Buying an HDB flat in Singapore involves one of the most consequential financial decisions most households will ever make — yet the mechanics of the downpayment are frequently misunderstood. How much cash do you actually need on completion day? How much can come from your CPF? Does it matter whether you take an HDB loan or a bank loan? The answers to these questions determine not just how much you need to have saved, but also how quickly you can buy and how you should be managing your CPF Ordinary Account in the months before applying.

This guide walks through the 2026 HDB downpayment rules in full — the minimum sums, the loan-to-value limits, the CPF rules, and the practical implications of choosing between an HDB concessionary loan and a bank mortgage. All figures reflect the rules administered by the Housing & Development Board (HDB) and the Monetary Authority of Singapore (MAS) as at July 2026.

Quick Answer — HDB Downpayment Singapore 2026

With an HDB loan (LTV 90%): minimum downpayment is 10%, payable entirely from CPF OA or cash — no mandatory cash component.

With a bank loan (LTV 75%): minimum downpayment is 25%, of which at least 5% must be in cash; the remaining 20% can come from CPF OA or cash.

If you have an existing HDB loan or any other outstanding home loan, your LTV drops further — down to 45%–55% depending on the loan count.

HDB loan interest is currently 2.60% per annum (0.10% above the CPF OA rate). Bank rates in 2026 range roughly 2.30%–3.20% depending on the package.

CPF can be used to pay both the downpayment and the monthly instalments, subject to the CPF accrued interest rule on eventual sale.

The HDB Flat Eligibility (HFE) letter replaces the former HDB Loan Eligibility (HLE) letter and the in-principle approval (IPA); you must obtain it before applying for any flat, BTO or resale.

For resale flats, you must also obtain a valuation from a licensed appraiser; your CPF and loan quantum are pegged to the lower of price or valuation.

The Minimum Occupation Period (MOP) for Standard flats is 5 years from keys; selling within MOP incurs claw-back of CPF-funded downpayment and grants.

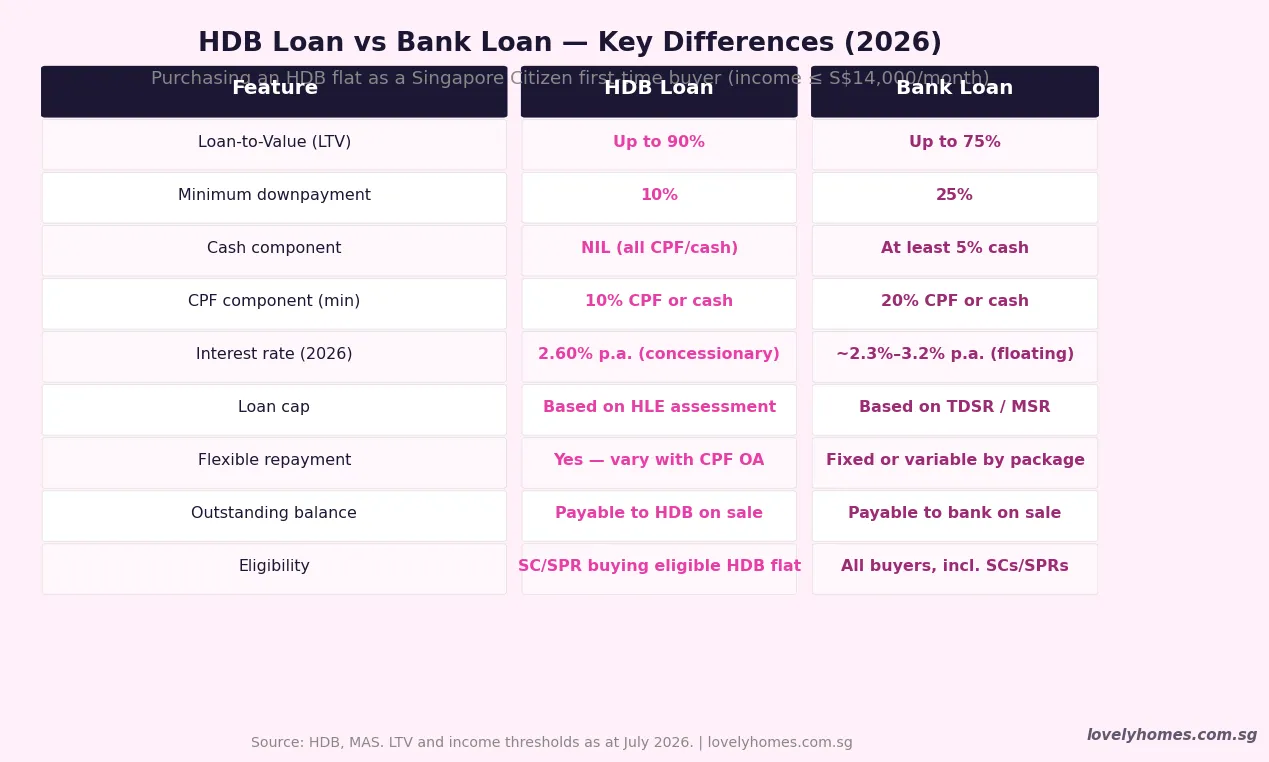

Understanding Loan-to-Value (LTV) for HDB Flats

The Loan-to-Value ratio is the maximum proportion of a property’s purchase price (or valuation, whichever is lower) that a lender is permitted to finance through a loan. For HDB flats in Singapore, the LTV is governed by different rules depending on whether you borrow from HDB directly or from a commercial bank — and whether you have any existing outstanding home loans.

The HDB concessionary loan — available only to Singapore Citizens and, in some cases, PRs buying eligible HDB flats — offers a maximum LTV of 90%. This means you need to fund only 10% of the purchase price from your own resources. The bank loan, regulated by MAS, has a maximum LTV of 75% for a first housing loan. This means a 25% downpayment is required, with a hard cash floor of 5%.

Critically, these LTV limits apply to the lower of purchase price or valuation. If you are buying a resale HDB flat at S$650,000 but the HDB-appointed valuer values it at S$620,000, your loan will be calculated on S$620,000 — and the S$30,000 difference (called Cash Over Valuation, or COV) must be paid entirely in cash.

Figure 1: HDB concessionary loan vs bank loan — key differences in LTV, downpayment, cash requirement, and interest rate. Source: HDB, MAS (July 2026).

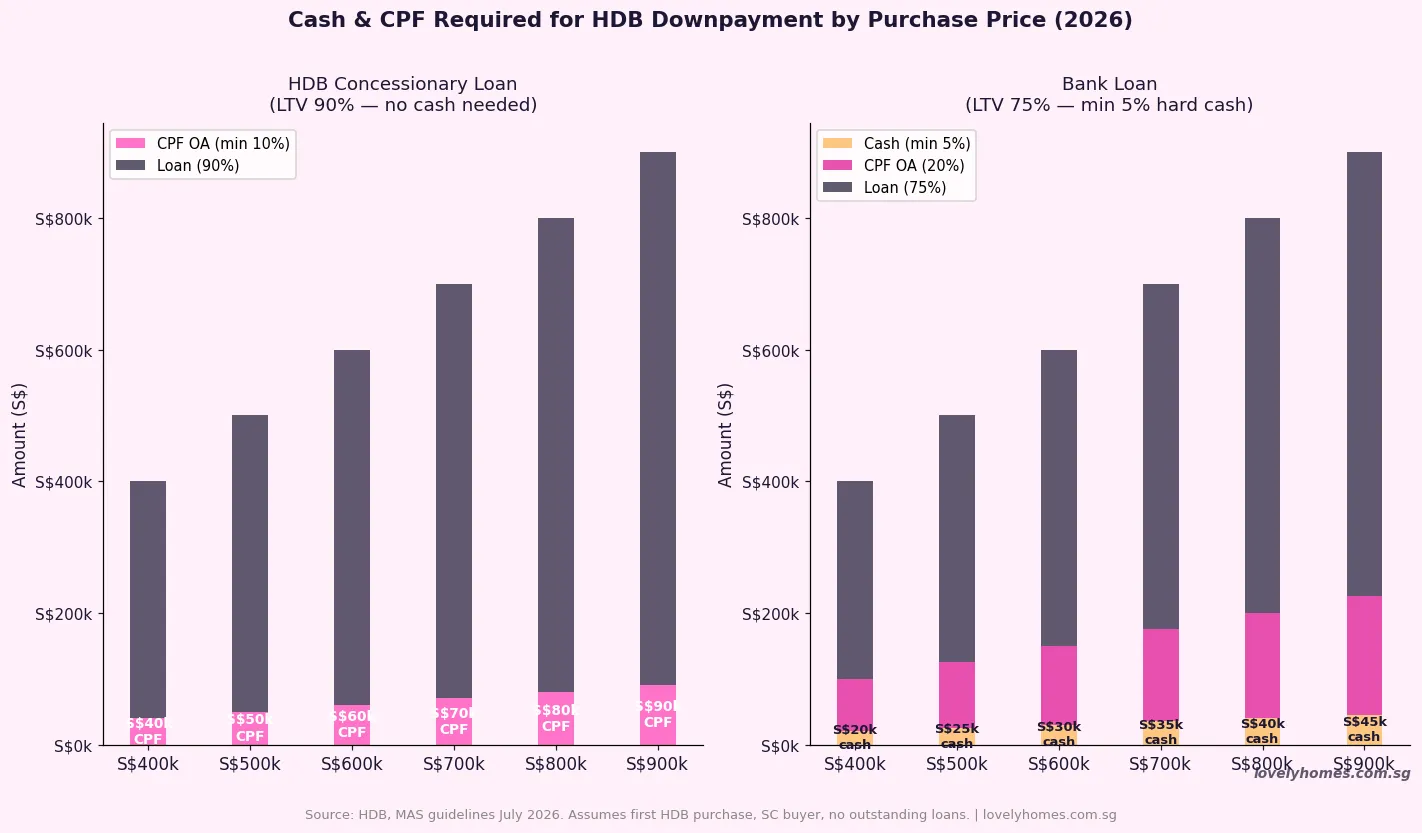

How Much Cash Do You Actually Need?

This is the question most first-time buyers ask first — and the answer depends entirely on your loan choice.

HDB Loan — Minimum Cash: S$0

If you qualify for and take an HDB concessionary loan, the 10% downpayment can come entirely from your CPF Ordinary Account (OA). There is no mandatory cash component. This is the key practical advantage of the HDB loan for buyers who may not have significant liquid savings but have been building CPF through employment.

However, “no mandatory cash” does not mean no cash at all. You will still need to pay BSD (Buyer’s Stamp Duty) — typically S$4,800–S$11,800 for a resale HDB flat priced below S$500,000 — and legal fees of around S$1,500–S$2,500. Both of these can be paid from CPF OA. If there is a Cash Over Valuation component, that must be paid in cash.

