriction. LTV starts at 75% for a first property, falling to 45% and 35% for second and subsequent properties respectively.

HDB resale flats (bank loan): Both TDSR 55% and MSR 30% apply simultaneously. MSR requires that the monthly HDB mortgage payment alone must not exceed 30% of gross income. MSR is usually the binding constraint for most HDB buyers since 30% is typically hit before the 55% TDSR ceiling.

HDB resale flats (HDB loan): The HDB Concessionary Loan is administered by HDB, not subject to MAS Notice 645 in the same way, but HDB applies its own 30% MSR equivalent. The HDB loan rate is pegged at 0.1% above the CPF OA rate, currently 2.6% per annum (effective 1 January 2026).

Executive Condominiums: Both TDSR 55% and MSR 30% apply at point of purchase. After the five-year mark, once an EC is privatised, resale buyers are only subject to TDSR (no MSR restriction).

Commercial and industrial property: TDSR applies but MAS sets the cap for non-residential property loans at 60% — a more lenient threshold than the 55% residential cap.

TDSR and MSR — Summary Table

| Loan / Property Type | TDSR Cap | MSR Cap | LTV (1st Prop.) | Notes |

|---|---|---|---|---|

| Private condo / landed (1st property) | 55% | None | 75% | 5% cash + CPF for balance of DP |

| Private condo / landed (2nd property) | 55% | None | 45% | 25% cash mandatory downpayment |

| Private condo / landed (3rd+ property) | 55% | None | 35% | 25% cash mandatory downpayment |

| HDB resale flat (bank loan) | 55% | 30% | 75% | Both caps apply; MSR typically binds first |

| HDB resale flat (HDB loan) | N/A | 30% | 80% | No cash DP required; CPF OA used |

| Executive Condominium (at launch) | 55% | 30% | 75% | 5% cash booking fee; MSR applies |

| Commercial / industrial property | 60% | None | Up to 70% | Higher TDSR cap for non-residential loans |

Worked Example: Mr and Mrs Ong Buy Their First Private Condo

Mr and Mrs Ong are a Singapore Citizen couple. Combined gross monthly income: S$12,000 (Mr Ong S$7,500 fixed; Mrs Ong S$4,500, of which S$2,000 is commission).

Existing debts: car hire purchase S$850 per month; personal loan S$300 per month.

Target property: OCR 3-bedroom condo at S$1,500,000. Bank loan 75% LTV = S$1,125,000 over 30 years at 3.2% p.a. Monthly repayment: approximately S$4,862.

Income adjustment: Mrs Ong’s S$2,000 commission is haircut by 30% (bank counts S$1,400). Qualifying income = S$7,500 + S$2,500 fixed + S$1,400 variable = S$11,400 per month.

TDSR calculation: Total obligations = S$4,862 (new mortgage) + S$850 (car) + S$300 (personal) = S$6,012 per month. TDSR = S$6,012 ÷ S$11,400 = 52.7% — below the 55% cap. Loan approved (subject to credit assessment and valuation).

Sensitivity: If the Ongs wished to buy at S$1,700,000 instead (loan S$1,275,000, repayment ~S$5,517), total obligations would rise to S$6,667, giving TDSR = 58.5% — which exceeds 55%. The S$1,700,000 purchase would be declined unless they clear the car loan (saving S$850/mth) or increase their qualifying income.

Why TDSR Matters: Singapore in Global Context

Singapore’s TDSR framework is widely regarded as one of the most comprehensive income-based mortgage controls in the Asia-Pacific region. Countries like Australia and the UK use similar debt-to-income concepts in their macroprudential toolkits, but Singapore’s version is legally binding on all lenders — there is no discretion to override it for high-net-worth clients or particularly creditworthy borrowers.

The practical effect is a structurally cautious mortgage market. Singapore mortgage arrears remain among the lowest in Asia, and the 2022 cooling measures (which included the TDSR tightening) contributed to a soft-landing scenario rather than a sharp price correction. For buyers, this means the market is protected from speculative excess, but also that stretching to buy at the top of your affordability range carries real interest-rate risk if rates rise post-purchase.

