Executive Condominium Singapore 2026: Complete Guide to Eligibility, MOP, Privatisation & Pricing

Executive Condominiums (ECs) are Singapore’s most distinctive housing hybrid — built by private developers, regulated by HDB for the first ten years, then quietly graduating into full private property. For the right buyer profile, an EC delivers condo facilities, family-sized layouts and capital appreciation at a 25–35% discount to comparable mass-market private condos. For the wrong buyer profile, the eligibility rules, MOP restrictions and resale-levy traps can be expensive surprises.

This guide walks through how ECs work in 2026 — who can buy, how much you can borrow, what happens at the 5-year MOP and 10-year privatisation milestones, and the worked maths on a typical S$1.46 million Tampines unit. Figures reflect the rules administered by the Housing & Development Board (HDB) and the financing limits set by the Monetary Authority of Singapore (MAS).

Quick Answer — Executive Condominium 2026 at a glance

- Income ceiling: S$16,000 gross monthly household income

- At least one applicant must be a Singapore Citizen; co-applicant can be SC or PR

- Minimum Occupation Period (MOP): 5 years owner-occupier from key collection

- After MOP: sell to SCs or PRs only on the open market

- Privatisation: 10 years from TOP — sell to anyone, including foreigners

- Loan: 75% LTV from a bank, 30% MSR cap (HDB-style during MOP), 55% TDSR stress-tested at 4.0%

- CPF Enhanced Housing Grant (EHG): up to S$30,000 for first-timers (vs S$120,000 for BTO/resale)

- Stamp duty: BSD applies normally; ABSD is 0% on a first EC bought from the developer

What is an Executive Condominium — and Why Does It Exist?

An Executive Condominium is a class of housing introduced in 1995 to bridge the gap between HDB flats and private condominiums. The Government’s logic was simple: a sandwich class of professionals earned too much to qualify for a BTO flat, but could not yet afford a S$1.5 million private condo. ECs solved that with a structured concession — private-condo developers build to private specifications (gym, pool, security, full Strata-Title), but the units are sold at HDB-style prices to eligible Singaporean families, with restrictions on resale and ownership for the first ten years.

The economic trade-off is straightforward. Buyers accept a 5-year MOP (no selling, no whole-unit subletting) and a further 5-year ban on selling to foreigners, in exchange for entry pricing roughly 25–35% below comparable mass-market private condos. After ten years, the EC is fully privatised and trades like any other private property — at which point much of the discount has typically been realised as capital gain.