Bank Loan — Minimum Cash: 5% of Purchase Price

With a bank mortgage, MAS rules require that at least 5% of the purchase price be paid in cash — not CPF. For a S$600,000 flat, that is S$30,000 in cash. The remaining 20% of the downpayment (S$120,000) can come from CPF OA or cash. The cash floor exists because MAS wants borrowers to have genuine liquidity at stake, not just paper CPF balances.

In practice this means the bank loan path is only viable if you either have sufficient CPF OA savings to cover the 20% CPF component, or you have cash savings sufficient to cover more than the 5% minimum. Many first-time buyers who have not built up their CPF OA (for example, recent graduates or self-employed individuals with irregular CPF contributions) find the HDB loan more accessible for this reason.

CPF and the Downpayment — What You Need to Know

CPF Ordinary Account savings are the primary vehicle for funding an HDB flat downpayment in Singapore. As at July 2026, the CPF OA earns interest at 2.50% per annum (with an additional 1% on the first S$20,000 for members below 55). You can withdraw from your CPF OA to fund the downpayment on any eligible HDB property, subject to two key rules:

1. Valuation Limit: CPF can only be used up to the valuation of the property. If you paid COV above the valuation, that premium cannot be funded by CPF. It must come from cash.

2. Accrued Interest Obligation: All CPF used for property (including the downpayment) must be returned to your CPF account when you sell, together with accrued interest at 2.5% per annum compounded. This is sometimes called the “CPF accrued interest” and it can significantly reduce your net cash proceeds on eventual sale — particularly if you hold for many years. It is not a penalty, but it can feel like one if you have not accounted for it in your financial planning.

Figure 2: Cash and CPF required for the downpayment across common HDB resale price points, comparing HDB loan (LTV 90%, no cash required) and bank loan (LTV 75%, min 5% cash). Source: HDB, MAS; calculations by LovelyHomes.

HDB Loan Eligibility — The HFE Letter

Since 9 May 2023, HDB replaced both the HDB Loan Eligibility (HLE) letter and the separate bank in-principle approval step with a single document: the HDB Flat Eligibility (HFE) letter. The HFE letter confirms three things simultaneously: (a) whether you are eligible to buy an HDB flat, (b) the CPF housing grants you qualify for, and (c) the HDB concessionary loan quantum you are eligible for.

You must have a valid HFE letter before applying for any BTO exercise or before submitting a resale application. The HFE letter is applied for through the HDB website using your Singpass. Assessment considers your household income, existing property holdings, outstanding loans, and citizenship status.

If you plan to take a bank loan instead, you will still need to obtain an HFE letter confirming your flat-buying eligibility, plus separately obtain an In-Principle Approval (IPA) from your chosen bank confirming the loan quantum they will offer. Most banks provide an IPA within two to three working days.

The Minimum Occupation Period and Your CPF

The Minimum Occupation Period (MOP) for Standard HDB flats — including the vast majority of BTO projects launched before 2024 — is five years from the date of physical possession of the keys. If you sell within the MOP, all CPF used for the purchase (downpayment, instalments) plus accrued interest must be refunded to your CPF OA, which can wipe out a significant portion of your sale proceeds. For Plus and Prime flats launched under the new classification framework, the MOP is 10 years.

This MOP interacts with your downpayment decision in a practical way: the more CPF you use for the downpayment, the higher your CPF accrued interest obligation grows with each passing year — meaning the longer you hold, the larger the CPF refund you owe. Some financially sophisticated buyers manage this by paying more cash upfront (even if not required to) in order to reduce their CPF drawdown and therefore their eventual CPF refund obligation.

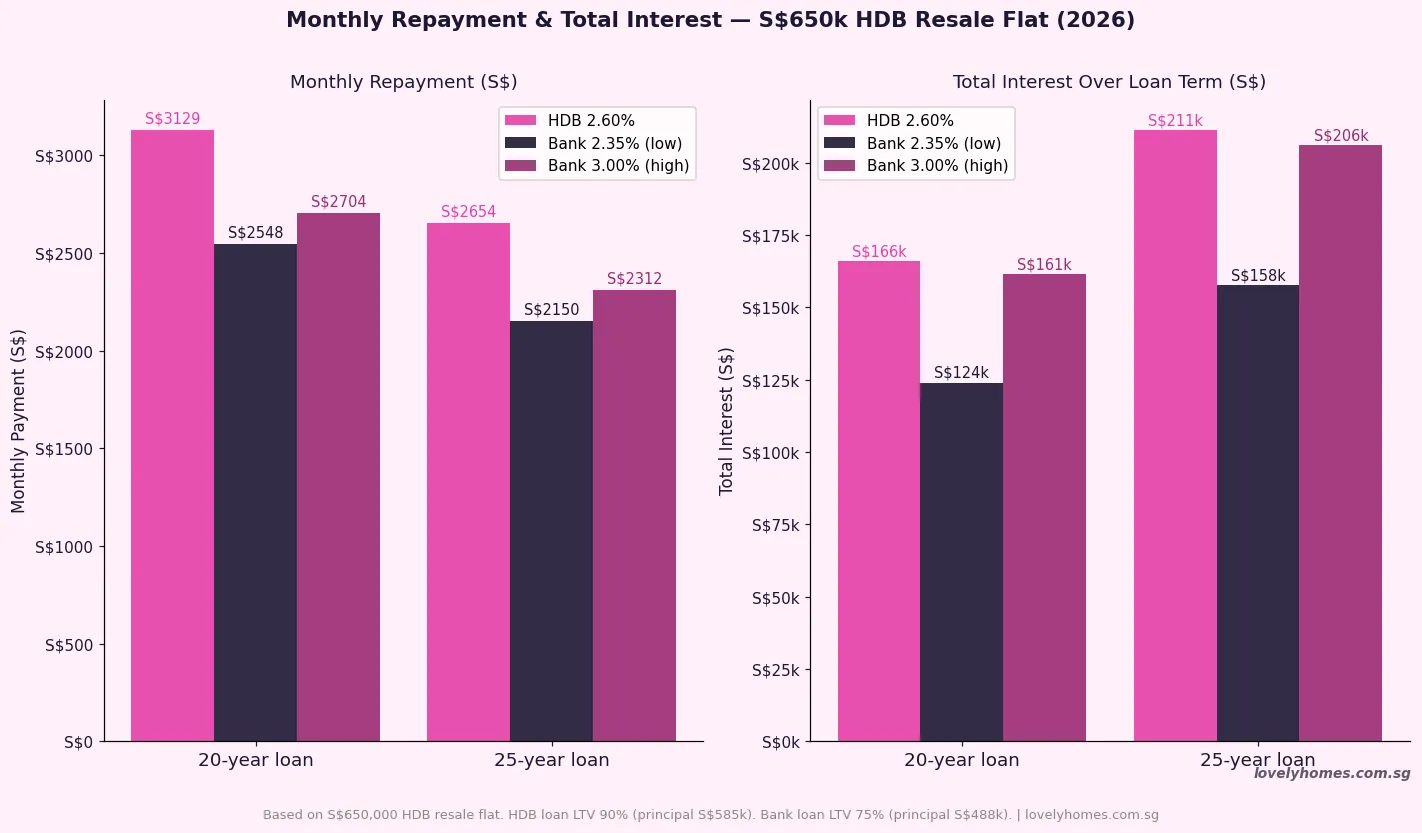

Worked Example — 4-Room Resale Flat in Tampines, S$650,000

The Tan couple (both SCs) are buying a 4-room resale HDB flat in Tampines for S$650,000. HDB valuation: S$635,000. COV: S$15,000 (must be paid in cash). Combined income: S$7,800/month. They have S$130,000 in CPF OA combined and S$35,000 in savings.

Option A — HDB Concessionary Loan (LTV 90%)

Loan quantum: 90% × S$635,000 (valuation) = S$571,500

Downpayment (10%): S$63,500 — payable from CPF OA

COV (cash only): S$15,000

BSD on S$650,000: S$1,800 + S$3,600 + S$16,950 = S$12,750 (payable CPF or cash)

Legal fees: approximately S$2,000 (payable CPF)

Total cash needed on completion: S$15,000 (COV only, if BSD and legal paid from CPF)

Monthly repayment at 2.60% over 25 years: approximately S$2,584

MSR check (30%): S$7,800 × 30% = S$2,340 — repayment S$2,584 exceeds MSR threshold, so loan tenor must be extended or CPF/cash prepayment considered, or loan quantum adjusted

Option B — Bank Loan (LTV 75%)

Loan quantum: 75% × S$635,000 = S$476,250

Downpayment (25%): S$158,750

Cash component (min 5% of S$650,000): S$32,500 cash

CPF component (balance): S$126,250 from CPF OA

COV: S$15,000 cash

BSD: S$12,750 (CPF or cash)

Total cash needed: S$32,500 + S$15,000 = S$47,500 minimum

Monthly repayment at 2.50% over 25 years: approximately S$2,138

MSR check: S$2,138 / S$7,800 = 27.4% — PASS (below 30%)

The Tan couple’s decision: Option A requires only S$15,000 cash but the monthly repayment slightly stresses the MSR limit. A 30-year loan tenor reduces the monthly payment to about S$2,280, which passes. Option B requires S$47,500 cash upfront — more than their savings buffer — but results in a lower monthly repayment. Given their CPF savings, Option B works if they are comfortable with a tighter cash position at completion. Most buyers in this situation choose Option A for its lower cash requirement.

Figure 3: Monthly repayment and total interest payable over 20 and 25-year loan tenors for a S$650,000 HDB resale flat — comparing HDB concessionary loan (2.60%), bank loan low scenario (2.35%), and bank loan high scenario (3.00%). Source: LovelyHomes calculations.

HDB Loan or Bank Loan — What Matters for Your Decision

The choice between HDB and bank is not simply about interest rates. Several factors determine which is better for your specific situation. If you have limited cash savings and strong CPF, the HDB loan’s zero-cash-downpayment requirement is a decisive advantage. If you have substantial cash and want to reduce your total interest cost (and expect interest rates to remain low), the bank loan’s lower starting rate can be appealing — though the fixed-rate advantage over the HDB rate has narrowed significantly since 2022.

One important consideration in 2026 is that fixed-rate bank mortgage packages have come down from their 2023–2024 peaks, with the best promotional fixed-rate packages now available at around 2.20%–2.35% for the first two years. By contrast, the HDB loan rate of 2.60% has been stable and will remain at 0.10% above the CPF OA rate unless the Government changes the CPF OA rate — which it has not done since 2008. If you expect interest rates to fall further, floating-rate bank packages may outperform the HDB rate from 2027 onward. If you value certainty, the HDB rate’s long-term stability is valuable.

