HDB Resale Procedure Guide 2026: Step-by-Step for Buyers and Sellers

Quick Answer: HDB Resale in 2026 — Key Facts

- Who manages HDB resale: the Housing & Development Board (HDB) via the HDB Resale Portal (my.hdb.gov.sg).

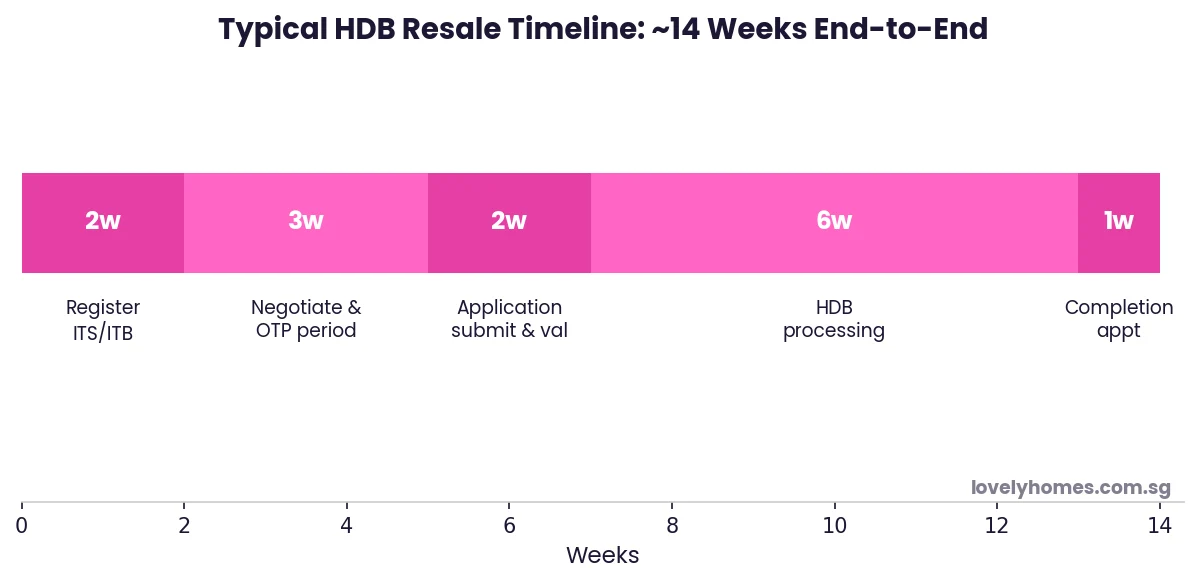

- Process duration: typically 8–14 weeks from OTP exercise to legal completion.

- Option to Purchase (OTP): validity up to 21 calendar days; option fee S$1–S$1,000 (non-refundable); exercise fee S$1–S$5,000.

- Both parties must submit resale application within 7 days of OTP exercise — failure may invalidate the transaction.

- Grants available: EHG (up to S$120,000), Family Grant (up to S$50,000), Proximity Housing Grant (S$20,000–S$30,000), Singles Grant — subject to eligibility.

- Minimum Occupation Period (MOP): sellers must have occupied the flat for the MOP (typically 5 years) before listing for resale. Prime and Plus flats have enhanced MOP rules.

- Ethnic Integration Policy (EIP): buyers must ensure the resale does not breach HDB’s EIP quota for the block and neighbourhood before exercising the OTP.

- HDB loan vs bank loan: HDB loan offers up to 80% LTV at the concessionary rate (2.6% p.a. as at 2026); bank loans offer up to 75% LTV but competitive variable rates.

What Is the HDB Resale Market?

HDB resale flats are Housing & Development Board flats that have completed their Minimum Occupation Period (MOP) and are being sold by existing flat owners on the open market — as opposed to new BTO (Build-To-Order) or SBF (Sale of Balance Flats) exercises directly from HDB. The resale market offers buyers immediate availability and greater locational choice than BTO exercises, but at higher prices and without the benefit of the new-flat purchase price.