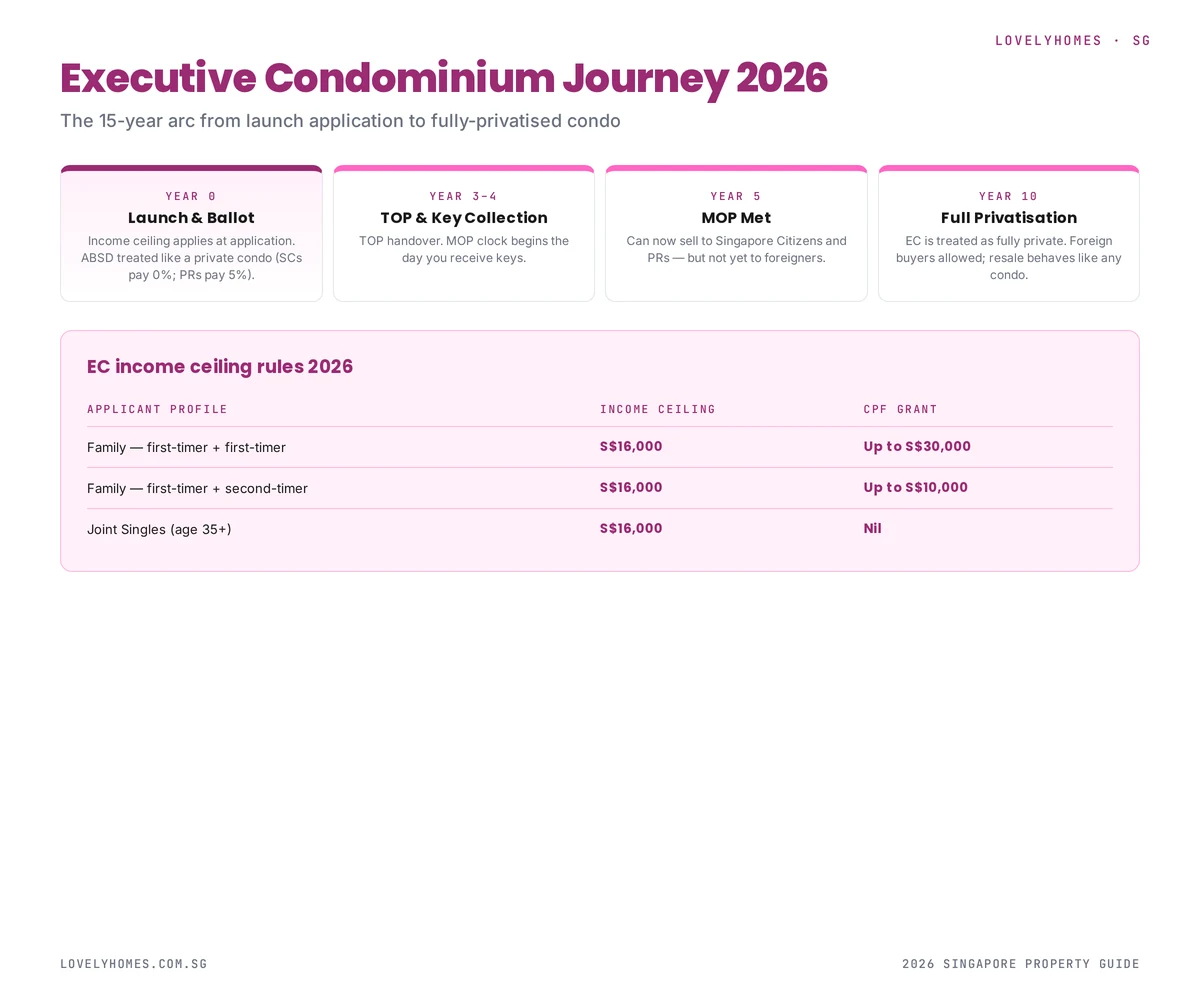

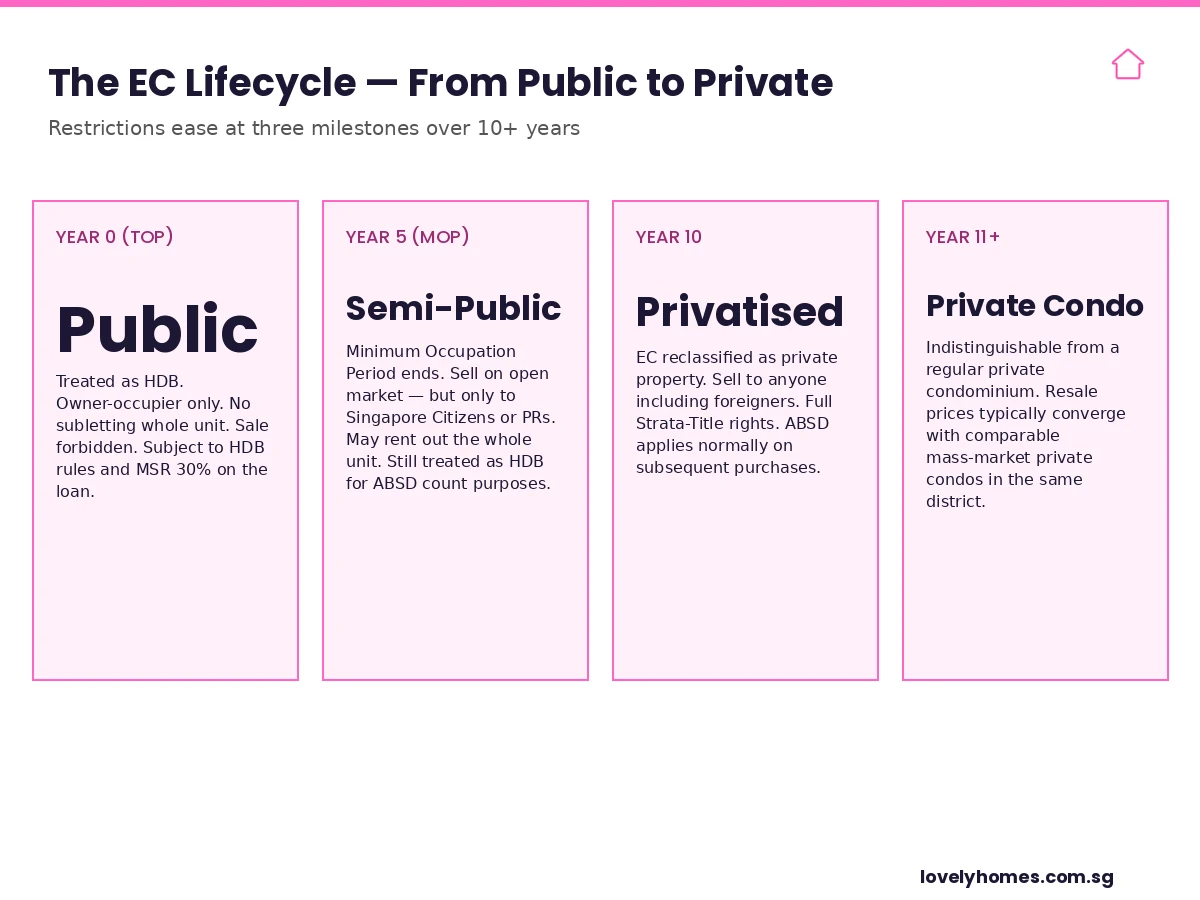

The EC Lifecycle — From Public to Private in 10 Years

The most-misunderstood feature of an EC is that it changes legal status three times across its first decade. Buyers who plan around these milestones consistently outperform buyers who treat an EC like a regular condo from day one.

Year 0 – TOP and Key Collection

You move in. The unit is treated as HDB property under the Executive Condominium Housing Scheme. You may not sell, transfer or rent the entire unit. Renting individual rooms is permitted (subject to HDB sub-letting rules), but the household must continue to occupy the flat as the principal residence.

Year 5 – MOP Ends

The Minimum Occupation Period of 5 years (from the issuance of the Temporary Occupation Permit, or in practice from key collection) ends. You may now sell on the open market — but only to Singapore Citizens or Permanent Residents. Whole-unit rental is permitted. The unit still counts as HDB-equivalent for ABSD purposes (which means an SC family selling and buying a private condo elsewhere may still face ABSD on the next purchase, depending on timing).

Year 10 – Privatisation

Ten years from TOP, the EC is reclassified as a private property. Restrictions on foreign-buyer eligibility lift. The Strata Title comes through cleanly — in most projects, owners receive a Subsidiary Strata Certificate of Title (SSCT) at this milestone. Sale to anyone, anywhere in the world, becomes possible. From this point onwards, the EC is, for all market and legal purposes, a private condominium.

Year 11+ – Mature Private Condo

Resale prices typically converge with comparable mass-market private condos in the same district. Historic data from URA caveats suggests the privatisation premium is often 8–15% — the simple act of crossing the 10-year threshold tends to add a measurable price uplift, on top of the underlying district-level appreciation.