A third path — starting with an HDB loan, then refinancing to a bank loan after the MOP — is also possible. HDB permits borrowers to repay the HDB loan in full and switch to a bank loan at any time. There is no penalty for early repayment of the HDB concessionary loan, which gives buyers flexibility.

What Might Change — Downpayment Policy Outlook

The MAS Macroprudential Policy Review and HDB supply-demand management have been the primary levers for adjusting property accessibility rules. In 2022–2023, the Government adjusted LTV and MSR/TDSR parameters as part of the broader property cooling framework. As at July 2026, there is no official signal of any imminent change to the LTV, MSR, or downpayment rules for HDB flats. However, the upcoming release of the Full Q2 2026 HDB resale statistics (expected around 23 July 2026) will provide a clearer picture of whether the sequential price declines seen in Q1 and Q2 2026 prompt any policy review. A further softening of the resale market might create space for a modest easing of downpayment requirements — but this is speculative.

Summary — HDB Downpayment at a Glance, 2026

Item

HDB Loan

Bank Loan

Max LTV

90%

75%

Minimum downpayment

10%

25%

Mandatory cash component

None

Min 5%

CPF OA usable

Yes — up to 10%

Yes — up to 20%

Interest rate (July 2026)

2.60% p.a.

~2.30%–3.20% p.a.

MSR cap (monthly repayment)

30% of gross income

30% of gross income

Eligibility letter required

HFE letter (via HDB)

HFE letter + bank IPA

Who can use

SC (some SPR) buying eligible HDB

All eligible buyers

Frequently Asked Questions

Can I use my CPF Special Account (SA) for the HDB downpayment?

No. Only the CPF Ordinary Account (OA) can be used for property purchases, including the downpayment and monthly mortgage repayments. CPF Special Account (SA) and MediSave Account funds are not permitted for property payments. This is an important distinction — some buyers conflate their total CPF balance with what is available for property, but only the OA balance is accessible for this purpose.

What is Cash Over Valuation (COV) and how does it affect my downpayment?

COV is the amount you pay above the HDB-appointed valuation for a resale flat. For example, if you agree to pay S$680,000 for a flat valued at S$650,000, the COV is S$30,000. COV must always be paid entirely in cash — it cannot be funded by CPF or a bank loan. This is in addition to your regular downpayment and is one reason why buying a resale flat at a significant premium to valuation can demand more cash than buyers anticipate. In the current (mid-2026) market, COV has moderated from the peaks seen in 2022–2023, but still occurs frequently for popular mature-estate resale flats.

Does the MSR limit apply if my spouse is not employed?

Yes. The Mortgage Servicing Ratio (MSR) limit of 30% applies to the combined gross monthly income of all applicants on the HDB application. If your spouse is not employed, their income is counted as S$0, which means only your individual income is used to calculate the MSR threshold. This can significantly reduce the loan quantum you are eligible for, and may require you to extend the loan tenor to bring the monthly repayment within the 30% limit. Borrowers relying on a single income should calculate their maximum eligible loan quantum carefully before making an offer.

What happens if I switch from an HDB loan to a bank loan mid-mortgage?

You can refinance from an HDB concessionary loan to a bank loan at any time — HDB charges no early repayment penalty. However, once you switch to a bank loan, you cannot switch back to an HDB concessionary loan. This is a one-way door, so the decision deserves careful consideration. When refinancing, you will need to ensure the bank’s IPA covers the outstanding loan balance, and you should account for legal/administrative costs of refinancing (typically S$2,000–S$3,000 in conveyancing and valuation fees). Banks sometimes offer cashback promotions on refinancing that offset these costs.

Can CPF grants be used as part of the downpayment?

Yes. CPF housing grants (such as the Enhanced CPF Housing Grant, Family Grant, and Proximity Housing Grant for eligible resale flat buyers) are credited directly to your CPF OA and can be applied toward the downpayment and purchase price. This effectively reduces the CPF savings you need to have pre-existing in your account before the purchase. However, grants are credited only after the resale application is approved by HDB — they are not available to fund the initial Option exercise fee or the initial downpayment tranche. For BTO buyers, grants are applied at key collection. The maximum combined grant for an eligible first-timer SC couple buying a resale flat can reach S$190,000.

What if my CPF OA balance is not enough to cover the downpayment?

If your CPF OA balance falls short of the required downpayment, the shortfall must be made up in cash. For HDB loan buyers, the 10% downpayment can be a mix of CPF OA and cash — there is no restriction on using cash for this portion. For bank loan buyers, you must still ensure the 5% mandatory cash component is in cash, but any additional downpayment shortfall can also be funded by cash. If your combined CPF OA and cash are insufficient to cover the full downpayment, you may need to negotiate a lower purchase price, seek a higher grant, or delay your purchase until your CPF OA balance has grown sufficiently.

This article is produced by LovelyHomes for general information purposes only and does not constitute financial, legal, or mortgage advice. HDB loan eligibility, CPF rules, LTV limits, and interest rates are subject to change by the Housing & Development Board, Monetary Authority of Singapore, and Central Provident Fund Board. Readers should verify all current rules and figures directly at hdb.gov.sg, cpf.gov.sg, and mas.gov.sg, and should obtain independent financial and mortgage advice before making any purchase decision.

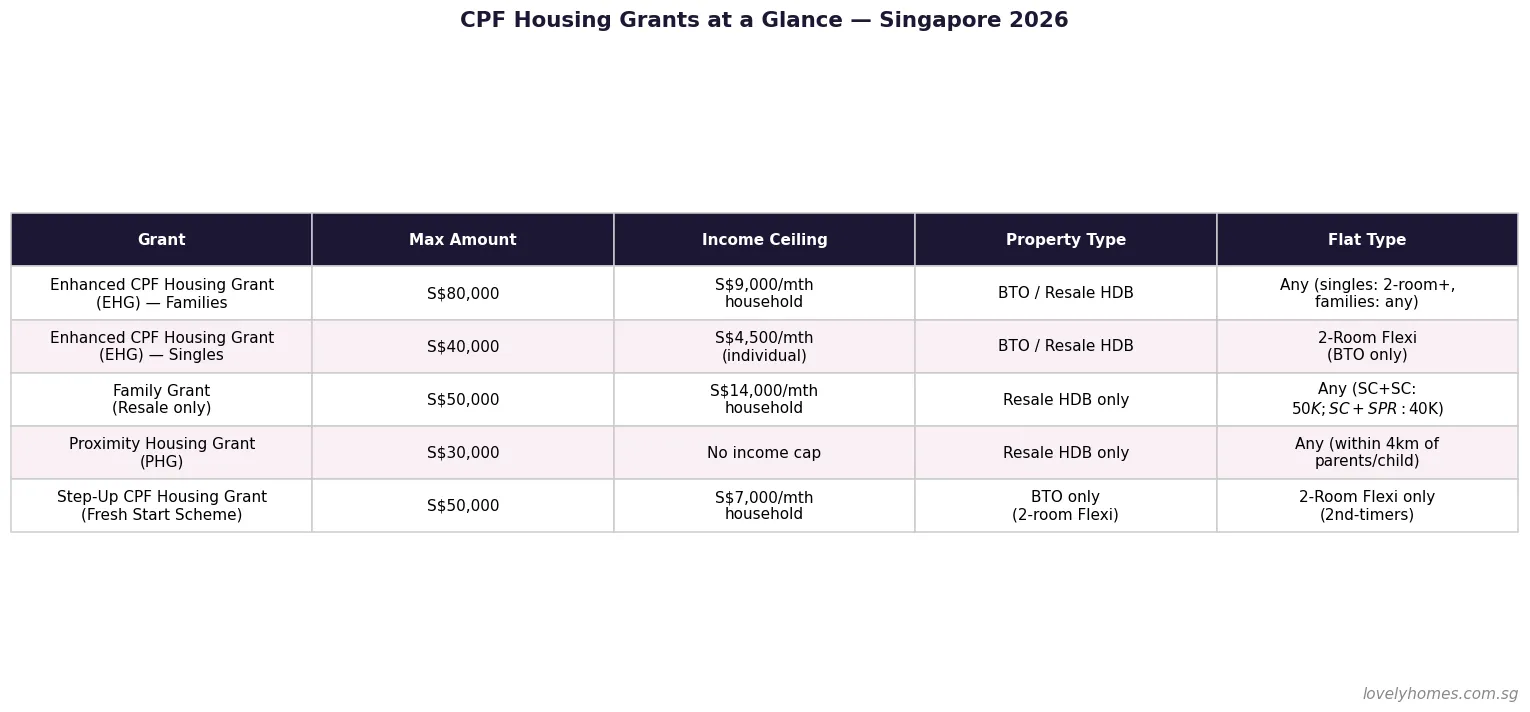

First-timer families can receive up to S$80,000 in Enhanced CPF Housing Grant (EHG) for BTO or resale flats (household income ≤ S$9,000/month).

Singles buying a 2-Room Flexi BTO qualify for up to S$40,000 EHG (individual income ≤ S$4,500/month).

Resale buyers can stack the Family Grant (up to S$50,000) with the EHG and the Proximity Housing Grant (PHG, up to S$30,000) — potentially S$160,000 in total grants.

The PHG has no income ceiling and rewards buyers who live near or with parents or children.

All CPF grants go into your CPF Ordinary Account (OA) and are used against the purchase price — but they accrue interest that must be refunded upon sale.

Grants do not eliminate your cash component of the downpayment — at least 5% cash is still required for bank loans.

Applications are via the HDB flat portal and must be completed before exercising the Option to Purchase (OTP).

What Are CPF Housing Grants and Who Administers Them?

CPF Housing Grants are direct subsidies paid by the Singapore Government into the buyer’s CPF Ordinary Account (OA) to help Singaporeans afford their first — and in some cases, second — HDB flat. They are administered jointly by the Housing & Development Board (HDB) and the Central Provident Fund Board (CPF Board), with eligibility rules updated periodically to reflect prevailing market conditions and government housing policy.

Unlike an ABSD remission or a bank subsidy, a CPF Housing Grant is a genuine cash transfer from the public purse into your CPF OA. It immediately reduces the amount you need to borrow or fund from savings, which lowers your monthly mortgage instalment. However, grants are not free in the accounting sense: when you eventually sell the flat, the grant amount — plus accrued interest at the CPF OA rate of 2.5% per annum — must be refunded back into your CPF OA. The net effect is deferred rather than eliminated cost.

As of 26 April 2026, the key grant types in force are the Enhanced CPF Housing Grant (EHG), the Family Grant, the Proximity Housing Grant (PHG), and the Step-Up CPF Housing Grant for eligible second-timers under the Fresh Start Housing Scheme.