As at the second quarter of 2026, the HDB resale market is active: the HDB regularly publishes resale transaction data showing strong demand across mature and non-mature estates alike. Understanding the resale procedure thoroughly — from the first portal registration through to the handover of keys — is essential for both buyers and sellers navigating this market.

The HDB Resale Portal (accessible via my.hdb.gov.sg with a Singpass login) is the single platform through which all HDB resale transactions are managed. Both buyers and sellers must use this portal, and all key milestones — Intent to Sell, Intent to Buy, resale application, valuation request, and approval confirmation — flow through it.

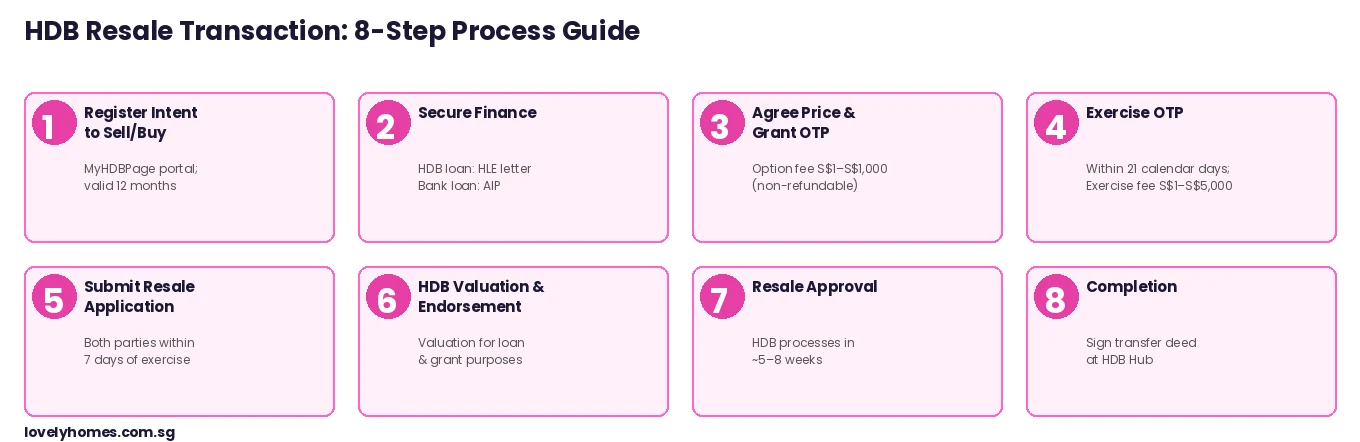

Figure 1: HDB resale transaction — 8 core steps from registration to completion. Source: HDB, LovelyHomes.

Step 1: Register Intent to Sell (Seller) and Intent to Buy (Buyer)

Sellers must register their Intent to Sell (ITS) on the HDB Resale Portal before marketing the flat. This registration is valid for 12 months and can be done at any time — there is no fee. Once the ITS is active, the portal generates an indicative valuation range, a list of financial planning requirements, and eligibility details including whether any co-owners need to be involved. Sellers cannot grant an OTP to a buyer before registering ITS.

Buyers register their Intent to Buy (ITB) on the portal. This is where eligibility checks are made: HDB verifies whether the buyer meets the citizenship and family nucleus requirements, whether the EIP quota is available at the target flat, and whether the buyer has a valid HDB Loan Eligibility (HLE) letter or a bank Approval In Principle (AIP). The ITB is also valid for 12 months.

Both registrations can be done concurrently — buyers and sellers do not need to find each other before registering. In practice, most buyers register ITB first (to get their finances ready) before actively searching for a flat.