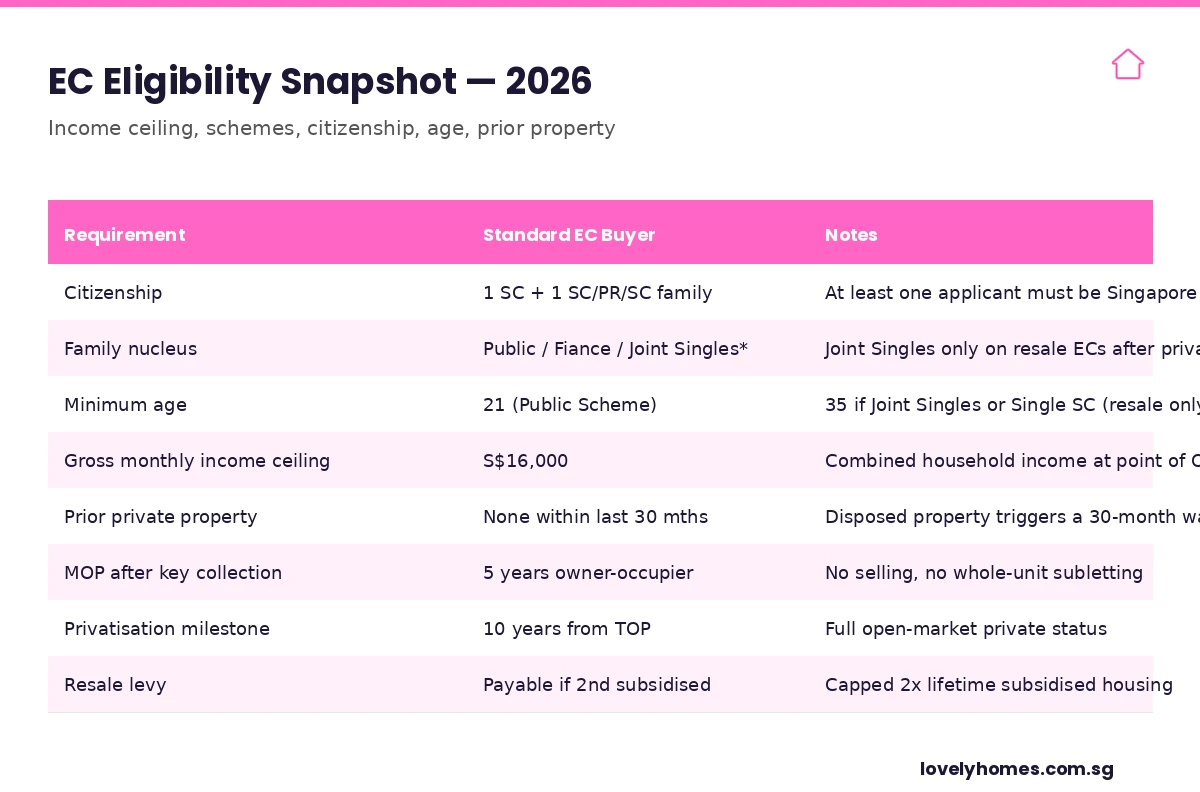

Who Can Buy an EC in 2026? Eligibility Snapshot

EC eligibility is administered by HDB, even though the developer is private. The rules are stricter than a private-condo purchase but looser than a BTO. The 2026 framework is unchanged from the 2025 reset, with the gross monthly household income ceiling holding at S$16,000.

The detail behind each row matters:

- Income ceiling: S$16,000 gross household income at the date of the Option to Purchase. A single dollar over disqualifies. HDB looks at the trailing 12 months in most cases. Variable bonuses are typically averaged.

- Citizenship: at least one SC. The classic mixed-citizenship case — SC + PR — is allowed under the Public Scheme. SC + foreigner is not allowed for new ECs from the developer (only for resale ECs after privatisation).