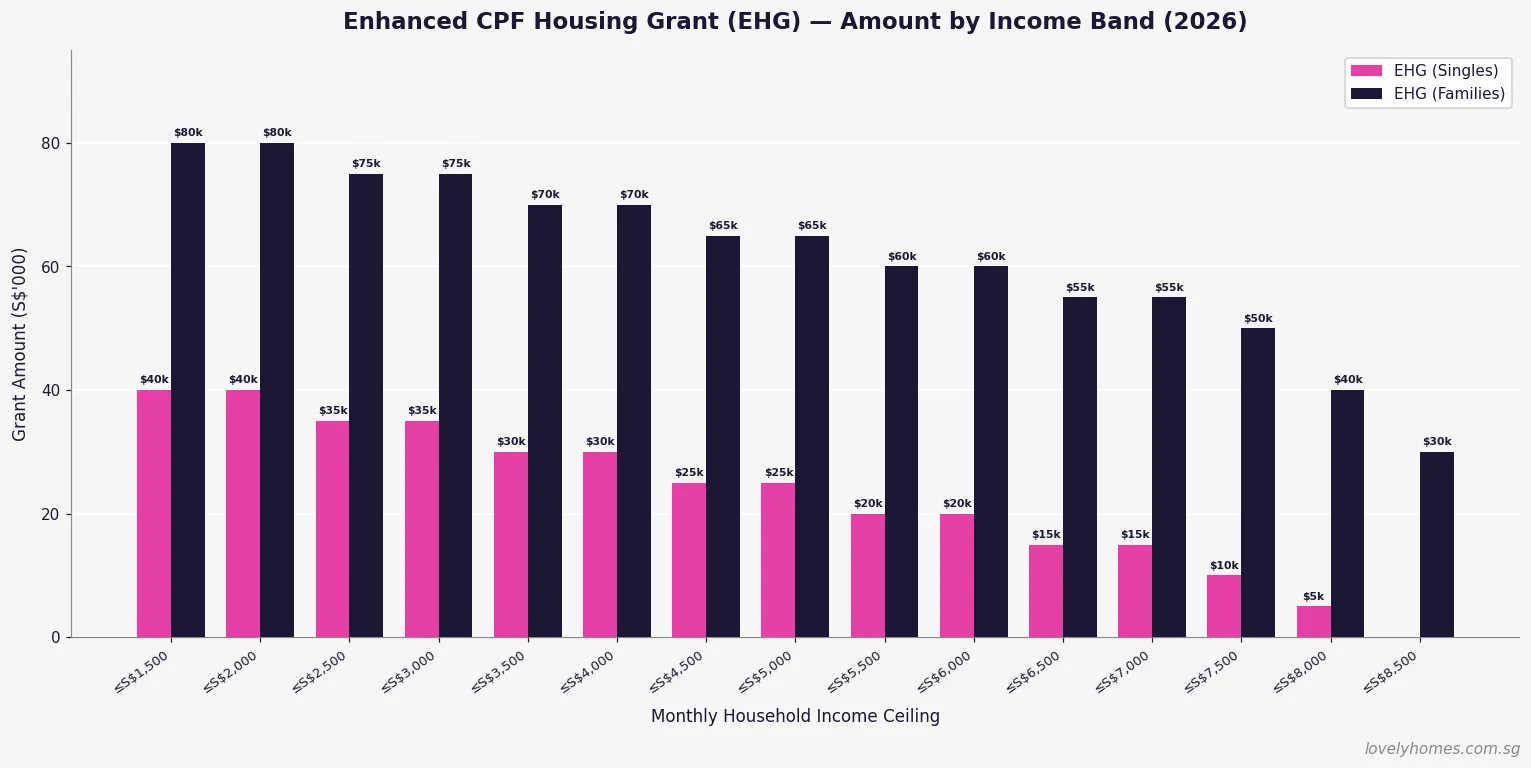

Enhanced CPF Housing Grant (EHG) — Rates and Eligibility

The Enhanced CPF Housing Grant, introduced in September 2019 to replace the Additional CPF Housing Grant (AHG) and Special CPF Housing Grant (SHG), is the flagship subsidy for first-timer buyers. It is progressive — the lower the household income, the higher the grant — and applies to both new BTO flats and resale HDB flats, making it more flexible than its predecessors.

Figure 1: EHG amounts (S$’000) for singles vs families, by monthly household income band. Source: HDB (2026).

EHG for Families

For married or engaged couples — including those applying under the Fiancé/Fiancée Scheme — the EHG ranges from S$5,000 (household income ≤ S$8,000/month) to S$80,000 (household income ≤ S$1,500/month). The income assessed is the average gross monthly income of both applicants over the 12 months preceding the application. If the combined household income exceeds S$9,000/month, no EHG is payable.

EHG for Singles

First-timer singles aged 35 and above buying a 2-Room Flexi BTO flat in a non-mature estate qualify for EHG on a scaled basis, up to S$40,000 (individual income ≤ S$1,500/month). A single with income ≤ S$4,500/month qualifies for a minimum S$5,000 grant. Singles buying resale flats under the Single Singapore Citizen (SSC) scheme are also eligible, provided they purchase a 5-room flat or smaller.

Monthly Gross Income (Household)

EHG — Families

EHG — Singles

≤ S$1,500

S$80,000

S$40,000

≤ S$2,500

S$75,000

S$35,000

≤ S$3,500

S$70,000

S$30,000

≤ S$4,500

S$65,000

S$25,000

≤ S$5,500

S$60,000

S$20,000

≤ S$6,500

S$55,000

S$15,000

≤ S$7,500

S$50,000

S$10,000

≤ S$9,000

S$30,000–S$40,000

Not eligible

Family Grant — For Resale HDB Buyers

The Family Grant is available exclusively to buyers of resale HDB flats and is stackable on top of the EHG. It acknowledges that resale flat prices in many estates carry a premium over BTO prices, and provides an additional buffer for buyers who prefer a specific location or immediate occupancy over the BTO ballot process.

The Family Grant is administered by HDB and paid into the CPF OA of eligible applicants. Key parameters as of 2026:

SC + SC couple or family: S$50,000

SC + SPR couple or family: S$40,000

Singles (SSC scheme, resale 5-room or smaller): S$25,000

Income ceiling: S$14,000/month combined household income

Flat type restriction: any resale flat type; no restriction by town or estate

The S$14,000/month income ceiling makes the Family Grant accessible to many dual-income professional couples who earn too much for the EHG but still value the additional subsidy when purchasing resale.

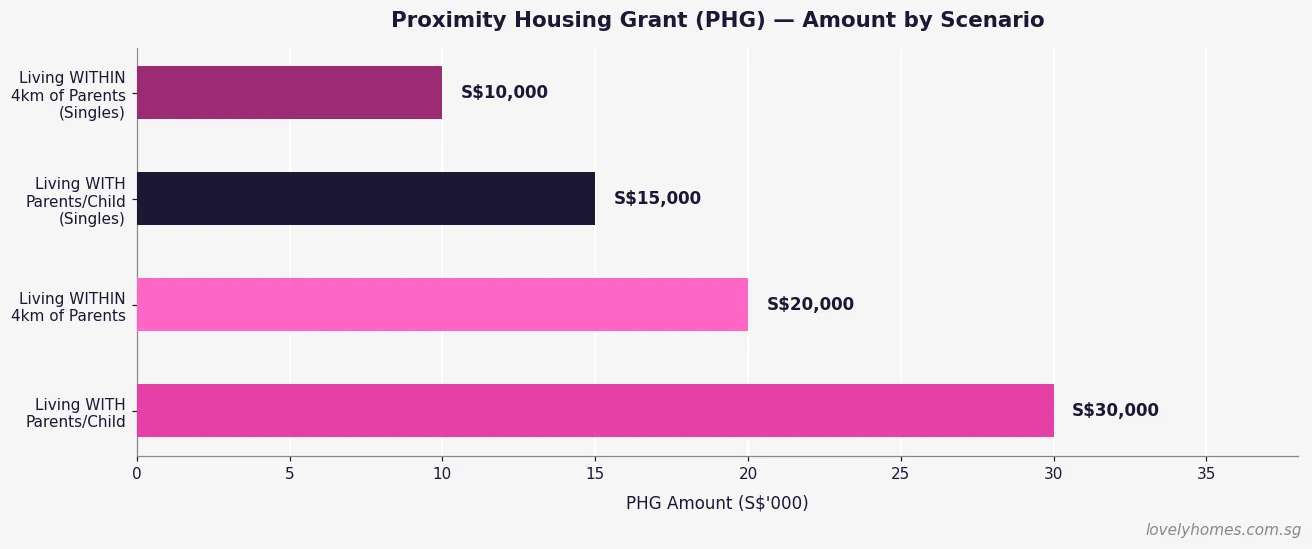

Proximity Housing Grant (PHG) — Rewarding Family Ties

Introduced in August 2015, the Proximity Housing Grant is one of the most distinctive features of Singapore’s housing policy. It uses a direct cash subsidy to incentivise multi-generational proximity — encouraging adult children to live near, or with, their elderly parents. It applies only to resale HDB flats and has no income ceiling, meaning higher-earning buyers can benefit too.

Figure 3: PHG amounts by proximity scenario, for families and singles. Source: HDB (2026).

The PHG has four tiers based on whether you are buying as a family or single, and whether you are moving with parents or children (same household) or within 4 km of them:

Buyer Type

Living With Parents/Child

Living Within 4 km

Families (married/engaged couples)

S$30,000

S$20,000

Singles (SSC scheme)

S$15,000

S$10,000

The “living with” criterion requires the parent or child to be registered on the same flat as an occupier. The “within 4 km” criterion uses the straight-line distance between postal codes, verified at the point of application. The PHG is a one-time benefit — once received, it cannot be claimed again on a subsequent flat purchase.

Step-Up CPF Housing Grant — Fresh Start Scheme

The Step-Up CPF Housing Grant is a targeted measure for a specific group: second-timer applicants who previously owned a subsidised flat and now qualify for a second chance at affordable owner-occupied housing under HDB’s Fresh Start Housing Scheme, which was introduced in October 2016 and expanded over subsequent years.

Eligibility is tightly defined: second-timer families with at least one child aged under 16; monthly household income ≤ S$7,000; must apply for a 2-Room Flexi BTO flat; must not currently own a flat or private residential property; and must fulfil a 5-year Fresh Start Housing Scheme Minimum Occupation Period on the new flat. The grant amount is up to S$50,000. It is not stackable with the EHG.