Step 2: Secure Financing — HLE Letter or Bank AIP

Before proceeding to the OTP stage, buyers must have their financing in place. There are two routes:

| Feature | HDB Concessionary Loan | Bank Loan |

|---|---|---|

| Maximum LTV | 80% of lower of valuation/price | 75% of lower of valuation/price |

| Interest rate (2026) | 2.6% p.a. (pegged to CPF OA rate + 0.1%) | Variable; fixed/floating packages from ~2.5%–3.8% p.a. |

| MSR limit | 30% of gross monthly household income | 30% of gross monthly household income (HDB flats) |

| TDSR | 55% (applies in conjunction with MSR) | 55% |

| Cash down payment | Minimum 20% (CPF OA can cover) | Minimum 25% (5% must be in cash) |

| Eligibility | SC/SC or SC/SPR households; income ceiling S$14,000/mth | All eligible flat buyers |

| Prepayment penalty | None | Depends on package (typically 1.5% for fixed-rate packages) |

A HDB Loan Eligibility (HLE) letter must be obtained from HDB before the buyer can proceed if using an HDB loan. The HLE is valid for 6 months and must be renewed if it lapses before the OTP is exercised. For bank loans, an Approval In Principle (AIP) from the bank serves the equivalent role.

The Mortgage Servicing Ratio (MSR) cap of 30% of gross household income applies specifically to HDB flat purchases. This is more restrictive than the general TDSR of 55% — buyers with higher incomes buying higher-priced resale flats may find the MSR the binding constraint on their loan quantum.

Step 3: Negotiate Price and Grant the Option to Purchase (OTP)

Once buyer and seller agree on a price, the seller issues an Option to Purchase. The OTP is a legally binding option contract: the buyer pays an option fee (S$1 to S$1,000 at the seller’s discretion) in exchange for the right to purchase the flat at the agreed price within the OTP validity period.

The OTP validity period must be at least 7 calendar days and no more than 21 calendar days. This gives the buyer time to exercise the option (i.e., formally commit to buy) while providing a brief cooling-off window. A buyer who decides not to exercise the option forfeits the option fee but has no further obligation to proceed.

Key negotiating points at this stage include: whether the seller agrees to include any fittings (air-conditioners, kitchen cabinets, curtain tracks), the completion timeline, and the allocation of expenses such as property tax for the partial year. These should be documented in the OTP or in a separate Schedule of Fixtures.

Step 4: Exercise the Option to Purchase

To exercise the OTP, the buyer signs the OTP and pays the exercise fee (S$1 to S$5,000) to the seller. Once exercised, the transaction is legally binding on both parties — neither party can withdraw without facing legal consequences. The exercise fee forms part of the overall purchase price (i.e., it is not a separate cost on top of the agreed price).

Before exercising, the buyer should: (a) confirm the EIP quota is available (this can be checked on the HDB Resale Portal using the flat’s postal code), (b) confirm the flat’s resale levy status if upgrading from a subsidised flat, and (c) confirm the CPF and cash amounts needed for completion. Exercising the OTP without completing these checks can result in a failed transaction and forfeiture of the exercise fee.

Figure 2: Typical HDB resale timeline — ~14 weeks end-to-end from registration to completion. The longest phase is HDB processing (5–8 weeks). Source: HDB, LovelyHomes.

Step 5: Submit Resale Application (Both Parties, Within 7 Days)

After the OTP is exercised, both the buyer and seller must each submit their respective halves of the resale application on the HDB Resale Portal within 7 days of the OTP exercise date. This is a strict requirement — failure by either party to submit within 7 days may cause the application to lapse and require the OTP to be re-issued.

The buyer’s application requires: confirmation of financing (HLE letter or bank AIP), CPF withdrawal details, grant applications (EHG, Family Grant, etc.), and SPR/citizenship verification. The seller’s application requires: confirmation of bank loan redemption details (if there is an outstanding mortgage), CPF refund instructions, and details of any co-owners.

HDB will send an SMS or email to both parties confirming receipt of the complete application and providing an estimated processing timeline.

Step 6: HDB Valuation and Financial Endorsement

For buyers using an HDB concessionary loan, HDB commissions an official valuation of the flat. This valuation determines the loan quantum and the maximum CPF amount that may be used — the LTV ceiling is applied against whichever is lower, the agreed price or the HDB valuation. If the agreed price exceeds the HDB valuation (i.e., there is a Cash-Over-Valuation, or COV), the excess must be paid entirely in cash — CPF cannot be used for COV.