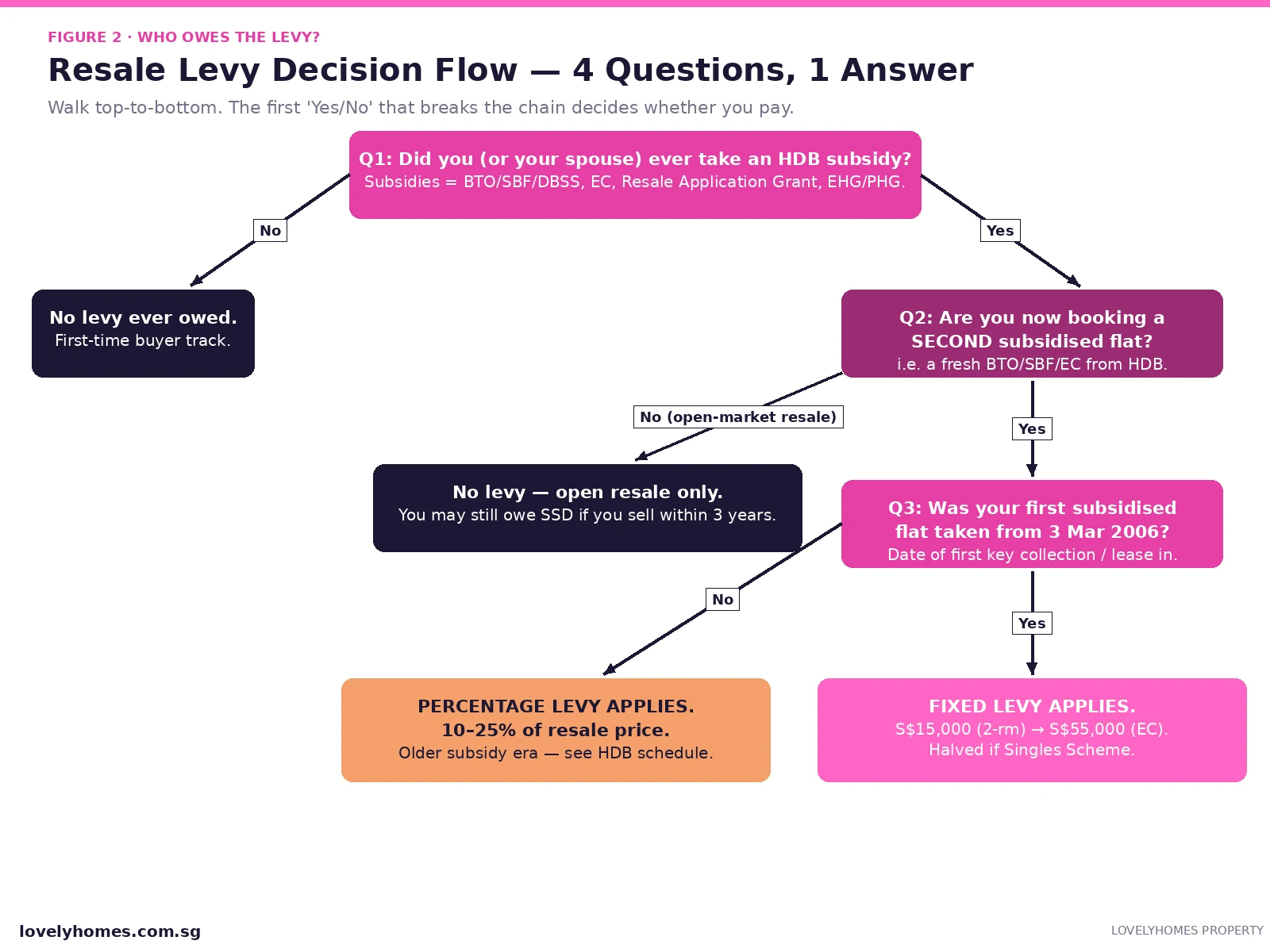

- 30-month rule: if you have owned or disposed of any private residential property in the last 30 months, you cannot buy a new EC. This catches HDB-upgrader-then-downgrader patterns. The 30 months runs from the date of disposal — not the date of physical move-out.

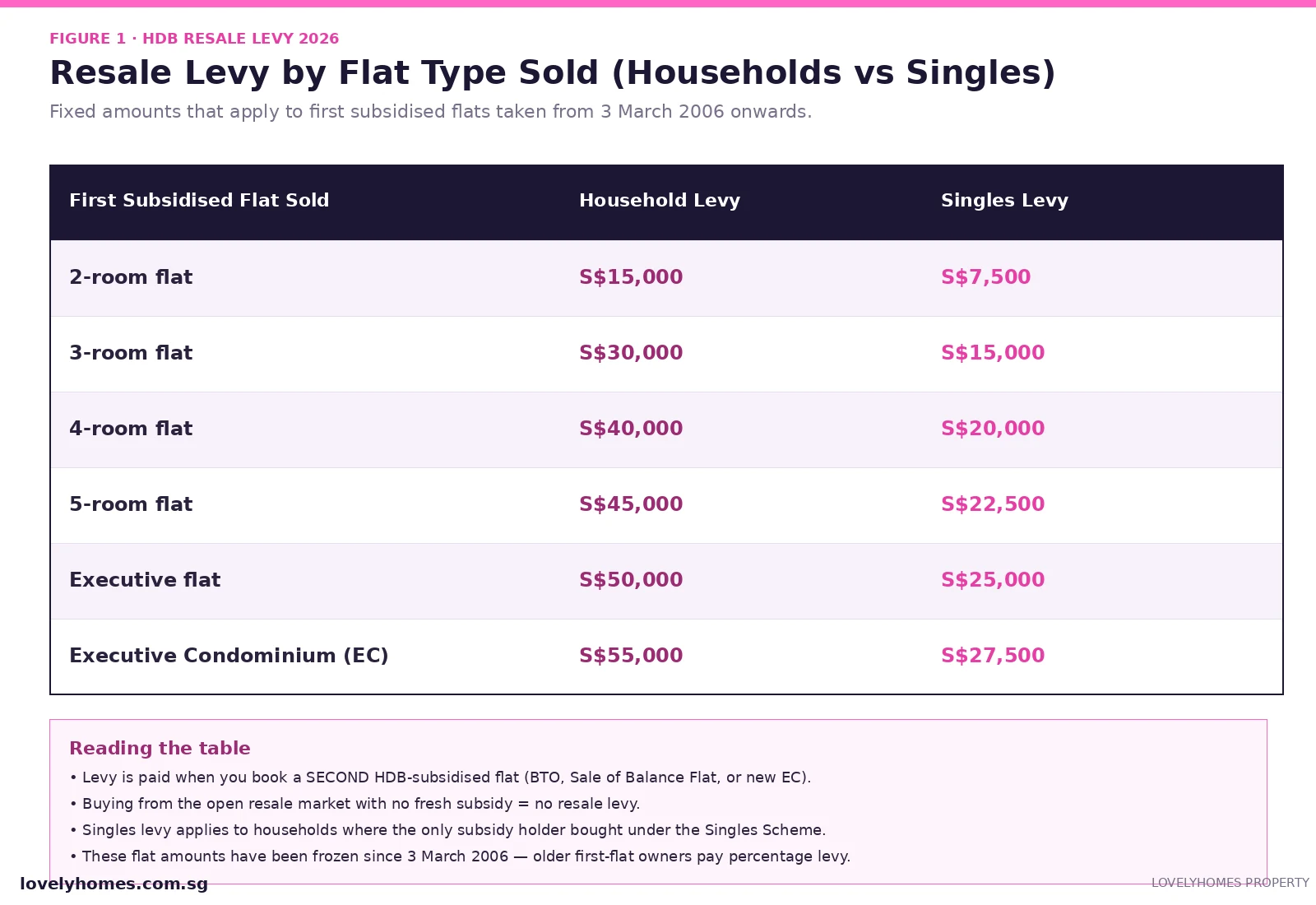

- Resale levy: if you have previously bought a subsidised flat from HDB or a previous EC, a resale levy applies on the new EC purchase. The levy is fixed (not means-tested) and is deducted from the CPF refund or paid in cash at the next purchase. See our HDB Resale Levy guide for the lookup tables.