CPF Housing Grants at a Glance — Summary Table

Figure 2: Summary of all CPF Housing Grant types — amounts, income ceilings, and eligible property types. Source: HDB / CPF Board (2026).

Worked Example — Maximum Grant Stack for a Resale Buyer

Scenario: SC + SC First-Timer Couple, Resale Flat Near Parents

Buyer profile: Mr and Mrs Tan — married, both Singapore Citizens, first-timer applicants. Combined monthly gross income: S$6,800. Mrs Tan’s parents reside in the same block as the resale flat they are purchasing in Ang Mo Kio.

EHG (family, income band S$6,500–S$7,500): S$50,000

Family Grant (SC + SC, resale): S$50,000

PHG (same block as parents = “living with”): S$30,000

Total grants: S$130,000

Purchase price: S$600,000 (4-Room resale, Ang Mo Kio) Effective net cost after grants: S$470,000 (before stamp duties and legal fees). BSD on S$600,000: approximately S$12,600. ABSD: Nil (first residential property, Singapore Citizen buyers). Legal / conveyancing fees: approximately S$2,500–S$4,000.

Taking an HDB concessionary loan at 90% LTV: loan = S$540,000 less S$130,000 grants = S$410,000 loan needed, reducing the monthly instalment significantly versus purchasing without grants.

The CPF Accrued Interest Rule — The Hidden Cost of Grants

Every dollar drawn from your CPF OA — including grant monies — accrues interest at the CPF OA rate (currently 2.5% per annum). When you sell the flat, the CPF Board requires you to refund the principal amount used (including grants) plus the hypothetical interest that amount would have earned in the OA. This refund is returned to your CPF OA — not the government — and is available for future use in retirement or a subsequent property purchase.

Practical implication: a S$80,000 EHG held for 10 years accrues approximately S$22,000–S$25,000 in interest (compounded at 2.5% p.a.), bringing the total CPF refund for the grant alone to roughly S$102,000–S$105,000. Plan for this when modelling net sale proceeds on exit. If the sale price is insufficient to cover the full CPF refund, you keep the shortfall — you are not personally liable to top up the difference.

Why CPF Housing Grants Matter for Singapore’s Property Market

CPF Housing Grants fulfil a dual function in Singapore’s property ecosystem. At the individual level, they represent one of the most powerful demand-side subsidies in the world — transferring significant public funds directly to low- and middle-income buyers to help them achieve owner-occupation without over-relying on private financing. At the market level, they compress effective pricing for first-timers in the HDB resale segment, sustaining affordability across economic cycles.

The 2019 introduction of the EHG deliberately raised the income ceiling to S$9,000/month (from S$6,000/month under the legacy AHG/SHG regime), reflecting the Government’s recognition that median household incomes had risen and the historical ceilings were excluding a growing segment of first-timers who genuinely needed assistance.

Compared with equivalent policies in Hong Kong — where the Home Ownership Scheme provides a flat discount on market price rather than a direct grant — or Australia, where the First Home Owner Grant is a modest flat sum, Singapore’s progressive, stackable grant framework is both more generous and more targeted to income need.

What Might Come Next — Grant Policy Outlook for 2026–2028

The CPF Housing Grant framework is reviewed periodically in tandem with BTO flat pricing and HDB resale indices. Three plausible near-term developments:

EHG income ceiling revision: With household income growth continuing, HDB may raise the S$9,000/month family ceiling to extend coverage to the lower-professional bracket — especially as Prime Location Public Housing (PLH) flat prices edge towards S$700,000–S$800,000 in central estates.

PHG extension to BTO buyers: Currently restricted to resale buyers, extending the PHG to BTO buyers in family-friendly towns like Tengah and Bidadari has been discussed in policy circles, though not confirmed as of this date.

Grant indexing to flat type or BTO pricing band: A flat S$80,000 EHG ceiling becomes proportionally less meaningful as PLH BTO prices climb. Grant amounts indexed to flat type could better reflect affordability gaps across different segments.

These are speculative. Always verify current grant levels at the HDB Grant Eligibility page before exercising any OTP.

Frequently Asked Questions

Can I use CPF Housing Grants towards the downpayment?

Grants are credited into your CPF OA and can be applied in the same way as your own CPF savings — towards the downpayment, the purchase price, and stamp duties (BSD). However, if you are taking a bank loan, the minimum 5% cash downpayment must be paid in cash; CPF (including grants) cannot cover this component. If you are taking an HDB concessionary loan, there is no mandatory cash component, so grants can fully offset the downpayment requirement alongside your other CPF OA balance.

Can both the EHG and Family Grant be claimed for the same resale flat purchase?

Yes. For resale flat purchases, a first-timer SC couple can claim both the EHG and the Family Grant simultaneously, provided they meet the eligibility criteria for each. If the couple also qualifies for the PHG — for example, buying near parents — that can be added on top. The theoretical maximum for an SC + SC couple buying resale is S$80,000 (EHG) + S$50,000 (Family) + S$30,000 (PHG living-with) = S$160,000, though achieving the maximum EHG requires a household income ≤ S$1,500/month, which is uncommon for buyers at today’s resale prices.

Does receiving a CPF Housing Grant affect my HDB Loan Eligibility (HLE)?

Grants and HLE are assessed separately. Your HDB Loan Eligibility letter determines the maximum HDB concessionary loan you can borrow, based on income, credit history, outstanding debts, and MSR/TDSR compliance. Grants reduce the net amount you need to borrow, but the HLE loan quantum is not directly inflated by the grant. You apply for both the HLE and the grant through the HDB flat portal before exercising the OTP.

I am a Singapore Permanent Resident married to a Singapore Citizen. What grants are we eligible for?

An SC + SPR couple counts as a mixed-citizenship household for CPF grant purposes. You are eligible for the EHG at the family rate (since one applicant is SC), the Family Grant at the reduced SC + SPR amount of S$40,000, and the PHG if applicable. You are not eligible for the full SC + SC Family Grant of S$50,000. The SPR spouse’s income is included in the combined household income calculation for EHG and Family Grant means-testing.

What happens to my grant if I divorce after purchasing the flat?

Divorce does not trigger a grant clawback. The grant remains in the CPF OA of the respective owner(s) and normal CPF refund-on-sale rules apply. However, if the divorce results in one party retaining the flat and the other being bought out, the outgoing party’s CPF contributions — including grant amounts attributed to them — must be refunded at that point, with accrued interest. This is handled through the matrimonial asset division process, usually with the assistance of a family law solicitor.

Can I appeal for a higher grant if my income is irregular or I am self-employed?

Yes. HDB uses average gross monthly income over the 12 months preceding the application for means-testing. If your income is irregular — for example, you are a freelancer, commission-based worker, or recently returned to employment — HDB has a declared income process for the self-employed and an appeal mechanism for unusual circumstances. Supporting documents such as Notice of Assessment from IRAS, payslips, or CPF contribution history are typically required. Speak to an HDB branch officer early in the process if your income situation is non-standard.

Do the grants expire if I do not use them within a certain period?

CPF Housing Grants are credited into your CPF OA at the point of flat purchase — they are not a time-limited voucher. However, your eligibility to receive grants can change: if your income rises above the ceiling before application, or if you purchase a private property before your HDB flat, you may lose eligibility. The grant application must be submitted before you exercise the Option to Purchase, and the grant is disbursed only upon completion of the purchase.

Disclaimer: This article is intended for general information only and does not constitute financial, legal, or tax advice. CPF Housing Grant amounts, income ceilings, and eligibility conditions are subject to change. Always verify current grant details on the official HDB Grant Eligibility page and the CPF Board Home Ownership page. Consult a licensed property agent (CEA-registered) or HDB branch officer before making any purchase decision.

For most Singaporeans, the home loan is the largest financial commitment of their lives — and in a market where private condo prices now range from S$1.2 million to S$4 million and beyond, getting the loan structure right can save (or cost) hundreds of thousands of dollars over a 25–30 year mortgage. This guide covers everything you need to know about home loans in Singapore in 2026: how much you can borrow, what the rates look like, how to compare packages, and how to build the strongest possible loan application.

Quick Answer — Singapore Home Loan Basics 2026

Maximum LTV: 75% for first private property (5% cash + 20% CPF/cash); 45% if holding an existing property

TDSR cap: Total monthly debt repayments cannot exceed 55% of gross monthly income

Typical fixed rates (2026): 2.5%–3.5% p.a. for 2–3 year lock-in packages

SORA benchmark: 3-month SORA fluctuates; total SORA-linked rate approximately 3.3%–3.8% in April 2026

Maximum loan tenure: 30 years (or limited so borrower does not exceed age 65 at loan end)

IPA (In-Principle Approval): Obtain before visiting any showflat — it defines your budget precisely

Singapore Home Loan Key Parameters 2026

Private residential properties — framework in force as at 24 April 2026

55% of gross monthly income — all debt obligations

Mortgage Servicing Ratio (MSR)

30% of gross income — applies to HDB and EC loans only

Stress Test Rate

Typically 4% p.a. or prevailing rate + 2%, whichever is higher

Typical Fixed Rate (2026)

~2.5%–3.5% p.a. (3-year package) — compare across banks

Typical SORA-linked (2026)

3M SORA + spread (~0.7%–0.9%); total ~3.3%–3.8% p.a.

Max Loan Tenure

30 years (private); 25 years if borrower age at end of tenure >65

Source: MAS Regulations + MND / bank rate surveys — 24 April 2026

lovelyhomes.com.sg

How Much Can You Borrow? LTV, TDSR, and Stress Tests Explained

Your maximum home loan in Singapore is determined by three overlapping constraints. The most restrictive of the three sets your actual limit.

1. Loan-to-Value (LTV): For a private property loan from a bank, the LTV ceiling is 75% of the purchase price or market value (whichever is lower) for buyers with no outstanding property loans. This means a maximum loan of S$1.387 million on a S$1.85 million purchase. If you hold an existing property loan (e.g., you are buying a second property before selling the first), the LTV drops sharply to 45%, requiring a 55% down payment. These LTV rules are set by MAS and apply uniformly across all banks.

2. Total Debt Servicing Ratio (TDSR): Your total monthly repayments across all debts — home loan, car loan, personal loan, credit card minimum payment, student loan — must not exceed 55% of your gross monthly income. Banks assess TDSR at a stress-tested rate (the higher of 4% p.a. or the prevailing rate plus 2%) to ensure your repayment capacity holds under adverse rate conditions. A joint applicant’s income can be combined; however, guarantors’ income typically cannot be included for TDSR purposes.

3. Loan Tenure Cap: Banks impose a maximum tenure of 30 years, subject to the borrower not exceeding age 65 at loan maturity. A 45-year-old borrower is therefore limited to a 20-year tenure; a 35-year-old can take the full 30 years. Shorter tenure = higher monthly instalment but lower total interest paid. Longer tenure = lower monthly instalment but significantly higher total interest cost over the life of the loan.