Cash-Over-Valuation became a significant market dynamic in the 2021–2023 resale boom, when median COV for 4-room resale flats in mature estates reached S$30,000–S$60,000. In a more moderate 2026 market, COV remains common in sought-after areas (central districts, near MRT) but has compressed from peak levels.

For bank loan buyers, the bank conducts its own valuation for lending purposes. The buyer should discuss the valuation outcome with the bank’s mortgage specialist before endorsing the financial plan.

Step 7: Resale Approval by HDB

HDB processes the resale application and checks that all eligibility conditions are met: flat ownership rules, EIP compliance, income ceiling (for grants), CPF withdrawal limits, MOP completion, and resale levy (if applicable for second-subsidised-flat buyers). Processing typically takes 5–8 weeks from the complete application date.

HDB notifies both buyer and seller by SMS and email once the resale is approved in principle and a completion appointment is set. At this stage, the conveyancing lawyers for both parties also receive documents to prepare for the transfer of title at completion.

Step 8: Completion Appointment at HDB Hub

The final step is the completion appointment, held at HDB Hub in Toa Payoh (or virtually for eligible straightforward cases). At this appointment:

- Buyer and seller (or their lawyers) sign the Transfer Deed transferring ownership.

- CPF refunds to the seller’s CPF OA account are processed (CPF monies used toward the original flat purchase must be returned with accrued interest).

- The sale proceeds (net of CPF refund, outstanding mortgage redemption, and any resale levy) are disbursed to the seller.

- Stamp duties (BSD, and ABSD if applicable) are confirmed as paid.

- Keys are handed over, and the buyer takes possession of the flat.

The entire process from OTP exercise to completion typically takes 8–12 weeks, though complex cases (outstanding mortgage redemptions, CPF disputes, estate matters) may take longer.