Financing an EC — The Three Gates

EC financing is a hybrid of HDB-style and private-style limits. Because the unit is HDB-classified during the first five years, the Mortgage Servicing Ratio (MSR) cap of 30% applies. But because HDB does not issue concessionary loans on ECs, the buyer must use a bank loan — meaning private-loan rules apply too: 75% LTV cap, 55% TDSR, and stress-testing at the medium-term interest-rate floor of 4.0%.

The financing pass requires clearing all three gates in turn:

- LTV (Loan-to-Value): bank loan capped at 75% of the lower of price or valuation. The remaining 25% must be in cash and CPF, with at least 5% in cash.

- TDSR (Total Debt Servicing Ratio): 55% of gross monthly income, stress-tested at 4.0% medium-term floor. All debts count — car loans, education loans, credit-card minimums.

- MSR (Mortgage Servicing Ratio): 30% of gross monthly income on the mortgage instalment alone, again stress-tested at 4.0%. This is the binding constraint for most EC buyers.

For full mechanics, see our LTV Limits Singapore 2026 guide and the companion TDSR & MSR explainer.

Worked Example — A S$1.46M Tampines EC for a Dual-Income SC Couple

Let’s run a realistic 2026 case. Mr and Mrs Lim, both 32, both Singapore Citizens, no children yet, combined gross monthly income S$13,500. They are first-timer buyers (no prior subsidised housing) and have S$160,000 cash savings plus S$220,000 combined CPF Ordinary Account balance. They intend to buy a 4-bedroom unit at Aurelle of Tampines at S$1,460,000.

| Component | Amount (S$) | Notes |

|---|---|---|

| Purchase price | 1,460,000 | Aurelle of Tampines, ~828 sq ft, 4-bed |

| Cash + CPF down payment (25%) | 365,000 | 5% cash (S$73,000) + 20% cash or CPF (S$292,000) |

| Bank loan (75% LTV) | 1,095,000 | 25-year tenure, 2.85% pa fixed indicative |

| Monthly instalment | 5,094 | 37.7% of gross — fails MSR 30% cap |

| Adjusted loan (to clear 30% MSR @ 4% stress) | 763,000 | Implies S$697,000 cash + CPF down payment |

| Buyer’s Stamp Duty (BSD) | 36,200 | Progressive on S$1.46M, payable in cash within 14 days |

| ABSD (first home, SC) | 0 | EC is exempt from ABSD on the first-home purchase |

| CPF Enhanced Housing Grant (EHG) | 5,000 | Income S$13,500 → EHG S$5,000 (capped, EC band) |

| Legal & conveyancing | 3,000 | Approximate, including title search and registration |

| Effective net upfront outlay | ~731,200 | After EHG offset; the binding constraint is MSR, not LTV |

The headline finding: at this income level, MSR — not LTV — is the binding constraint. The Lims can borrow up to S$763,000 (giving a stress-tested instalment of ~30% of gross at 4.0%), which means they need almost double their original cash + CPF down payment. Many EC buyers run into this exact wall and either (a) extend tenure to the maximum 30 years allowed by the bank, (b) bring in a third co-applicant from the family nucleus, or (c) downsize to a 3-bedroom unit at S$1.2 million.

EC vs HDB BTO vs Mass-Market Private Condo

For dual-income families earning S$13,000–16,000 a month, the choice in 2026 typically comes down to three options. The trade-offs are summarised below.

| Dimension | 5-room BTO | EC (e.g. Aurelle) | Mass-market private condo |

|---|---|---|---|

| Indicative price (4-bed) | S$680k | S$1.46m | S$2.20m |

| Indicative psf | S$680–780 | S$1,766 | S$2,400–2,600 |

| Income ceiling | S$14,000 | S$16,000 | None |

| Time to keys | 4–5 yrs | 3–4 yrs | 3–4 yrs (new launch) |

| MOP | 5 yrs | 5 yrs (HDB-style) | None |

| Privatisation | N/A | 10 yrs from TOP | Already private |

| CPF EHG cap | S$120,000 | S$30,000 | None |

| Loan source | HDB or bank | Bank only | Bank only |

| LTV cap | 85% (HDB) / 75% (bank) | 75% | 75% |

| MSR cap | 30% | 30% | N/A |

The right choice depends on the household’s priorities. BTO maximises grants and minimises price but requires patience and a thinner facility set. ECs add condo facilities and a faster handover but demand much more cash. A mass-market private condo gives full flexibility but at a meaningful premium and without the EC’s built-in price cushion.