What Might Change in TDSR Policy

MAS reviews the TDSR threshold as part of its broader macroprudential toolkit, typically alongside reviews of LTV limits and stamp duty rates. With the 3-month compounded SORA having eased to approximately 1.0% in early 2026, some market observers have speculated whether MAS might loosen the TDSR to 60% if sustained rate normalisation persists. However, as at June 2026, no public consultation or announcement has been made. Prospective buyers should plan all financing decisions on the current 55% threshold and not rely on any anticipated easing.

Frequently Asked Questions

Does CPF count as income in the TDSR formula?

The gross monthly income used in TDSR is your gross salary before CPF deduction. CPF contributions are not separately added — they are already implicit in the gross figure. However, CPF OA contributions do help service the mortgage (reducing your cash outlay), which gives HDB buyers and those using CPF for loan repayment meaningful payment relief even though the income figure itself is unchanged in the TDSR calculation.

Can I exclude a loan that will be fully paid in six months?

Some banks will exclude short-term residual debt (typically fewer than 6 to 12 months remaining) from the TDSR calculation at their discretion, since such obligations will not affect long-term serviceability. Policies differ by bank. If your car loan has only a few months left, it is worth asking your mortgage banker whether it will be included. Alternatively, fully clearing the loan before applying can improve your TDSR ratio — and often has an outsized positive impact on your maximum loan quantum.

What if my TDSR exceeds 55%?

A bank is required under MAS Notice 645 to decline your application if TDSR exceeds 55%. There is no exception or waiver for residential property loans. Your options are to: (a) make a larger downpayment to reduce the loan amount and therefore the monthly mortgage obligation; (b) clear existing debts before applying; (c) choose a lower-priced property; or (d) add a co-borrower whose income improves the combined TDSR, provided that person’s debts do not make things worse.

How is TDSR calculated for the self-employed?

Banks require at least two years of IRAS Notices of Assessment and, for incorporated businesses, audited or signed financial statements. Qualifying income is typically the lower of the two-year average or the most recent year’s net trade income. Many banks apply an additional haircut of 20–30% on top of this. Self-employed borrowers should expect their qualifying income to be assessed conservatively, which reduces their maximum mortgage relative to a salaried employee with the same stated earnings.

Does TDSR apply when I refinance?

Yes. Refinancing is a new loan application and must satisfy TDSR at the time of application. If your financial circumstances have changed since your original purchase — new debts, a drop in income — you may find you fail the current TDSR test even if you passed it years ago. This is an important practical risk for borrowers on fixed-rate packages coming up for repricing who intend to switch lenders.

Is TDSR the same as DSCR?

No. TDSR is a consumer-lending rule for individuals applying for property loans in Singapore. DSCR (Debt Service Coverage Ratio) is a commercial-lending metric used for corporate or commercial real estate loans; it measures whether a property’s net operating income covers its debt service. A residential buy-to-let investor is subject to TDSR on the individual borrower side; a developer or company owning commercial property typically uses the DSCR framework instead.

Joint purchase — is TDSR calculated on combined income?

Yes. Joint borrowers’ incomes are pooled and their debts are also pooled. This generally allows a couple to qualify for a much larger loan than either could secure individually. However, if one co-borrower carries significant debts (a large car loan, for instance), those debts also enter the combined TDSR calculation and reduce the joint loan quantum. Both parties will need to provide full income and liability documentation.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Property Downpayment Guide 2026: How Much Cash and CPF You Need

- HDB Loan vs Bank Loan Singapore 2026: Which Saves You More?

- Singapore Private Property Buying Costs 2026: All-In Cost Guide

- Stamp Duty Remission Guide 2026: ABSD Upgrader Refunds

- Condo Buying Guide for HDB Upgraders 2026

- Using CPF to Buy Private Property Singapore 2026

Disclaimer: This article is for general informational purposes only and does not constitute financial, tax, or legal advice. TDSR rules and MAS policies are subject to change without notice. All borrowers should seek independent advice from a licensed financial adviser or mortgage broker, and verify current rules directly with the Monetary Authority of Singapore at mas.gov.sg and the Housing & Development Board at hdb.gov.sg.