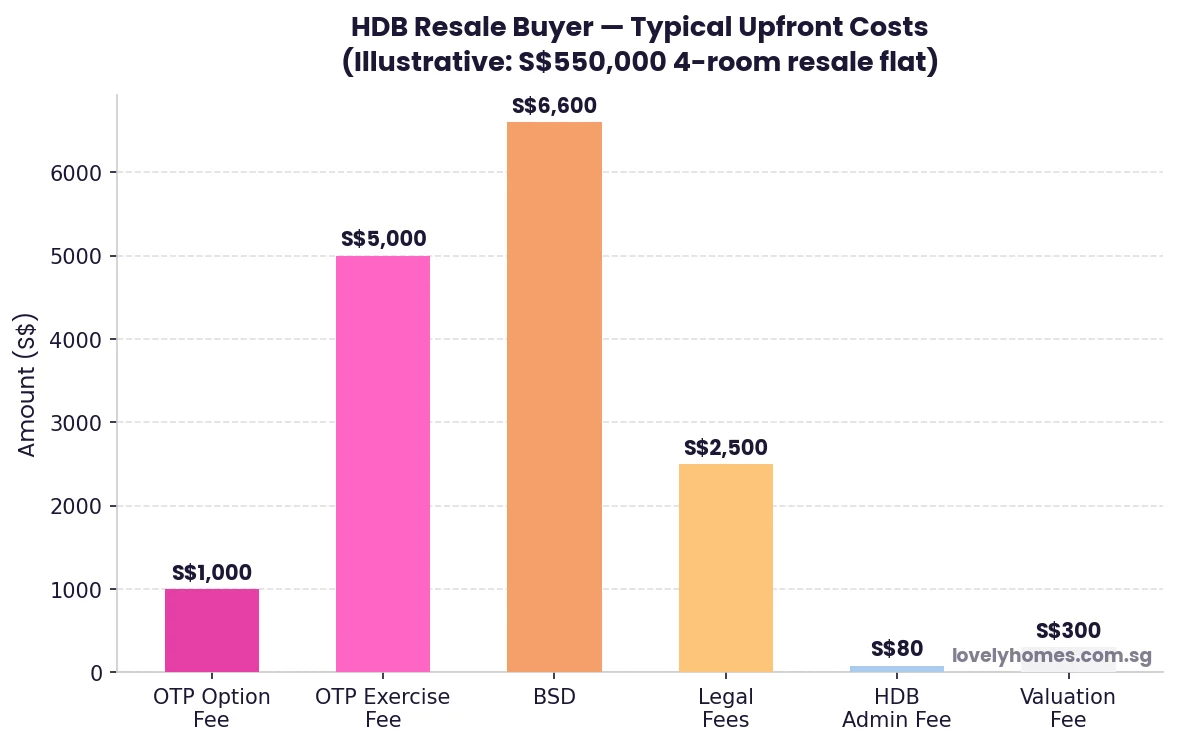

Figure 3: Typical upfront costs for a buyer of a S$550,000 4-room HDB resale flat — excluding grants and CPF housing schemes. Source: HDB, IRAS, LovelyHomes calculations.

HDB Resale Grants: Reducing Your Out-of-Pocket Cost

Eligible first-timer buyers of HDB resale flats may receive substantial CPF grants from HDB to reduce the effective purchase price. The main grants in 2026 are:

| Grant | Maximum Amount | Key Eligibility Conditions |

|---|---|---|

| Enhanced CPF Housing Grant (EHG) | S$120,000 (families); S$60,000 (singles) | At least one first-timer applicant; monthly household income ≤ S$9,000 (families) or ≤ S$4,500 (singles); must buy flat that meets income-tiered price ceiling |

| Family Grant | S$50,000 (SC/SC, 4-room and smaller); S$40,000 (SC/SC, 5-room and larger) | At least one SC applicant; first-timer buying with SC or SPR spouse/fiancé; income ≤ S$14,000/mth |

| Half-Housing Grant | S$25,000 (4-room and smaller); S$20,000 (5-room and larger) | One first-timer, one second-timer applicant in the same household |

| Proximity Housing Grant (PHG) | S$30,000 (moving to be near parents/children within 4km) | SC or PR; living within 4km or in the same town as parents or married child; conditions apply |

| Singles Grant | S$40,000 (SC, 4-room and smaller); S$25,000 (SC, 5-room and larger) | Singapore Citizen aged 35+; first-timer single; resale flat only; income ≤ S$7,000/mth |

Grants are disbursed directly by HDB into the buyer’s CPF OA account and can only be used toward the flat purchase — they cannot be withdrawn as cash. Buyers who receive grants are subject to a resale grant clawback if they sell the flat within 5 years of the grant. Planning the long-term holding horizon is therefore important when maximising grants.

Worked Example: Mr and Mrs Tan’s First HDB Resale Flat

Case Study — 4-room Jurong West Resale, S$550,000

Profile: Mr Tan (SC, 29) and Mrs Tan (SC, 28), first-timer household, combined gross income S$7,500/mth, no existing property.

Target flat: 4-room HDB resale in Jurong West (District 22), agreed price S$550,000. HDB valuation: S$545,000. COV = S$5,000 (to be paid in cash).

Grants:

- EHG: income S$7,500/mth → S$55,000 (income band S$7,001–S$8,000 for families)

- Family Grant (SC/SC, 4-room): S$50,000

- Total grants: S$105,000 — credited to CPF OA

Effective purchase cost after grants: S$550,000 − S$105,000 = S$445,000

Financing: HDB loan at 80% of S$545,000 (valuation) = S$436,000 maximum; MSR check: S$436,000 at 2.6% over 25 years ≈ S$1,982/mth. MSR = 30% × S$7,500 = S$2,250. S$1,982 ≤ S$2,250 → MSR PASS.