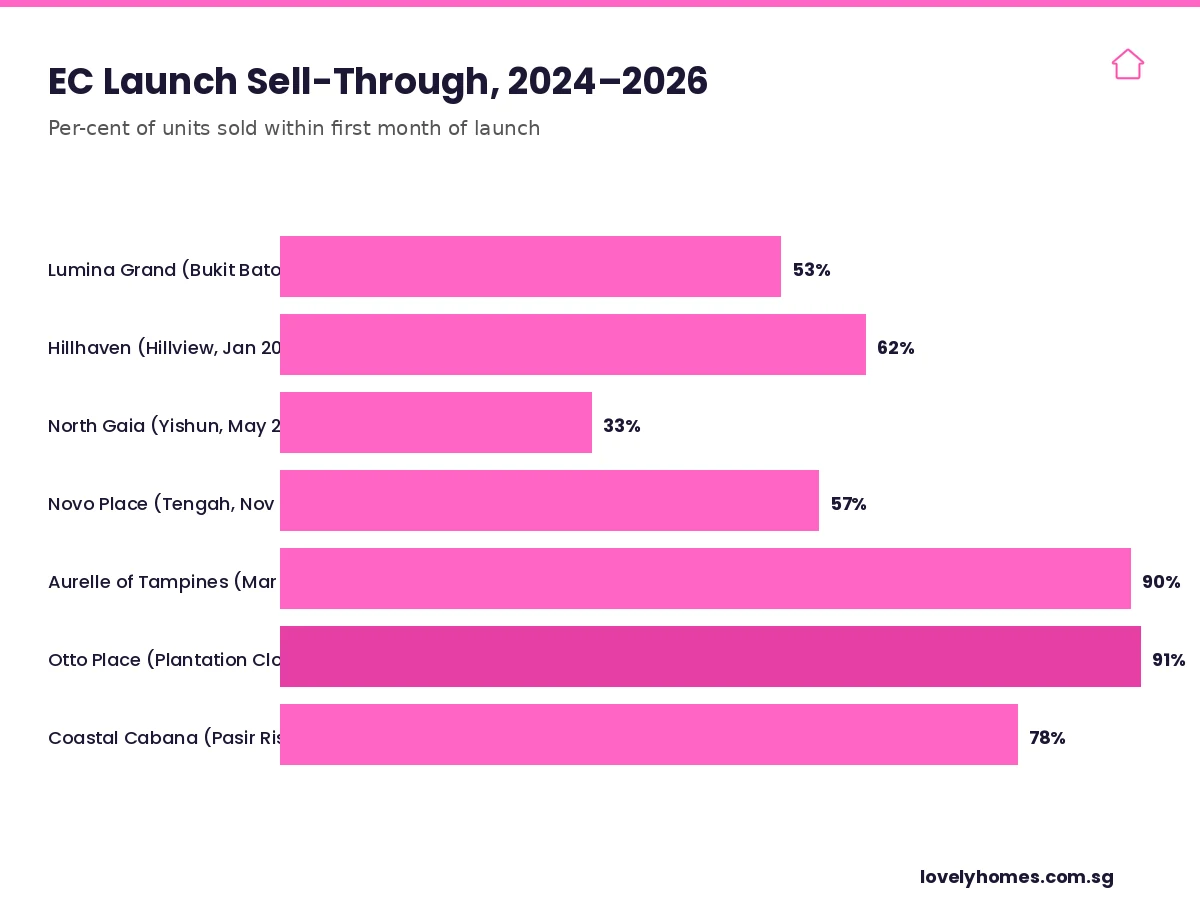

EC Launches in Singapore — The 2024–2026 Sales Track Record

The EC market has materially tightened since the 2023 cooling measures. With the 60% ABSD wall pushing foreign and investor demand out of the mass-market private space, EC launches have absorbed a disproportionate share of upgrader demand. The chart below tracks first-month sell-through across the most recent EC launches.

The standout pair — Aurelle of Tampines (March 2025, 90%) and Otto Place at Plantation Close (July 2025, 91%) — effectively re-priced the EC market upwards, both clearing above S$1,700 psf. Coastal Cabana in Pasir Ris (January 2026, 78%) confirmed that the new pricing band held. The 2026 pipeline is thin — Rivelle Tampines is the next major release expected, with Miltonia Close (Yishun) and the Sembawang Drive site coming through 2027–2028. Thin pipeline plus strong upgrader demand has been a recipe for sustained pricing power in the EC segment.

Why This Matters for You

For most dual-income SC households earning S$13,000–16,000 a month, an EC is the single most efficient way to access condo facilities and family-size layouts without paying private-condo prices. The five things that determine whether the maths works in your favour:

- Income trajectory. Bonuses and increments after OTP do not retroactively disqualify you, but they do reduce the value of any EHG you may have applied for. Apply at the lowest reasonable income point.