Down Payment: What You Need in Cash vs CPF

At 75% LTV, the required down payment is 25% of the purchase price. Of this 25%, at least 5% must be in cash (hard cash — not CPF, not bank loan). The remaining 20% can be funded from any combination of cash and CPF Ordinary Account (OA) savings. This means a buyer purchasing a S$2 million condo must have at least S$100,000 in cash available on the day of OTP exercise, plus access to S$400,000 in additional cash and/or CPF OA for the remaining down payment component.

For upgraders who have just sold an HDB, the CPF OA refund (principal + accrued interest) can provide a significant top-up — in many cases, several hundred thousand dollars — making the 20% non-cash component relatively manageable. The critical cash requirement is the minimum 5%.

Fixed Rate vs SORA-Linked: Which Package is Right for You?

The Singapore Overnight Rate Average (SORA) replaced SIBOR as the benchmark rate for floating-rate home loans from 2021 onwards. As of April 2026, the 3-month compounded SORA sits in the range of approximately 2.5%–3.0%, with bank spreads of 0.7%–0.9%, producing effective all-in SORA-linked rates of approximately 3.3%–3.8% per annum. Fixed-rate packages for 2–3 year lock-in periods are broadly competitive at 2.5%–3.5% p.a. depending on the bank and loan quantum.

Fixed Rate vs SORA-Floating — When Each Makes Sense

Package Type

Rate Profile

Best For

Key Risk

Fixed Rate (2–3 yr lock-in)

Rate fixed for 2–3 yrs, then reverts to board/SORA

Buyers who want payment certainty; rate rising environment

Early repayment penalty during lock-in

SORA Floating

Rate moves monthly with 3-month SORA + spread

Buyers expecting rates to fall; short hold period

Payment volatility; budgeting harder

Fixed + SORA Hybrid

First 2 yrs fixed, then SORA

Hedge approach; balance of certainty and flexibility

Transition risk if SORA spikes after lock-in expires

HDB Concessionary Loan (HDB only)

2.6% p.a. flat (CPF OA rate + 0.1%); 80% LTV

HDB flat buyers; first-timers with limited cash

Only for HDB flats; not available for private property

Key Takeaway

As at April 2026, fixed rates are broadly competitive with SORA-linked packages. Buyers planning a >5-year hold with stable income generally benefit from a 2-year fixed package for predictability, then re-finance at the end of the lock-in.

Source: MAS / bank surveys — April 2026

lovelyhomes.com.sg

Worked Example — S$1.85m New Launch Purchase

The following illustrates the full upfront financial requirement for a Singapore Citizen couple buying their first private property (a new launch condo at S$1.85 million) after selling their HDB flat.

Worked Example — S$1.85m New Launch Condo Purchase (SC, First Property)

Item

Amount

Basis

Purchase Price

S$1,850,000

New launch indicative price

Down Payment (25%)

S$462,500

5% cash (S$92,500) + 20% CPF/cash (S$370,000)

Buyer’s Stamp Duty (BSD)

~S$62,100

Progressive BSD table; paid in cash within 14 days of OTP

ABSD (SC 1st property)

S$0

0% for Singapore Citizen first purchase

Loan Amount (75% LTV)

S$1,387,500

Subject to TDSR and stress test

Monthly Instalment (3% fixed, 30 yr)

~S$5,849/month

Estimated; varies by bank and package

TDSR threshold (55% rule)

Monthly income ≥ S$10,635 (combined, all debts)

To support the above instalment with zero other debt

Legal / Conveyancing (est.)

~S$3,500–S$5,000

One-time cost; varies by law firm

Total Upfront Cash Required

~S$100,000–S$110,000

5% cash down + BSD + legal (CPF funds balance)

Key Takeaway

A Singapore Citizen couple with a combined gross monthly income of S$12,000 can comfortably qualify for a S$1.387 million home loan on a S$1.85 million first property, using CPF OA for the 20% non-cash component of the down payment.

Source: IRAS + MAS + Bank estimates — 24 April 2026

lovelyhomes.com.sg

How to Secure the Best Home Loan: A Step-by-Step Approach

1. Pull your credit report: Before approaching any bank, request your credit report from Credit Bureau Singapore (CBS). A credit score above 1,844 (AA or BB grade) gives you the strongest negotiating position. Clear any outstanding small debts that may drag down your score.

2. Compile your income documents: The standard package is your most recent 3 months’ payslips, latest CPF contribution history statement (12 months), Notice of Assessment (NOA) for the past 2 years, and your NRIC. Self-employed buyers need their NOA for 2 years plus certified management accounts or bank statements. Commission-based earners typically have their variable income haircut by 30% for TDSR calculation.

3. Obtain IPAs from at least 3 banks: Compare the IPA quantum, the indicative rate offered, and the lock-in terms. Banks compete actively for quality home loan customers; do not accept the first offer. Use a mortgage broker if you prefer to have the comparison done for you, but be aware they receive referral fees and may not compare all available options.

4. Read the fine print on lock-in periods and clawback: Most competitive fixed-rate packages have a 2–3 year lock-in during which early redemption triggers a penalty (typically 1.5% of the outstanding loan). Check also for legal fee subsidies, valuation fee waivers, and free conversion clauses — these can save S$3,000–S$8,000 in the first year and are worth negotiating.

5. Consider a mortgage offset account: Some banks offer a 100% offset account facility that links your current account balance to your mortgage principal. Funds parked in this account reduce your effective interest cost dollar for dollar. This is particularly valuable for buyers who accumulate savings quickly or receive occasional large bonuses.

Using CPF for Your Home Loan

Your CPF Ordinary Account can be used to fund (a) the initial down payment (the non-cash component of the 25%), (b) the BSD, (c) monthly mortgage instalments up to the Valuation Limit, and (d) legal fees. The key rule is the CPF Usage Limit for private property:

If the property’s remaining lease covers the youngest buyer to age 95, full CPF usage is permitted up to the property’s Valuation Limit.

If the remaining lease does NOT cover the youngest buyer to age 95 but covers at least 60 years, CPF usage is capped pro-rata.

If the remaining lease is less than 30 years, CPF cannot be used at all.

For new launch condos (99-year leasehold, purchased in 2026), the lease will comfortably cover the youngest buyer to age 95 in the vast majority of cases, so full CPF usage is available. Remember: when you sell the property, all CPF monies drawn must be returned to your OA with accrued interest — this is not optional and is enforced automatically by the CPF Board upon completion of sale.

Frequently Asked Questions

Can I take a loan from HDB and a bank simultaneously?

No. The HDB concessionary loan (2.6% p.a., 80% LTV) is available only for HDB flats. Private property purchases must use a bank loan. You cannot hold an HDB loan and a bank mortgage on a private property simultaneously; the two loan types are for distinct property classes.

How does SORA work for home loans?

The Singapore Overnight Rate Average (SORA) is published daily by MAS and represents the weighted average overnight unsecured borrowing rate among banks. Most banks use the 3-month compounded SORA (3M Compounded SORA), which is smoothed and less volatile than the daily rate. Your mortgage rate = 3M Compounded SORA + bank spread. Both components change over time; your monthly instalment adjusts accordingly, typically quarterly. Check the MAS SORA statistics page for the latest published rate.

What is the stress test rate and why does it matter?

Banks assess your TDSR at the higher of (a) 4% p.a. or (b) the prevailing rate plus a 2% buffer. This “stress test rate” is typically higher than the actual rate you will pay, so the loan amount you are approved for is lower than what you could technically service at today’s market rate. This is a deliberate prudential measure to ensure borrowers can still service the loan if rates rise significantly.

Can I refinance during the lock-in period?

You can, but you will typically incur an early redemption penalty of 0.75%–1.5% of the outstanding loan balance. After the lock-in period expires, you are free to re-price (switch to a new package with the same bank) or refinance (move to a different bank) without penalty. Most active mortgage managers review their loan package at the end of every lock-in period.

Does a larger down payment lead to a better rate?

Not directly in Singapore’s home loan market. Unlike some markets where LTV directly influences the mortgage rate, Singapore banks generally offer the same rate bands across LTV ranges (within the MAS limit). However, a larger down payment reduces your loan quantum, which may bring you within a bank’s “premium package” tier (typically loans above S$1.5 million attract slightly different product options). Focus more on the total-cost comparison between packages than on trying to optimise the down payment size for rate purposes.

Disclaimer: All information in this article is for general educational purposes only and does not constitute financial, legal, or mortgage advice. Loan rates, LTV limits, CPF rules, and MAS regulations are subject to change. Always obtain a personalised In-Principle Approval from a licensed bank and consult a licensed financial adviser before committing to any home loan. Interest rates quoted are indicative as at April 2026 and will vary by bank, product, and applicant profile.

Upgrading from an HDB flat to a private condominium is the most common property milestone in Singapore. For a Singapore Citizen couple who bought their HDB in the early 2010s, the combination of substantial HDB appreciation, accumulated CPF savings, and rising household income has made condo upgrading more achievable than it has ever been — but the transaction is still the most financially consequential decision most families will make. Getting the sequencing wrong can cost S$300,000 or more in avoidable Additional Buyer’s Stamp Duty (ABSD). This guide walks you through every step, from checking your eligibility to collecting your new keys.

Quick Answer — HDB to Condo Upgrade at a Glance

Minimum Occupation Period (MOP): You must have fulfilled 5 years’ MOP before selling your HDB flat

ABSD — Sell First: Zero ABSD if you sell your HDB before purchasing the condo

ABSD — Buy First: 20% ABSD upfront, claimable if you sell the HDB within 6 months (SC couples only)

LTV for second property: 45% maximum loan-to-value (55% down payment required) if you still hold the HDB at the time of condo purchase

CPF usage: Your CPF OA (refunded from HDB sale + current balance) can fund the new condo’s down payment and monthly mortgage

2026 market context: Private prices up 0.3% q-o-q in Q1 2026; just ~8,100 new launch units in the 2026 pipeline — act with research but without panic

Step 1 — Check Your HDB Eligibility: Has Your MOP Been Met?

The first gateway to upgrading is the Minimum Occupation Period. For most HDB flats (BTO and resale), the MOP is 5 years from the date you collect the keys. You cannot sell your HDB flat, rent out the entire flat, or purchase a private property — whether in Singapore or overseas — until your MOP has been fulfilled. This applies to both joint owners.

Exceptions exist for certain special categories (e.g., divorce, death of owner, financial hardship), but these require HDB approval. For the vast majority of upgraders, the path is straightforward: wait out the MOP, then proceed. Check your MOP completion date on the HDB website or via the My HDBPage portal.