Upfront cash/CPF needed (excluding grants):

- Down payment (20% of S$545,000 valuation): S$109,000 — payable from CPF OA or cash

- COV: S$5,000 — must be cash (cannot use CPF for COV)

- BSD: (S$180k×1%) + (S$180k×2%) + (S$190k×3%) = S$1,800 + S$3,600 + S$5,700 = S$11,100 (payable via CPF OA)

- Legal fees (buyer’s conveyancing): ~S$2,500

- OTP option fee (non-refundable): up to S$1,000

- Total cash minimum: ~S$8,500 (COV + legal + option fee)

- CPF OA used: ~S$109,000 + S$11,100 = S$120,100 (offset by S$105,000 grants → net CPF outflow ~S$15,100 if grants insufficient; actual depends on existing CPF OA balance)

This illustrates why first-timer couples with combined income around S$7,500/mth can often purchase a resale 4-room flat in a non-mature estate with relatively modest cash upfront, provided grants are maximised.

What This Means for Buyers and Sellers in 2026

The HDB resale market in mid-2026 is characterised by solid but moderating demand. With the BTO backlog largely cleared and significant new flat supply coming onstream, buyers have more choices than in the 2021–2022 peak. Resale prices in non-mature estates such as Jurong West, Woodlands, and Sengkang have stabilised or softened modestly, while mature estates — particularly those near Thomson-East Coast Line (TEL) stations — continue to command premiums.

For sellers, the 14-week timeline to completion means planning is critical, especially if the sale proceeds are needed to fund a new home purchase. Sellers should align OTP issuance with their own housing timeline to avoid a gap period. Where a new purchase is concurrent, engaging a conveyancing lawyer who can coordinate both transactions is strongly recommended.

For buyers, the combination of a higher-priced resale market and HDB’s 80% LTV cap means the absolute cash and CPF commitment is substantial. Maximising eligible grants — particularly the EHG and Family Grant — is the single most effective way to reduce upfront costs. Buyers should apply for the HLE letter well in advance and factor in the COV risk for popular precincts.

What Might Come Next

The following is analytical commentary based on publicly available signals — not official guidance.

HDB’s June 2026 BTO exercise produced 6,952 flats across 7 projects, with the Prime-classified Berlayar Rise (Bukit Merah) oversubscribed at 4.5× and Lakeview Cascadia (Bishan) at 4.7×. The continued strong demand for Prime and Plus flats signals that buyers remain willing to accept the enhanced MOP and clawback conditions for well-located flats. Over the medium term, as these new Prime/Plus flats reach their MOP in the early 2030s, they will add an entirely new tier of resale transactions subject to the Prime/Plus resale conditions — including clawback on subsidy.

HDB has signalled it will continue to release BTO supply at elevated levels to address the demand backlog. As supply catches up with demand over 2026–2028, resale prices — particularly in non-mature estates — are expected to moderate gradually. Buyers with a long-term horizon and flexibility on location have a strengthening case to wait for upcoming BTO exercises, while those needing immediate occupation continue to turn to the resale market.

Frequently Asked Questions

Can I buy an HDB resale flat without an HLE letter?

Yes — if you are using a bank loan rather than an HDB concessionary loan, you do not need an HLE letter. You would instead provide your bank’s Approval In Principle (AIP) letter as part of the resale application. However, you will need to have registered your Intent to Buy on the HDB Resale Portal and confirmed your financing method before the OTP is issued. If you wish to switch from a bank loan to an HDB loan at any point before completion, you would need to obtain an HLE letter at that stage — switching mid-way can delay the completion timeline.

What is Cash-Over-Valuation (COV) and how does it affect my purchase?

Cash-Over-Valuation (COV) is the difference between the agreed resale price and the HDB or bank valuation of the flat, when the agreed price is higher than the valuation. Because CPF and HDB loan proceeds are capped at a percentage of the lower of the valuation or the agreed price, any COV must be paid entirely in cash. For example, if the agreed price is S$680,000 but HDB’s valuation is S$650,000, the S$30,000 COV must be paid in cash. Buyers should budget for COV when purchasing in popular precincts where demand regularly pushes prices above HDB’s assessed value — checking recent transaction prices on the HDB website before negotiating helps set realistic expectations.