- Cash buffer. The 5% minimum cash component (S$73,000 on a S$1.46m unit) plus BSD (S$36,200) plus furnishing reserve must come from cash, not CPF. Underestimating this is the most common reason ECs fall through at the OTP-exercise stage.

- MSR vs LTV. Most EC buyers think in terms of LTV (75%); the real binding constraint is MSR (30%). Stress-test your monthly instalment at the 4.0% medium-term floor, not at the bank’s teaser rate.

- 30-month rule. If anyone in the household has owned a private property recently, the clock starts from disposal date, not the move-out date. This blocks more EC purchases than buyers expect.

- Privatisation premium. The 10-year reclassification from EC to private is a documented price uplift event of 8–15% on top of underlying district appreciation. Holding through Year 10 is almost always the higher-EV choice.

What Might Come Next

The 2026–2027 EC outlook depends on three policy variables to watch.

- Income ceiling. Last raised to S$16,000 in September 2019. If household incomes continue to drift upwards, a recalibration to S$18,000–20,000 would expand the addressable EC buyer pool significantly. Government has not signalled this in 2026.

- Mortgage rates. Three-month SORA was around 2.95% in April 2026, with 25-year fixed at 2.78–2.85%. A meaningful drop in rates would loosen the MSR constraint and immediately raise EC affordability ceilings; a meaningful rise would do the opposite. The 4.0% stress-test floor remains the more binding number for the foreseeable future.

- EC supply. The 1H 2026 GLS programme has slotted Sembawang Drive and Canberra Drive as EC sites. If both are awarded and launched in 2027, the pipeline thickens. If either is withdrawn or pushed to 2028, expect continued price discipline at the existing-launch level.

Frequently Asked Questions

Can a Permanent Resident buy a new EC?

Yes, but only as a co-applicant alongside at least one Singapore Citizen. Two PRs cannot buy a new EC together; the SC anchor is mandatory under the Public Scheme. Two PRs can, however, buy a resale EC after the unit has been privatised at Year 10.

Can a foreigner buy an EC?

Not within the first ten years from TOP. After privatisation at Year 10, the EC is a fully private property and may be bought by foreigners, subject to the standard ABSD framework (60% on residential property as of 2026). Before Year 10, even a fully privatised resale EC remains restricted to Singapore Citizens and PRs.

Do I pay ABSD when I buy a new EC from the developer?

No. EC purchases under the Executive Condominium Housing Scheme are exempt from ABSD on the first-home transaction. ABSD applies normally on any subsequent residential property purchase — including a private condo bought after the EC.

What happens if my income exceeds S$16,000 after I sign the OTP?

You are not retroactively disqualified. The income test is applied at the date the OTP is granted. A subsequent pay rise, bonus, or windfall does not affect your eligibility — though it may affect the EHG you receive (if any). HDB occasionally re-checks income at the date of S&P signing for resale ECs; for new ECs, the OTP-date check is generally final.

Can I rent out the entire EC unit during MOP?

No. Whole-unit subletting is prohibited during the 5-year MOP. Renting individual rooms is permitted, but the household must continue to occupy the unit as the principal residence. Breaching this rule can result in compulsory acquisition of the unit by HDB at the original purchase price.

If I sell my EC after MOP but before Year 10, who can I sell to?

Singapore Citizens and Permanent Residents only. Foreign buyers, companies and trusts are excluded. The pool of eligible buyers expands at Year 10 when the EC is fully privatised — which is why many EC owners prefer to hold through privatisation if the holding cost is manageable.

How does the resale levy work for an EC?

If you previously bought a subsidised flat from HDB (BTO, SBF, EC, etc.) and now buy a new EC, you pay a resale levy on the second purchase. The levy is fixed by the type of the previous flat — ranging from S$15,000 (2-room BTO) to S$55,000 (Executive flat). It is deducted from your CPF refund or paid in cash at the time of OTP exercise. Singapore households can take only two subsidised housing units in a lifetime.

Related Articles

- HDB BTO Application Guide Singapore 2026

- HDB Resale Levy Singapore 2026

- CPF Housing Grant Singapore 2026

- LTV Limits Singapore 2026

- Mortgage Refinancing in Singapore 2026

- HDB Upgrader Guide Singapore 2026

- ABSD Singapore 2026: Complete Guide

- Buyer’s Stamp Duty Singapore 2026

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. EC eligibility, income ceilings, grant amounts and financing rules can change. Always verify the current position with the HDB Executive Condominium eligibility page, the IRAS Stamp Duty page, the Central Provident Fund Board (CPF) and a licensed conveyancing lawyer or financial adviser before signing any OTP.