Step 2 — The Critical Decision: Sell First or Buy First?

This is the most consequential decision in the entire upgrader journey. It determines whether you pay S$0 or potentially hundreds of thousands of dollars in ABSD, and it shapes your entire financing plan. There is no universally right answer, but there is a framework for making the decision.

Option A — Sell First (Recommended for most upgraders)

You sell your HDB flat first, collect the proceeds, clear your HDB loan (if any), and receive your CPF refund (principal drawn plus accrued interest). You are then in the position of a first-time private property buyer: clean title history, 75% LTV (25% down payment), and zero ABSD as a Singapore Citizen buying your first private property. The trade-off is a temporary housing gap — you need somewhere to stay between selling the HDB and moving into the new condo. Options include renting privately, staying with family, or timing the HDB sale to coincide with a condo’s TOP date.

Option B — Buy First (ABSD Remission Route)

An SC couple can purchase a replacement private home while still owning the HDB flat, pay the 20% ABSD upfront, and then apply for a remission from IRAS after selling the HDB — provided the HDB is sold within 6 months of the condo’s purchase date (or 6 months after the condo’s TOP date for uncompleted projects). If the conditions are met, IRAS refunds the full 20% ABSD. The advantage is continuity of housing with no displacement. The risks are: (1) LTV drops to 45% because you hold two properties; (2) the 6-month sale deadline creates pressure; (3) if you miss the deadline for any reason, the ABSD is forfeited.

Important: Only SC-SC or SC-SPR couples qualify

The ABSD remission for replacement property purchases applies only to married couples where at least one spouse is a Singapore Citizen. Single buyers and SPR-SPR couples do not qualify for this remission. Always verify your eligibility with your conveyancing lawyer before relying on this route.

Sell First vs Buy First — Side-by-Side Comparison

Factor

Sell First

Buy First (with Remission)

ABSD payable upfront

S$0

S$370,000 (20% on S$1.85m)

ABSD recoverable?

N/A — no ABSD paid

Yes, if HDB sold within 6 months of new purchase

Interim housing needed?

Likely yes — bridge gap between sale and move-in

No — can stay in HDB until new condo TOP or handover

Bridging loan required?

Possibly (for IPA lapse or timing gap)

Usually no; but servicing 2 mortgages concurrently is a risk

Financial flexibility

Full sales proceeds available before next purchase

Tie-up of capital; dual mortgage risk

Ideal for

Buyers who want a clean break; financial discipline preferred

Families who need continuity of housing; confident of selling HDB within 6 months

Risk

Temporary displacement; may miss specific launch

ABSD remission application not guaranteed; timing pressure

Key Takeaway

For most HDB upgraders, Sell First eliminates ABSD entirely and reduces financial risk. Buy First suits families who cannot afford temporary displacement and are confident in selling their HDB within 6 months.

Source: IRAS / CPF Board — 24 April 2026

lovelyhomes.com.sg

Step 3 — Understanding Your Finances: How Much Can You Afford?

The upgrader’s budget equation has three inputs: net HDB sale proceeds, current CPF OA balance, and borrowing capacity. Here is how each works.

Net HDB proceeds: Your gross HDB sale price minus (a) the outstanding HDB loan balance (if any), (b) the CPF principal withdrawn plus accrued interest at 2.5% per annum (this is refunded back to your CPF OA, not paid in cash), (c) legal and conveyancing costs, and (d) agent commission (typically 1–2% of sale price). The cash proceeds are what remains after all of the above — in a fully-paid-up HDB bought in 2010, this could be substantial cash plus a large CPF refund.

CPF OA balance (post-refund): Once your HDB is sold, all CPF OA monies drawn for the purchase (plus 2.5% p.a. accrued interest) are returned to your OA. This refreshed CPF balance can be applied toward the down payment and monthly instalments of the new condo. Note: the CPF Usage Rules for private property limit how much you can use depending on the remaining lease of the property and your age at the time of purchase. For a 99-year leasehold condo with >60 years remaining, the full Valuation Limit applies.

Loan eligibility (TDSR): Your Total Debt Servicing Ratio must not exceed 55% of your gross monthly income across all outstanding debt obligations. For most salaried couples in dual-income households, this is not the binding constraint. The loan quantum for a private property is subject to a 75% LTV (Sell First) or 45% LTV (Buy First while HDB still held). At 75% LTV, a S$1.85 million condo requires a S$462,500 down payment (25%), of which at least 5% (S$92,500) must be in cash.

Step 4 — Buyer’s Stamp Duty: What You Will Pay

BSD is payable by every buyer — it applies regardless of whether you hold any other property. It is calculated on the higher of the purchase price or the market value of the property, using the progressive table below.

BSD Rates in Singapore 2026

Purchase Price Band

BSD Rate

BSD on That Band

First S$180,000

1%

S$1,800

Next S$180,000 (S$180k–S$360k)

2%

S$3,600

Next S$640,000 (S$360k–S$1m)

3%

S$19,200

Next S$500,000 (S$1m–S$1.5m)

4%

S$20,000

Next S$1,500,000 (S$1.5m–S$3m)

5%

S$75,000 max in this band

Above S$3,000,000

6%

Variable

Key Takeaway

BSD on a S$1.85 million condo = S$1,800 + S$3,600 + S$19,200 + S$20,000 + (S$350,000 × 5%) = S$1,800 + S$3,600 + S$19,200 + S$20,000 + S$17,500 = ~S$62,100.

Source: IRAS — iras.gov.sg/taxes/stamp-duty — 24 April 2026

lovelyhomes.com.sg

Step 5 — New Launch vs Resale: Which Route for Upgraders?

New launch condos offer the Progressive Payment Scheme (PPS), where you pay in stages as construction milestones are reached. This creates a natural cash-flow buffer: you do not need the full loan amount drawn down on day one, giving you time to sell your HDB and rebuild savings before full monthly instalments begin. The trade-off is a 3–4 year wait for TOP, during which you may need to rent. New launches in Singapore’s 2026 pipeline are heavily subscribed — popular projects such as Pinery Residences achieved a 92.5% launch-weekend take-up rate in early 2026 — so acting decisively at launch is important for choice units.

Resale condos offer immediate occupation, avoiding the rental gap entirely. You can time the HDB sale to coincide with resale condo completion in as little as 8–12 weeks. The full loan amount is drawn down from day one, so your monthly commitment is immediate. Resale units in popular districts (15, 19, 23, 26) may command a premium over new launches on a per-square-foot basis, but you avoid the risk of TOP delays and the uncertainty of unit quality before handover.

Step 6 — Executive Condominiums: The Upgrader’s Middle Ground

Executive Condominiums (ECs) are a hybrid product developed by private developers but sold at subsidised prices to HDB upgraders. They are subject to an eligibility framework (Monthly Household Income ceiling: S$16,000; you must not have owned private property in the preceding 30 months; at least one applicant must be SC or PR), but if you qualify, ECs offer condo-standard facilities at prices typically 20–30% below comparable private condos in the same area. ABSD is not payable when buying a new EC directly from the developer, even if you still own your HDB flat — a significant advantage over the private condo route.

The 2026 EC pipeline includes Rivelle Tampines EC and projects in Sembawang and Plantation Close. These are worth considering for eligible upgraders who prioritise value over prime CCR address.

Step 7 — Getting Your In-Principle Approval (IPA)

Before signing any Option to Purchase (OTP), secure an In-Principle Approval (IPA) from your bank. An IPA gives you a formal indication of the loan quantum, interest rate, and tenure the bank is willing to offer, based on your income documents and credit profile. Having an IPA in hand at the showflat means you know your exact budget envelope and can make a confident, irreversible decision when the OTP is presented. Note that an IPA is not a formal Letter of Offer — the bank will conduct a full assessment when you submit a formal loan application — but it is the closest proxy available before a specific unit is identified. Most banks issue IPAs within 2–3 business days. Compare rates across at least 3 banks, including fixed-rate (typically 2.5–3.5% in 2026), floating SORA-linked, and fixed-SORA hybrid packages.

Step 8 — The Legal Process: From OTP to Keys

For a new launch condo, the process runs: (1) exercise the OTP (1% booking fee) → (2) sign the Sale & Purchase Agreement within 3 weeks (typically 4–9% more paid) → (3) engage a conveyancing lawyer → (4) pay BSD (and ABSD if applicable) within 14 days of OTP exercise → (5) progress payments as per the PPS schedule over the construction period → (6) collect keys at TOP → (7) complete final payment and receive Certificate of Statutory Completion. The conveyancing lawyer handles stamp duty payments, title searches, bank loan drawdown, and final completion. Budget S$3,000–S$5,000 in legal fees for a standard new-launch purchase.

2026 Market Context — Is Now the Right Time?

The Q1 2026 URA flash estimate showed a modest 0.3% quarter-on-quarter increase in private residential prices, with the OCR (where most upgrader condos are priced) leading at +1.3% q-o-q. The 2026 launch pipeline is significantly constrained at approximately 8,100 units across 17 projects, down 30% from 2025. This supply tightness tends to sustain prices and take-up rates at quality launches, as seen in the strong weekend sales figures at Pinery Residences (92.5% sold) in Q1 2026.

For upgraders, the current environment suggests a window of stable prices with limited new supply — not a runaway market, but also not a buyer’s market in the traditional sense. Prioritise location, unit type, and fit-for-purpose over speculation. The best condo purchase for an upgrader family is one they can comfortably afford and intend to occupy for at least 5 years.

Frequently Asked Questions

Can I own an HDB and a condo at the same time?

Yes, but only after fulfilling the HDB MOP. An SC or SPR can hold both an HDB flat and a private property simultaneously after MOP, subject to paying 20% ABSD (SC) or 30% ABSD (SPR) on the private purchase. You must then sell the HDB within the prescribed timeframe to claim ABSD remission (SC couples only). You cannot own an HDB and a private property at the same time before MOP — this would breach HDB ownership rules.

Does CPF need to be returned when I sell my HDB?

Yes. All CPF monies withdrawn for the HDB purchase (including the principal and accrued interest at 2.5% p.a.) are automatically returned to your CPF OA upon sale. You do not get this cash in hand; it goes back into your CPF OA. However, you can then re-use this CPF OA balance for the new condo purchase, subject to CPF usage rules for private properties.

What is the maximum loan for a condo if I still own my HDB?

If you hold an existing property (including an HDB flat) at the time of the condo purchase, the maximum LTV for a bank loan is 45% — meaning a 55% down payment is required, of which 25% must be in cash. This is a significant constraint and one of the key reasons most upgraders prefer the Sell First strategy.