What happens if the HDB resale application lapses?

An HDB resale application lapses if both parties do not submit within 7 days of the OTP exercise, or if required documents are not provided within HDB’s stipulated timeframe. A lapsed application means the transaction does not proceed; the seller is not obligated to return the option fee and exercise fee, and both parties may face legal liability depending on which party caused the lapse. To prevent this, ensure both parties understand the 7-day submission window, and engage conveyancing lawyers before the OTP is exercised — they can guide both parties through the submission process efficiently.

How long does a seller have to vacate the flat after completion?

The transfer of possession happens at the completion appointment. From the completion date, the seller is typically required to vacate the flat immediately or within a very short grace period agreed in the OTP. In practice, seller and buyer may negotiate a short leaseback arrangement (where the seller continues to occupy for a few weeks post-completion as a tenant) if both parties agree and the terms are documented. Such arrangements must be disclosed to HDB as they may affect certain ownership rules. The flat must be vacant and in the agreed condition (with agreed fittings left in place) by the agreed possession date.

Can a Singapore Permanent Resident (SPR) buy an HDB resale flat?

Yes, Singapore Permanent Residents may purchase HDB resale flats — but with important restrictions. An SPR cannot buy an HDB resale flat alone; they must purchase with an SC spouse, child, or parent (i.e., the household must include at least one SC under the family scheme). SPRs applying under the Non-Citizen Spouse Scheme or the Non-Citizen Family Scheme with at least one SC member can proceed. Fully SPR households (no SC member) cannot buy HDB resale flats. SPRs also pay ABSD on the resale purchase (5% for an SPR purchasing a first residential property), while SCs buying their first residential property pay no ABSD.

What is the Resale Levy and when does it apply?

The HDB Resale Levy is a levy payable by second-timer buyers — those who have previously purchased a subsidised HDB flat (BTO, DBSS, or bought a resale flat with CPF housing grants) and now wish to purchase a second subsidised flat. The levy ranges from S$15,000 (2-room) to S$55,000 (5-room), must be paid in cash (not CPF), and is deducted from the sale proceeds of the first flat if the first flat is sold to HDB. The resale levy applies regardless of whether the second purchase is a BTO or a resale flat purchased with grants. Detailed levy amounts by flat type are covered in our dedicated HDB Resale Levy guide.

Do I need a lawyer for an HDB resale transaction?

Yes. Both buyer and seller in an HDB resale transaction are required to engage licensed conveyancing lawyers to represent their respective interests. Lawyers handle the OTP preparation and review, HDB portal submissions, CPF withdrawal applications, BSD and ABSD stamping, title transfer documentation, and coordination with the seller’s bank (for mortgage redemption). HDB maintains a list of conveyancing law firms and recommended panels for HDB transactions. Legal fees for an HDB resale transaction typically range from S$1,800 to S$3,000 for standard cases.

Related Articles

- HDB Resale Levy Singapore 2026: Complete Guide for Second-Timer Buyers

- HDB CPF Housing Grant Guide 2026: EHG, Family Grant, PHG and Singles Grant

- HDB Ethnic Integration Policy (EIP) Singapore 2026

- HDB Prime, Plus and Standard Flats Singapore 2026: Complete Classification Guide

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty Singapore 2026: BSD Rates, Calculation and Remissions

- Singapore Renovation Cost Guide 2026: HDB, Condo & Landed Budgets

Disclaimer

This article is for general informational purposes only and does not constitute legal, financial, or housing advice. HDB resale eligibility criteria, grant amounts, interest rates, MOP requirements, and administrative procedures are set by the Housing & Development Board (HDB), IRAS, and the CPF Board and may change without prior notice. Readers should refer to official sources — www.hdb.gov.sg, www.iras.gov.sg, and www.cpf.gov.sg — for authoritative and up-to-date information. Before any property transaction, consult a licensed conveyancing solicitor and a qualified financial adviser.