Can I use my CPF to pay for the condo if the remaining lease is short?

CPF usage for private property is subject to the Lease Remnant Restriction: the property’s remaining lease must cover the youngest buyer to age 95. For most new-launch 99-year leasehold condos, this requirement is easily satisfied. Shorter-lease or older resale properties may restrict CPF usage or trigger a pro-rated cap. Check the CPF online calculator or consult your conveyancing lawyer.

What if I miss the 6-month ABSD remission deadline?

If you fail to sell your HDB within the 6-month window, the ABSD is not refunded. It is permanently forfeited. IRAS does grant extensions in exceptional circumstances (e.g., death of a co-owner), but these are discretionary and not guaranteed. If you are buying first, build in a buffer and engage a property agent to market your HDB promptly after exercising the condo OTP.

Disclaimer: This guide is for general information only and does not constitute financial, legal, or tax advice. ABSD rates, LTV limits, CPF rules, and HDB eligibility conditions are subject to change. Always verify current figures on the IRAS website and CPF Board, and consult a licensed property agent and conveyancing solicitor before proceeding.

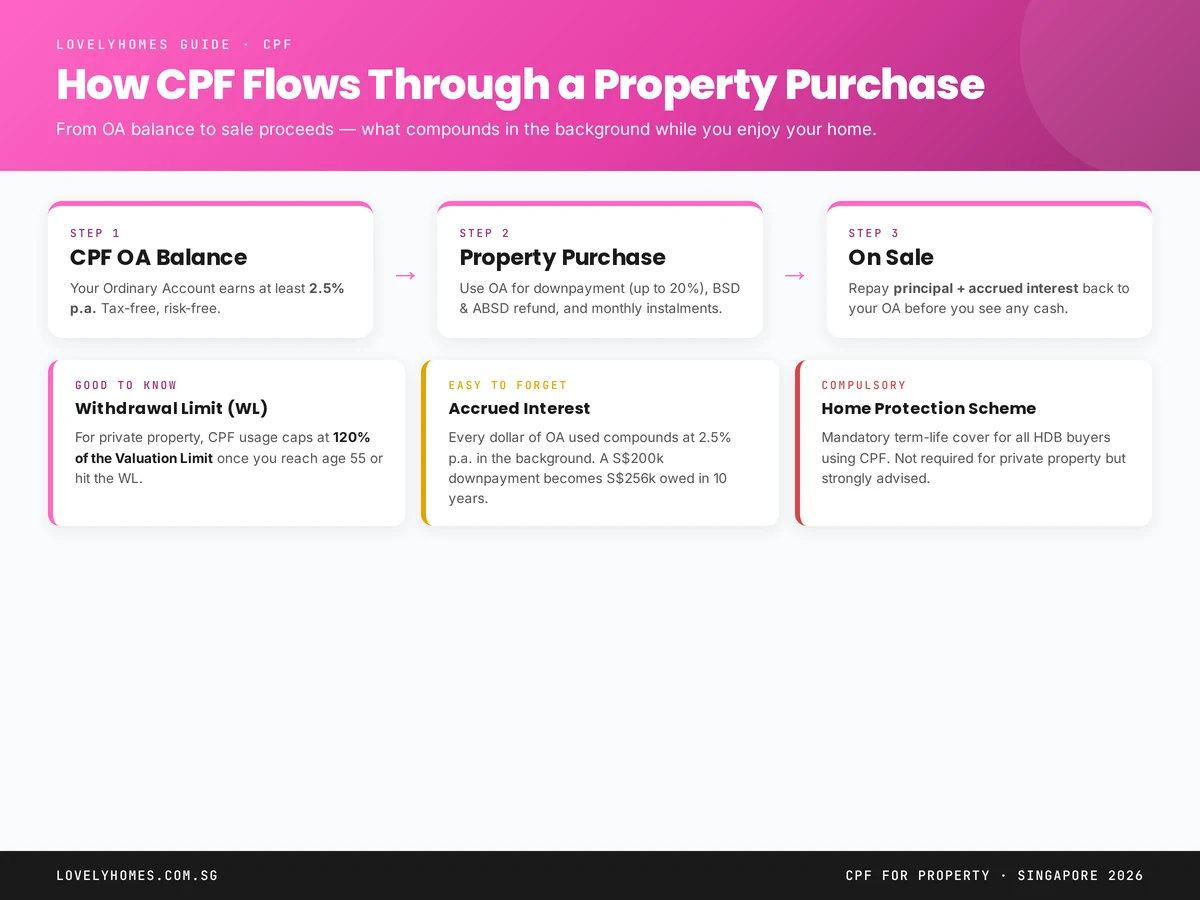

Using CPF for property in Singapore is so routine that most buyers treat the Ordinary Account as a second bank account. That casual mental model is the source of nearly every CPF surprise at resale time — because CPF money put into a home does not behave like cash. It compounds in the background at 2.5% a year and must be repaid, with interest, the moment you sell.

This 2026 guide walks through how CPF flows into a purchase, what the withdrawal and valuation limits actually mean, how accrued interest is calculated, when the Home Protection Scheme is compulsory, and what lands in your pocket when you sell. For the authoritative rulebook, see the CPF Board’s home ownership pages.

Quick Answer — CPF for Property at a Glance

CPF Ordinary Account (OA) can be used for downpayment, stamp duties, monthly instalments, legal and valuation fees.

Interest rate: OA earns at least 2.5% per annum — and every dollar used for property continues to accrue at 2.5% in the background until repaid.

Withdrawal Limit (WL): CPF usage on private property caps at 120% of the Valuation Limit once you reach age 55 or exhaust the WL.

Home Protection Scheme (HPS): Mandatory term-life cover for HDB buyers using CPF. Not required for private property.

At sale: Principal plus accrued interest must be refunded to your OA before any cash reaches you.

What You Can Use CPF For

Your CPF Ordinary Account can be deployed at six points in the property journey:

Downpayment. For an HDB loan, CPF can fully fund the 20% minimum downpayment. For a bank loan, at least 5% must be cash and the remainder (up to 20% for a first property) can come from CPF.

Buyer’s Stamp Duty (BSD). Payable in cash initially but reimbursable from CPF after stamping.

Additional Buyer’s Stamp Duty (ABSD). Also reimbursable from CPF after stamping — cash up front, then drawn down from OA.

Monthly loan instalments. Direct GIRO from OA covers principal + interest. You can choose partial cash/CPF if you want to preserve OA for other uses.

Legal fees. Conveyancing fees capped at S$675 per transaction are reimbursable from CPF.

Property tax, renovation, utilities:Not covered by CPF. Always cash.

Figure 1: CPF OA funds flow from downpayment through monthly instalments and must be refunded with accrued interest on sale.

Valuation Limit, Withdrawal Limit & Why They Exist

CPF imposes two caps on how much OA money can be used for a private property:

Valuation Limit (VL): the purchase price or valuation of the property, whichever is lower, at the time of purchase.

Withdrawal Limit (WL): 120% of the Valuation Limit.

Up to the VL, you can use CPF freely. Between the VL and the WL, you can continue using CPF if you are below 55 or above 55 with your Basic Retirement Sum (BRS) set aside. Once the WL is hit, no further CPF can service the property loan — you must switch to cash.

For HDB flats bought with an HDB concessionary loan, the VL/WL framework does not apply in the same way — there is no cap beyond what the loan quantum supports.

Accrued Interest: The Silent Compounding

This is the single most misunderstood part of CPF for property. Every dollar of OA you use for a property is treated as if it had stayed in your OA, continuing to earn 2.5% compounded annually. When you sell, you must refund principal + accrued interest to your OA before any cash reaches your pocket.

Worked example: S$200,000 used over 10 years

Assume you use S$200,000 of CPF OA for your downpayment and contribute another S$1,500/month from OA to servicing the loan. After 10 years:

Accrued interest at 2.5% compounded: approximately S$77,500

Total refund to OA on sale: roughly S$457,500

If your sale proceeds after repaying the outstanding bank loan are only S$420,000, there is a S$37,500 negative sale — the shortfall is waived but you walk away with no cash, even though the property “made money” in headline terms.

Home Protection Scheme (HPS)

HPS is a term-life insurance scheme administered by CPF that covers the outstanding housing loan in the event of death, terminal illness, or total permanent disability. It is compulsory for HDB buyers using CPF to service the loan.

HPS is not required for private property — bank home loans are typically paired with privately purchased Mortgage Reducing Term Assurance (MRTA) instead. You can compare MRTA against HPS using the illustrative premium tables on the CPF HPS page — for most buyers below 45, privately sourced MRTA is cheaper.

Voluntary Housing Refund (VHR): Paying Down Accrued Interest Early

You can voluntarily refund cash into your OA at any time to reduce the accrued-interest trap. Every dollar you refund stops compounding — effectively giving you a 2.5% risk-free return on that cash. In a 3-4% deposit-rate environment, the maths sometimes wins for your home-loan net position; in a 0.5% environment, it is a clear winner.

VHR is especially useful in the final 3–5 years before a planned sale, when accrued interest is compounding hardest. Speak to your CPF servicing officer before making a lump sum refund.

CPF at 55: What Changes

At 55, two things shift:

The Retirement Account (RA) is created and funded with your Full Retirement Sum (FRS) — or Basic Retirement Sum (BRS) if you own property and pledge it.

OA usage for property becomes capped at the 120% Withdrawal Limit, and only if FRS/BRS is already met in the RA.

For most homeowners near 55 with significant mortgages, this means they transition to cash servicing for instalments. Plan for this 5 years ahead.

Frequently Asked Questions

Can I use CPF OA to pay ABSD?

Yes, but only as a reimbursement after you have paid the ABSD in cash and the property has been stamped. You cannot draw CPF directly to IRAS.

What happens to accrued interest if I die?

Accrued interest is written off on death. The CPF member’s nominees inherit whatever is in the OA at that time; no refund from the property is required.

Can I use my CPF OA to buy a second property?

Yes, once the Full Retirement Sum has been set aside in your RA (at 55) or if you are below 55 — but CPF usage on the second property only kicks in after you reach the Basic Retirement Sum for the first.

Does accrued interest continue to compound after I pay off the loan?

Yes. As long as the property is in your name and CPF money has been used, accrued interest compounds until sale or your death.

Is there any way to avoid HPS?

Applications to opt out are considered only if you have equivalent private insurance covering the loan. CPF assesses case-by-case — the default position is compulsory participation.

What to Do Next

CPF shapes not just affordability but also upgrade strategy and retirement planning. Your next reads:

Disclaimer: This guide is for general information and not financial advice. CPF policies are updated regularly. Verify current rules on cpf.gov.sg and speak to a licensed financial adviser before making CPF-related property decisions.